Sample Category Title

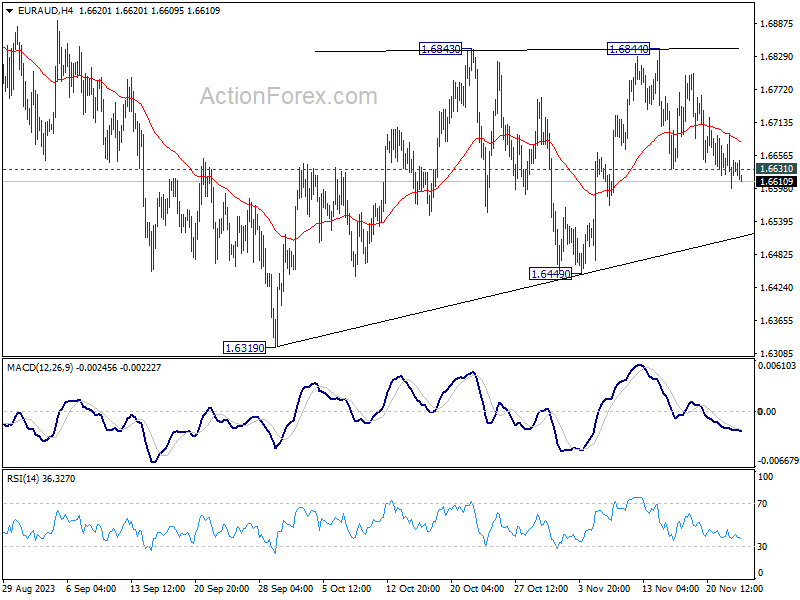

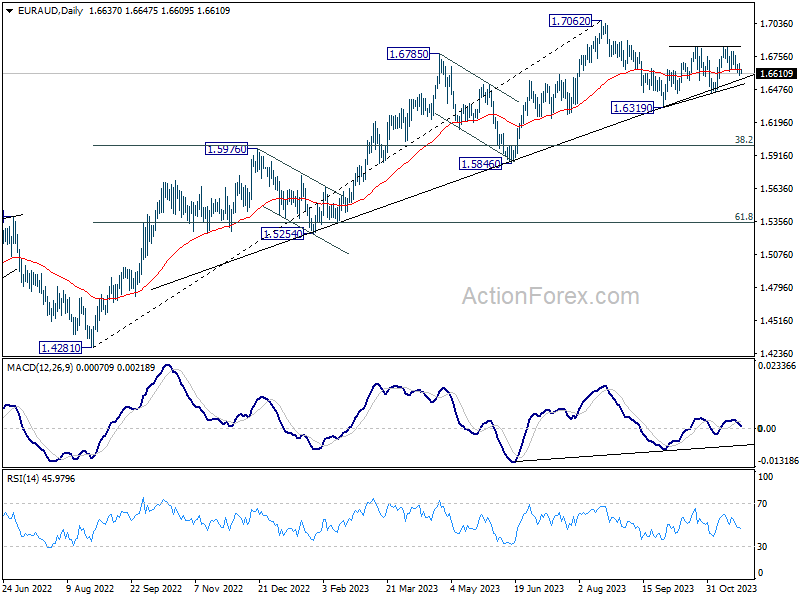

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6596; (P) 1.6647; (R1) 1.6693; More...

Intraday bias in EUR/AUD is back on the downside with break of 1.6631 support. Deeper fall would be seen to 1.6449 support next. Firm break there will argue that the pattern from 1.6319 has completed at 1.6844 as a corrective move, and fall from 1.7062 is ready to resume through 1.6319. On the upside, however, sustained break of 1.6843/4 will resume the rebound from 1.6319 for retesting 1.7062 high next.

In the bigger picture, while 1.7062 is a medium term top, there is no clear sign of trend reversal as EUR/AUD continues to draw strong support from the medium term trend line. Break of 1.7062 will resume the larger up trend from 1.4281 (2022 low) to 1.7691 fibonacci level. Nevertheless, break of 1.6449 support will argue that deeper correction is underway to 38.2% retracement of 1.4281 to 1.7062 at 1.6000.

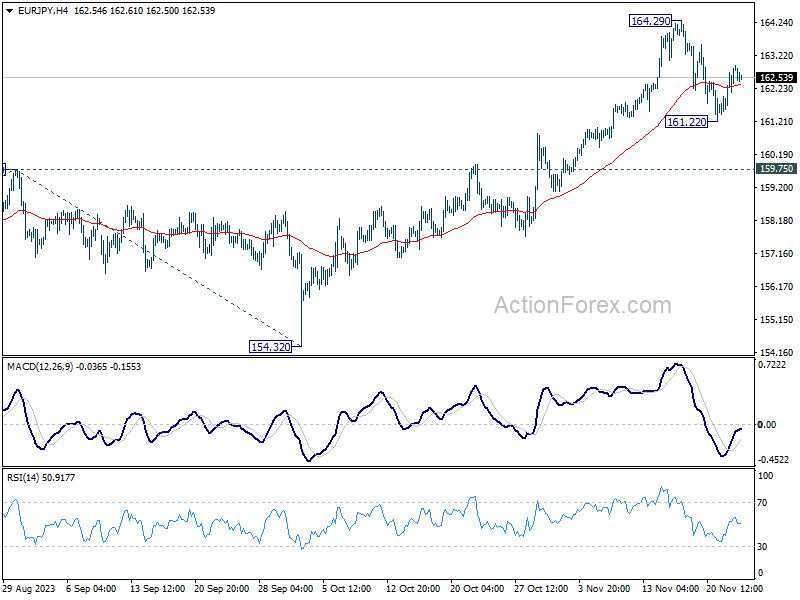

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.99; (P) 162.46; (R1) 163.33; More....

Intraday bias in EUR/JPY stays mildly on the upside at this point. Rebound from 161.22 could extend further to retest 164.29 high. Firm break there will resume larger up trend. On the downside, though, below 161.22 will resume the fall from 164.29 to 159.75 resistance turned support.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 169.96 (2008 high). On the downside, break of 159.75 resistance turned support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish even in case of deep pullback.

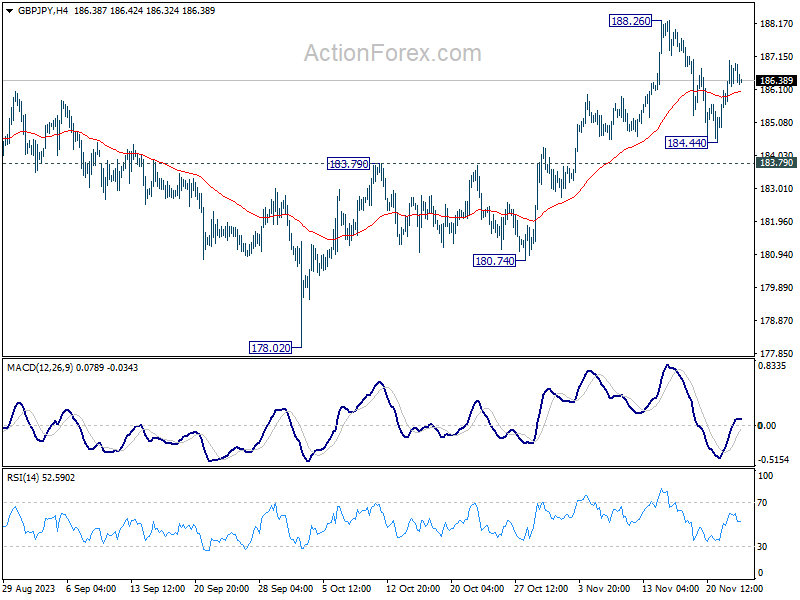

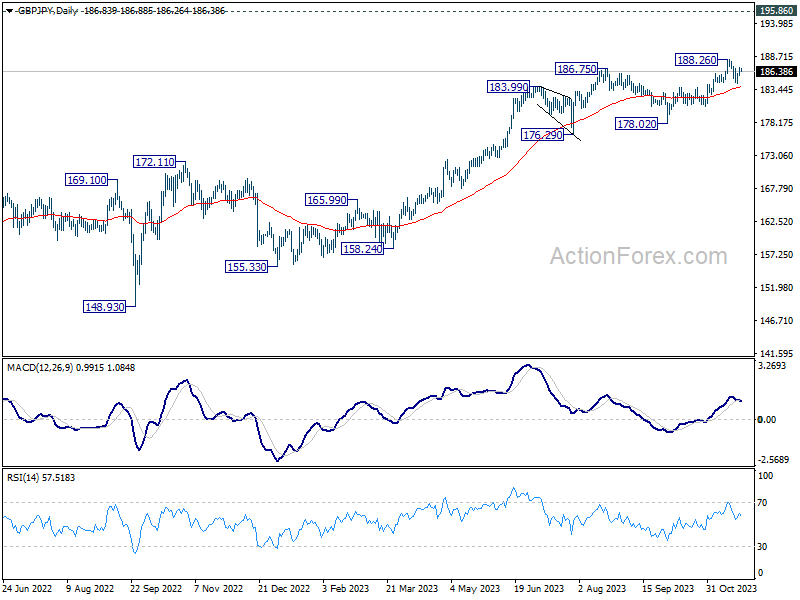

GBP/JPY Daily Outlook

Daily Pivots: (S1) 185.98; (P) 186.51; (R1) 187.37; More...

Intraday bias in GBP/JPY remains mildly on the upside at this point. Rebound from 184.44 would extend to retest 188.26 high first. Decisive break there will resume larger up trend. On the downside though, below 184.44 support will resume the fall from 188.26 to 183.79 resistance turned support.

In the bigger picture, as long as 180.74 support holds, larger up trend from 123.94 (202 low) should still be in progress, next target is 195.86 (2015 high). However, firm break of 180.74 will now argue that a medium term top is formed, possibly in bearish divergence condition in D MACD, and bring deeper fall back to 178.02 support.

Eurozone and UK PMIs Grab the Limelight in Thanksgiving Quietude

Global financial markets are experiencing subdued activity in Asian session today, with market participants scaling back their activity in light of Thanksgiving holiday. Major US stock indexes managed to close higher overnight, yet there's a palpable reluctance among investors to propel these indexes to new highs for the year. In contrast, Asian markets are demonstrating mixed reactions, oscillating within tight ranges without clear directional trends.

The commodities market is seeing some interesting movements. Gold has retreated below 2000 psychological level, after failing to break through its October high. This pullback might reflect a combination of profit-taking and market reassessment of Gold's near-term path. Oil prices are also experiencing limited movement, remaining in a narrow range. This stagnation follows news that OPEC+ is postponing its meeting, which has introduced uncertainty regarding future output cuts and consequently influenced oil prices.

In the currency markets, Dollar is showing slight signs of softening after yesterday's recovery attempt. It's now in a consolidation phase with downside potentially expected in the near term. Canadian Dollar and Sterling are also showing softness. Contrastingly, Australian and New Zealand Dollars, along with Yen, are emerging as stronger currencies for the day. Australian Dollar, in particular, is drawing strength from hawkish comments by RBA, despite disappointing PMI data indicating economic slowdown.

Euro is exhibiting mixed performance for the day and currently stands as the weakest for the week. As investors shift their focus to the upcoming PMI data from the Eurozone and the UK, there's potential for market movement. Eurozone's manufacturing sector has shown signs of stabilization in recent months, despite remaining in contraction territory. Services sector also seems to be avoiding further deterioration. Today's PMI data could potentially bring positive surprises, providing Euro with a much-needed boost.

From technical analysis standpoint, EUR/GBP is holding above 0.8687 support despite this week's deep retreat. Further rally is still in favor and break of 0.8764 resistance will resume whole rise from August low at 0.8491. However, break of 0.8687 and sustained trading below 55 D EMA (now at 0.8681) will argue that the rebound from 0.8491 has completed as a corrective move. That would turn near term outlook bearish for deeper fall.

In Asia, Japan is on holiday. Hong Kong HSI is down -0.24. China Shanghai SSE is up 0.32%. Singapore Strait Times is down -0.26%. Overnight, DOW rose 0.53%. S&P 500 rose 0.41%. NASDAQ rose 0.46%. 10-year yield fell -0.002 to 4.416.

ECB's Nagel: Close to terminal rate, but nobody knows

Bundesbank President Joachim Nagel, in his remarks at a conference overnight, suggested an element of uncertainty regarding further ECB rate hikes, adding that will be "data driven."

However, he expressed a belief that ECB is "close to that level we see as the terminal rate," and added, "rates will stay where they are for a while."

On a positive note, Nagel observed that inflation is on the decline, describing it as "a greedy beast" that ECB is actively working to tame. He expressed confidence in ECB's strategy, projecting that it is on track to bring inflation closer to its 2% target over the next 12-15 months.

Despite this optimistic view on inflation, Nagel cautioned that there are still risk factors that could spur another round of inflation. He acknowledged the uncertainty in predicting future economic developments, concluding with "So nobody knows" what's next.

BoC's Macklem: Interest rates may now be restrictive enough

BoC Governor Tiff Macklem, at an event overnight, acknowledged monetary tightening is "working". He suggested that the existing level of interest rates might be "restrictive enough" to achieve price stability.

Addressing the economic outlook, Macklem anticipates a period of softness in the near future. He noted, and highlighted the dissipation of excess demand that previously facilitated easier price increases in the economy.

Despite this outlook, Macklem reiterated BoC's willingness to increase rates again if the situation warrants.

Macklem's comments also came in the wake of the government's Fall Economic Statement, which he believes aligns with the central bank's objectives.

He remarked positively on the statement's implications that the government is "not adding new or additional inflationary pressures," Macklem said. Furthermore, he appreciated the introduction of new "fiscal guardrails", considering them beneficial from a monetary policy perspective.

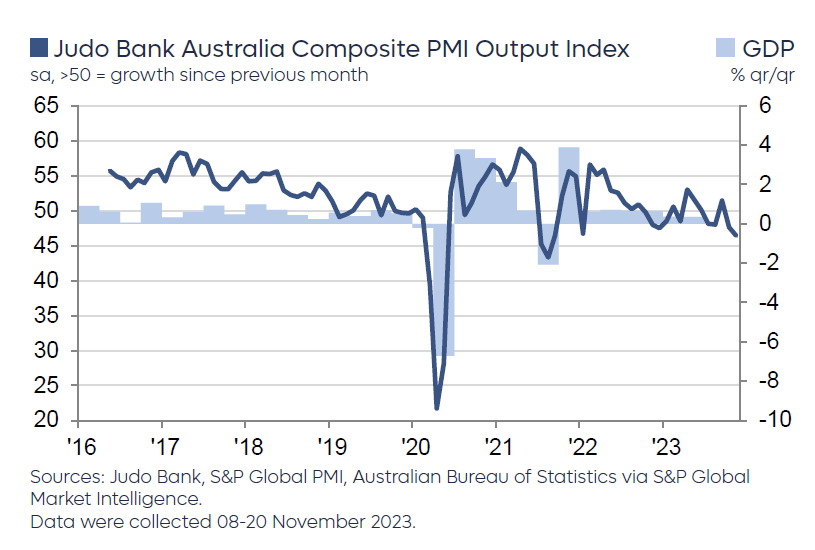

Australia PMI composite fell to 27-mth low at 46.4, but no real signs of hard landing

Australia's manufacturing and services sectors showed continued contraction in November, reaching multi-month lows. PMI Manufacturing index fell from 48.2 to a 42-month low of 47.7, while PMI Services index dropped from 47.9 to a 26-month low of 46.3. PMI Composite also decreased from 47.6 to a 27-month low of 46.4.

Warren Hogan, Chief Economic Advisor at Judo Bank, interpreted these figures as evidence of a further slowdown in Australian economic activity. He commented that the data "all but confirms that the economy is experiencing a soft landing," aligning with RBA's expectations. However, Hogan also noted that there are "no real signs of a hard landing" in the survey, indicating a more controlled economic deceleration.

Despite the overall softness in manufacturing, Hogan observed that the sector "does not appear to be slipping into recession" at this stage. Additionally, an improvement in the employment index in the services sector was seen as indicative of "continued strong demand for labour." This sustained high demand for labour, despite lower activity indexes, points to a persistent imbalance between labour demand and supply.

For RBA, the slowdown in business activity is a welcome development. Still, the strong employment index and an increase in price indexes signal ongoing inflation risks into 2024.

Hogan cautions that it is "still too early to think about rate cuts" in Australia.

Looking ahead

Eurozone and UK PMIs will be the main focuses in European session while ECB will also publish meeting accounts.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 185.98; (P) 186.51; (R1) 187.37; More...

Intraday bias in GBP/JPY remains mildly on the upside at this point. Rebound from 184.44 would extend to retest 188.26 high first. Decisive break there will resume larger up trend. On the downside though, below 184.44 support will resume the fall from 188.26 to 183.79 resistance turned support.

In the bigger picture, as long as 180.74 support holds, larger up trend from 123.94 (202 low) should still be in progress, next target is 195.86 (2015 high). However, firm break of 180.74 will now argue that a medium term top is formed, possibly in bearish divergence condition in D MACD, and bring deeper fall back to 178.02 support.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | Manufacturing PMI Nov P | 47.7 | 48.2 | ||

| 22:00 | AUD | Services PMI Nov P | 46.3 | 47.9 | ||

| 08:15 | EUR | France Manufacturing PMI Nov P | 43.2 | 42.8 | ||

| 08:15 | EUR | France Services PMI Nov P | 45.7 | 45.2 | ||

| 08:30 | EUR | Germany Manufacturing PMI Nov P | 41.3 | 40.8 | ||

| 08:30 | EUR | Germany Services PMI Nov P | 48.5 | 48.2 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Nov P | 43.4 | 43.1 | ||

| 09:00 | EUR | Eurozone Services PMI Nov P | 48 | 47.8 | ||

| 09:30 | GBP | Manufacturing PMI Nov P | 45 | 44.8 | ||

| 09:30 | GBP | Services PMI Nov P | 49.5 | 49.5 | ||

| 12:30 | EUR | ECB Meeting Accounts |

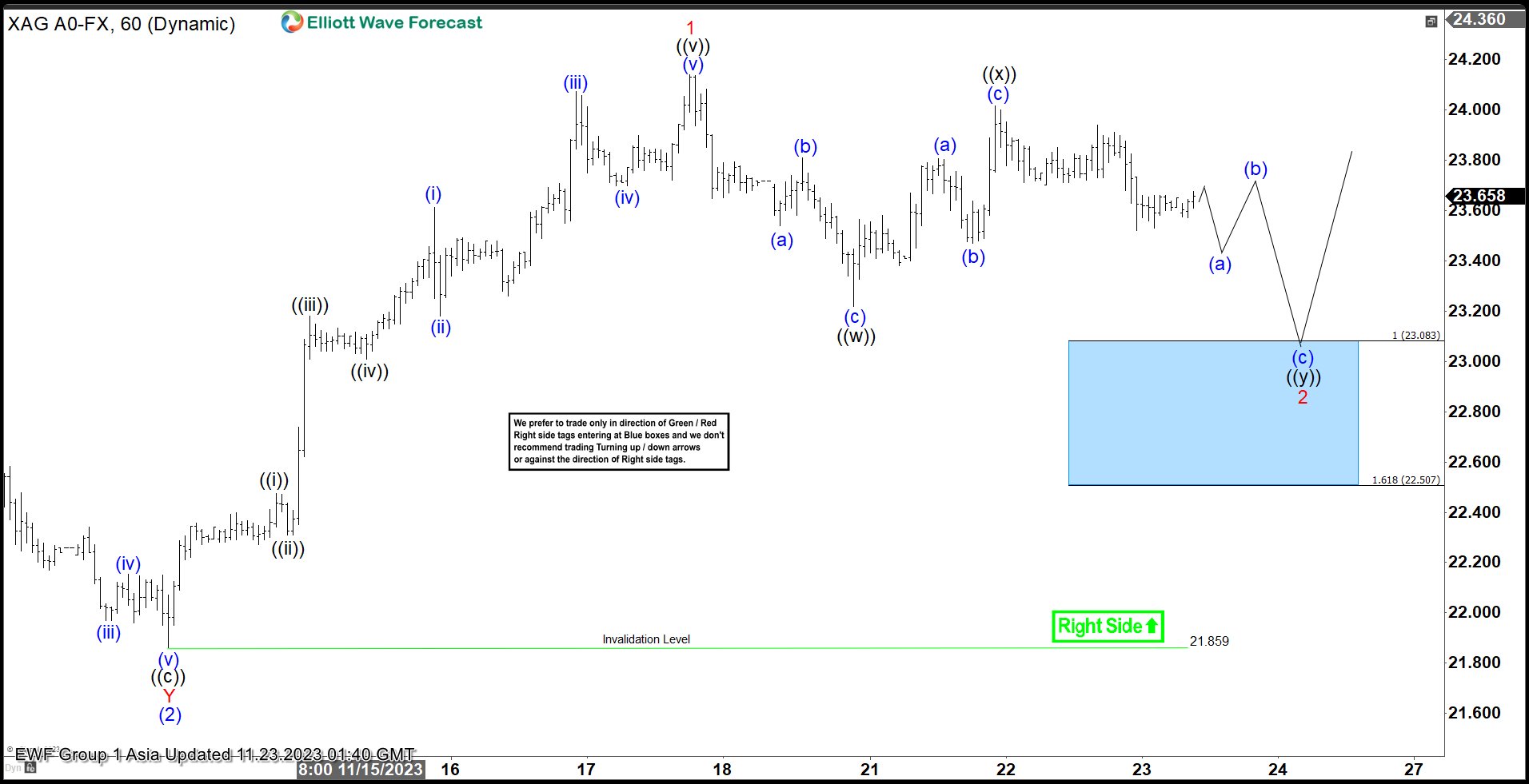

Silver (XAGUSD) Preparing for Breakout Higher

Silver (XAGUSD) shows a higher high (bullish) sequence from 10.3.2023 low favoring further upside. The rally higher from 10.3.2023 is unfolding as a 5 waves impulse. Up from 10.3.2023 low, wave (1) ended at 23.69 and pullback in wave (2) ended at 21.86 as the 1 hour chart below shows. Wave (3) higher is currently in progress with internal subdivision as an impulse in lesser degree. Up from wave (2), wave ((i)) ended at 22.47 and wave ((ii)) ended at 22.31.

Wave ((iii)) ended at 23.18, wave ((iv)) ended at 23.01, and final wave ((v)) higher ended at 24.14. This completed wave 1 in higher degree. Wave 2 pullback is currently in progress with internal subdivision as a double three. Down from wave 1, wave (a) ended at 23.54, wave (b) ended at 23.8, and wave (c) ended at 23.22. This completed wave ((w)). Wave ((x)) rally is proposed complete at 24.01. Expect the metal to turn lower in wave ((y)) towards the blue box area of 23.5 – 23.08. From this area, buyers should appear and the metal should resume higher. As far as pivot at 21.85 low stays intact, expect pullback to find support in 3, 7, 11 swing for further upside.

Silver (XAGUSD) 60 Minutes Elliott Wave Chart

Silver (XAGUSD) Elliott Wave Video

https://www.youtube.com/watch?v=lYM9tLyQa70

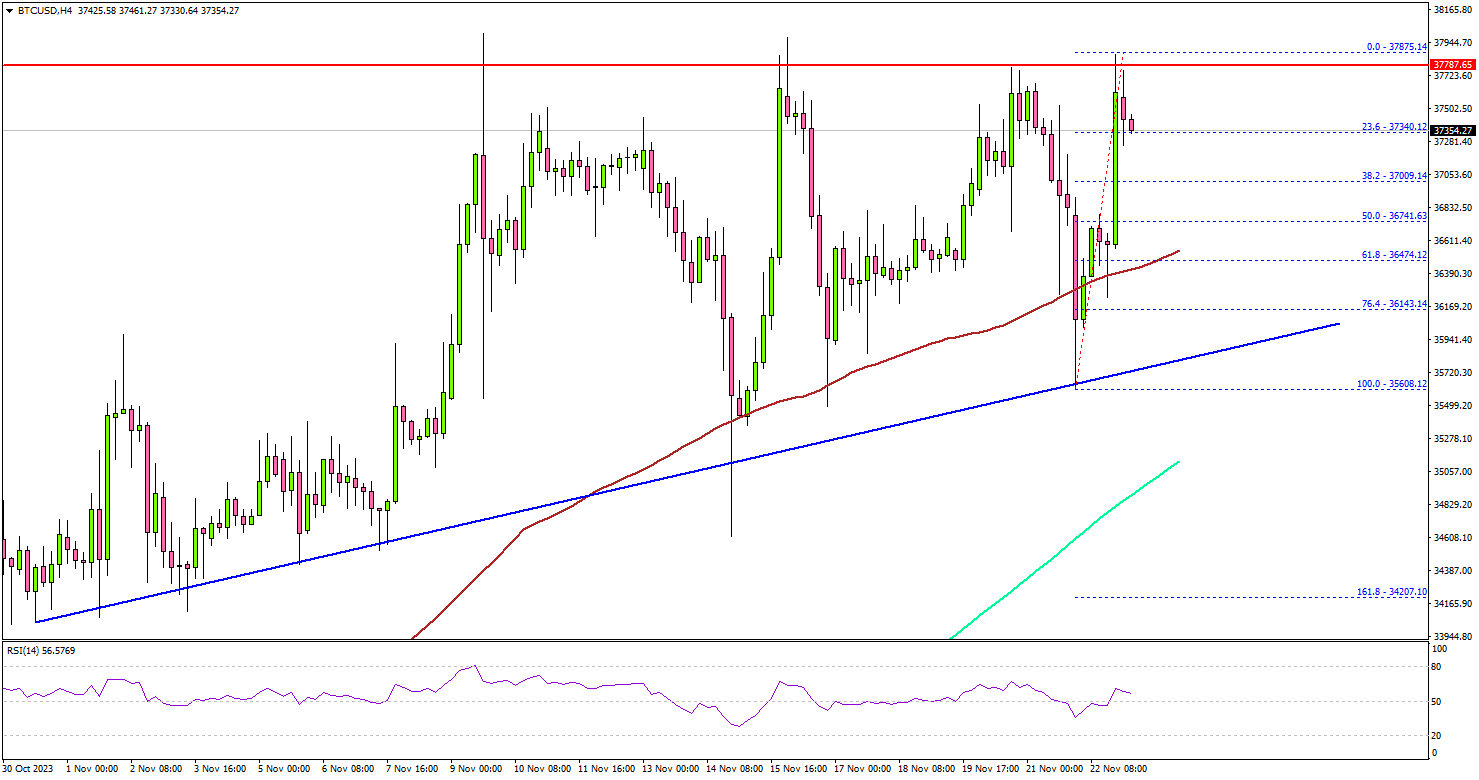

Bitcoin Price Holds Uptrend Support, Gold Consolidates

Key Highlights

- Bitcoin price started a fresh decline from the $37,750 resistance.

- BTC is still above a major bullish trend line with support at $35,800 on the 4-hour chart.

- Gold prices climbed higher toward the $2,000 resistance.

- Oil prices are struggling to recover above the $78.50 resistance.

Bitcoin Price Technical Analysis

Bitcoin price made a few attempts to gain strength above $37,750 and $38,800. However, BTC failed to extend gains and started a downside correction below $37,500.

Looking at the 4-hour chart, the price declined steadily below the $37,000 and $36,500 levels. It even spiked below the $36,000 level and the 100 simple moving average (red, 4 hours). However, the bulls were active near the $35,600 level.

BTC seems to be holding a major bullish trend line with support at $35,800 on the same chart. A low was formed near $35,608 and the price is still in a positive zone.

If there is a fresh increase, Bitcoin could face resistance near $37,600. The next resistance is near $38,000. A successful close above the $38,000 level might start a decent increase. In the stated case, the price may perhaps rise toward the $40,000 level.

If not, the price might continue to move down. The bears could attempt a downside break below the trend line support and the $36,500. The next major support is near $35,000 or the 200 simple moving average (green, 4 hours). Any more losses might send the price toward the $34,000 level.

Looking at gold prices, it is now consolidating gains and might soon attempt a fresh move above the $2,000 level.

Economic Releases

- Germany’s Manufacturing PMI for Nov 2023 (Preliminary) - Forecast 41.2, versus 40.8 previous.

- Germany’s Services PMI for Nov 2023 (Preliminary) - Forecast 48.5, versus 48.2 previous.

- Euro Zone Manufacturing PMI for Nov 2023 (Preliminary) – Forecast 43.4, versus 43.1 previous.

- Euro Zone Services PMI for Nov 2023 (Preliminary) – Forecast 48.1, versus 47.8 previous.

Weekly Economic & Financial Commentary: FOMC Proceeding Carefully on Policy

Summary

United States: A Feast of Economic Data Ahead of Thanksgiving

- The cornucopia of economic indicators stuffed into the first half of the week showed that economic growth is slowing. The Leading Economic Index fell for the 19th consecutive month in October, while durable goods orders and existing home sales both declined more than expected. That said, a drop in initial jobless claims is a sign that the labor market is still holding up. According to the University of Michigan, consumer sentiment improved in November, although inflation expectations ticked up again—an indication that price pressures have not yet been fully extinguished.

- Next week: New Home Sales (Mon.), Personal Income & Spending (Thu.), ISM Manufacturing (Fri.)

International: Argentina Shifts Away from Peronism

- This week, the presidential candidate representing traditional Peronism in Argentina's election lost in a relative landslide to Javier Milei, the Libertarian candidate looking to implement absolute change in Argentina.

- Next week: Bank of Israel (Mon.), Eurozone CPI (Thu.), India GDP (Thu.)

Interest Rate Watch: FOMC Proceeding Carefully on Policy

- The minutes from the Fed's November meeting emphasized that policymakers are proceeding carefully in terms of setting policy. The FOMC is in the fine-tuning stage of its tightening cycle and will adjust policy as needed to guide inflation back to target. We still forecast the FOMC is done hiking rates, though it will be some time before it begins to outright ease policy.

Australia PMI composite fell to 27-mth low at 46.4, but no real signs of hard landing

Australia's manufacturing and services sectors showed continued contraction in November, reaching multi-month lows. PMI Manufacturing index fell from 48.2 to a 42-month low of 47.7, while PMI Services index dropped from 47.9 to a 26-month low of 46.3. PMI Composite also decreased from 47.6 to a 27-month low of 46.4.

Warren Hogan, Chief Economic Advisor at Judo Bank, interpreted these figures as evidence of a further slowdown in Australian economic activity. He commented that the data "all but confirms that the economy is experiencing a soft landing," aligning with RBA's expectations. However, Hogan also noted that there are "no real signs of a hard landing" in the survey, indicating a more controlled economic deceleration.

Despite the overall softness in manufacturing, Hogan observed that the sector "does not appear to be slipping into recession" at this stage. Additionally, an improvement in the employment index in the services sector was seen as indicative of "continued strong demand for labour." This sustained high demand for labour, despite lower activity indexes, points to a persistent imbalance between labour demand and supply.

For RBA, the slowdown in business activity is a welcome development. Still, the strong employment index and an increase in price indexes signal ongoing inflation risks into 2024.

Hogan cautions that it is "still too early to think about rate cuts" in Australia.

BoC’s Macklem: Interest rates may now be restrictive enough

BoC Governor Tiff Macklem, at an event overnight, acknowledged monetary tightening is "working". He suggested that the existing level of interest rates might be "restrictive enough" to achieve price stability.

Addressing the economic outlook, Macklem anticipates a period of softness in the near future. He noted, and highlighted the dissipation of excess demand that previously facilitated easier price increases in the economy.

Despite this outlook, Macklem reiterated BoC's willingness to increase rates again if the situation warrants.

Macklem's comments also came in the wake of the government's Fall Economic Statement, which he believes aligns with the central bank's objectives.

He remarked positively on the statement's implications that the government is "not adding new or additional inflationary pressures," Macklem said. Furthermore, he appreciated the introduction of new "fiscal guardrails", considering them beneficial from a monetary policy perspective.

ECB’s Nagel: Close to terminal rate, but nobody knows

Bundesbank President Joachim Nagel, in his remarks at a conference overnight, suggested an element of uncertainty regarding further ECB rate hikes, adding that will be "data driven."

However, he expressed a belief that ECB is "close to that level we see as the terminal rate," and added, "rates will stay where they are for a while."

On a positive note, Nagel observed that inflation is on the decline, describing it as "a greedy beast" that ECB is actively working to tame. He expressed confidence in ECB's strategy, projecting that it is on track to bring inflation closer to its 2% target over the next 12-15 months.

Despite this optimistic view on inflation, Nagel cautioned that there are still risk factors that could spur another round of inflation. He acknowledged the uncertainty in predicting future economic developments, concluding with "So nobody knows" what's next.