Sample Category Title

Delay is No Good Sign

OPEC decided to delay this weekend’s meeting to next week because talks between Saudi and African members apparently ran into trouble. Saudi likely sensed in this week’s poor price action - ‘buy the fact that Saudi will double its production cuts’ action - that 1mbpd extra cut wouldn’t send the oil prices higher, sustainably. Hence, Saudis need other member to put their hand in the mud, and seemingly the negotiations aren’t easy.

A bit of history

Saudi has a history of walking away from its role of ‘swing producer’ - a crucial role in balancing global oil markets by adjusting its production levels to stabilize prices. Back in the 1980s, Saudi Arabia has shifted its strategy and opted for a market share approach. Instead of cutting production to support oil prices, Saudi Arabia had decided to increase its output significantly, contributing to a glut in the global oil market.

Therefore, if Saudi doesn’t get the support that it needs from the other producer countries after all the unilateral efforts that they put in, they will naturally be tempted to abandon the idea of doubling its supply cut, and eventually reverse it. Such a decision would lead to a sharp decline in oil prices and have a significant impact on the economies of other oil-producing nations.

The barrel of American crude sank to $73.50pb before rebounding to the $76 this morning. Brent fell below $80pb before rebounding above this level. Both in Brent and crude, the 200-DMA remains a solid resistance, as the worries of global slowdown outweigh the worries of supply restrictions, even more so as Saudis start giving signs of stress regarding their solo role in cutting production.

Speaking of morose growth projections

Forecasts for German growth in 2024 have been significantly lowered following the recent budget chaos after the German Constitutional Court declared government’s spending plans unconstitutional. Germany – Europe’s growth engine – is now seen growing just 0.4% next year. The UK, on the other hand, cut its own growth forecast significantly in yesterday’s Autumn Statement. Jeremy Hunt said that the economy would grow only by around 0.7% - still better than Germany, but that projection is down from the 1.7% announced earlier. The good news for British people and businesses is that Hunt announced tax cuts for both individual and companies and lowered the national insurance payroll levy. The Brits will now make a permanent 100% - yes 100% tax relief – on companies’ capital spending. But don’t be fooled by these beautiful numbers. In reality, the British tax burden will still mount to 38% of its GDP by the end of this decade and will reach its highest since post-WW2 and that 100% tax relief – the so-called ‘full expensing’ - is good for businesses that invest in big machinery but in a service-focused economy like the UK’s, the benefits will likely remain limited. This is certainly why the market reaction was muted yesterday. The 10-year gilt yield was slightly up, the FTSE 100 closed the session slightly in the negative, while Cable fell below the 1.25 mark, on the back of a broad-based rebound in the US dollar that hit most major peers.

Disinflation is on this year’s Thanksgiving menu

The US dollar index rebounded yesterday, and the rebound was on the back of some data points that cooled down the Fed doves’ enthusiasm. First, the short-term inflation expectations advanced to a seven-month high in November, with Americans expecting a 4.5% jump in prices over the next year. Then, the University of Michigan’s sentiment index improved more than expected, and the weekly jobless claims fell the most since June – all negative for the Federal Reserve (Fed) doves.

Adobe Analytics said that Thanksgiving shopping will be up by 5.4% this year, and no it is not because of inflated prices. On the contrary, according to Adobe e-commerce prices fell for the 14th straight month, by 6% from last October to this October and if we factor in the online deflation, the Thanksgiving spending growth would be an eye-popping 12%. But it’s always the same old story. Americans spend, but they spend their savings, and worse, they spend on debt. In this context, the use of buy now spend later options has jumped by 14.5% since last year – and it will certainly hit back, one day. For now, the US 2-year yield remains real steady around the 4.90% level, the US 10-year is headed back to fresh lows since this fall, after a short attempt for a rebound yesterday and the dollar index is back to testing the 200-DMA to the downside.

Happily, for the American people, the Fed doves and all of us, disinflation is on the menu of this Thanksgiving. Turkey prices cost around 5.6% less than last year, stuffing mix costs nearly 3% less, pie crusts are nearly 5% cheaper and cranberry prices are down by more than 18%. It is said that an average 10 people Thanksgiving feast would cost less than $62 - that’s less than $6.2 per person, down from around 4.5% compared to last year.

Last word

Thanksgiving is one of the calmest trading days of the year. Expect thin trading volumes and higher volatility.

Stronger EU Opposition as Dutch Politics Turn Right

Market movers today

Today will be the most exciting day of the week on the macro front.

On the global front we get preliminary Euro zone PMIs for November. We look for a rise in manufacturing PMI as several indicators have improved lately. Last week the German ZEW moved higher and it tends to give a good signal for Ifo and PMI. We have also seen Asian exports improve for some months, normally a sign the global manufacturing cycle is turning. However, the service PMI is even more important at this stage as the majority of jobs are in this sector. The PMI has fallen a lot over the past quarter.

We might receive the ECB's Q3 negotiated wage indicator today or tomorrow. The ECB does not publish the release date but the previous data releases have been between the 23rd and 25th in the second month following the quarter in question. We expect the indicator to show a slight increase in wage growth compared to the last quarter at 4.5% y/y. The latest agreements point to upside risks while high frequency trackers point to lower wage growth.

In Scandi, it is time for Riksbank meeting where we look for a "hawkish hold", see more below. Norway releases GDP for Q3.

The 60 second overview

UK fiscal policy: Yesterday, UK chancellor Jeremy Hunt presented the Autumn Statement, which was accompanied by a report by the OBR, the independent fiscal watchdog in the UK. The statement was overall in line with expectations with measures such as an increase in the national living wage, making full capex expending permanent, cut to national insurance, freeze alcohol duty for a limited period of time were presented. However, the cut to national insurance was larger than expected at 2%-points from 12% to 10% and is expected to affect 27m people. Additionally it is already set to come into effect from January 2024 instead of the usual spring 2024 with the new fiscal year. Markets reacted accordingly, sending rates higher given the possible inflationary nature of the measures. Combined with increase in National Living Wage this is set to put upward pressure on wage growth, a key input factor to service inflation, which is currently significantly above the long run average and a key concern for the BoE. In the broad picture however we see the effects on inflation as negligible but emphasise the upside risk to consumption in the near-term. Overall, we do not expect further hikes from the BoE and expect the first cut in June 2024.

Dutch election: According to an exit poll, the Dutch election did not go as expected. Far-right Gert Wilders' Freedom Party (PVV) supposedly got 35 out of 150 seats, 10 seats more than former EU Commissioner Frans Timmermans' Labour/Green Left combination. The conservative VVD, was in third place at 24 seats. Wilders is expected to try to form a right-wing government with the VVD and the new party 'New Social Contract', who together would hold a 79-seat majority. It could prove difficult though, due to Wilders' outspoken anti-Islam stance. Wilders is explicitly anti-EU, urging the Netherlands to control borders, to significantly reduce its payments to the EU and to block the entrance of any new members.

Equities: Global equities returned to positive yesterday driven by upbeat sentiment in the US. Please note, this was not just about 7 stocks and a bad excuse for underperformance. Both NVDA and TSLA where lower by more than 2% yesterday and we still saw a lift to all major indices. As vol is coming down, equity and importantly also bond vol, it supports all stocks, and we see a lift across sectors and styles. VIX yesterday broke down below 13, which is low in a full business cycle perspective but a typical late cycle phenomenon. In US yesterday, Dow +0.5%, S&P 500 +0.4%, Nasdaq +0.5% and Russell 2000 +0.7%. Markets in Asia are mixed this morning with optimism outside China while Chinese indices are struggling. US and European futures are roughly unchanged.

FI: EGB yields ended marginally higher yesterday, though intraday volatility remains elevated. The Bund curve flattened 4-5bp from the front as hawkish US data was released in the afternoon. Peripheral spreads widened a bit with the German ASW-spread. UST yields closed the session up 2-3 across the curve, while the Gilt curve rose 5bp following the higher than expected planned issuance next year announced yesterday by the UK DMO. Long-term inflation swap rates traded stable despite the high volatility in oil prices due to issues on building consensus for further production cuts within OPEC.

FX: EUR/USD declined significantly below 1.09, reaching a three-day low, driven by a robust USD following the release of strong US economic data. GBP moderately weakened on the back of the Autumn Statement accompanied by a weaker growth forecast by the OBR. The setback to oil prices sent NOK on the back foot in yesterday's session thereby putting a stop to the 3-day consecutive declines in EUR/NOK. Today, focus turns to Riksbank monetary policy with the decision at 9:30 CET where we expect an "unchanged" decision. For SEK, we see the outcome space as wide where a hawkish hold could prove slightly positive for the SEK, at least short term.

Credit: CDS indices were slightly tighter yesterday as iTraxx Main closed at 68bp (-1bp) and Xover at 377bp (-6bp). The primary market remained busy with several corporate deals (Vestas SLB, Coca Cola, Ericsson green bond, Imerys SLB) as well as further financial senior supply from Banco BPM and Credit Mutuel Arkea.

Nordic macro

Market pricing and analyst forecasts are split, close to 50/50, ahead of today's monetary policy decision from the Riksbank. We expect the Riksbank to keep the policy rate unchanged at 4.0% while still keeping the door open for a rate hike later on, if inflationary pressures remain higher than forecast (signalling around 10bp in the rate path for February). In other words a "hawkish hold". The main reasons behind this stance are: 1) both headline and core CPIF was around 0.1 percentage points higher than Riksbank's forecasts in October and this is too small to justify a rate hike in our view. Moreover, calculations of frontloaded and momentum inflation suggest inflationary pressures are receding quickly now. 2) The Krona (KIX index) is almost 5 percent stronger than Riksbank's forecast, at a level the Riksbank does not expect to see until Q2 2025. The implication of this deviation is that it adds to lower inflationary pressures than assumed in Riksbank's forecasts. 3) Other central banks, most notably the ECB, have taken on a "hawkish hold" approach to the policy rate. 4) Riksbank's own semi-annual business survey showed that household-related companies are signalling price cuts going forward on the back of easing labour and energy costs, weakening demand and increasing competition. 5) Recent Swedish macro data such as consumption, GDP and labour market data has weakened somewhat. We do not expect any news about the pace of QT, however, it is not possible to entirely rule out a step to speed up bond sales further. The decision and MPR released at 9.30 CET and a press conference with governor Thedéen (in Swedish) is scheduled for 11.00 CET.

We expect growth in mainland-GDP at +0.2 % q/q in Q3, but that the monthly figures will reveal a slowing trend pointing to a weak Q4.

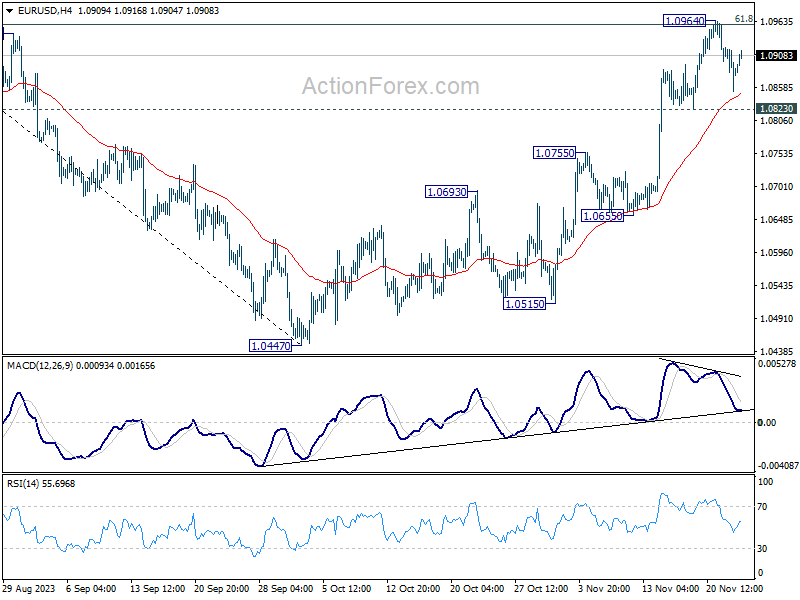

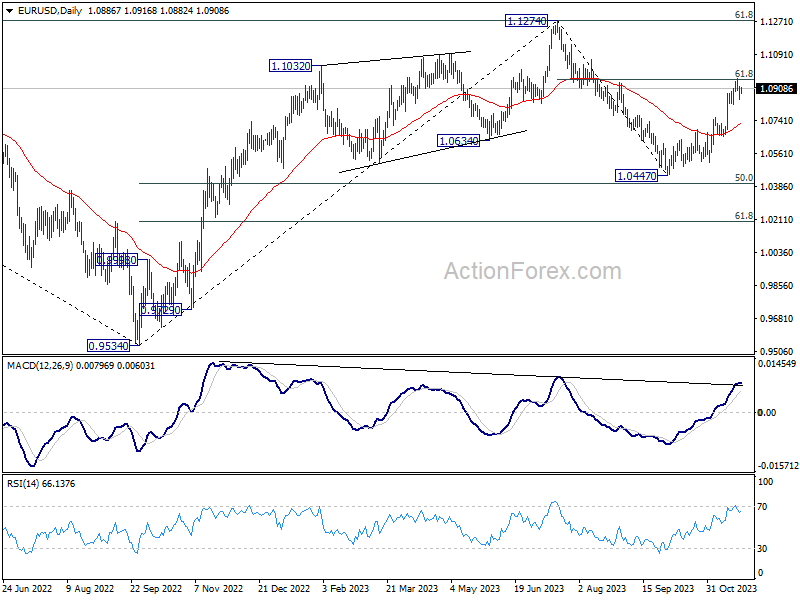

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0854; (P) 1.0888; (R1) 1.0924; More...

EUR/USD is staying in consolidation below 1.0964 and intraday bias remains neutral first. Further rally is in favor as long as 1.0823 support holds. Sustained break of 61.8% retracement of 1.1274 to 1.0447 at 1.0958 will resume the rise from 1.0447 to retest 1.1274 high. However, firm break of 1.0823 will indicate short term topping, and turn bias back to the downside for deeper decline.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

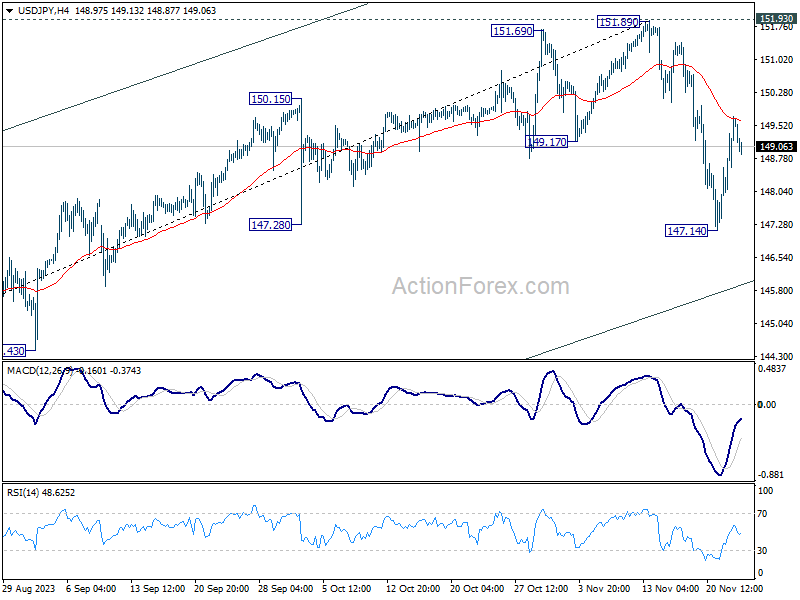

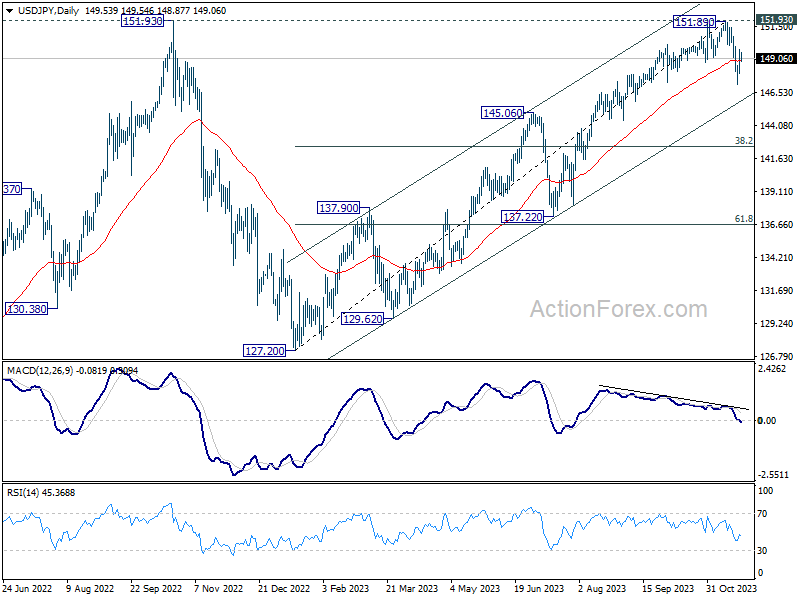

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.46; (P) 149.10; (R1) 150.19; More...

USD/JPY retreated after hitting 55 4H EMA (now at 149.62) holds. Intraday bias is turned neutral first, and further decline is expected. Break of 147.14 will resume the fall from 151.89 and target medium term channel support at 146.00 next. Nevertheless, sustained break of 55 4H EMA will revive near term bullishness, and target a retest on 151.89/93 resistance zone.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 resistance (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

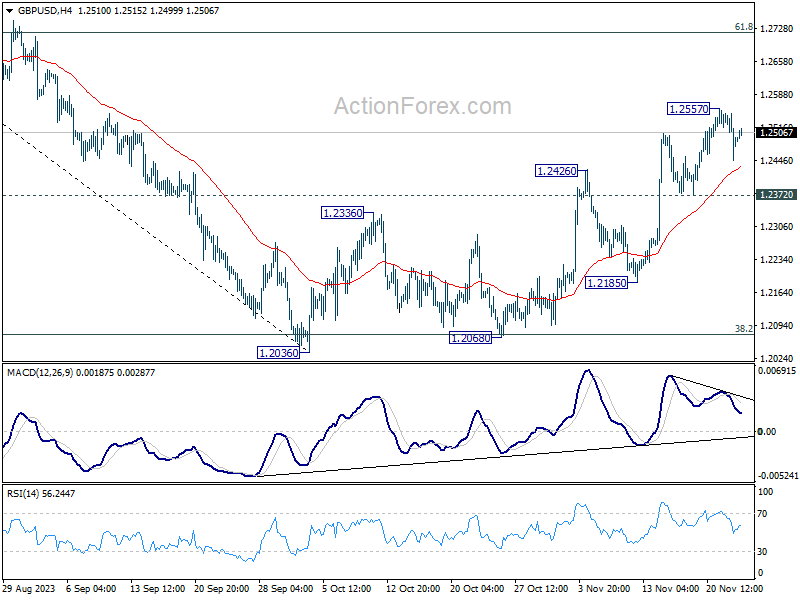

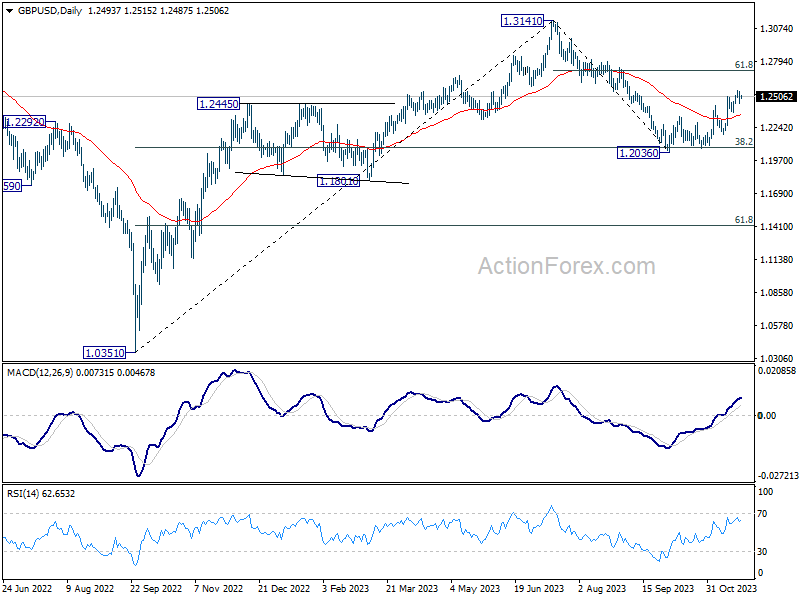

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2445; (P) 1.2498; (R1) 1.2546; More...

GBP/USD is staying in consolidation below 1.2557 and intraday bias stays neutral. While deeper retreat might be seen, further rally is expected as long as 1.2372 support holds. Above 1.2557 will resume the rise from 1.2036, and target 61.8% retracement of 1.3141 to 1.2036 at 1.2716 next.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 argues that current rise from 1.2036 is the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

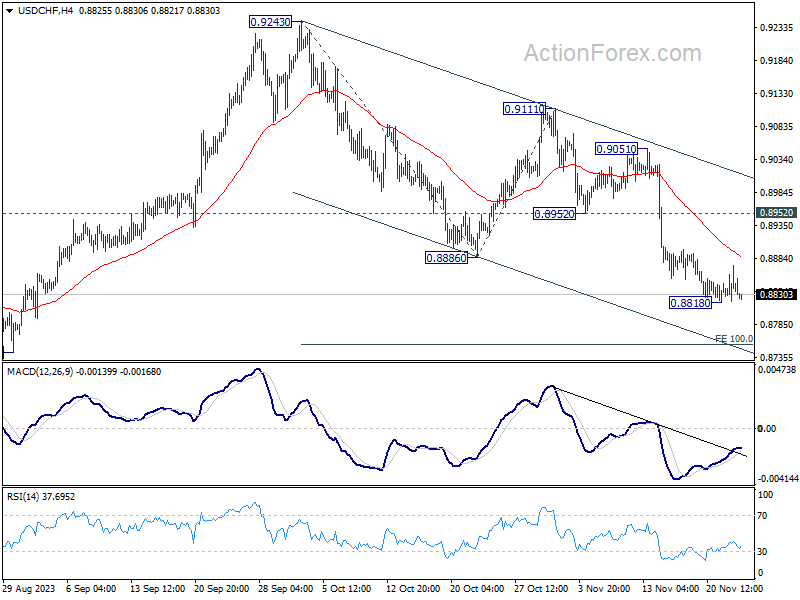

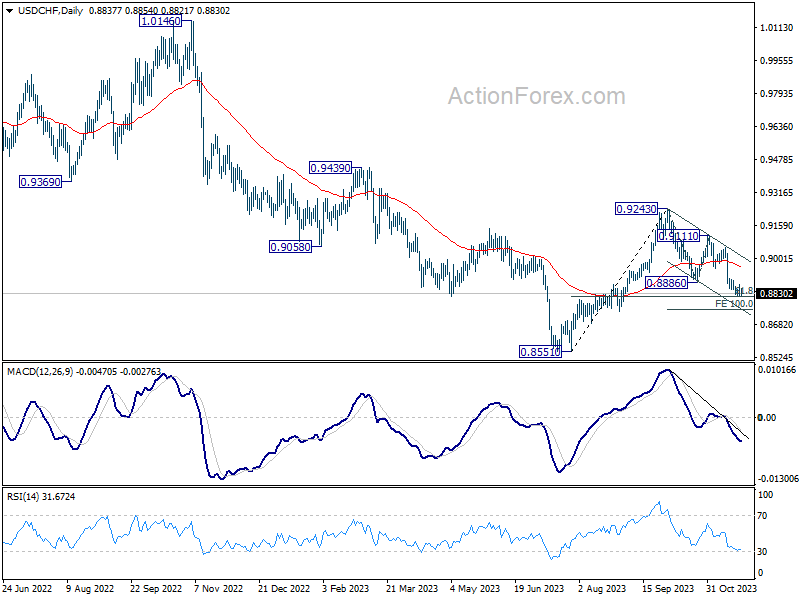

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8814; (P) 0.8845; (R1) 0.8869; More....

Intraday bias in USD/CHF remains neutral as consolidation from 0.8818 is extending. Stronger recovery cannot be ruled out, but near term outlook will stay bearish as long as 0.8952 support turned resistance holds. On the downside, below 0.8818 will resume whole decline from 0.9243 to 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754 next.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper fall would be seen to 61.8% retracement of 0.8551 to 0.9243 at 0.8815. Sustained break there will bring retest of 0.8551 low. For now, this will remain the favored case as long as 0.9111 resistance holds.

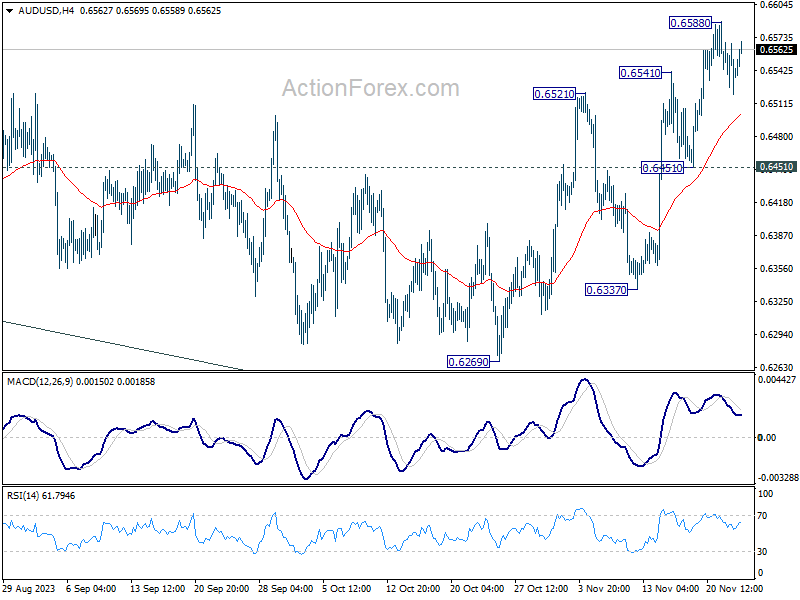

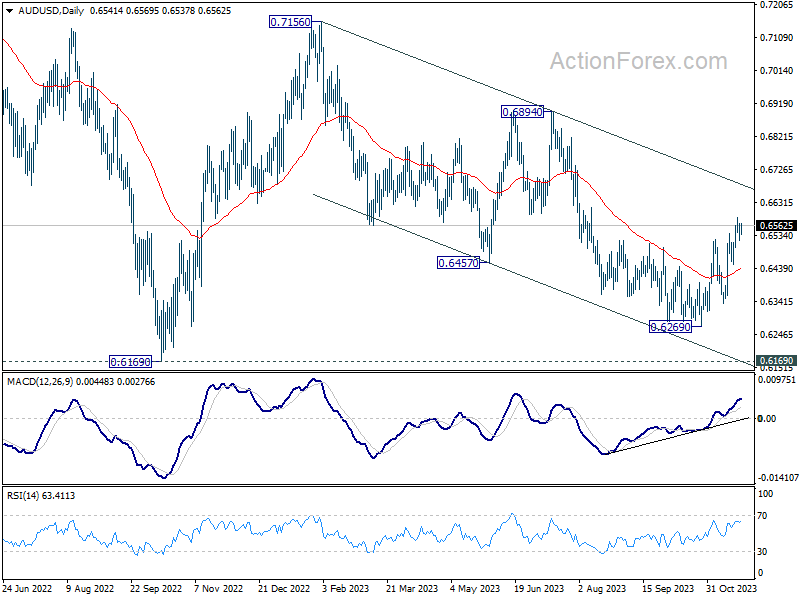

AUD/USD Daily Report

Daily Pivots: (S1) 0.6520; (P) 0.6545; (R1) 0.6568; More...

Intraday bias in AUD/USD remains neutral for the moment. More consolidations could be seen below 0.6588. But downside should be contained above 0.6451 support to bring another rally. On the upside, above 0.6588 will resume the rebound from 0.6269 to falling channel resistance (now at 0.6676) next.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of the corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3660; (P) 1.3712; (R1) 1.3740; More...

No change in USD/CAD's outlook as sideway trading continues below 1.3897. While another fall cannot be ruled out, downside should be contained by 38.2% retracement of 1.3091 to 1.3897 at 1.3589 to bring rebound. Break of 1.3897 is expected at a later stage to resume larger rally.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will remain the favored case as long as 1.3378 support holds.

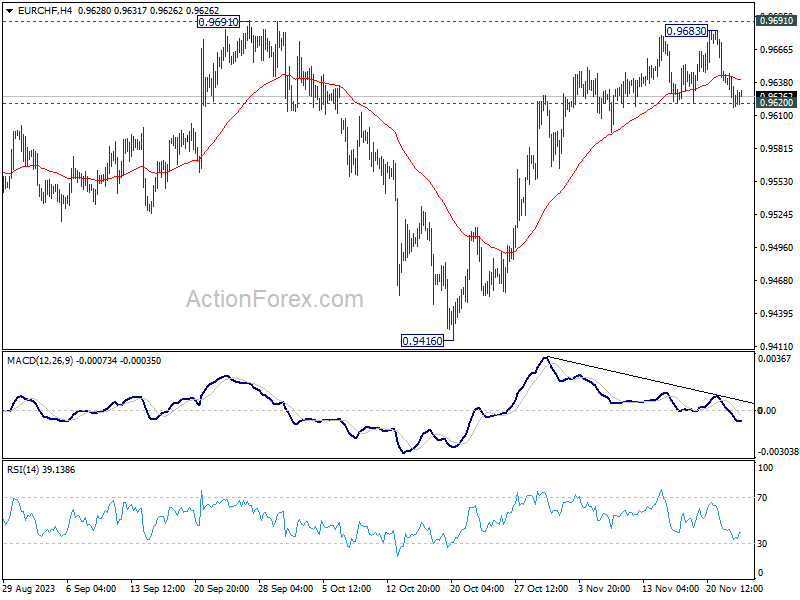

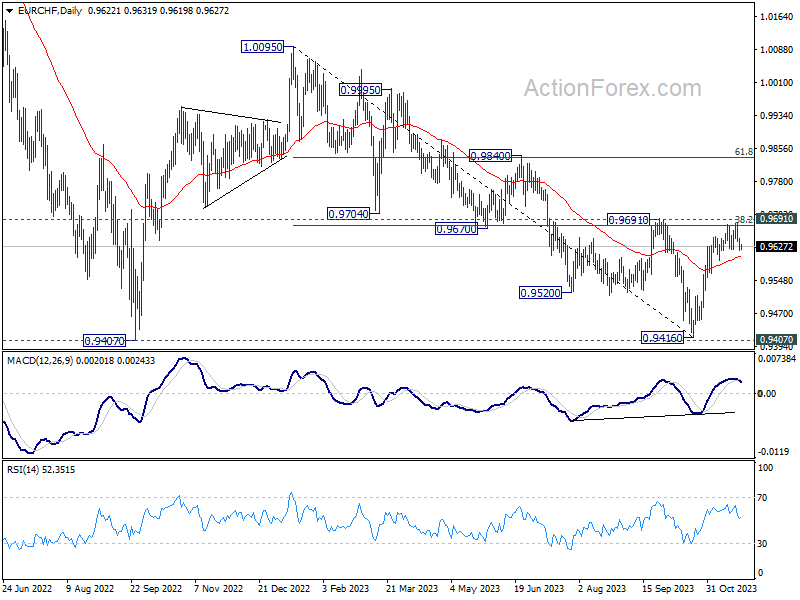

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9612; (P) 0.9631; (R1) 0.9642; More...

Intraday bias in EUR/CHF stays neutral for the moment. On the upside, decisive break of 0.9691 resistance will carry larger bullish implication, and target 0.9840 resistance next. However, break of 0.9620 support will indicate short term topping, and turn bias back to the downside for deeper pull back.

In the bigger picture, fall from 1.0095 (2023 high) might have completed at 0.9416, just ahead of 0.9407 support (2022 low). Sustained break of 0.9691 cluster resistance (38.2% retracement of 1.0095 to 0.9416 at 0.9675) will pave the way to 61.8% retracement at 0.9836 and above. However, rejection by 0.9691 will maintain medium term bearishness for another test on 0.9407 at least.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8696; (P) 0.8711; (R1) 0.8729; More....

Intraday bias in EUR/GBP remains neutral for the moment. Also, another rally is in favor with 0.8687 support holds. On the upside, break of 0.8764 will resume whole rebound from 0.8491. However, decisive break of 0.8687 will confirm short term topping, and turn bias back to the downside for 0.8648 support and below.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. This will remain the favored case as long as 0.8648 support holds.