Sample Category Title

Preview of RBNZ: Talking Tough About Doing Little

- We expect the RBNZ will leave the OCR unchanged at 5.5% at its November policy meeting.

- The RBNZ's forward profile for the OCR is likely to be little changed and suggest no change in the OCR in 2024.

- Short term inflation forecasts will be reduced, but the longer-term profile will likely be little changed.

- The RBNZ will be keen to ensure as much of the recent increase in mortgage rates remains in place for a while.

The RBNZ's decision and forward track.

We expect the RBNZ will leave the OCR unchanged at 5.5% at its November policy meeting. There will be more interest in the profile for interest rates in 2024 given recent market speculation of a pivot towards OCR cuts in 2024. We think the RBNZ will show a slightly flatter OCR profile that will still convey an on-hold stance through 2024.

We anticipate that recent progress on tradables inflation will be acknowledged and incorporated into the RBNZ's short term inflation forecasts. But we also see the RBNZ continuing to emphasise the medium-term risks to inflation given that the level of inflation remains high and core inflation pressures (including non-tradables inflation) are yet to significantly moderate.

We think the RBNZ's objective will be to try to maintain recent tighter financial conditions by talking tough but doing little in 2024.

Key developments.

Prior to the October Monetary Policy Review we think the RBNZ likely interpreted the data flow as indicating slightly increased medium-term inflation risks. Key relevant factors that would have contributed to these concerns included: stronger GDP in the June quarter and hence less progress in reducing excess demand; ongoing jobs and employment growth (compared to expectations of a weakening trend); higher energy and fuel prices, and improved commodity prices compared to the downside risks apparent in August. Offsetting factors will have been further evidence of weak discretionary spending, investment, and some reductions of firm costs and business and household inflation expectations. Crucially, the significant rise in mortgage rates and longer-term interest rate expectations that occurred over the August- October period were a significant offset and could be the equivalent of another rate hike if sustained. Our assessment is that the net of these factors probably would have led to a slightly higher peak OCR but mainly an extension of the period over which the RBNZ expected the OCR to remain at 5.5% (and into 2025).

Since then, the data flow has been supportive of RBNZ's view that a 5.5% OCR will prove sufficient. Tradables inflation has fallen more quickly than anticipated. Labour market indicators showed signs of the required move higher in unemployment and softening wage growth (at least in the private sector). The price of oil receded from its October highs, reducing headline inflation and expectations concerns the RBNZ may have had. Also, we have continued to see weakness in cyclical demand indicators (retail spending, PMIs, credit growth, imports) which the RBNZ will see as removing any pressure it was feeling to lift the OCR. On balance there's likely little net change in the OCR profile required for the totality of the data seen since August.

Some key medium term inflation risks remain which we think will make the Bank reticent to validate the market's pricing of rate cuts next year. A key issue is ongoing strength in population growth and migration with associated pressures on housing and rental markets. The RBNZ recognises the risks here but is reserving judgement until next year to see if the composition of migration or the level of interest rates proves sufficient to balance the risks. We don't see them making substantial judgements aside from perhaps some further upward adjustment to the forecast of near-term potential growth and a further modest upward adjustment to house price expectations - enough to acknowledge that the risks but not enough to warrant action.

The RBNZ may have some discussion on its initial take on the implications of the new government for the macroeconomic outlook. As of writing no coalition agreement has been signed and hence, we don't have a fully articulated set of policies to go on. The RBNZ probably also won't have much detail but will have an idea of the broad parameters of what the next government will do and could have a box discussing the potential implications (it did so in 2017, following the election of the new Labour-led government). The most prominent policies likely would relate to the housing market (which would likely increase inflation concerns at the margin) and the general fiscal stance (which will likely be supportive of disinflation, again at the margin). We don't think the new government's policies will significantly shift the OCR stance now. Certainly, the PREFU fiscal assumptions, with their slightly more restrictive stance, will be incorporated into the RBNZ's updated forecasts.

The communications objective.

We think the RBNZ will want to discourage markets from pricing an early reduction in the OCR. Mainly, this is because the RBNZ will not want to encourage any more easing in financial conditions than appropriate given the still present medium-term inflation risks.

The RBNZ will be aware of the current tendency for markets to run with dovish expectations and we think it will tailor communications to offset that tendency. Hence, they will talk tough about doing nothing for the foreseeable future. This likely means the RBNZ won't move their OCR forecast profile much. We expect they will emphasise a determination to get inflation sustainably inside the target range in 2024 and keep it in there in 2025. Those medium-term risks will be enough to keep them talking tough and pushing aside market views of 50-100bps of easing in 2024.

We see three main scenarios:

- Baseline case (70% probability) the OCR remains at 5.5% and the forecast track still shows the small chance of a rate hike in H1 2024, but the OCR remains at 5.5% until early 2025.

- Hawkish case (10%) the OCR remains at 5.5% but the forecast track is revised up in H2 2024 to convey an increased risk of higher rates through 2024. This would be linked to risks of housing strength, a slower rise in the unemployment rate and an ongoing sluggish response of core inflation to tight monetary policy (even though tradables inflation will be revised lower).

- Dovish case (20%) the OCR remains at 5.5% and the OCR track is revised down to a flat profile at 5.5% until Q4 2024 with a full cut indicated by the February 2025 MPS. There may be some chance of a cut at the Nov 2024 MPS on the assumption the Q3 CPI shows inflation inside the target range or provides sufficient confidence that it will be by end of 2024.

We don't think the dovish scenario will achieve the RBNZ's communications objectives, but it may attempt to discourage the pricing of earlier easings by stridently emphasising the near-term on-hold message. As we discussed in our note "When's the pivot?" we don't see many plausible scenarios for an OCR cut before the September quarter of 2024. There's still plenty of potential for upside risks given we haven't seen much evidence of non-tradables inflation pressures declining and the jury is still well and truly out on the impact population growth is going to have on demand and medium-term inflation pressures.

Our OCR view for 2024.

We still project a 25bp hike in the OCR in February 2024, with policy settings then on hold from there to February 2025. However, that call for higher rates teeters on a knife edge as the RBNZ has plenty of reasons for standing pat. We will review our forecast based on what the RBNZ tells us about its reaction function next week.

Markets Daily

Bond yields and the US dollar rose in response to second-tier US economic data (jobless claims, inflation expectations). Australian yields rose in response to RBA Governor Bullock’s speech but AUD slipped to 0.6540. Today we see November PMIs in the Eurozone and UK while US markets are closed for Thanksgiving.

Yesterday

Major currencies were mostly little changed to a touch weaker against the US dollar, after recent strong gains. News flow was light, with perhaps only a flicker of improvement in risk appetite on the Israel-Hamas hostage agreement. AUD/USD touched 0.6570 at the time of those headlines, but generally traded quietly ahead of the Bullock speech, -0.2% in late trade at 0.6540.

Currencies/Macro

The US dollar was either flat or firmer against G10 FX on the day. EUR/USD fell from 1.0910 to 1.0885. GBP/USD fell 45 pips to 1.2495. USD/JPY rose from 148.40 to 149.60. AUD/USD dipped to 0.6521 then trimmed losses to -0.2% at 0.6540. NZD/USD fell a net 30 pips to 0.6020. AUD/NZD rose 0.25% to 1.0865.

RBA Governor Bullock delivered a speech overnight to the annual Australian Business Economists dinner, including some hawkish comments on Australia’s inflation challenge, saying it is “increasingly homegrown and demand driven…If inflation is simply the product of global supply disruptions or other price rises” then the appropriate interest-rate response would be limited…However, a more substantial monetary policy tightening is the right response to inflation that results from aggregate demand exceeding the economy’s potential to meet that demand.”

US weekly initial jobless claims were lower than expected at 209k (est.228k, prior 233k), with continuing claims at 1940k (est. 1875k, prior 1862k).

US durable goods orders, a volatile series, fell -5.4%m/m in October (est. -3.2%, prior revised to +4.0% from 4.6%). Ex-transport and non-defence orders were close to expectations.

November consumer sentiment (University of Michigan) was finalised higher at 61.3 (preliminary 60.4), with 1yr-ahead inflation expectations at 4.5% (est. and prelim. 4.4%) and 5-10yr-ahead at 3.2% (est. 3.1%, prelim. 3.2%).

Interest rates

US 2yr treasury yields bounced off an overnight low of 4.84% to 4.90%, while the 10yr yield bounced off 4.36% to 4.45% then closed at 4.40%, with the jobless claims data causing the initial rise, and then the inflation expectations survey. Markets are pricing the Fed funds rate, currently 5.375% (mid), to be unchanged at the next few meetings, with a 50% of a rate cut in from May 2024.

Australian 3yr government bond yields (futures) initially rose from 4.08% to 4.17% following RBA Governor Bullock’s speech, later extending to 4.17% after the US data, while the 10yr yield rose overall from 4.44% to 4.52%. Markets are pricing no hike at the next meeting on 5 December, but a 70% chance of one by May 2024. New Zealand rates markets price the OCR, currently at 5.50%, to be unchanged on 29 November, and in February as well, with a 40% chance of a rate cut by May 2024.

Credit markets continued to outperform with Main another bp tighter to 68, CDX in 1.5bp to 62.5 and US IG cash 2-3bp better in anticipation of tonight’s Turkey dinner. Notably, while US IG credit is now beginning to approach its low range for the year, banks are far from that mark having not yet recovered post SVB, providing further potential upside as relationships normalise. Primary activity remain light with the US effectively shut on the way into Thanksgiving while Europe saw 8 issuers price ~EUR4bn.

Commodities

Crude markets slumped circa 5% on news that the OPEC+ meeting slated for this weekend Sunday had been postponed until the following Thursday, though prices recovered much of the lost ground as fingers were pointed at African nations including Angola and Nigeria as the source of disagreement. The January WTI contract is down 86c at $76.91 while the January Brent contract is down 65c at $81.80. The EIA reported that Cushing stocks rose for the fifth consecutive week and national stocks rose by a hefty 8.7mb to the highest since July. However, a four-week measure of diesel demand hit the highest in almost a year and other oil stockpiles fell the most since September, taking some of the bearish slant off the report. Morgan Stanley described the upcoming OPEC decision as “especially critical now”. Bloomberg noted that the January Brent crude options contracts expire on Monday November 27, meaning that hedges put in place for the OPEC meeting will expire before the outcome is known.

Metals were also hit by the rise in the US$ and the deepening of bearish contango structures on the LME. Copper is down 0.9% to $8,376 while aluminium is down 1.6% to $2,221. Nickel fell by a hefty 2.9% to $16,505. The spot discount to 3-month copper dropped to a fresh record low at -$100 while Bloomberg noted that all six key metals traded on the LME are now in contango. LME on warrant zinc stocks rose by a hefty 56% to the highest since 2021 and nickel prices hit fresh two-year lows with Macquarie noting “an ongoing surge in nickel related exports” from Indonesia. Nickel prices are down 45% year to date. Codelco was cut by Fitch “due to declining output related to operational issues and the delayed completion of its key investment projects”. Codelco and the Japan Bank for International Cooperation signed a critical minerals funding accord covering the supply of copper, lithium and molybdenum.

Iron ore markets showed some signs of profit taking after the NDRC summonsed key market participants for a meeting where the current market structure was discussed. The December SGX contract is down $1 from the same time yesterday to $132.95 though the 62% Mysteel index (spot) rose 55c to $135.50.

Day ahead

Today we see S&P Global flash November PMIs in various jurisdictions, most notably the Eurozone and UK. The Eurozone PMIs will likely remain little changed in November, given manufacturing’s downbeat outlook and services activity experiencing a continual reduction in new orders growth (market f/c: 43.5 and 48.1, respectively).

In the UK, the S&P Global PMIs are expected to remain relatively stable in November, as manufacturing slows from struggling demand and services cools (market f/c: 45.0 and 49.5, respectively).

US markets will be closed due to Thanksgiving Day.

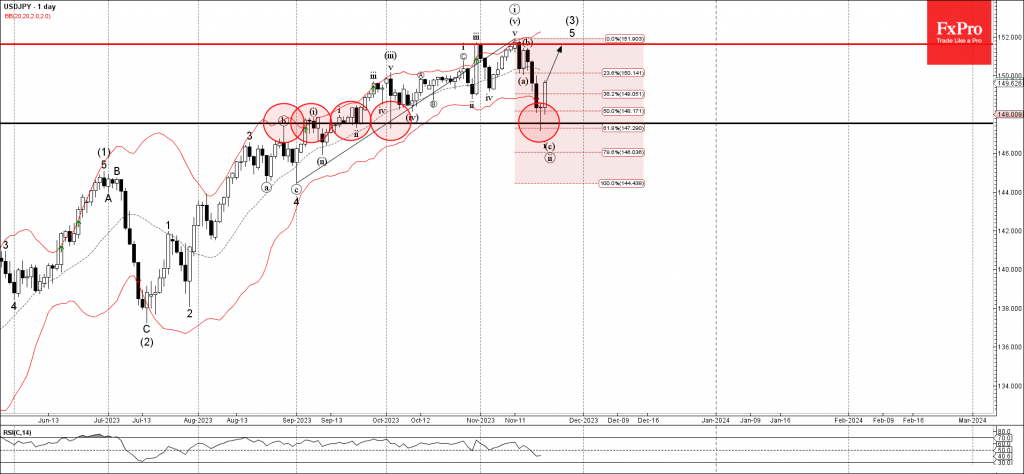

USDJPY Wave Analysis

- USDJPY reversed from key support level 147.55

- Likely to rise to resistance level 152.00,

USDJPY currency pair recently reversed up from the key support level 147.55 (which has been supporting the price from September) intersecting with the 61.8% Fibonacci correction of the upward impulse from August.

The upward reversal from the support level 147.55 is currently forming the daily Morning Star candlesticks reversal pattern, which stopped the earlier minor correction ii.

Given the predominant daily uptrend, USDJPY currency pair can be expected to rise further to the next resistance level 152.00, which stopped the previous waves iii and i.

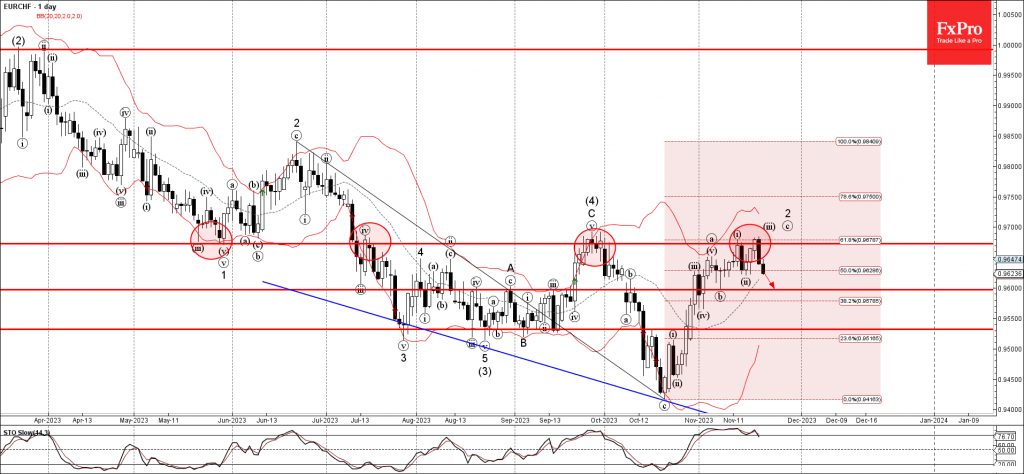

EURCHF Wave Analysis

- EURCHF reversed from resistance level 0.9670

- Likely to fall to support level 0.9600

EURCHF currency pair recently reversed down from the strong resistance level 0.9670 (former strong support from May, which has been repeatedly reversing the pair from July) intersecting with the 61.8% Fibonacci correction of the downward impulse from June

The downward reversal from the resistance level 0.9670 created the daily Evening Star, which stopped the earlier correction 2.

Given the clear daily downtrend, EURCHF currency pair can be expected to fall further to the next support level 0.9600, low of the previous correction b.

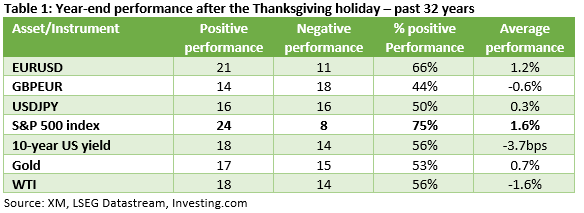

Does Santa Claus Rally Really Exist?

- US equities exhibit a strongly positive year-end performance post-Thanksgiving

- FX pairs do not follow a specific pattern in the examined period

- Gold and USDJPY rally every time the Thanksgiving holiday falls on November 23

We are nearing the end of another trading year and the newswires are crammed with stories about the famous Santa Claus rally. In a nutshell, the market believes that risky assets tend to rally towards the end of the year. Most analysts calculate the assets’ performance during the last five trading days of the year and the first two of the new year when analysing this “phenomenon”. However, others are confident that this rally tends to start after the annual Thanksgiving holiday.

Consequently, we decided to have a look at the performance of the main tradable assets for the period between the Thanksgiving holiday and the last trading day of the year. We selected 1991 as our starting year, not for the lack of data but because we feel that this timeframe is a closer match to current market conditions.

S&P 500 index sends the strongest message

Table 1 below presents our findings for the 32 years of market data examined. After a quick glance, one can see that there is no widespread rally at the instruments in question. However, there are some interesting results. The S&P 500 index is sending the strongest message as it has managed to finish the year in the green in 75% of the periods examined, i.e. 24 years, with an respectable average gain of 1.6% achieved. Regarding the FX world, only EURUSD tends to exhibit a pattern with 66% of the years ending on a positive note and recording a decent return of 1.2% on average.

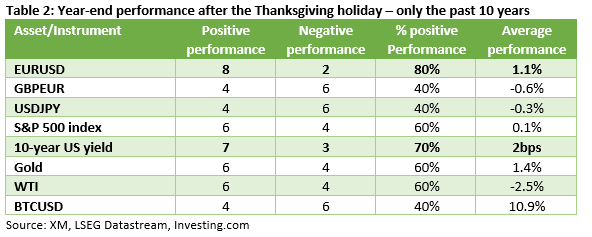

When focusing only on the past 10 years, the results somewhat change. More specifically, EURUSD tends to rally after the Thanksgiving holiday with an average gain of 1.1%. The 10-year US yield exhibits a similar score, but the average yield increase is just 2bps, which is rather miniscule for its standards. We have also included BTCUSD (Bitcoin) in Table 2 below, but the results do not really confirm the Santa Claus rally, despite the 10.9% average rally.

What happens in the pre-election years?

We could not complete our analysis without the main 2024 event: the US election held in November. Such a major event affects investment decisions long before the actual election date as market participants prepare for the next administration. Therefore, we examined the year-end performance of key assets, after the Thanksgiving holiday, in the eight pre-elections years appearing in our data. Interestingly, only the performance of the S&P500 index stands out. Except for 2015, this index tends to end the year positively with an average gain of 4.3% registered.

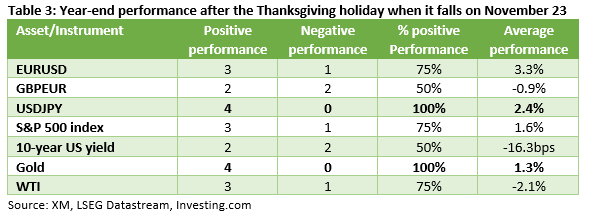

What happens when the Thanksgiving holiday falls on November 23?

Our final step was to examine the performance of these assets when the Thanksgiving holiday falls on November 23, like in 2023. We found four instances in the 1991-2022 period when this occurred: in 1995, 2000, 2006 and 2017. A smaller sample to play with but we have two assets, gold and USDJPY, rallying in these four periods. Gold is seen gaining 1.3% on average, while USDJPY tends to climb by 2.4%.

To sum up, the market appears to be gearing up for a Santa Claus rally and, according to our findings, the S&P500 index tends to confirm this expectation when examining the 32 years of data. Drilling down to just the past 10 years, EURUSD exhibits a strong tendency to rally into year-end. Finally, when the Thanksgiving holiday falls on November 23, USDJPY and gold appear to enjoy a strong upleg by the end of the trading year.

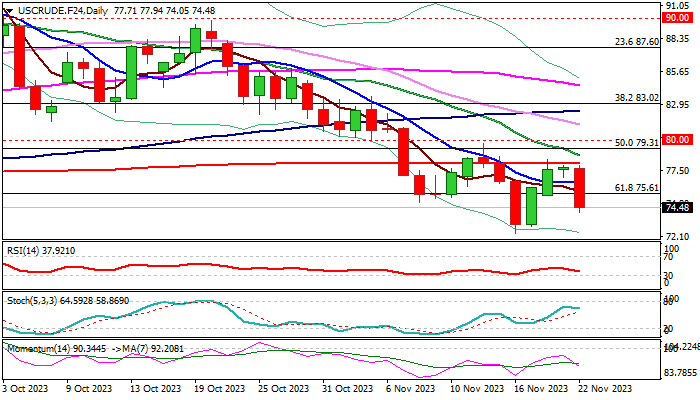

WTI Oil Price Tumbles on OPEC News

WTI oil price was sharply down on Wednesday (4.1% until early US session), deflated by the news that OPEC+ group delayed their meeting scheduled for Nov 26 to Nov 30.

The cartel is widely expected to extend its supply cut into next year, but there are also speculations that world biggest oil producers may deepen cuts, as the outlook for global demand remains gloomy.

Fresh weakness further weakened the picture on daily chart, as bull-trap above 200DMA was initial negative signal, boosted by today’s strong bearish acceleration which retraced over 61.8% of $77.36/$78.44 upleg and signaling that recovery phase is likely over.

Daily MA’s returned to full bearish configuration and 14-d momentum fell deeper into negative territory, contributing to threats of retesting Nov 16 multi-month low ($72.36) loss of which would signal continuation of larger downtrend from $95.00 (2023 high).

Broken Fibo 61.8% ($75.61) reverted to initial resistance, followed by 10DMA ($76.54), with 200DMA ($78.06) being a game changer.

Res: 75.61; 76.51; 78.06; 78.78.

Sup: 74.05; 73.57; 72.89; 72.36.

Sunset Market Commentary

Markets

European markets this morning kept a soft approach. Lower yields at that time still were the path of least resistance. Eco data were few. The ECB in its financial stability report warned that stability in the euro area remains fragile as tighter financial conditions are testing the resilience of euro area firms, households and sovereigns. Financial markets and non-banks are vulnerable to adverse macro-economic surprises. For now higher rates underpinned bank profitability, but worsening asset quality and higher funding costs pose headwinds. In this respect, macroprudential policies should help to maintain resilience of the financial systems. The ECB also warned that it is key for the European Union to bring clarity on new fiscal rules as this is important to reduce uncertainty. The report didn’t bring any new guidance on monetary policy, but markets maybe saw growing risks as a potential reason for the ECB to take a more cautious approach going forward. Whatever the reason, German yields ceded up to 5 bps at the long end of the curve. Bond market momentum slowed after the publication of the US data. Weekly jobless claims again reversed an uptick over the previous weeks returning to 209k from 233k. October durable goods orders (-5.4%) dropped slightly more than expected after a strong September print, but core measures and shipments as expected stabilized. Still US yields reversed part of an earlier decline and currently show intraday changes between +1.5 bps (2-y) and -2.5 bp(30-y). The US 10-y yield is nearing the 4.34% support (38% retracement April-Oct rebound, currently 4.375). US data also temporary blocked the rally in Bunds, but German yields currently trade between 0.5 bps (2-y) and 5 bps (30-y) lower. The German 10-y yield came close to the 2.5% barrier, but a real test was avoided (currently 2.53%), at least for now. After a pause earlier this week, European equities resume their rebound (EuroStoxx 50 +0.6%). US indices also open in positive territory (S&P +0,6%). However volumes might decline as US investors look forward to the Thanksgiving Holiday/a Black Friday long weekend. Oil tumbled sharply lower from the $82.5/b area (Brent) to currently trade near $79/b as OPEC+ delayed meetings for this weekend (cf infra).

On FX markets, the dollar rebounded despite a constructive risk sentiment and some easing of geopolitical tensions (short truce in the Israel-Hamas conflict). DXY trades near 104 (from about 103.6). EUR/USD struggles to hold near the 1.09 big figure (1.089). USD/JPY extends yesterday’s turn north trading at 149.3 from 148.40. EUR/GBP is going nowhere, hovering near the 0.87 big figure. UK finance minister Hunt in his Autumn Statement, amongst others, announced an 2ppt cut in the rate of contributions of employees to the National Security system and made incentives for business investment permanent, which the government says can increase investment by £20bn/year. Even so, the 2024 growth outlook was reduced to 0.7% from 1.8% in the OBR march forecast.

News & Views

OPEC+ announced that it will postpone its Joint Ministerial Monitoring Committee (JMMC) from 25 and 26 November to Thursday 30 November. Rumours suggest growing disagreement over Saudi-led production cuts. That was already the case for several African nations at the previous ministerial meeting in June. Russian deputy PM Novak today said that current oil prices are at a fairly good level. Saudi Arabia on the other hand is looking for higher prices to compensate for weaker global demand. OPEC+ members need to be careful not to misread the Saudi reaction function. It’s in their own interest that the Kingdom doesn’t return to full capacity. Brent crude prices faced a big setback today over the growing unease between OPEC+ member with price/barrel dropping by $3 to $79.

Polish consumer confidence improved further from -17.9 to -15.1 and extending the run of consecutive increases to 11 months. The indicator stands at its best level since September 2021. Both the current assessment and 12 months forward looking component improved for financial conditions and for the general economic situation in Poland. October retail sales at constant prices rose by 2.8% Y/Y (from 0.7% in October and vs 1.7% forecast). In the period January-October 2023 sales decreased by 2.6% vs 6% growth in 2022. The Polish zloty holds strong below the previous YTD low at 4.40 broken last week. Current levels around 4.36 were last seen early 2020.

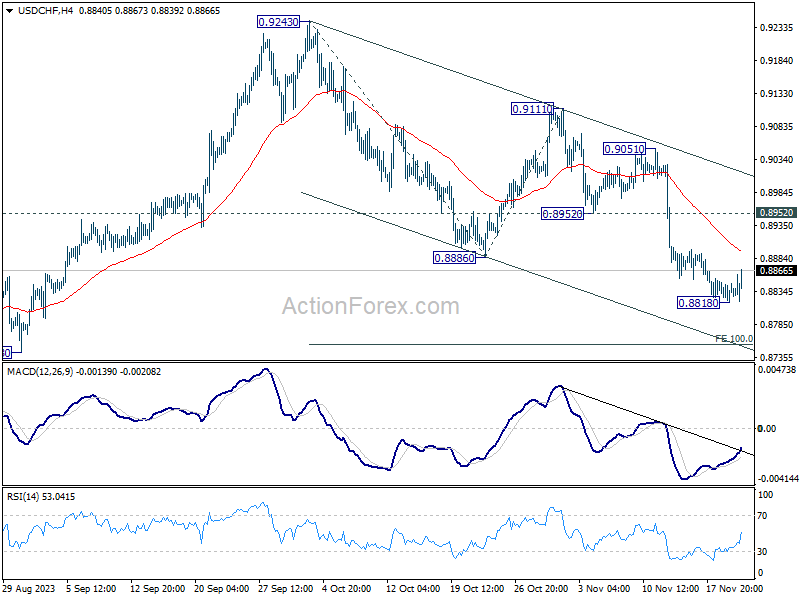

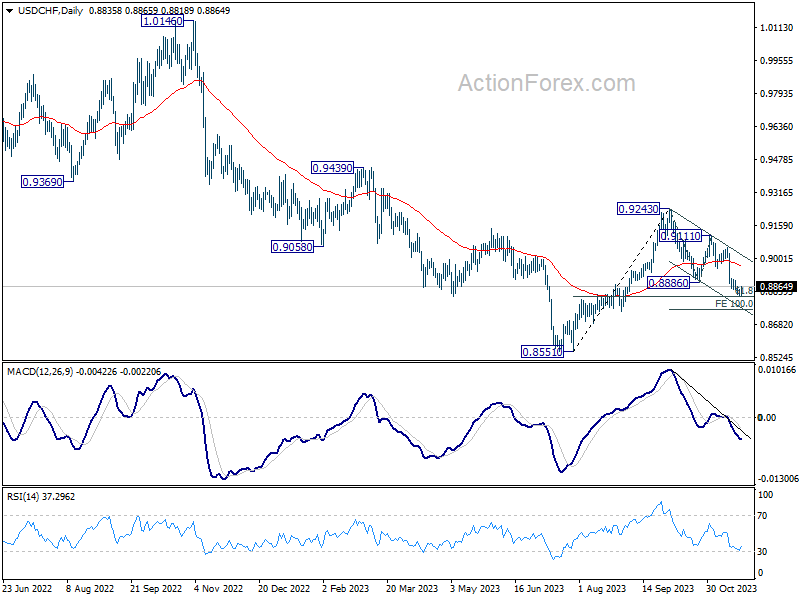

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8821; (P) 0.8836; (R1) 0.8853; More....

A temporary low is formed at 0.8818 with current recovery. Intraday bias in USD/CHF is turned neutral for consolidations. Near term outlook will stay bearish as long as 0.8952 support turned resistance holds. On the downside, below 0.8818 will resume whole decline from 0.9243 to 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754 next.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper fall would be seen to 61.8% retracement of 0.8551 to 0.9243 at 0.8815. Sustained break there will bring retest of 0.8551 low. For now, this will remain the favored case as long as 0.9111 resistance holds.

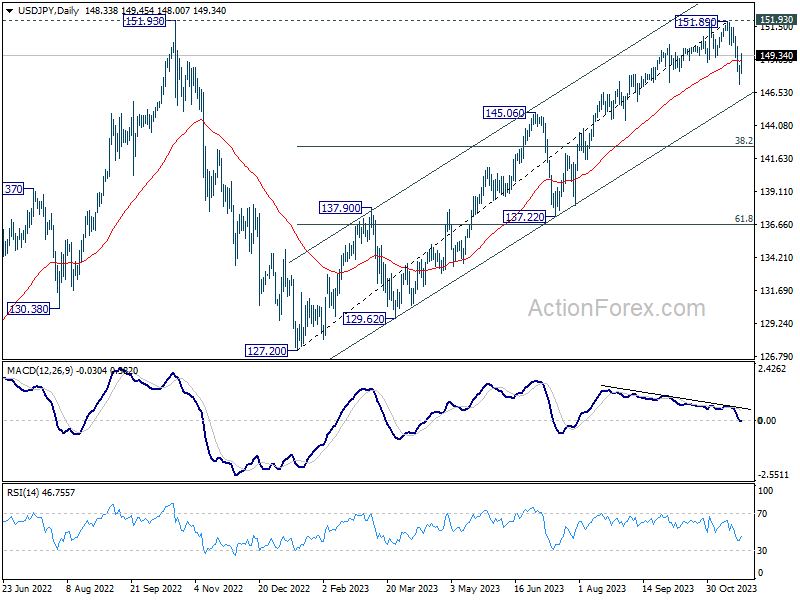

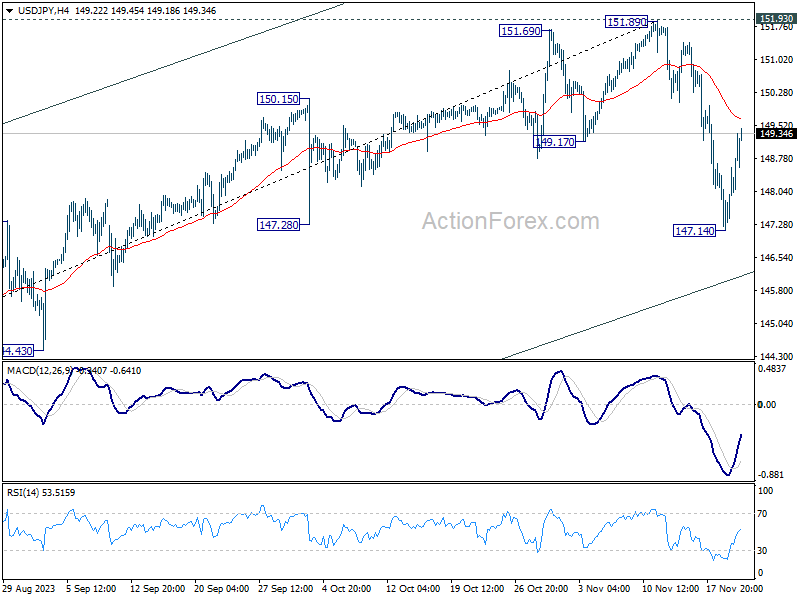

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.51; (P) 148.05; (R1) 148.94; More...

USD/JPY's recovery from 147.14 extends higher, but risk will stay on the downside as long as 55 4H EMA (now at 149.68 holds. Below 147.14 will target medium term channel support at 146.00 next. Nevertheless, sustained break of 55 4H EMA will revive near term bullishness, and target a retest on 151.89/93 resistance zone.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 resistance (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.