Sample Category Title

GBPUSD Hits a 10-week High as BOE Officials Remain Hawkish

The British pound (GBP) rose by 0.26% on Tuesday, reaching a new 2.5-month high as the Bank of England's (BOE) Governor gave some hawkish statements.

Possible effects for traders

During yesterday's Monetary Policy Hearings in the British Parliament, the BOE Governor Andrew Bailey said that the central bank's stance on monetary policy should remain 'restrictive'. Bailey also said it's 'far too early to be thinking about rate cuts.' 'They (the Bank of England) are trying to retain the option to hike again if needed and at a minimum delay markets pre-emptively pricing any easing,' said Simon Harvey, head of FX analysis at Monex Europe. According to Reuters, JP Morgan, a major U.S. investment bank, expects the BOE to start decreasing interest rates only in Q4 2024. Fundamentally, there is a bullish divergence between the U.K. and the U.S. monetary policies, which contributed to GBPUSD's rise by 3.5% in November.

GBPUSD was falling slightly in the Asian and early Europen trading sessions. Today, traders should focus on the U.S. macroeconomic reports: Jobless Claims and Durable Goods orders at 1:30 p.m. may trigger increased volatility. Weaker-than-expected reports may widen the bullish divergence in countries' monetary policies, potentially pushing GBPUSD towards 1.26000. However, higher-than-expected numbers may pull GBPUSD towards 1.24400.

Gold Hovered Near 2,000, But FOMC Minutes Weakened Bullish Momentum

Gold (XAU) price rose by over 1% on Tuesday, breaching the critical 2,000 mark. Still, XAUUSD later declined as the FOMC minutes revealed officials' restrictive monetary policy stance.

Possible effects for traders

The Federal Reserve (Fed) minutes had no hints of imminent interest rate cuts, but officials discussed a cautious approach to additional hikes. According to yesterday's protocols, 'participants noted that further tightening of monetary policy would be appropriate if incoming information indicated that progress toward the Committee's inflation objective was insufficient.' Fundamentally, XAUUSD remains bullish amid rising expectations of potential U.S. interest rate cuts next year following weaker-than-expected economic data. The Fed is expected to maintain its current base rate in the December meeting, but the market sees a 30% chance of a rate cut by March 2024. Indeed, the latest data indicates that the U.S. economy is slowing. In October, existing home sales fell to their lowest point in over 13 years, according to Tuesday's report. Meanwhile, the physical demand for gold seems strong. Swiss gold exports reached their highest point since May, driven by a rise in exports to India during its festive season.

XAUUSD was relatively flat during the Asian trading session but rose slightly in the early European trading hours. Today, several events will likely provoke extra volatility in gold. Traders should focus on three events: Jobless Claims and Durable Goods Orders reports at 1:30 p.m. UTC and the Consumer Sentiment Index at 3:00 p.m. UTC. If the numbers reveal a continuing weakening of the U.S. economy, the chance of imminent rate cuts will increase, pushing XAUUSD higher. However, the pair may sharply correct downwards if the figures are better than expected. 'Spot gold may retrace into the $1,972–1,982 range per ounce, as suggested by a rising channel,' said Reuters analyst Wang Tao.

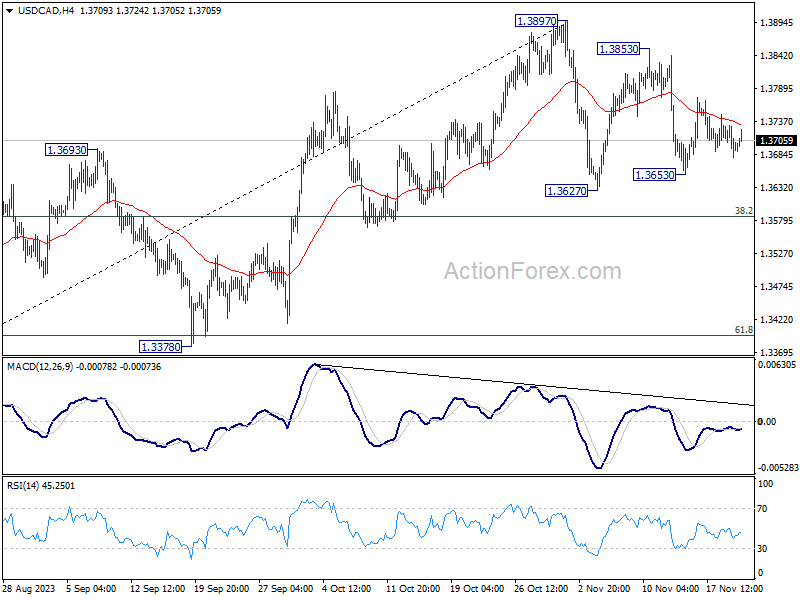

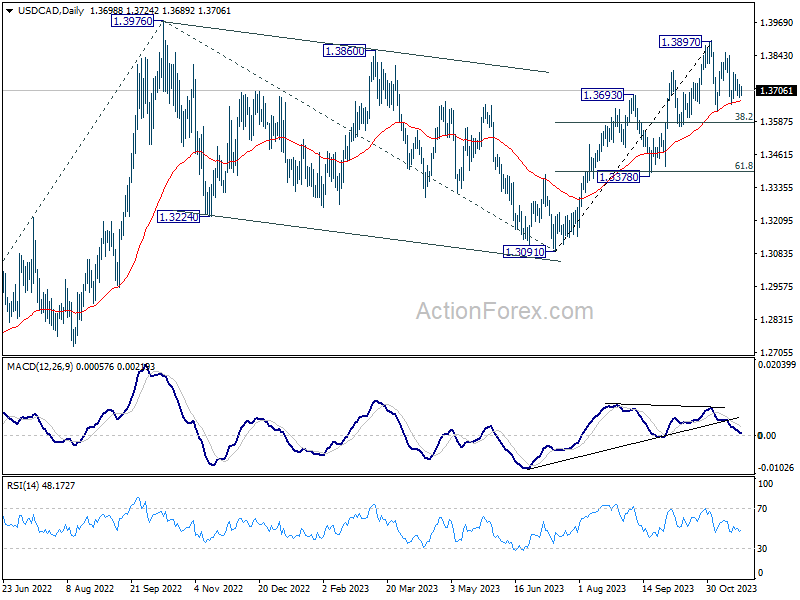

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3678; (P) 1.3705; (R1) 1.3728; More...

Intraday bias in USD/CAD stays neutral for the moment. More sideway trading could be seen. While another fall cannot be ruled out, downside should be contained by 38.2% retracement of 1.3091 to 1.3897 at 1.3589 to bring rebound. Break of 1.3897 is expected at a later stage to resume larger rally.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will remain the favored case as long as 1.3378 support holds.

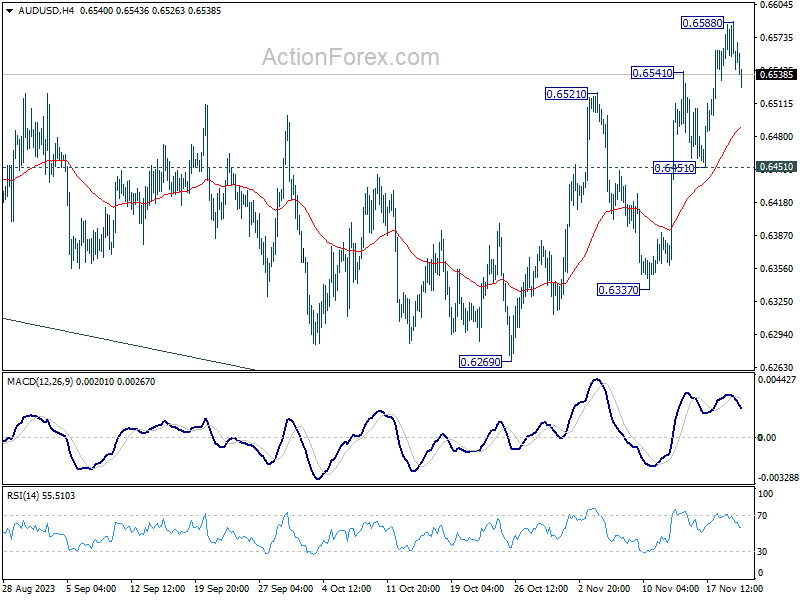

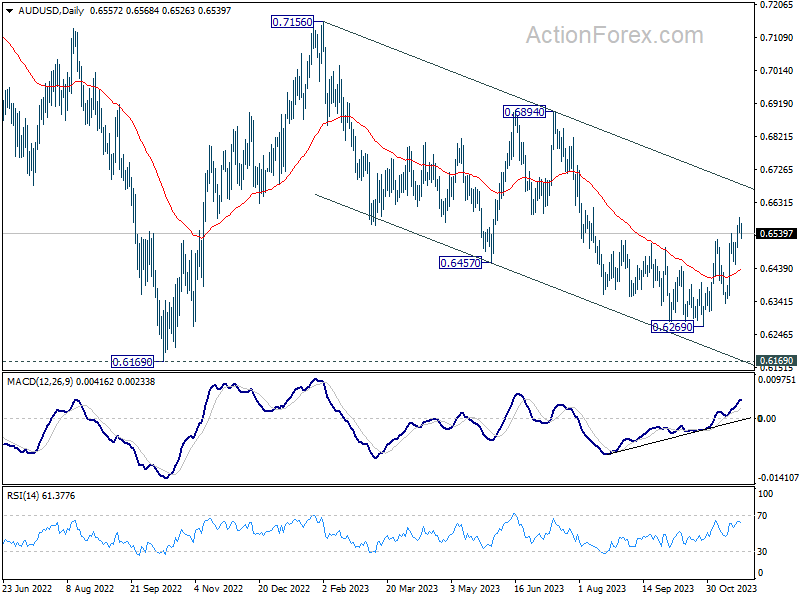

AUD/USD Daily Report

Daily Pivots: (S1) 0.6537; (P) 0.6564; (R1) 0.6582; More...

A temporary top should be in place at 0.6588 in AUD/USD with current retreat. Intraday bias is turned neutral for consolidations. Downside should be contained above 0.6451 support to bring another rally. On the upside, above 0.6588 will resume the rebound from 0.6269 to falling channel resistance (now at 0.6676) next.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of the corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

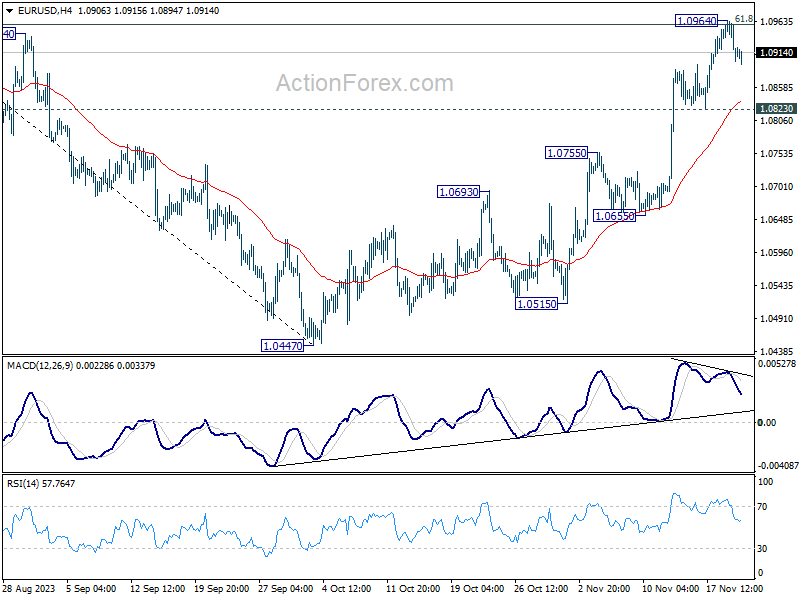

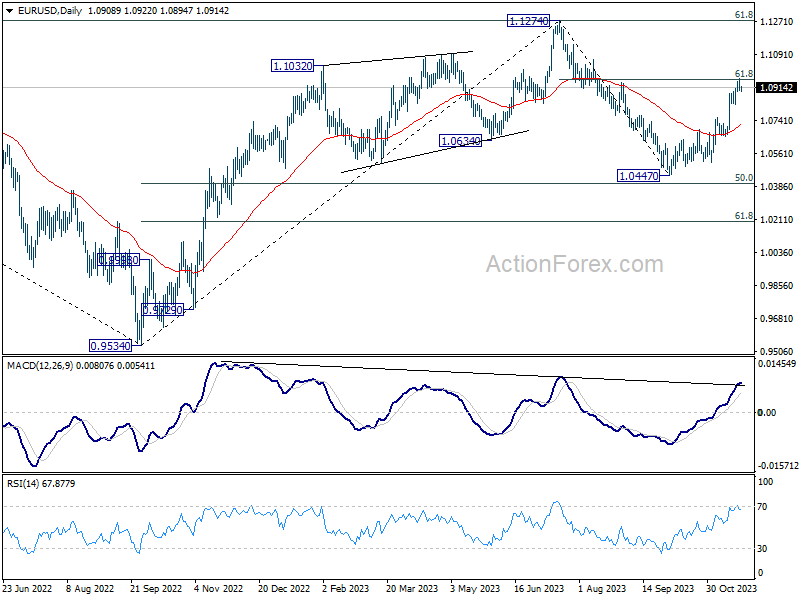

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0885; (P) 1.0926; (R1) 1.0951; More...

A temporary top was formed at 1.0964 in EUR/USD after hitting 61.8% retracement of 1.1274 to 1.0447 at 1.0958. Intraday bias is turned neutral for some consolidations first. Downside of retreat should be contained by 1.0823 support to bring another rally. On the upside, sustained trading above 1.0958 will pave the way to retest 1.1274 high.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

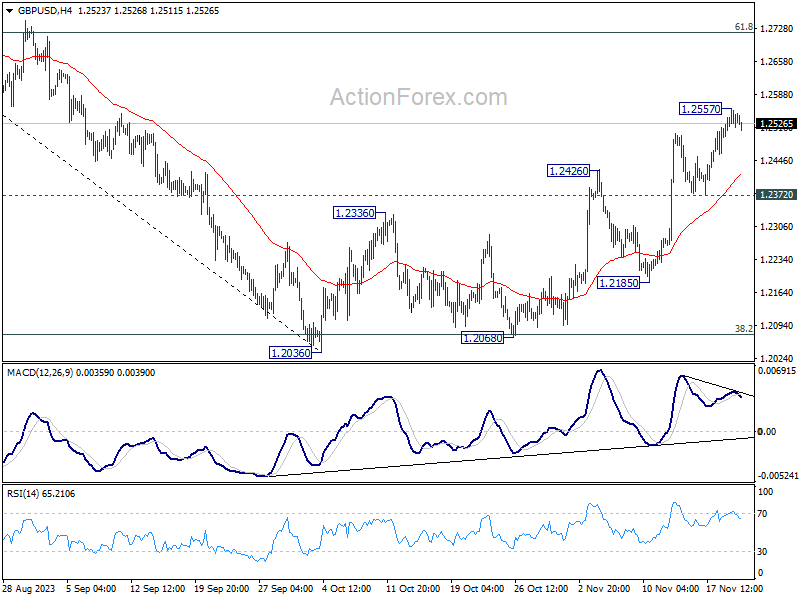

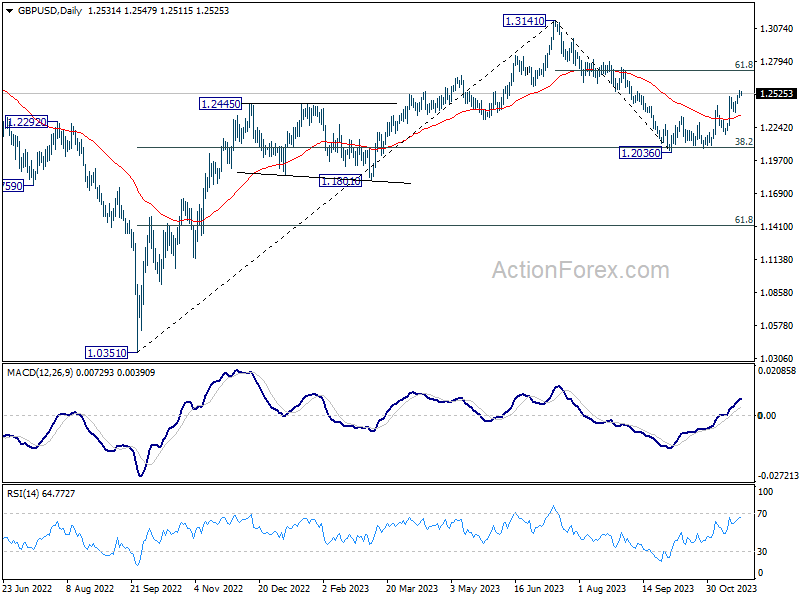

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2505; (P) 1.2532; (R1) 1.2565; More...

A temporary top is in place at 1.2557 in GBP/USD and intraday bias is turned neutral for some consolidations first. But further rally is expected as long as 1.2372 support holds. Above 1.2557 will resume the rise from 1.2036, and target 61.8% retracement of 1.3141 to 1.2036 at 1.2716 next.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 argues that current rise from 1.2036 is the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

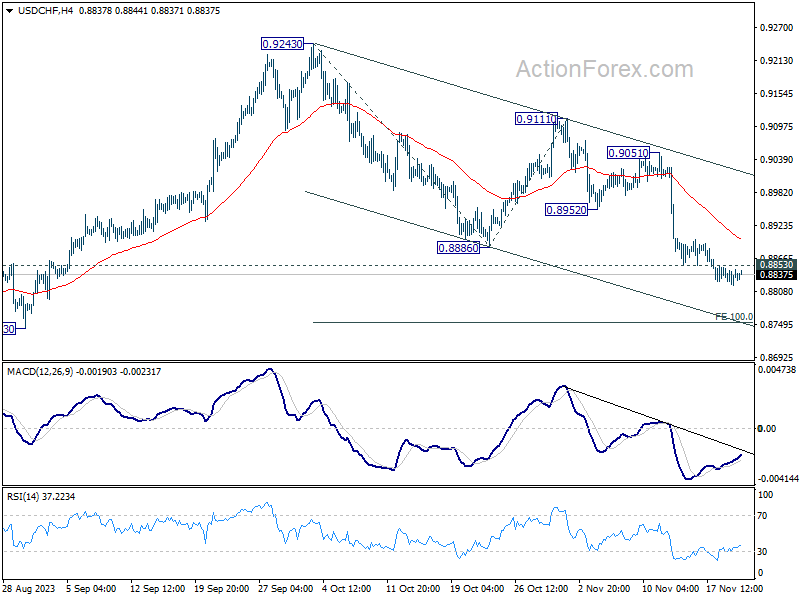

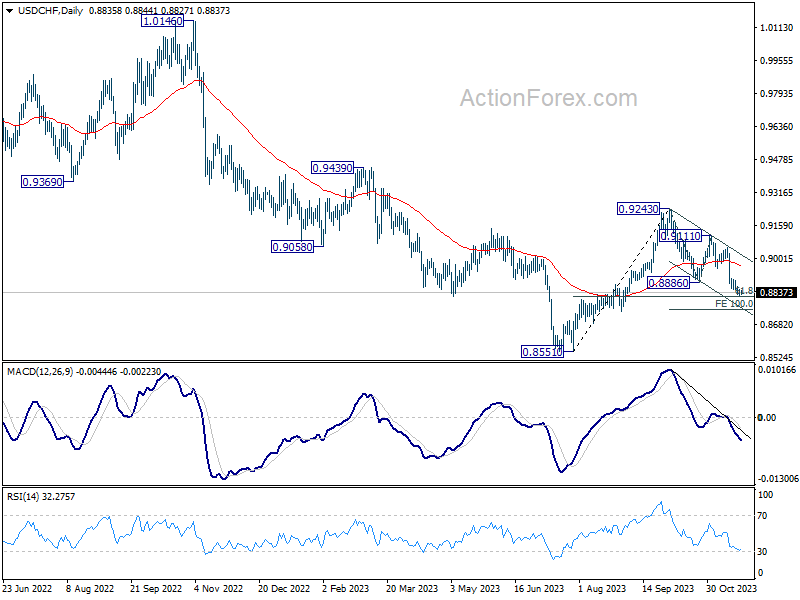

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8821; (P) 0.8836; (R1) 0.8853; More....

While USD/CHF continues to lose downside moment as seen in 4H MACD, there is no clear sign of bottoming yet. Intraday bias stays on the downside. Current fall from 0.9243 should target 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754 next. On the upside, above 0.8893 minor resistance will turn intraday bias neutral and bring consolidations again. But in case of recovery, outlook will stay bearish as long as 0.8952 support turned resistance holds.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper fall would be seen to 61.8% retracement of 0.8551 to 0.9243 at 0.8815. Sustained break there will bring retest of 0.8551 low. For now, this will remain the favored case as long as 0.9111 resistance holds.

AUD/JPY Technical: Holding Above 20-day Moving Average

The AUD/JPY cross pair tends to be used as a proxy for “risk-on/risk-off” behaviour where a clear uptrend movement can be considered as a persistent “risk-on-herding” behaviour is at play and vice versa.

In the past four weeks, the AUD/JPY has rallied by +445 pips from its 16 October 2023 low of 94.14 to the recent 16 November 2023 high of 98.58 which was in line with the rallies seen in major benchmark stock indices.

This risk-on behaviour has been driven by the anticipation that the US Federal Reserve has reached the peak of its current interest rate hike cycle with a potential terminal rate of 5.25%-5.50% on the Fed funds rate.

98.40 long-term secular resistance remains a key hurdle for the bulls

Fig 1: AUD/JPY major trend as of 22 Nov 2023 (Source: TradingView, click to enlarge chart)

The recent push-up in price actions also saw a fourth retest on its long-term secular descending range in place since the October 2007 major swing high now acting as resistance at 98.40.

Only a clear weekly close above 98.40 may trigger a major bullish breakout where a multi-month uptrend phase may occur with the next major resistance coming in at 104.50 (upper boundary of a major ascending channel from August 2021 low, major swing highs of July 2008/April 2013 & 1.00 Fibonacci extension from March 2020 low).

Short-term downside momentum has started to dissipate

In the past week, the AUD/JPY has started to retrace its recent gains with a decline of -175 pips from its 16 November 2023 high of 98.58 to print a recent low of 96.83 yesterday, 21 November.

Interestingly, yesterday’s price action has formed a daily bullish reversal “Dragonfly Doji” candlestick, a whisker above the 20-day moving average.

In addition, the hourly RSI momentum indicator has staged a bullish breakout above the 50 level, suggesting a potential revival of short-term bullish momentum.

These observations suggest the prior four days of decline have started to exhibit signs of a potential bullish reversal. Watch the 96.85 key short-term pivotal support (also the 20-day moving average) for a potential retest on the 98.40 key long-term secular resistance.

However, a break below 96.85 negates the bullish tone to expose the next intermediate support zone of 96.10/96.80 (also the 50-day moving average).

We Don’t Expect Big Swings Ahead of US Long Weekend

Markets

ECB Lagarde addressed a German finance ministry event just before yesterday’s European close. While her quote that the ECB is “not done” in its inflation fight drew most (headline) attention, markets focused on – and reacted to – other comments. Mainly that the central bank switched to a phase in the cycle which president Lagarde would characterize as being attentive and focused, allowing some time to see how fast disinflationary forces take effect. Markets interpret the ECB’s first pause since the rate hike cycle started in July 2022 as final, banking on rate cuts as soon as Q2 2024 in a goldilocks soft landing scenario where central banks can eventually shift their focus to supporting growth again from fighting inflation. Anything short of backing more imminent rate hikes is currently interpreted as lower (policy) rates being the next move. German yields closed up to 5 bps lower at the 5-yr tenor yesterday. The single currency faced a setback with EUR/USD closing at 1.0911 from 1.0940 following a failed test of 1.0960 resistance (62% retracement on mid-July to early October decline). EUR/GBP copied the move south in EUR/USD with the pair ending just above 0.87 from 0.8750. Lagarde warned however about the path forward for the two main forces pushing inflation down today. The impact of the unwinding of the energy and supply shocks – accountable for two-thirds of the inflation surge – is fading while there is some uncertainty about the strength of the impact of the current restrictive monetary policy on growth. Therefore, headline inflation is set to rise again slightly in the coming months, mainly owing to base effects (aforementioned energy but also reversal of fiscal support measures). Minutes of the early November Fed meeting showed broad unanimity on decisions taken. The US central bank needs to proceed carefully, watching data in coming months. The release didn’t trigger any market reaction. Daily changes on the US yield curve ranged between -2.3 bps and -4 bps yesterday. The rally on European and US equity markets ended with a day of minor losses (-0.5%). Consensus-beating earnings by Nvidia and the Gaza hostage/prisoner swap deal do little to improve risk sentiment this morning. The eco calendar is thin today with only weekly jobless claims and durable goods orders. We don’t expect big swings ahead of the US long weekend (Thanksgiving) suggesting recent corrective tops (bonds/stocks) and bottoms (dollar) to stay out of reach.

News headlines

The Hungarian central bank cut the base rate yesterday by 75 bps to 11.5%. A close advisor to the rate-setting committee last week followed by vice-governor Virag a day later strongly hinted at this to happen. Doing so quashed speculation that the MNB would speed up the cutting pace following disinflation stronger than markets expected. CPI in October stood at 9.9% while core inflation rose by 10.9%, both being in the lower half of the range provided in the MNB September report. The three-month annualized change in core inflation fell below 3%, from 4% in September. Inflation is expected to decrease further all the way to 2.5-3.5% in 2025. The MNB added that a positive real interest rate supports the process, revealing a preference to keep this the case as it further normalizes the tight monetary policy stance. Growth forecasts were left unchanged compared to September with GDP seen expanding at a 3-4% rate in 2024 and 2025. The economy this year is expected in the lower half of the -0.5-0.5% September range. The Hungarian forint lost territory but was no exception in the region. At a close EUR/HUF 381.05, the currency trades close around recent highs though below YtD highs of 370.

The Bank of Japan may say on the record that it does not want to exit its ultra-easy policy stance, its actions increasingly suggest otherwise. Data up to November 21 show that the central bank hasn’t bought any real estate investment trusts (J-REIT) this year. In addition, it has bought exchange-traded funds at only three occasions in 2023 so far. The BoJ has accumulated these risk assets on a large scale since 2010 to complement its easing stance. Both are now growing robustly on themselves, offering a perfect opportunity for the central bank to step back. Also, the BoJ in its updated quarterly plan cut the minimum amounts of bonds it will buy across all maturities. The biggest reductions take place in the 5-10y bucket and maturities over 25 years. This follows actual buying in the previous quarter which was already lower than the pre-announced minima. It triggered a corresponding curve underperformance. Japanese yields this morning rise 3-6 bps in the 10-30y bucket.

When Fantastic Falls Short

The minutes from the Federal Reserve’s (Fed) latest monetary policy meeting showed that the Fed members agreed to ‘proceed carefully’ with their future rate decisions. Carefully doesn’t mean that the Fed is done tightening, it means that it will ‘proceed carefully’ in the light of the economic data and the market conditions to decide whether it should hike, pause, or cut the interest rates. Note that ‘most’ members ‘continued to see upside risks to inflation’.

Alas, the cautious tone in Fed minutes went completely unheard as the latest CPI data acted as a shield against the Fed hawks. As such, the market reaction to the Fed minutes was muted. The US 2-year yield remained little changed near the 4.90% level, the 10-year yield rebounded past 4.40%, and is still around 60bp lower than the October levels. The S&P500, which is now trading in the overbought market, retreated 0.20% and Nasdaq 100 fell 0.60% from an almost 2-year high, as investors didn’t want to do much before seeing the Nvidia’s results.

When fantastic falls short

Nvidia’s Q3 results were strong. The company exceeded the $16bn revenue forecast by $2bn. They earned more than $18bn, made more than $4 profit per share and said that they will be earning around $20bn this quarter. But the latter forecast couldn’t meet the top forecast ($21bn) and the share price fell in the afterhours trading, though by less than 2%; investors couldn’t decide whether they should buy the fact that the company exceeded the sky-high expectations, or they should sell the reality that the chip sales to China will slow this quarter and that would weigh on revenue – although Nvidia stated that the ‘decline will be more than offset by strong growth in other regions’ and that they are working to comply with regulations to sell to China, anyway.

Taking a step back: Nvidia is growing, it is growing fast, it has potential to grow further, but the valuation of the company is also sky-high, its price got multiplied by almost five since October 2022. Its PE ratio stands around 120 versus a PE ratio of around 25 in average for S&P500 companies. And its market capitalization is more than $1 trillion more than Intel’s, which used to be the world’s biggest chipmaker. In summary, the company is growing but that strong growth is already priced in and out. Therefore, we will probably not see a big profit taking post-earnings, we will likely see correction and consolidation instead below the $500 psychological hurdle.

And with that – the Nvidia earnings – out of the way, the S&P500 and Nasdaq futures are slightly in the negative at the time of writing. The market will likely digest the Fed minutes and the Nvidia results in a calm mood before the Thanksgiving holiday.

Hunt in the spotlight

British Chancellor of Exchequer Jeremy Hunt will make his Autumn Statement today and he will do his best to try to please British voters by announcing tax cuts amid slowing inflation, try to make the Tories – who lost a lot of support over the past year-and-so and fell around 20 points behind Labour in the latest polls - look good again, while pursuing a hard-won economic and financial stability after the Liz Truss mini-budget crisis, and keep the country’s finances together to avoid another Truss-style bond meltdown.

Happily, for him, the Gilt yields have been falling along with other major economies’ bond yields since the October peak. The British 10-year yield tested the 4% level to the downside last Friday. Households are happy to see inflation slow, Rishi Sunak is living up – with a bit of luck – to his promise to halve inflation by year-end, and investors think that the Bank of England (BoE) is done hiking the interest rates. The BoE is also expected to start cutting its rates by May next year - to which the BoE Governor Bailey replies saying that if the market conditions loosen too fast, they may have to raise interest rates again. But that’s a detail. Cable advanced to 1.2560 yesterday on the back of a broadly softer US dollar. A too generous Autumn Statement – in terms of pleasing voters – could revive the inflation expectations for the UK hence tame the BoE doves. The latter could trigger a selloff in gilts, push yields higher and help sterling extend its gains against the greenback and pave the way for a further advance to the 1.27 level.

Yet, Cable’s upside potential also depends on the dollar’s downside potential. The US dollar – which came under a decent bearish pressure since the beginning of the month – is near the oversold territory. And the selloff in the dollar could soon bottom out given the Fed’s cautious tone faced with the significant decline in the US long-term bond yields.

Elsewhere the EURUSD sees resistance above a major Fibonacci resistance, near the 1.0955 mark, gold is testing the $2000 per ounce this morning as investors chose safety into the long Thanksgiving holiday in the US while US crude sees resistance at the 200-DMA and Bitcoin is down from recent highs on news that Binance CEO was pleaded guilty as his company prioritized growth over compliance and violated anti-money laundering and unlicensed money transmitting to finance terrorists, cyber criminals and child abusers. The Binance verdict will hardly impact the recent appetite in Bitcoin, which is expected to get a boost thanks to potential spot ETF approvals.