Sample Category Title

Canada retail sales rose 0.6% mom in Sep, well above expectations

Retail sales in Canada rose 0.6% mom to CAD 66.5B in September, much better than expectation of 0.0% mom. Sales were up in four of nine subsectors and were led by increases at motor vehicle and parts dealers.

Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were down -0.3% mom.

In volume terms, retail sales increased 0.3% mom.

Retail sales were up 0.6% in Q3, while in volume terms, retail sales declined 0.5%.

Advance information suggests that sales rose 0.8% mom in October.

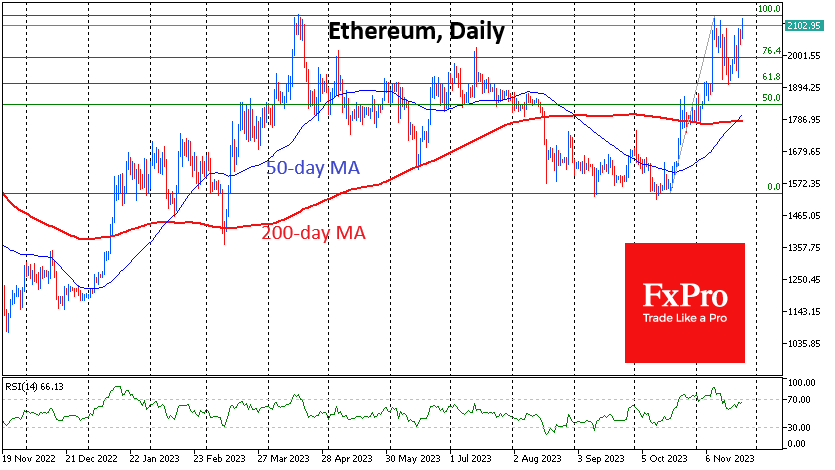

Ethereum Took $2100, Heading Towards $2500

Market picture

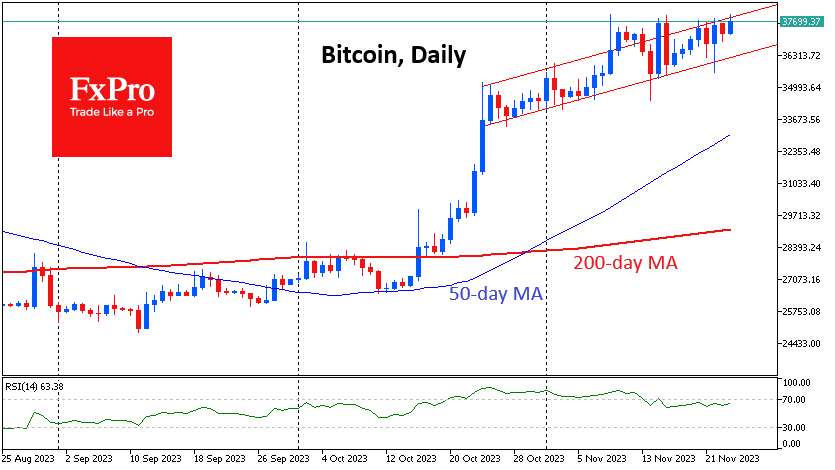

The crypto market continues to move higher, adding another 0.8% overnight to $1.44 trillion as Greed stays as a major driver right now, according to a popular sentiment indicator.

Friday morning saw a fresh test of the $38K level for Bitcoin. It failed, but we continue to see the persistence of growth attempts and less and less deep retreats from local peaks. The dynamics of November lead us to believe that the chances of the price rising by another 2.5K and exceeding the $40K level are higher than the chances of it falling by the same amount to $35K.

Ethereum crossed the $2100 level, returning to the peak set on 10 November. There was a classic Fibonacci retracement with a 61.8% pullback from the initial rally. Breaking through the $2135 level will set up the main scenario of a 161.8% growth, which in this case is close to $2500.

News background

The SEC and BlackRock held a meeting to discuss the details of a spot bitcoin ETF. According to the memo, the management company showed a presentation outlining two possible redemption mechanisms for its iShares Bitcoin Trust.

Grayscale updated the GBTC application to convert to an ETF and changed the ticker symbol to BTC. Bloomberg saw this as another sign of the company’s ongoing negotiations with the SEC.

The SEC has no reason to prevent the launch of a spot bitcoin ETF, said SEC Commissioner Hester Pearce, known for her positive attitude towards cryptocurrencies.

The agreements between Binance and the US authorities are favourable as they neutralise the systemic risk to the industry from a hypothetical collapse of the platform, JPMorgan said.

Nansen said the market’s reaction to the Binance scandal and Changpeng Zhao’s guilty plea was muted. This event did not lead to a significant flight of capital from the cryptocurrency platform.

Germany on the Brink of Recession, UK Consumer Confidence Improving

A quiet end to the week draws to a close with European indices treading water and economic data highlighting the challenges facing the bloc.

Nowhere is that more evident than in Germany which appears to be on the brink of a double-dip recession and facing immense uncertainty over its budget for next year as it scrambles to patch up finances for this one.

A supplementary budget next week alongside a proposal to suspend the debt brake now looks likely but even this is just a temporary solution that won't give investors much confidence in the outlook for an economy already under significant strain.

The economy was confirmed to have contracted by 0.1% in Q3 this morning and as we move into the final month of Q4, it's looking likely data early next year will confirm the country is back in recession.

The Ifo business climate survey was a little better and appears to be turning a corner which is hopefully a good sign but at 87.3, it's still printing figures near historical lows. The early months of the pandemic were understandably much worse, as you'd imagine, but that aside, recent readings have fallen close to 2001 and 2009 levels.

UK consumers buoyed by improving real earnings

UK consumer confidence is also gradually improving, albeit from very weak levels. At -24, the Gfk survey is 25 points from last September's lows but still some way below all surveys from mid-2013 through to the pandemic. Still, the direction of travel is more promising and inflation is now running below wage growth which should continue to support that.

Trading calm going into the weekend after OPEC+ postponed meeting

It could have been a nervy end to the week in oil markets had OPEC+ not pushed back its meeting from this Sunday to next Thursday. Instead, it's all looking a little calm. While I wouldn't be entirely surprised to see leaks or comments over the weekend that still have an impact on the oil price on the open next week, the actual meeting now occurring Thursday could put traders' minds somewhat at ease.

Gold not giving up on $2,000 yet

Gold is continuing to flirt with $2,000 despite repeatedly failing to break and hold above the psychological resistance zone. We saw that on a number of occasions at the end of October and again earlier this week, buoyed on this occasion by a less hawkish Fed and favorable inflation and jobs reports from the US. It will be interesting to see how explosive the move is if the price does break significantly above, with it having taken some effort to break down. A rebound lower on the other hand could set up an interesting battle at the November lows around $1,930.

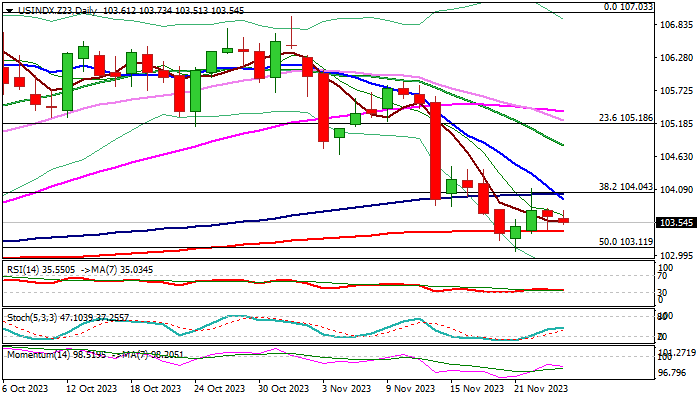

Dollar Index: Consolidation to Likely Precede Fresh Weakness

The dollar index is holding in prolonged sideways mode and ranging between 200DMA (103.39) and 100DMA (104.02) in a holiday-thinned markets.

The bear-leg from a double top at 106.98/107.03) is taking a breather after 1.9% drop previous week, but bears hold grip and warn of fresh weakness after consolidation.

Strong negative momentum and multiple MA bear-crosses on daily chart weigh on near-term action, with additional pressure on dollar expected from shift in Fed’s view on interest rates, as narrative changed from signals for further tightening to rate cuts in just a couple of weeks.

Also, the greenback is likely to be sold more towards the end of the year, as investors may further clear larger longs from the second half of 2023.

Break of 200DMA to generate initial bearish signal, which will look for verification on clear break of 103.11 pivot (50% retracement of 99.20/107.03 uptrend) and signal bearish continuation.

Caution on bounce above 100DMA (104.02) which would sideline immediate downside risk and challenge upper pivot at 104.33 (base of thick daily cloud, reinforced by daily Tenkan-sen).

Res: 104.02; 104.45; 104.66; 105.18.

Sup: 103.39; 103.11; 102.84; 102.19.

Japanese Yen Shrugs as Core CPI Ticks Higher

- Japanese core inflation rises

- US PMIs expected to show little change

The Japanese yen is unchanged on Friday, trading at 149.57.

Japan’s core inflation rises to 2.9%

Japan’s core CPI rose slightly in October to 2.9% y/y, up from 2.8% in September and just below the consensus estimate of 3.0%. The core CPI print excludes fresh food but includes energy. Core CPI has now exceeded the Bank of Japan’s 2% target for 19 consecutive months. Headline inflation jumped to 3.3% y/y, up from 3.0% in September and above the market consensus of 3.2%.

The acceleration in inflation will put further pressure on the BoJ to tighten its ultra-loose policy. There is growing speculation that the BoJ could raise interest rates from -0.1% to zero early in 2024. The BoJ is known to be very tight-lipped and there’s little chance of any communication with the markets with regard to a shift in policy.

What is clear is that any move away from the current policy could cause market turmoil and hurt Japan’s fragile economy. Still, with inflation remaining stubbornly high, a shift in monetary policy is likely only a question of time. The Bank of Japan meets next on December 19th. Once dull affairs that barely made the radar of investors, the meetings are now closely watched on expectations that the BoJ could change policy, which would be a sea-change after years of ultra-loose policy.

The US wraps up the week with the release of manufacturing and services PMIs, with little change expected. Still, the markets will be watching carefully, as the data will provide insights into the strength of the US economy.

The consensus estimates for November stand at 49.8 for manufacturing (Oct: 50.0) and 50.4 for services (Oct. 49.8). The manufacturing sector has been particularly weak, with the PMI indicating declines over most of the past year. If either PMI misses expectations, the US dollar could show stronger movement.

USD/JPY Technical

- 149.29 and 148.54 are providing support

- There is resistance at 150.22 and 151.25

ECB’s Lagarde: We can now observe very attentively

ECB President Christine Lagarde, said at Bundesbank event today that the central bank has "already done a lot" in fighting inflation, referring to the series of rate hikes. Now, given the "amount of ammunition" being deployed, ECB is positioned to "observe very attentively".

With observations on how tightening have impacted people's economic life, ECB can decide, "how long we have to stay there and what decision we have to make — up or down, she added.

However, despite these efforts, Lagarde emphasized that "the battle is not over and we're certainly not declaring victory."

Is Gold Forming a Double Top Pattern?

- Gold gets rejected a tad below its recent 5-month peak

- A failure to claim that level could validate a double top structure

- While momentum indicators remain tilted to the upside

Gold had been in a steep uptrend since November 10, when the price bounced off the crucial 200-day simple moving average (SMA). The latest rally seems to be faltering though after bullion failed to surpass its five-month high of 2,009, but the short-term oscillators suggest that buyers have not given up yet.

Should the bulls attempt to push the price higher, the recent five-month peak of 2,009 could be the first barrier for them to conquer. A break above that territory could bring the April resistance of 2,032 under examination. Surpassing that region, bullion could then challenge the April-May resistance zone of 2,049.

On the flipside, bearish actions could send the price lower towards the July resistance of 1,987, which could serve as support in the future. Further declines might then cease at the October support of 1,954. Failing to halt there, gold could challenge its November bottom of 1,932.

In brief, gold’s failure to post a fresh higher high after testing its previous five-month peak is increasing the odds of a double top pattern. Should that scenario materialize, it could be the beginning of a downside correction.

Germany 30 Technical: Bullish Momentum Remains Intact

- Key elements remain positive that support the ongoing short-term uptrend phase.

- Watch the key short-term support at 15,930.

- Next intermediate resistance stands at 16,200.

Since its bullish breakout from its former medium-term descending channel resistance last Tuesday, 14 November, the price actions of the Germany 30 Index (a proxy for the DAX futures) have continued to exhibit positive elements.

Oscillating within a short-term uptrend phase since end of October 2023

Firstly, it has continued to oscillate within the upper half of a minor ascending channel in place since the 27 October 2023 low of 14,586.

Secondly, the hourly RSI momentum indicator managed to stage a rebound from key parrel support at the 45 level without any prior bearish divergence condition at its overbought condition which suggests that short-term bullish momentum remains intact.

Watch the 15,930 key short-term pivotal support (the median line of the minor ascending channel & minor congestion area of 21/23 November 2023 and a clearance above 16,050 near-term resistance sees the next intermediate resistance coming in at 16,200 (upper boundary of the minor ascending channel & Fibonacci extension cluster.

On the flip side, failure to hold at 15,930 negates the bullish tone for a minor corrective decline towards the next intermediate support zone of 15,660/560 (also the 200 and 20-day moving averages).

Fig 1: Germany 30 minor short-term trend as of 24 Nov 2023 (Source: TradingView, click to enlarge chart)

EUR/USD Steady as German GDP Contracts

- German GDP shrinks in Q3

- US to release manufacturing and services PMIs

The euro is almost unchanged on Friday. In the European session, EUR/USD is trading at 1.0903, down 0.03%.

German economy declines

German GDP posted a minor drop in the third quarter, coming in at -0.1% q/q. This was down slightly from -0.1% in the second quarter and matched the market consensus. On an annualized basis, GDP declined by 0.4%, down from a revised o.1% gain in Q2 and missing the market consensus of -0.3%. The consumer spending component of GDP decelerated in the third quarter and was a key driver of the decline in GDP. German consumers remain in a sour mood and are being squeezed by rising interest rates and a high inflation rate of 3.8%.

The German business sector is also pessimistic about economic conditions. The Ifo Business Climate index managed to climb to 87.3 in November, up from 86.9 in October but below the market consensus of 87.5. A reading below 100 indicates that a majority of the companies surveyed expect business conditions to deteriorate in the next six months. Earlier this week, German services and manufacturing PMIs pointed came in below 50, which points to contraction. The manufacturing sector is particularly weak and has been in decline since June 2022.

It has been a relatively light week for US releases, with markets back in action after the Thanksgiving holiday. Later today, the US releases manufacturing and services PMIs, with little change expected. Still, the markets will be watching carefully, as the data will provide insights into the strength of the US economy. The consensus estimates for November are 49.8 for manufacturing (Oct: 50.0) and 50.4 for services (Oct. 49.8). If the readings diverge significantly from the estimates, we could see some strong movement from the US dollar before the weekend.

EUR/USD Technical

- There is resistance at 1.0943 and 1.0997

- 1.0831 and 1.0748 are providing support

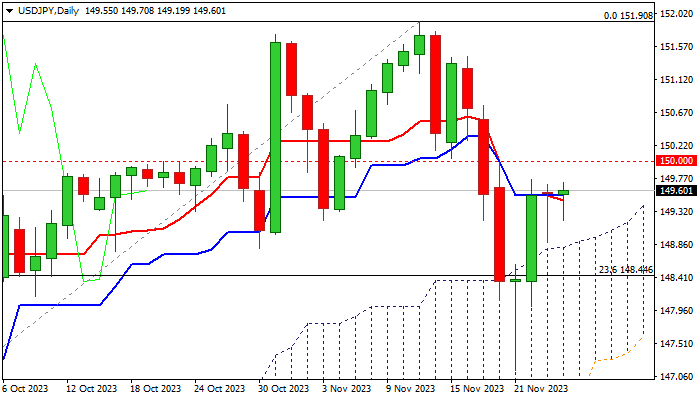

USD/JPY: Recovery Turns Sideways Between Daily Cloud Top and Psychological 150 Barrier

USDJPY is holding within a narrow consolidation for the second consecutive, with quiet mode seen as a result of lower volumes on closure of US markets for Thanksgiving Day holiday.

Recent recovery from 147.15 (Nov 21 low of correction from 151.90 peak) seems to be losing traction, despite formation of reversal pattern on daily chart and the action still being underpinned by thick ascending daily Ichimoku cloud.

Weakening studies on daily chart as14-d momentum returned to negative territory, with 10/20 and 10/30DMA bear-cross adding to initial warning of recovery stall under 150 barrier.

However, fresh signals require confirmation on penetration into daily cloud (cloud top lays at 148.90) and violation of Fibo support at 148.44 (23.6% retracement of 137.23/151.90 rally), to open way for attack at 147.15 (Nov 21 spike low) and expose pivotal supports at 146.73/30 (100DMA / Fibo 38.2%).

Fundamentals also contribute to such scenario, as narrowing rate gap between the Fed and BOJ and quick change in Fed’s rate outlook from further hikes towards rate cuts, may prompt traders to exit dollar longs and increase pressure on greenback.

Res: 150.00; 150.23; 151.00; 151.43.

Sup: 148.90; 148.44; 148.01; 147.15.