Sample Category Title

Will RBNZ Pour Cold Water on Rate Cut Expectations?

- Since the last RBNZ meeting, data have been coming on the weak side

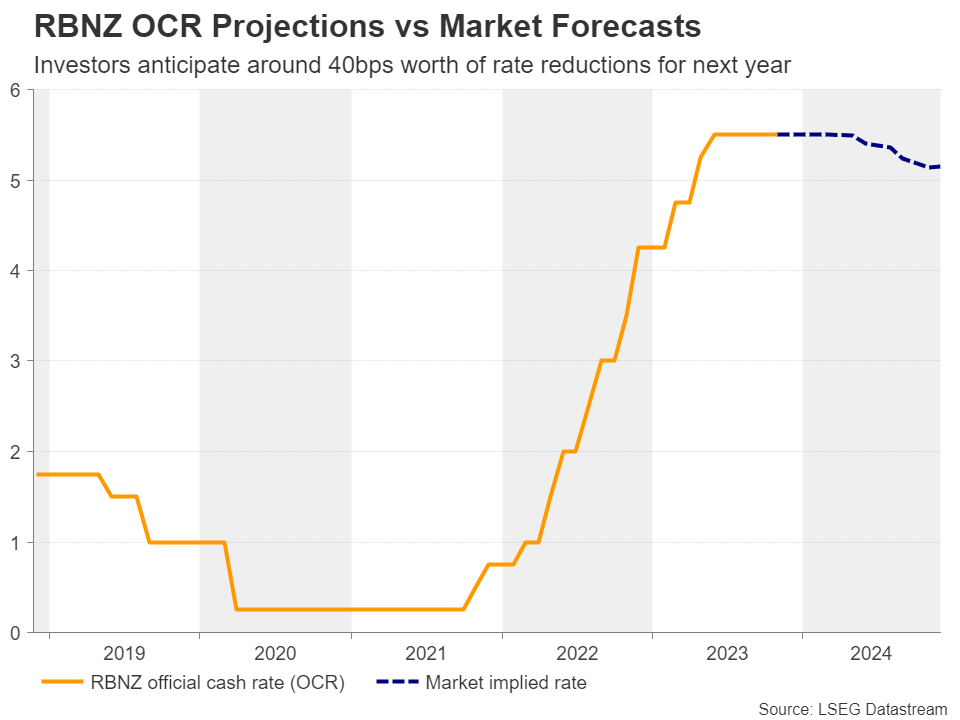

- Investors see no more hikes and expect 40bps worth of cuts for 2024

- But the RBNZ is unlikely to satisfy market bets

- The meeting is scheduled for Wednesday, at 01:00 GMT

Data points to softening economic activity

At its latest gathering, the Reserve Bank of New Zealand (RBNZ) held its Official Cash Rate (OCR) steady at 5.5%, noting that interest rates are constraining economic activity and are reducing inflationary pressures as required. Officials also added that there is a near-term risk that activity and inflation do not slow as much as needed, and that’s why the policy rates should stay at restrictive levels for a sustained period of time.

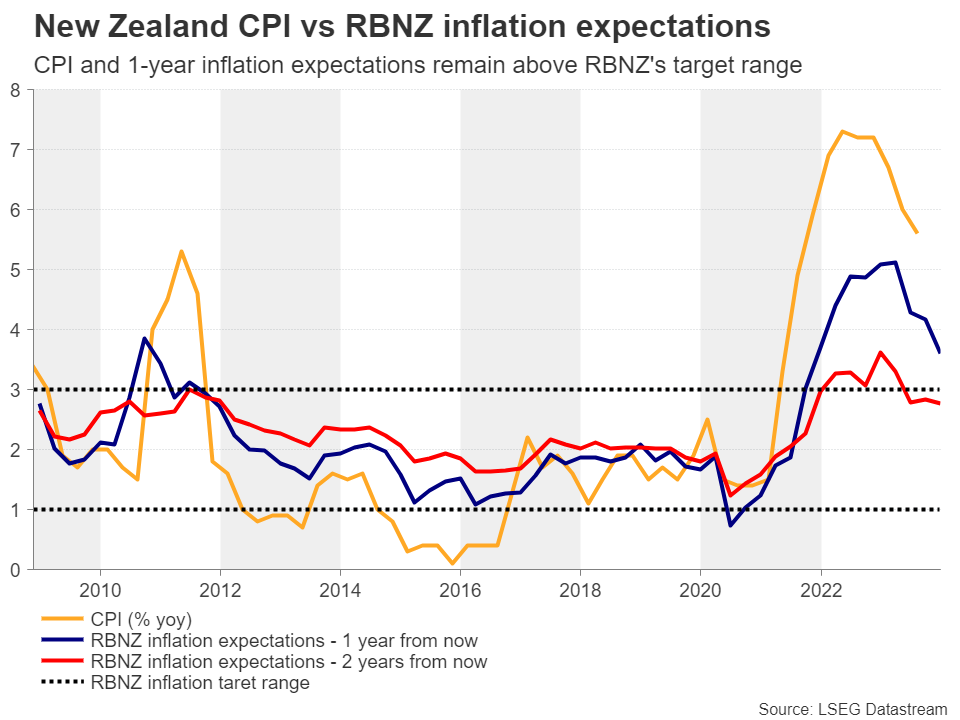

Since then, data have been pointing to further softening of economic activity, with retail sales shrinking 0.8% q/q in Q3 after dropping 1.0% in Q2, and the business PMI for October sliding to 42.5 from 45.3. What’s more, the unemployment rate increased further to 3.9% from 3.6% during Q3 and the CPI slowed to 5.6% y/y from 6.0%. All these numbers allowed investors to continue believing that this tightening crusade is over and to pencil in around 40bps worth of rate cuts for next year.

But upside risks to inflation unlikely to result in a dovish RBNZ

The Bank’s upcoming gathering is scheduled for Wednesday, with analysts agreeing with the market that officials are most likely to keep their hands off the hike button. Therefore, the attention is likely to fall on the Bank’s new macroeconomic projections and any clues on how they are planning to proceed with monetary policy in 2024.

Given that inflation is still nearly double the upper bound of the RBNZ’s 1-3% target range, and that, although cooling, the RBNZ’s own expectations continue to suggest that inflation will stay above that bound in 12 months, officials are unlikely to affirm market expectations and revise lower their OCR projections.

What’s more, it will be interesting to see whether policymakers will incorporate into their forecasts the implications of a new government for the macroeconomic outlook. An official agreement has yet to be signed, but the new coalition is more likely to be led by the National Party, which promised less spending than the previous Labor-led government, but also tax cuts, which is an inflationary policy. It also called for a change in how the RBNZ conducts policy, arguing that the dual mandate should be dropped and suggesting the adoption of a stricter inflation targeting. This means that if the Bank switches to a 2% objective like other major central banks, policy may need to stay restrictive for longer than previously estimated to achieve that target. According to the RBNZ’s inflation projections, inflation would not be at 2% even in 2 years.

Kiwi may have room to gain more

Having all these variables in mind, even if officials lower their short-term inflation projections based on the latest data releases, the longer-term outlook is unlikely to be changed much, and they will most likely continue to suggest that interest rates will finish 2024 at the current 5.5% level. Compared to the market’s own implied path, this could be interpreted as a relatively hawkish hold and could prove positive for the New Zealand dollar, which has been outperforming its US counterpart lately on speculation that the Fed may need to cut interest rates by around 90bps next year.

Apart from monetary policy, the kiwi is also driven by the broader risk-appetite and developments surrounding the Chinese economy, New Zealand’s main trading partner. The market expectations regarding the Fed’s future course of action have triggered a wave of market euphoria, fueling the latest rally in stocks, and that’s why the risk-linked kiwi and aussie gained more than other currencies against the dollar. On top of that, despite the major problems facing the Chinese economy, the latest data releases are suggesting that the world’s second largest economy may be bottoming out, which is another plus for the kiwi and its neighboring aussie.

From a technical standpoint, kiwi/dollar has been printing higher lows and higher highs since the October 26 bottom, while today, it poked its nose above the crossroads of the 200-day exponential moving average (EMA) and the 0.6060 key zone. If the week closes above that hurdle, then the bulls may decide to climb towards the 0.6130 barrier, marked by the high of August 4, the break of which could carry larger bullish implications.

For the outlook to darken again, kiwi/dollar may need to slide and close below the 0.5940 barrier, a move that could pave the way towards the next support zone, at around 0.5860.

Week Ahead – All Eyes on OPEC+ Meeting, US and Eurozone Inflation to Dominate Too

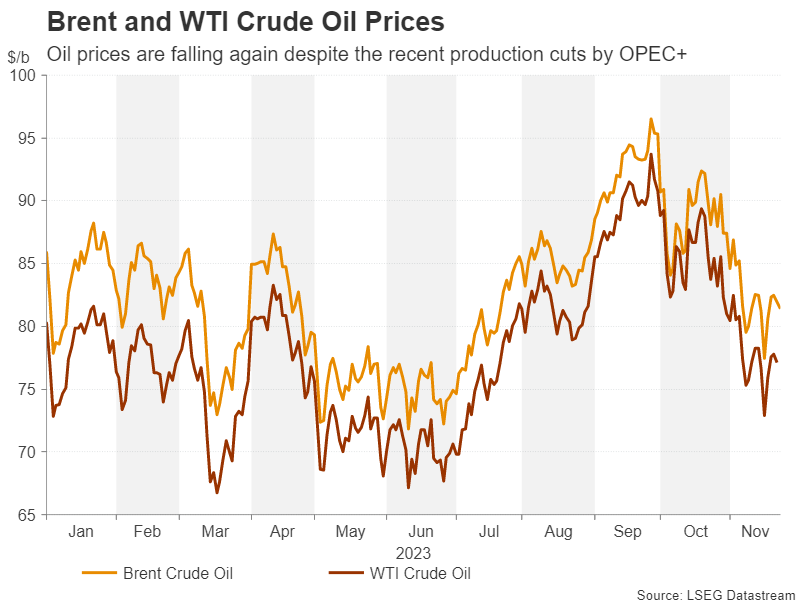

- Oil’s fortunes hinge on OPEC+ meeting outcome on Thursday

- Eurozone flash inflation and US core PCE also due on Thursday

- RBNZ to likely hold rates on Wednesday

- Loonie faces GDP and employment tests in addition to OPEC+ decision

Will OPEC+ agree to production cuts?

Amid weakening growth prospects for the major economies in 2024, expectations that the big oil producers will soon announce further production cuts had been the only thing keeping a floor under the price of oil lately. But that floor broke when OPEC unexpectedly announced that the meeting scheduled for Sunday, November 26, has been postponed to the following Thursday.

Investors have interpreted this as a sign that there are growing differences within the alliance about whether or not additional production cuts are necessary. The likely scenario is that Saudi Arabia, who is the keenest to prevent prices from spiralling further downwards, will find a way to negotiate some kind of a compromise.

The only problem is that even if that turns out to be the case and OPEC+ delivers a package aimed at tightening supply over the coming months, the reductions will almost certainly not be as deep as Saudi Arabia had originally hoped. Furthermore, any new cuts beyond those possibly to be announced on Thursday will now probably be off the table.

When also considering the rising output by countries outside of OPEC+, particularly the United States, it’s hard to see a positive outcome for oil prices. Even if there is a rebound, it will likely be a corrective one rather than an actual trend reversal.

Deflation risks if oil slips below $80

There are implications too for the major currencies if OPEC+ fails to come up with substantial cuts. Elevated oil prices have been the main reason why central banks such as the Bank of England and European Central Bank have had to be so hawkish, and why even the Bank of Japan is now contemplating exiting negative rates.

But this is true to a much lesser extent for the Federal Reserve, as excess demand has been as much if not more of a problem for the US economy in the fight against high inflation.

Therefore, should oil prices drop and stay below $80 a barrel, sticky inflation would become much less of a threat for the ECB, BoE and BoJ than for the Fed, and monetary policy divergence could switch back in favour of the US dollar.

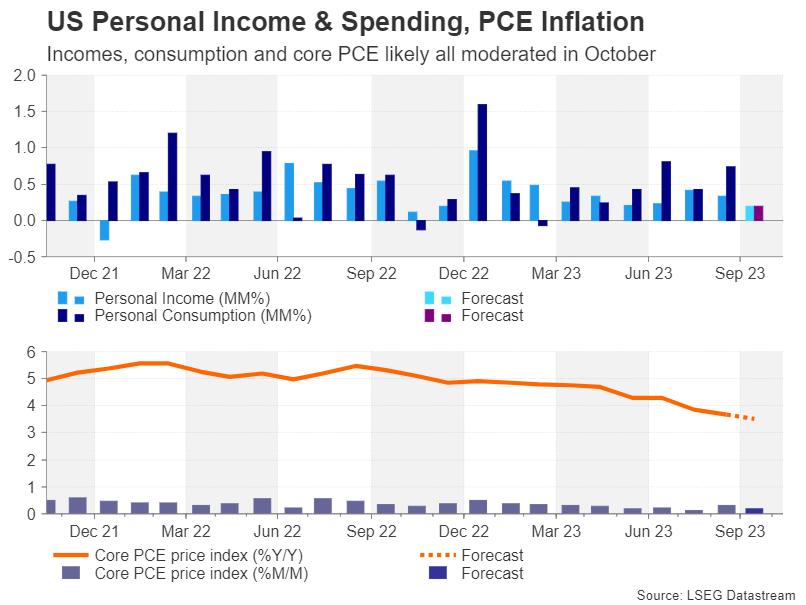

Core PCE to headline packed US calendar

Looking at next week’s agenda for the US, there may be some good and bad news for the greenback. The housing market will be in focus at the start of the week, with October new home sales out on Monday and the Case-Shiller 20-city home price index on Tuesday. Pending home sales will follow on Thursday.

On Wednesday, the third quarter GDP estimate is expected to be revised up slightly from 4.9% to a 5.0% annualized pace, while on Friday, the ISM manufacturing PMI will be important. The ISM manufacturing PMI has been in contractionary territory for the past year and although it is forecast to have edged up in November, it’s expected to remain below 50 at 47.7.

The real highlight, however, will be Thursday’s set of data, containing personal income and spending, as well as the core PCE price index. Both personal income and consumption are expected to have moderated in October, rising by just 0.2% m/m, suggesting that consumers started to tighten their belts at the start of the new quarter after going on a spending spree during the summer.

The all-important core PCE inflation gauge is projected to have slowed too, with forecasts pointing to a drop in the annual rate from 3.7% to 3.5% in October.

Assuming that there are no big surprises, the incoming data should support the view that inflation and the economy overall are cooling off. Markets are likely to take this as a sign that the Fed will have to begin cutting rates by the middle of 2024 if monetary policy isn’t to become too restrictive.

From the Fed’s perspective, however, there’s still some way to go before the 2% target is met and policymakers may attempt to steer investors in the right direction when a host of them hit the podium next week, including Chair Powell, who is scheduled to speak on Friday.

Hence, there are both upside and downside risks for the US dollar over the next seven days.

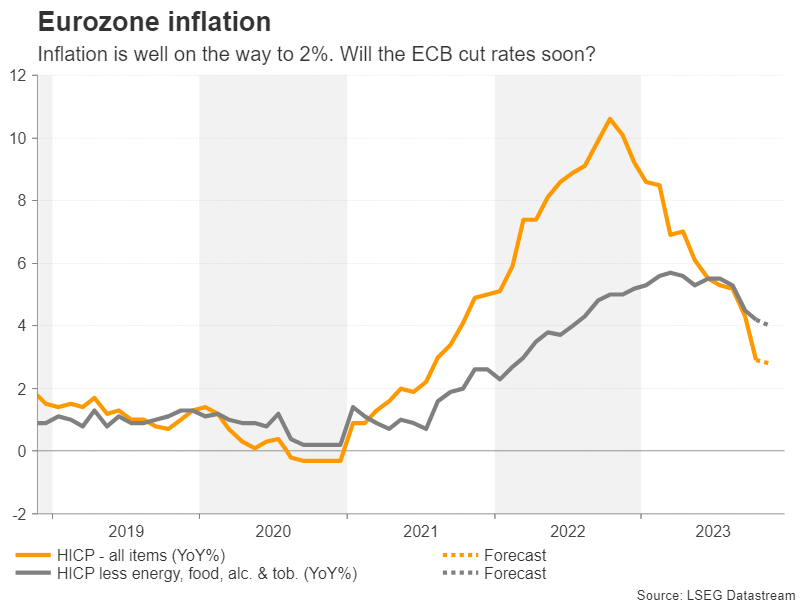

Further easing in inflation could pressure the euro

For the euro, on the other hand, its latest uptrend could come under scrutiny from the Eurozone’s flash inflation readings due on Thursday. The Harmonised Index of Consumer Prices (HICP) is forecast to inch lower slightly in November from 2.9% to 2.8% - the lowest in more than two years. The core measure that strips out all volatile items is expected at 4.0% versus 4.2% in October.

With the Eurozone economy likely to have entered a technical recession in the fourth quarter and fears of a fresh energy crisis not materializing, some traders are betting that the ECB will cut rates before the Fed does next year. This raises question marks about whether the euro’s recovery can stretch beyond the critical $1.10 region.

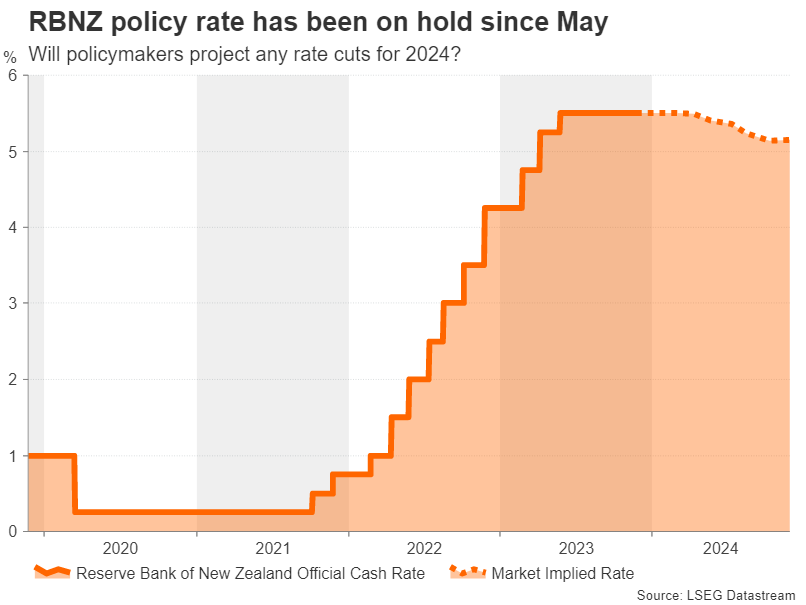

RBNZ could confirm end of rate hikes

The Reserve Bank of New Zealand meets on Wednesday and is widely anticipated to hold the official cash rate at 5.5%, having last raised it in May. Although inflation in New Zealand remains one of the highest among the advanced economies, it is falling and more importantly, tighter monetary policy is working in slowing the economy.

Unemployment is creeping higher, while consumption has been sluggish lately. This somewhat contradicts with the sharp pickup in business confidence over the past few months, although this may be linked more to the improving economic conditions in China and the increased hopes of a soft landing in the US than to the current domestic picture.

Nevertheless, policymakers will probably judge that no further tightening is needed, which then shifts the attention on how long rates will stay at current levels. The RBNZ will publish its updated quarterly projections on Wednesday and so much of the reaction in the New Zealand dollar will depend on whether there are any changes to the rate path.

Back in August, the RBNZ had predicted that rates will stay higher for longer, only being cut slightly towards the end of 2024. The kiwi could extend its rebound against the US dollar if the RBNZ no longer expects to cut rates at all in 2024.

Underperforming loonie braces for a bumpy week

The coming week will be quite a crucial one for the Canadian dollar too as Q3 GDP numbers are due on the same day as the OPEC+ decision on Thursday, before the November employment report arrives on Friday.

The loonie has been somewhat of a laggard among the major currencies in November, with its rebound looking the least convincing and the greenback’s broader uptrend from July remaining intact. The slide in oil prices since late September is mostly to blame for this.

But markets pricing in rate cuts for 2024 have also been a drag on the loonie. Only a couple of months ago, investors saw rates holding above 5.0% during the course of next year compared to at least three 25-bps cuts priced in currently.

But markets pricing in rate cuts for 2024 have also been a drag on the loonie. Only a couple of months ago, investors saw rates holding above 5.0% during the course of next year compared to at least three 25-bps cuts priced in currently.

Better-than-expected readings in GDP and jobs growth could help the loonie play catch up, but that would only be possible if OPEC+ agrees to extend the production cuts into 2024.

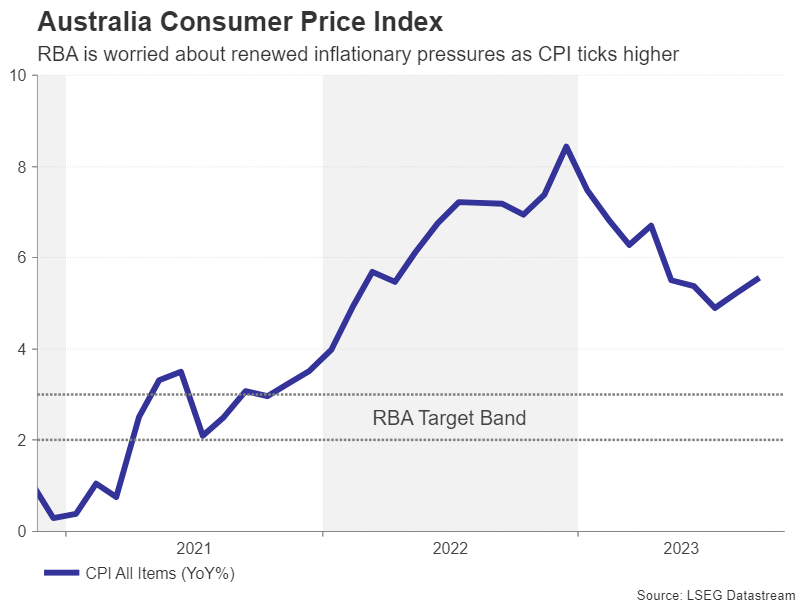

Aussie eyes CPI and Chinese PMI data

Not to be left out, the other of the commodity-linked currencies – the Australian dollar – will also be in the spotlight next week, with traders keeping an eye on both domestic and Chinese indicators. The aussie has enjoyed a strong rally over the past week as the Reserve Bank of Australia’s new chief, Michele Bullock, has continued to strike a hawkish tone amid renewed concerns about inflation, and so the monthly CPI prints out on Wednesday will undoubtedly grab a lot of attention.

Other Australian releases will include quarterly construction output and capital expenditure on Wednesday and Thursday, respectively, as well as retail sales on Tuesday. In addition, manufacturing PMIs out of China will be watched on Thursday and Friday amid ongoing angst among investors about the strength of the recovery in the world’s second largest economy and Australia’s largest trading partner.

Weekly Focus – Soft Landing Hopes Continue to Support Market Sentiment

Market sentiment continues to be supported by hopes of inflation cooling further, even if macro data came out somewhat on the strong side this week. Euro area and UK PMIs edged cautiously higher, albeit from low levels, while output price indices remained above pre-pandemic averages on the key service sectors. US jobless claims fell back after the surprising uptick earlier in November, and euro area Q3 indicator of negotiated wages continued to point towards sticky price pressures stemming from the labour markets.

Bond yields moderated further, providing support for equity markets as well. OPEC's decision to delay a meeting where markets had anticipated possible new production cuts sparked some volatility in the oil markets, but generally oil prices have continued to edge lower, which has also weighed on markets' long-term inflation expectations.

While we have anticipated lower long-end bond yields, and continue to see further downside towards 2024 we also think that much of the decline could already be behind us. The sharp uptick in yields earlier in the fall was largely driven by an increase in term premium, which was likely linked to the high bond issuance and rising concerns of public debt sustainability not least in the US. These concerns have all but faded ever since, which could lead to persistently higher term premium also going forward. In addition, we do not anticipate the markets to price in significantly faster rate cutting cycles for either the ECB or the Fed unless we see further clear signs of weakening in macro data. Read more in our latest Yield Outlook - Too much too soon? 23 November.

On the central bank front, Swedish Riksbank left rates unchanged this week, in line with our expectations. Markets speculated in a possibility for another hike ahead of the meeting, but lower October inflation print, the recent SEK appreciation and lower oil prices have likely eased the need for further tightening. Furthermore, Riksbank still hawkishly signalled that it remains on a tightening bias going forward. The updated rate path shows the policy rate 10bp higher in Q1 2024, and Riksbank also mentioned that it is considering an increase to the QT sales volumes. For now though, we stick to our call that Riksbank is most likely already done with rate hikes, and that its next move will be a rate cut in June 2024. See our Flash comment Riksbank - "Hawkish hold", 23 November.

Next week the focus will once again turn to inflation. We expect euro area November flash HICP to continue easing both in headline (2.7% y/y; Oct 2.9%) and core (3.9% y/y; Oct 4.2%) terms, slightly below consensus forecasts. Some of the negative base effects, which have pushed the headline figure lower over the past months, are now fading and we expect headline inflation to remain close to 3% towards next summer. US October PCE data is also due for release, consensus expects Core PCE inflation to slow down to +0.2% m/m SA, mirroring a similar decline in the CPI measure released earlier.

Markets will also keep an eye out for PMI data from China and the US. The official Chinese NBS PMIs are due for release on Thursday followed by the private Caixin Manufacturing survey on Friday. US ISM Manufacturing Index will round up the week on Friday afternoon. The Reserve Bank of New Zealand is the only G10 central bank having a monetary policy meeting next week, we expect an unchanged rate decision.

Sunset Market Commentary

Markets

After the Thanksgiving Holiday (some) US traders rejoined. For once, they had to catch up with the price dynamics in Europe yesterday. They found bond markets under corrective pressure. A poor EMU PMI causing no further decline in yields was a technical signal to the (potential) the end of the bond rally since end October. Even more important, the German government being forced to again suspend the debt brake procedure highlighted the risk of persistent fiscal deficits that will have to be financed at time a central bankers are withdrawing support. This topic of ‘excess bond supply’ not only applies to Germany or Europe but for sure also to the US. US yields today jumped 4.5 bps (2-y) to 7.0 bps (10-y) going into the release of the US PMI’s. EMU yields initially tried further follow-through gains, but the move stalled. German IFO confidence was in line with the PMI’s. Sentiment among German firms improved slightly from 86.9 to 87.2, the third consecutive gain as businesses turned slightly more positive/less negative both on their current situation as on the expectations. Ifo concludes that the German economy is stabilizing at a low level. The impact of the release was negligible. Comments from ECB Chair Lagarde and colleagues were considered as balanced, maybe even tentatively soft. At a Bundesbank event, the ECB Chair said that the ECB had already done a lot and that it’s now time to attentively observe the impact on the economy. It then can decide how long to stay at current position and on what decision to make next. Higher rates still are not excluded, but this clearly isn’t the most likely scenario the ECB Chair has in mind. ECB vice Chair de Guindos kept a similar balanced approach as he pointed to downside risk to the economic outlook. ECB’s Villeroy was even more outspoken as he said that the ECB won’t raise rates again, ‘excluding surprises’. This assessment of course doesn’t contradict the higher for longer narrative. It also doesn’t mitigate the ‘supply risks’ that might further weigh, especially on the long end of the curve. Still it was enough to block a further rise in yields. German yields are rising 1.5-2.0 bps across the curve. European equities still show marginal gains (EuroStoxx50 + 0.15%). US indices open little changed. Oil is going nowhere near $81.3 p/b looking for the OPEC+ decision on quotas at a virtual meeting next week. US PMI’s released at the time of finishing this report printed mixed. The composite index stabilized at 50.7 as services improved (50.8 from 50.6) while manufacturing dropped back in contraction territory (49.4 from 50.0). Impact on (bond) markets is limited.

Moves in major FX cross rates mostly are technically insignificant. The dollar is modest ground. DXY trades near 103.50 (from 103.75). EUR/USD (1.0925) is holding north of 1.09, but the key 1.0960/65 area remains intact. USD/JPY trades little changed near 149.55. Modest gains of the yen after slightly higher Japanese inflation data this morning couldn’t be sustained. Sterling remains better bid. After yesterday’s better than expected PMI, GfK consumer confidence (-24 from -30) was enough a reason for some further sterling outperformance (EUR/GBP 0.868).

News & Views

Czech consumer confidence fell from 92.7 to 90.7 in November. Consumers postpone making major purchases as they feel their financial situation is worse than 12 months ago and fear that they’ll be even worse off in 12 months’ time. The number of respondents expecting a worsening of the overall situation in the Czech Republic over the next 12 months remained almost unchanged compared to October. Business confidence improved from 92.8 to 93.5, a 3-month high. On a sector level, there are improvements in construction (+6.6), selected services (+1.3) and retail (+0.2) while industrial confidence slightly decreased (-0.3). The Czech koruna tried to escape the upward trend channel in EUR/CZK this week (support line currently kicking in at 24.35), but the move lacked dash.

Belgian business confidence rebounded from a 3-yr low of -16.8 to -15 in November (vs -16.5 expected). On a sector level, sentiment improvement significantly in business-related services (2.3 from -14.2) with trade enthusiasm (-15.5 from -20.1) and moral in building industry (-13.3 from -13.6) also better than in October. Only manufacturing sentiment deteriorated (-19.3 from -17.9). A simultaneously published quarterly business survey on credit conditions (October release) showed general conditions to access bank credit deteriorating from the previous quarter. 41.8% of firms surveyed considered them to be tight (up from 37.3%). The tightening of conditions was reported by firms across all sectors and of all sizes. Earlier this week, Belgian consumer confidence extended its rebound, rising from -5 to -4, the best reading since February 2022.

US PMI composite unchanged at 50.7, another marginal rise in business activity

US PMI Manufacturing fell from 50.0 to 49.4 in November. PMI Services rose from 50.6 to 50.8. PMI Composite was unchanged at 50.7.

Siân Jones, Principal Economist at S&P Global Market Intelligence said:

"The US private sector remained in expansionary territory in November, as firms signalled another marginal rise in business activity. Moreover, demand conditions – largely driven by the service sector – improved as new orders returned to growth for the first time in four months. The upturn was historically subdued, however, amid challenges securing orders as customers remained concerned about global economic uncertainty, muted demand and high interest rates. Business uncertainty was also heightened among US firms, as expectations regarding the year-ahead outlook slipped to the weakest since July.

"Businesses cut employment for the first time in almost three-and-a-half years in response to concerns about the outlook. Job shedding has spread beyond the manufacturing sector, as services firms signalled a renewed drop in staff in November as cost savings were sought.

"On a more positive note, input price inflation softened again, with cost burdens rising at the slowest rate in over three years. The impact of hikes in oil prices appear to be dissipating in the manufacturing sector, where the rate of cost inflation slowed notably. Although ticking up slightly, selling price inflation remained subdued relative to the average over the last three years and was consistent with a rate of increase close to the Fed's 2% target."

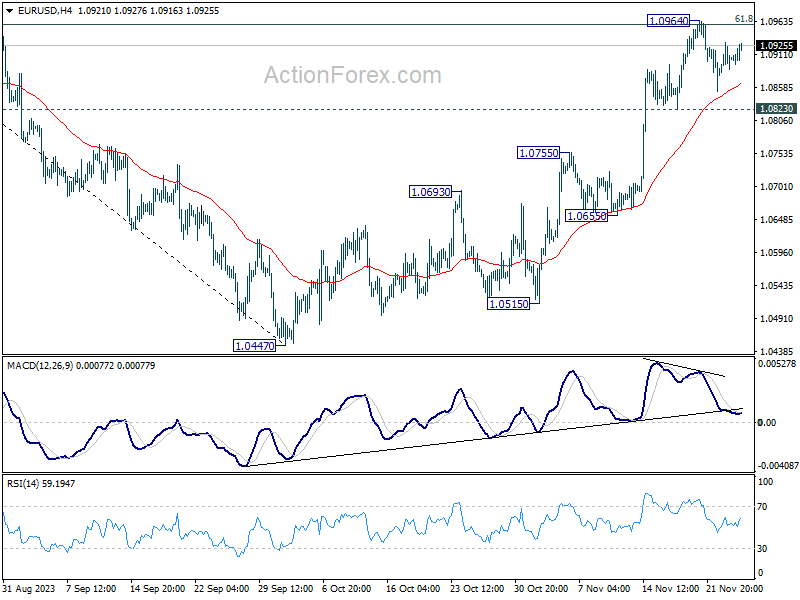

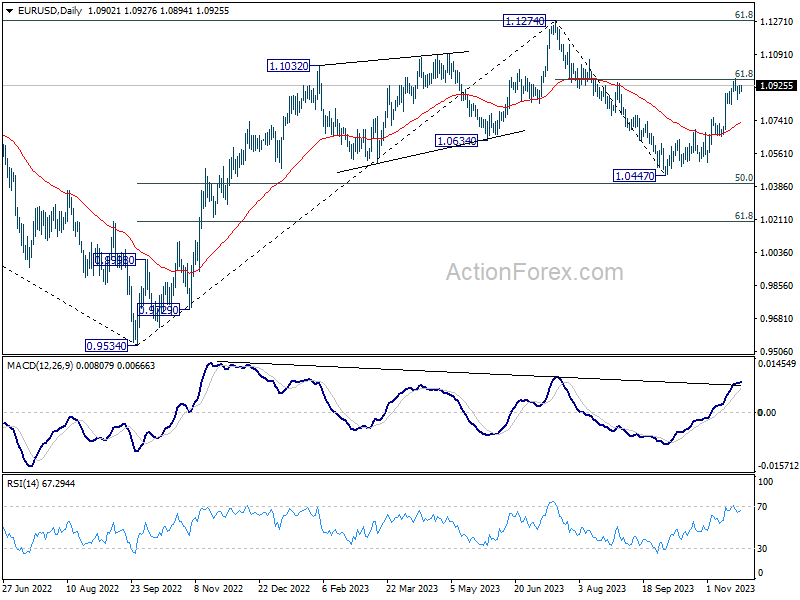

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0883; (P) 1.0906; (R1) 1.0929; More...

Intraday bias in EUR/USD remains neutral as consolidation from 1.0964 is still in progress. Further rally is in favor as long as 1.0823 support holds. Sustained break of 61.8% retracement of 1.1274 to 1.0447 at 1.0958 will resume the rise from 1.0447 to retest 1.1274 high. However, firm break of 1.0823 will indicate short term topping, and turn bias back to the downside for deeper decline.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

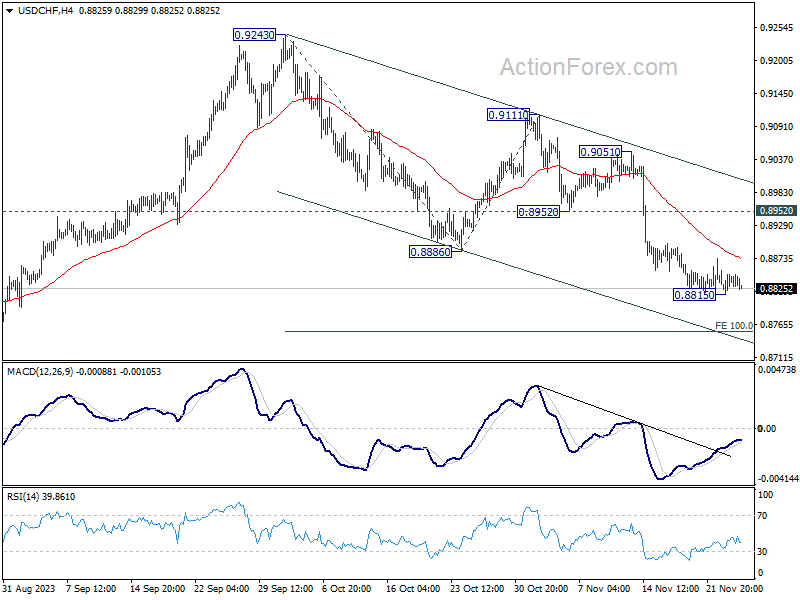

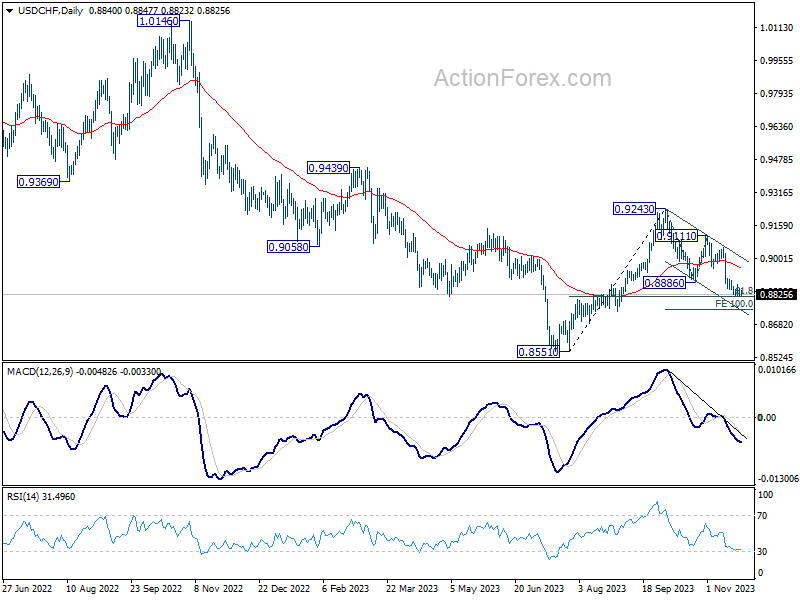

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8820; (P) 0.8839; (R1) 0.8861; More....

USD/CHF is extending consolidation above 0.8815 and intraday bias remains neutral. Stronger recovery cannot be ruled out. But near term outlook will stay bearish as long as 0.8952 support turned resistance holds. On the downside, below 0.8815 will resume whole decline from 0.9243 to 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754 next.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper fall would be seen to 61.8% retracement of 0.8551 to 0.9243 at 0.8815. Sustained break there will bring retest of 0.8551 low. For now, this will remain the favored case as long as 0.9111 resistance holds.

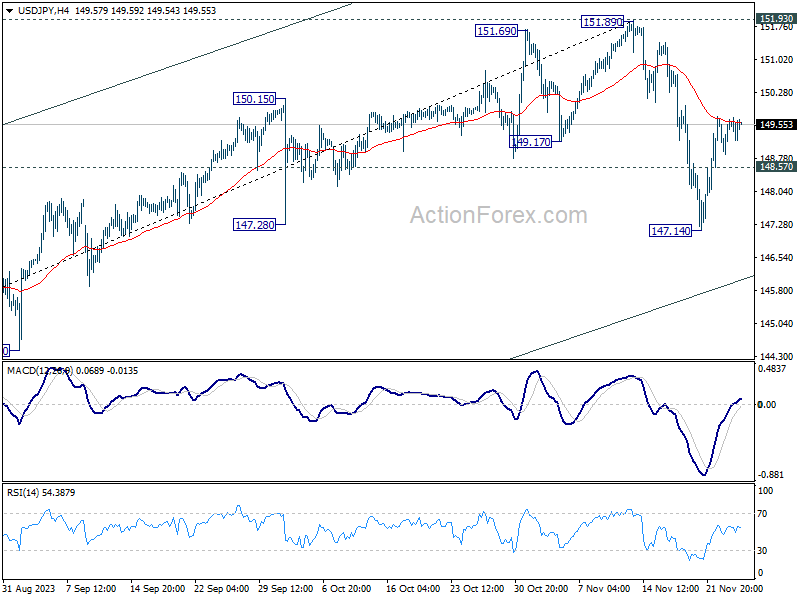

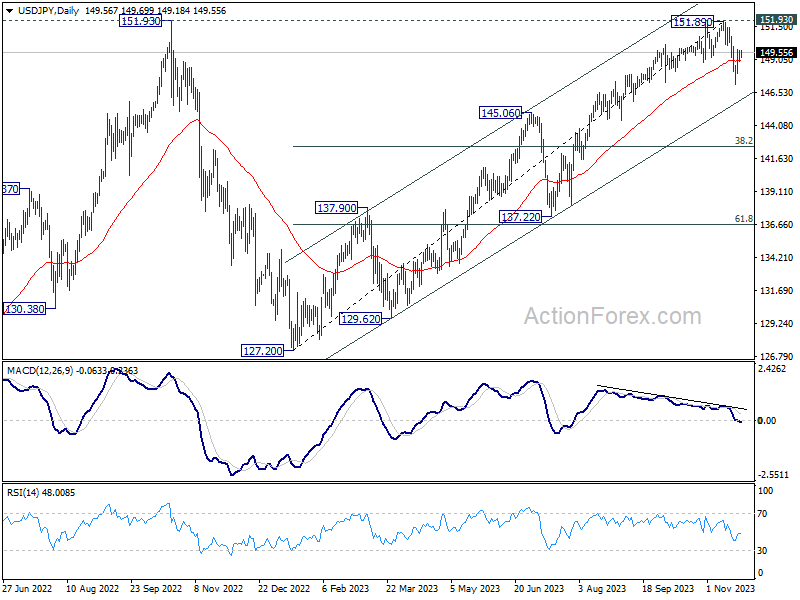

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.08; (P) 149.38; (R1) 149.88; More...

Intraday bias in USD/JPY remains neutral and outlook is unchanged. On the downside, break of 148.57 minor support will indicate rejection by 55 4H EMA, and turn bias back to the downside for 147.14 and below, to resume the fall from 151.89. However, sustained break of 55 4H EMA (now at 149.62) will revive near term bullishness, and target a retest on 151.89/93 resistance zone.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 resistance (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

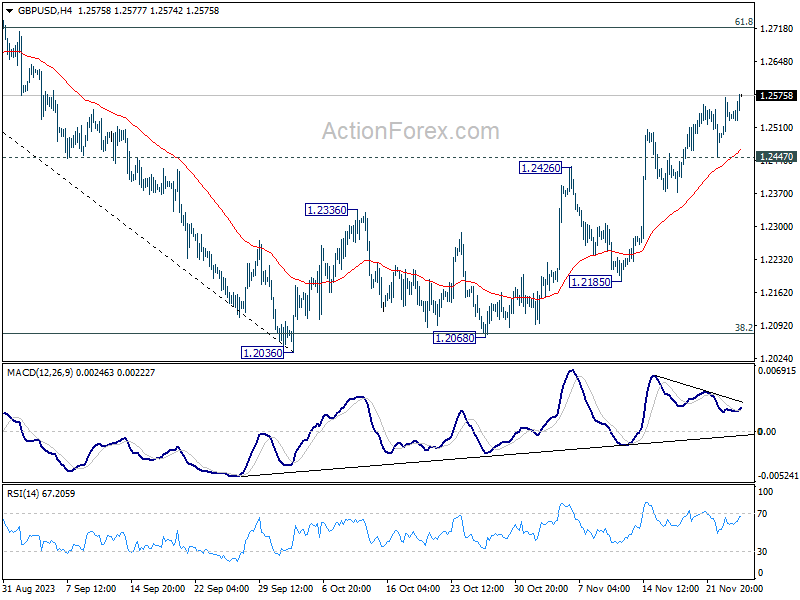

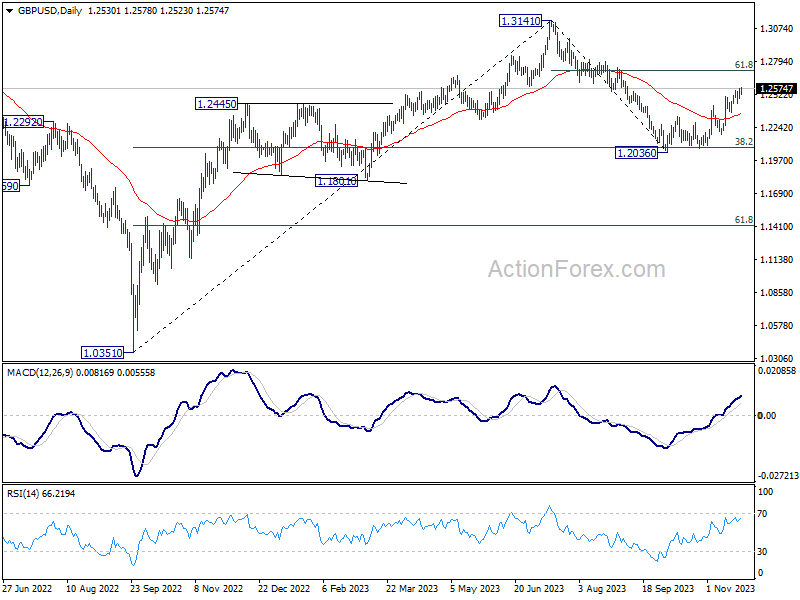

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2494; (P) 1.2529; (R1) 1.2568; More...

GBP/USD's rally is still in progress and intraday bias stays on the upside. Current rise from 1.2036 should target 61.8% retracement of 1.3141 to 1.2036 at 1.2716 next. On the downside, though, below 1.2447 minor support will turn intraday bias again first, and bring lengthier consolidations.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 argues that current rise from 1.2036 is the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

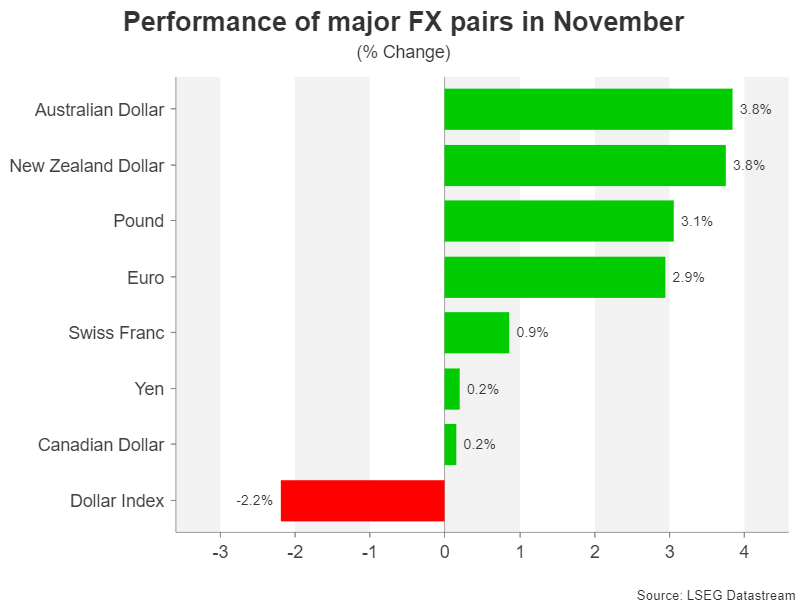

Canadian Dollar Rallies on Retail Sales Surprise, Kiwi and Sterling Firm

Canadian Dollar is having a notable rebound in early US session, fueled by unexpectedly robust Canadian retail sales data. This data indicated a surprising resurgence in consumer spending, defying the constraints of high interest rates and ongoing inflation.

Despite this uplift, Loonie was overshadowed by New Zealand Dollar, which also saw a lift from its own country's encouraging retail sales data. Similarly, British Pound is performing well, supported by improvement in UK consumer confidence.

Meanwhile, Japanese Yen is facing renewed pressure following a brief recovery after the release of Japan's CPI data. Both Dollar and Euro are exhibiting some softness, while Swiss Franc and Aussie are mixed.

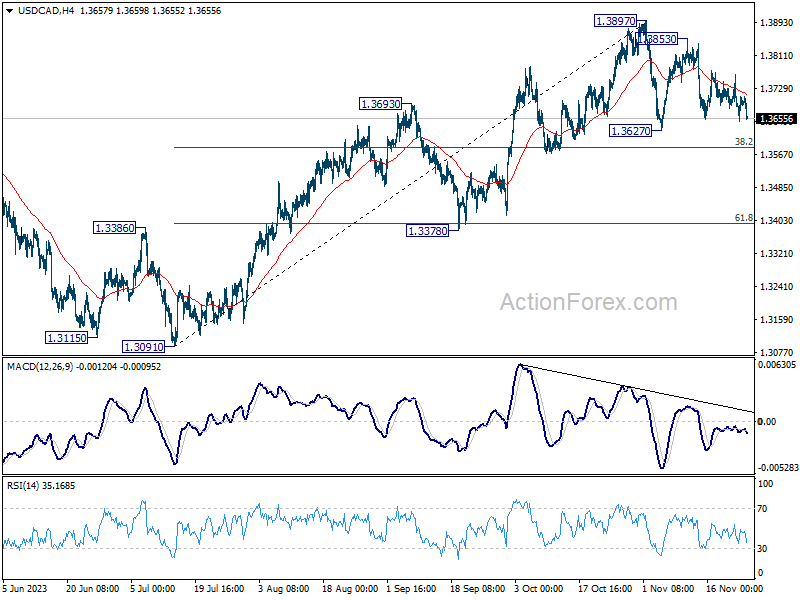

Technically, USD/CAD is possibly extending the third leg of the near term corrective pattern from 1.3897. Deeper fall could be seen to 1.3627 and possibly below. But downside should be contained by 38.2% retracement of 1.3091 to 1.3897 at 1.3589 to bring rebound. Hence, downside potential should be relatively limited based on current outlook.

In Europe, at the time of writing, FTSE is down -0.37%. DAX is up 0.03%. CAC is up 0.08%. Germany 10-year yield is up 0.0175 at 2.638. Earlier in Asia, Nikkei rose 0.52%. Hong Kong HSI fell -1.96%. China Shanghai SSE dropped -1.96%. Singapore Strait Times fell -0.54%. Japan 10-year JGB yield rose 0.0471 to 0.778.

Canada retail sales rose 0.6% mom in Sep, well above expectations

Retail sales in Canada rose 0.6% mom to CAD 66.5B in September, much better than expectation of 0.0% mom. Sales were up in four of nine subsectors and were led by increases at motor vehicle and parts dealers.

Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were down -0.3% mom.

In volume terms, retail sales increased 0.3% mom.

Retail sales were up 0.6% in Q3, while in volume terms, retail sales declined 0.5%.

Advance information suggests that sales rose 0.8% mom in October.

ECB's Lagarde: We can now observe very attentively

ECB President Christine Lagarde, said at Bundesbank event today that the central bank has "already done a lot" in fighting inflation, referring to the series of rate hikes. Now, given the "amount of ammunition" being deployed, ECB is positioned to "observe very attentively".

With observations on how tightening have impacted people's economic life, ECB can decide, "how long we have to stay there and what decision we have to make — up or down, she added.

However, despite these efforts, Lagarde emphasized that "the battle is not over and we're certainly not declaring victory."

German Ifo business climate rose to 87.3, economy stabilizing

German Ifo Business Climate rose from 86.9 to 87.3 in November, slightly below expectation of 87.5. But that is still the third consecutive increase. Current Assessment index ticked up from 89.2 to 89.4, matched expectations. Expectations index also rose from 84.8 to 85.2, missed expectation of 85.7.

By sector, manufacturing rose from -15.7 to -13.5. Services fell from -1.5 to -2.5. Construction rose from -30.8 to -29.4. Trade rose from -27.3 to -22.2.

Ifo said: "The German economy is stabilizing, albeit at a low level."

Japan's CPI core rises to 2.9%, above BoJ target for 19th mth, services prices surge

Japan's core CPI, which excludes fresh food prices, rose slightly from 2.8% yoy to 2.9% yoy in October, falling just below expected 3.0% yoy. Notably, this core CPI has stayed above BoJ's target of 2% for the 19th consecutive month, indicating persistent inflationary pressures.

Headline CPI, which includes all items, accelerated from 3.0% yoy to 3.3% yoy. However, core-core CPI, which excludes both food and energy, showed a slight deceleration, dropping from 4.2% yoy to 4.0% yoy. Despite this decrease, core-core CPI has remained above 4.0% for seven consecutive months, highlighting sustained inflation in areas beyond just the volatile items.

Breaking down the details, energy prices saw a significant decrease of -8.5% yoy. In contrast, food prices continued to climb, recording a 7.6% yoy increase. Durable goods also experienced a price rise of 3.2% yoy. Notably, services prices surged by 2.1% yoy, marking the fastest gain since 1993. This sharp increase in services prices underscores the broadening of inflationary pressures within the Japanese economy.

Japan's PMIs: Manufacturing contracts, services slightly improve

Japan's PMI for November shows a continuing contraction in the manufacturing sector and a slight improvement in services.

Manufacturing PMI dropped from 48.7 to 48.1, falling below the expected 48.8 and marking another month below the crucial 50.0 threshold, which separates contraction from expansion. This ongoing contraction has been the trend since June.

Conversely, Services PMI saw a marginal increase, moving up from 51.6 to 51.7, indicating a slight expansion in this sector. However, Composite PMI, which combines both manufacturing and services, edged down from 50.5 to exactly 50.0, highlighting stagnation in overall private sector activity.

Usamah Bhatti, an economist at S&P Global Market Intelligenc said: "Activity at Japanese private sector firms stagnated midway through the fourth quarter of 2023." This stagnation is further reflected in the demand conditions, which Bhatti noted remained "muted in November and were little-changed from October."

New Zealand retail sales volume flat in Q3, value up 1.5% qoq

In New Zealand, Q3 2023 saw retail sales volumes remain unchanged at 0.0% qoq, defying expectations of a -0.8% decline.

However, a contrasting trend emerged in the sales value, which increased by 1.5% qoq, indicating a disparity between the number of goods sold and their monetary value.

On an annual basis, there was a -3.4% yoy decrease in sales volume, whereas sales value saw 1.1% yoy increase.

These divergences should be reflective of inflationary pressures and corresponding shift in consumer purchasing patterns.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2494; (P) 1.2529; (R1) 1.2568; More...

GBP/USD's rally is still in progress and intraday bias stays on the upside. Current rise from 1.2036 should target 61.8% retracement of 1.3141 to 1.2036 at 1.2716 next. On the downside, though, below 1.2447 minor support will turn intraday bias again first, and bring lengthier consolidations.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 argues that current rise from 1.2036 is the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Retail Sales Q/Q Q3 | 0.00% | -0.80% | -1.00% | -0.90% |

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q3 | 1.00% | -1.50% | -1.80% | -1.60% |

| 23:30 | JPY | National CPI Y/Y Oct | 3.30% | 3.00% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Oct | 2.90% | 3.00% | 2.80% | |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Oct | 4.00% | 4.20% | ||

| 00:01 | GBP | GfK Consumer Confidence Nov | -24 | -27 | -30 | |

| 00:30 | JPY | Manufacturing PMI Nov P | 48.1 | 48.8 | 48.7 | |

| 00:30 | JPY | Services PMI Nov P | 51.7 | 51.6 | ||

| 07:00 | EUR | Germany GDP Q/Q Q3 F | -0.10% | -0.10% | -0.10% | |

| 09:00 | EUR | Germany IFO Business Climate Nov | 87.3 | 87.5 | 86.9 | |

| 09:00 | EUR | Germany IFO Current Assessment Nov | 89.4 | 89.4 | 89.2 | |

| 09:00 | EUR | Germany IFO Expectations Nov | 85.2 | 85.7 | 84.7 | 84.8 |

| 13:30 | CAD | Retail Sales M/M Sep | 0.60% | 0.00% | -0.10% | |

| 13:30 | CAD | Retail Sales ex Autos M/M Sep | 0.20% | -0.30% | 0.10% | |

| 14:45 | USD | Manufacturing PMI Nov P | 49.8 | 50 | ||

| 14:45 | USD | Services PMI Nov P | 50.4 | 50.6 |