Sample Category Title

EURUSD Looking to End Impulsive Rally

Short Term Elliott Wave in EURUSD suggests rally from 10.4.2023 low is in progress as a 5 waves impulse structure. Up from 10.4.2023 low, wave ((i)) ended at 1.0694 and pullback in wave ((ii)) ended at 1.0517. Pair then extended higher in wave ((iii)) towards 1.0965 as the 1 hour chart below shows. Pullback in wave ((iv)) ended at 1.085 with internal subdivision as a zigzag structure.

Down from wave ((iii)), wave (a) ended at 1.0882 and rally in wave (b) ended at 1.0917. Wave (c) lower ended at 1.085 which completed wave ((iv)) in higher degree. Pair has turned higher in wave ((v)), but it has yet to break above wave ((iii)) at 1.0965 to rule out a double correction. Up from wave ((iv)), wave (i) ended at 1.093 and pullback in wave (ii) ended at 1.0886. Wave (iii) higher ended at 1.0959 and pullback in wave (iv) ended at 1.09243. Near term, as far as pivot at 1.085 low stays intact, expect dips to find support in 3, 7, or 11 swing and pair to extend higher in wave ((v)). Potential target higher is 123.6% – 161.8% inverse retracement of wave ((iv)) at 1.099 – 1.103

EURUSD 60 Minutes Elliott Wave Chart

EURUSD Elliott Wave Video

https://www.youtube.com/watch?v=chIdCvVpZmM

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.26; (P) 148.97; (R1) 149.40; More...

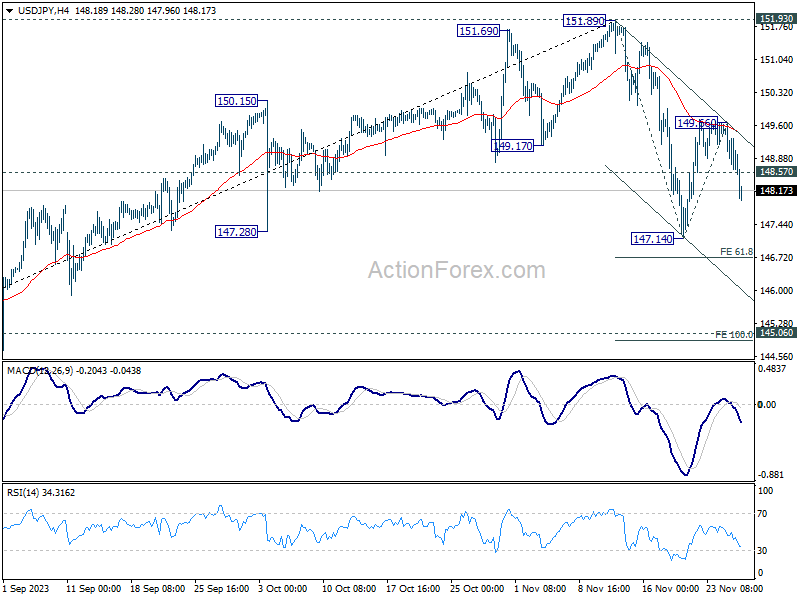

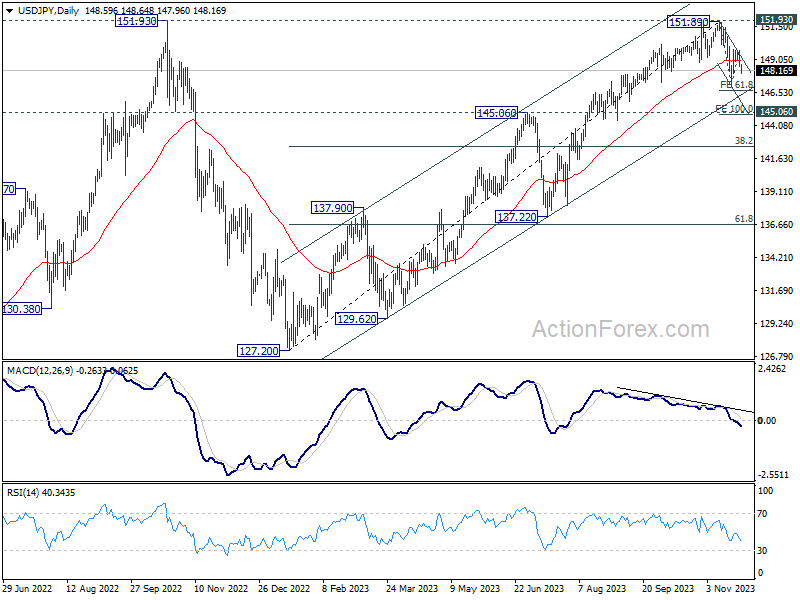

USD/JPY's break of 148.57 minor support indicates rejection by 55 4H EMA. Intraday bias is back on the downside to extend the decline from 151.9. Next target is 147.14 support. Further break of 61.8% projection of 151.89 to 147.14 from 149.66 at 146.72will pave the way to 100% projection at 149.91, which is close to 145.06 key resistance turned support. For now, risk will stay on the downside as long as 149.66 resistance holds, in case of recovery.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

Yen Strengthens Amid Speculation of BoJ Policy Shift and Business Sector’s Currency Concerns

Yen has a notable bounce in Asian session today, fueled by a Nikkei report suggesting that BoJ is finally near to the end its negative interest rate policy. This policy shift, which could see interest rates rise as early as the first half of next year, hinges on the outcomes of spring labor-management negotiations and consumer spending development. Such a move, if realized, would mark a major shift in monetary policy, being the first interest rate hike in 17 years.

Nikkei report indeed aligns closely with BoJ's existing communication, where a wage-price spiral is considered a prerequisite for any rate hike. While BoJ has not specified a timeline, the timing of spring wage negotiations make the first half of 2024 a plausible period for this policy change.

In a related development, Yomiuri newspaper reported that Japan's top business lobby, Keidanren, plans to discuss the potential negative impacts of Yen's weakness on the economy. This is a notable shift, as Keidanren, comprising major companies in the automotive and electronics sectors, has traditionally favored a weak yen. A reevaluation of this stance could intensify calls for BoJ to end ultra-loose monetary policy, reflecting a changing perspective in Japan's business sector regarding currency valuation and economic impact.

Globally, Dollar is underperforming, extending its near-term sell-off. Euro, continuing to struggle too, has failed to break out from its near-term range against the weak Dollar. Swiss Franc is performing marginally better than Euro, while Sterling appears firmer among European currencies. Interestingly, Australian Dollar is currently the second strongest after Yen, showing resilience despite weak retail sales data, followed by Canadian Loonie and New Zealand Kiwi.

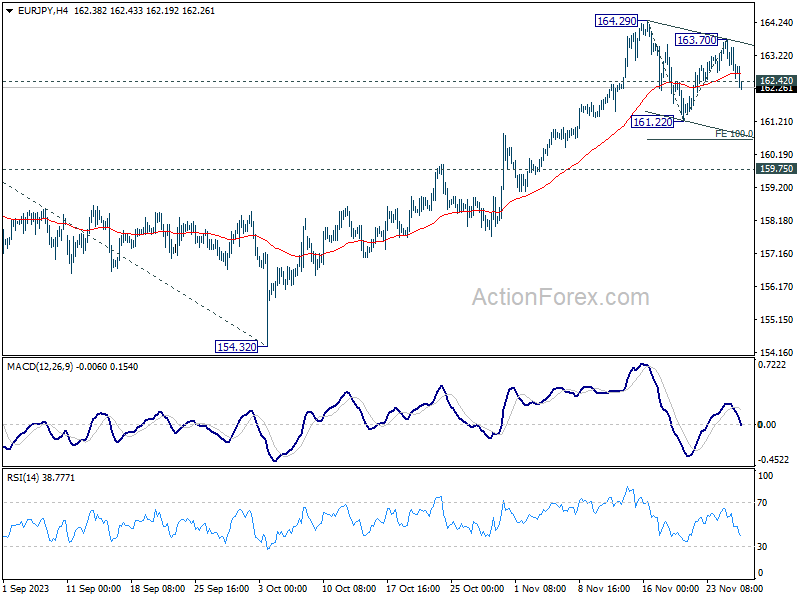

From a technical standpoint, EUR/JPY's break of 162.42 minor support indicates the start of the third leg of the corrective pattern from 164.29. Deeper fall could reach 161.22 support and potentially lower, though strong support is expected around 159.75 resistance-turned-support to complete the correction. However, decisive fall through 159.75 would be a significant indicator of Yen's underlying strength.

In Asia, at the time of writing, Nikkei is down -0.31%. Hong Kong HSI is down -0.60%. China Shanghai SSE is up 0.10%. Singapore Strait Times is down -0.38%. Japan 10-year JGB yield is down -0.0075 at 0.768. Overnight, DOW fell -0.16%. S&P 500 fell -0.20%. NASDAQ fell -0.07%. 10-year yield fell -0.083 to 4.389.

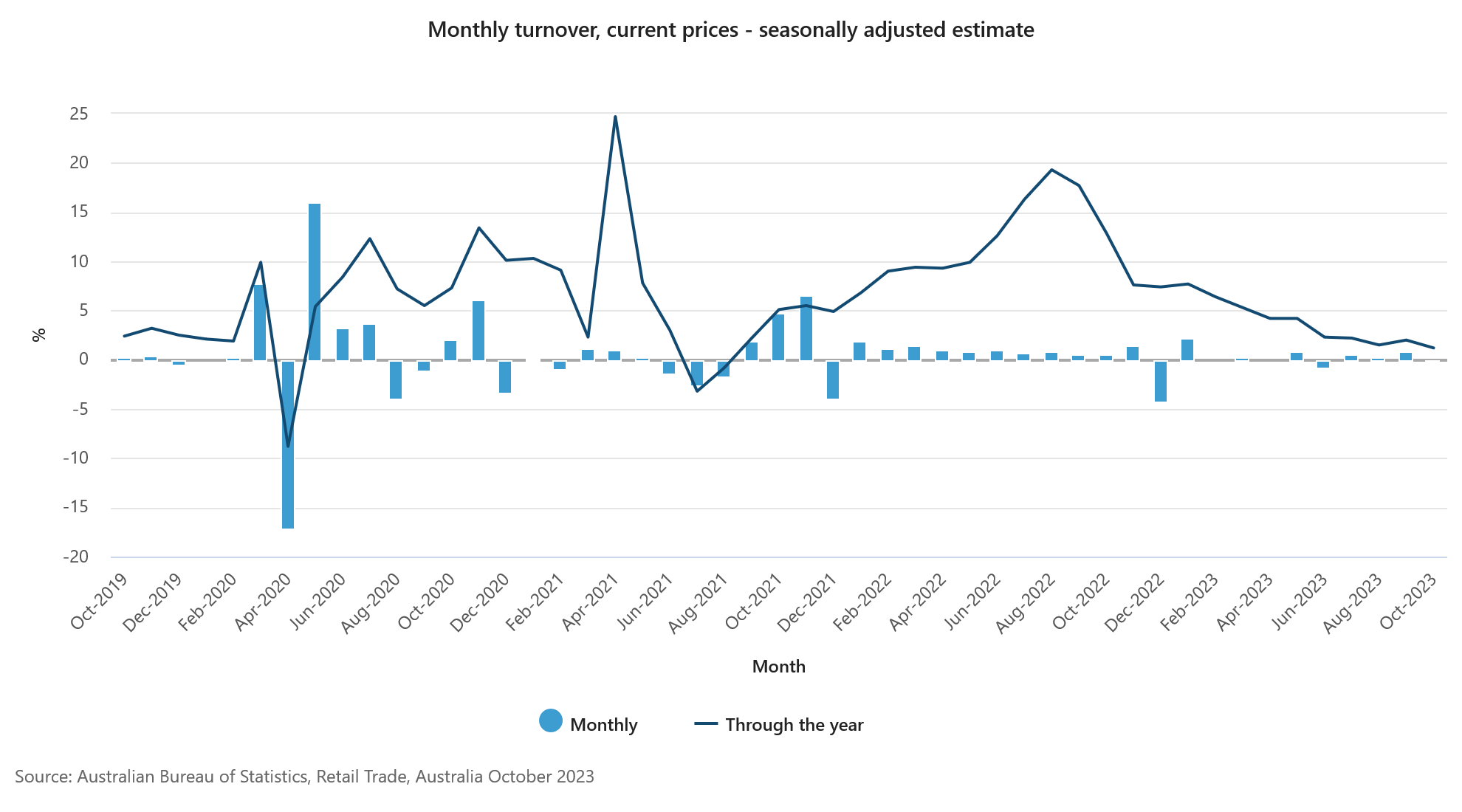

Australia retail sales down -0.2% mom in Oct, strategic delay for Black Friday

Australia's retail sales turnover in October displayed an unexpected downturn, falling by -0.2% mom, contrary to the anticipated rise of 0.1% mom. This decline follows a period of growth, with 0.9% mom increase in September and 0.2% mom rise in August.

Ben Dorber, head of retail statistics at ABS, noted "Retail turnover fell in October after a short-lived boost in spending in September." This downturn was seen across all retail categories except food retailing.

Dorber attributed this pause in consumer spending to a strategic delay by consumers, who are likely waiting to capitalize on Black Friday sales events in November. He observed that this has become a recurring pattern in recent years, with Black Friday sales gaining increasing popularity among consumers.

RBA's Bullock: we have to be a little bit careful in this period

In a central bank conference held in Hong Kong, RBA Governor Michele Bullock said that monetary policy is currently restrictive, a necessary stance to moderate demand and anchor inflation expectations.

Bullock highlighted the need to be "a little bit careful," in this period, aiming to control inflation and bring it back within target range of 2-3%, while also being mindful of not overly burdening the economy or causing a significant rise in unemployment rates.

Bullock also pointed out the emergence of "second-round effects" in areas like wages, observing that businesses are currently able to pass on increased costs to maintain profit margins, a trend reflecting sufficient demand.

At the same panel, BoE Deputy Governor Dave Ramsden stated that monetary policy in UK would likely need to remain "restrictive for an extended period" to effectively bring inflation back to 2% target.

Additionally, Pablo Hernández de Cos, Governor of Bank of Spain, noted that tight monetary policy is necessary in the short term. However, he also mentioned the possibility of easing should inflation slow as forecasted.

Looking ahead

Germany Gfk consumer confidence and Eurozone M3 will be release in European session. Later in the day, US will release house price index and consumer confidence.

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.26; (P) 148.97; (R1) 149.40; More...

USD/JPY's break of 148.57 minor support indicates rejection by 55 4H EMA. Intraday bias is back on the downside to extend the decline from 151.9. Next target is 147.14 support. Further break of 61.8% projection of 151.89 to 147.14 from 149.66 at 146.72will pave the way to 100% projection at 149.91, which is close to 145.06 key resistance turned support. For now, risk will stay on the downside as long as 149.66 resistance holds, in case of recovery.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:01 | GBP | BRC Shop Price Index Y/Y Oct | 4.30% | 5.20% | ||

| 00:30 | AUD | Retail Sales M/M Oct | -0.20% | 0.10% | 0.90% | |

| 07:00 | EUR | Germany Gfk Consumer Confidence Dec | -28.5 | -28.1 | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Oct | -0.90% | -1.20% | ||

| 14:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Sep | 4.20% | 2.20% | ||

| 14:00 | USD | Housing Price Index M/M Sep | 0.40% | 0.60% | ||

| 15:00 | USD | Consumer Confidence Nov | 101 | 102.6 |

RBA’s Bullock: we have to be a little bit careful in this period

In a central bank conference held in Hong Kong, RBA Governor Michele Bullock said that monetary policy is currently restrictive, a necessary stance to moderate demand and anchor inflation expectations.

Bullock highlighted the need to be "a little bit careful," in this period, aiming to control inflation and bring it back within target range of 2-3%, while also being mindful of not overly burdening the economy or causing a significant rise in unemployment rates.

Bullock also pointed out the emergence of "second-round effects" in areas like wages, observing that businesses are currently able to pass on increased costs to maintain profit margins, a trend reflecting sufficient demand.

At the same panel, BoE Deputy Governor Dave Ramsden stated that monetary policy in UK would likely need to remain "restrictive for an extended period" to effectively bring inflation back to 2% target.

Additionally, Pablo Hernández de Cos, Governor of Bank of Spain, noted that tight monetary policy is necessary in the short term. However, he also mentioned the possibility of easing should inflation slow as forecasted.

Markets Daily

US bond yields fell substantially despite only minor data, weighing on the US dollar. AUD/USD traded above 0.6600 for the first time since August. Today’s data includes Australia October retail sales and US November consumer confidence, while RBA Governor Bullock takes part in an HKMA-BIS panel.

Yesterday

Australia’s data calendar was empty but there was plenty of news about the RBA from the government. Legislation to reform the RBA was announced though with no real surprises given substantial previous commentary. The surprise was in Treasurer Chalmers’ selection of a Bank of England official to be RBA deputy governor, Andrew Hauser. He has lengthy experience in financial markets. AUD/USD traded a range of 0.6567 to 0.6595, for no net change at 0.6580. US equity futures joined the sour mood in Asia-Pacific stocks, though most moves weren’t especially large. The ASX 200 closed -0.75%, one of the weaker performances.

Currencies/Macro

The US dollar fell against all G10 currencies on the day. EUR/USD rose 15 pips to 1.0955. GBP/USD rose 0.2% to 1.2630. USD/JPY followed the fall in Treasury yields, down from 149.45 to 148.65. AUD/USD rose a net 20 pips to 0.6605, its first trade above 0.6600 since 10 August. NZD/USD rose from 0.6075 to 0.6100, also printing highs since August. AUD/NZD is little changed at 1.0830.

US new home sales in October fell -5.6% (est. -5.1%, prior revised down to +8.6%), the decline attributed to high mortgage rates. Inventory rose for a third month, and the median home price slipped to $409k from $422k. The Dallas Fed manufacturing index was little changed in November at -19.9 (est. -16.0, prior -19.2), the production component falling into contraction territory.

ECB President Lagarde reiterated vigilance was needed against inflation that remains too high, with risks that it could rise again in the near term. She also said bond holdings relating to the PEPP (Pandemic Emergency Purchase Programme) might be reviewed soon.

Interest rates

The US 2yr treasury yield initially rose to 4.98% but then began a steady descent, to 4.88%. The 10yr yield also rose early, to 4.51%, only to roll over to 4.39%. Markets are pricing the Fed funds rate, currently 5.375% (mid), to be unchanged at the next meeting on 14 December, with a 50% of a rate cut by May 2024.

Australian 3yr government bond yields (futures) fell from 4.24% to 4.15%, while the 10yr yield fell from 4.58% to 4.48%. Markets are pricing no change at the next meeting on 5 December, but a 50% chance of one in February 2024. New Zealand rates markets price the OCR, currently at 5.50%, to be unchanged on 29 November, and in February, with a 40% chance of a rate cut by July 2024.

Primary markets saw an uptick after the Thanksgiving shortened week; in Europe ANZ placed a GBP1.0bn covered and Roche placed EUR1.5bn across two lines, US markets saw an active session with Citibank NA issuing USD2.5bn across two lines, The Home Depot Inc issuing USD2.0bn and Brookfield placing USD700M. Itraxx Europe widened 1.5bps to 69.7bps with Unibail-Rodamco-Westfield amongst the worst performers. CDX IG widened 0.6 bps to 63.8bps; Dominion Energy and Verizon had the best performing contracts while Whirlpool and Ally Financial were a drag on the index. Cash bonds widened 0.2bps to 142.7, the best performing sectors were technology and communications, while utilities and materials were the worst performing.

Commodities

Crude markets slipped again as traders focused on the chances of OPEC+ extending and deepening cuts into 2024. The January WTI contract is down 62c at $74.92 while the January Brent contract is down 55c at $80.03. Bloomberg ran a story suggesting that Saudi Arabia is “asking others in the coalition to reduce their oil-output quotas in a bid to shore up global markets but some members are resisting, delegates said”. Eurasia group said that “if the group does not announce an additional cut of about 1mbpd on top of an extension of the Saudi voluntary measure, the risk is that the $80 per barrel floor that has largely held so far will shift downward to the mid or even low $70s”. Weak industrial profits data in China for October hit sentiment too. However, a storm on the Black Sea suspended loadings at the Novorossiysk and the CPC terminal used by Kazakhstan.

Metals were lower again with copper down 0.6% at $8,375 and nickel down another 0.7% to $16,025. Tin slumped another 3.8% to $22,979 and is down by a hefty 7.6% over the last 5 sessions, hitting lows back to March of this year. Nickel is down 12.3% so far this month. Goldman noted that the “combination of hitting the capacity cap and Yunnan winter cuts means that onshore primary [aluminium] production will likely grow 2% next year”. Chinese production year to date is up 3.4%yy. Goldman sees a shortage of 1.23mmt of primary aluminium next year, almost double the deficit in 2023 with the price rising to $2,600 in 12 months. France was said to be moving to save a struggling nickel processing plant in New Caledonia due to weakening prices. Finance Minister Bruno Le Maire said, “I want us to get a primary agreement in the early days of January”. Uganda will start issuing certification for exports of tin and a tin refinery in the west of the country is awaiting a licence to start operations.

Iron ore markets softened as China’s NDRC said it had conducted research on steel, iron ore and other commodity indices. Coming on top of an announcement yesterday that it was “studying and strengthening the supervision of iron ore at port, strengthening industry self-discipline, setting up reasonable and relevant rules for the use of storage yards, speeding up the turnover of goods, resolutely preventing the use of hoarding and speculation, and effectively maintaining market order”, it emphasised the lengths that the authorities are going to. The December SGX contract is down 25c at $131.40 while the 62% Mysteel index is down by $1.10 to $133.75. China will report its PMIs Thursday and Friday. Goldman sees a balanced market into 2024, noting greater risk to the upside than downside for iron ore prices. Citi noted that “any dip in iron ore from here through to at least the Chinese New Year could represent a buying opportunity”.

Day ahead

RBA Governor Bullock will speak as a panel participant at the HKMA-BIS “high-level” conference in Hong Kong, from 12:18pm Syd.

At 11:30am Syd, Australia October retail sales are expected to be more subdued after the 0.9% bounce in September, which was partly attributed to transitory factors including unseasonal early spring warmth and the new iPhone model. Westpac forecasts a 0.2%mth rise, keeping the annual rate consistent with contraction in inflation-adjusted, per capita retail spending. Note however that the ABS plans to discontinue this survey in 2025 as it now accounts for only 33% of household consumption.

The Conference Board measure of US November consumer confidence index may continue to reflect potential optimism after a pause in rate hikes (market f/c: 101.0). An unstable outlook for manufacturing may feature in the November Richmond Fed index (market f/c: +1).

Chicago Fed president Goolsbee (dove) and Fed governor Waller (hawk) are due to speak.

USDJPY Forecasting The Rally After Elliott Wave Double Three Pattern

Hello fellow traders. In this technical article we’re going to take a look at the Elliott Wave charts charts of USDJPY published in members area of the website. As our members know USDJPY has recently made pull back that has unfolded as Elliott Wave Double Three Pattern. It made clear 7 swings from the November 13th peak and completed correction right at the Equal Legs zone . In further text we’re going to explain the Elliott Wave pattern and forecast

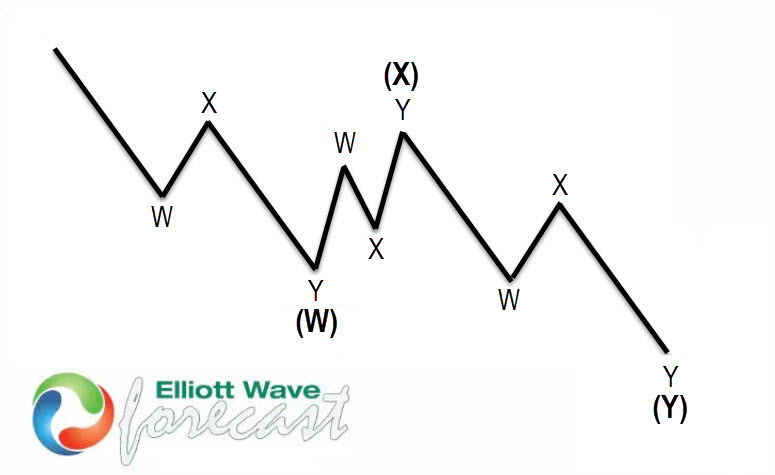

Before we take a look at the real market example, let’s explain Elliott Wave Double Three pattern.

Elliott Wave Double Three Pattern

Double three is the common pattern in the market , also known as 7 swing structure. It’s a reliable pattern which is giving us good trading entries with clearly defined invalidation levels.

The picture below presents what Elliott Wave Double Three pattern looks like. It has (W),(X),(Y) labeling and 3,3,3 inner structure, which means all of these 3 legs are corrective sequences. Each (W) and (Y) are made of 3 swings , they’re having A,B,C structure in lower degree, or alternatively they can have W,X,Y labeling.

USDJPY H4 Update 11.20.2023

USDJPY is doing correction that is unfolding as a 7 swings pattern. Pull back has (W)(X)(Y) blue labeling. First leg (W) is having Zig Zag Structure – 3 waves ABC red, while (Y) leg can be WXY Double Three Pattern. The structure is still incomplete at the moment. The pair is showing lower low sequences from the 151.89 peak. We expect to see another leg down toward extreme area: 147.26-146.62 ( buying zone). Once USDJPY reaches proposed extreme zone, we expect the pair to make a rally toward new highs or in 3 waves bounce alternatively.

USDJPY H4 Update 11.21.2023

The pair found buyers at the Equal Legs Area . It made nice rally from the zone which looks to be impulsive. Bounce already reached 50 fibs against the (X) blue connector which confirms cycle from the peak is done for sure. Consequently, any long positions from the equal legs area should be risk free by now. As far as the price stays above 147.13 low, we can consider correction completed and see further strength in the commodity.

Australia retail sales down -0.2% mom in Oct, strategic delay for Black Friday

Australia's retail sales turnover in October displayed an unexpected downturn, falling by -0.2% mom, contrary to the anticipated rise of 0.1% mom. This decline follows a period of growth, with 0.9% mom increase in September and 0.2% mom rise in August.

Ben Dorber, head of retail statistics at ABS, noted "Retail turnover fell in October after a short-lived boost in spending in September." This downturn was seen across all retail categories except food retailing.

Dorber attributed this pause in consumer spending to a strategic delay by consumers, who are likely waiting to capitalize on Black Friday sales events in November. He observed that this has become a recurring pattern in recent years, with Black Friday sales gaining increasing popularity among consumers.

Dollar Could Get Caught Between Soft Data and Hawkish Fed Talk

- Expected drop in core PCE inflation could fuel rate cut bets

- But will Fed officials move a step closer to a dovish pivot?

- Dollar starts week on the backfoot ahead of Thursday’s data due 13:30 GMT

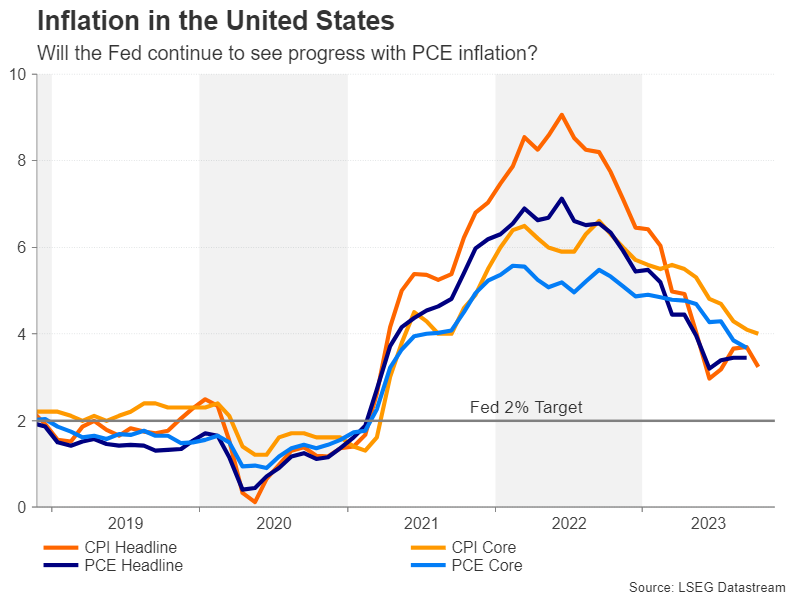

US inflation still headed in the right direction

Whilst CPI inflation suffered a setback from the oil price rally earlier in the year, PCE inflation has maintained a downward trajectory, bolstering expectations that the Federal Reserve will begin cutting rates by the middle of 2024. Specifically, the core PCE price index that the Fed attaches the most weight to for its policy decisions has come down markedly in recent months after stalling around 5% at the start of the year.

Core PCE is expected to have eased from 3.7% to 3.5% y/y in October. That’s still one-and-a-half percentage points above the 2% objective but the slowdown in the month-on-month pace during the course of the year suggests the Fed is well on its way to hitting its target. The question is, though, how soon will it get there, and can it achieve this without tightening further?

Don’t fight the Fed?

Markets have already made up their minds about this and think that with the added slowdown in economic growth and the pullback in oil prices policymakers will need to lower the Fed funds rate at some point over the coming months to prevent policy from becoming too restrictive.

This doesn’t seem like an unreasonable assumption to make. The big danger, though, with this thinking isn’t so much the mere speculation about rate cuts, but just how strong investors’ conviction has been, as the latest pricing in Fed fund futures points to at least three 25-bps cuts by the end of 2024.

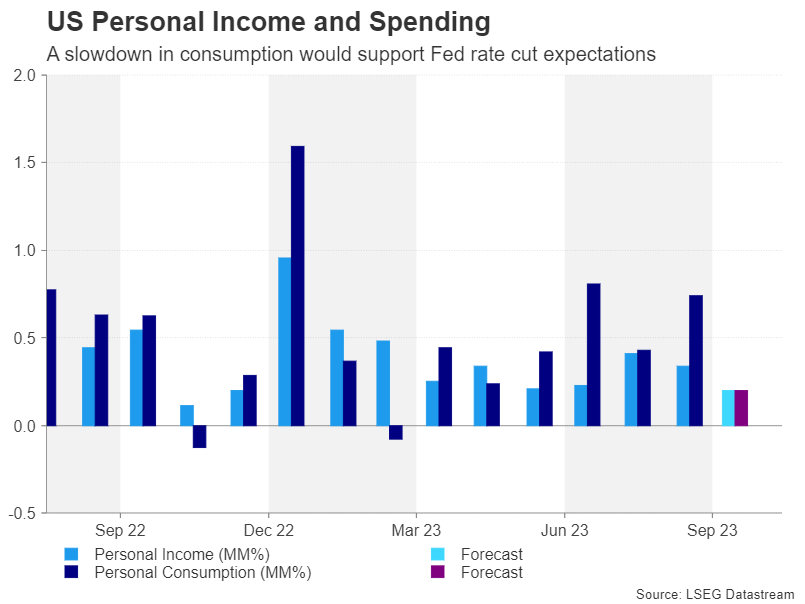

Consumer spending may finally be coming off the boil

The personal income and spending numbers that will be released alongside the PCE price gauges will likely support the markets’ view. After a bumper few months for the US consumer, personal consumption is expected to have cooled from 0.7% to 0.2% m/m in October, with personal income also projected to have moderated to 0.2% m/m.

Furthermore, the ISM manufacturing PMI that’s due the following day at 15:00 GMT is forecast to remain below the 50.0 level that separates contraction from expansion. The manufacturing PMI has been stuck below 50 since November 2022 and although it likely edged up in November to 47.6, the improvement won’t be enough to ease concerns about stagnating growth.

Aside from the aforementioned reports, investors will also be sifting through the consumer confidence index (Tuesday), the second estimate of Q3 GDP (Wednesday) and the Chicago PMI (Thursday).

Will Powell steer market expectations?

Unless there are some significant positive surprises in the data, investors are not about to alter their predictions for the rate path, keeping the US dollar on the backfoot. However, it is not just economic indicators that traders will have to keep an eye on this week as several Fed officials are scheduled to speak in the coming days, the most important of which will be Chair Powell’s address on Friday (16:00 GMT).

The Fed chief may try to use this opportunity to guide markets in a particular direction before the blackout period begins at the weekend for the December 13-14 meeting.

This would be especially true if investors ratchet up their rate cut bets on the back of softer-than-anticipated data and the Fed then attempts to rein in those expectations. So far, Powell has only been partially successful in doing that, but nevertheless, there is a risk of some dollar volatility if the markets read the latest numbers on the economy one way and the Fed another.

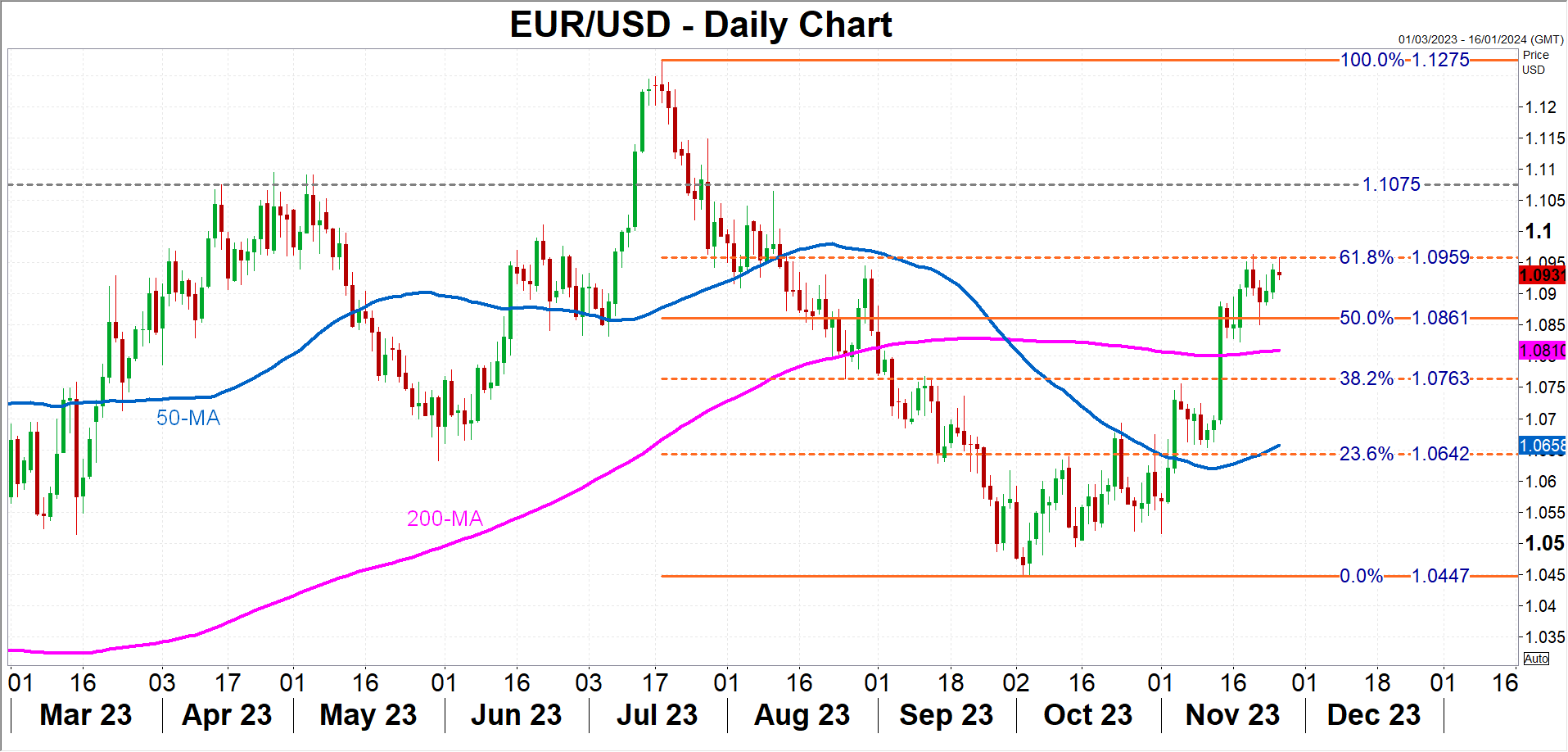

Make or break for euro’s latest rebound

For currencies such as the euro that have reached critical junctures in their recovery against the dollar, the data and the rhetoric coming from the Fed could decide whether their rebound can be stretched any further.

The euro is currently testing the 61.8% Fibonacci retracement of the July-October downleg at $1.0959. A break above this level is possible if the US releases disappoint, setting the stage for a re-challenge of the July peak of $1.1275, although euro/dollar would first have to overcome the $1.1075 hurdle.

But if either the data or hawkish talk from the Fed dampen rate cut expectations, the euro could fall back, seeking support from its 200- and 50-day moving averages at $1.0810 and $1.0658, respectively.

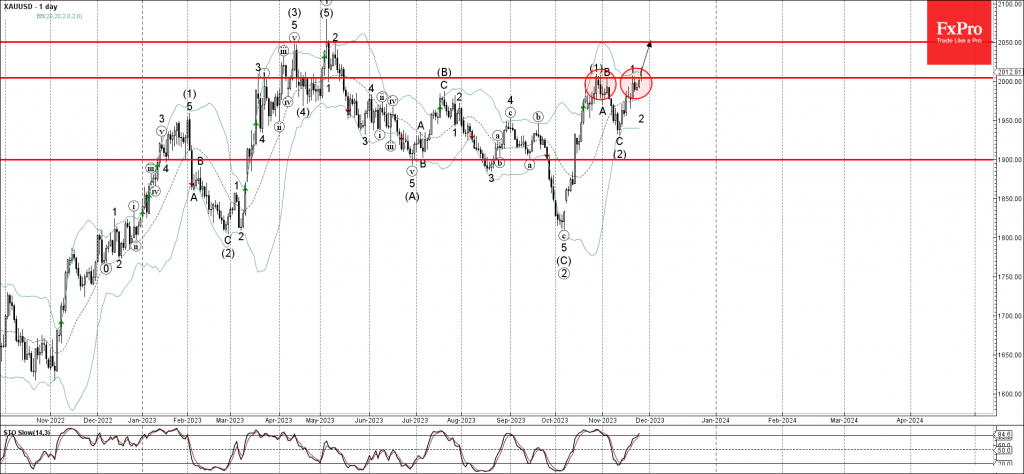

Gold Wave Analysis

- Gold broke key resistance level 2000.00

- Likely to rise to resistance level 2050.00

Gold recently broke the key resistance level 2000.00 (which stopped the previous waves (1), B and 1, as can be seen below).

The breakout of the resistance level 2000.00 continues the active minor impulse wave 3 which belongs to wave (3) from the start of this month.

Gold can be expected to rise further to the next resistance level 2050.00 (former strong resistance from April and May) – from where the downward correction is likely.