Sample Category Title

Australian Dollar Reaches Its Highest Since Early August

Important events regarding AUD took place this morning:

→ the level of retail sales for the month in Australia unexpectedly fell: actual = -0.2%, expected = +0.1%, a month earlier = +0.9%.

→ a press conference was held by the head of the RBA, Michelle Bullock, according to whom inflation in Australia follows the path of overseas countries. That is, inflation is decreasing, as in the USA and Great Britain.

Against the background of these events, the AUD/USD rate exceeded the level of 0.663 for the first time since the beginning of August. The rally from the late October low is already about 5.5%. However, this upward trend has 3 important obstacles:

- The upper limit of the November ascending channel (shown in blue).

- The upper limit of the longer-term parallel channel (shown in red).

- Level 0.660. During 2023, it worked as support once. Therefore, from the point of view of technical analysis, there is reason to expect that it will provide resistance.

And although the price of AUD/USD today exceeded these levels, it can hardly be said with confidence that it has consolidated there. Also pay attention to the RSI indicator, which is on the border of the overbought zone.

Taking into account the above factors, it is acceptable to expect a pullback in the market. The trigger could be news about the CPI values for Australia, which will be published tomorrow.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Euro Continues to Rise, But Further Gains Questionable

The euro (EUR) gained 0.13% on Monday as weaker-than-expected sales of new homes in the U.S. brought the U.S. dollar lower.

Possible effects for traders

Technically, the U.S. Dollar Index did enough damage over the last two weeks to really suggest a breakdown. So the dollar's heyday is done, and we're now looking at a softer dollar,' said Amo Sahota, the director at FX consulting firm Klarity FX. The market believes the Federal Reserve (Fed) has ended hiking interest rates and may start cutting them by Q1 2024. Also, expectations for the eurozone's monetary policy don't differ drastically. Christine Lagarde, the President of the European Central Bank (ECB), said it's too early to claim success in the battle against inflation. However, she acknowledged the economy is stagnating, suggesting that the eurozone may have reached the peak in the interest rate. Eurozone inflation data and the U.S. core Personal Consumption Expenditure data will be released on Thursday. Both indicators are expected to show a trend of disinflation.

EURUSD was falling slightly during the early European trading session. The latest data showed that consumer confidence in Germany improved in November but remained at a rather low level. Later today, traders should pay attention to the U.S. Consumer Confidence Index at 3:00 p.m. UTC. Higher-than-expected figures will likely reverse the bullish trend in EURUSD.

Gold Continues Rising as Dollar Weakens

The gold (XAU) price rose for the third consecutive trading session, gaining 0.58% and reaching a six-month high.

Possible effects for traders

The U.S. economy continues signalling a slowdown, increasing the chances for interest rate cuts and pulling down the U.S. Dollar Index (DXY). Market sentiment currently shows a 25% probability the Federal Reserve (Fed) might start reducing rates in March 2024, with the likelihood increasing to 45% by May. Recent data revealed a 5.6% decline in U.S. new home sales to 679,000 units in October, lower than the expected 723,000 units. DXY reached its lowest point since late August, making gold more affordable for holders of other currencies. Meanwhile, yields on 10-year Treasury notes remained close to their two-month low of 4.363%. The probability of lowering interest rates decreases the opportunity cost associated with holding non-yielding bullion. However, the most recent data from the physical market shows that China's net gold imports via Hong Kong fell for a second consecutive month in October as slow economic recovery reduced demand.

XAUUSD was relatively flat during the Asian and early European trading sessions. Today, traders should focus on the release of the U.S. CB Consumer Confidence report at 3:00 p.m. UTC. Lower-than-expected figures will have a positive impact on XAUUSD. However, higher-than-expected numbers may bring the pair down towards 2,000. 'Spot gold may extend gains into a range of $2,026 to $2,032 per ounce, as it has more or less broken a resistance at $2,016,' said Reuters analyst Wang Tao.

Bundesbank’s Nagel: Encouraging inflation outlook doesn’t mean hike cycle is over

In a speech in Cyprus today, Joachim Nagel, ECB Governing Council member and Bundesbank President, described the inflation outlook as "encouraging". But he was quick to caution that this "that does not necessarily mean that the current hike cycle is now over."

Nagel emphasized the potential need to raise rates again if the "inflation outlook worsened"

He mentioned that a downside surprise, where price growth returns to ECB's 2% target quicker than anticipated, is "much less probable." As a result, Nagel believes it is too soon to even consider the possibility of rate cuts.

On the economic growth front, Nagel projected a rebound next year. He noted that wage growth remains robust and pointed out that the disinflationary effect of falling energy prices has faded.

Nagel also specifically advocated for a "significantly" smaller balance sheet. He stressed his preference to "err on the side of caution" to ensure a timely return to price stability.

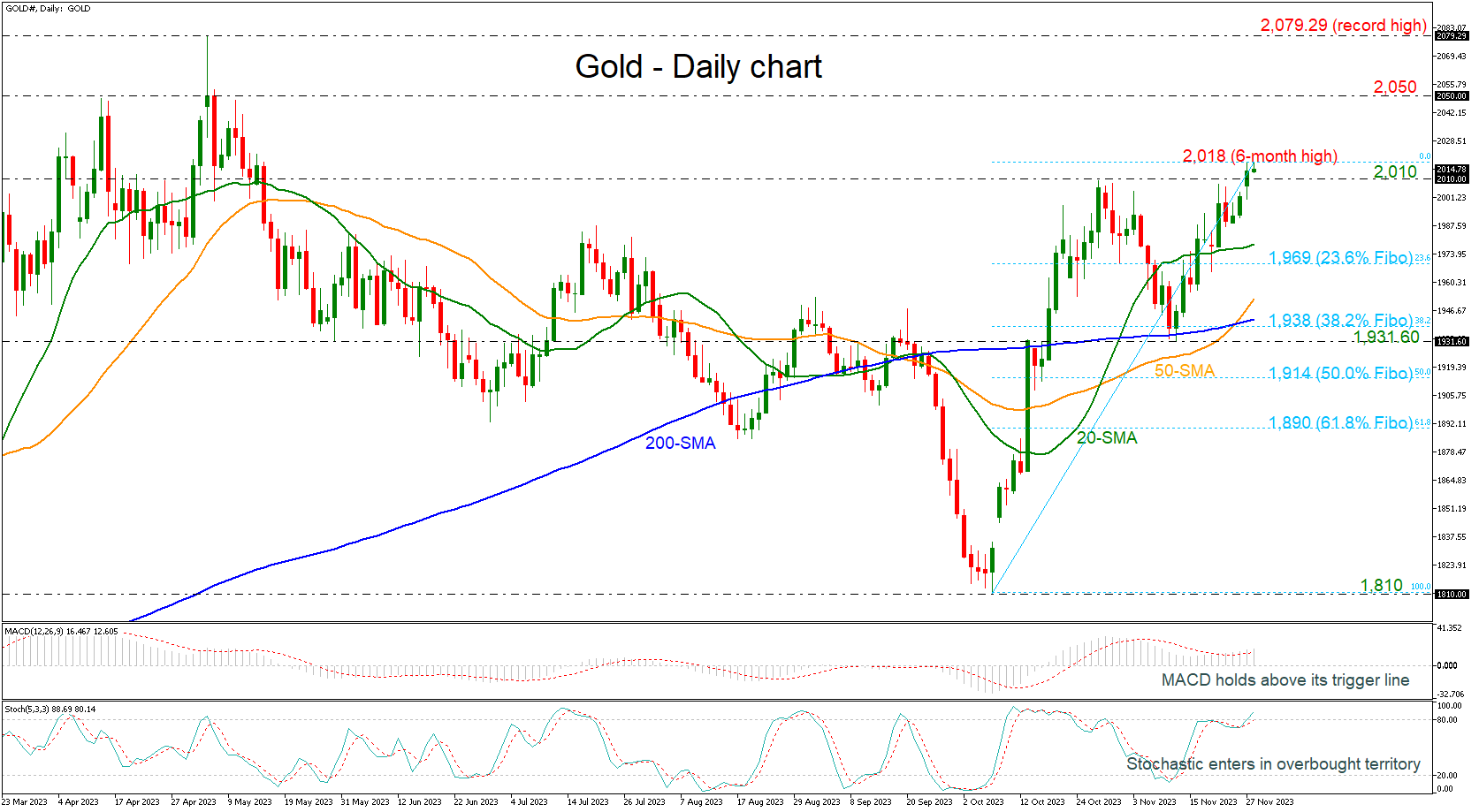

Gold Posts New 6-Month High

- Gold surges in short-term

- Stochastic stands in overbought area, indicating bearish correction

Gold prices are extending their bullish rally towards a fresh six-month high of 2,018, holding well above the simple moving averages (SMAs) in the daily timeframe.

Technically, the MACD oscillator is strengthening its bullish structure above its trigger and zero lines; however, the stochastic oscillator is showing overbought conditions as it is holding above the 80 level, so a bearish correction may be a possible scenario for the next few sessions.

If the market continues to the upside, then it may target the 2,050 resistance level ahead of the record high of 2,079.29, achieved on May 4.

On the other hand, if the bears take control, the yellow metal could move towards the 20-day SMA at 1,978 and the 23.6% Fibonacci retracement level of the upward wave from 1,810 to 2,018 at 1,969. Underneath these lines, the 50- and the 200-day SMAs at 1,952 and 1,942, respectively could come in focus before meeting the 38.2% Fibonacci of 1,938.

All in all, gold is looking strongly bullish in the short-term so the worries may rise for a bearish retracement, according to the stochastic oscillator, before heading higher again.

Dollar Still Looks Vulnerable Short-Term

Markets

European bonds after a hesitant start captured a solid bid yesterday. Markets again raised the odds for an ‘early spring’ ECB rate cut (April 70% chance). ECB’s Lagarde before the European parliament holding a ‘balanced leaning against the wind’-bias clearly didn’t change the intraday momentum, on the contrary. The ECB chair reiterated that it’s not the time to declare victory on inflation and that the medium term outlook on inflation remains considerably uncertain. However, admitting that inflationary pressures will continue to ease only reinforced the markets’ view that the debate from now on will be on the timing of a rate cut. Lagarde also indicated that the ECB will reassess PEPP reinvestment policy in a not too distant future, however with little impact on LT yields for now. German yields declined about 7.0 bps for the 2-y and 30-y.The belly of the curve outperformed (5-y -10 bps). The German 10-y yield again nears recent correction lows just north of 2.50%. US bonds initially lagged the broader rally, as investors awaited the outcome of the 2-y and 5-y Treasury auctions. The 5-y sale was ok. The 2-y sale was less buoyant as bonds already rallied into the sale. Even so, it only caused a temporary blip in the intraday rally. In the end, US yields declined between 8 bps (10-y) and -6.0 bps (2 & 30-y). Lower yields this time didn’t help equities. (Eurostoxx50 - 0.40%, S&P 500 -0.2%). The dollar is struggling to maintain ST support levels. DXY (103.2) closed near last week’s low. USD/JPY dropped from the 149.50 area to close at 148.7. EUR/USD (close 1.0954) nears the 1.0965 resistance.

Asian equities are trading mixed with Japan and Hong Kong underperforming and Korea outperforming. US yields decline marginally as does the dollar, especially against the yen. Today, plenty of central bankers are again scheduled to speak. Regarding the data, the focus is on the US house price data and consumer confidence (Conference Board). With yields again nearing key support (US 10-y 4.34%, German 10-y 2.50% area) the bond rally might slow, but we don’t see a trigger for a U-turn as markets are counting down to the EMU inflation data (tomorrow and Thursday) and the US PCE deflators (Thursday). The dollar still looks vulnerable short-term. A break of 1.0960/65 opens the way to the 1.10 big figure even as we remain cautious on sustained EUR/USD gains further out. UK BRC shop prices (November) this morning eased further (cf infra). For now it didn’t hurt the ST sterling momentum. EUR/GBP 0.8650 (ST neckline) serves as intermediate support.

News & Views

Adobe Analytics forecasts online sales to the tune of $12.4bn on “Cyber Monday”, beating last year’s $11.3bn thanks to new demand and not simply higher prices. Online spending was bigger than a year ago and larger than estimated on Thanksgiving ($5.6bn; +5.5% Y/Y) and Black Friday ($9.8bn; +7.5% Y/Y) as well. Adobe indicated as well that more shoppers are using the “buy now, pay later” formula ($782mn on Monday; +18.8% Y/Y and $7.3bn so far in November; +14% Y/Y). Analysts at Adobe said that the uncertain demand environment pushed retailers to deliver big discounts this season, while also fortifying their e-commerce services with flexible payment methods. Consumers have taken note and spent at record rates despite dealing with rising costs in other parts of their lives.

The British Retail Consortium published its monthly shop price index. Shop price inflation stabilized on a monthly basis, with the annual reading slowing for a sixth consecutive month, from 5.2% Y/Y to 4.3% Y/Y. Details showed a discrepancy between falling non-food (-0.1% M/M & 2.5% Y/Y from 3.4% Y/Y) and rising monthly food prices (+0.3% M/M & 7.8% Y/Y from 8.8% Y/Y). BRC commented that retailers compete fiercely to bring prices down for customers ahead of Christmas. Lower domestic energy prices are also reducing overall input costs. In 2024, retailers face new headwinds from government-imposed increases in business rates to the hidden costs of complying with new regulation. Adding the biggest rise to the National Living Wage on record suggests that especially disinflation in food prices is at risk of stalling or even reversing.

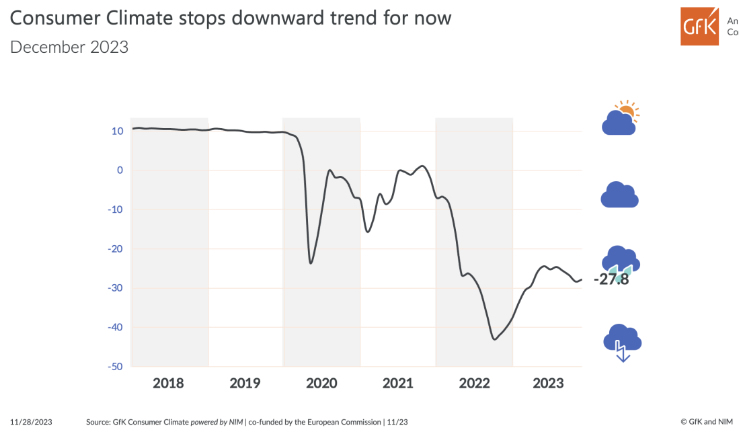

Germany’s Gfk consumer sentiment ticks up to -27.8, mood still characterized by uncertainty and concern

Germany's Gfk consumer sentiment index for December showed a marginal improvement, rising from -28.3 to -27.8, slightly better than expected -28.5. This slight uptick indicates a subtle shift in consumer sentiment as the year ends.

In November, economic expectations had a minor increase from -2.4 to -2.3. However, income expectations dropped from -15.3 to -16.7. There was a slight rise in willingness to buy, from -16.3 to -15.0, while willingness to save decreased from 8.5 to 5.3.

Rolf Bürkl, consumer expert at NIM,noted that "after three consecutive months of decline, consumer sentiment is stabilizing as the year draws to a close."

Despite this stabilization, Bürkl pointed out that consumer confidence remains at a very low level, with no indications of a sustainable recovery in the upcoming months. He emphasized that the overall mood is still "characterized by uncertainty and concern."

Cheap Oil, Low Yields

Monday morning’s rebound in US bond yields didn’t last long; the US sovereign bond yields fell as rapidly as they rose on Monday as a $55bn auction of 5-year US bonds saw strong demand after a weak sale of 2-year bond. The US 5-year bond yield returned to 4.40%, the US 10-year yield also snapped back to 4.40% after an attempt past the 4.50% level earlier, the 2-year yield was under pressure and retreated to 4.87%.

The Fed expectations remain soft and sweet, the falling yields further weigh on the US dollar. The US dollar index is now testing the 103 support to the downside and has given away more than half of gains it recorded between July and October. And the combination of falling long-term yields and cheaper dollar continues to push the price of an ounce of gold higher. This morning, the precious metal trades just shy of the $2020 level. Yet, the upside potential is limited as the US bond rally will likely leave its place to consolidation and correction, the Middle East tensions have been softer over the past few days, and gold is about to step into the overbought territory, while the price of an ounce is at a spitting distance of the ATH of around $2080 per ounce.

Cheaper Oil, lower yields

A deeper fall in oil prices could support a further bond rally. There is a positive correlation between crude oil prices and US 10-year yield. The cheaper the oil, the lower the US 10-year yield, because cheaper oil tames inflation expectations and softens Fed expectations. And oil prices could decline further if OPEC+ fails to deliver a substantial supply cut at their meeting this week. Saudi is reportedly asking other cartel members to reduce their supply to have a powerful impact on oil prices, as it looks clear as the daylight that another 1mbpd cut from Saudi alone won’t even suffice to stabilize prices. The barrel of US crude is down for the 5th consecutive day, it remains offered into the $75pb this morning. Both bulls and bears are waiting in ambush to buy, or to sell, in reaction to what solution OPEC+ will come out this week.

Gasoline prices in the US gasoline prices are down for the 60th straight day. It is good news for the Fed’s inflation battle. It is even better news for Joe Biden’s election campaign.

And there's another noteworthy point: The process of replenishing the US emergency oil reserve is facing delays due to companies holding back on returning the borrowed oil. Shell, Chevron, and TotalEnergies, among nine firms participating in a government oil exchange program over the past two years, were slated to return the oil this year and the next. However, these three companies received approval from the US government to defer the return of approximately 5 million barrels until 2024 and 2025. This indicates that there is no urgency on the part of the US government to replenish these reserves before the upcoming US elections. Full stop.

Yields Drop Further

Market movers today

Another quiet day on the data front. German consumer sentiment and US Conference Board's consumer confidence surveys will be released today.

There will be a range of Fed speakers on the wires today, including Goolsbee, Waller and Bowman.

Overnight, the Reserve Bank of New Zealand (RBNZ) will have a monetary policy meeting, we expect an unchanged rate decision in line with market pricing.

The 60 second overview

Market wrap: Markets are mostly in a wait-and-see mode ahead of Thursday's key inflation data out of the US and the Euro area. Equities have not moved much while US yields dropped further after the European close. EUR/USD moved back up above 1.095 in US trading hours.

US new home sales fall more than expected: The sale of new homes (chart) dropped to 671k in November from 719k in October (revised from 759k). However, it is still above pre-pandemic levels while existing home sales have declined more than 25% compared to 2019 levels hit by the sharp rise in mortgage rates.

Lagarde speech in European Parliament: In her hearing at the EU Parliament yesterday, Christine Lagarde signalled an openness to discussing the reinvestment timeline for the PEPP program in the "not-too-distant future." Several ECB hawks have been vocal in recent months about the need to accelerate the reduction of PEPP reinvestments, but until now, Lagarde has been cautious about opening that debate.

Israel-Hamas extend truce: Israel and Hamas agreed to extend the truce by another two days until Thursday morning as 11 more hostages held by Hamas were freed. More hostages are expected to be freed in the coming days.

China's central bank to support domestic demand with forceful policy: The People's bank of China yesterday said it would use precise and forceful monetary policy "with greater emphasis on cross-cyclical and countercyclical adjustments, enriching the monetary policy toolbox". The signals point to further easing in the pipeline but it may not be in terms of rate cuts but rather more discretionary financial support in troubled areas such as developers and via cuts in the Reserve Requirement Ratio to free up liquidity for lending. We also expect continued fiscal stimulus in order to keep growth close to 5%.

Equities: Equities were slightly lower on Monday in a very quiet session. Both Europe and US surfed closed to the zero-line, despite a 10bp drop in yields. In fact, VIX even rose a little, which is a contrast to the sharp drops in November. Growth- and quality stocks generally beat value and cyclicals beat defensives. However, with a small margin and sector performance was tight. Utilities, retail and real estate were some of the better groups while an odd mix of health care and industrials underperformed. S&P 500 -0.2% and Stoxx 600 -0.3%. Another slow session could be emerging, as US futures are unchanged and Asian markets mixed this morning.

FI: Global yields declined gradually yesterday as markets priced in more rate cuts from major central banks to be delivered in 2024. No single factor appeared to be driving the move. Bund yields closed down by 10bp across the curve, while the 10-year US Treasury yield fell 8bp throughout the session. German ASW spreads widened marginally along with European credit spreads during the day. Markets are now pricing the ECB to cut rates by 88bp next year, up from 80bp last Friday.

FX: EUR/USD consolidated within the mid 1.09-1.10 range after a quiet start to the week. USD/JPY declined below 149 on a strong day for the JPY amid month-end flows. EUR/GBP declined during yesterday's session, trading firmly around the mid 0.86 mark.. Both the SEK and, especially, the NOK appreciated against the EUR, with EUR/SEK at around 11.40 and EUR/NOK declining to around 11.65

Credit: Yesterday, credit markets followed a cautious sentiment while global rates moved downwards across the curves, leaving CDS indices slightly wider with iTraxx Main (+1.5bp) at 69.6bp and iTraxx Xover (+7.6bp) at 382.2bp. In addition, the primary Euro market started the week with a number of new mandates including the pharmaceutical company, Roche Holding AG who priced a total of EUR1.5bn in two tranches with noticeable spread tightening relative to IPT levels.

Nordic macro

No key movers out of the Nordics today.

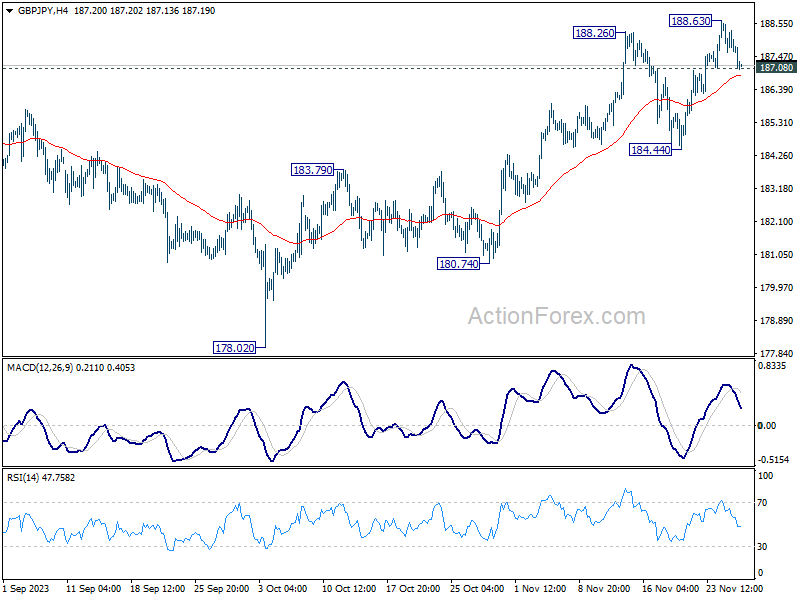

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.39; (P) 187.96; (R1) 188.32; More...

Intraday bias in GBP/JPY is turned neutral again with current retreat. Some more consolidations could be seen below 188.63 temporary top first. But near term outlook will stay bullish as long as 184.44 support holds. Break of 188.63 will resume larger up trend.

In the bigger picture, as long as 184.44 support holds, larger up trend from 123.94 (202 low) should still be in progress, next target is 195.86 (2015 high). However, firm break of 184.44 will now argue that a medium term top is formed, possibly in bearish divergence condition in D MACD, and bring deeper fall back to 178.02 support.