Sample Category Title

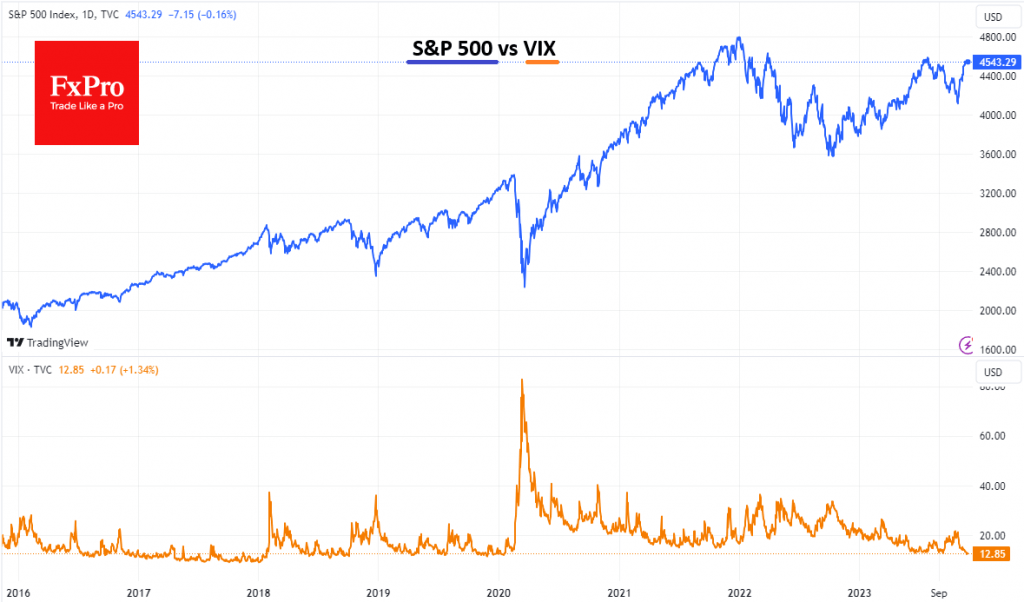

VIX Drop: Stocks Collapse or Boring Growth Ahead?

Financial market volatility has plunged to its lowest level in almost four years, according to the VIX index. This so-called “fear index” fell to 12.45 on Friday, the lowest level since January 2020. Such low levels could be both a sign of the market entering a smooth bullish trend or a lull before a sharp decline.

Low VIX values indicate weak expected market volatility in the coming months.

Sometimes, such market signals should be perceived as overconfidence by investors. And then, the calm is followed by a storm wave, knocking down everything in its path. The peak of overconfidence is usually followed by bitter disappointment in the form of a painful sell-off in stocks.

This can be a period of quiet growth in stocks. And while bears should be prepared for a reversal in stocks, they should not be in a hurry to make a quick bet on it because a rally in stocks can take an indefinitely long time while the VIX is at such low levels.

The VIX has spent most of June and July this year in the range between 13 and 14, and the S&P500 has added nearly 7.5% during that time. The S&P500 gained twice as much between October 2019 and January 2020, when we saw similar or lower VIX levels. Moreover, the VIX spent all of 2017 and early 2018 mostly below 12, dipping to 9.5 at times, and this was also a period of smooth, persistent 27% gains for the S&P500.

Thus, stocks are now close to a point where there could be both a painful switch into risk-off mode and the start of a long and boring uptrend for speculators.

In the short term, we see more bearish signals for the market as the last upside momentum in equities was extremely sharp. It looks like the market driver was closing shorts rather than building long positions. A similar amplitude rally in equities has been a sign of a reversal to growth in recent years with monetary easing, but now the pause is more of what the markets are hoping for, but the Fed is not confirming those hopes.

Sunset Market Commentary

Markets

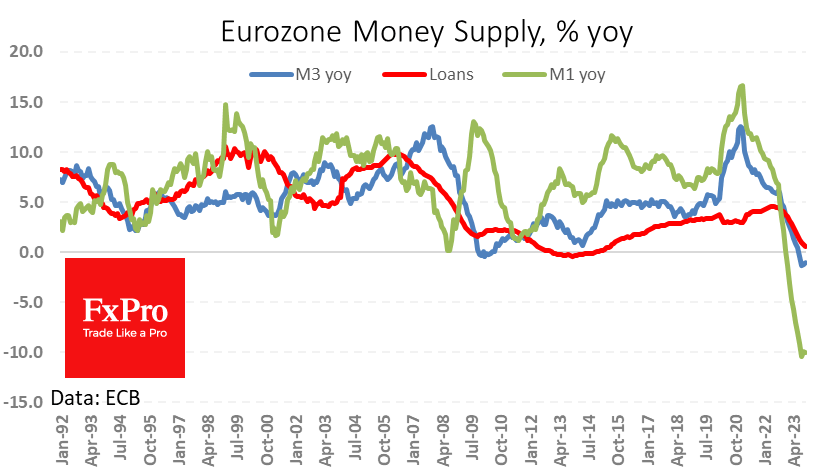

With few important data on the agenda, trading on US and EMU (bond) markets was mainly order driven and technical in nature. At the start of the session, Bunds tried to extend their recent rally, but the move soon stalled. ECB’s Nagel airing that its too early to speculate about rate cuts hardly can be considered as ‘news’. In a sign to recent moves, he also said that not only the level of interest rates matters, but also expectations about the future path. ECB monetary data showed a further slowdown in M3 money supply (-1.0% Y/Y). Monetary tightening also feeds into credit availability. Loans to households slowed to 0.6% Y/Y in October from 0.8%. Loans to non-financial corporates even dropped below last year’s level (-0.3% Y/Y from 0.2%). However, this is exactly what policy tightening is aiming for. After a brief up-tick early in US dealings, German yields are currently ceding between 4 bps and 1 bp (30-y). The 10-y German yield (2.53%) is holding above the 2.50% support. Tomorrow’s German inflation and Thursday’s EMU CPI will help bring clarity whether or not the recent decline in yields has run its course. Intra-EMU spreads halted their recent tightening as the ECB (Lagarde yesterday, Nagel today) flagged it intends starting to reduce PEPP bond holdings well before end 2024 as currently guided. The 10-y Italian spread vs German widens 5 bps today. US yields show a similar picture as EMU counterparts (2-y -4 bps, 30-y unchanged). US house price data (S&P Corelogic CS 20 city at 0.67% M/M and 3.92% Y/Y) were close to expectations. After finishing this report, US consumer confidence (conference Board) was stronger than expected, but with a downward revision to the October figure. Tonight, the US Treasury sells $39bn of 7-y Notes. Equity markets yesterday to some extent ‘decoupled’ from bond markets and ran into resistance. This tentative topping out process continued today. The EuroStoxx 50 is losing about 0.5%. The 4400/4491 resistance probably remains a high hurdle even after the recent easing on interest rate markets. The US S&P 500 index opened 0.15% lower. Brent oil hovers near $80/b. Rumours from ‘informed sources’ say that the OPEC+ cartel still hasn’t reached an agreement on output levels.

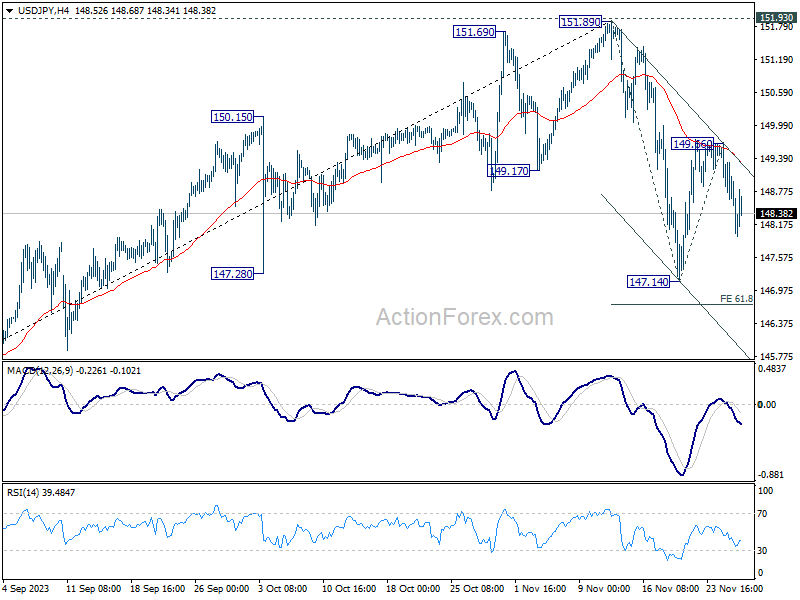

On FX markets the dollar is still looking for a bottom on its recent setback. EUR/USD (1.0980) is breaking the 1.0960/65 resistance. DXY is setting a minor correction low below 103.18, but follow-trough price action stays modest for now (103.0). USD/JPY (148.3) holds in the ST 147.15/149.75 corridor. Sterling’s recent outperformance halted today, with EUR/GBP at 0.868, holding above the 0.8650 ST neckline.

News & Views

The ECB published results of its twice-yearly Survey on the Access to Finance of Enterprises (SAFE) in the euro area, covering the period from April to September. Firms signaled a continued increase in turnover, while higher labour, production and interest costs weighed on their profitability (net deterioration of -14% compared with previous survey). They expect non-labour input costs to increase by 6.1% over the next 12 months with employees’ wages up 4.3% (from 5.4% in previous survey). Selling prices are projected 3.7% higher in the year-ahead (from 6.1%). Average employment is still forecast to increase (1.7% average) The financial vulnerability indicator, which provides a comprehensive picture of firms’ financial situation, suggests that 9% of EMU enterprises encountered major difficulties in running their business and servicing their debts over the past six months, a level last seen during the Covid-19 pandemic. Looking ahead, firms expect a decline in the availability of all external financing sources, and especially bank loans. This suggests that part of the transmission of monetary policy to firms’ financing conditions is still in the pipeline.

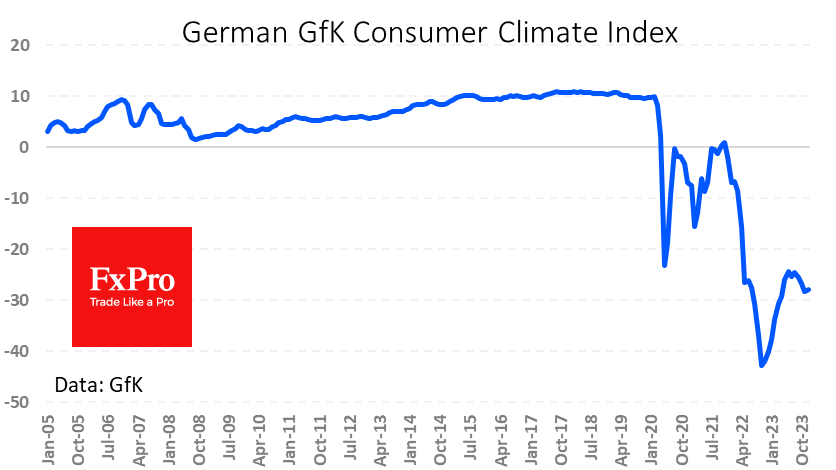

German GfK consumer confidence bounced back slightly in December (-27.8 from -28.3) after hitting a 7-month low in November. The slight increase in consumer sentiment results from the decrease in willingness to save this month from 8.5 to 5.3 points. GfK reacted that consumer sentiment is stabilizing as the year draws to a close, but continues to be at a very low level with no signs of a sustainable recovery in the coming months. French consumer confidence increased from 84 to 87 in November, the highest level since April 2022. Details showed consumers turning less pessimistic on their future personal financial situation and standard of living, while they do fear an increase in unemployment.

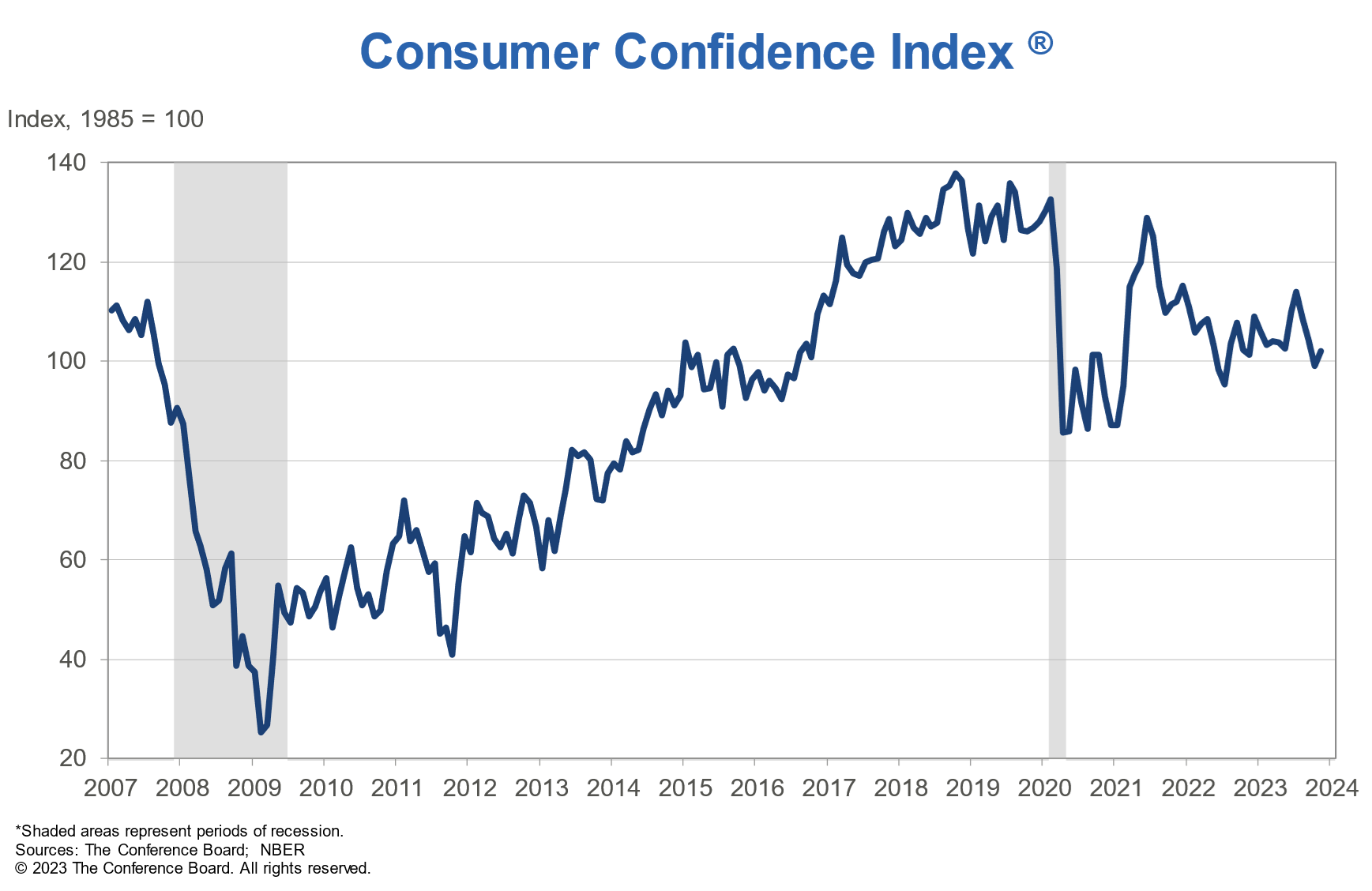

US consumer confidence rose to 102, but expectations index still point to recession

US Conference Board Consumer Confidence rose from 99.1 to 102.0 in November, above expectation of 101.0. Present Situation Index ticked down slightly from 138.6 to 138.2. Expectations Index rose from 72.7 to 77.8. Expectations Index remains below 80 for a third consecutive month—a level that historically signals a recession within the next year.

"Consumer confidence increased in November, following three consecutive months of decline," said Dana Peterson, Chief Economist at The Conference Board. "This improvement reflected a recovery in the Expectations Index, while the Present Situation Index was largely unchanged. November's increase in consumer confidence was concentrated primarily among householders aged 55 and up; by contrast, confidence among householders aged 35-54 declined slightly. General improvements were seen across the spectrum of income groups surveyed in November. Nonetheless, write-in responses revealed consumers remain preoccupied with rising prices in general, followed by war/conflicts and higher interest rates."

BoE Haskel: Rates have to be held higher and longer than many expecting

BoE MPC member Jonathan Haskel, in a speech, delivered a clear message about the UK's interest rate policy. Addressing the possibility of cutting interest rates in the near future, Haskel's response was a definitive "no."

He substantiated this viewpoint by referring to the ongoing tightness in the labor market, a crucial factor in determining monetary policy.

Haskel noted that the labor market remains "historically tight", and based on current trends, it would take "at least a year" to return to the average tightness levels seen before the pandemic.

Further emphasizing his stance, Haskel stated "rates will have to be held higher and longer than many seem to be expecting."

FX Market Temporarily Looking Past Weakness in Euro Area Data

Worrying news on the Eurozone economy continues to come in, although this is not hurting the single currency so far, which is trading at fifteen-week highs at 1.0950.

Germany’s business climate index rose from -28.3 to -27.8 in December but remains deeply negative. According to the report, Germans expect their incomes to decline slightly. Their propensity to spend is picking up slightly due to entrenched inflation expectations, but they struggle to reflect a rebound in consumer activity.

A separate report from the ECB noted a slowdown in loan growth in the eurozone to 0.6% y/y – the slowest in 8 years. However, the worst is apparently ahead for the indicator, judging by the dynamics of monetary aggregates. Trends in monetary aggregates M1-M3 are generally more than a year ahead of credit trends.

Monetary aggregate M1 is now 10% lower than a year earlier. It has been in negative territory so far this year. M3 in October was 1% lower than a year ago. In both cases, it is stabilising near historic lows, reflecting tightening financial conditions.

EURUSD’s strength is now driven by high hopes for a Fed rate cut soon, but the weakness in Eurozone indicators should set the mood that a policy change from the ECB could be earlier and deeper, not saying that the US already has higher rates. This is a long-term negative for the single currency. However, markets prefer to play down US policy changes first.

NZD/USD Eyes RBNZ Rate Meeting

- RBNZ likely to maintain rates at 5.5%

- US CB Consumer Confidence expected to fall

The New Zealand dollar posted slight gains earlier on Tuesday but has recovered. In the European session, NZD/USD is trading at 0.6101, up 0.07%.

RBNZ expected to hold rates

The Reserve Bank of New Zealand meets on Wednesday and is likely to maintain the cash rate at 5.5% for a fourth straight time. The central bank’s stance appears to be one of “higher for longer”, which will provide policy makers the flexibility to raise or lower rates as needed.

The RBNZ’s stance does not dovetail with the market view that rate cuts could come as early as May 2024. Inflation is falling and the labor market is slowing down, and the markets are betting that this trend will continue and allow the RBNZ to trim rates.

This makes Wednesday’s meeting quite interesting, not so much as to the rate decision but to how strongly Governor Orr pushes back against market expectations of rate cuts. The RBNZ said in October that rates might need to stay higher for longer in to bring inflation back down to the 1%-3% target, but a more forceful message may be needed to send the message that rate cuts are not around the corner. Orr’s press conference and updated forecasts will be opportunities to counter market expectations and present a hawkish stance on rate policy.

The US releases Conference Board Consumer Confidence later today. Consumer confidence has been falling and the downtrend is expected to continue, with a market consensus of 101.0, down from 102.6. We’ll also hear from a host of Fed members during the day, which could provide some insights into the Fed’s plans for the December meeting..

NZD/USD Technical

- NZD/USD is putting pressure on resistance at 0.6121. Above, there is resistance at 0.6167

- There is support at 0.6053 and 0.5996

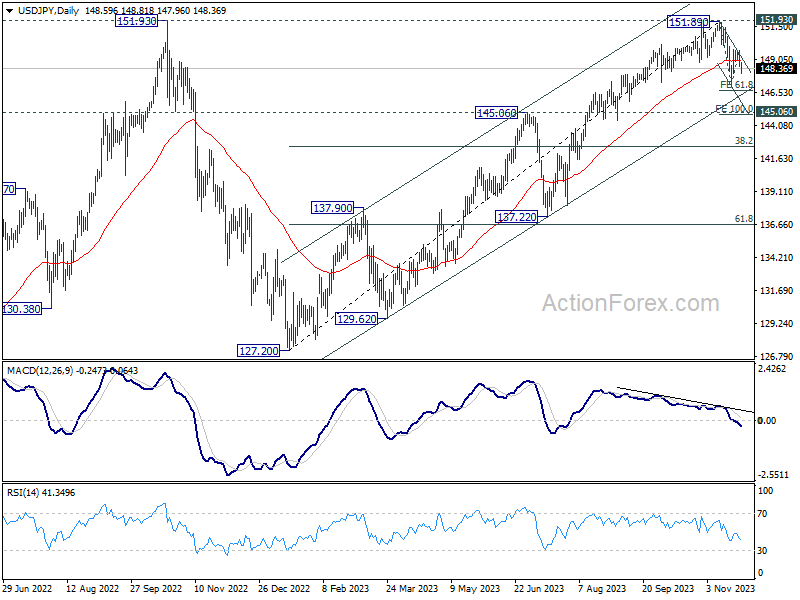

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.26; (P) 148.97; (R1) 149.40; More...

Intraday bias in USD/JPY remains on the downside for the moment. Fall from 151.89 should be resuming, and should target 147.14 support first. Further break of 61.8% projection of 151.89 to 147.14 from 149.66 at 146.72will pave the way to 100% projection at 149.91, which is close to 145.06 key resistance turned support. For now, risk will stay on the downside as long as 149.66 resistance holds, in case of recovery.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

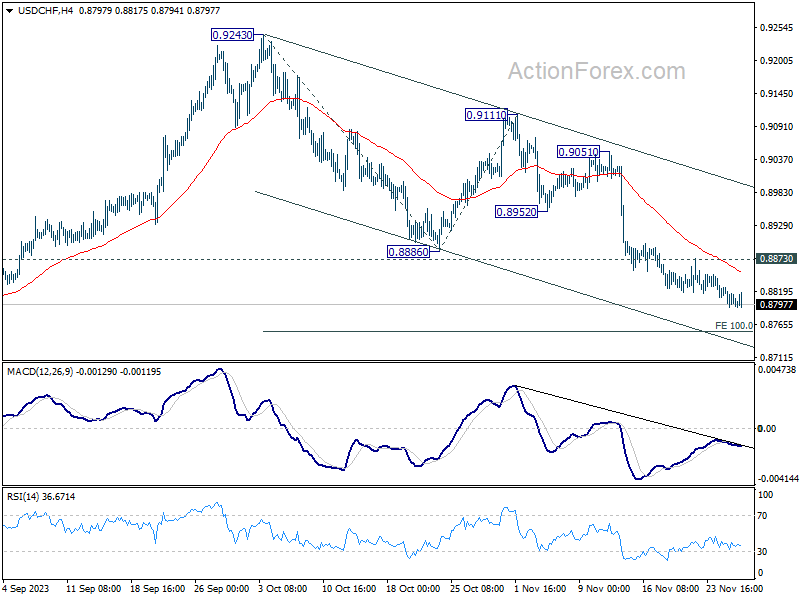

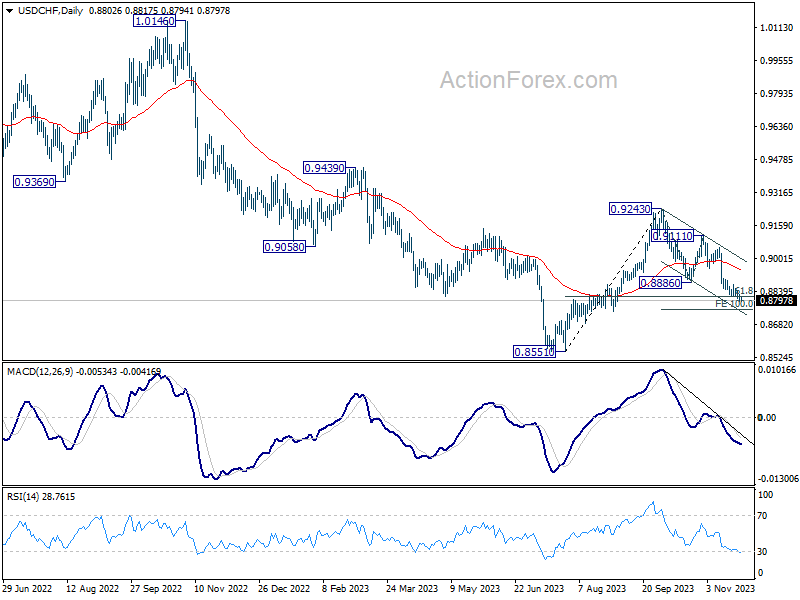

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8790; (P) 0.8809; (R1) 0.8824; More....

No change in USD/CHF's outlook and intraday bias stays on the downside. Current fall from 0.9243 should target 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754 next. Nevertheless, break of 0.8873 resistance will turn bias to the upside for stronger rebound.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. 61.8% retracement of 0.8551 to 0.9243 at 0.8815 was already met. Sustained break there will bring retest of 0.8551 low. For now, this will remain the favored case as long as 0.9111 resistance holds.

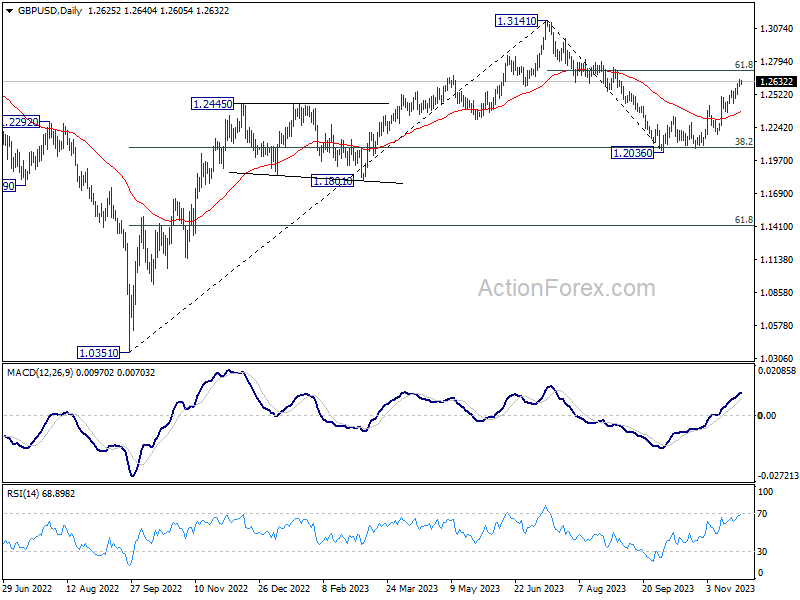

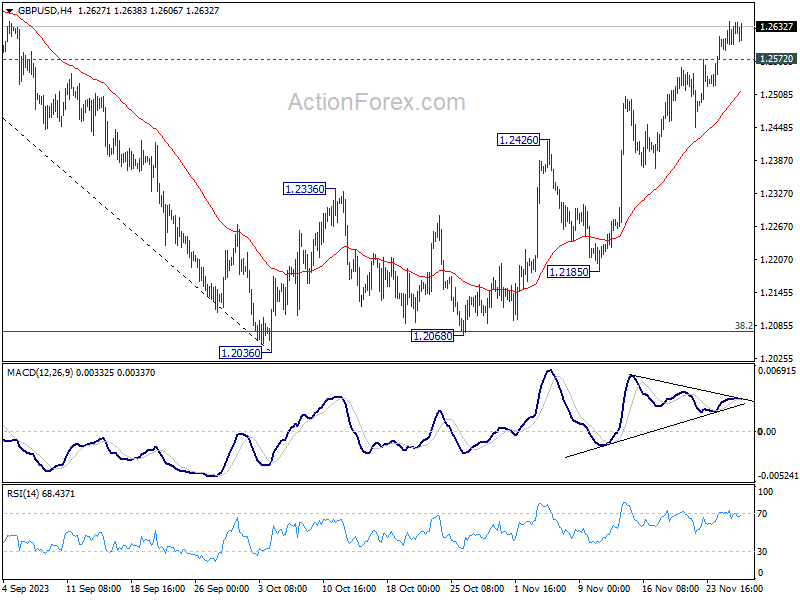

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2597; (P) 1.2621; (R1) 1.2650; More...

Intraday bias in GBP/USD stays on the upside for the moment. Current rise from 1.2036 should target 61.8% retracement of 1.3141 to 1.2036 at 1.2716. Upside could be capped there on first attempt, on loss of momentum as seen in 4H MACD. On the downside, below 1.2572 minor support will turn intraday bias neutral and bring consolidations. But further rally will remain in favor as long as 1.2426 resistance turned support holds.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.