Sample Category Title

Overstretched

The US bonds extended their rally ladies and gentlemen, as one of the Federal Reserve’s (Fed) most hawkish members, Christopher Waller, said in a speech named ‘Something appears to be giving’ that he is ‘increasingly confident that policy is currently well positioned to slow the economy and get inflation back to 2%’. The Chicago Fed President said that the slowdown in inflation has been the biggest such drop in 71 years, while NY Fed President John Williams said that the decline was indeed encouraging. No one mentioned the falling yields, and the possibility that it could be a challenge for the Fed’s tightening. So the dovish comments from the Fed members sent the US 2-year yield below this month’s critical support of 4.80%. The 2-year yield has slipped below 4.70% this morning. The 10-year yield fell below 4.30%. The dollar index tumbled to the lowest levels since August, as gold rallied past the $2050 level this morning on the back of a broadly softer US dollar and tumbling US yields – which decrease the opportunity cost of holding the non-interest-bearing gold and makes gold more attractive to hold.

The US dollar’s selloff also echoed across the global FX markets. The EURUSD traded above the 1.10 psychological level this morning, Cable hit 1.27, and the USDJPY tipped a toe below the 147 level and below its 100-DMA.

Note that we have a few technical levels across currencies and commodities that are being tested as a result of a significant meltdown in the US yields – which are the most popular indication of the safe rate on which investors could build their risk/return models. And when the yields go down, investors accept lower return, or higher risk elsewhere.

Elsewhere is everywhere: options in Gamestop see wild volumes in recent days, it appears that investors expect the stock to rally by 50% in little more than a week from now. Most positions have recently been opened and small, meaning that the market optimism now vacuum retail traders in – and it’s the ultimate signal that the rally is overstretched. At the current levels, the US bonds are approaching overbought market, the US dollar has stepped into the oversold territory, gold is overbought, the euro and the pound are overbought against the dollar, and the S&P500 – which barely gained amid yesterday’s bond rally – is also in the oversold territory. The RSI indicators across most asset classes are screaming that it’s time for correction. Fundamentally, the only thing that could push the US yields lower from the current levels is increased evidence that the US economy is going to experience a hard landing – which would then justify the actual market pricing that the Fed will cut the rates by 100bp next year.

Other than the Fed

Many central bankers from around the world also spoke in an event in HK this week, and their assessment of monetary policies was less – say – optimistic than their Fed peers. The European Central Bank’s (ECB) Joachim Nagel for example repeated that it’s premature to even talk about rate cuts in Europe as there is certainly a ‘bumpy road ahead’ for inflation on the old continent. A policymaker at the Bank of England (BoE) warned that the services inflation in the UK remains sticky and that inflation becomes more ‘home-grown’ and will be challenging to squeeze out of the system, Reserve Bank of Australia’s (RBA) Michelle Bullock had also mentioned the same thing less week. And the Reserve Bank of New Zealand (RBNZ) kept the rates unchanged today – as expected – but repeated that the policy will remain restrictive for some time to tame inflation.

Globally, we see a growing divergence between the Fed members – which sound more dovish than in the previous weeks – and the other major central bankers – which maintain their hawkish stance regarding their rate policy. But the US economy is in a stronger position to withstand higher rates than the European economies, and inflation in the US could prove to be ‘volatile’ in the next quarters. Therefore, the selloff in the US dollar seems overstretched, and correction is certainly on the menu for December.

Data-wise, have a look at the latest US GDP update today and at the latest European inflation updates between today and tomorrow. The US GDP data is expected to confirm a nearly 5% growth in Q3 with an amazing 4% growth on consumer spending and inflation in Europe is expected to continue to ease. Keep in mind that a robust US growth is positive for the USD, and softening inflation is negative for the euro.

In energy, US crude rebounded past $76pb, but gains remain timid as the latest news suggest that Angola and Nigeria continue to resist to Saudi’s demand for a joint effort to reduce supply and that there is a chance that the OPEC meeting, which is rescheduled to tomorrow, could be delayed again. Any further delay could trigger another selloff in oil prices in the second half of this week.

Focus on German and Spanish inflation

Market movers today

In the euro area, today's main focus will be on preliminary inflation data from Germany and Spain. The November figures will give markets the first sense of what to expect from the euro area HICP which is due for release tomorrow.

In Sweden, October retail sales and NIER consumer confidence will be released.

In the US, the 2nd estimate of Q3 GDP will be released in the afternoon, and the Fed's Barkin and Mester will be on the wires in the evening.

Overnight, Chinese NBS PMIs are due for release for November. Generally, most indicators suggest we are likely to see either flat or moderately improving numbers.

The 60 second overview

Euro area: Credit to the private sector in the euro area continues to be weak and was the main weak point for ECB in the monetary aggregate release yesterday. The decline in loan growth continued with the loans to NFC decreasing by -0.3% in Oct. Loans to households grew by 0.6% in Oct (-0.2pp from Sep).

US: The US' Conference Board consumer confidence released weakened slightly in November. The labour market indicators gave somewhat mixed signals as both the 'jobs plentiful' and the 'jobs hard-to-get' index rise at the same time (usually these would move in opposite directions). Promisingly for the Fed however, inflation expectations return back to a declining trend (5.7%; from 5.9%).

NZ: Overnight the RBNZ kept policy rates unchanged yet signalled that they may hike rates in 2024 if inflation do not decelerate quickly enough.

Geopolitics: Yesterday, we published a new Research article where we discuss the political and economic relations in the Middle East. The piece is less about the day-to-day developments in the Gaza war and more about the long-standing religious and ideological rifts in a region that is often referred to as powder keg. Despite the temporary ceasefire between Israel and Hamas, we think the risk of escalation remains. Moreover, we think there is a risk that bottled tensions in the region explode, potentially leading to a scenario similar to Arab spring. We highlight that broader social unrest or political instability in the region could have severe implications globally, and that here, the West also has a lot at stake. International investors and corporates should be aware of the geopolitical risks related to Middle East, particularly since the Gulf states have grown to become increasingly important partners for the West, both in trade and in politics. Read more in Research Global: The Middle East unveiled - how a regional storm could ignite global flames, 28 November.

Equities: Equities closed somewhat higher, recovering at the end of the session, driven by falling yields. US closed up 0.1% but Europe down -0.3%. Interestingly, a new drop in yields were not enough to whip new risk appetite into equities. Cyclicals and growth admittedly outperformed, but not by a huge margin. Industrials were even a tad lower for the session. One explanation is that we are approaching a point where weakness in macro (and thereby yields) could even be interpreted negatively in equity markets again. Another explanation is that the drop in yields reiterates that bond volatility remains too high, which is typically disliked among investors. US futures are a notch higher this morning but Asian markets lower.

FI: European bond market was virtually unchanged for most of the day, yet in the afternoon a 5bp rally across the sub 10y segment occurred following dovish interpreted remarks from Fed's Waller saying monetary policy is well positioned. 10s30s steepened as the 30y only ended 2bp lower. 10y Bunds ended just below the 2.5% mark, which is the lowest since late August. Markets added 10bp of ECB rate cut expectations to 2024 and have now 4 full 25bp cuts priced for 2024.

FX: EUR/USD briefly breached the 1.10 mark but mostly traded just below as the USD weakened against most G10 currencies, hitting a three-month low against most major currencies. USD/JPY fell below 148, while EUR/GBP remained around the mid-0.86 mark. EUR/SEK declined to below 11.40, while EUR/NOK mostly traded below 11.70.

Credit: Credit markets turned around late yesterday, iTraxx Main went 1.4bp lower to 68.2bp while iTraxx Crossover went 4.8bp lower to 377.3bp. The new issue activity across the Nordic market remains busy demonstrated by deals in SEK from Gettinge AB, Stockholm Exergi and Volkswagen Financial Services. In the broader Euro primary market Piraeus Bank, Mediobanca, Hamburg Commercial Bank, Electricite de France and Lottomatica were active with benchmark transactions. We see a constructive investor appetite as we observe sizeable spread compression in most deals relative to the initial price indications.

Nordic macro

No key movers out of the Nordics today

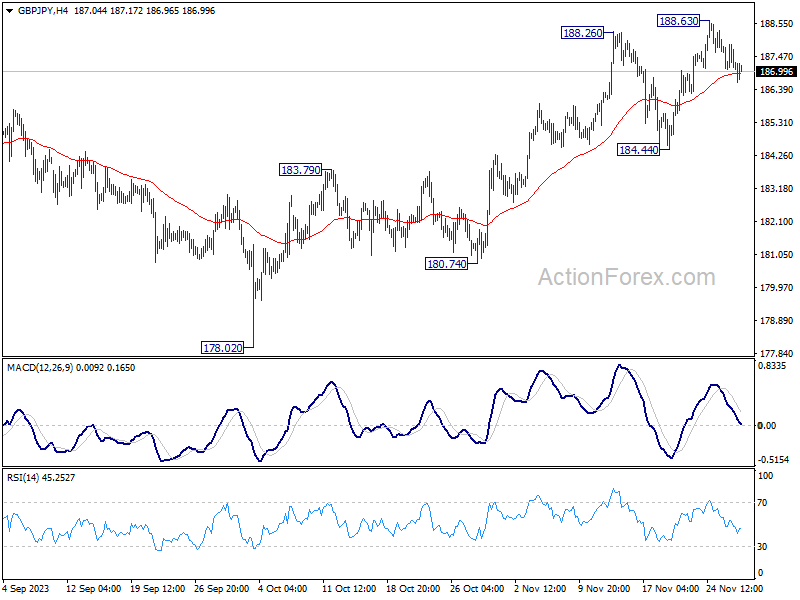

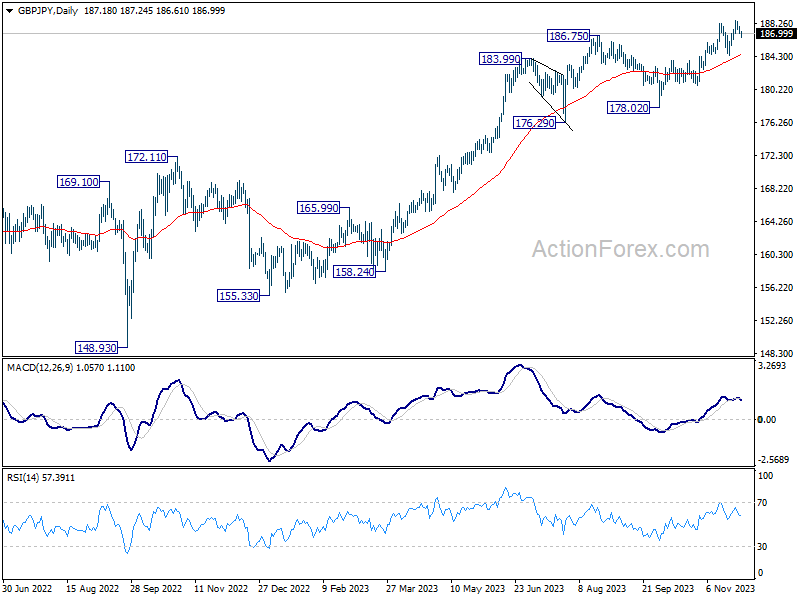

GBP/JPY Daily Outlook

Daily Pivots: (S1) 186.91; (P) 187.39; (R1) 187.73; More...

Intraday bias in GBP/JPY remains neutral for the moment, and some more consolidations could be seen below 188.63. While deeper retreat cannot be ruled out, near term outlook will stay bullish as long as 184.44 support holds. On the upside, break of 188.63 will resume larger up trend.

In the bigger picture, as long as 184.44 support holds, larger up trend from 123.94 (202 low) should still be in progress, next target is 195.86 (2015 high). However, firm break of 184.44 will now argue that a medium term top is formed, possibly in bearish divergence condition in D MACD, and bring deeper fall back to 178.02 support.

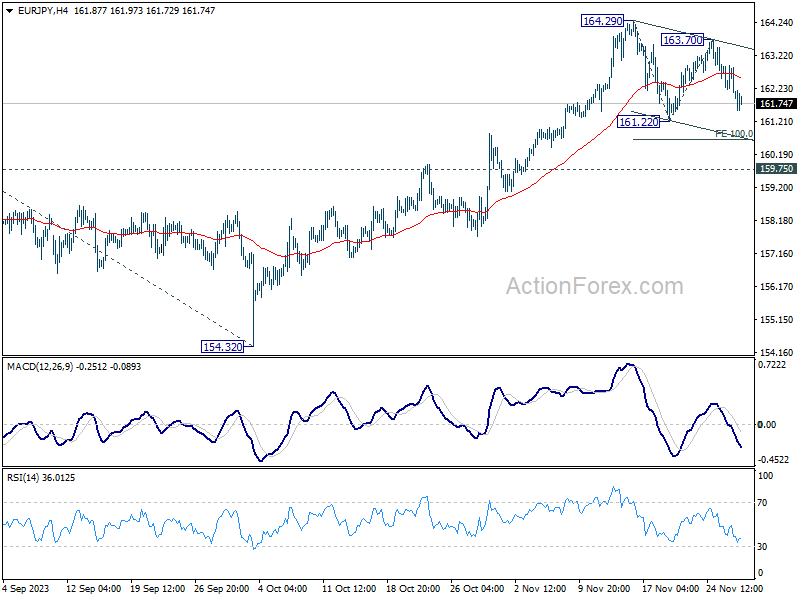

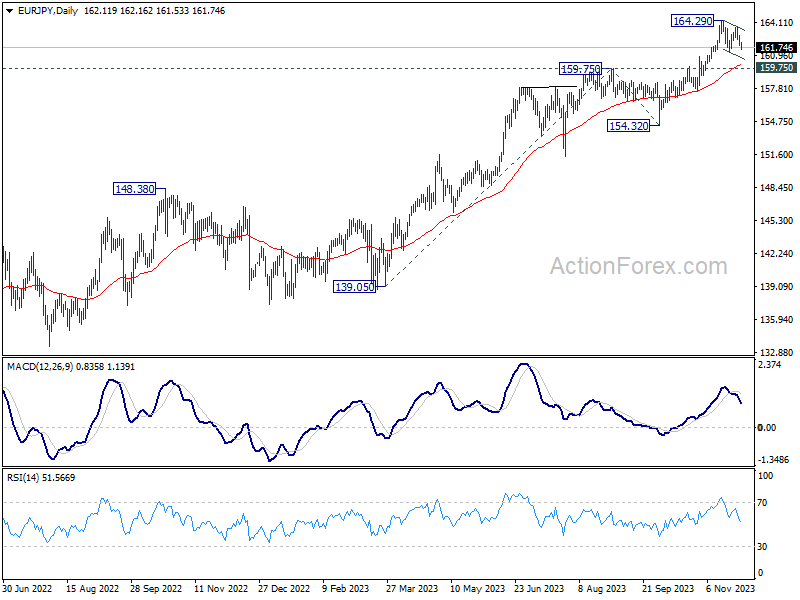

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.72; (P) 162.35; (R1) 162.78; More....

Intraday bias in EUR/JPY remains on the downside at this point. Corrective fall from 164.29 is in progress and deeper decline should be seen to 100% projection of 164.29 tot 161.22 from 163.77 at 160.63 and possibly below. But strong support should be seen from 159.75 resistance turned support to bring rebound. Nevertheless, for now, risk will stay on the downside as long as 163.70 resistance holds, in case of recovery.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 169.96 (2008 high). On the downside, break of 159.75 resistance turned support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish even in case of deep pullback.

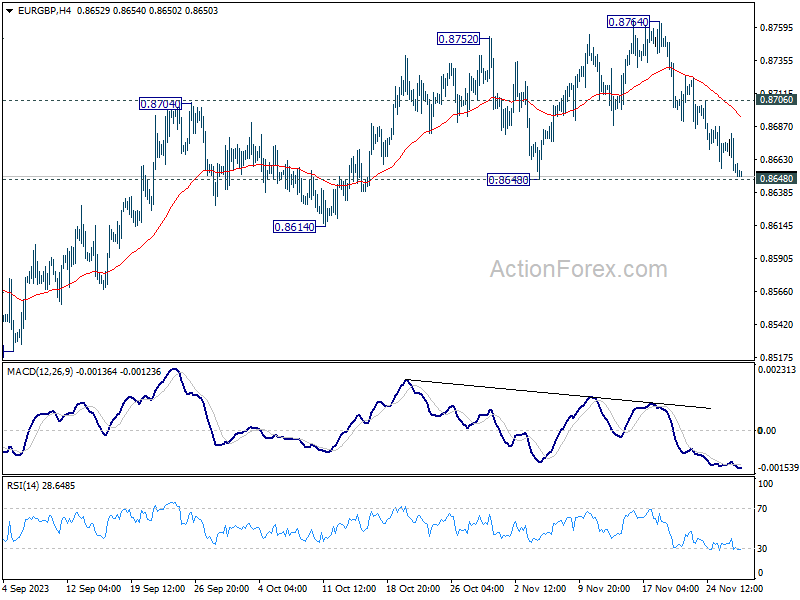

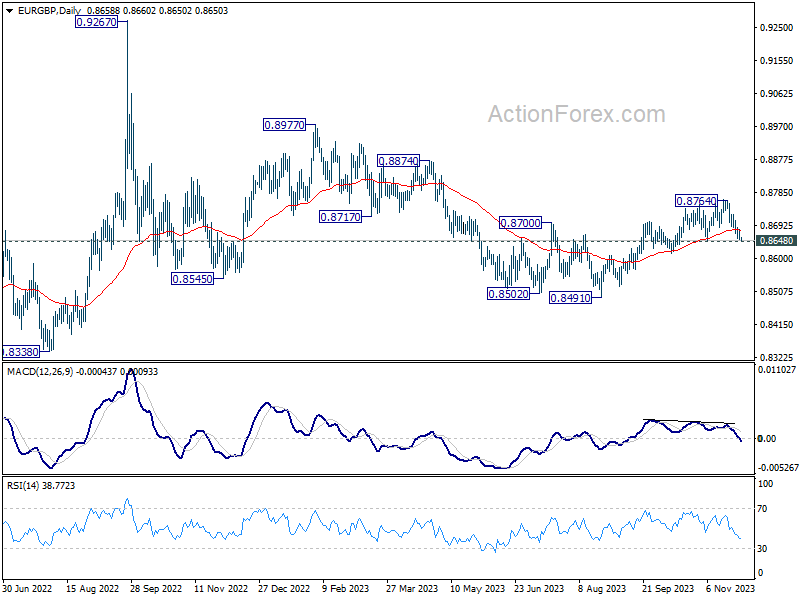

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8649; (P) 0.8666; (R1) 0.8678; More....

No change in EUR/GBP's outlook. Intraday bias stays on the downside at this point. Decisive break of 0.8648 support will argue that whole rise from 0.8491 has completed and turn near term outlook bearish. Nevertheless, break of 0.8706 minor resistance will retain near term bullishness and bring retest of 0.8764 instead.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. However, firm break of 0.8648 support will dampen this view, and open up the case for another medium term decline through 0.8941.

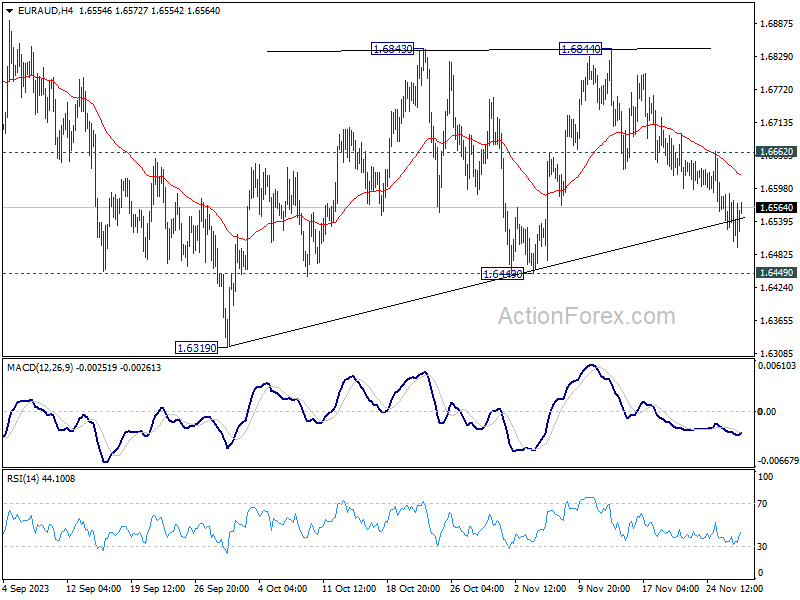

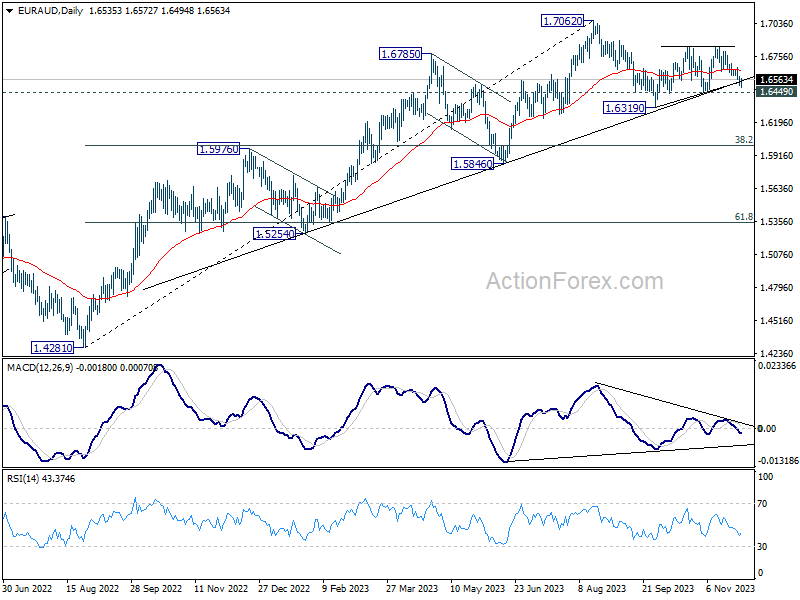

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6499; (P) 1.6546; (R1) 1.6582; More...

Further decline is expected in EUR/AUD with 1.6662 resistance intact. Firm break of 1.6449 support will argue that the pattern from 1.6319 has completed at 1.6844 as a corrective move, and fall from 1.7062 is ready to resume through 1.6319. On the upside, above 1.6662 minor resistance will turn bias back to the upside for 1.6844 resistance instead.

In the bigger picture, while 1.7062 is a medium term top, there is no clear sign of trend reversal as EUR/AUD continues to draw strong support from the medium term trend line. Break of 1.7062 will resume the larger up trend from 1.4281 (2022 low) to 1.7691 fibonacci level. Nevertheless, break of 1.6449 support will argue that deeper correction is underway to 38.2% retracement of 1.4281 to 1.7062 at 1.6000.

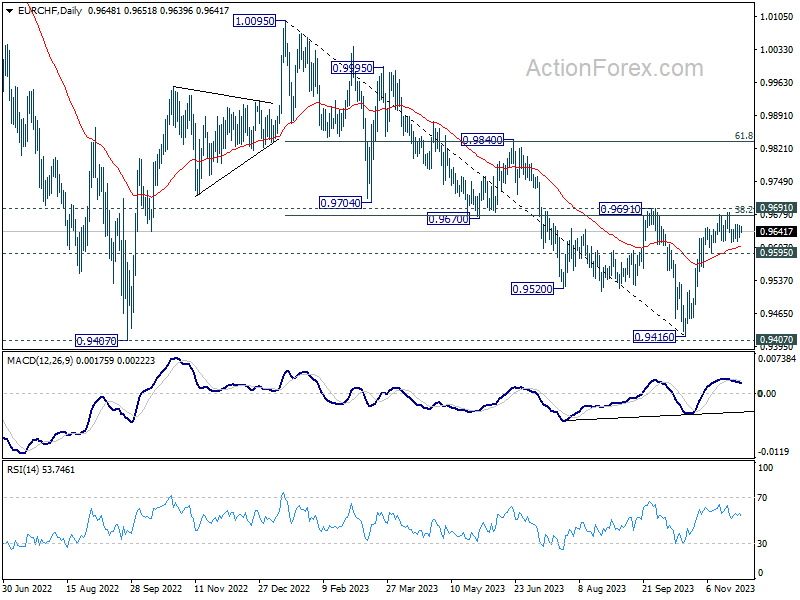

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9638; (P) 0.9647; (R1) 0.9663; More...

Intraday bias in EUR/CHF remains neutral as it's still stuck in sideway trading. Overall, further rally is expected with 0.9595 support intact. Decisive break of 0.9691 resistance will carry larger bullish implication, and target 0.9840 resistance next. However, break of 0.9595 support will turn bias back to the downside for deeper pull back.

In the bigger picture, fall from 1.0095 (2023 high) might have completed at 0.9416, just ahead of 0.9407 support (2022 low). Sustained break of 0.9691 cluster resistance (38.2% retracement of 1.0095 to 0.9416 at 0.9675) will pave the way to 61.8% retracement at 0.9836 and above. However, rejection by 0.9691 will maintain medium term bearishness for another test on 0.9407 at least.

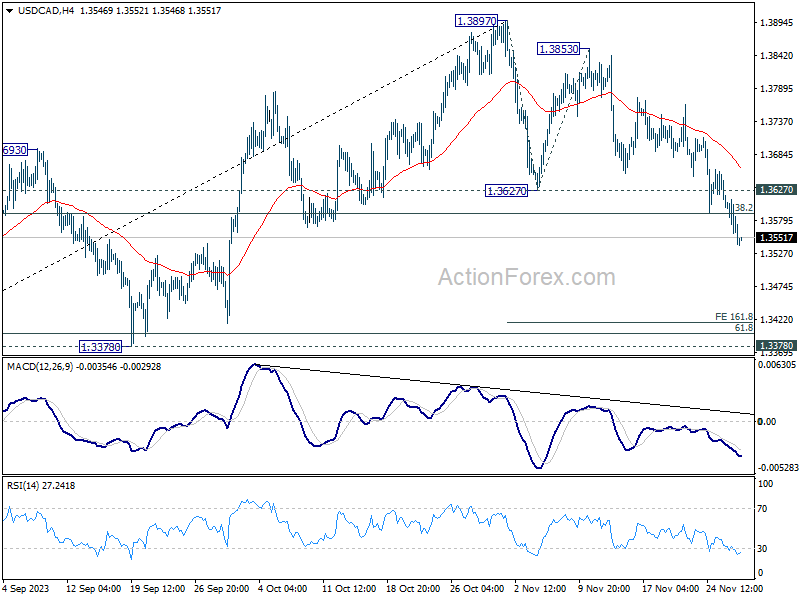

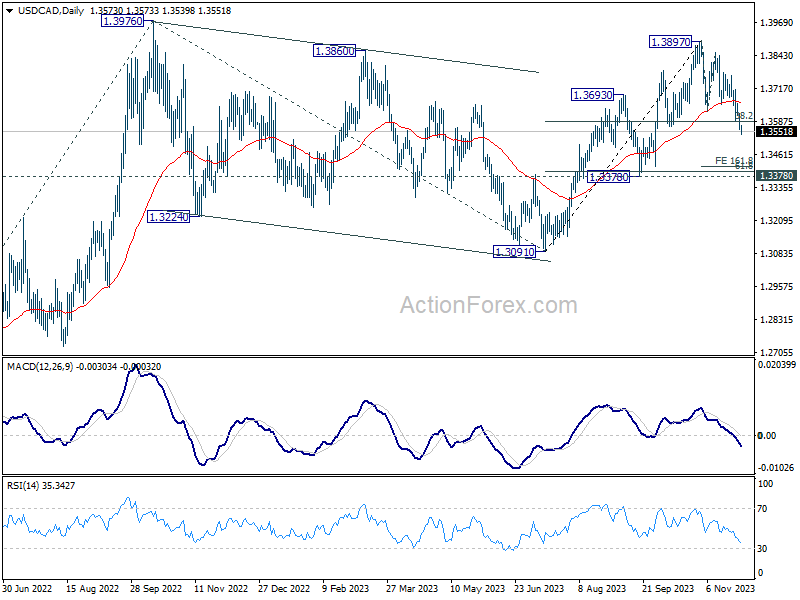

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3547; (P) 1.3585; (R1) 1.3610; More...

USD/CAD's decline extends today and the break of 38.2% retracement of 1.3091 to 1.3897 at 1.3589 indicates deeper correction is underway. Intraday bias remains on the downside. Next target is 161.8% projection of 1.3897 to 1.3627 from 1.3853 at 1.3416. On the upside, above 1.3627 support turned resistance will turn intraday bias neutral and bring recovery first.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will remain the favored case as long as 1.3378 support holds.

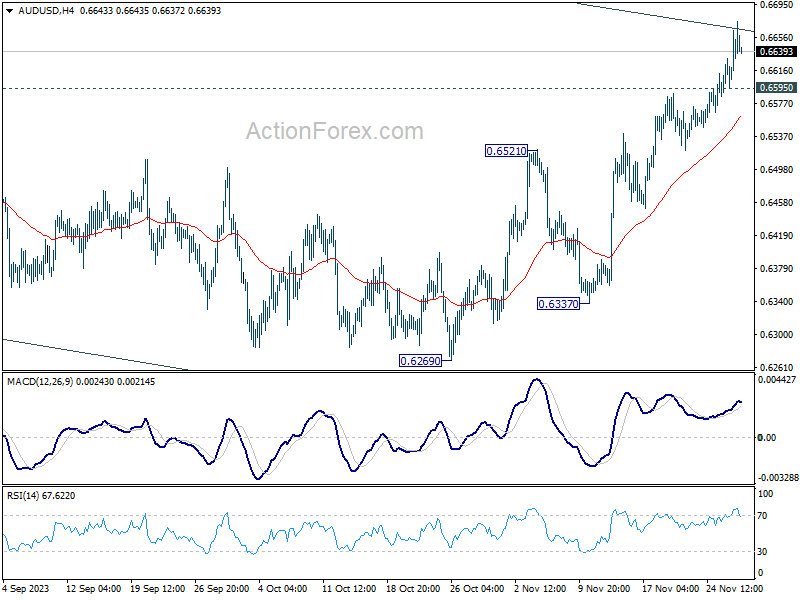

AUD/USD Daily Report

Daily Pivots: (S1) 0.6609; (P) 0.6637; (R1) 0.6678; More...

AUD/USD's rally is still in progress and intraday bias stays on the upside. Sustained break of channel resistance (now at 0.6663) will argue that whole decline from 0.7156 has completed with three waves down to 0.6269. Further rally should then be seen to 0.6894 resistance for confirmation. On the downside, below 0.6595 minor support will turn intraday bias neutral first. But further rise will remain in favor as long as 0.6521 resistance turned support holds.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. price actions from 0.6169 (2022 low) could be just a medium term corrective pattern, with rise from 0.6269 as the third leg. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

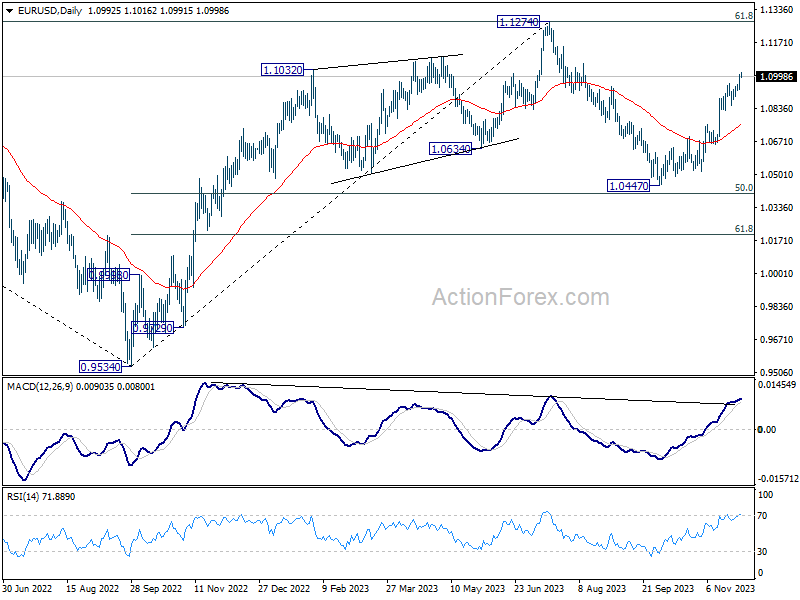

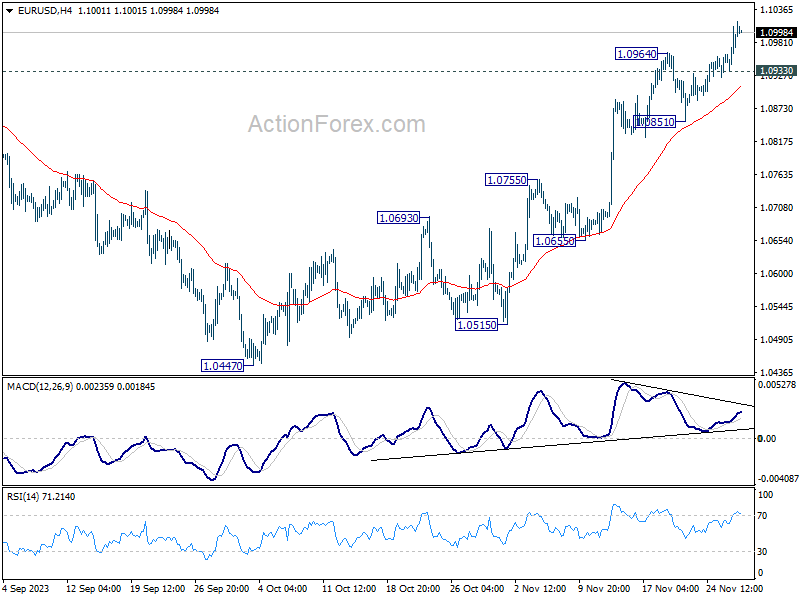

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0950; (P) 1.0980; (R1) 1.1024; More...

EUR/USD's rally resumed by breaking through 1.0964 and intraday bias is back on the upside. Current rise from 1.0447 should now target 1.1274 resistance next. But strong resistance should be seen there to limit upside. On the downside, below 1.0933 minor support will turn intraday bias neutral and bring consolidations. But further rally will remain in favor as long as 1.0851 support holds.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.