Sample Category Title

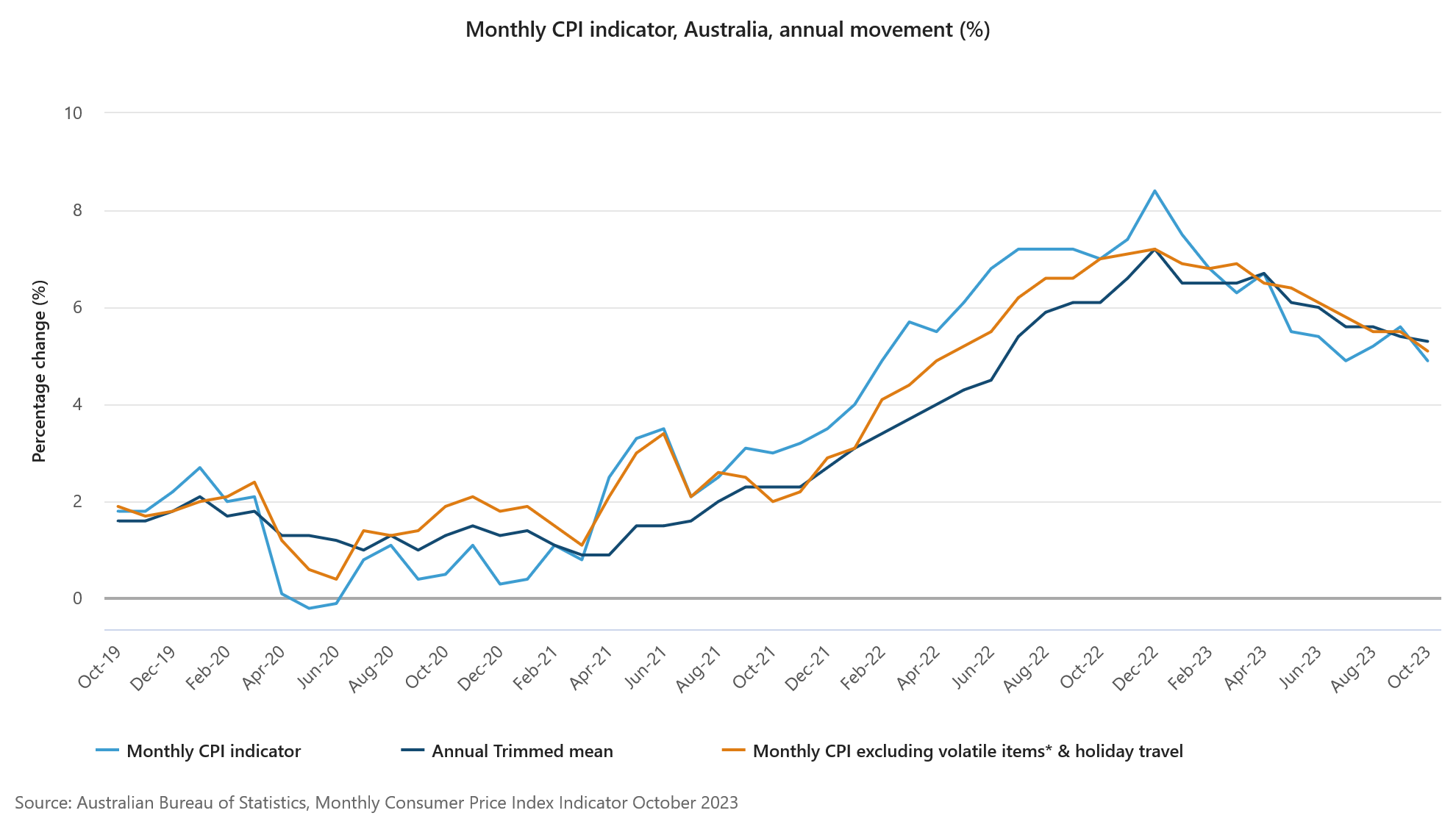

Australia’s monthly CPI slowed to 4.9% in Oct, below exp 5.2%

Australia monthly CPI slowed from 5.6% you to 4.9% yoy in October, below expectation of 5.20%. Excluding volatile items and holiday travel, CPI slowed from 5.5% yoy to 5.1% yoy. Annual trimmed mean CPI also slowed from 5.4% yoy to 5.3% yoy.

The most significant contributors to the October annual increase were Housing (+6.1%), Food and non-alcoholic beverages (+5.3 per cent) and Transport (+5.9%).

GBP/USD Eyes Additional Gains, US GDP Next

Key Highlights

- GBP/USD is aiming for more gains above 1.2750.

- A key bullish trend line is forming with support at 1.2600 on the 4-hour chart.

- Gold prices are accelerating higher above the $2,025 resistance.

- The US GDP could grow 5% in Q3 2023 (Preliminary), up from 4.9%.

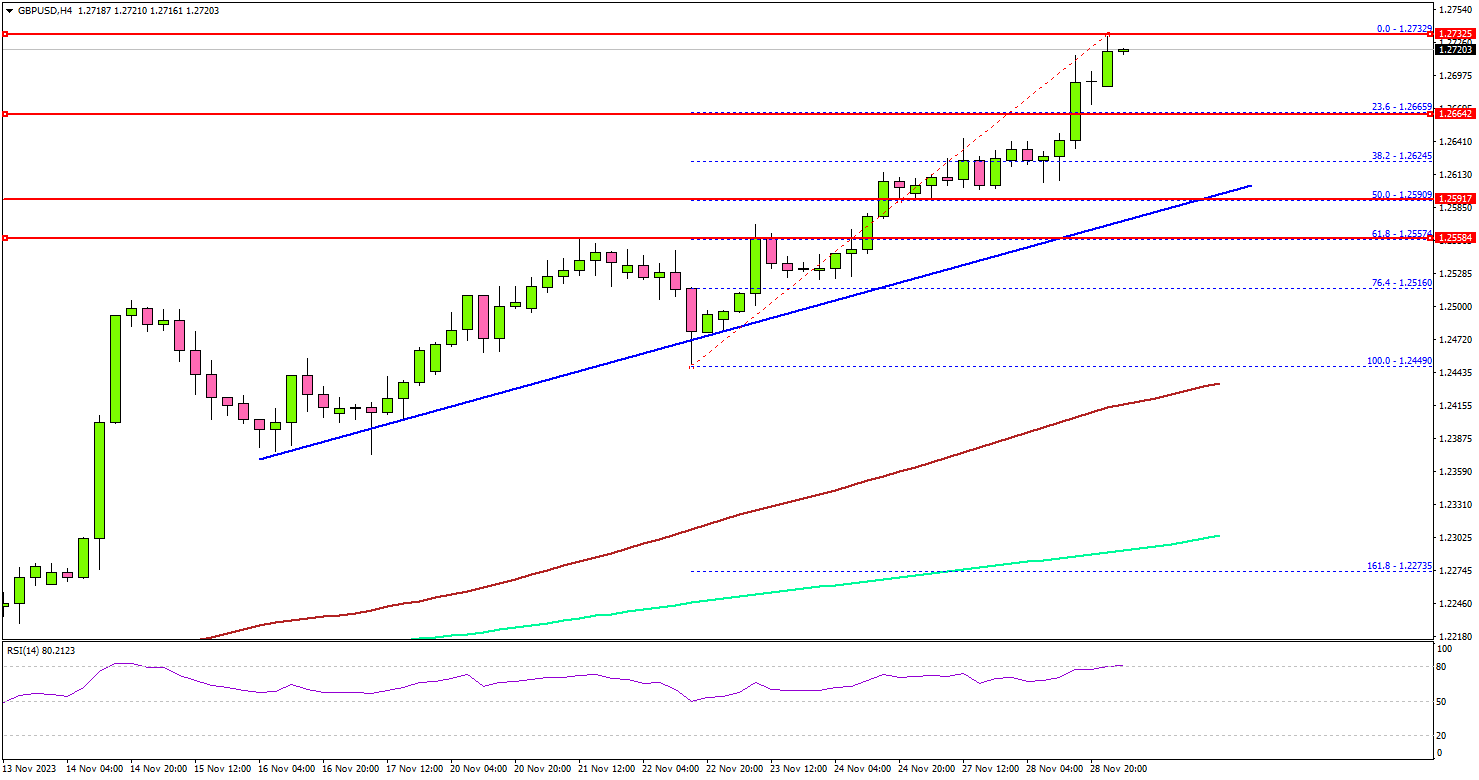

GBP/USD Technical Analysis

The British Pound started a major increase above the 1.2450 level against the US dollar. GBP/USD even climbed above the 1.2550 level to enter a positive zone.

Looking at the 4-hour chart, the pair settled above the 1.2600 level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

It even tested the 1.2730 resistance before there was a consolidation phase. On the upside, immediate resistance is near the 1.2730 level. The next key resistance is near the 1.2750 level. A close above the 1.2750 zone could open the doors for more upsides. The next stop for the bulls might be 1.2800.

If there is a downside correction, the pair might find support near the 1.2665 zone. There is also a key bullish trend line forming with support at 1.2600 on the same chart.

The trend line is close to the 50% Fib retracement level of the upward move from the 1.2449 swing low to the 1.2732 high. If there is a downside break below the trend line, the pair could decline toward the 1.2550 support.

The 61.8% Fib retracement level of the upward move from the 1.2449 swing low to the 1.2732 high is also near 1.2550. The next key support sits at 1.2450, below which the pair could test the 1.2420 pivot level in the near term.

Looking at Gold, there were strong bullish moves above $2,025 and there could be more upsides toward $2,050 in the coming sessions.

Economic Releases

US Goods Trade Balance for Oct 2023 - Forecast $-85.5B, versus $-86.3B previous.

US Gross Domestic Product for Q3 2023 (Preliminary) – Forecast 5.0% versus previous 4.9%.

NZD/USD soars, AUD/NZD dives after RBNZ hawkish hold

New Zealand Dollar surges sharply after hawkish RBNZ holds, which hints at another rate hike in Q2 next year.

From a technical standpoint, NZD/USD's rally from 0.5771 accelerates to as high as 0.6206 so far today. The development strengthen the case that whole corrective fall from 0.6537 (Feb high), has completed with three waves down to 0.5771 (Oct low).

Near term outlook will stay bullish as long as 0.6078 support holds. Next target is trend line resistance at around 0.6300. Sustained break there would pave the way through 0.6537 to resume the rise from 0.5511 (2022 low).

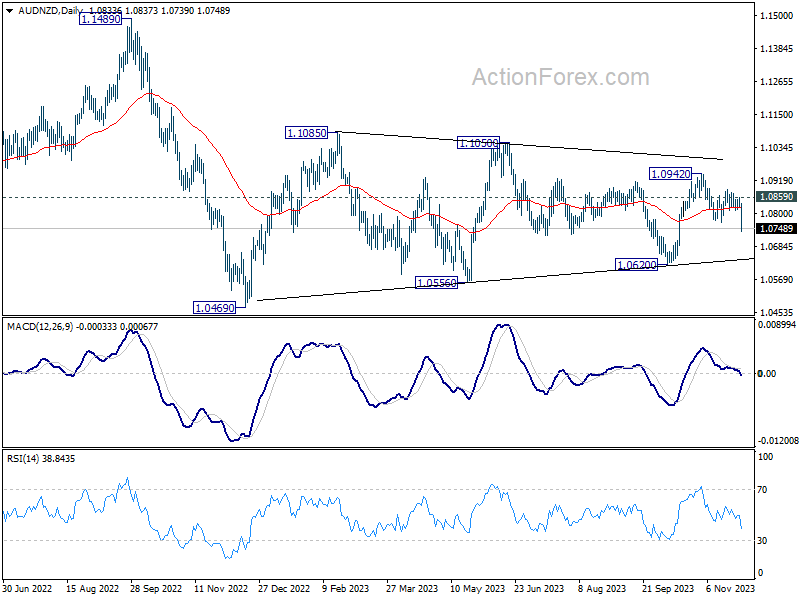

In gauging Kiwi's strength, AUD/NZD is always a reference. Today's sharp decline suggests that fall from 1.0942 is in progress. Near term outlook remains bearish as long as 1.0859 resistance holds, next target is 1.0620 support.

More importantly, it's possible that the triangle consolidation pattern from 1.0469 (2022 low) has completed at 1.0942. Firm break of 1.0620 will argue that whole fall from 1.1489 (2022 high) is ready to resume through 1.0469 in the medium term.

NZ First Impressions: RBNZ Monetary Policy Statement

Short description: The RBNZ left the OCR at 5.5% as expected but was more hawkish on future prospects. The RBNZ’s projections continue to reflect the risk of further increases in the OCR in 2024. An easing cycle looks quite some time off.

- The RBNZ’s projections for the OCR were revised 10bp higher to a peak of 5.69% in September 2024, implying around a 75% chance of a further 25bp rate hike. The projections imply a gradual easing of policy from the first half of 2025. The long-run neutral OCR was adjusted up 25bp to 2.5%.

- The RBNZ’s short term CPI forecasts have been revised down slightly in the near term but significantly higher from mid-2024 reflecting a concern that migration driven population growth will add to demand and the housing market. CPI inflation still gets back inside the range in Q3 2024, but the RBNZ sees upside risks here.

- Our overall impression is that this is in line with our concern that more tightening may be required to ensure inflation returns promptly to target.

Talking tough and maybe doing something.

As widely expected, the RBNZ left the OCR at 5.5% at its final policy review for this year. Of much greater interest to markets was what the Bank had to say about the outlook for the OCR next year and beyond.

In summary, the updated projections in the accompanying Monetary Policy Statement (MPS) contained significant revisions from those published back in August. The projections continue to reflect a risk that a higher OCR will ultimately be required, with the probability of a further 25bp hike in 2024 now estimated at around 75% compared with 36% previously (the peak OCR increased to 5.69% from 5.59% previously). Thereafter, with CPI inflation forecast to move back inside the target range in Q3 next year (unchanged from the August forecast) the RBNZ’s projections imply a modest easing cycle might be possible from mid-2025 – much later than implied by current market pricing.

The most notable changes in the press statement and meeting record from those which accompanied the October policy review was increased concern that inflation would remain persistent and upside risks from these upwardly revised forecasts. A key driver is increased concern that migration and population would drive increased demand and medium-term inflation pressures. The RBNZ’s forecast for house prices was revised up from 4.3% to 5.5% for 2024 reflecting these pressures. The statement of record also notes that government investment looks set to be stronger (in line with PREFU) which also adds to medium term demand concerns.

Our overall first impression is that the RBNZ is concerned that further increases in interest rates may be required towards the middle of 2024. Key will be migration and housing market indicators over the next few months and the next couple of CPI outturns. The new government’s fiscal projections in the HYEFU before Christmas will also be a key focus. OCR cuts certainly do not seem to be on the radar for the RBNZ right now.

We will publish a bulletin with further commentary and analysis later today, including implications for our call on the outlook for the OCR, once we have had time to read the full MPS and observe the Governor’s post-meeting press conference.

RBNZ raises rate track, signaling additional rate hike

RBNZ decided to keep the Official Cash Rate steady at 5.50%, aligning with market expectations. However, a significant aspect of their announcement is the upward revision of their "rate track."

According to the bank's forecasts in the Monetary Policy Statement, OCR is expected to peak at 5.70% in Q2 of 2024 and maintain this level throughout the year. Looking ahead, RBNZ anticipates a rate cut in Q2 of 2025, bringing it down to 5.4%.

In the accompanying statement, RBNZ noted, "ongoing excess demand and inflationary pressures are of concern, given the elevated level of core inflation."

RBNZ also emphasized its readiness to hike again. "If inflationary pressures were to be stronger than anticipated, the OCR would likely need to increase further."

Moreover, RBNZ underlined the necessity of maintaining interest rates at a restrictive level for a sustained period, aiming at ensuring consumer price inflation returns to target level and to support maximum sustainable employment.

(RBNZ) Monetary policy to remain restrictive

The Monetary Policy Committee today agreed to maintain the Official Cash Rate at 5.50%.

Interest rates are restricting spending in the economy and consumer price inflation is declining, as is necessary to meet the Committee's Remit. However, inflation remains too high, and the Committee remains wary of ongoing inflationary pressures.

Internationally, economic growth has been stronger than was expected at the start of this year but remains below trend and is likely to slow further. This subdued growth outlook will continue to restrain New Zealand's export revenues.

In New Zealand, demand growth has eased, but by less than anticipated over the first half of 2023 in part due to strong population growth. The OCR will need to stay restrictive, so demand growth remains subdued, and inflation returns to the 1 to 3 percent target range.

Wage growth has eased from recent peaks. Demand for labour is softening, with job advertisements now below pre-COVID-19 levels. At the same time, strong inward migration is increasing the population and adding to labour supply.

While population growth has eased supply constraints, the effects on aggregate demand are becoming apparent. This is increasing the risk of inflation remaining above target.

The Committee is confident that the current level of the OCR is restricting demand. However, ongoing excess demand and inflationary pressures are of concern, given the elevated level of core inflation. If inflationary pressures were to be stronger than anticipated, the OCR would likely need to increase further.

The Monetary Policy Committee agreed that interest rates will need to remain at a restrictive level for a sustained period of time, so that consumer price inflation returns to target and to support maximum sustainable employment.

Media contact

James Weir

Senior Adviser External Stakeholders

Phone:+64 4 471 3962 | Mobile: 021 103 1622

Email:James.Weir@rbnz.govt.nz

Summary record of meeting

The Monetary Policy Committee discussed recent developments in the New Zealand economy. The Committee agreed that monetary conditions are restricting spending and reducing inflationary pressure. Supply constraints in the economy continue to ease and demand growth is slowing, but to a lesser extent than expected. Inflation remains too high and inflationary pressures continue to emerge. Further slowing in spending growth is needed to reduce demand toward the economy's ability to supply goods and services, to ensure that consumer price inflation returns to its target range.

Global economic growth remains below trend as high interest rates weigh on demand. Easing global demand is placing downward pressure on New Zealand exports, and export revenues are lower than in recent years. However, global prices for some products, such as dairy, have stabilised in recent months. Members noted that to date, global growth has been stronger than was expected at the start of this year, supported by sustained strength in the US economy and a recent lift in economic activity in China. However, going forward, subdued global growth is expected to restrain demand and prices for New Zealand's exports over the medium term.

The Committee discussed international inflation trends. Globally, headline inflation continues to fall, but there are differences in both the timing and magnitude of these declines across countries. Housing rent inflation is an important source of difference in services inflation across countries, with greater upward pressure in economies experiencing high net immigration, such as New Zealand and Australia.

In discussing global financial conditions, the Committee noted that long-term interest rates for government debt have increased, largely in response to the rising volume of public debt. More recently, interest rates have decreased as financial markets anticipate the end of the phase of monetary policy tightening by major central banks. Members also noted that most major central banks have indicated that they intend to retain current restrictive policy rates for longer, and are willing to tighten further, if required.

The Committee discussed recent domestic economic developments. While growth in parts of the economy is slowing, there has been less of a decline in aggregate demand growth than expected earlier in the year. As was noted in the October Review, GDP growth in the second quarter of 2023 was higher than expected while growth in the first quarter was revised up. Consumer spending growth is broadly easing, but some areas of services spending remain more resilient. On an aggregate level, consumption is being supported by the strong growth in population, whereas on a per capita basis, consumption is declining.

Members noted that net immigration has been higher than previously assumed. This has increased the supply of workers into a tight labour market. However, the demand-side effects are becoming apparent. Strong population growth has contributed to an increase in housing rents. Rent increases, and any increases in construction costs in response to greater housing requirements, affect inflation directly, as rental prices and construction costs are accounted for in the consumer price index. Members noted that the outlook for residential investment was currently muted, despite the surge in population growth.

House prices have stabilised after earlier declines, with strong population growth and increased nominal disposable incomes offsetting the effect of higher debt servicing costs. House price increases affect inflationary pressures indirectly, via higher household wealth and an associated increase in consumption. Some members considered that the willingness of households to consume out of wealth may be lower given recent house price falls, higher debt servicing costs, and a softening labour market. Other members considered that there may be upside risks to house prices, and therefore consumption, given the anticipated decline in residential investment.

Annual headline inflation was lower than expected in the September 2023 quarter. This was accounted for by lower inflation for tradable goods and services. Members noted that tradable inflation can be volatile and cannot be relied upon to achieve their inflation target. Non-tradable inflation is easing only gradually and, while all measures of core inflation have declined, they are still elevated. Short-term inflation expectations have declined, and members expect this to continue as headline inflation moves lower. Some members were concerned that 2-year inflation expectations were not declining particularly quickly and that longer-term inflation expectations had also increased. Other members were less concerned as they viewed longer-term inflation expectations as still close to the target midpoint.

In discussing the labour market, members noted that the underutilisation rate and unemployment rate both increased in the September 2023 quarter. Population growth has increased labour supply, as seen in declines in surveyed measures of labour shortages. As economic activity slows, labour demand is also declining, with job advertisements falling to below pre-COVID-19 levels. Wage inflation has eased. Members noted that whilst pressures in the labour market are easing, it is still tight, and employment remains above its maximum sustainable level.

At the time of the October Review, members had noted updates in the Pre-election Economic and Fiscal Update 2023 (PREFU). Specifically, while total government spending as a share of potential GDP is still forecast to decline, this was now by less than previously expected. The PREFU included a material increase in government investment over the medium term, linked to infrastructure requirements.

Members agreed that population growth and government investment would both likely support aggregate supply in the economy. However, they noted that in the short to medium term, demand could only sustainably grow at the economy's production potential without adding to inflationary pressure. The current context is that aggregate demand has been greater than the economy's ability to supply goods and services, creating inflationary pressure. While the economy is moving back into balance, ensuring that demand remains contained will make the task of returning inflation to target much easier.

The Committee noted that the estimate of the long-run nominal neutral OCR has increased by 25 basis points to 2.50 pecrent within the economic projections, consistent with the Reserve Bank's indicator suite. The long-run nominal neutral rate impacts the central economic projections but has a larger impact in the latter part of the forecast horizon and beyond. Members agreed that the current level of the OCR remains contractionary.

The Committee discussed domestic financial conditions. Credit demand remains subdued as higher interest rates and a slowing economy reduce the ability and willingness of businesses and households to borrow. Mortgage rates have continued to increase, as expected. Members noted that the average rate on outstanding mortgages is expected to increase from 5.4 percent currently to 6.4 percent by mid-2024. The share of disposable income going to debt servicing for households with a mortgage is expected to increase from 15 percent currently to 19 percent.

The Committee discussed the expected evolution of retail interest rates, given ongoing changes in bank funding. Term deposit rates and volumes have increased. Higher term deposit rates are now contributing to ongoing increases in mortgage rates. As competition for term deposits continues, the margin between mortgage rates and wholesale interest rates is expected to return to more historically normal levels. Members agreed this expectation was consistent both with their previous discussions around future changes to retail interest rates, and with assumptions in the economic projection.

The Committee discussed the balance of risks for inflation, output, and employment. Members agreed that while the risk profile remained broadly similar to that discussed at the time of the August Statement, some of the short-term upside risks to activity appear to have eventuated and have therefore been incorporated in the central economic projection. In considering risks, members also specifically discussed two scenarios.

The first scenario was one of persistent domestic demand strength supported by strong population growth, with increases in rents and aggregate consumption feeding into greater inflationary pressure and higher house prices. The second scenario considered a larger global economic slowdown, with growth below trend for longer than currently anticipated. A greater slowdown in global growth would see a fall in the price of imports and further reduce goods export prices and export volumes.

Given the current high level of core inflation, members agreed that there was an asymmetry in the distribution of risks to the outlook for monetary policy across the two scenarios. A global slowdown would likely unwind the additional inflationary pressure that has recently been observed, whereas further domestic demand strength would likely necessitate additional monetary tightening. Some members noted that inflation has now been above target for some time, and that there should be a low tolerance for any increase in the time to return inflation to target.

The Committee noted that the incoming Government's policy programme will have implications for economic activity and inflation. Members agreed that this would be assessed as policies are formally incorporated into the Treasury's official forecasts.

The Committee discussed the backdrop of heightened geopolitical tension and risk of spillovers to the global economy. Members noted that whilst they remain attentive to global developments, they will respond to shocks if and when they eventuate. The Committee also discussed the outlook for China and noted that while economic data over recent months have improved, structural challenges facing the Chinese economy remain concerning for long-term growth prospects. Potential growth is slowing, partly due to demographic trends, but also due to substantial declines in productivity growth. High levels of debt, particularly in the property sector, and weak demand remain the most acute downside risks.

Members were cognisant of the likelihood of an El Niño climate pattern in coming months. They noted that the scale of potential impact is highly uncertain and depends on the timing and location of any droughts. There may be differentiated impacts for different agricultural commodities. No specific drought impacts have been incorporated in the economic projection and members agreed they would continue to closely monitor the evolution of El Niño over coming months.

The Committee agreed that in the current circumstances, there is no material trade-off between meeting their inflation and employment objectives and maintaining stability of the financial system. Members noted that slowing economic activity is not being experienced evenly across the economy. The commercial property and agricultural sectors are starting to experience challenges and may be vulnerable. For highly-indebted households, pockets of stress are likely to grow as debt servicing burdens increase.

In discussing their Remit objectives, the Committee noted inflation is still expected to decline to within the target band by the second half of 2024. Pressure in the labour market is easing, although employment remains above its maximum sustainable level. Members agreed that monetary policy was supportive of sustainable house prices.

In discussing the appropriate stance of monetary policy, members agreed they remain confident that monetary policy is restricting demand. Nevertheless, ongoing excess demand and inflationary pressures were of concern, given high core inflation. Members discussed the possibility of the need for increases to the OCR. Members agreed that with interest rates already restrictive, it was appropriate to wait for further data and information to observe the speed and extent of easing in capacity pressures in the economy.

The Committee agreed that interest rates will need to remain at a restrictive level for longer, to ensure annual consumer price inflation returns to the 1 to 3 percent target range and to support maximum sustainable employment. On Wednesday 29 November, the Committee reached a consensus to maintain the Official Cash Rate at 5.50 percent.

Attendees

Reserve Bank members of MPC: Adrian Orr, Christian Hawkesby, Karen Silk, Paul Conway

External MPC members: Bob Buckle, Peter Harris, Caroline Saunders

Treasury Observer: Dominick Stephens

MPC Secretary: Kate Poskitt

Will Deeper OPEC+ Output Cuts Matter for Oil Prices?

- Oil prices slide after OPEC+ alliance delays meeting

- But recent headlines point to consensus

- Oil prices could gain, but any recovery may prove limited

- The meeting was postponed from Sunday to this Thursday

OPEC+ delays decision on lack of consensus

Oil prices tumbled after OPEC and other major oil producing nations, known as the OPEC+ group, decided to delay a meeting scheduled for Sunday, November 26, to Thursday, November 30. Investors may have sold black gold on concerns that the group was unable to reach consensus on further production cuts amid a weakening global growth outlook, as it was anticipated heading into the meeting.

Sources said that this was due to African countries Nigeria and Angola aiming for higher oil output allowance, as they were earlier given lower targets after years of failing to meet the previous ones. Nonetheless, on Friday, news hit the wires that the alliance has moved closer to a compromise, which increases the likelihood of having a consensus on Thursday.

Are deeper cuts on the table?

Before the announcement of the postponement, it was largely anticipated that members are likely to extend or even deepen the existing supply cuts into next year. Saudi Arabia was also expected to stretch its additional voluntary supply cuts to at least the first quarter of 2024, so the big question may be whether there will be consensus of deeper cuts by other nations.

Although Saudi Arabia may be willing to cut more, it will likely want concessions from other nations as well. For example, Iraq is already exceeding its existing production target and could be tempted to take more barrels to the market if an accord to reopen its Kurdish export pipeline is soon reached. Iran’s exports have also been increasing. Iran’s targets have been suspended due to the imposition of US sanctions, but there is clear frustration among Gulf producers regarding soft enforcement by the US. Thus, there may be clear calls for this nation to be also given a target.

Any recovery could be limited and short-lived

As for the market’s reaction, Friday’s news that members have nearly reached common ground did not trigger a rebound in oil prices, which means that investors may be thinking that whatever cuts are decided, the alliance may have been on track to agree more if it weren’t for the disagreements. A relief bounce remains a likelihood in case the group as a whole deepens its production cuts, but the hypothesis that they could have done more could keep the recovery limited and short-lived.

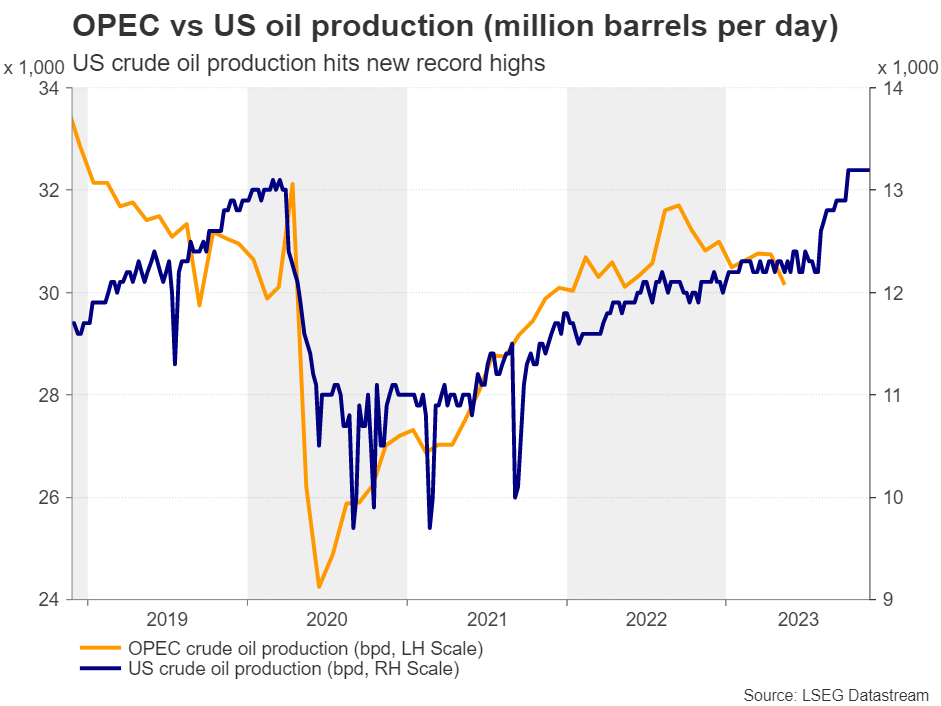

What’s more, US output is also on the rise, hitting new records, which combined with weakening global demand prospects constitutes another reason why any decision-related recovery is likely to be brief. Therefore, oil prices could stay in a downtrend for a while longer, which could result in lower headline inflation around the world and perhaps prompt central banks whose economies are on the verge of recession, like the Eurozone, to cut interest rates earlier than currently anticipated.

WTI’s broader path remains to the downside

From a technical standpoint, WTI’s price structure remains of lower highs and lower lows below the downside resistance line drawn from the high of September 29. What’s more, the 50-day EMA appears ready to fall below the 200-day EMA soon, which could validate the bearish picture. Although the 74.00 barrier provided decent support recently, it could soon be violated by the bears, with the next stop perhaps being the low of November 16 at around 72.15. A break lower would confirm a lower low on the daily chart and could see scope for extensions all the way down to the key area of 67.00.

For the picture to turn brighter, WTI may need to climb all the way above the crossroads of the aforementioned downtrend line and the round number of 80.00.

Can USD Recover?

The EURUSD pair is currently making steady gains, approaching multi-month highs around 1.0960, driven by a weakened USD and Christine Lagarde's somewhat hawkish remarks before the European Parliament. Minor housing data from the U.S., specifically New Home Sales for October, came in below expectations but didn't significantly impact the pair. Lagarde, President of the European Central Bank, cautioned that headline inflation might see a slight increase, and economic growth is anticipated to remain weak. However, Lagarde didn't provide clear indications on the duration of maintaining restrictive rates or the timeline for rate cuts. The focus for the rest of the week will be on Eurostat's release of the Harmonized Index of Consumer Prices (HICP) and the U.S. report on the Core Personal Consumption Expenditures Index (PCE), influencing short-term expectations for the ECB and the Fed.

EURUSD - D1 Timeframe

EURUSD is currently trading around a major supply zone on the daily timeframe. The bearish array of the moving averages can be considered an additional confluence in support of the bearish sentiment. In the meantime though, there is a trendline support on the 4-Hour timeframe that I will be expecting price to break, before the bearish move can commence.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.06965

- Invalidation: 1.10556

GBPUSD - D1 Timeframe

GBPUSD is currently at an intersection of a supply zone and a trendline resistance. Usually, this is considered basis enough for a bearish sentiment. However, considering the apparent lack of volatility from the US Dollar, I will personally wait to see a break of the minor trendline support on the 4-Hour timeframe for a safer entry, as in the case of EURUSD.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.22494

- Invalidation: 1.27452

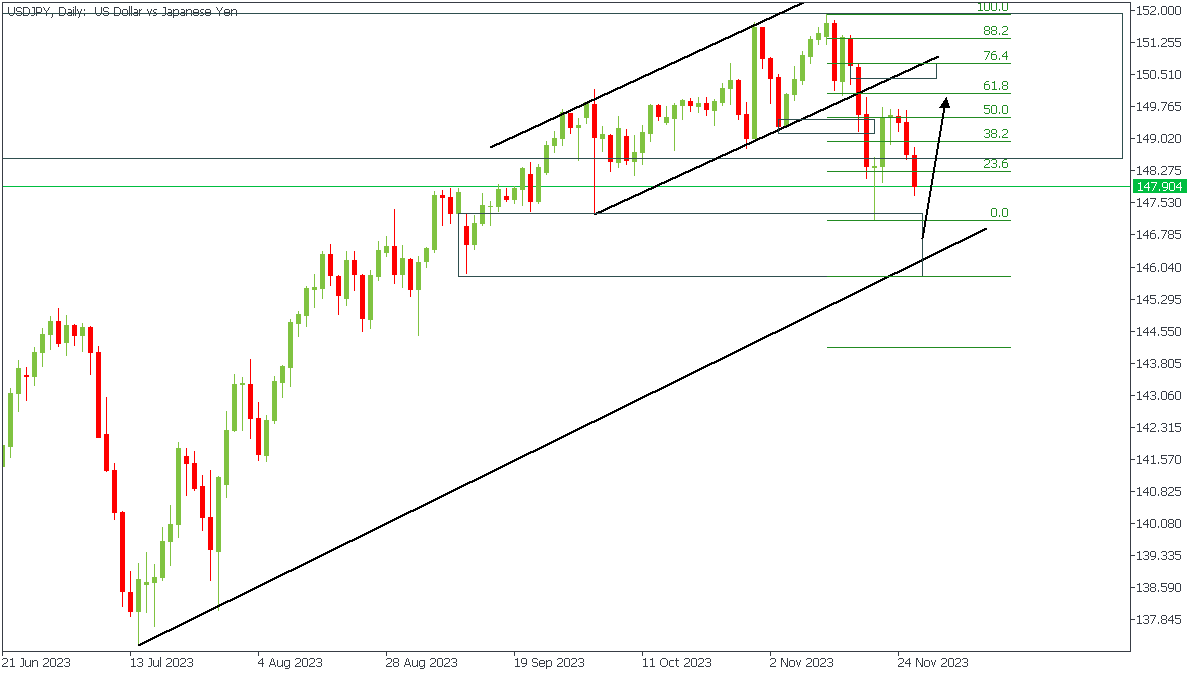

USDJPY - D1 Timeframe

USDJPY is currently approaching the major demand zone with an overlapping trendline support. Based on this, I am expecting a bounce off of the trendline with an initial target at the 76% of the Fibonacci retracement level.

Analyst’s Expectations:

- Direction: Bullish

- Target: 150.281

- Invalidation: 145.692

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

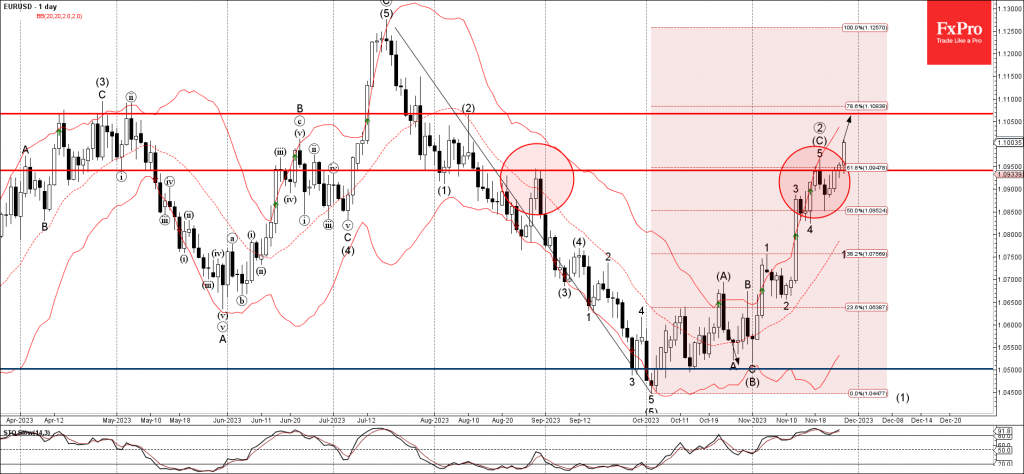

EURUSD Wave Analysis

- EURUSD broke resistance level 1.0950

- Likely to rise to resistance level 1.1065

EURUSD currency pair recently broke the key resistance level 1.0950, intersecting with the 61.8% Fibonacci correction of the downward impulse from July.

The breakout of the resistance level 1.0950 should further increase the bullish pressure on this currency pair.

Given the continuation of the strong US dollar sales seen today, EURUSD currency pair can be expected to rise further to the next resistance level 1.1065, former top of wave (2) from August.

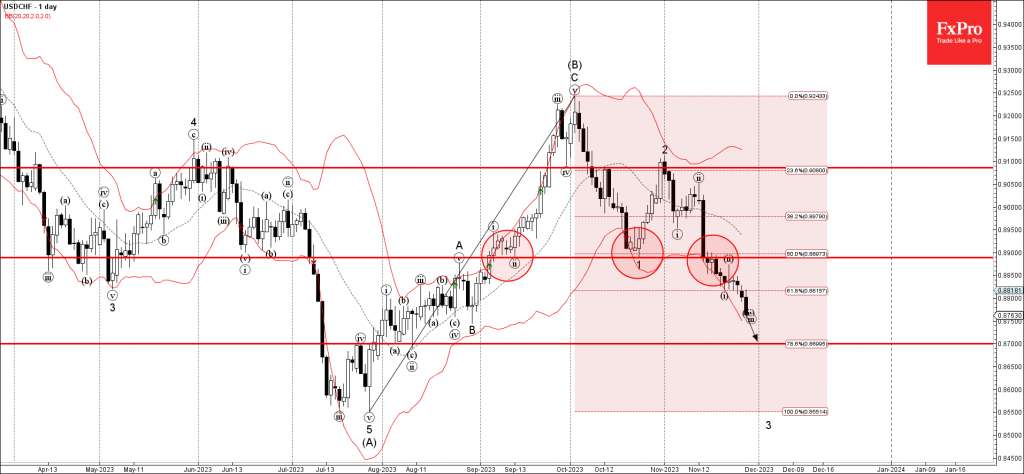

USDCHF Wave Analysis

- USDCHF broke key support level 0.8900

- Likely to fall to support level 0.8700

USDCHF currency pair continues to fall inside the minor impulse wave 3, which previously broke the key support level 0.8900, coinciding with the 50% Fibonacci correction of the upward wave (B) from the end of July.

The active impulse wave 3 belongs to the higher order downward impulse wave C from the start of October.

USDCHF currency pair can be expected to fall further to the next support level 0.8700, previous monthly low from August.