Sample Category Title

USD/JPY Mid-Day Outlook

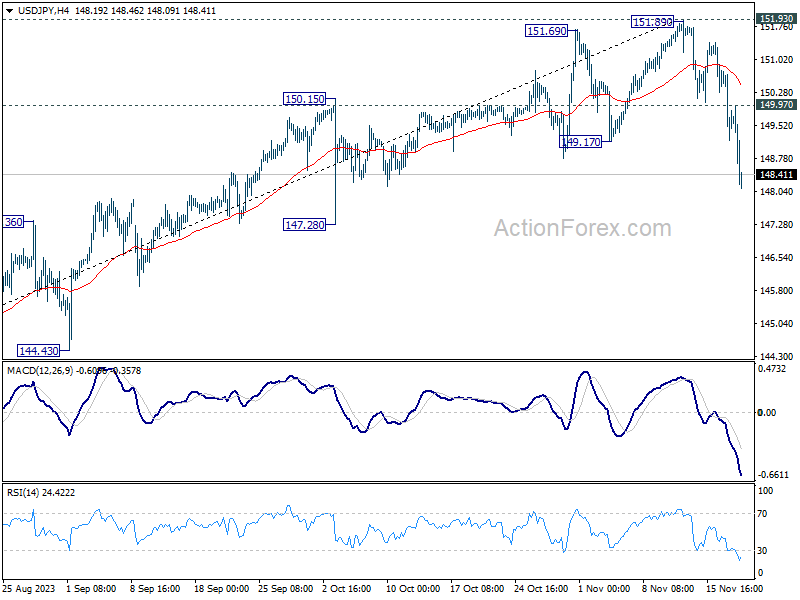

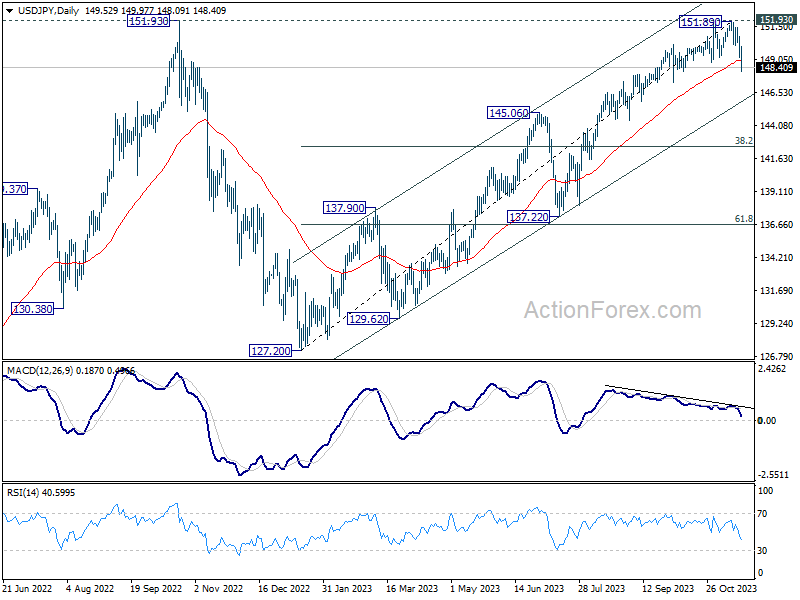

Daily Pivots: (S1) 148.91; (P) 149.85; (R1) 150.49; More...

USD/JPY's fall from 151.89 extends to as low as 148.00 so far, and there is no sign of bottoming yet. Intraday bias stays on the downside for medium term channel support at 145.80 next. On the upside, break of 149.97 resistance is needed to indicate completion of the decline. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 resistance (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

Yen’s Strong Rally Reflects Broader Shifts in Global Monetary Policy Expectations

Japanese Yen's remarkable rally has become a focal point in the currency markets today. It's strength is extending into US session. This surge is not an isolated event but a reflection of broader shifts in global monetary policy expectations. A crucial factor propelling Yen upwards is the increasing speculation that BoJ would finally abandon its negative interest rates policy in the coming year. This potential policy shift represents a significant reversal from BoJ's longstanding accommodative monetary stance, which has been a defining feature of Japan's economic policy recent years.

Simultaneously, there's a contrasting trend emerging in other parts of the world. Market participants are increasingly betting on the likelihood of rate cuts by other major global central banks in the next year. This anticipation points to a narrowing of the interest rate differentials between Japan and other major economies. It's a noteworthy reversal from the trend observed over the past two years, where the gap in interest rates had been widening. Should these market predictions come to fruition, the sustainability of Yen's strength could be reinforced, supported by realignment in global interest rate policies.

As of now, Australian Dollar and New Zealand Dollar are following Yen's lead, ranking as the next strongest currencies for the day. However, their rallies have been somewhat tempered by the stabilization of risk sentiment in European session. These currencies, typically sensitive to changes in risk appetite, have shown moderated movements in response to the evolving market mood. On the other end of the spectrum, Dollar is languishing at the bottom of the performance chart, with Canadian Dollar, Sterling, and Euro trailing behind. Swiss Franc finds itself in a mixed position, reflecting a more nuanced market response.

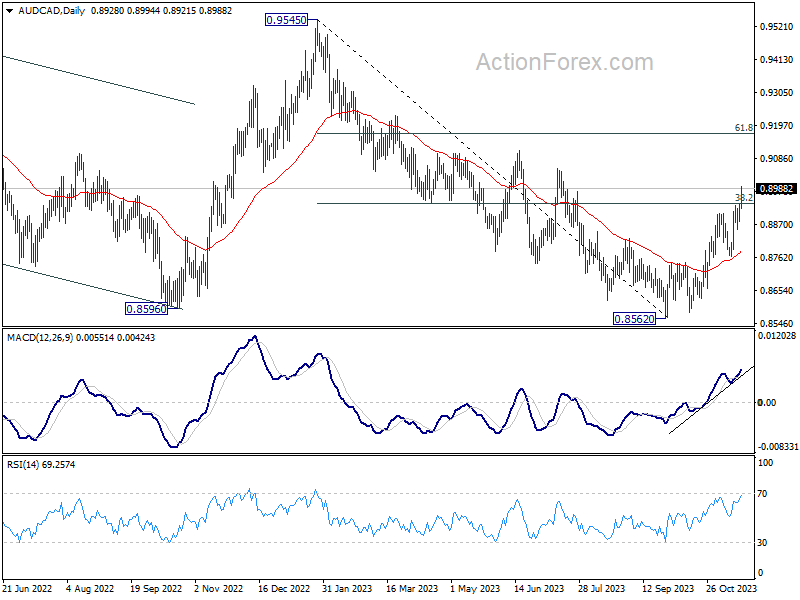

From a technical standpoint, AUD/CAD's rally from 0.8652 accelerates higher today, and hit as high as 0.8990 so far. The strong break of 38.2% retracement of 0.9545 to 0.8562 at 0.8938, and the strong upside momentum affirm the case that it's reversing whole down trend from 0.9545. Further rally should be seen to 61.8% retracement at 0.9169 next. The forthcoming RBA minutes and Canada's CPI data tomorrow will be critical in determining the pair's trajectory, potentially acting as catalysts for the next significant move.

In Europe, at the time of writing, FTSE is down -0.37%. DAX is down -0.40%. CAC is up 0.04%. Germany 10-year yield is up 0.0351 at 2.624. Earlier in Asia, Nikkei lost -0.49%. Hong Kong HSI gained 1.86%. China Shanghai SSE rose 0.46%. Singapore Strait Times fell -0.42%. Japan 10-year JGB yield dropped -0.0040 to 0.744.

Bundesbank report: Inflation likely to hover around current level

The latest monthly report from Bundesbank presents a mixed outlook for the German economy, highlighting persistently high inflation and a slow yet expected recovery.

According to the report, headline inflation at 3.0% and core inflation at 4.2% are "still well above historical average." The Bundesbank anticipates that the inflation rate is "likely to fluctuate around its current value in the coming months," indicating ongoing price stability concerns.

The report forecasts that a slight economic recovery is "only expected after the turn of the year". This recovery is expected to be driven by an increase in real net income of private households, buoyed by significant wage hikes a reduction in price pressures. Despite anticipated cautious approach to spending by private households, there is expectation of gradual expansion in real consumption, which could bolster domestic economy.

The industrial sector, however, continues to face challenging conditions. The Bundesbank's report points to weak foreign demand and the lingering effects of previous energy price shocks as factors hampering production. Yet, there are initial signs of improvement on the horizon. The report notes that the basic trend in incoming orders suggests a potential stabilization in foreign demand.

ECB's Wunsch: Early rate cut bets may trigger opposite action

ECB Governing Council member Pierre Wunsch today expressed skepticism regarding market expectations of an early easing of monetary policy. His comments highlight a crucial divergence between market forecasts and ECB's potential policy path in the face of ongoing inflationary pressures.

Wunsch described the market's anticipation of a reduction in ECB's deposit rate from the current 4% by April as "optimistic." He pointed out the necessity for ECB to either continue with the current rate or possibly increase it, contrary to market expectations.

He raised concerns about the implications of market bet on rate cuts. "Is it a problem if everybody believes we're going to cut?" he questioned. This could lead to "less restrictive monetary policy" which may then be insufficient, and eventually, "it increases the risk that you have to correct in the other direction."

Wunsch emphasized the ECB's readiness to adapt its strategy based on inflation trends. "If we arrive at the conclusion that inflation is not going down fast enough, we'll communicate it through our projection and through our communication," he stated.

China maintains 1-yr and 5-yr LPR

As reported by the National Interbank Funding Center today, China's one-year loan prime rate retains is unchanged 3.45%. Similarly, the over-five-year LPR, a critical determinant of mortgage rates, is also steady at 4.2%.

The LPR, derived from the quotations by various banks with adjustments based on the open-market operation rates, serves as a pivotal indicator for loan pricing. This stability comes in the wake of PBoC's substantial liquidity injection of CNY 1.45 into the market through the medium-term lending facility last week, maintaining an interest rate of 2.5%.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.91; (P) 149.85; (R1) 150.49; More...

USD/JPY's fall from 151.89 extends to as low as 148.00 so far, and there is no sign of bottoming yet. Intraday bias stays on the downside for medium term channel support at 145.80 next. On the upside, break of 149.97 resistance is needed to indicate completion of the decline. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 resistance (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | EUR | Germany PPI M/M Oct | -0.10% | -0.10% | -0.20% | |

| 07:00 | EUR | Germany PPI Y/Y Oct | -11.00% | -11.00% | -14.70% | |

| 11:00 | EUR | German Buba Monthly Report |

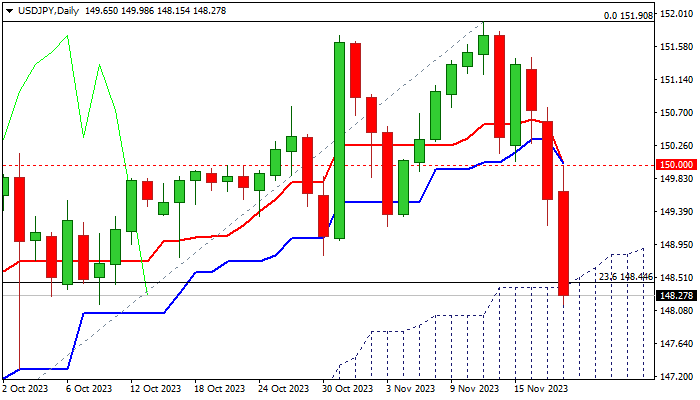

USD/JPY: Bears Increase Pace and Penetrate Rising Daily Cloud

USDJPY remains under increased pressure on Monday and extends steep bear-leg from 151.43 lower top into third straight day.

Last week’s close below psychological 150 level generated initial bearish signal which was boosted by today’s extension through 148.44 (Fibo 23.6% of 137.23/151.90 rally) and drop into rising daily cloud (cloud top lays at 148.37).

Daily close below these levels to add to signals of a double top and reversal, which may spark deeper pullback towards next strong supports at 146.30 and 145.84 (Fibo 38.2%/daily cloud base).

Weakening daily studies (south-heading 14-d momentum is travelling deeply into negative territory/converged daily Tenkan/Kijun-sen are about to form a bear-cross) support bears, though the action may slow due to oversold conditions.

Limited upticks should be ideally capped by broken 55DMA (149.28) to keep bears in play and offer better selling opportunities.

Only sustained break above 150 level would sideline immediate downside threats.

Res: 148.80; 149.28; 150.00; 150.38.

Sup: 147.29; 146.51; 146.30; 145.84.

AUD/USD Extends Gains, RBA Minutes Next

- Australian dollar rises to 13-week high

The Australian dollar is in positive territory on Monday. In the European session, AUD/USD is trading at 0.6553, up 0.59%. The Aussie is flexing its muscles, gaining some 3% in the past week.

Investors eye RBA minutes

The Reserve Bank of Australia releases the minutes of the meeting earlier this month on Tuesday. There wasn’t much of a surprise as the RBA raised rates by a quarter-point to 4.35%, but the Australian dollar dropped sharply in the aftermath, which is an unusual move after a rate hike. Investors jumped all over the language of the rate statement, which suggested that the bar had risen for an additional rate hike. Interestingly, the statement also warned that inflation was “too high” and the “risk of inflation remaining higher has increased”, but investors ignored this hawkish assessment.

The RBA minutes may provide more clarity on whether rates have peaked. The markets are betting that the tightening cycle is over, but if the minutes signal that rates could go up, the Australian dollar could get a boost. As for 2024, the markets are expecting a rate cut, but the RBA is still trying to convince the markets that rate hikes are on the table and it isn’t discussing trimming rates.

Just a month ago, 10-year US Treasuries were trading at 4.98%, but have fallen to 4.44% at present. The lower yields have made US Treasuries less attractive and the US dollar has fallen against the majors recently, including the Australian dollar.

The FOMC minutes will be released on Wednesday and the markets will be combing through, looking for hints about upcoming rate decisions. Despite the Fed insisting that rate hikes remain on the table, the markets are confident that Fed policy will be less restrictive in the first half of 2024. According to the CME’s FedWatch tool, there is a 100% likelihood of a pause in December, with a 30% chance of a rate cut in March 2024, followed by a 64% chance in May.

AUD/USD Technical

- There is resistance at 0.6587 and at 0.6600

- 0.6470 and 0.6397 are providing support

Bundesbank report: Inflation likely to hover around current level

The latest monthly report from Bundesbank presents a mixed outlook for the German economy, highlighting persistently high inflation and a slow yet expected recovery.

According to the report, headline inflation at 3.0% and core inflation at 4.2% are "still well above historical average." The Bundesbank anticipates that the inflation rate is "likely to fluctuate around its current value in the coming months," indicating ongoing price stability concerns.

The report forecasts that a slight economic recovery is "only expected after the turn of the year". This recovery is expected to be driven by an increase in real net income of private households, buoyed by significant wage hikes a reduction in price pressures. Despite anticipated cautious approach to spending by private households, there is expectation of gradual expansion in real consumption, which could bolster domestic economy.

The industrial sector, however, continues to face challenging conditions. The Bundesbank's report points to weak foreign demand and the lingering effects of previous energy price shocks as factors hampering production. Yet, there are initial signs of improvement on the horizon. The report notes that the basic trend in incoming orders suggests a potential stabilization in foreign demand.

Japanese Yen Improves to Six-Week High

- Japanese yen posts sharp gains on Monday

The Japanese yen is up for a third straight day on Monday and has climbed 2% against the US dollar in the current rally. In the European session, USD/JPY is trading at 148.40, down 0.84%.

Yen rebounds as US/Japan rate differential narrows

After falling to a one-year low last week, the yen has rebounded and is trading at a six-week high. The swing in favour of the yen has been driven by expectations that Fed policy will be less restrictive in the first half of 2024. According to the CME’s FedWatch tool, there is a 100% likelihood of a pause in December, with a 30% chance of a rate cut in March 2024, followed by a 64% chance in May.

The yen has received a boost as the US/Japan rate differential has decreased. Just a month ago, 10-year US Treasuries were trading at 4.98%, but have fallen to 4.44% at present. The lower yields have made US Treasuries less attractive to investors and the yen has capitalized on this sentiment. The FOMC minutes will be released on Wednesday and could provide some insights into the Fed’s future rate path.

The recent strength of the yen has tempered talk of intervention by Japan’s Ministry of Finance, which threatened to step in after the USD/JPY fell close to 152 last week. The yen has been showing sharp swings of late, raising the question of whether the yen’s recent upswing is sustainable.

Investors are also looking for hints from the Bank of Japan about tightening policy. The central bank has tried to dampen expectations for a shift in monetary policy, but there have been some subtle signals that the BoJ will exit negative rates in 2024.

USD/JPY Technical

- USD/JPY has pushed below support at 149.29 and is testing support at 148.54

- There is resistance at 150.22 and 151.25

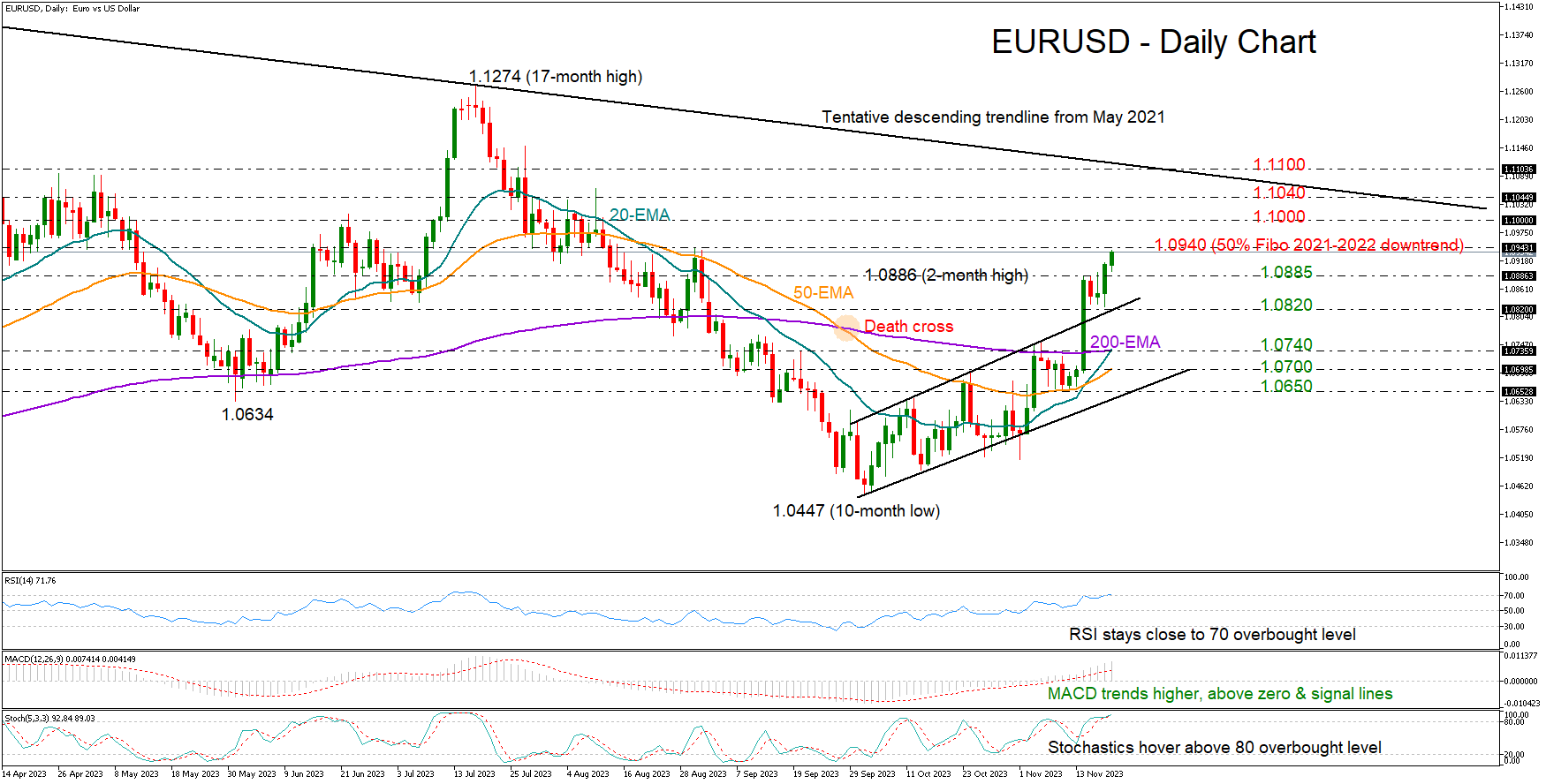

EURUSD Halfway to July’s Top; Tests 1.0940 Level

- EURUSD stretches to fresh highs ahead of important PMI data

- Overbought signals strengthen near August’s hurdles

EURUSD stepped into the 1.0900 zone after an exponential rally last week, marking a new 2½-month high of 1.0934 during Monday’s early European trading hours.

The pair has passed the halfway mark to July's peak from the October low and some profit-taking would not be a big surprise as the RSI and the stochastic oscillator are hinting at overbought conditions while the price is testing its August’s resistance levels.

Encouragingly though, the 20-day exponential moving average (EMA) has crossed above the 50-day EMA and is preparing for another intersection with the 200-day EMA, indicating the possibility of the positive trend continuing. Meanwhile, it would be also interesting to see if the 50- and 200-day EMAs will manage to reverse the death cross registered at the end of September.

The 1.0940 caution area, which overlaps with the 50% Fibonacci retracement of the 2021-2022 downtrend, is under examination. Breaking the wall could propel the bulls into an uptrend towards the 1.1000 psychological level. The former resistance at 1.1040 and the 1.1100 number could attract attention, especially the latter, as the tentative descending trendline from May 2021 happens to be there too.

Alternatively, a backward flip beneath 1.0885 might seek support around the upper band of the broken bullish channel at 1.0820. Should sellers dominate there, the decline could worsen towards the 20- and 200-day EMAs at 1.0740. The 50-day EMA might also be on guard near 1.0700. If the latter proves fragile, the next stop could be at the channel’s lower band seen at 1.0650.

All in all, EURUSD retains a positive monthly picture, with the bulls looking for a close above 1.0940 to run higher ahead of Eurozone’s flash business PMI figures due on Thursday. Given the overbought signals though, additional gains could come with some delay.

US 500 Index Reclaims 4,500, Threatening September Highs

- US 500 stock index posts fresh 2½ -month high

- But advance seems to be taking a breather

- Momentum indicators approach their overbought zones

The US 500 stock index (cash) has been staging an aggressive rally since it bottomed out in late October, piercing through the descending trendline that connects its recent lower highs. However, the uptrend appears to be on hold in the last few sessions as the short-term oscillators have approached overbought levels.

Should buyers attempt to push the price higher, immediate resistance could be found at the September peak of 4,540. Surpassing that zone, the index could ascend towards the 2023 high of 4,606. A break above that territory could open the door for the March 2022 high of 4,637.

On the flipside, if the price experiences a pullback, the September support of 4,430 could act as the first line of defence. Should that barricade fail, the bears could attack 4,342, which is the 23.6% Fibonacci retracement of the 3,486-4,606 upleg. Failing to halt there, the price may then challenge the 38.2% Fibo of 4,178.

Overall, the US 500 index has been facing strong upside pressures in the past three weeks, while the widening Bollinger bands are hinting at increased volatility. However, the price could enter a consolidation phase as the momentum indicators currently suggest that the advance is overdone.

NIKKEI Analysis: High of 33 Years

The Japanese stock market index, made up of shares of 225 companies, is showing high volatility today, attempting to break through the September high. Reuters wrote that the index had reached its highest level since 1990. The record is due to low rates from the Bank of Japan, which are helping the country's export-oriented industry (in particular, the automobile industry) and financial sector to grow.

At the same time, in various financial markets, Nikkei-related instruments may not have recorded a maximum in 33 years — the reason is liquidity and what appears to be the top of the market:

→ there was a massive liquidation of short positions;

→ major market participants recorded profits.

Therefore, the daily candlestick on European Monday morning has a long upper shadow. Note that today's high could be a false breakout of the September top, which in turn is a false breakout of the August top.

The chart shows that the price of NIKKEI is forming a tapering wedge pattern (shown with blue lines) pointing upward. A bearish breakout of this pattern could lead to the development of a downtrend.

Something similar (but in a mirror image) was recorded at the end of October, when a downward wedge formed on the chart (shown by red lines, more clearly visible on the 4-hour chart). The breakout of this wedge led to a rally of over 9%.

If the NIKKEI enters a downtrend, it could be fueled by rumors of an end to the low rate policy. Experts in the media are increasingly predicting this move by the Bank of Japan.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

ECB’s Wunsch: Early rate cut bets may trigger opposite action

ECB Governing Council member Pierre Wunsch today expressed skepticism regarding market expectations of an early easing of monetary policy. His comments highlight a crucial divergence between market forecasts and ECB's potential policy path in the face of ongoing inflationary pressures.

Wunsch described the market's anticipation of a reduction in ECB's deposit rate from the current 4% by April as "optimistic." He pointed out the necessity for ECB to either continue with the current rate or possibly increase it, contrary to market expectations.

He raised concerns about the implications of market bet on rate cuts. "Is it a problem if everybody believes we're going to cut?" he questioned. This could lead to "less restrictive monetary policy" which may then be insufficient, and eventually, "it increases the risk that you have to correct in the other direction."

Wunsch emphasized the ECB's readiness to adapt its strategy based on inflation trends. "If we arrive at the conclusion that inflation is not going down fast enough, we'll communicate it through our projection and through our communication," he stated.