Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2234; (P) 1.2258; (R1) 1.2302; More...

GBP/USD's strong rally today and breach of 1.2426 resistance indicates that rise from 1.2036 is resuming. Intraday bias is back on the upside. Decisive break of 38.2% retracement of 1.3141 to 1.2036 at 1.2458 will pave the way to 61.8% retracement at 1.2716. For now, further rise will remain in favor as long as 1.2185 support hold, in case of retreat.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 will argue that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

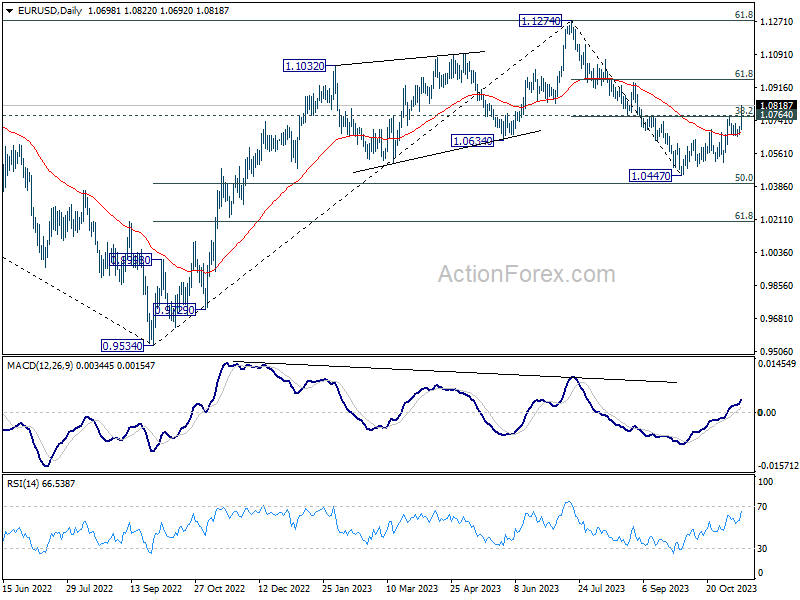

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0674; (P) 1.0690; (R1) 1.0715; More...

EUR/USD's rebound from 1.0447 resumed by breaking through 1.0755 resistance and intraday bias is back on the upside. The strong break of 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763) confirms that fall from 1.1274 has already completed. Intraday bias is back on the upside for 61.8% retracement at 1.0958 next. For now, near term outlook will stay bullish as long as 1.0655 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. However, break of 1.0447 will resume the fall to 61.8% retracement of 0.9543 to 1.1274 at 1.0199.

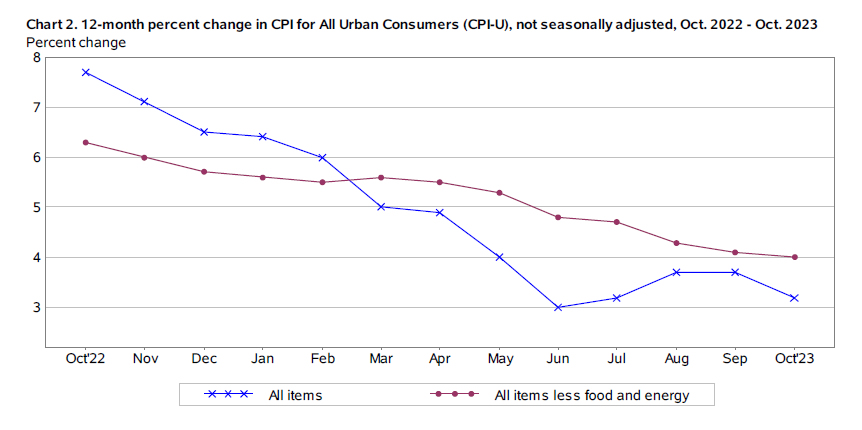

Market Jubilation as US CPI Signals Continuing Disinflation, Dollar Plunges

Investor sentiment is riding high in the wake of the latest US CPI report, with a notable surge in the DOW futures, climbing over 300 points, and a marked drop in 10-year yield, plunging from above 4.6% to below 4.5%. The report presented a picture of easing inflation, with both headline and core inflation rates falling short of market expectations. Significantly, core CPI has reached its lowest point in over two years. The weaker monthly price rise also bolsters the notion that disinflation is underway. This development could potentially revive Fed Chair Jerome Powell's "confidence" that the existing monetary policy is sufficiently restrictive to steer inflation back towards target.

In the currency markets, Dollar is experiencing broad decline following CPI release, with EUR/USD notably breaking through a critical resistance level at 1.076. The upbeat risk sentiment is propelling Australian and New Zealand Dollars, while other European currencies are also exhibiting strong performance. Canadian Dollar and Japanese Yen, despite trailing behind, are still recording substantial gains against the greenback.

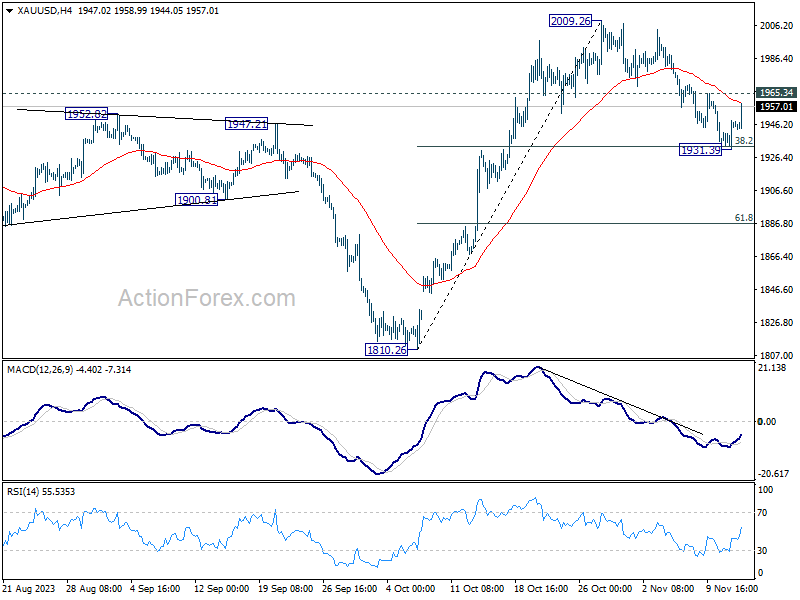

From a technical perspective, the significant rebound in Gold, propelled by Dollar's weakness, suggests that the correction from 2009.26 high might have concluded at 1931.39. This turnaround occurred after Gold found support from 38.2% retracement of 1810.26 to 2009.26 at 1933.24. Focus is now on 1965.34 resistance. A decisive break through here would strengthen the bullish scenario and set the stage for a retest of 2009.26 high.

In Europe, at the time of writing, FTSE is down -0.34%. DAX is up 0.50%. CAC is up 0.12%. Germany 10-year yield is down -0.0727 at 2.648. Earlier in Asia, Nikkei rose 0.34%. Hong Kong HSI dropped -0.17%. China Shanghai SSE rose 0.31%. Singapore Strait Times dropped -0.07%. Japan 10-yer JBG yield fell -0.0202 to 0.856.

US CPI core down to 4%, lowest since Sep 2021

US CPI slowed from 3.7% yoy to 3.2% yoy in October, below expectation of 3.3% yoy. CPI core (less food and energy) fell from 4.1% yoy to 4.0% yoy, below expectation of being unchanged at 4.1% yoy. That's the lowest core CPI reading since September 2021. Energy index was down -4.5% yoy. Food index was up 3.3% yoy.

For the month, CPI was flat at 0.0% mom, below expectation of 0.1% mom. CPI core rose 0.2% mom, below expectation of 0.3% mom. Energy index fell -2.5% mom. Food index rose 0.3% mom.

Germany's ZEW economic sentiment surges to 9.8, suggesting bottoming out

Germany's ZEW Economic Sentiment soared to 9.8 in November, far surpassing the anticipated 4.9, signaling increasing optimism among financial market experts. However, Current Situation Index barely moved, nudging from -79.9 to -79.8, and falling short of expected -75.5.

Eurozone's ZEW Economic Sentiment experienced a similar upswing, rising from 2.3 to 13.8, well ahead of the forecast of 6.1. Despite this, Current Situation Index in Eurozone showed a decline, dropping by -9.4 points to -61.8.

Achim Wambach, ZEW President, noted that while current economic conditions are still challenging, there's growing optimism. He added, "These observations support the impression that the economic development in Germany has bottomed out."

The increase in economic expectations is supported by a more positive view of the German industrial sector and both domestic and foreign stock markets. Additionally, "inflation and short- and long-term interest rates also appear to have reached turning points in expectations," he added.

SNB's Jordan: Price stability not ensured, won't hesitate to tighten further

In today's remarks at a central bank conference in Zurich, SNB Chairman Thomas Jordan warned that "price stability may not yet be ensured." He pledged that the central bank "will not hesitate to tighten monetary policy further if necessary."

This statement comes as inflation have dipped and interest rates have risen compared to last year, presenting a challenging environment for policy to balance the risk of tightening too much and too little.

"Given the high uncertainty regarding the economic outlook, there is no clearly mapped-out path for monetary policy in the near future," he remarked.

With SNB's next policy meeting scheduled for December 15, market expectations currently lean towards maintaining policy rate at 1.75%.

UK payrolled employment rose 33k in Oct, unemployment rate unchanged at 4.2% in Sep

UK payrolled employment rose 33k, or 0.1% mom in October. Over the year, payrolled employment rate 398k or 1.3% yoy. Median monthly pay rose 5.9% yoy, down from prior month's 6.0% yoy. Claimant count rose 17.8k, above expectation of 15.0k.

In the three months to September, unemployment rate was unchanged at 4.2%, matched expectations. Average earnings including bonus rose 7.9% yoy, above expectation of 7.4%, slowed from prior 8.2%. Average earnings excluding bonus rose 7.7% yoy, matched expectations, slowed from prior month's 7.8%.

Australia's consumer sentiment plummets post RBA rate hike

Australia's Westpac Consumer Sentiment Index saw a significant decline in November, dropping by -2.6% mom to 79.9, reflecting a deepening pessimism among consumers.

Westpac attributed this drop to the recent RBA rate hike, noting a -6% decrease in confidence during the survey period. Despite the overarching pessimism, labor market confidence and housing-related sentiment remained relatively stable.

Westpac further commented, "The Reserve Bank Board next meets on December 5. The November Consumer Sentiment survey highlights the weak and uneven conditions across Australia's consumer sector. How this plays out for wider domestic demand in the context of strong population growth is something the Board will need to consider as it acts to ensure inflation returns to target."

Australia NAB business confidence dips to -2, conditions resilient

In Australia, NAB reported a dip in Business Confidence for October, falling from 0 to -2. However, Business Conditions saw a slight improvement, rising from 12 to 13. Notably, trading conditions increased from 18 to 20, and profitability conditions improved from 9 to 12, while employment conditions slightly decreased from 9 to 8.

NAB Chief Economist Alan Oster commented, "Business conditions remain healthy, picking up in October and still well above average. Still, business confidence remained soft in the month, still well below average at -2 index points." He highlighted the persistent gap of 10-15 index points between current conditions and the more forward-looking confidence indicator, emphasizing that "Businesses clearly remain cautious about the outlook for the economy despite the resilience we are seeing."

The report also noted a slowdown in price and cost growth. Labour cost growth eased to 1.8% in quarterly equivalent terms, and purchase cost growth declined to 1.8%. Retail price growth remained stable at 1.9%, while overall price growth eased to 1.0%, marking the slowest rate since July 2020.

Oster added, "The Q3 CPI showed inflation had been persistent through the middle of the year and the survey suggests this remained the case heading into Q4. We still expect to see gradual moderation over time but it will be a protracted process, especially given the resilience of domestic demand thus far."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0674; (P) 1.0690; (R1) 1.0715; More...

EUR/USD's rebound from 1.0447 resumed by breaking through 1.0755 resistance and intraday bias is back on the upside. The strong break of 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763) confirms that fall from 1.1274 has already completed. Intraday bias is back on the upside for 61.8% retracement at 1.0958 next. For now, near term outlook will stay bullish as long as 1.0655 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. However, break of 1.0447 will resume the fall to 61.8% retracement of 0.9543 to 1.1274 at 1.0199.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Nov | -2.60% | 2.90% | ||

| 00:30 | AUD | NAB Business Conditions Oct | 13 | 11 | 12 | |

| 00:30 | AUD | NAB Business Confidence Oct | -2 | 1 | 0 | |

| 07:00 | GBP | Claimant Count Change Oct | 17.8K | 15.0K | 20.4K | |

| 07:00 | GBP | ILO Unemployment Rate (3M) Sep | 4.20% | 4.20% | 4.20% | |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Sep | 7.90% | 7.40% | 8.10% | 8.20% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Sep | 7.70% | 7.70% | 7.80% | |

| 07:30 | CHF | Producer and Import Prices M/M Oct | 0.20% | 0.10% | -0.10% | |

| 07:30 | CHF | Producer and Import Prices Y/Y Oct | -0.90% | -1.00% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | -0.10% | -0.10% | -0.10% | |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 P | 0.30% | 0.20% | 0.20% | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Nov | 9.8 | 4.9 | -1.1 | |

| 10:00 | EUR | Germany ZEW Current Situation Nov | -79.8 | -75.5 | -79.9 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | 13.8 | 6.1 | 2.3 | |

| 13:30 | USD | CPI M/M Oct | 0.00% | 0.10% | 0.40% | |

| 13:30 | USD | CPI Y/Y Oct | 3.20% | 3.30% | 3.70% | |

| 13:30 | USD | CPI Core M/M Oct | 0.20% | 0.30% | 0.30% | |

| 13:30 | USD | CPI Core Y/Y Oct | 4.00% | 4.10% | 4.10% |

US CPI core down to 4%, lowest since Sep 2021

US CPI slowed from 3.7% yoy to 3.2% yoy in October, below expectation of 3.3% yoy. CPI core (less food and energy) fell from 4.1% yoy to 4.0% yoy, below expectation of being unchanged at 4.1% yoy. That's the lowest core CPI reading since September 2021. Energy index was down -4.5% yoy. Food index was up 3.3% yoy.

For the month, CPI was flat at 0.0% mom, below expectation of 0.1% mom. CPI core rose 0.2% mom, below expectation of 0.3% mom. Energy index fell -2.5% mom. Food index rose 0.3% mom.

Pound Shrugs as Wage Growth Cools, US Inflation Next

- UK wage growth eases

- US inflation expected to fall to 3.3%

The British pound has edged higher on Tuesday. In the European session, GBP/USD is trading at 122.91, up 0.10%.

UK job growth improves, wage growth ease

The UK labour market remains strong, despite high inflation and elevated interest rates. The unemployment rate was unchanged at 4.2% in the three months to September, just below the market consensus of 4.3%. Wage growth excluding bonuses eased to 7.7% y/y in the three months to September, after a 7.9% gain in the previous two periods. This was the first decline since January and is an encouraging sign that inflation is moving lower.

The UK will release inflation data on Wednesday, with headline inflation expected to fall to 4.8% y/y in October, down from 6.7%. Core inflation is projected to fall from 6.1% to 5.8%. If inflation falls as expected, it will be easier for the Bank of England to pause for a second straight time at the December meeting and that would put pressure on the pound.

The US releases its inflation report later today and the release could provide insights as to the Fed’s rate path. Headline inflation is expected to rise 3.3% y/y in October, compared to 3.7% in September. The core rate is expected to remain unchanged at 4.1% y/y.

If inflation falls, it will support the market’s expectation for rates cutes in mid-2024 and the US dollar could lose ground. Conversely, a hot inflation print would support the Fed’s stance of ‘higher for longer’ and would push off expectations of a rate cut to later in 2024, which would be bullish for the US dollar. The markets expect the Fed to pause at the December meeting, with just a 14% chance of a quarter-point hike, according to the CME Group’s FedWatch Tool.

GBP/USD Technical

- GBP/USD is testing resistance at 1.2281. Above, there is resistance at 1.2374

- 1.2175 and 1.2133 and are providing support

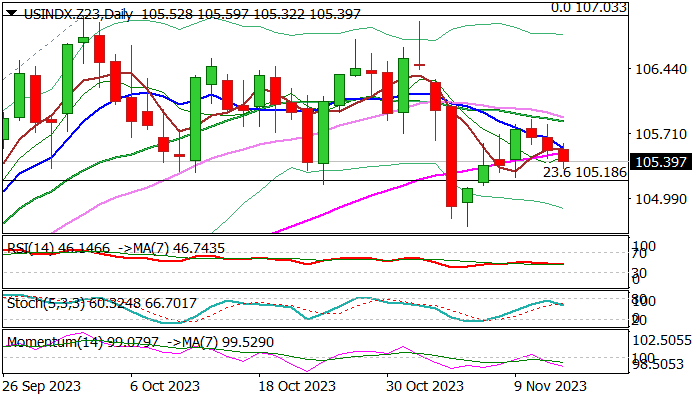

Dollar Index Standing at the Back Foot on Tuesday Morning

The dollar index is standing at the back foot on Tuesday morning, extending pullback from last week’s recovery high (150.87), with slower pace expected ahead of key release – US inflation report, due later today.

Daily studies weakened as the price eventually broke into rising and thick daily cloud and negative momentum is rising, marking a negative signal and keeping the downside vulnerable, while near-term action stays capped by daily cloud top (105.35) reinforced by daily Kijun-sen.

Initial support lays at 105.18 (Fibo 23.6% of 99.20/107.03 rally) guarding more significant Nov 6 low (104.66) violation of which would risk deeper pullback and expose key supports at 104.00 zone (Fibo 38.2% . 100DMA).

Larger picture, however, remains dollar favored as the greenback enjoys support from the US rates being higher than most of major central banks (except (BoE) and recent renewed hawkishness in Fed’s view of monetary policy, suggesting that the US central bank would keep high rates for some time.

US inflation report will be closely watched for fresh signals, with expectations that CPI will ease to 3.3% in Oct from 3.7% last month, but core CPI which excludes volatile food and energy components is expected to stay unchanged at 4.1% y/y, which could be seen as discouraging for those who expect rate cuts in the near future.

Res: 105.54; 105.81; 106.31; 106.67.

Sup: 105.32; 105.18; 104.66; 104.32.

Aussie Steady as Confidence Data Softens

- Consumer confidence slides

- Business confidence eases while business conditions improve

The Australian dollar has edged lower on Tuesday. In the European session, AUD/USD is almost unchanged, trading at 0.6376.

Australian consumer, business confidence eases

Australian consumers have been hit hard by high inflation and steep interest rates, so it’s no surprise that consumers are deeply pessimistic about the economy. The Westpac Consumer Sentiment index declined by 2.6% in November, down from 82 to 79. The RBA’s recent rate hike certainly didn’t boost confidence, as consumers expect mortgage rates to continue rising over the next 12 months.

The NAB Business Confidence index fell to -2 in October, down from a revised zero in September. This was below the market consensus of 1 and was the lowest level since May. The silver lining was an improvement in business conditions, which rose in October from 12 to 13.

The Reserve Bank of Australia raised rates earlier this month after four consecutive pauses. Is the RBA done with its tightening cycle? The central bank meets next on December 5th and has stressed that future rate decisions will be based on the data. Australia releases retail sales and inflation reports a week prior to the meeting, and these releases could determine whether the RBA hikes again or pauses.

The US releases the October inflation report later today. The release could provide clues as to how long the Fed plans to keep rates at elevated levels. Headline inflation is expected to rise 3.3% y/y, compared to 3.7% in September. The core rate is expected to remain unchanged at 4.1% y/y.

The markets have priced in a rate cut in mid-2024 and an unexpected inflation reading would likely lead to the repricing of a rate cut. The Fed has pushed back against talk of a rate cut, as inflation remains well above the 2% target. The markets haven’t been listening to the Fed, but they’ll be keeping a close eye on the inflation report.

AUD/USD Technical

- AUD/USD continues to put pressure on support at 0.6351. Below, there is support at 0.6292

- 0.6408 and 0.6476 are the next resistance lines

Germany’s ZEW economic sentiment surges to 9.8, suggesting bottoming out

Germany's ZEW Economic Sentiment soared to 9.8 in November, far surpassing the anticipated 4.9, signaling increasing optimism among financial market experts. However, Current Situation Index barely moved, nudging from -79.9 to -79.8, and falling short of expected -75.5.

Eurozone's ZEW Economic Sentiment experienced a similar upswing, rising from 2.3 to 13.8, well ahead of the forecast of 6.1. Despite this, Current Situation Index in Eurozone showed a decline, dropping by -9.4 points to -61.8.

Achim Wambach, ZEW President, noted that while current economic conditions are still challenging, there's growing optimism. He added, "These observations support the impression that the economic development in Germany has bottomed out."

The increase in economic expectations is supported by a more positive view of the German industrial sector and both domestic and foreign stock markets. Additionally, "inflation and short- and long-term interest rates also appear to have reached turning points in expectations," he added.

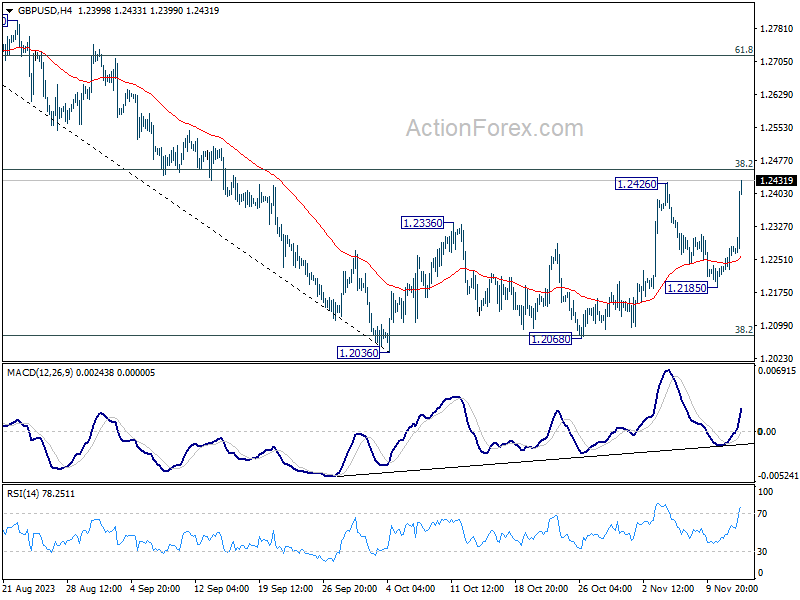

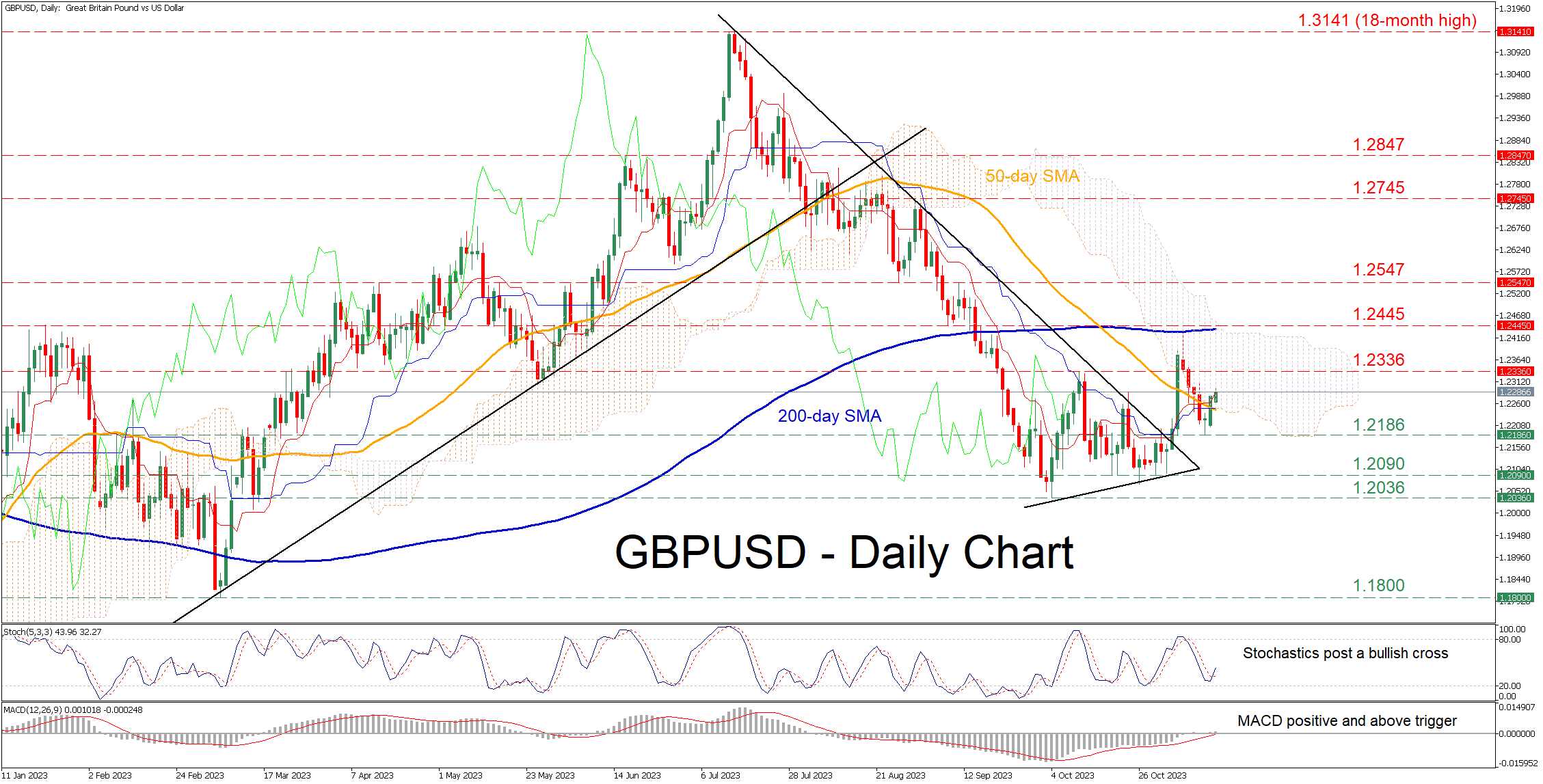

GBPUSD Enters Ichimoku Cloud after Claiming 50-SMA

- GBPUSD breaks out of triangle but 200-day SMA curbs advance

- Despite a mild pullback, the bulls conquer the 50-day SMA

- Oscillators suggest that positive momentum is picking up

GBPUSD had been forming a profound structure of lower highs and lower lows since its 16-month peak of 1.3141. Although the pair’s latest attempt to recoup some losses got rejected by the 200-day simple moving average (SMA), buyers managed to halt the retreat and reclaim the 50-day SMA.

Should buying interest intensify further, the October peak of 1.2336 could act as the first barrier for the price to clear. Surpassing that zone, the pair could advance towards the December-January resistance zone of 1.2445, which lies close to the 200-day SMA and rejected the latest advance. A break above that level could open the door for the 1.2547 hurdle.

Alternatively, if the price moves lower, initial declines could cease around the recent support of 1.2186. Failing to halt there, the pair may challenge the 1.2090 support territory ahead of the eight-month low of 1.2036. Even lower, the March bottom of 1.1800 could provide downside protection.

In brief, GBPUSD seems to be regaining some traction as the momentum indicators have turned positive in the last couple of sessions. However, the bearish long-term pattern remains intact.

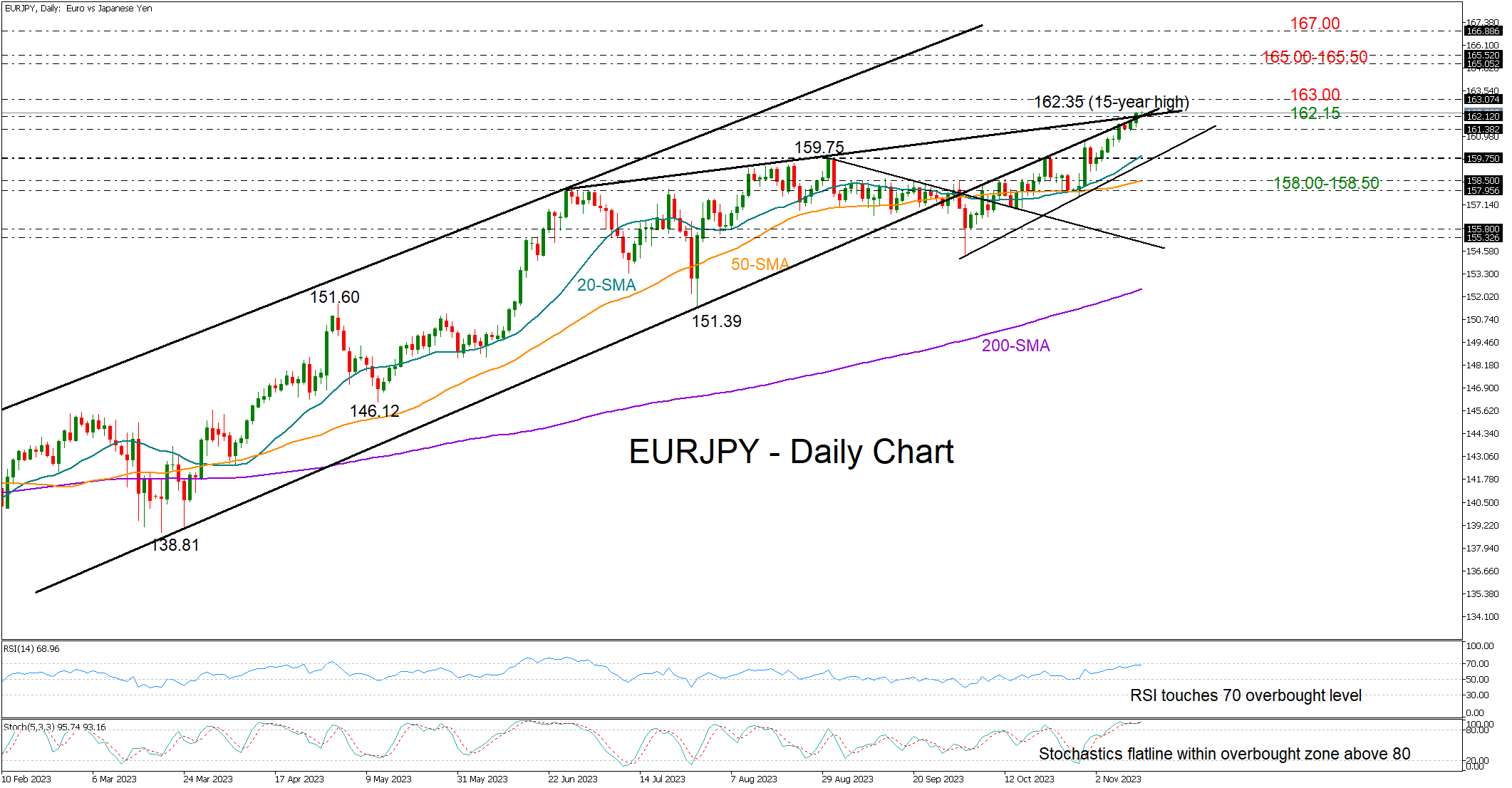

EURJPY Uptrend Continues But Carries Risks

- EURJPY hits new highs, but still close to caution zone

- Next resistance could emerge near 163.00

EURJPY surged to 162.35 on Monday–the highest level since August 2008–surpassing the caution trendline zone, though marginally.

The ongoing upleg seems secure, but the overbought signals from the RSI and stochastic oscillator raise the risk of a negative reversal.

The 163.00 round level, which capped bullish actions back in August 2008, will be closely watched in the coming sessions. If the bulls breach that wall, the pair might power up to the 165.00-165.50 constraining zone last seen in June 2007-August 2008, while higher, the spotlight might turn to the 167.00 bar.

If the price slides back below the 162.00 mark, last week’s base of 161.35 could cancel any drops towards the previous high of 159.75 and the 20-day simple moving average (SMA). A step lower and beneath the tentative support trendline October seen at 159.45 would neutralize the bullish short-term picture, likely motivating another bearish correction towards the 50-day SMA and the 158.00-158.50 restricted territory. If the latter proves fragile too, the pair could experience an aggressive downfall.

All in all, EURJPY must sustain strength above 162.00 and perhaps cross above 163.00 to raise fresh buying traction in the short-term, as downside risks have not entirely faded.