Sample Category Title

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8685; (P) 0.8708; (R1) 0.8727; More....

EUR/GBP is extending the consolidation pattern from 0.8752, with fall from 0.8754 as the third leg. Deeper decline could still be seen to 0.8648 support. But strong support should be seen around there to complete the consolidation and bring rebound. On the upside, decisive break of 0.8752/4 will resume whole rise from 0.8491 to 0.8874 resistance next.

In the bigger picture, current development suggests that whole down trend from 0.9267 (2022 high) has completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. This will remain the favored case as long as 0.8614 support holds.

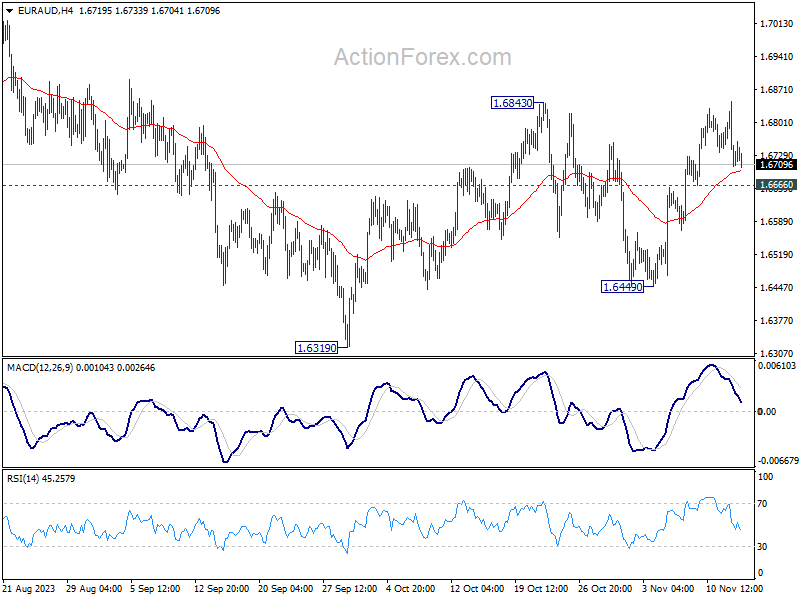

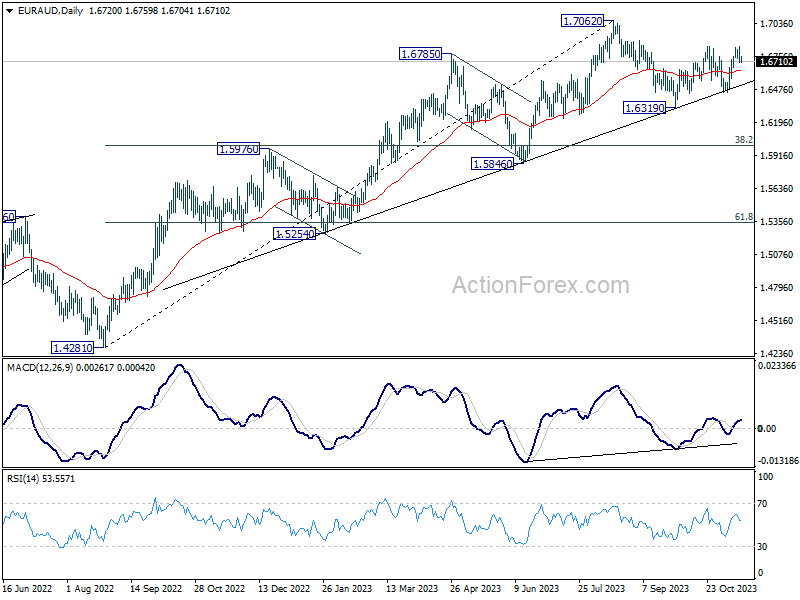

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6672; (P) 1.6756; (R1) 1.6802; More...

EUR/AUD fails to break through 1.6843 resistance decisively and retreated. Intraday bias is turned neutral first. On the upside, sustained break of 1.6843 will resume the rebound from 1.6319 for retesting 1.7062 high next. On the downside, however, below 1.6666 minor support will turn bias back to the downside for 1.6449 support instead.

In the bigger picture, while 1.7062 is a medium term top, there is no clear sign of trend reversal as EUR/AUD continues to draw strong support from the medium term trend line. Break of 1.7062 will resume the larger up trend from 1.4281 (2022 low) to 1.7691 fibonacci level. Nevertheless, break of 1.6449 support will argue that deeper correction is underway to 38.2% retracement of 1.4281 to 1.7062 at 1.6000.

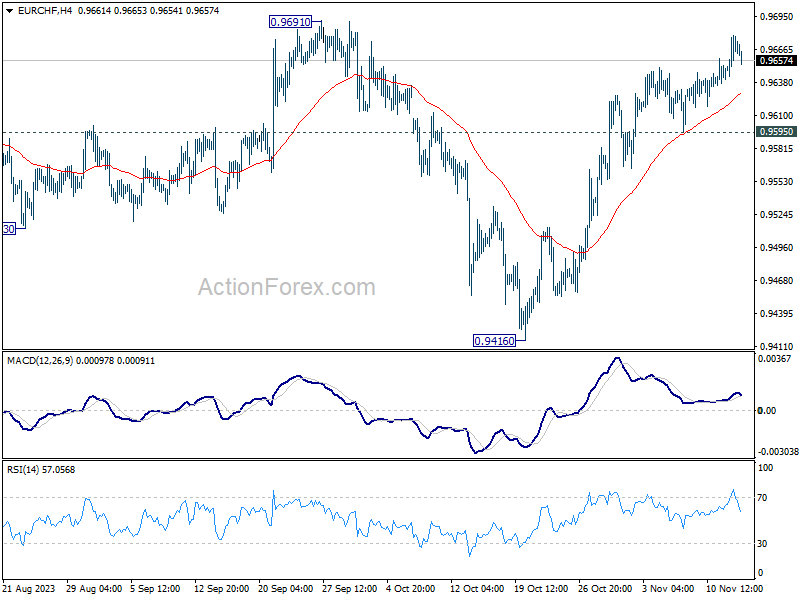

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9652; (P) 0.9666; (R1) 0.9688; More...

EUR/CHF's rally from 0.9416 is still in progress and intraday bias stays on the upside for 0.9691 resistance. Firm break there will argue that whole decline from 1.0095 has completed, just ahead of 0.9407 support (2022 low). Nevertheless, break of 0.9595 support will indicate short term topping, and turn bias back to the downside for deeper pull back.

In the bigger picture, fall from 1.0095 (2023 high) might have completed at 0.9416, just ahead of 0.9407 support (2022 low). Sustained break of 0.9691 cluster resistance (38.2% retracement of 1.0095 to 0.9416 at 0.9675) will pave the way to 61.8% retracement at 0.9836 and above. However, rejection by 0.9691 will maintain medium term bearishness for another test on 0.9407 at least.

Inflation Fever Breaks

The Federal Reserve (Fed) doves got a big energy boost yesterday by a slightly lower-than-expected inflation report. The headline inflation fell to 3.2% in October from 3.7% printed a month earlier, and core inflation eased to 4% from 4.1% printed a month earlier. Services excluding housing and energy costs – the so-called super core figure closely watched by the Fed - rose only 0.2% and shelter costs rose only 0.3%, down from a 0.6% advance printed a month earlier. The soft set of inflation print cemented the expectation that the Fed is done hiking the interest rates. The US 2-year yield – which best captures the rate bets – tanked 24bp to 4.81%. The 10-year slipped below 4.50% and activity on Fed funds futures gives around 95% chance for a no rate hike in December. That probability stood at around 85% before yesterday’s US CPI data.

In equities, the S&P500 jumped past its 100-DMA, spiked above the 4500 mark, and closed the session a few points below this level. Nasdaq 100 extended its gain to 15850. In the FX, the US dollar took a severe hit. The index fell 1.50% on Tuesday, pulled out a major Fibonacci support and sank into the medium-term bearish consolidation zone. The EURUSD jumped to almost the 1.09 level. Yes, there is no mistake – to nearly 1.09 level, and Cable flirted with the 1.25 resistance. What a day!

A small parenthesis on UK inflation

Good news came from Britain this morning, as well. Inflation in the UK fell 6.7% to 4.6% in October, lower than the 4.7% penciled in by analysts. Core inflation also eased more than expected to 5.7%. There is growing evidence that the major central banks’ efforts are bearing fruit. Cable is sold after the CPI data, but the pullback will likely remain short-lived if the USD appetite continues to wane globally.

Back to US: Retail sales, big retail earnings & US political jitter

Yesterday’s rush to open fresh long US Treasury positions was likely intensified by a hurry to cover short positions. We shall see a correction in the US yields, as the Fed members still maintain their position for ‘higher for longer’ interest rates. But the market position is clear. The pricing now suggests a 50bp cut from the Fed by July next year; the sweet and sour cocktail of softening jobs market and easing inflation suggests that the Fed’s next move will probably be a rate cut, rather than a rate hike.

So yes, ladies and gentlemen, the way is being paved for a potential Santa rally this year. But the Fed will continue to calm down the game, and any strength in the US economic data should reinforce the ‘high for long’ rhetoric and tame appetite.

Investors will watch the US retail sales data today. A strong figure could pour cold water on heated Fed cut bets. A soft figure, on the other hand, could bring in more buyers to US bond markets.

On the individual front, Home Depot shares rallied more than 5% yesterday. Earnings and revenue narrowed and the company released a cautious year-end guidance, but the results were better than expected. Target is due to report today, and Walmart on Thursday.

To add another layer of complexity – on top of the economic data and corporate earnings – the US political scene will impact bond pricing in the next few days. The US politicians try to avoid a government shutdown by Friday. The latest news suggests that the odds of shutdown diminished yesterday as House Speaker Mike Johnson gained more Democratic support for his interim funding plan. The interim plan however excludes aid for Ukraine, aid for Israel and could lead to a two-step shutdown at the start of next year. And it does not include the steep spending cuts that the hardcore Republicans are looking for. In summary, the political mess continues.

In the best-case scenario, the US politicians will agree on another short-term relief package and avoid a government shutdown, push away the threat of another rating cut – from Moody’s this time. The latter would maintain appetite in US bonds and support a further rally in the US stocks. In the worst-case scenario, the US government will stop its operations by the end of this week and the political chaos will lead to a bounce in US yields and stall the equity rally.

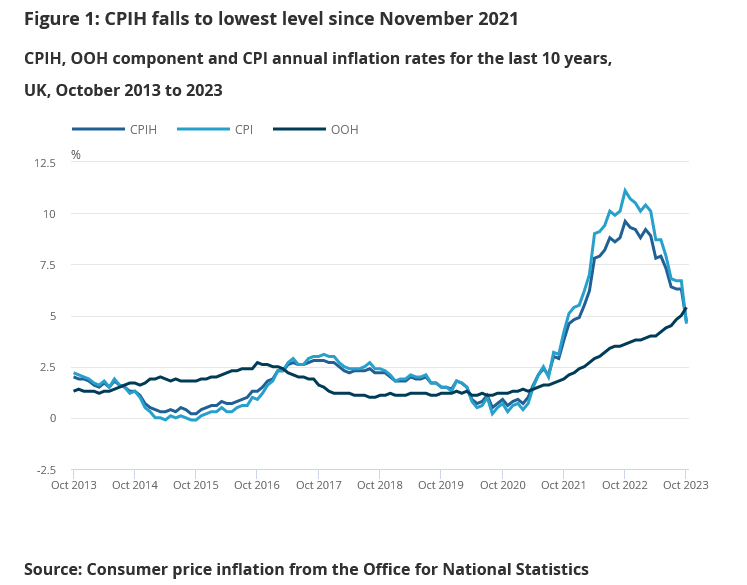

UK CPI eases significantly to 4.7% in Oct, another step to BoE’s target

UK CPI showed a marked slowdown in October, dipping below market expectations. The annual CPI rate decelerated from 6.7% yoy to 4.6% yoy , falling short of the anticipated 4.7% yoy. This decline reflects a broader trend of easing inflationary pressures, as evidenced by a flat monthly CPI rate of 0.0% mom, which was below the forecasted 0.2% mom.

Delving deeper, core CPI, which excludes volatile items such as energy, food, alcohol, and tobacco, mirrored this downtrend. It slowed from an annual rate of 6.1% yoy to 5.7% yoy, again undershooting the expected 5.8% yoy.

A notable aspect of the report was the significant drop in CPI goods annual rate, which plummeted from 6.2% yoy to 2.9% yoy. Meanwhile, services sector also saw a decline, albeit less pronounced, with CPI services annual rate reducing from 6.9% yoy to 6.6% yoy.

The most substantial downward pressure on the annual rates came from housing and household services sector. Notably, CPI annual rate in this category recorded its lowest level since record-keeping began in January 1950. Additionally, food and non-alcoholic beverages sector contributed to the downward trend, marking its lowest annual rate since June 2022.

Was Inflation Transitory After All?

Market movers today

Joe Biden and Xi Jinpeng meet in San Francisco.

US retail sales will be the first hard data point on how consumption has developed after the very strong September. Leading indicators and weekly credit card data point towards slowing growth, a new experimental CNBC/NRF indicator shows -0.08% m/m. US PPI inflation should decline on headline due to energy prices but core is expected at 0.3% m/m, same as in September. The Empire manufacturing PMI is a warm up to the national PMI next week, but not strongly correlated with it.

Industrial production figures for the euro area for September will shed light on how much of the decline in Q3 GDP manufacturing was accountable for.

UK October inflation is released where we expect a large downtick in headline inflation given the downtick in household energy bill and base effects. Core and in particular service inflation will however be the main market movers as the BoE sees these as key indicators of inflation persistence.

Japanese foreign trade data for October is released early Thursday morning.

The 60 second overview

The US House of Representatives reached a deal on a temporary budget bill such that a government shutdown on Friday is avoided. However, the deal is lasting only till January next year, but was passed with a majority of Republicans and Democrats in the House. This should limit the risk for a downgrade of US Treasuries for now.

The preliminary Q3 GDP numbers from Japan surprised on the downside as the annualized growth was -2.1% Q/Q compared to expectations of -0.4% Q/Q. Hence, the numbers show the challenge for Bank of Japan given the rise in inflation.

The Chinese central bank left policy rates unchanged this morning, but gave a big injection of cash through the medium-term lending facility (MLF). The amount (USD 83bn) was the largest amount since 2016.

Yesterday's, US October CPI surprised to the downside both in headline (+0.04% m/m SA; consensus +0.1%, Sep +0.40%) and core (+0.23% m/m SA; consensus +0.3%; Sep +0.32%) terms. Shelter accounted for the majority of the downtick in core inflation, but promisingly for the Fed, price pressures in the broader services sector also appeared to moderate. UAW's strike had little impact on car prices, and Core Goods CPI overall continued its modest decline. While realized inflation data clearly cooled in October, some inflation expectations measures still flagged upside risks. NFIB's small business survey showed that companies' price plans have risen further despite still bleak outlook for general business conditions, mirroring signals from University of Michigan's consumer survey last Friday. However, despite the broad-based easing in financial conditions seen yesterday after the CPI release, oil prices remained surprisingly stable, and the past weeks' decline should help with keeping both realized and expected inflation under control. Read more details in our monthly Global Inflation Watch - Signs of weaker demand ease inflation risks in October, 14 November.

Equities: Inflation relief sparked huge moves in the bond market, which in turn sparked an outright rally in equities. US surged about 2% and Europe 1.5%. This was a risk-on session with all sectors higher. Most notably a jump up in real estate and especially Nordics, with most names surging double digit. Cyclicals beat defensives and oversold utilities recovered. Positioning plays a part here too of course, as we have seen in slightly oversold conditions, which we have written a great deal about lately. Asian markets are surging in catch-up this morning while US futures are pointing slightly upwards.

FI: There was a broad-based rally in the global fixed income markets after the weaker than expected US inflation data as inflation may prove transitory after all. However, several Fed officials were out stating that there is some way to go and several market participants also warned that inflation might not go away that quickly and that the Federal Reserve should not cut rates too fast.

FX: The US CPI induced rally in global fixed income markets and the subsequent decline in the USD gave a substantial relief boost to risk appetite globally, which in turn strongly benefitted cyclically sensitive currencies such as ZAR, the CEEs and the Scandies. Also, the GBP benefitted while the CAD, CNH and naturally the USD were the clear underperformers with EUR/USD notably moving close to the 1.09 mark

Credit: Credit and equity markets rallied on Tuesday, after a more dovish than expected US inflation print. Itrax Main tightened 3.4bp to close at 70.5, while Itrax Xover tightened 14.6bp to close at 389.5bp (the lowest level since mid-September). Primary markets were once again fairly active, as was the case on Monday.

Nordic macro

Following yesterday's lower-than-consensus inflation print in Sweden, today's highlight is Prospera's inflation expectations survey. However, as it is the (small) monthly survey, its market impact is likely to be muted.

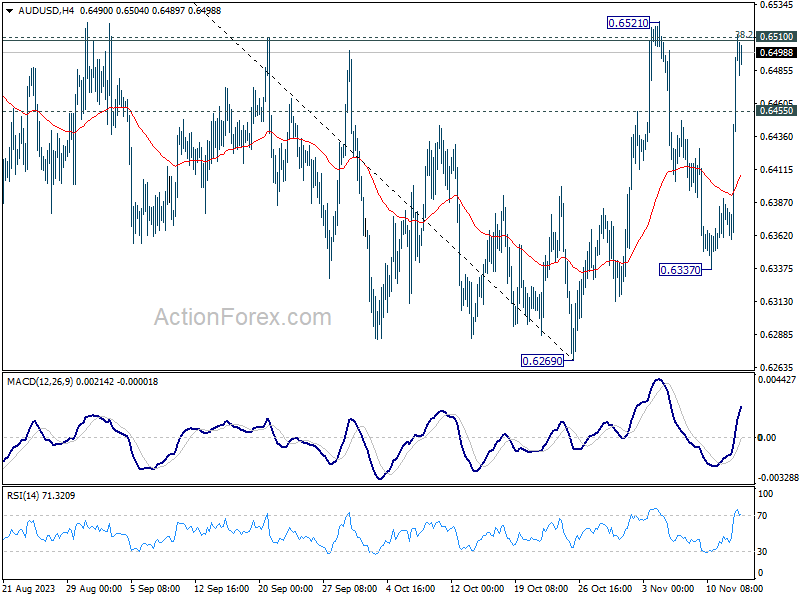

AUD/USD Daily Report

Daily Pivots: (S1) 0.6408; (P) 0.6461; (R1) 0.6560; More...

Intraday bias in AUD/USD stays on the upside at this point. Decisive break of 0.6510 cluster resistance (38.2% retracement of 0.6894 to 0.6269 at 0.6508) will argue that whole corrective fall from 0.7156 has completed with three waves down to 0.6269. Stronger rally should seen to falling channel resistance (now at 0.6684) next. On the downside, below 0.6455 minor support will turn intraday bias neutral first.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of the corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

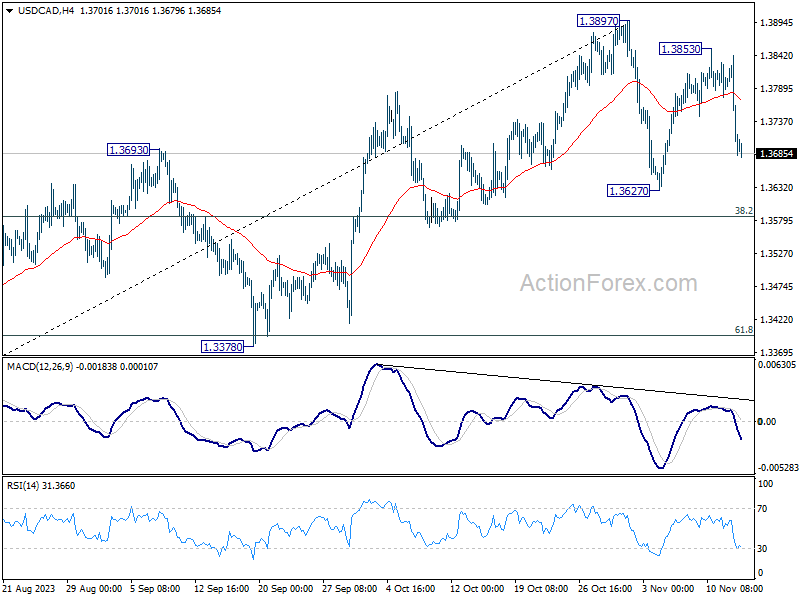

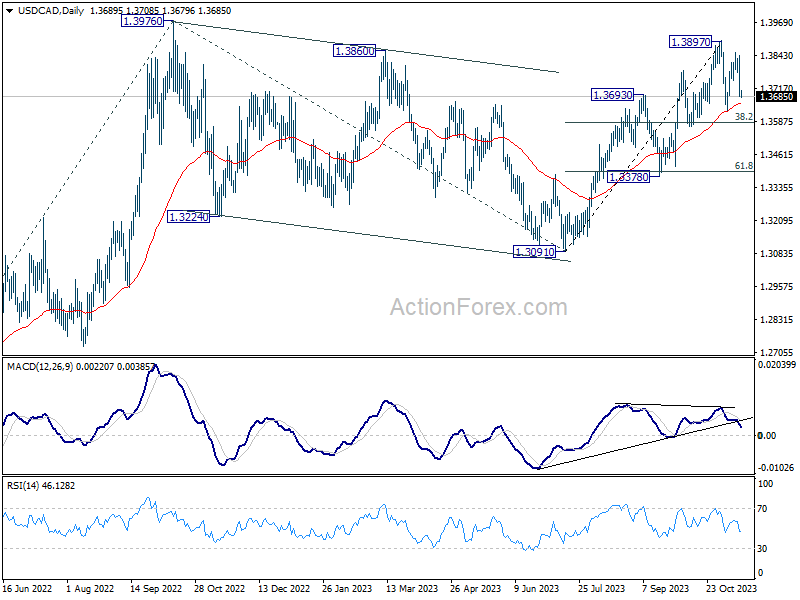

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3637; (P) 1.3741; (R1) 1.3796; More...

Intraday bias in USD/CAD remains on the downside for the moment. Fall from 1.3853 is seen as the third leg of the corrective pattern from 1.3897. Deeper fall would be seen to 1.3627 and possibly below. Strong support should be seen from 38.2% retracement of 1.3091 to 1.3897 at 1.3589 to bring rebound. Break of 1.3897 is expected at a later stage to resume larger rally.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will remain the favored case as long as 1.3378 support holds.

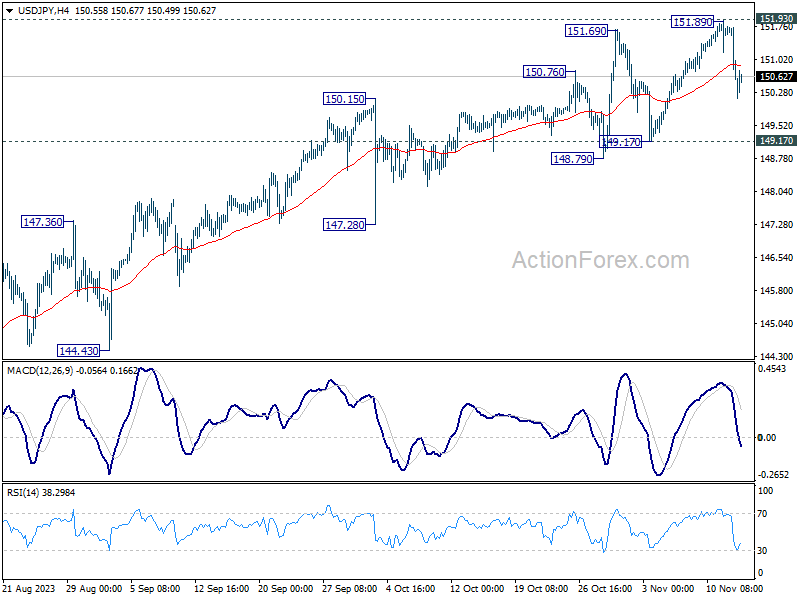

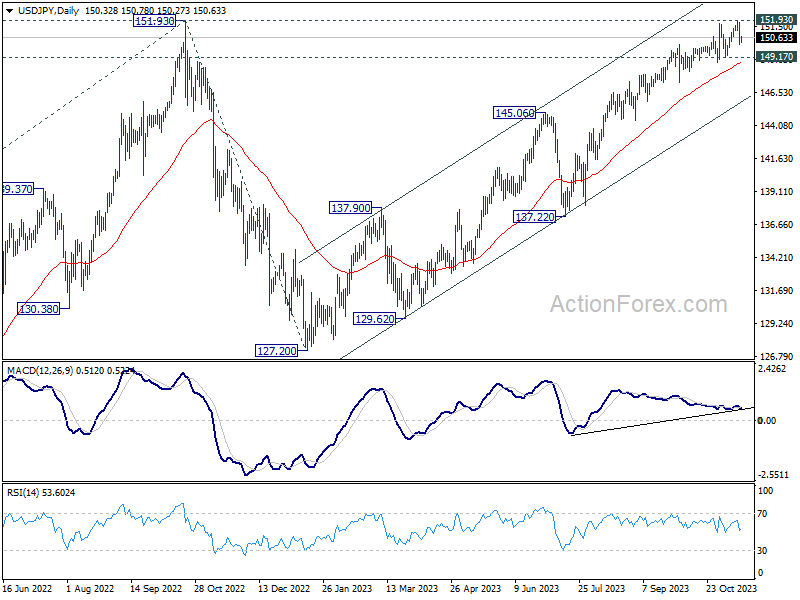

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.77; (P) 150.78; (R1) 151.39; More...

Intraday bias in USD/JPY remains neutral for the moment and some more sideway trading could be seen. Further rally is in favor as long as 149.17 support holds. On the upside, decisive break of 151.93 resistance will confirm resumption of long term up trend. Next target will be 157.69 projection level. However, firm break of 149.17 will be a sign of bearish reversal and bring deeper fall to 147.28 support first.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 (2021 low) to 151.93 from 127.20 at 157.69.

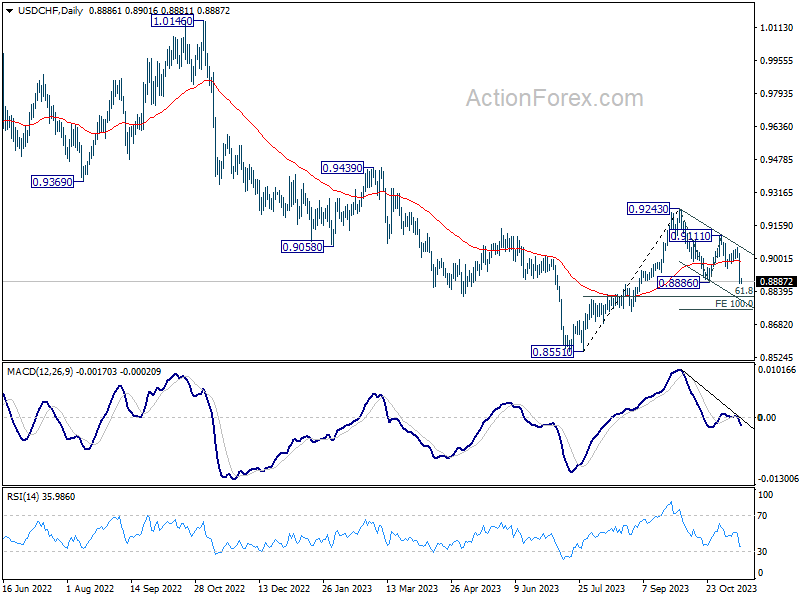

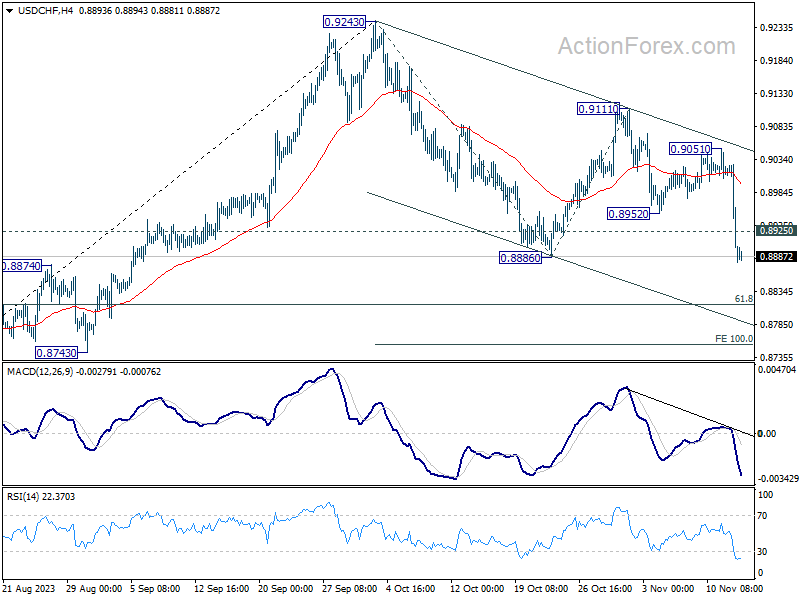

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8837; (P) 0.8933; (R1) 0.8988; More....

Intraday bias in USD/CHF remains on the downside for the moment. Decisive break of 0.8886 support will resume whole decline from 0.9243, and target 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754. On the upside, above 0.8925 minor resistance will turn intraday bias neutral first. But recovery should be limited well below 0.9051 resistance to bring another fall.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.