Sample Category Title

Australian Jobs Report Eyed After Upbeat Wage Data

- Australia to create more jobs, but no serious improvement expected

- Quarterly wage growth the strongest in 14 years

- Another rate hike could remain on the table

RBA resumes data-dependent approach

In contrast to other major central banks, the Reserve Bank of Australia (RBA) hiked interest rates in November under its new chair Michelle Bullock after a four-month pause. But the announcement was well anticipated and a slight dovish tweak in guidance was enough to hammer the Australian dollar.

The central bank judged that another quarter percentage rate increase to 4.35%–the highest in twelve years–was necessary to achieve its 2.0% midpoint inflation target, as progress on inflation had been slower than previously anticipated, despite passing its peak. Nevertheless, the RBA refrained from providing any commitment to additional tightening, linking the future path of rates to a data-dependent approach as the Fed did.

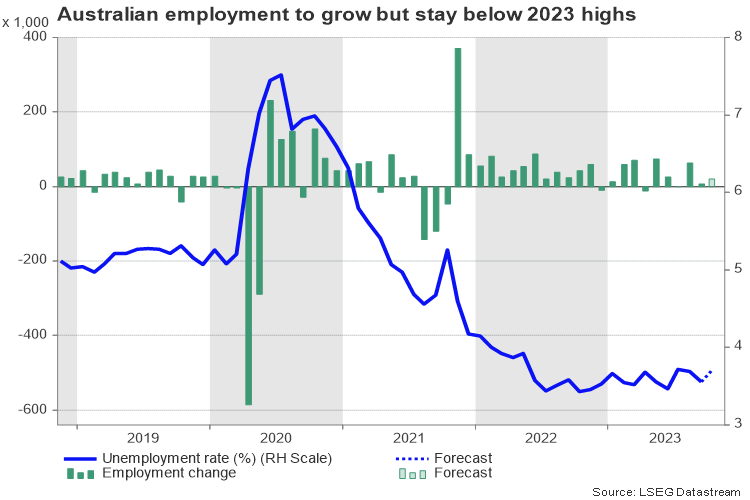

Employment growth to strengthen but nothing cheering expected

Thursday’s employment report for October will be the first piece of data information after the RBA’s latest policy meeting and given the central bank’s dual mandate of price stability and full employment, aussie traders might be sensitive to the headlines.

That said, the results may not excite traders. Analysts foresee a mixed report, with jobs growth accelerating by 20k in October from 6k previously and the unemployment rate inching up to 3.7% from 3.6%. That could still be among the weakest surveys so far in 2023.

Recall that job creation was three times larger in Australia during the previous months, while the unemployment rate was ranging between 3.5%-3.7% throughout the year. Hence, the data must surprise significantly to fuel strong volatility in the aussie.

Rate expectations

Perhaps, the monthly CPI indicator due on November 29th could be a bigger market mover following the continuous increase in October to 5.6% y/y. Futures markets are currently pointing to steady interest rates in December, but they reflect a potential for another rate increase to 4.6% at some point during February-September 2024 as the central bank does not expect inflation to return to 2.0% before 2025.

On the other hand, the RBA believes that the unemployment rate could stretch up to 4.2% in 2024–the highest since early 2022. Taking into account the recent record growth in population and the supply restraints in the housing sector, household spending could keep supporting inflation.

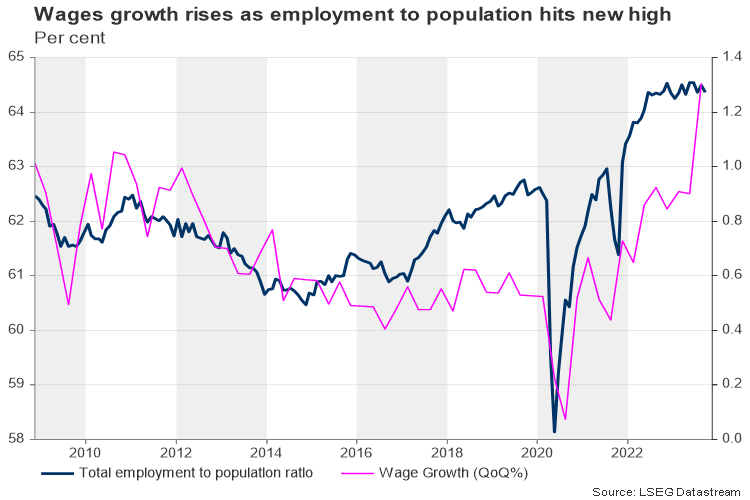

Interestingly, quarterly wage growth hit a fourteen-year high of 1.3% in Q3, suggesting that employees can still bargain for higher payments despite the surge in population. The problem here is that if the positive trend in wages continues, the RBA might have some difficulty in achieving its inflation target.

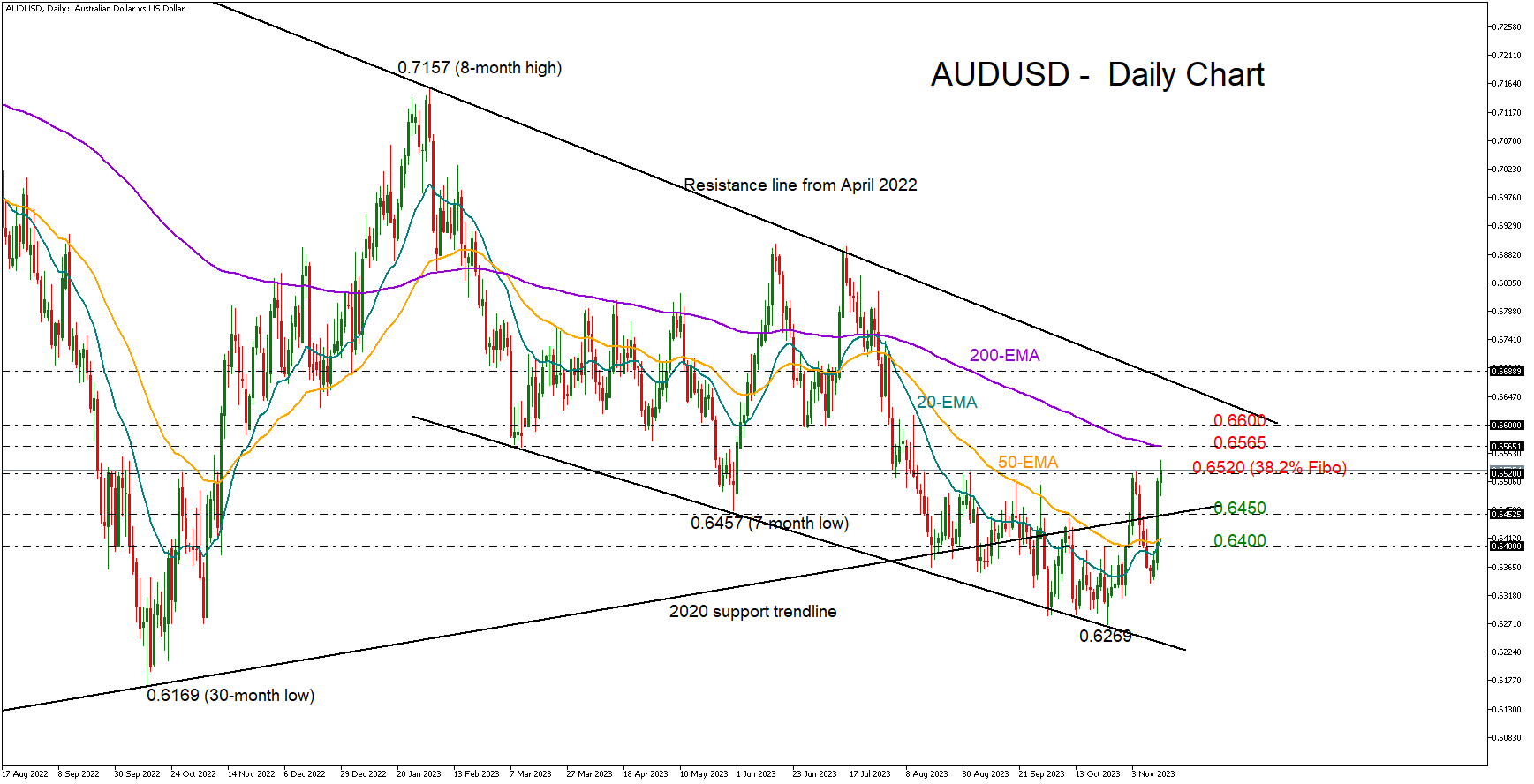

AUD/USD

Turning to FX markets, AUDUSD resumed its positive momentum after the upbeat wage data earlier today, stretching Tuesday’s rocket rally above the key nearby resistance of 0.6520 and to a high of 0.6540. A few hours later, a soft positive surprise in US retail sales pressed the pair back below that ceiling.

Investors will look at whether the employment report can help the pair reach its falling 200-day exponential moving average (EMA) higher at 0.6565 on Thursday, and perhaps challenge the 0.6600 psychological mark too.

A disappointing report could alternatively squeeze the pair towards the 0.6450 constraining zone, while a more aggressive decline could take a breather around the 20- and 50-day EMAs at 0.6400.

Strong Consumer Demand Did Not Prevent Inflation from Softening

A new batch of statistics from the US once again reminds us of the Goldilocks story, when one can have fun and not pay the price for it.

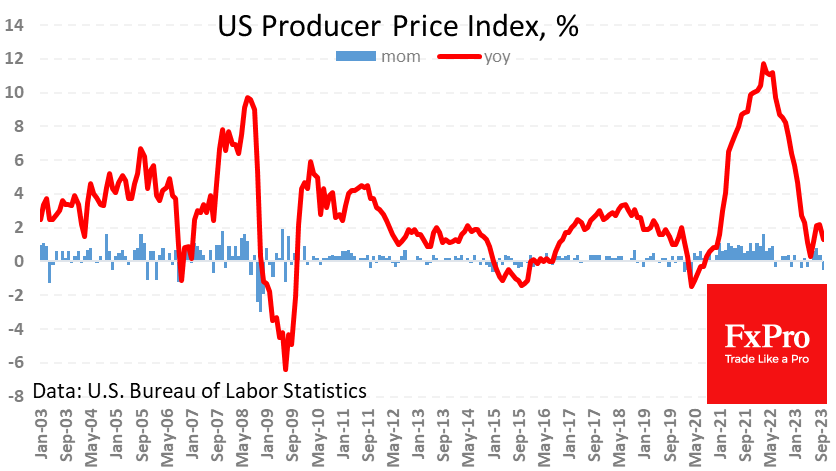

Producer prices fell 0.5%, against expectations for a 0.1% rise. And that’s a weaker report than expected after the release of consumer prices the day before. The annual inflation rate fell from 2.2% to 1.3%, against expectations of 1.9%. The core index, which excludes food and energy, was virtually unchanged for the month, and the annual growth rate fell to 2.4% from 2.7% expected. Had the market not overreacted the day before, such a report could have encouraged fresh dollar sellers and buyers of risk assets.

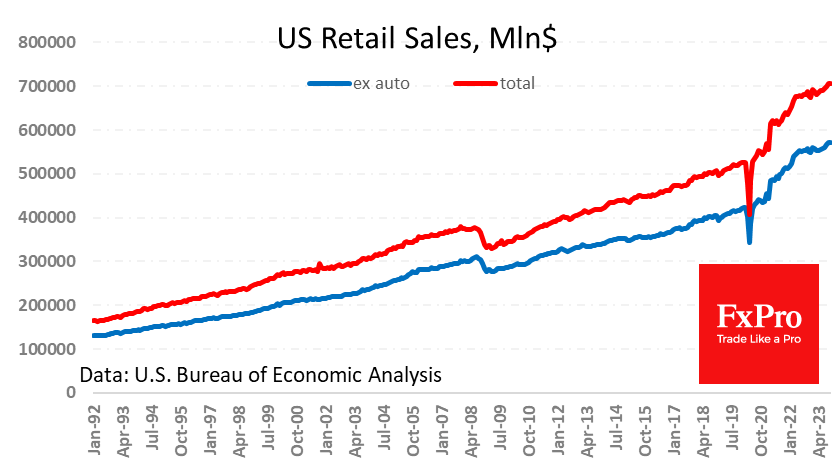

Another report showed that retail sales fell by 0.1%. This is a strong result, as a correction in spending was expected after a 0.9% rise the month before. Sales were virtually flat from September last year to March this year, but there was a strong rebound in sales last summer. Interestingly, this coincided with a pause in policy tightening by the Fed. This acceleration in spending is probably a concern for the regulator, so it is in no hurry to take the option of further policy tightening off the table.

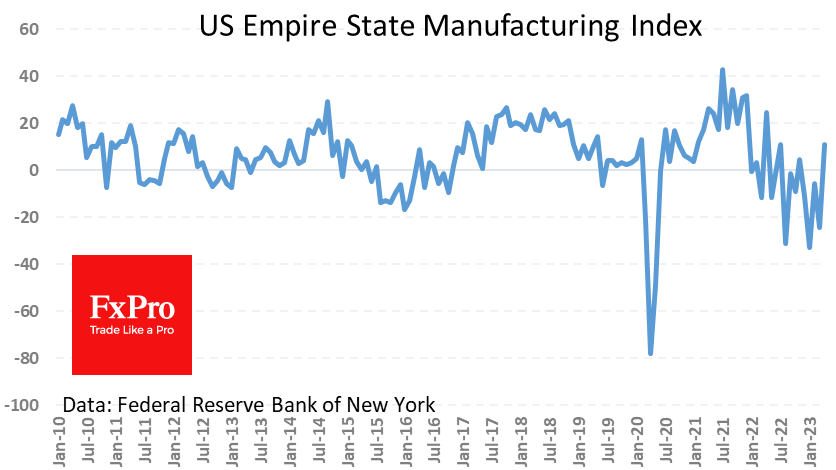

The Empire Manufacturing Index jumped from -4.6 to +9.1 – much better than the expected -3.3 – and the highest since April.

Theoretically, this should allow retailers to join the battle for profit (not market share) by passing costs through to prices. In practice, however, producer prices fell sharply, giving retailers more room to manoeuvre.

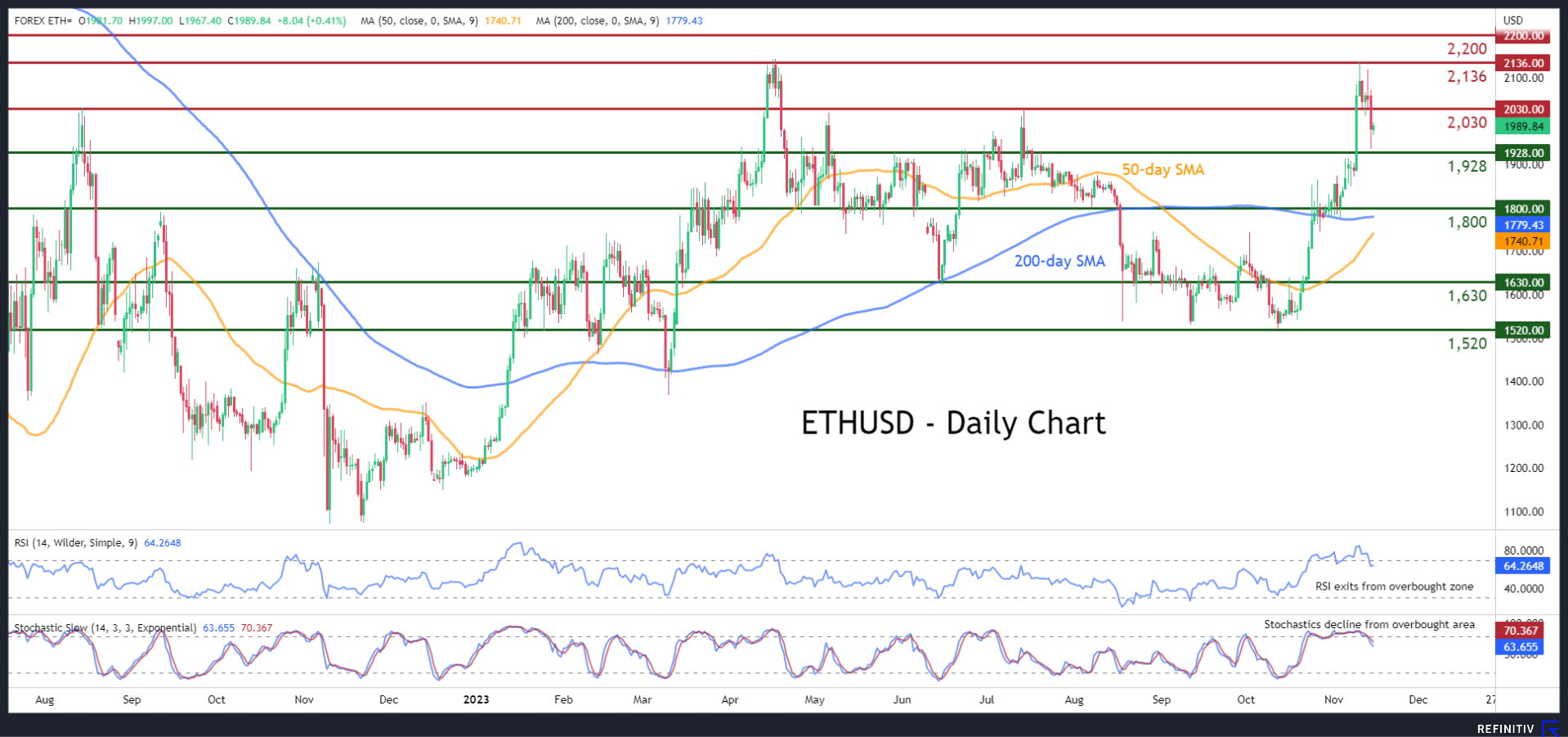

ETHUSD Falls Back Below 2,000

- Ethereum pulls back from recent multi-month high

- Impending golden cross could revive the rally

- Momentum indicators ease from overbought conditions

ETHUSD (Ethereum) experienced a strong correction after peaking at 2,136, its highest level since April 2023. However, the 50-day simple moving average (SMA) is closing the gap with the 200-day SMA, where a potential golden cross could induce upside pressures.

Should the positive momentum strengthen, the bulls might attack the July resistance of 2,030, which also held strong in August 2022. A violation of that zone could pave the way for the recent high of 2,136 just shy of the 2023 peak of 2,142. Slicing through the latter, the price may then challenge the 2,200 psychological mark.

On the flipside, if the recent slide resumes, immediate support could be found at the May-June resistance of 1,928. Further declines could then come to a halt at the May support of 1,800. Even lower, the June bottom of 1,630 might provide downside protection.

In brief, ETHUSD experienced a strong pullback as the second largest cryptocurrency had reached extreme overbought conditions. However, the completion of a golden cross could help the bulls propel the price back above the 2,000 mark.

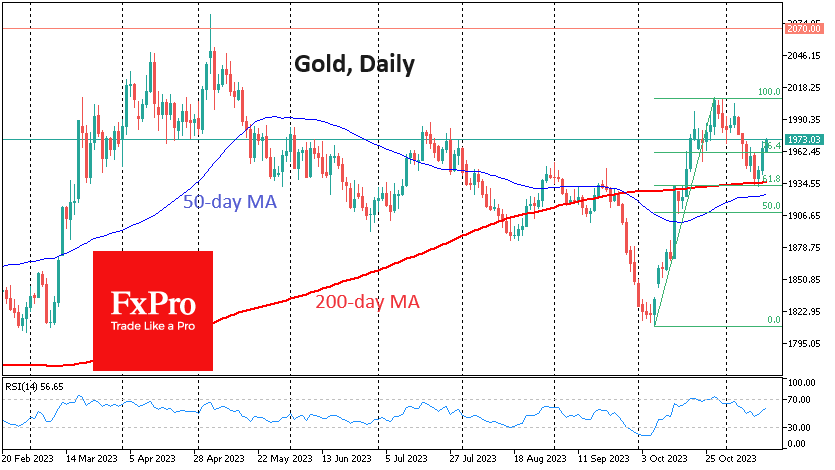

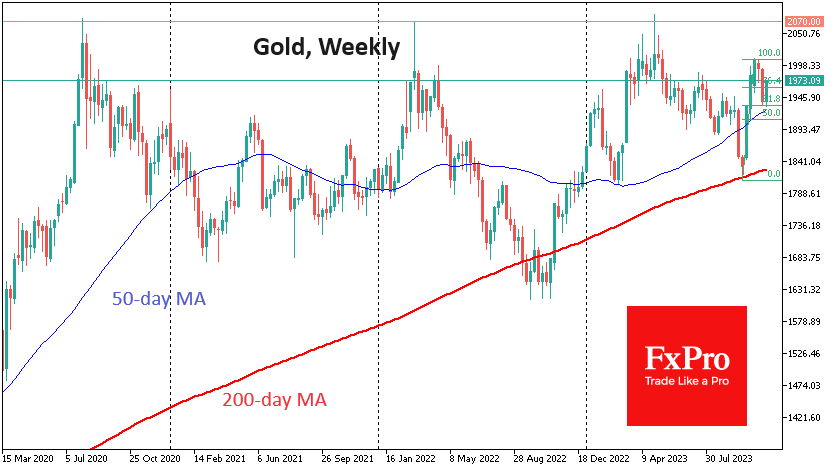

Gold Ends Retreat and Heads Higher

Gold has made a decisive reversal to the upside this week. We are likely to see the start of a new bullish momentum with the potential to renew all-time highs above $2100.

Gold rallied by $200 in October and peaked at $2010, driven by three main factors. Early in the month, gold was an attractive buy on oversold conditions and a touch of the critical 200-week moving average provided a technical reason for a rebound.

But fundamental news continued to drive the buying. The first was the US labour market data, strong employment growth with a moderate slowdown in wage growth. Then, over the weekend, the conflict between Israel and Hamas added fuel to the fire.

By the end of October, gold was overheated and went into a correction, which deepened in November despite the return of risk appetite in US markets after the Fed meeting. As a result, the value of the troy ounce retreated to the 200-day moving average and the 61.8% Fibonacci level of the initial spike.

Gold’s rally from these levels since the start of the week should be seen as a confident return of buyers from technically significant levels and the end of the corrective pullback. According to the Fibonacci pattern, gold’s next upside target is $2130, or 161.8% of last month’s upside amplitude.

However, this pattern will only be fully realised on a confident break of the previous local highs at $2010. A strong break above will confirm that gold is ready to settle above the crucial milestone this time. Over the past three years, gold has rallied strongly on several occasions, but these have always been upside impulses, and we soon see a reversal to the downside. The coming days will tell us if this is the case this time.

Sunset Market Commentary

Markets

US October retail sales served as the main dish for today. The countdown was rewarded with a small beat across all gauges. The headline series dropped less than expected, -0.1% m/m vs -0.3%. Two core measures printed a slight uptick of 0.1%. A private consumption proxy, the control group (excluding food services, auto dealers, building materials and gas stations), added 0.2%. The underlying components showed a mixed picture. The drag from furniture (-2% m/m), motor vehicles & parts (-1%) and sporting goods (-0.8%) was offset by rising sales in electronics (0.6%), health & personal care (+1.1%) and food & beverages (+0.6%). The numbers are actually not at all bad if you take into account the strong September month. Its readings which were revised even higher, resulting in advances from 0.7% to 0.9%. It means the fourth quarter started of on decent footing. We’re also keen to find out to what this consumer resilience will lead to in the current holiday season (starting with Thanksgiving’s Day and Black Friday next week). US yields briefly dropped after the release but we suspect this was a kneejerk move on PPI data released simultaneously. All variants came in on the weaker side of expectations. The New York’s manufacturing index unexpectedly re-entered positive territory, jumping from -4.6 to 9.1. Details, however, offered less reasons to be optimistic though. Shipments rose sharply but new orders and number of employees either became more or turned negative while hours worked were cut. Either way, yields try to recover some ground after yesterday’s outsized market reaction to a <0.1% CPI miss. They add 5.8-7.6 bps across the curve, the belly underperforming. German yields eke out an 1.9-3.4 bps advance in technically insignificant trading. The European Commission lowered its autumn growth forecast for the bloc, citing losing momentum on the high cost of living, weak external demand and monetary tightening. It now expects 0.6% growth this year with the running quarter seen printing at 0.2%. It therefore should avoid a recession (as well as Germany). Growth is expected to pick up to 1.2% in 2024 and 1.6% in the next year. After an average of 5.6% this year, inflation in the euro area should ease to 3.2% (from 2.9% in the previous estimate) and 2.2% in the two years thereafter. Belgium is one of the four EU member states where HICP is expected to drop below 2% in 2025. Turning to currency markets, the dollar barely recovers from yesterday’s uppercut. It does strengthen against the three major currencies. EUR/USD (1.0852) eases back below the 50% retracement of the 2023H2 decline. USD/JPY bounces back from the 150 barrier to 150.93 and cable (GBP/USD, 1.2443) called off the attack on the 1.25 resistance level. The latter also features sterling weakness after inflation in the UK followed the US in dropping a little more than expected. It cemented money market expectations for the Bank of England having reached the end of the tightening cycle while preparing for rate cuts from 2024H2 on.

News & Views

Zsolt Kuti, Hungarian central bank’s director in charge of monetary policy and therefore very close advisor to the rate-setting committee argued against cutting policy rates too hastily. “For a return to sustainable growth, the country needs to ensure price stability by cautiously chipping away at interest rates, instead of rushed ax blows that would lead to sustained high inflation and to falling behind,” he wrote. Hungarian inflation (9.9% Y/Y in October) remains unacceptably high with the central bank’s efforts only at “half-time”. Kuti’s comments come after markets stepped up easing bets following a bigger-than-expected 75 bps rate cut last month. They also conflict with recent comments by Hungarian PM Orban’s economic policy chief Nagy who criticized the central bank’s fetish with positive real rates which are ‘the greatest impediment to growth”. The Hungarian forint lost some ground today with EUR/HUF bouncing back from a 4-month low around 375 to 377.50. HUF swap rates fall 6 to 9 bps across the curve.

Swedish Kantar Prospera published results of its monthly survey mapping money market player’s expectations of Swedish inflation, GDP, policy rate, 5-yr bond and FX rates. 1-year ahead CPIF annual inflation forecasts picked up from 2.7% to 2.8%, while 3-yr and 5-yr prognosis stayed unchanged both at 2.1%. They see the policy rate peaking higher (4.2% from 4.1% in 3 months’ time) and remaining sticky for longer (2.8% from 2.6% in 2 years’ time. The Swedish Riksbank meeting next week with money markets attaching a 25% probability for a final 25 bps rate hike to 4.25%. The Swedish koruna extends yesterday’s bullish run with EUR/SEK approaching the 11.40 technical neckline of a big triple top formation.

U.S. Retail Sales Retreat in October for the First Time in Seven Months

Retail sales fell by -0.1% month-on-month (m/m) in October, down from September's reading of 0.9% growth. This was slightly better than consensus forecast calling for a larger decline of -0.3%.

Trade in the auto sector pulled back on the month falling by -1.0% m/m, reflecting a decline in sales at motor vehicle dealers (down -1.1%) which was partially offset by growth at automotive parts and accessory stores (up +0.4%).

Sales at gasoline stations fell -0.3% m/m relative to the 1.0% increase recorded in September, largely reflecting the pullback in gas prices. The building materials and equipment category declined by -0.3% m/m for a second consecutive month.

Sales in the retail sales "control group", which excludes the above volatile components (autos, building materials and gas) and is used to estimate personal consumption expenditures (PCE) came in at 0.2% m/m. September's figure was also revised upwards to show an increase of 0.7% instead of the previously reported 0.6%.

- Among the control group, the largest contribution came from sales at health and personal care store (+1.1% m/m), food and beverage stores (+0.6%) and non-store retailers (+0.2% m/m).

- The main categories posting declines were miscellaneous stores retailers (-1.7% m/m), sporting goods and hobby store (-0.8% m/m), and department stores (-0.2% m/m).

Food services & drinking places – the only services category in the retail sales report – was up 0.3% m/m.

Key Implications

And there you have it. The pullback in retail spending in October did not come as a surprise as market participants have been forecasting a retrenchment in sales for some time. While part of the decline in the headline number reflected lower prices for gasoline, sales in the key control group also lost momentum, though still maintaining its seven month growth streak. Today's numbers kick off the fourth quarter on a softer note, with real consumption expenditure currently tracking around 1.8% for Q4.

The slowdown in spending reported today, combined with yesterday's lower inflation numbers is another step in the direction the Fed wants to go. As higher interest rates continue to work through the economy, spending is likely to remain much more tepid, relative to the boil witnessed in Q3.

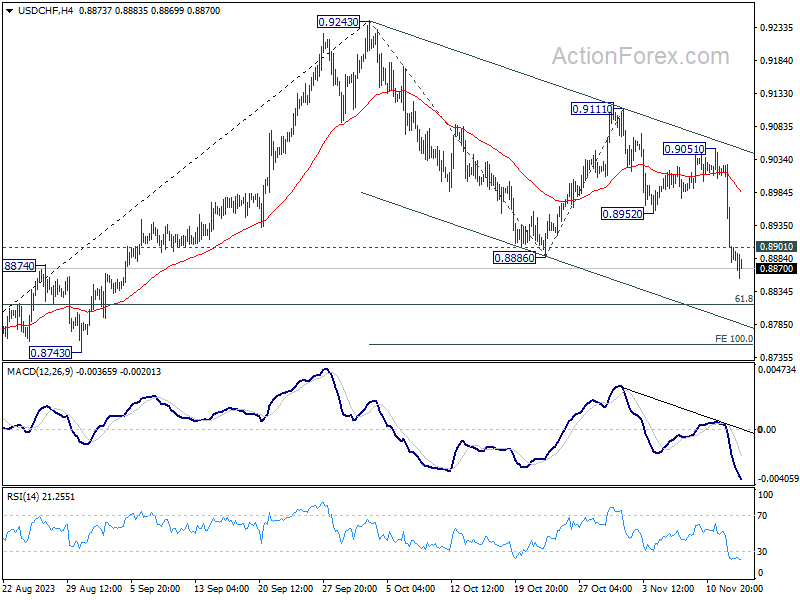

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8837; (P) 0.8933; (R1) 0.8988; More....

USD/CHF's decline continues today and intraday bias stays on the downside. Fall from 0.9243 should target 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754. On the upside, above 0.8901 minor resistance will turn intraday bias neutral and bring consolidations first. But recovery should be limited well below 0.9051 resistance to bring another fall.

In the bigger picture, price actions from 0.8551 are currently seen as a correction to the decline from 1.0146. Fall from 0.9243 is seen as the second leg for now. Deeper fall would be seen to 61.8% retracement of 0.8551 to 0.9243 at 0.8815. Sustained break there will bring retest of 0.8551 low. For now, this will remain the favored case as long as 0.9111 resistance holds.

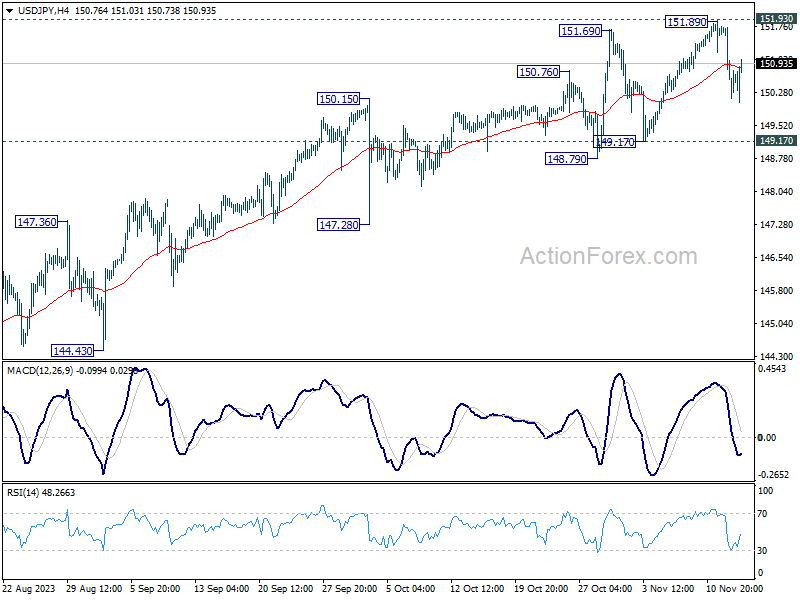

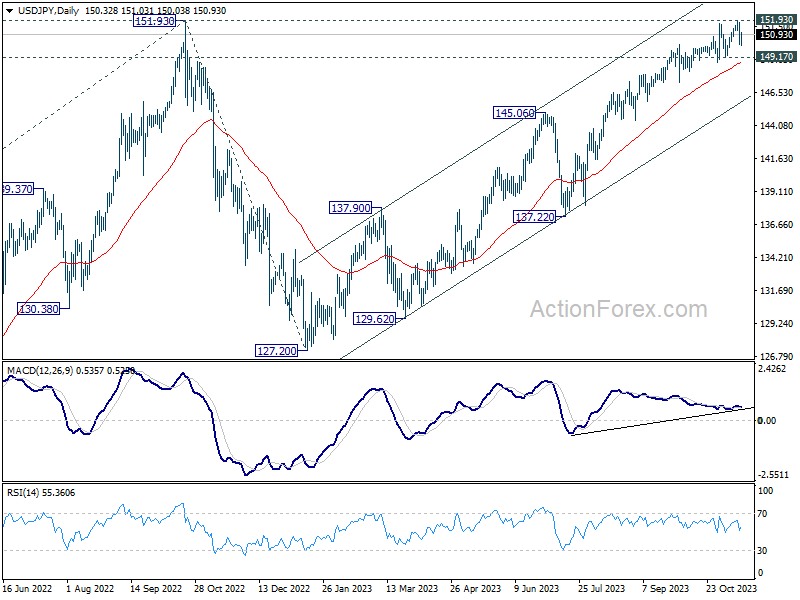

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.77; (P) 150.78; (R1) 151.39; More...

USD/JPY recovers today as range trading continues. Intraday bias remains neutral for the moment. Further rally is in favor as long as 149.17 support holds. On the upside, decisive break of 151.93 resistance will confirm resumption of long term up trend. Next target will be 157.69 projection level. However, firm break of 149.17 will be a sign of bearish reversal and bring deeper fall to 147.28 support first.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 (2021 low) to 151.93 from 127.20 at 157.69.

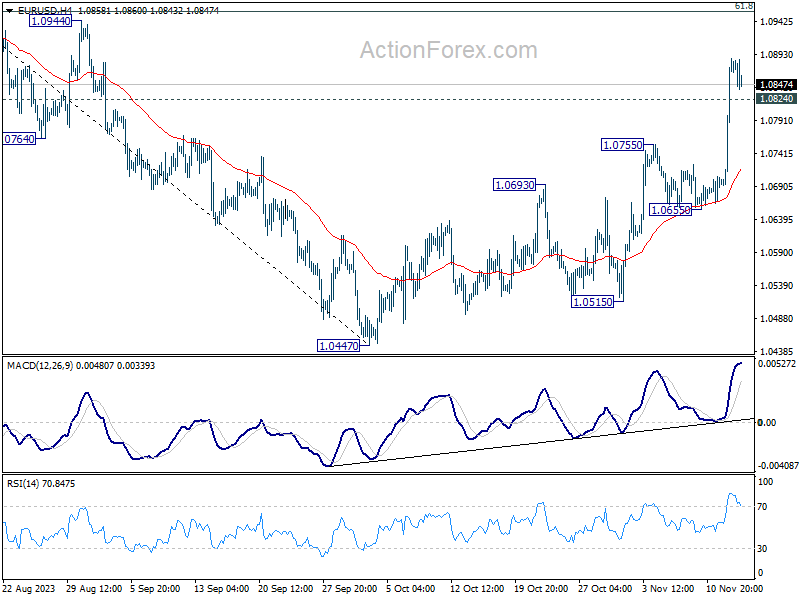

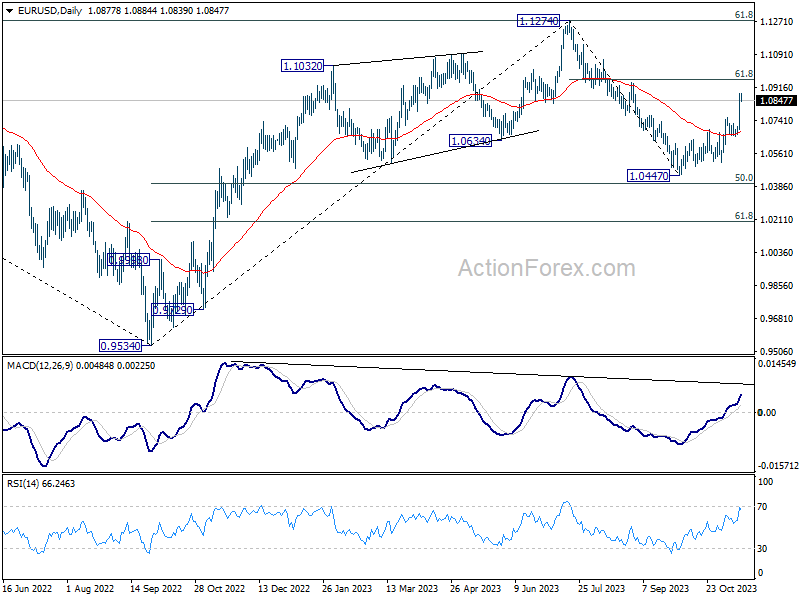

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0752; (P) 1.0820; (R1) 1.0947; More...

With 1.0824 minor support intact, intraday bias in EUR/USD remains on the upside despite current retreat. Rise from 1.0447 should extend to 61.8% retracement of 1.1274 to 1.0447 at 1.0958 next. On the downside, below 1.0824 minor support will turn intraday bias neutral and bring consolidations first. But downside should be contained well above 1.0655 support to bring another rally.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. However, break of 1.0447 will resume the fall to 61.8% retracement of 0.9543 to 1.1274 at 1.0199.

Sterling Falters Post-UK Inflation Report, Dollar Sees Momentary Respite

Sterling emerged as the standout underperformer today, reacting notably to the latest CPI data from the UK. This data indicated a more rapid deceleration in both headline and core inflation rates than many had predicted. Such a shift in inflation dynamics is feeding into growing belief among market participants that BoE has reached the pinnacle of its interest rate hiking cycle.

Nevertheless, the sentiment towards the Pound is distinctly different from the US scenario, where Dollar witnessed a dramatic plunge following a similar inflation trend. In the case of Sterling, however, market response has been relatively muted, suggesting a more cautious recalibration of expectations rather than a drastic reassessment.

Euro is not far behind in terms of weakness, partly pressured by the resurgence in the Swiss Franc. Japanese Yen is also experiencing downward pressure, primarily due to Japan's GDP contraction in the third quarter, which was much steeper than many analysts had anticipated.

In contrast, commodity-linked currencies such as Australian and New Zealand Dollars are maintaining their upward momentum, buoyed by strong risk-on sentiment that is evident across both Asian and European markets. Dollar, meanwhile, is displaying a mixed performance, having a breather after its steep decline earlier in the week, and shows little reaction to retail sales and PPI data.

Analyzing the performance over the week, Dollar continues to languish as the weakest among its peers, trailed by Japanese Yen, Canadian Dollar, and Swiss Franc. Australian Dollar stands out as the strongest, followed by New Zealand Dollar, Sterling, and the Euro.

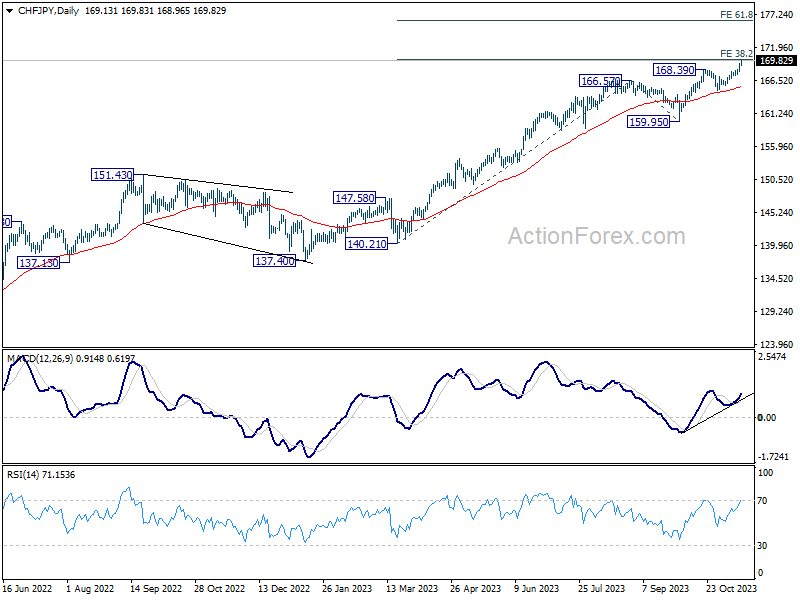

Technically, CHF/JPY's uptrend resumed this week by breaking through 168.39 resistance, and hits as high as 169.37 so far. Immediate focus is now on 38.2% projection of 140.21 to 166.57 from 159.95 at 170.01. Decisive break there could prompt further upside acceleration to 61.8% projection at 176.24.

In Europe, at the time of writing, FTSE is up 1.04%. DAX is up 0.68%. CAC is up 0.44%. Germany 10-year yield is up 0.0189 at 2.625. In Asia, Nikkei surged 2.52%. Hong Kong HSI rose 3.92%. China Shanghai SSE rose 0.55%. Singapore Strait Times rose 0.88%. Japan 10-year JGB yield dropped -0.0495 to 0.797.

US retail sales down -0.1% mom in Oct, ex-auto sales up 0.1% mom

US retail sales fell -0.1% mom to USD 705.0B in October, better than expectation of -0.3% mom. Ex-auto sales rose 0.1% mom to USD 570.9B, above expectation of -0.2% mom decline. Ex-gasoline sales fell -0.1% mom to 648.4B. Ex-auto and gasoline sales rose 0.1% mom to USD 514.3B.

Total sales for August through October period were up 3.1% from the same period a year ago.

US PPI down -0.5% mom in Oct, biggest fall since Apr 2020

US PPI for final demand fell -0.5% mom in October, below expectation of 0.1% mom rise. That's also the largest monthly decline since April 2020. PPI goods fell -1.4% mom while PPI services was unchanged. For the 12 months period, PPI slowed from 2.2% yoy to 1.3% yoy, below expectation of 1.9% yoy.

PPI less foods, energy and trade services rose 0.1% mom, the fifth consecutive rise. For the 12 months period, PPI less goods, energy and trade services rose 2.9% yoy.

European Commission trims Eurozone growth forecasts for 2023 and 2024

In European Commission's Autumn Economic Forecasts, 2023 GDP growth forecast has been lowered to 0.6%, a reduction from the earlier summer forecast of 0.8%. Outlook for 2024 is also tempered, with GDP growth projections scaled back to 1.2%, compared to previous 1.3%. However, there is an anticipation of pickup in growth to 1.6% in 2025.

In terms of inflation, 2023 forecast remains unchanged at 5.6%. However, there was an upward adjustment for 2024, with inflation rate now predicted to be 3.2%, higher than summer's forecast of 2.9%. The Commission expects inflation to decelerate further in 2025, slowing to 2.2%.

Valdis Dombrovskis, Executive Vice-President of European Commission, expressed a cautiously optimistic view, stating, "Following very weak growth this year, we can expect growth to rebound modestly in 2024, helped by strong labour markets and continued easing of inflation." He also highlighted the uncertain geopolitical context, particularly noting the recent conflict in the Middle East and its potential implications.

Paolo Gentiloni, Commissioner for Economy, echoed these sentiments. He pointed out that "Strong price pressures and the monetary tightening needed to contain them, as well as weak global demand, have taken their toll on households and businesses."

Looking ahead, Gentiloni expects "a modest uptick in growth as inflation eases further and the labour market remains resilient." He also acknowledged the limited immediate economic impact of the Middle East conflict, while cautioning about the heightened geopolitical tensions and the increased uncertainty and risks they pose for the future economic landscape.

Eurozone industrial production down -1.1% in Sep, EU down -0.9% mom

Eurozone industrial production fell -1.1% mom in September, worse than expectation of -0.9% mom. Production of durable consumer goods and non-durable consumer goods fell both by -2.1%, energy by -1.3% and intermediate goods by -0.3%, while production of capital goods grew by 0.3%.

EU industrial production fell -0.9% mom. Among Member States for which data are available, the largest monthly decreases were registered in Belgium (-3.2%), Portugal (-3.0%), Estonia and Ireland (both -2.9%). The highest increases were observed in Croatia (+4.3%), Slovenia (+4.1%) and Hungary (+1.3%).

Eurozone goods exports falls -9.3% yoy in Sep, imports down -23.9% yoy

Eurozone exports of goods fell -9.3% yoy to EUR 235.8B in September. Imports fell -23.9% yoy. As a result, a EUR 10.0B trade surplus was recorded. Intra-Eurozone trade fell -15.5% yoy to EUR 217.3B.

In seasonally adjusted term, Eurozone goods exports fell -0.5% mom to EUR 234.0B. Imports rose 0.3% mom to 224.8B. Trade surplus narrowed from August's EUR 11.1B to EUR 9.2B, smaller than expectation of EUR 12.3B. Intra-Eurozone trade fell from August's 215.8B to EUR 213.9B.

UK CPI eases significantly to 4.7% in Oct, another step to BoE's target

UK CPI showed a marked slowdown in October, dipping below market expectations. The annual CPI rate decelerated from 6.7% yoy to 4.6% yoy , falling short of the anticipated 4.7% yoy. This decline reflects a broader trend of easing inflationary pressures, as evidenced by a flat monthly CPI rate of 0.0% mom, which was below the forecasted 0.2% mom.

Delving deeper, core CPI, which excludes volatile items such as energy, food, alcohol, and tobacco, mirrored this downtrend. It slowed from an annual rate of 6.1% yoy to 5.7% yoy, again undershooting the expected 5.8% yoy.

A notable aspect of the report was the significant drop in CPI goods annual rate, which plummeted from 6.2% yoy to 2.9% yoy. Meanwhile, services sector also saw a decline, albeit less pronounced, with CPI services annual rate reducing from 6.9% yoy to 6.6% yoy.

The most substantial downward pressure on the annual rates came from housing and household services sector. Notably, CPI annual rate in this category recorded its lowest level since record-keeping began in January 1950. Additionally, food and non-alcoholic beverages sector contributed to the downward trend, marking its lowest annual rate since June 2022.

Japan's GDP down -0.5% qoq, -2.1% annualized in Q3

Japan's GDP contracted -0.5% qoq in Q3, starkly underperformed market expectations of -0.1% qoq decline. On annualized basis, the situation appears even more drastic, with the economy shrinking by -2.1%, far exceeding anticipated -0.6% contraction, and being the worst since Q3 2021.

A critical factor in this downturn was a -0.6% decrease in business investment, marking a continuous decline for two consecutive quarters. This reduction was primarily influenced by reduced spending on semiconductor production equipment, reflecting broader challenges in global tech sector.

Additionally, private consumption, a key driver of economic activity, saw a marginal fall of -0.04%. This marks the second successive quarter of decline, with slump in vehicle sales significantly impacting consumer spending.

China's industrial and retail growth surpass expectations, PBOC injects fresh funds

China's industrial output and retail sales for October exceeded market expectations. Industrial production rose 4.6% yoy, surpassing forecasted 4.5% yoy, marking an improvement from September's 4.5% yoy growth. Retail sales recorded a robust 7.6% yoy growth, significantly higher than anticipated 7.0% yoy and showing a considerable improvement from 5.5% yoy increase in September.

However, fixed asset investment experienced slower growth, rising only 2.9% ytd yoy, which was below the expected 3.1%. The real estate sector particularly faced challenges, with investment dropping by -9.3% ytd yoy, a deterioration compared to the previous period through September.

In a separate development, People's Bank of China C) maintained the interest rate on CNY 1.45T worth of one-year medium-term lending facility loans at 2.50%, consistent with previous operations. As CNY 850B worth of MLF loans were set to expire this month, this move resulted in a net injection of CNY 600B of fresh funds into the banking system.

The central bank stated that this loan operation aimed to keep the banking system's liquidity at a reasonably ample level, countering short-term factors such as tax payments and government bond issuances.

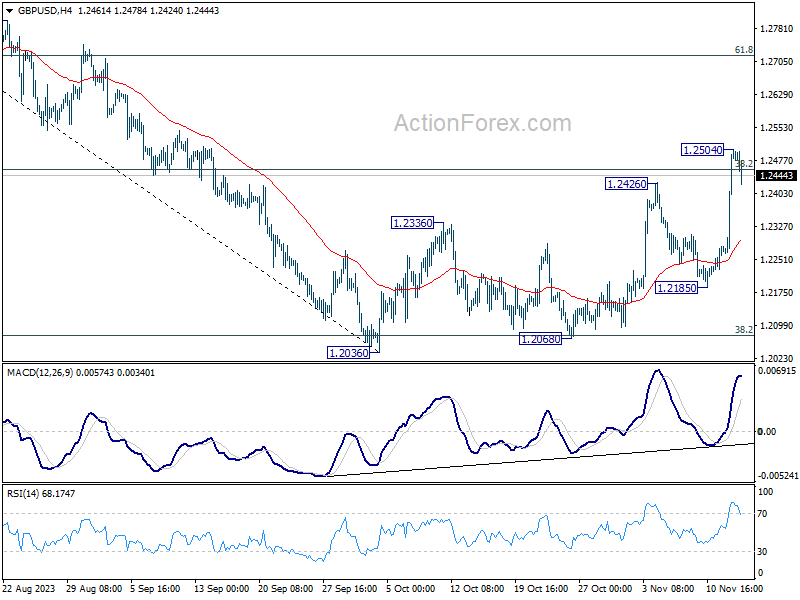

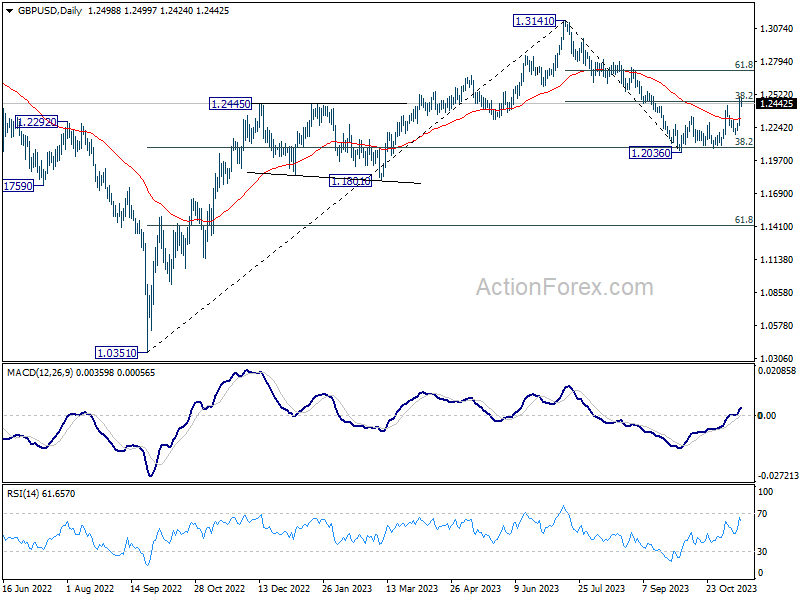

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2337; (P) 1.2421; (R1) 1.2583; More...

GBP/USD retreat slightly after edging higher to 1.2504 and intraday bias is turned neutral first. Some consolidations could be seen. But downside should be contained well above 1.2185 support to bring another rally. On the upside, break of 1.2504 will resume the whole rebound from 1.2036. Sustained trading above 38.2% retracement of 1.3141 to 1.2036 at 1.2458 will pave the way to 61.8% retracement at 1.2716.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 will argue that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Wage Price Index Q/Q Q3 | 1.30% | 1.30% | 0.80% | 0.90% |

| 23:50 | JPY | GDP Q/Q Q3 P | -0.50% | -0.10% | 1.20% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 P | 5.10% | 4.80% | 3.50% | |

| 02:00 | CNY | Industrial Production Y/Y Oct | 4.60% | 4.50% | 4.50% | |

| 02:00 | CNY | Retail Sales Y/Y Oct | 7.60% | 7.00% | 5.50% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Oct | 2.90% | 3.10% | 3.10% | |

| 04:30 | JPY | Industrial Production M/M Sep F | 0.50% | 0.20% | 0.20% | |

| 07:00 | GBP | CPI M/M Oct | 0.00% | 0.20% | 0.50% | |

| 07:00 | GBP | CPI Y/Y Oct | 4.60% | 4.70% | 6.70% | |

| 07:00 | GBP | Core CPI Y/Y Oct | 5.70% | 5.80% | 6.10% | |

| 07:00 | GBP | RPI M/M Oct | -0.20% | 0.50% | ||

| 07:00 | GBP | RPI Y/Y Oct | 6.10% | 6.40% | 8.90% | |

| 07:00 | GBP | PPI Input M/M Oct | 0.40% | 0.10% | 0.40% | 0.60% |

| 07:00 | GBP | PPI Input Y/Y Oct | -2.60% | -2.60% | -2.10% | |

| 07:00 | GBP | PPI Output M/M Oct | 0.10% | 0.10% | 0.40% | 0.60% |

| 07:00 | GBP | PPI Output Y/Y Oct | -0.60% | -0.10% | 0.20% | |

| 07:00 | GBP | PPI Core Output M/M Oct | 0.10% | 0.00% | ||

| 07:00 | GBP | PPI Core Output Y/Y Oct | 0.20% | 0.70% | 0.80% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | 9.2B | 12.3B | 11.9B | 11.1B |

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | -1.10% | -0.90% | 0.60% | |

| 13:30 | CAD | Manufacturing Sales M/M Sep | 0.40% | 0.80% | 0.70% | |

| 13:30 | CAD | Wholesale Sales M/M Sep | 0.40% | 1.40% | 2.30% | |

| 13:30 | USD | Empire State Manufacturing Index Nov | 9.1 | -2.6 | -4.6 | |

| 13:30 | USD | Retail Sales M/M Oct | -0.10% | -0.30% | 0.70% | 0.90% |

| 13:30 | USD | Retail Sales ex Autos M/M Oct | 0.10% | -0.20% | 0.60% | 0.80% |

| 13:30 | USD | PPI M/M Oct | -0.50% | 0.10% | 0.50% | 0.40% |

| 13:30 | USD | PPI Y/Y Oct | 1.30% | 1.90% | 2.20% | |

| 13:30 | USD | PPI Core M/M Oct | 0.00% | 0.20% | 0.30% | 0.20% |

| 13:30 | USD | PPI Core Y/Y Oct | 2.40% | 2.70% | 2.70% | |

| 15:00 | USD | Business Inventories Sep | 0.30% | 0.40% | ||

| 15:30 | USD | Crude Oil Inventories |