Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2337; (P) 1.2421; (R1) 1.2583; More...

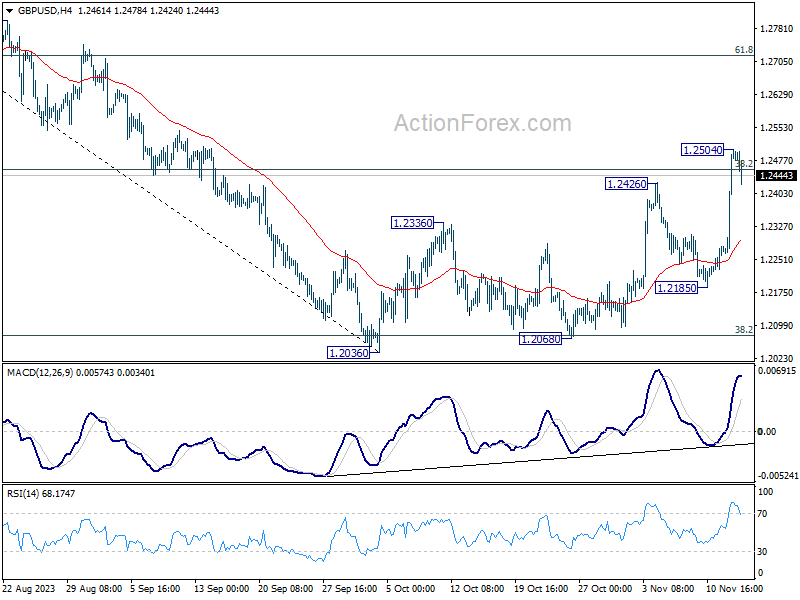

GBP/USD retreat slightly after edging higher to 1.2504 and intraday bias is turned neutral first. Some consolidations could be seen. But downside should be contained well above 1.2185 support to bring another rally. On the upside, break of 1.2504 will resume the whole rebound from 1.2036. Sustained trading above 38.2% retracement of 1.3141 to 1.2036 at 1.2458 will pave the way to 61.8% retracement at 1.2716.

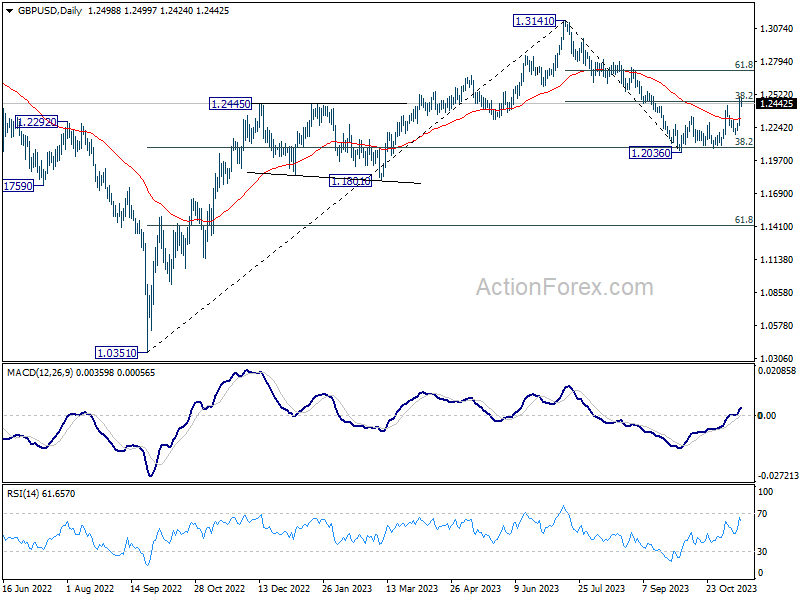

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 will argue that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

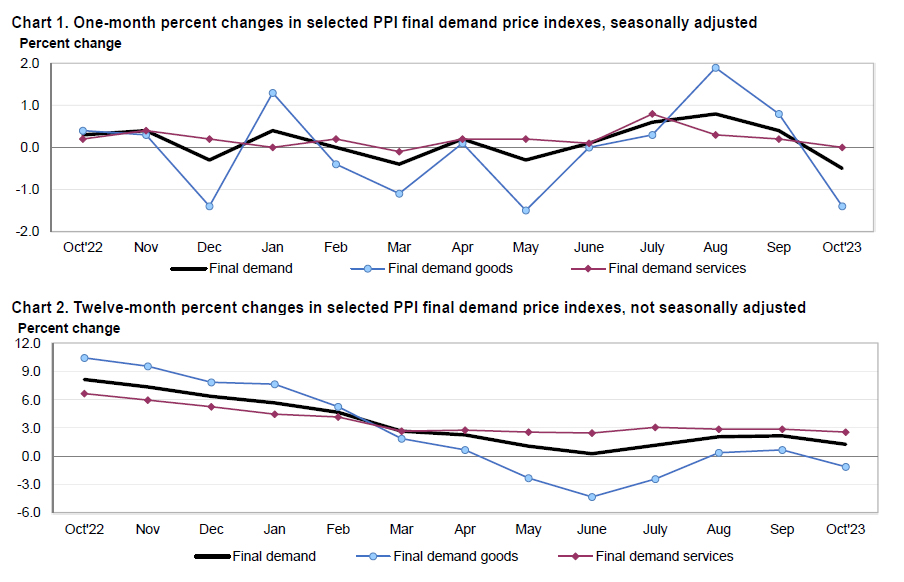

US PPI down -0.5% mom in Oct, biggest fall since Apr 2020

US PPI for final demand fell -0.5% mom in October, below expectation of 0.1% mom rise. That's also the largest monthly decline since April 2020. PPI goods fell -1.4% mom while PPI services was unchanged. For the 12 months period, PPI slowed from 2.2% yoy to 1.3% yoy, below expectation of 1.9% yoy.

PPI less foods, energy and trade services rose 0.1% mom, the fifth consecutive rise. For the 12 months period, PPI less goods, energy and trade services rose 2.9% yoy.

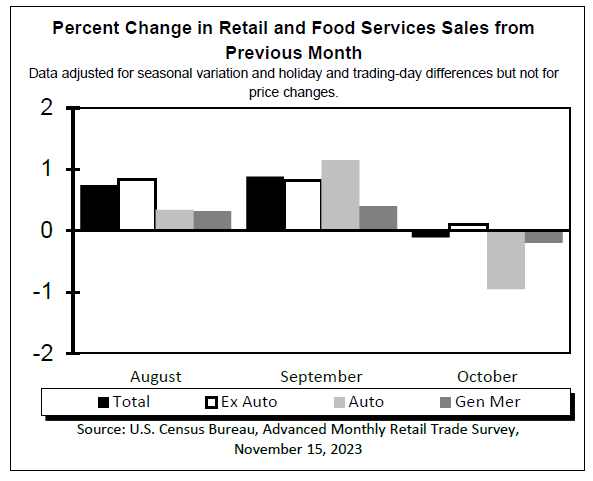

US retail sales down -0.1% mom in Oct, ex-auto sales up 0.1% mom

US retail sales fell -0.1% mom to USD 705.0B in October, better than expectation of -0.3% mom. Ex-auto sales rose 0.1% mom to USD 570.9B, above expectation of -0.2% mom decline. Ex-gasoline sales fell -0.1% mom to 648.4B. Ex-auto and gasoline sales rose 0.1% mom to USD 514.3B.

Total sales for August through October period were up 3.1% from the same period a year ago.

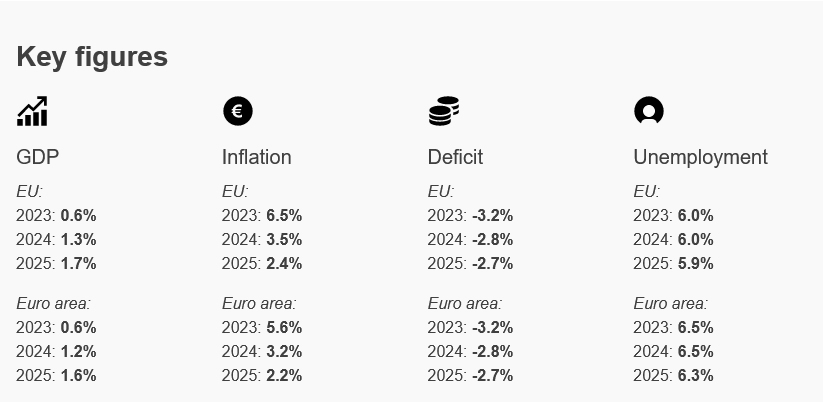

European Commission trims Eurozone growth forecasts for 2023 and 2024

In European Commission's Autumn Economic Forecasts, 2023 GDP growth forecast has been lowered to 0.6%, a reduction from the earlier summer forecast of 0.8%. Outlook for 2024 is also tempered, with GDP growth projections scaled back to 1.2%, compared to previous 1.3%. However, there is an anticipation of pickup in growth to 1.6% in 2025.

In terms of inflation, 2023 forecast remains unchanged at 5.6%. However, there was an upward adjustment for 2024, with inflation rate now predicted to be 3.2%, higher than summer's forecast of 2.9%. The Commission expects inflation to decelerate further in 2025, slowing to 2.2%.

Valdis Dombrovskis, Executive Vice-President of European Commission, expressed a cautiously optimistic view, stating, "Following very weak growth this year, we can expect growth to rebound modestly in 2024, helped by strong labour markets and continued easing of inflation." He also highlighted the uncertain geopolitical context, particularly noting the recent conflict in the Middle East and its potential implications.

Paolo Gentiloni, Commissioner for Economy, echoed these sentiments. He pointed out that "Strong price pressures and the monetary tightening needed to contain them, as well as weak global demand, have taken their toll on households and businesses."

Looking ahead, Gentiloni expects "a modest uptick in growth as inflation eases further and the labour market remains resilient." He also acknowledged the limited immediate economic impact of the Middle East conflict, while cautioning about the heightened geopolitical tensions and the increased uncertainty and risks they pose for the future economic landscape.

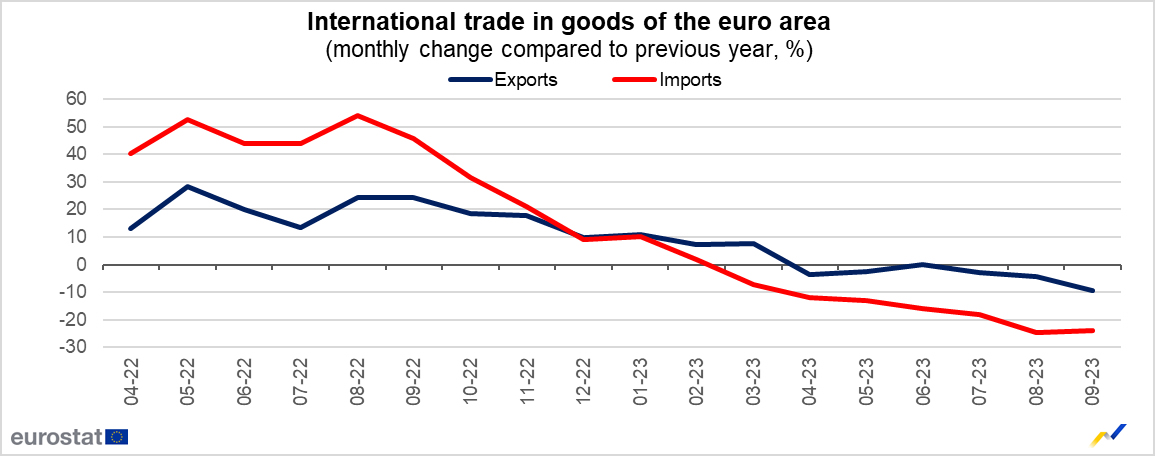

Eurozone goods exports falls -9.3% yoy in Sep, imports down -23.9% yoy

Eurozone exports of goods fell -9.3% yoy to EUR 235.8B in September. Imports fell -23.9% yoy. As a result, a EUR 10.0B trade surplus was recorded. Intra-Eurozone trade fell -15.5% yoy to EUR 217.3B.

In seasonally adjusted term, Eurozone goods exports fell -0.5% mom to EUR 234.0B. Imports rose 0.3% mom to 224.8B. Trade surplus narrowed from August's EUR 11.1B to EUR 9.2B, smaller than expectation of EUR 12.3B. Intra-Eurozone trade fell from August's 215.8B to EUR 213.9B.

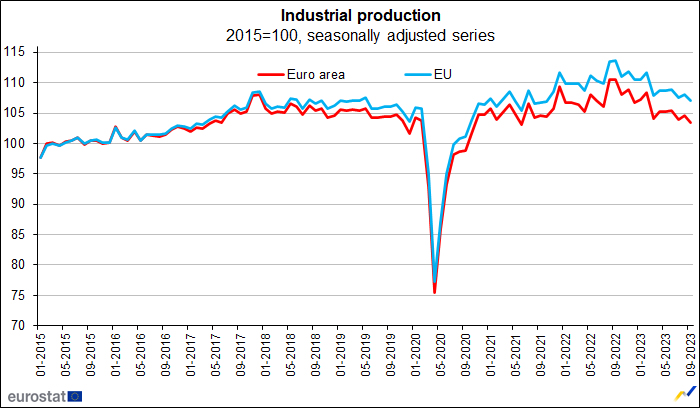

Eurozone industrial production down -1.1% in Sep, EU down -0.9% mom

Eurozone industrial production fell -1.1% mom in September, worse than expectation of -0.9% mom. Production of durable consumer goods and non-durable consumer goods fell both by -2.1%, energy by -1.3% and intermediate goods by -0.3%, while production of capital goods grew by 0.3%.

EU industrial production fell -0.9% mom. Among Member States for which data are available, the largest monthly decreases were registered in Belgium (-3.2%), Portugal (-3.0%), Estonia and Ireland (both -2.9%). The highest increases were observed in Croatia (+4.3%), Slovenia (+4.1%) and Hungary (+1.3%).

No More Rate Hikes Likely from BoE as Inflation Hits Two-Year Low

UK inflation fell sharply in October and faster than the Bank of England anticipated, further reducing the prospect of any more rate hikes in this tightening cycle.

It was already likely that the BoE was done raising rates but as that was based on the view that inflation would fall to 4.8% last month, that could have changed with a higher reading this morning. Instead, it fell even further to 4/6% so there's unlikely to be a big swing on the MPC in favour of hiking now, not unless the data performs much worse over the coming months.

It's not just the headline numbers that are encouraging though. Much like the other data we're seeing, the most recent monthly figures look extremely promising too, suggesting the pace of disinflation has accelerated recently in a manner consistent with inflation now running much lower than the annual comparisons suggest.

If we continue to see this over the coming months, especially if paired with similar trends in monthly wage growth, that first rate cut from the BoE could come earlier than many expect.

There will obviously be areas of stubbornness in the data, most notably services, but if monthly wage data continues to print at levels consistent with the 2% inflation goal and CPI data too, it's surely only a matter of time until services fall as well. All things considered, this week's data from the UK looks incredibly promising.

US retail sales, PPI, and a manufacturing survey in focus

There's still plenty more to come today, in a week filled with major economic releases from both sides of the pond. US retail sales, PPI inflation and the Empire State manufacturing index are due later and will offer some further insight into the resilience of household demand, price pressures and the manufacturing recession.

Oil prices easing again after running into a brick wall around October lows

Oil prices have bounced back over the last four trading sessions but appeared to run into a brick wall yesterday around $84 in Brent and $80 in WTI. That's around the October lows in WTI and perhaps a sign that traders have not become less bearish despite promising inflation data and improved prospects for an economic soft landing.

Considering the more than 10% decline we've now seen from the September peak, you have to wonder whether Saudi Arabia and Russia will feel compelled to extend their unilateral cuts beyond the end of the year in fear of what will happen if they don't. OPEC attempted to push back against pessimistic expectations recently but clearly to no avail. While they may not be too concerned about current price levels, the trend will be making them uncomfortable.

Gold moving closer to $2,000 back by better fundamentals

The US inflation data on Tuesday was a big positive for gold, which rallied as the dollar and US yields both fell. That came as markets fully priced out any further rate hikes from the Federal Reserve and the first rate cut by May. It's hard to argue considering the recent progress and suddenly gold is on an upward trajectory, not far from $2,000, and backed by better fundamentals.

AUD/USD Soars on US Inflation, Aussie Employment Next

- Australian wage growth hits record high

- US inflation slips to 3.2%

- Australian job growth expected to rise

The Australian dollar is unchanged on Wednesday, after massive gains a day earlier. In the European session, AUD/USD is trading at 0.6505.

Australian wages soar

Australian wage growth climbed 1.3% q/q in the third quarter, matching the consensus estimate and above an upwardly revised 0.9% gain in Q2. This was the highest gain since records started in 1997, but the spike was largely due to an increase in minimum wage and a pay rise for elderly care workers.

The unusual confluence of factors behind the strong wage growth print meant that it had little effect on market pricing of a rate hike. The markets have priced in a pause above 90% at the Reserve Bank of Australia’s next meeting on December 5th. The RBA raised rates earlier this month after four straight pauses but the hike was considered dovish by the markets and the Australian dollar took a tumble following the decision.

Australia releases employment data on Thursday, with the labour market continuing to show resilience. The economy is expected to have added 20,000 jobs in October, compared to 6,700 in September. The RBA will be keeping a close eye on consumer inflation expectations, which is expected to fall in October from 4.8% to 4.1%.

US inflation softer than expected

The US inflation report was only a bit lower than expected, but the US dollar was pummelled on Tuesday with sharp losses against the major currencies. The Australian dollar soared, gaining 2% against the greenback. Monthly, headline inflation was unchanged in October for the first time in 15 months, with lower gasoline prices helping to push inflation lower. On an annual basis, headline inflation fell from 3.7% to 3.2%, below the market consensus of 3.3%. Core inflation inched lower to 4.0%, down from the September reading of 4.1% which was also the market consensus.

AUD/USD Technical

- AUD/USD is putting pressure on resistance at 0.6526. Above, there is resistance at 0.6592

- 0.6476 and 0.6408 are providing support

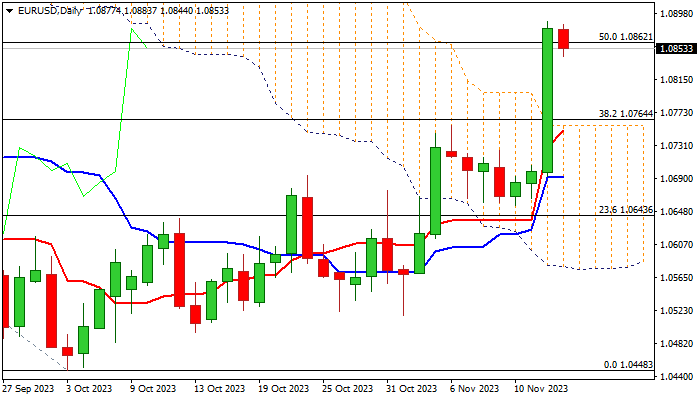

EUR/USD: Euro Consolidating After Biggest One-Day Advance in a Year

EURUSD edged lower in European trading on Wednesday as traders collected some profits after Tuesday’s 1.7% advance (the biggest one-day gain in one year), sparked by bigger than expected drop in US inflation in October, which deflated dollar

Near-term picture is increasingly bullish after Tuesday’s acceleration surged through few key technical barriers, resulting in close well above thick daily Ichimoku cloud and above 50% retracement of 1.1275/1.0448 downtrend.

Bulls are taking a breather and positioning for fresh push higher, with broken 200DMA (1.0802) to ideally contain dips and offer better buying opportunities for extension towards targets at 1.0959/1.1000 (Fibo 61.8% / psychological).

Broken Fibo 38.2% and daily cloud top (1.0764/1.0759 respectively) mark pivotal supports which should hold extended dips and keep near-term bias with bulls.

Res: 1.0887; 1.0945; 1.0959; 1.1000.

Sup: 1.0802; 1.0764; 1.0756; 1.0700.

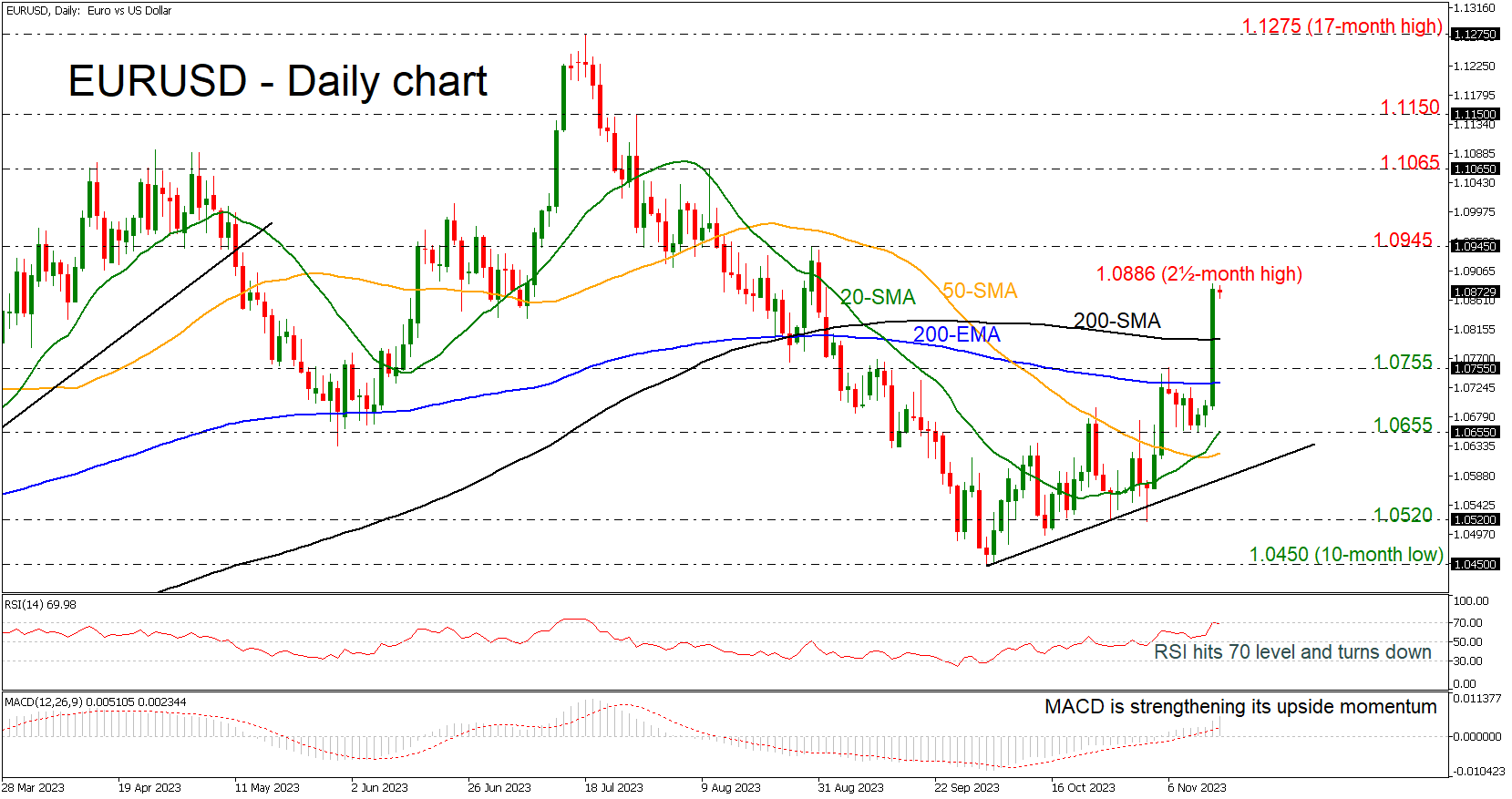

EURUSD Eases after Sharp Rally Towards 2½-month High

- EURUSD adds 200 pips and tries to reach 1.0900

- Trades well above moving average lines

- RSI suggests negative correction

EURUSD skyrocketed yesterday after the US CPI release and added almost 200 pips, recording a new two-and-a-half-month high of 1.0886, but its rally seems to have temporarily paused.

Approaching the 1.0900 area, it seems to be a real struggle to surpass this round number according to the RSI. The RSI is losing momentum after it touched the overbought region; however, the MACD oscillator is still strengthening its bullish movement, suggesting that the bulls may not give the battle yet. Also, the pair climbed well above the 200-day exponential moving average (EMA) and the 200-day simple moving average (SMA), which were acting as strong resistance levels in the past and the 20- and 50-day SMAs printed a bullish crossover.

In the event the pair re-activates its uptrend above Tuesday’s top of 1.0886, the next target will be the 1.0945 resistance. Even higher, the bulls might head for the 1.1065 barricade, which was a key resistance zone during August.

On the downside, the 200-day SMA at 1.0800 is the first stop to have in mind ahead of the 1.0755 support and the 200-day EMA at 1.0733. Hence, a step beneath that line, the 1.0655 line, which overlaps with the 20-day SMA might produce negative volatility.

Summarizing, EURUSD is sustaining an upward trend above the moving average lines and well above the short-term uptrend line. To attract new buyers, the pair will need to pierce through the 1.0900 psychological mark.