Sample Category Title

An Avalanche of (High-Profile) ECB and Fed Speeches

Markets

US eco data yesterday ranged from lower-than-expected PPIs over a decent headline but underlying weak NY manufacturing index to above-consensus retail sales. In the end, markets focused mainly on the latter, allowing yields to claw back some of the sharp CPI driven losses the day before. Treasury yields added between 7.3 and 8.7 bps with the belly of the curve outperforming. In an interview with the Financial Times, Fed’s Daly welcomed the deceleration in price rises but warned against proclaiming victory over inflation just yet. A stop-start (announcing the end of the hiking cycle only to reverse course again later) mentality would hurt credibility, she added. Daly, voting next year, noted that rate cuts are not happening for a while. German yields rose 2.2-5.7 bps in a steepener. In both regions, however, markets hold on to the idea of central banks starting to cut rates around mid-2024 with tentative pricing for an even earlier move in either May (Fed) or April (ECB). Against this backdrop, bourses stayed resilient despite the yield rise. It’s all about expectations for a one-in-a-lifetime soft landing scenario. European stocks rose 0.55% (EuroStoxx50), Wall Street added up to 0.47% (Dow Jones). The trade-weighted US dollar bounced off 104 support to close around 104.38. EUR/USD returned a fraction of Tuesday’s massive gain. The pair finished at 1.0848. Sterling slid after a tiny miss in CPI also sealed the BoE’s fate in the eyes of markets. EUR/GBP rose to 0.8736.

Eyes in the Asian session this morning were on the Biden-Xi encounter, the first in-person meeting in a year. Both sides hailed the progress made but it comes with little impact on markets. The US Senate approved a stopgap funding bill overnight. In doing so, Congress avoided a looming shutdown threat this Friday only to postpone it to early next year. The recurring debacle is rarely a topic of importance for markets. But these last-minute deals do highlight the continued polarization which was cited by several rating agencies (Moody’s most recently) as one of the reasons for downgrading the credit outlook. The eco calendar later today has little to offer but the weekly US jobless claims. There’s an avalanche of (high-profile) ECB and Fed speeches scheduled for release. They serve as a wildcard for trading. In any case we don’t think they’ll be able to dramatically turn the tide on core bond yields. The force of gravity remains strong for the time being with next support in the US 10-y yield kicking in at 4.34% and around 2.50% in the German 10-y yield. The dollar remains vulnerable if bets on a soft landing continue to support equity markets. EUR/USD 1.0945 is the upside reference on the technical charts.

News & Views

The Australian economy in October added 55k additional jobs, data from the Australian Statistics Office showed. Markets expected a gain of about 24k. Most of the growth came from part time jobs (37.9 k). However, the reacceleration followed modest job growth in September. In this respect the average increase over the past two months was even slightly lower than the average of the previous year. The unemployment rate increased from to 3.7% as the participation rate jumped from 66.8% to 67%. Growth of hours worked slowed recently as an indication of softening labour demand. Job growth mainly being driven by part-time rather than full time jobs points in the same direction. In this respect, the strong headline data probably don’t ask for immediate further action from the Reserve Bank of Australia. The 2-y Australia government bond yield currently holds little changed at 4.23%. After yesterday’s rebound, the Aussie dollar is again losing the AUD/USD 0.65 big figure. (0.6475).

Czech central Bank Vice governor Jan Frait yesterday in an interview said that he sees external and domestic conditions as being in favour of lowering borrowing costs. Frait was one of the two MPC members that voted for but didn’t get a first 25 bps rate cut at the November policy meeting. He admitted that he can’t predict when the majority of policymakers will back a rate cut. He noted that central bankers are facing a big dilemma as they ‘are concerned about the last mile and whether inflation won’t remain entrenched in people’s heads and whether they won’t demand significantly higher wages’ that are not in line with bringing inflation sustainably back to the 2.0% target. Frait said that other MPC members’ caution at the November meeting also occurred as they want to assess the extent of the traditional price increases in January. Frait sees less such need as the Bank should be forward looking. Next CNB policy meetings are scheduled for December 21 and February 8 next year.

EUR/USD Daily Outlook

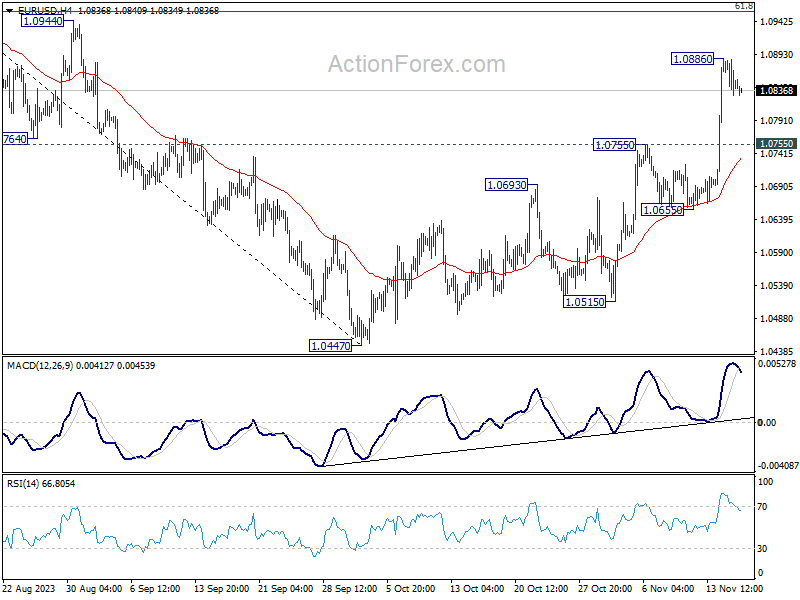

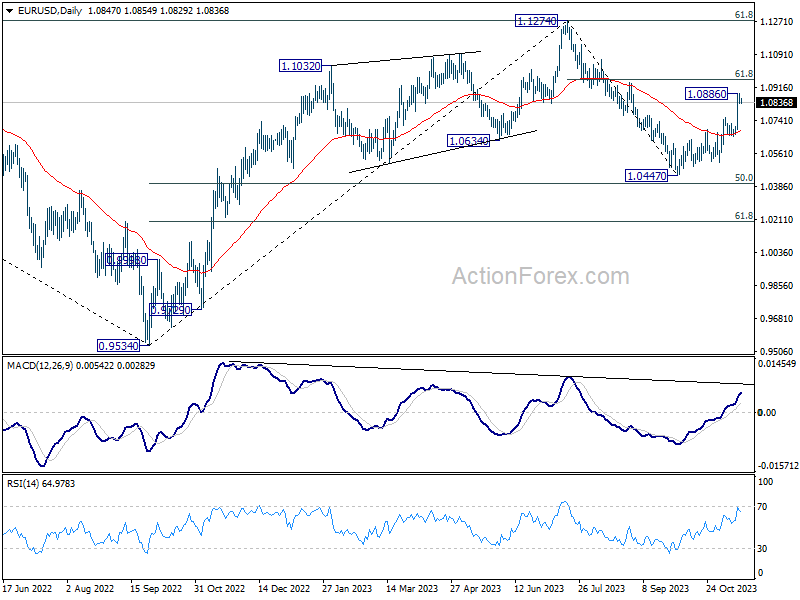

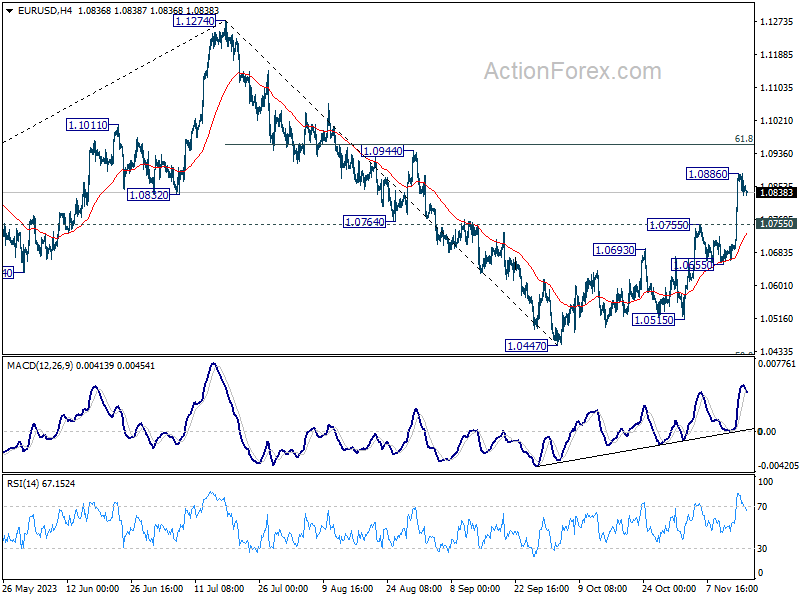

Daily Pivots: (S1) 1.0824; (P) 1.0855; (R1) 1.0878; More...

Intraday bias in EUR/USD is turned neutral with 4H MACD crossed below signal line. Some consolidations would be seen below 1.0886 temporary top first. Downside of retreat should be contained by 1.0755 resistance turned support to bring another rally. On the upside, above 1.0886 will resume the rebound from 1.0447 to 61.8% retracement of 1.1274 to 1.0447 at 1.0958 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. However, break of 1.0447 will resume the fall to 61.8% retracement of 0.9543 to 1.1274 at 1.0199.

GBP/USD Daily Outlook

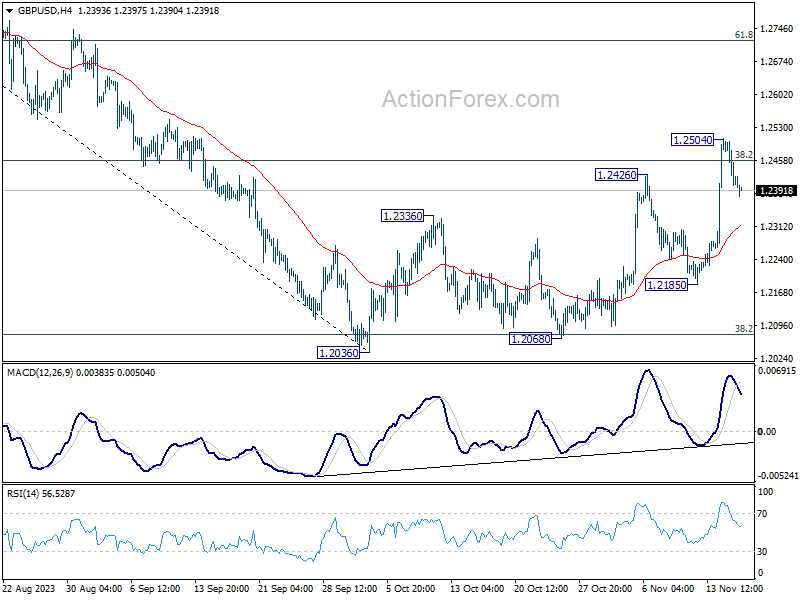

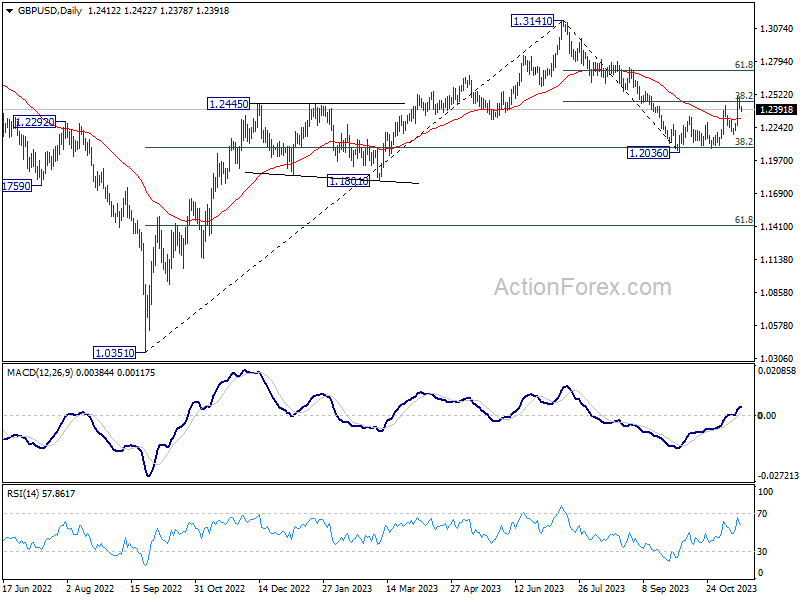

Daily Pivots: (S1) 1.2379; (P) 1.2441; (R1) 1.2477; More...

Intraday bias in GBP/USD remains neutral for consolidations below 1.2504 temporary top. Downside should be contained by 55 4H EMA (now at 1.2311) to bring another rally. On the upside, break of 1.2504 will resume the whole rebound from 1.2036. Sustained trading above 38.2% retracement of 1.3141 to 1.2036 at 1.2458 will pave the way to 61.8% retracement at 1.2716.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 will argue that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

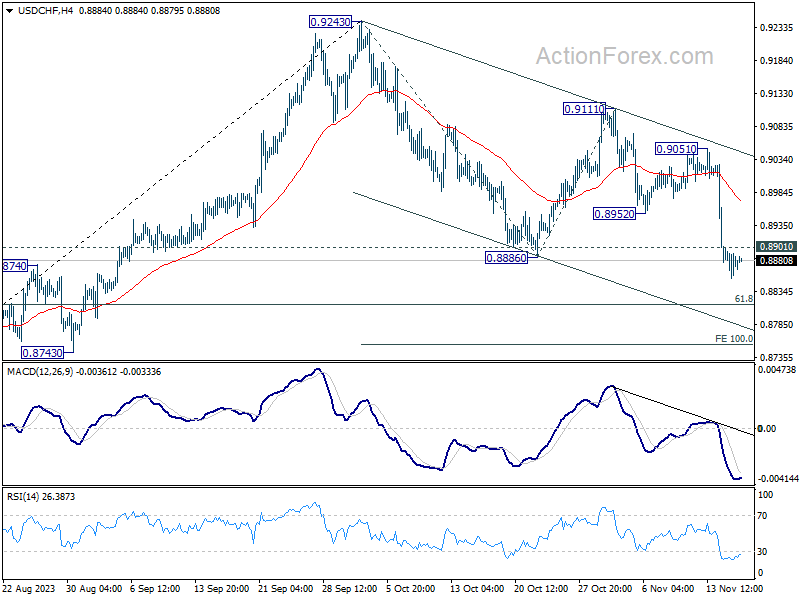

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8837; (P) 0.8933; (R1) 0.8988; More....

Intraday bias in USD/CHF stays on the downside at this point. Fall from 0.9243 is in progress and should target 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754. On the upside, above 0.8901 minor resistance will turn intraday bias neutral and bring consolidations first. But recovery should be limited well below 0.9051 resistance to bring another decline.

In the bigger picture, price actions from 0.8551 are currently seen as a correction to the decline from 1.0146. Fall from 0.9243 is seen as the second leg for now. Deeper fall would be seen to 61.8% retracement of 0.8551 to 0.9243 at 0.8815. Sustained break there will bring retest of 0.8551 low. For now, this will remain the favored case as long as 0.9111 resistance holds.

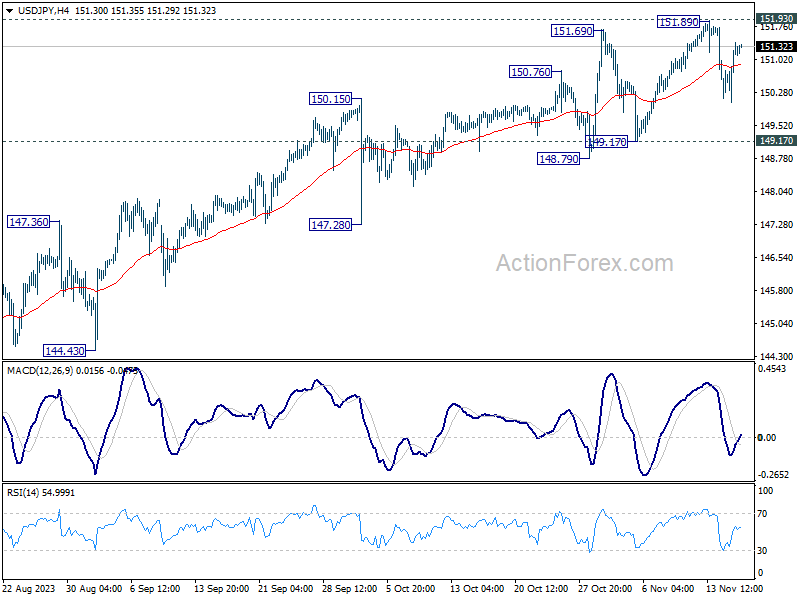

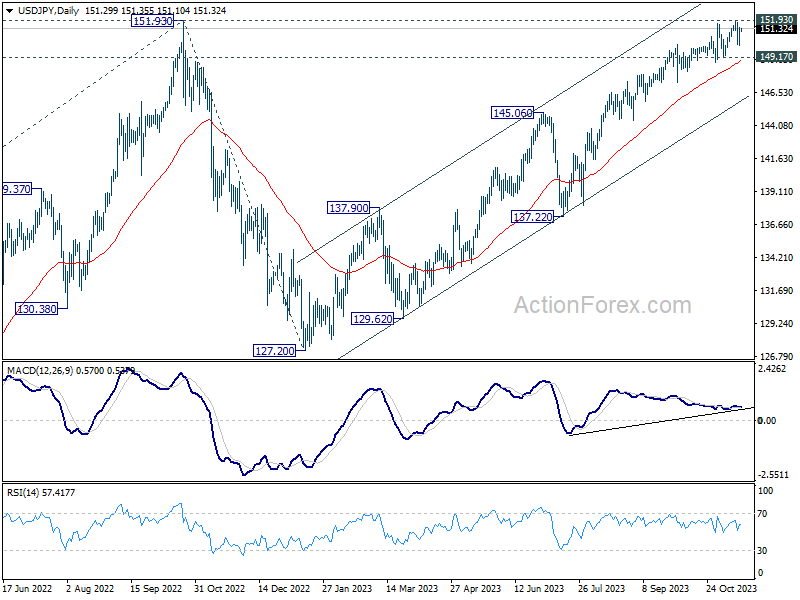

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.49; (P) 150.95; (R1) 151.86; More...

Intraday bias in USD/JPY stays neutral as range trading continues. Further rally is in favor as long as 149.17 support holds. On the upside, decisive break of 151.93 resistance will confirm resumption of long term up trend. Next target will be 157.69 projection level. However, firm break of 149.17 will be a sign of bearish reversal and bring deeper fall to 147.28 support first.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 (2021 low) to 151.93 from 127.20 at 157.69.

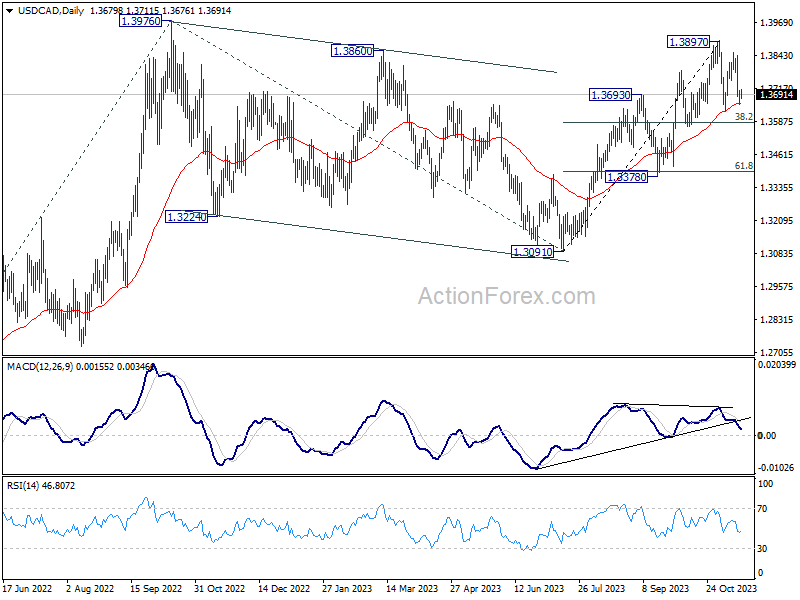

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3655; (P) 1.3683; (R1) 1.3710; More...

Intraday bias in USD/CAD is turned neutral first with current recovery. Overall outlook is unchanged that price actions from 1.3897 are developing into a consolidation pattern. While deeper fall cannot be ruled out, downside should be contained by 38.2% retracement of 1.3091 to 1.3897 at 1.3589 to bring rebound. Break of 1.3897 is expected at a later stage to resume larger rally.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will remain the favored case as long as 1.3378 support holds.

Happily Digesting

Yesterday was about digesting Tuesday’s softer-than-expected US CPI data, feeling relieved that the US Senate passed a stopgap spending bill to avert a government shutdown and welcoming a softer-than-expected producer price inflation, and a softer-than-expected decline in US retail sales – which came to support the idea that, yes, the US economy is probably slowing but it is slowing slowly, while inflation is easing at a satisfactory pace.

The sweet mix of the recent economic data backs the idea that the Federal Reserve (Fed) could achieve what they call a ‘soft landing’ following an aggressive monetary policy tightening – and more importantly stop hiking the interest rates.

At this point, investors are 100% sure that the Fed won’t hike rates in December. They are 100% sure that the Fed won’t hike rates in January. There is more than a quarter of a chance for a rate cut to be announced by March. And the pricing suggests that there is a higher chance for a rate cut in the Fed’s May meeting, than not.

Conclusion: investors threw the Fed’s ‘higher for longer’ mantra out of the window this week.

But this is certainly as good as it gets in terms of Fed optimism. If the markets go faster than the music, the Fed must calm down the game by a tough talk, and if needed, by more action. The Fed’s Mary Daly expressed her concerns about the Fed’s credibility if it declared victory over inflation prematurely. And credibility is the most important tool that a central bank has. When the credibility is broken, there is nothing to break.

Therefore, the US 2-year yield may have bottom at 4.80% level and should be headed back toward 5%. The US 10-year yield should hold ground above 4.50%. As per equities, the direction is unclear to everyone, but the recent dovish shift in Fed expectations and the dropping yields gave a great energy boost to the US stocks. The S&P500 jumped more than 10% since end of October, the rate-sensitive Nasdaq 100 is now flirting with the highest levels since summer while the Russell 2000 index is having a blast since its October dip. The index rallied almost 12% in 3 weeks, pulled out the 50-DMA, the major 38.2% Fibonacci retracement and consolidated gains in the medium-term bullish consolidation zone yesterday.

As equities move higher and inflation slows, the anxiety regarding short positions mount – hence short covering is adding to the positive pressure.

The Big Short’s Micheal Burry reportedly exited his short position against SPDR’s P&P500 and Invesco’s QQQ and began betting against semiconductor stocks, including Nvidia.

Nvidia, on the other hand, is flirting with its ATM levels near the $500 per share level. A quick glance at Nvidia’s long-term price chart clearly suggests that the chances are that we are in the middle of an AI-led bubble and that the exponential move cannot extend infinitely. Yes, AI is boosting Nvidia’s revenue and profits, but the revenues that will flow into the pockets of Nvidia thanks to AI are already embedded in the share price, and we will likely see the price bubble burst. But there are two things to keep in mind when you bet against a bubble. 1. A bubble is a bubble only when it bursts – it's like ‘you are innocent until proven guilty’. And 2. You can wait a while before the market comes back to its senses. For now, we are in the middle of making eye-popping predictions and beating them. The company is due to release earnings on November 21st.

One big risk for Nvidia is the tense relations between the US and China, and the extension of chip export curbs to a bigger range of Nvidia chips. This week’s meeting between Biden and Xi carried hope that the high-level communication could help melting ice. There has apparently been some ‘real progress’ in restoring military communication and foreign policy... Then, Joe Biden said that Xi is a dictator.

The Relief-Rally Fades Amid a Rebound in Fates

Market movers today

Today's US data is not the kind that usually moves markets a lot: industrial production, NAHB housing market index and Philly Fed index for November. On the latter, we saw a quite strong increase in the Empire index, but both Empire and Philly Fed are rather unreliable guides to the manufacturing PMI that we get next week.

We have speeches today from Fed's Mester and Williams, and from ECB's President Lagarde.

In Norway, the Q4 Expectations Survey will be important for Norges Bank (NB) in the current situation with a weakening NOK but all other inflation drivers are moving in the opposite direction. In the previous Expectations Survey, inflation expectations were rising across the board. Lower inflation and weaker GDP growth beyond the autumn have probably dampened inflation expectations, especially on 12-month and 2-year horizons.

The 60 second overview

Markets. After a string of sessions characterised by sharp declines in global real rates and a subsequent very strong risk appetite in markets risk sentiment has soured somewhat again over the last 18 hours. The culprits seem to be a combination of US data releases driving a rebound in US rates (see below) and weak Chinese house data overnight driving a sell-off in the big Chinese indices with some spill-over to Asian markets. The USD sell-off has stabilised and industrial metals have edged lower. Also oil has extended yesterday's decline on the back of both worse global risk appetite and the weekly US crude inventory report showing a larger-than-expected build in inventories.

Markets wrap. Yesterday' release of US data was a mixed bag. Overall data indicated a slowing economy and weaker price growth - yet the market reaction was to roll back expectations for US rate cuts next year. In short, both retail sales and not least Empire Manufacturing surprised to the topside while producer prices came in lower than expected. On US retail sales the headline figure printed at -0.1% m/m (cons.: -0.3%, prior: 0.9%). Excluding the volatile auto and gas sales, the retail sales control group revealed monthly growth of 0.2% m/m which was in line with expectations. Additionally, last month's retail sales control group was revised higher, from 0.6% to 0.7% which overall painted a picture of somewhat better goods buying from the US consumer in recent months than expected. On the other hand, the October PPI figures were weaker than expected, with the headline at -0.5% m/m (cons.: 0.1%, prior: 0.4%), while November Empire Manufacturing rose to 9.1 (cons.: -3.0, prior: -4.6), the highest reading since April.

In the euro area, industrial production declined slightly more than expected in September, at -1.1% (consensus: 1.0%, prior: 0.6%). Hence, the hard data continues to confirm the weakening in the soft indicators in the region.

US-China diplomatic relations. Chinese President Xi Jinping is currently meeting his US counterpart in Joe Biden in California. This is the first in-person meeting between the two presidents in a year and the initial remarks from both sides have been that the talks have been constructive. In particular the two country heads have agreed on resuming collaboration on military communication, drug trafficking prevention and on AI-progresses. Also the question on Taiwan was discussed with both parties explaining a wish to maintain peace. There has been no market reaction.

Equities: Equities continued higher yesterday but lost some steam during the afternoon. Yields continue to govern the direction of equities, and it was after yields began to rise that equities retreated. Europe rose a mild 0.4% and US 0.2%. Cyclicals beat defensives and value made a revenge vs growth. Staples and banks were in the top yesterday while utilities declined a little after the surge earlier this week. US futures are a tad lower this morning.

FI: US data releases drove global yields higher yesterday. UST yields ended the day up by 7-8bp across the curve, while the Bund curve bear steepened with the 10Y tenor rising 4bp. The 5y5y EUR inflation swap rate dropped to a new 6M low of 2.39% as prices on oil and European natural gas (TTF) fell throughout the day. Markets continue to price in close to 90bp worth of ECB cuts next year.

FX: Yesterday's session saw a slight reversal of the relief induced rallies to the cyclically sensitive currencies as NZD, AUD, NOK, SEK and the CEEs all traded on the back-foot. The USD decline has also stabilised with EUR/USD edging below the 1.0850 mark after having traded close to 1.09 yesterday morning.

Credit: Credit markets settled into calmer territory after the massive post-CPI rally on Tuesday. Itrax closed 0.5bp higher at 70.7bp, while Itrax Xover closed 2.1bp higher to close at 390.2bp. Primary markets were still fairly active with corporates and financials seeking to utilize the final couple of weeks of the pre-Xmas issuance window.

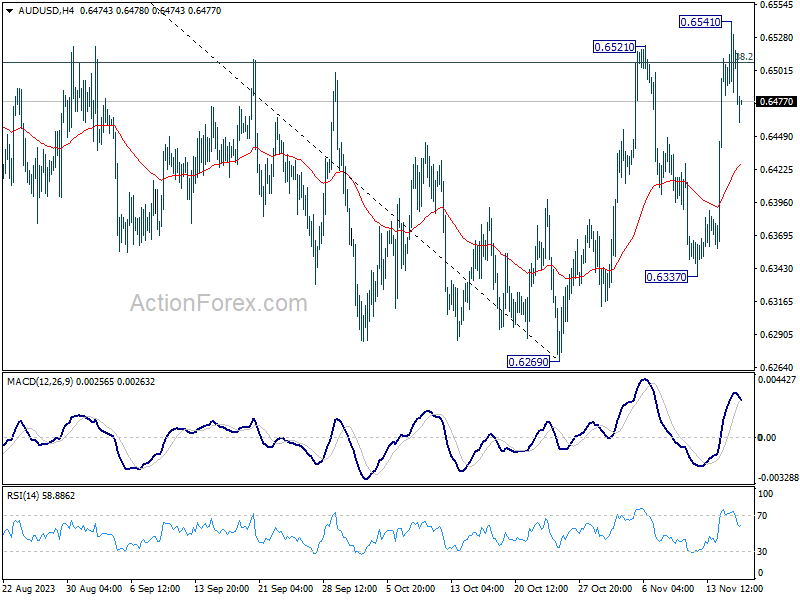

AUD/USD Daily Report

Daily Pivots: (S1) 0.6481; (P) 0.6512; (R1) 0.6540; More...

Despite spiking higher to 0.6541, subsequent retreat in AUD/USD suggests that a temporary top was formed. Intraday bias is turned neutral for some consolidations first. Downside should be contained by 55 4H EMA (now at 0.6427) to bring rebound. Break of 0.6541, and sustained trading above 38.2% retracement of 0.6894 to 0.6269 at 0.6508, will argue that whole corrective fall from 0.7156 has completed with three waves down to 0.6269. Stronger rally should seen to falling channel resistance (now at 0.6684) next.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of the corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

Aussie Dips Amid Mixed Employment Data and Global Market Cautiousness

Australian Dollar weakens broadly in Asian session, as Australian employment data and shifting global risk sentiment take center stage. The mixed nature of the latest Australian jobs report is causing a rethink among investors regarding RBA's next steps. Despite robust increase in overall employment numbers, a nuanced look reveals cracks in the job market's strength.

The unexpected uptick in the unemployment rate and deceleration in work hours growth are clear indicators of a cooling labor market. This cooling trend reinforces expectation for RBA to hit pause on its interest rate hikes again in December meeting. RBA is likely to closely monitor the economic indicators over the festive season to gauge the need for further monetary policy adjustments in February.

Australian Dollar's descent is also exacerbated by a cooling of risk-on sentiment that had buoyed the global markets earlier in the week. Investors are seemingly taking a breather and reassessing their positions. A key event that has captured the market's attention is the meeting between US President Joe Biden and Chinese President Xi Jinping, which occurred on the sidelines of APEC summit. Although the meeting marked a step forward in re-establishing high-level military communications, it fell short of offering substantial breakthroughs in broader geopolitical tensions. The absence of a new defense minister appointment in China, following the unexplained dismissal of Gen. Li Shangfu, adds to the air of uncertainty affecting market sentiment.

In the broader currency spectrum, New Zealand Dollar is joining Australian Dollar as one of the day's weakest performers so far, alongside British Pound and Canadian Dollar. On the flip side, Japanese Yen is emerging as the strongest currency for the day at this point, with t Dollar and Swiss Franc also showing resilience. Euro's performance remains uneven across different pairings.

Despite the daily fluctuations, when looking at the weekly performance, Dollar continues to be at the bottom of the league, with Japanese Yen and Canadian Dollar also underperforming. Australian and New Zealand Dollars, along with Swiss Franc and Euro, are experiencing the strongest gains, whereas British Pound exhibits mixed results across the board.

Technically, EUR/USD turned into consolidation after surging to 1.0886 earlier in the week. Some consolidations would be seen in the near term, but outlook will stay bullish as long as 1.0755 resistance turned support holds. Above 1.0886 will resume the rebound from 1.0447 to 61.8% retracement of 1.1274 to 1.0447 at 1.0958. Upside momentum will likely start to wane above 1.0958 fibonacci level. But any acceleration above there could be an early signal of more intense selloff in Dollar elsewhere.

In Asia, Nikkei closed down -0.27%. Hong Kong HSI is down -1.11%. China Shanghai SSE is down -0.49%. Singapore Strait Times is up 0.11%. Japan 10-year JGB yield is down -0.002 at 0.795. Overnight, DOW rose 0.47%. S&P 500 rose 0.16%. NASDAQ rose 0.07%. 10-year yield rose 0.094 to 4.535.

Fed's Daly cautions against premature end to rate hikes, emphasizes need for patience

San Francisco Fed President Mary Daly, in an interview with the Financial Times, acknowledged the "very, very encouraging" signs of falling inflation in this week's data. However, she cautioned against hastily concluding the rate-raising cycle, emphasizing the importance of a cautious and informed approach.

Daly expressed concern about prematurely ending the cycle, noting the potential risks involved. "We have to be bold enough to say 'we don't know' and bold enough to say 'we need to take the time to do it right'," she stated. She warned that a premature halt could lead to a 'stop-start' scenario, which could ultimately harm the Fed's credibility.

In her view, rate cuts are not on the immediate horizon. "Rate cuts are 'not happening for a while'," Daly remarked, suggesting a continued commitment to the current restrictive monetary policy direction until there is substantial evidence of a sustainable return to the 2% inflation target.

Australia's employment grows 55k, yet signs of cooling emerge

Australia's labor market displayed stronger-than-anticipated performance in October, with employment figures surpassing expectations. The economy added 55k jobs, well above forecasted growth of 22.8k. This increase was driven by both full-time and part-time employment, which rose by 17k and 37.9k respectively.

Despite this robust job growth, unemployment rate edged up slightly from 3.6% to 3.7%, aligning with market expectations. Pparticipation rate also saw an uptick, rising by 0.2% to 67.0%. Additionally, month-over-month hours worked in the economy increased by 0.5%.

Bjorn Jarvis, ABS head of labour statistics, noted that over the past two months, this equates to an average monthly employment growth of approximately 31k people, slightly lower than average growth of 35k people a month since October 2022.

He also highlighted that annual growth rate in hours worked has slowed to 1.7%, down from around 5% mid-year, and lower than annual employment growth of 3.0%. This slowdown may suggest that "the labour market is starting to slow, following a particularly strong period of growth."

Japan's exports increase for second month, despite persistent decline in China shipments

In October, Japan experienced a mixed bag in its trade sector. Exports saw a modest rise of 1.6% yoy to JPY 9167B, marking the second consecutive month of growth, albeit at a slower pace compared to September's 4.3% yoy increase.

One notable aspect was the continued decline in shipments to China, which fell by -4.0% yoy. This marks the eleventh consecutive month of decline, underscoring the strained trade relations and potentially shifting economic alliances in the region.

Conversely, exports to the US surged by 8.4% yoy, buoyed by robust demand for hybrid vehicles and mining and construction machinery. This surge propelled the value of U.S.-bound shipments to record levels. Similarly, exports to Europe experienced a healthy increase of 8.9% yoy, indicating diversified trade relations.

On the import front, Japan witnessed a significant drop of -12.5% yoy to JPY 9810B. The trade balance resulted in a deficit of JPY -663B.

Looking at seasonally adjusted terms, both exports and imports saw month-on-month declines, with exports decreasing by -1.2% mom to JPY 8800B and imports falling by -0.7% mom to JPY 9262B. Consequently, trade deficit widened from September's JPY -420B to JPY -462B.

Looking ahead

The European economic calendar is empty today. Canada will release housing starts in North American session. US will release jobless claims, Philly Fed survey, and industrial production.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6481; (P) 0.6512; (R1) 0.6540; More...

Despite spiking higher to 0.6541, subsequent retreat in AUD/USD suggests that a temporary top was formed. Intraday bias is turned neutral for some consolidations first. Downside should be contained by 55 4H EMA (now at 0.6427) to bring rebound. Break of 0.6541, and sustained trading above 38.2% retracement of 0.6894 to 0.6269 at 0.6508, will argue that whole corrective fall from 0.7156 has completed with three waves down to 0.6269. Stronger rally should seen to falling channel resistance (now at 0.6684) next.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of the corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (USD) Oct | -0.46T | -0.71T | -0.43T | |

| 23:50 | JPY | Machinery Orders M/M Sep | 1.40% | 0.90% | -0.50% | |

| 00:00 | AUD | Consumer Inflation Expectations Nov | 4.90% | 4.80% | ||

| 00:30 | AUD | Employment Change Oct | 55.0K | 22.8K | 6.7K | |

| 00:30 | AUD | Unemployment Rate Oct | 3.70% | 3.70% | 3.60% | |

| 04:30 | JPY | Tertiary Industry Index M/M Sep | -1.00% | -0.10% | -0.10% | 0.70% |

| 13:15 | CAD | Housing Starts Y/Y Oct | 255K | 270K | ||

| 13:30 | USD | Initial Jobless Claims (Nov 10) | 222K | 217K | ||

| 13:30 | USD | Import Price Index M/M Oct | -0.30% | 0.10% | ||

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Nov | -11 | -9 | ||

| 14:15 | USD | Industrial Production M/M Oct | -0.40% | 0.30% | ||

| 14:15 | USD | Capacity Utilization Oct | 79.40% | 79.70% | ||

| 15:00 | USD | Natural Gas Storage |