Sample Category Title

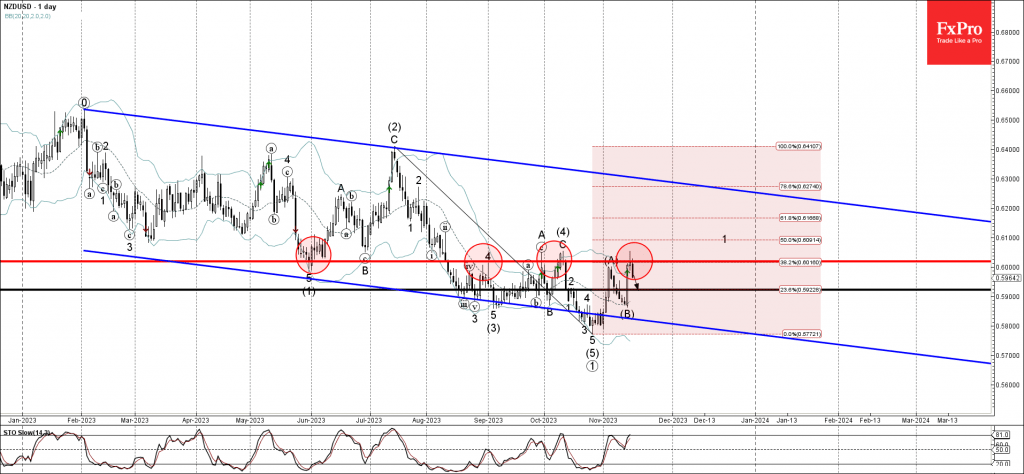

NZDUSD Wave Analysis

- NZDUSD reversed from resistance level 0.6020

- Likely to fall to support level 0.5925

NZDUSD currency pair recently reversed down from key resistance level 0.6020 (which has been reversing the price from August) coinciding with the upper daily Bollinger Band.

The resistance level 0.6020 was also strengthened by the coinciding 38.2% Fibonacci correction of the downward impulse from July.

Given the clear daily uptrend, NZDUSD currency pair can be expected to fall further toward the next support level 0.5925.

Bitcoin BTCUSD Buying The Dips At The Blue Box Area

In this article we’re going to take a quick look at the Elliott Wave charts of Bitcoin BTCUSD published in members area of the website. As our members know BTCUSD is showing impulsive bullish sequences in the cycle from the 24955.26 low that were calling for a further strength. Recently we got a pull back that has ended at the Blue Box zone,our buying area. In the further text we are going to explain the Elliott Wave Forecast and trading setup.

BTCUSD Elliott Wave 1 Hour Chart 11.04.2023

BTCUSD is giving us correction that is unfolding as a Zig Zag pattern. At the moment structure is still incomplete. Bitcoin can see more downside toward 35173.76-33717.907 blue box ( buying zone). We don’t recommend selling Bitcoin and prefer the long side. From the marked zone, BTCUSD should ideally make either rally toward new highs or in 3 waves bounce alternatively. Once bounce reaches 50 Fibs against the (b) blue high 37547, we will make long position risk free ( put SL at BE) and take partial profits.

Official trading strategy on How to trade 3, 7, or 11 swing and equal leg is explained in details in Educational Video, available for members viewing inside the membership area.

Quick reminder on how to trade our charts :

Red bearish stamp+ blue box = Selling Setup

Green bullish stamp+ blue box = Buying Setup

Charts with Black stamps are not tradable. 🚫

Bitcoin ( BTCUSD ) Elliott Wave 1 Hour Chart 4.14.2023

BTCUSD made extension toward our buying zone : 35173.76-33717.907. Bitcoin found buyers at the blue box as expected and we got good reaction from there , 5 waves impulsive rally that retested previous peak. Currently doing short term pull back against the 34805.11 low that can see approximately 36506-35663 area. As far as the pivot at 34805.11 low holds, we can see further rally once short term pull back completes.

Sunset Market Commentary

Markets

US eco data are at it again. Weekly jobless claims picked up slightly more than expected (from 218k to 231k) to the highest level since mid-August. Continuing claims, the number of people who have already filed an initial claim and are still filing for unemployment benefits, rose to 1865k. That’s slightly above the early April top (1861k) and the highest level since November 2021. October import and export prices completed this week’s hattrick of positive inflation surprises following CPI on Tuesday and PPI yesterday. Import prices fell by 0.8% M/M (-2% Y/Y) while export prices were 1.1% lower compared with September (-4.9% Y/Y). Markets anticipated a more gentle decline. The headline Philly Fed Business Outlook improved slightly more than hoped (-5.9 from -9), but underlying details showed deteriorations in new orders (1.3 from 4.4), employment (0.8 from 4), shipments (-17.9 from 10.8) and the general outlook six months from now (-2.1 from 9.2). Prices paid meanwhile confirmed the disinflationary trend (14.8 from 23.1) while prices received remain more sticky (14.8 from 14.6). The US Note future rallied back to this week’s earlier high, but failed for now to really test these tops. US yields obviously show a similar trading pattern, attempting to extend this week’s correction lower. Daily changes vary between -7.8 bps at the frond end and -5.7 bps at the very long end. German Bund yields again shadow US ones lower, but with a marginal outperformance of the very long end (-5.4 bps for 30-yr vs -4 bps for 2yr). The trade weighted dollar equally tries to keep it together just above this week’s sell-off lows (104.33 vs 104) with EUR/USD currently changing hands at 1.0869, up from an open at 1.0848 and compared to this week’s top at 1.0887. European stock markets are mixed, ending a three-day rally with key US gauges marginally weaker at the start of today’s US session. EUR/GBP set a new (intraday) cycle top 0.8766 (highest since May), ignoring central bank talk. Bank of England policy maker Greene suggested that monetary policy needs to be restrictive for longer as the notion that the long run neutral rate might be a bit higher as well as the natural rate of unemployment isn’t something everyone’s grappling with yet. Greene is one of the hawks on the board, unsuccessfully voting for higher rates at the previous meeting. Her comments contrast with analyst talk today that the BoE could pull the trigger on policy rates ahead of the Fed and the ECB.

News & Views

Hungary’s central bank (MNB) vice-governor Virag today said the monetary institution will likely continue to cut interest rates at an unchanged pace of 75 bps despite inflation declining more than hoped-for. He said that it’s realistic for rates to go below 11% by year’s end and below 10% in February. Real interest rates will remain positive in the period ahead, he added, with the central bank (and KBC Economics) expecting inflation to ease to 7-8% by December. The MNB started lowering the base rate end October. Doing so surprised markets who were at the time expecting a 50 bps cut. It underpinned the decision with inflation falling faster than expected. With October CPI two weeks later again dropping more than forecasted (sub 10%), speculation for more aggressive rate cuts to the tune of 100 bps promptly rose. Virag’s comments come after similar ones from Zsolt Kuti, a close advisor to the Hungarian rate-setting committee. He argued against cutting rates too hastily yesterday. Their (scripted?) appearance leaves little traces on the Hungarian forint, which is trading unchanged around a four-month high of EUR/HUF 376.3.

Adam Bodnar, the man widely tipped to be Poland’s next Justice minister, in a Reuters scoop said he’ll let the European Public Prosecutor’s Office (EPPO) know that it wishes to join in the first weeks after a new, pro EU opposition-led government is formed. The EPPO is an independent public prosecution office of the EU which deals with cases affecting the bloc's financial interests. 22 out of the 27 member states have joined but Poland under the outgoing PiS government hasn’t (yet). For Bodnar, joining EPPO is a sign of good faith to “show we are coming back to the rule of law”, a critical condition to unlock billions of EU funds that are currently held back. In other news, Polish core inflation came in bang in line with expectations. Monthly dynamics accelerated from -0.1% to +0.6% in October, bringing the y/y figure to 8%. The (PiS-minded) central bank recently took a hawkish turn after the October elections, with risks of the policy rate (5.75%) being kept stable at least through March 2024.The zloty vastly outperforms regional peers today. EUR/PLN drops to 4.37. This is the strongest PLN level since early 2020.

BoE Policymaker Pushes Back Against Market Interest Rate Expectations, Jobless Claims Promising

We're seeing a more muted session in financial markets on Thursday following a couple of days in which investors have been very encouraged by the economic data.

Inflation figures from the US and UK have been very promising, so much so that markets see almost no chance of another rate hike in this cycle from either the Fed or BoE and a high likelihood of a rate cut by the end of the second quarter of next year.

That's despite one BoE policymaker, Megan Greene, pushing back against that, although it is worth noting she does sit at the hawkish end of the committee having recently been in the minority voting for a rate hike. While her concerns over wages and where interest rates will land in the future are perfectly reasonable, it seems markets are more aligned with the dovish end of the MPC.

I expect many policymakers will continue to push back against markets for now until they can be absolutely certain that inflation has been controlled and is on a path back to 2%. A late pivot has likely always been the strategy and I expect it remains the case. Higher for longer remains the mantra but I suspect it won't be too much longer now.

Encouraging claims data but we've had numerous false dawns before

Jobless claims were a welcome addition to recent data that pointed to a slight cooling in the labour market and, perhaps, the US economy. Of course, we're talking about a very small step in the right direction, from the perspective of the Fed, and it will need to be backed by a lot more over the coming months, but it's a start. Claims have been trending higher in recent weeks but we've seen numerous false dawns this year and this could simply be the latest.

Will Oil prices encourage Russia and Saudi Arabia to extend cuts?

Oil prices have been trending lower again in recent days after rebounding on Tuesday, around the October lows in the case of WTI. There are clearly concerns around demand going into next year, particularly around China, which OPEC this week sought to relieve, to no avail.

The recent trend may make it difficult for Saudi Arabia and Russia to allow their unilateral cuts to expire at the end of the year, which is something markets may be gradually pricing in. The lack of a commitment to extend so far may reflect a desire to not but as we've seen so often in the past, the producers will do whatever it takes to support the price. The question may be whether they can get others on board.

Gold eyeing $2,000 after more promising US data

Gold prices are pushing higher once more after running into some resistance around $1,980 on Wednesday. While it hasn't yet moved above yesterday's highs, momentum still looks healthy and gold bulls may have sights set on $2,000 once more. Recent data has been very favorable for gold, it will be interesting to see whether that will be enough to propel it above this big psychological zone.

GBP/USD Edges Lower, Eyes Retail Sales

- UK retail sales expected to rebound in October

- US PPI and retail sales decline

The British pound has extended its losses on Thursday. In the European session, GBP/USD is trading at 1.2401, down 0.11%.

The pound is having a roller-coaster week. GBP/USD surged 1.8% on Tuesday following the soft US inflation print and climbed to a two-month high. However, the pound has since coughed up about half those gains and is trading at the 1.24 line. The UK releases retail sales on Friday, which could result in further volatility.

UK retail sales had a dreadful September, coming in at -0.9% m/m and missing the forecast of 0.2%. The markets are expecting a rebound in October, with a forecast of 0.3%. September was unseasonably hot, which led to fewer purchases of autumn clothing. Consumers remain deeply pessimistic about the economy and are being squeezed by higher heating and fuel costs, elevated borrowing costs and a softer job market.

On the inflation front, there was good news on Wednesday as inflation dropped to 4.6%, down sharply from 6.7% and below the forecast of 4.8%. This was the lowest level since October 2021 and inflation has finally dropped below 5%. However, the BoE has been stressing that the battle against inflation is far from over, and has projected that inflation won’t fall to the 2% target until late 2025.

In the US, producer prices fell 0.5% m/m in October, its largest drop since April 2020 and below expectations. The decline in gasoline prices was a major factor in the soft release. Retail sales for October dipped 0.1%, missing the estimate of 0.3% and snapping a six-month streak of gains. The weak numbers are further evidence that the US economy is cooling down.

GBP/USD Technical

- GBP/USD is putting pressure on support at 1.2374. Below, there is support at 1.2312

- 1.2476 and 1.2522 are the next resistance lines

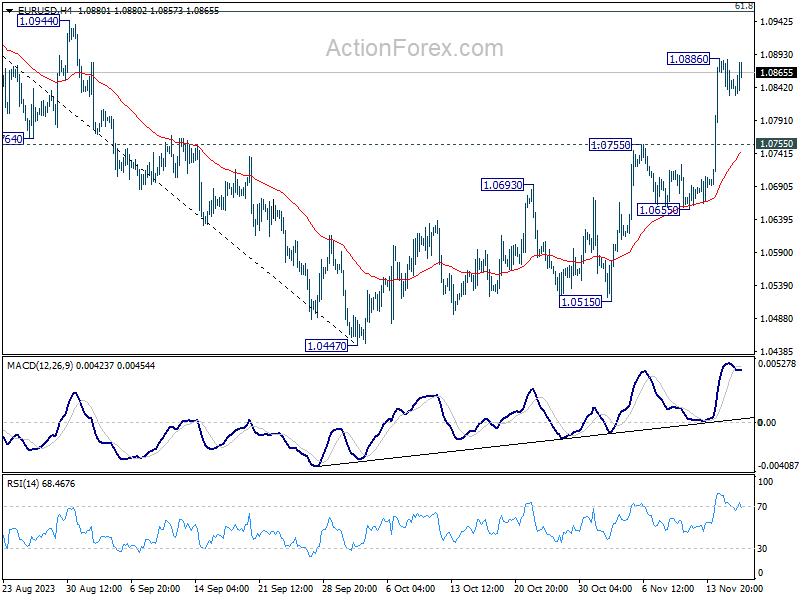

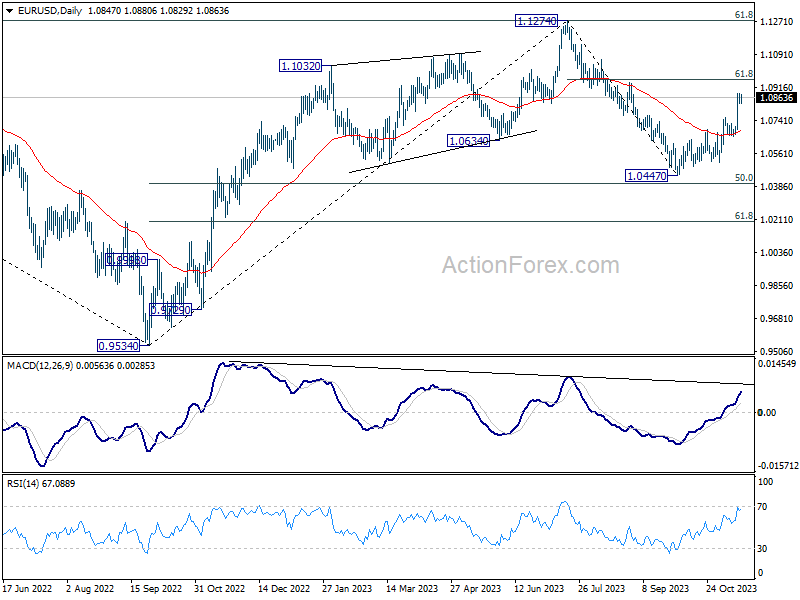

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0824; (P) 1.0855; (R1) 1.0878; More...

EUR/USD bounces mildly in early US session but stays below 1.0886. Intraday bias remains neutral and some more consolidations could be seen. But downside of retreat should be contained by 1.0755 resistance turned support to bring another rally. On the upside, above 1.0886 will resume the rebound from 1.0447 to 61.8% retracement of 1.1274 to 1.0447 at 1.0958 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. However, break of 1.0447 will resume the fall to 61.8% retracement of 0.9543 to 1.1274 at 1.0199.

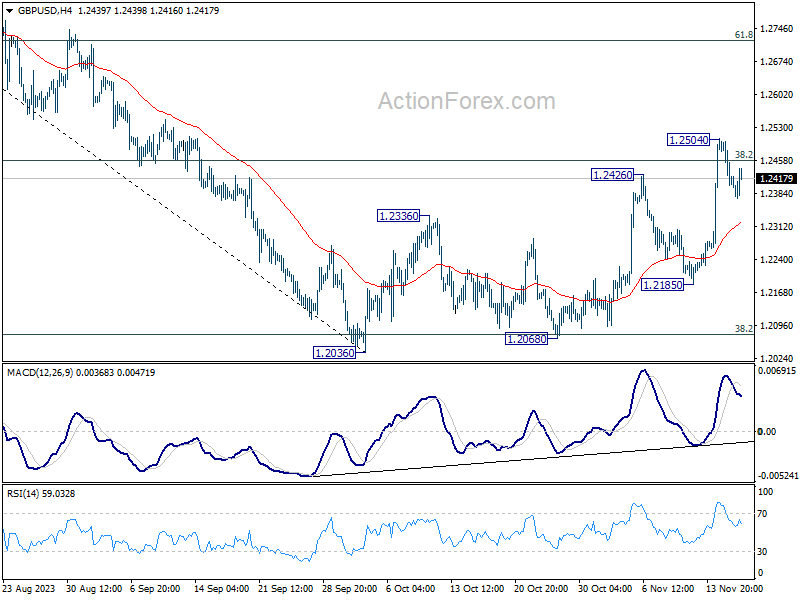

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2379; (P) 1.2441; (R1) 1.2477; More...

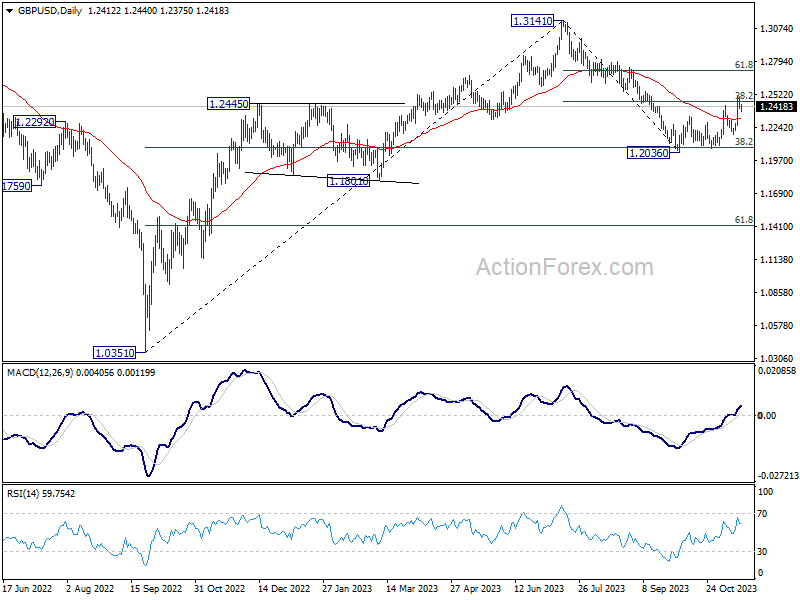

Intraday bias in GBP/USD stays neutral as consolidation from 1.2504 is extending. Downside should be contained by 55 4H EMA (now at 1.2323) to bring another rally. On the upside, break of 1.2504 will resume the whole rebound from 1.2036. Sustained trading above 38.2% retracement of 1.3141 to 1.2036 at 1.2458 will pave the way to 61.8% retracement at 1.2716.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 will argue that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

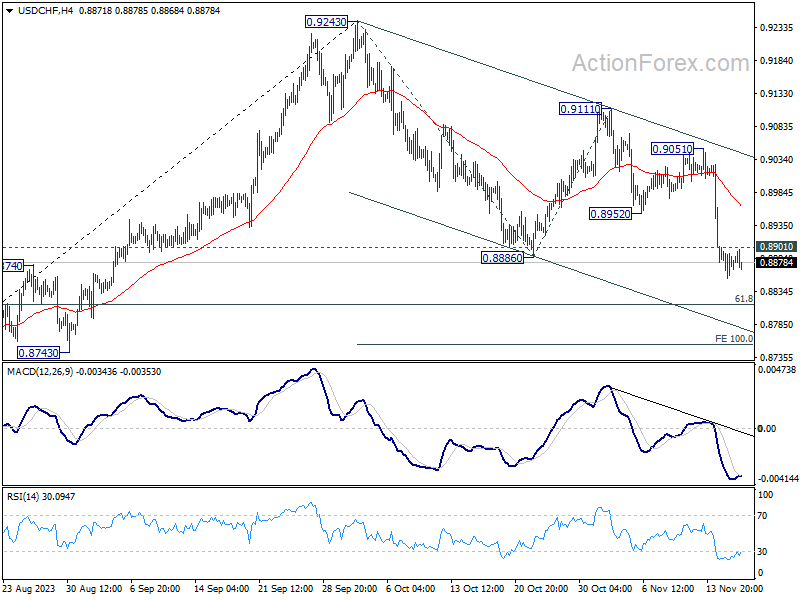

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8837; (P) 0.8933; (R1) 0.8988; More....

No change in USD/CHF's outlook and intraday bias stays on the downside. Fall from 0.9243 is in progress and should target 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754. On the upside, above 0.8901 minor resistance will turn intraday bias neutral and bring consolidations first. But recovery should be limited well below 0.9051 resistance to bring another decline.

In the bigger picture, price actions from 0.8551 are currently seen as a correction to the decline from 1.0146. Fall from 0.9243 is seen as the second leg for now. Deeper fall would be seen to 61.8% retracement of 0.8551 to 0.9243 at 0.8815. Sustained break there will bring retest of 0.8551 low. For now, this will remain the favored case as long as 0.9111 resistance holds.

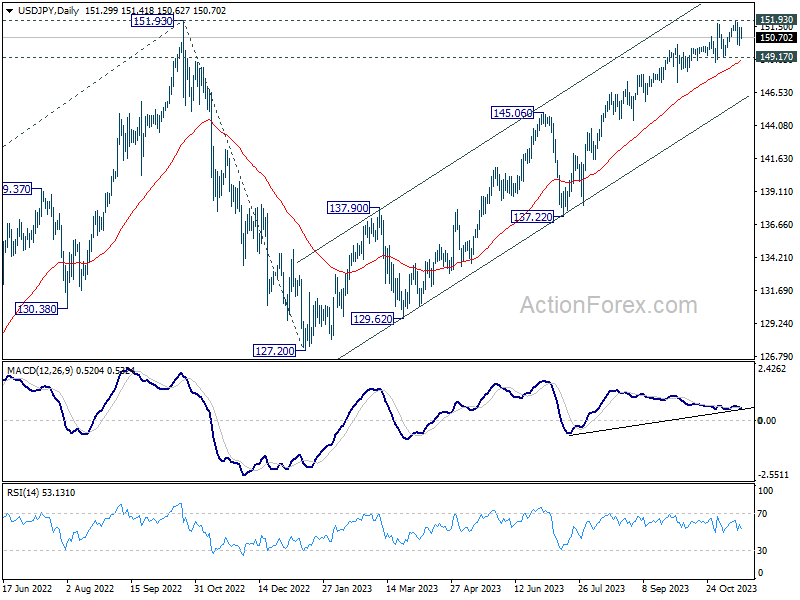

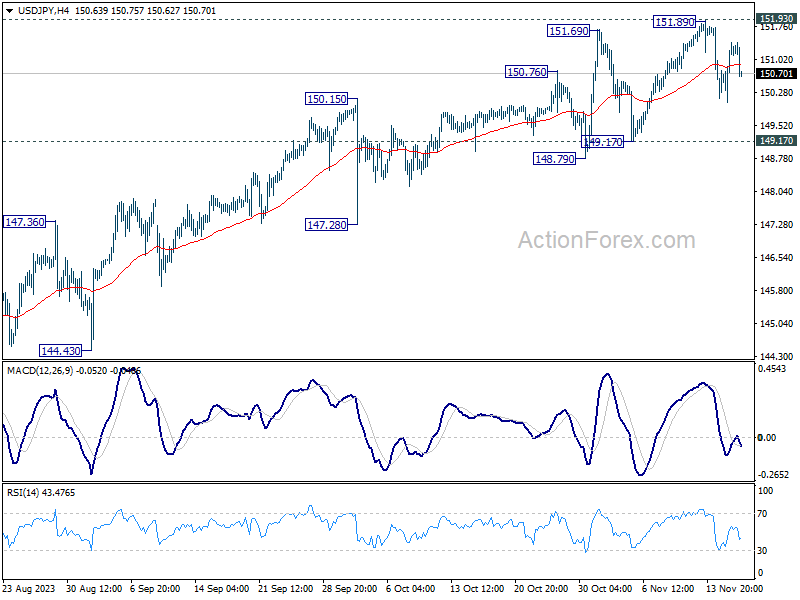

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.49; (P) 150.95; (R1) 151.86; More...

USD/JPY dips notably in early US session but stays well inside established range of 149.17/151.89. Intraday bias stays neutral for the moment. Further rally is in favor as long as 149.17 support holds. On the upside, decisive break of 151.93 resistance will confirm resumption of long term up trend. Next target will be 157.69 projection level. However, firm break of 149.17 will be a sign of bearish reversal and bring deeper fall to 147.28 support first.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 (2021 low) to 151.93 from 127.20 at 157.69.