Sample Category Title

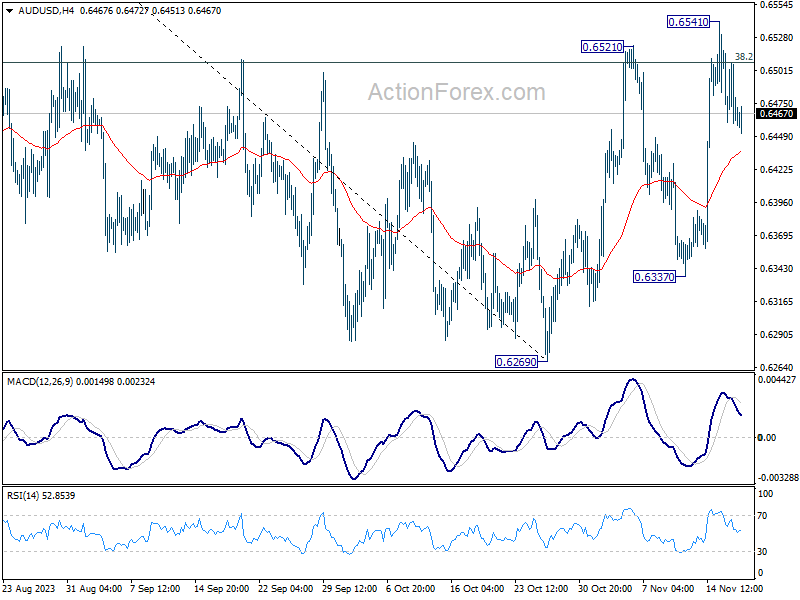

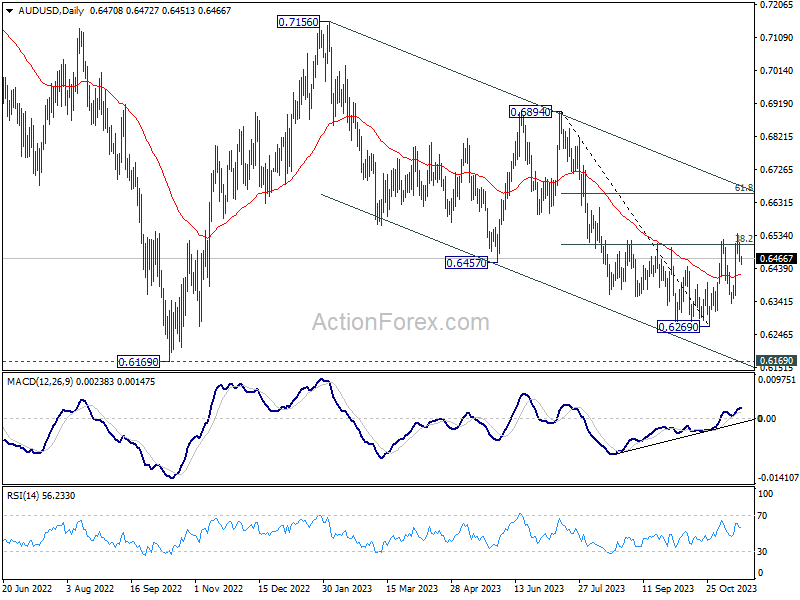

AUD/USD Daily Report

Daily Pivots: (S1) 0.6448; (P) 0.6485; (R1) 0.6508; More...

Intraday bias in AUD/USD remains neutral for consolidations below 0.6541. Downside should be contained by 55 4H EMA (now at 0.6437) to bring rebound. Break of 0.6541, and sustained trading above 38.2% retracement of 0.6894 to 0.6269 at 0.6508, will argue that whole corrective fall from 0.7156 has completed with three waves down to 0.6269. Stronger rally should seen to falling channel resistance (now at 0.6674) next.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of the corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

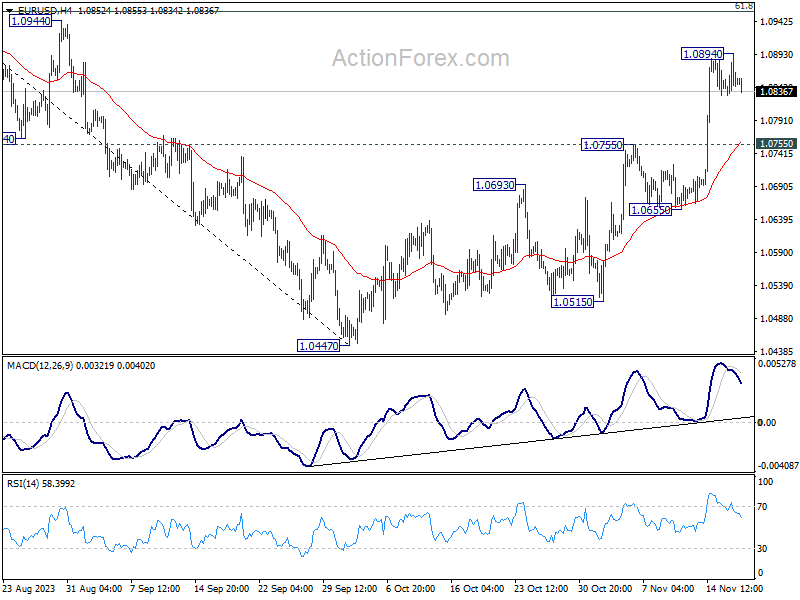

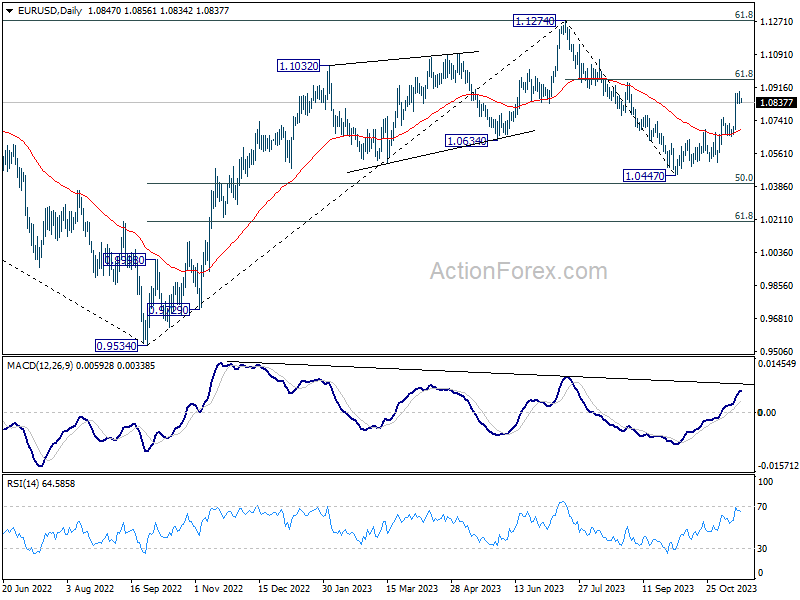

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0823; (P) 1.0860; (R1) 1.0889; More...

EUR/USD retreated back to established range and intraday bias remains neutral. Some more consolidation could be seen but downside of retreat should be contained by 1.0755 resistance turned support to bring another rally. On the upside, above 1.0894 will resume the rebound from 1.0447 to 61.8% retracement of 1.1274 to 1.0447 at 1.0958 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. However, break of 1.0447 will resume the fall to 61.8% retracement of 0.9543 to 1.1274 at 1.0199.

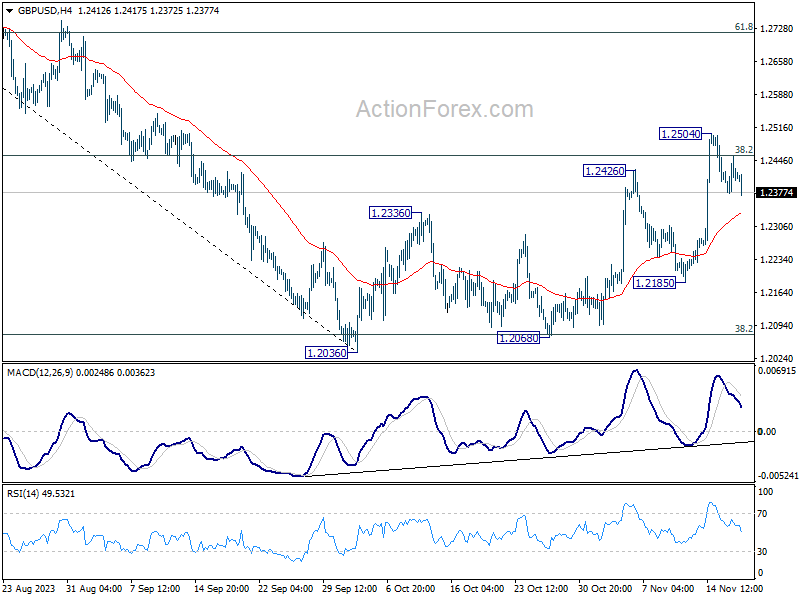

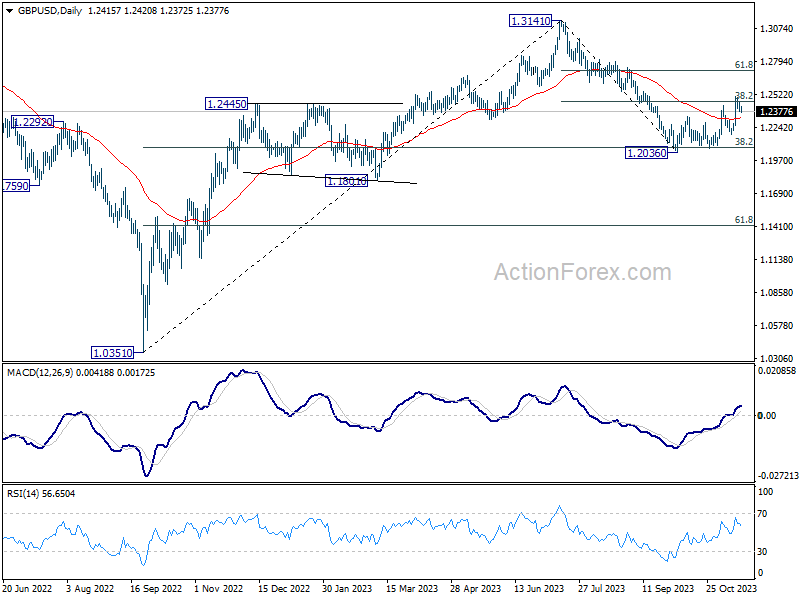

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2375; (P) 1.2416; (R1) 1.2454; More...

Intraday bias in GBP/USD remains neutral for the moment. Consolidation from 1.2504 is extending and deeper retreat could be seen. But downside should be contained by 55 4H EMA (now at 1.2334) to bring another rally. On the upside, break of 1.2504 will resume the whole rebound from 1.2036. Sustained trading above 38.2% retracement of 1.3141 to 1.2036 at 1.2458 will pave the way to 61.8% retracement at 1.2716.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 will argue that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

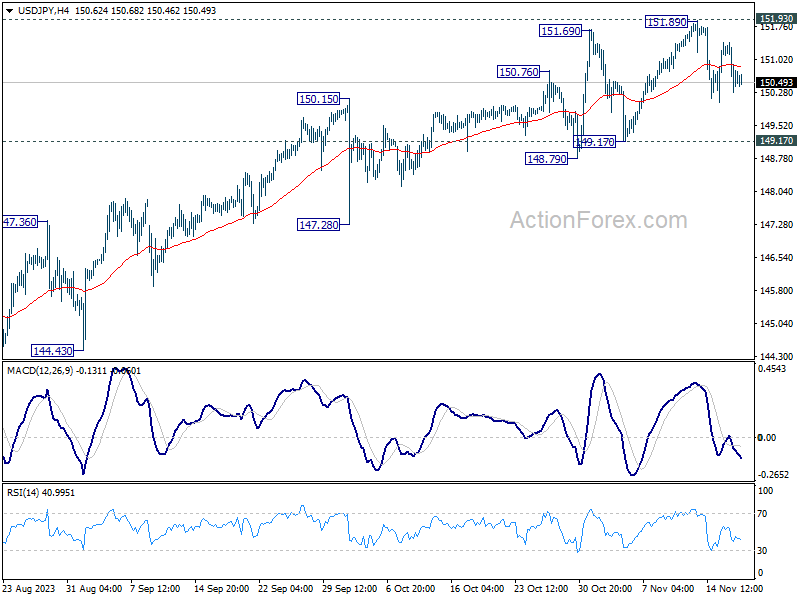

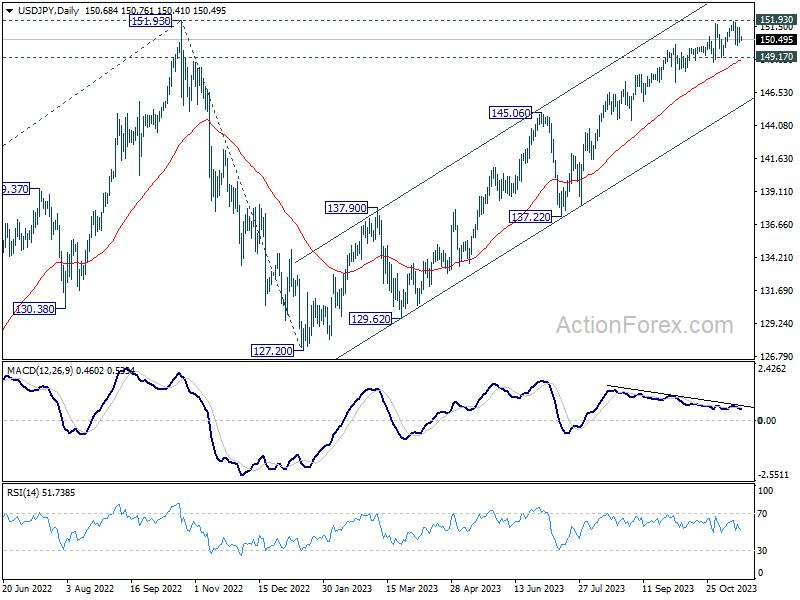

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.20; (P) 150.82; (R1) 151.34; More...

Range trading continues in USD/JPY and intraday bias stays neutral. Further rally is in favor as long as 149.17 support holds. On the upside, decisive break of 151.93 resistance will confirm resumption of long term up trend. Next target will be 157.69 projection level. However, firm break of 149.17 will be a sign of bearish reversal and bring deeper fall to 147.28 support first.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 (2021 low) to 151.93 from 127.20 at 157.69.

Yen Tops G10 Scoreboard in Quiet Asian Trading

Markets

The US yield curve hit a weekly low yesterday with declines ranging between 7.4 and 10.3 bps. Wednesday’s unconvincing rebound was indeed a head fake and got fully erased a day later on a set of sub-consensus economic data. These included jobless claims, industrial production and the NAHB housing market index. They pointed at a decelerating economy and, importantly, job market. German yields followed the US trend and slipped 4.4 to 6.6 bps across the curve. Moves on core bond markets this time however didn’t trigger a risk-on rally similar to what we’ve seen earlier this week. Stocks inched lower in Europe and treaded water in the US. Oil prices tanked 4.6% (Brent $77.42/b) amid demand concerns as well as supply being not as constrained as expected with producers outside OPEC+ swooping in to compensate for the cartel’s (voluntary) output curbs. Gold prices rallied 1%. FX markets favoured the big three: USD, EUR and JPY with the latter outperforming in a daily perspective. USD/JPY eased to 150.73 while EUR/JPY gave back some of the large gains over the past few days. EUR/USD neared 1.09 before settling in the mid 1.08-09 area. EUR/GBP mirrored those moves with an intraday high of 0.87665 only to finish at 0.8742.

The yen continues to top the G10 scoreboard in quiet Asian trading this morning, discarding dovish comments for BoJ governor Ueda. He expects inflation to slow in FY2025, adding that there’s not enough certainty that the central bank will reach its price goal sustainably. US Treasury yields recover 1-3 bps in technically insignificant trading. Today’s economic calendar won’t inspire much. US housing data is worth following up, given that this market is increasingly suffering from rising unaffordability (high mortgage rates and prices due to low supply/availability). If anything, a miss to the downside is more likely to strengthen current market thinking rather than vice versa. Central bank speeches will flood the terminal screens again. Many, if not most of the ones having talked recently show little willingness to play ball with markets. But neutral or even hawkish comments can’t compete with what the data are telling. The correction lower in core bond yields may slow but probably won’t reverse going into the weekend. Support to look for in the US 10-y yield stands at 4.34%. Germany’s 10-y is nearing the upward sloping trendline connecting the 2023 correction lows (but the ones in March). To the extent markets continue to see the Fed as being able to more aggressively cut rates, dollar weakness may prevail. EUR/USD’s downside looks solid. Poor UK retail sales this morning wrapped up this week’s eco update. Sterling slips, pushing EUR/GBP north to 0.8755. A weekly close above 0.871/0.873 (50% recovery on the EUR/GBP 2023 decline) worsens sterling’s technical picture.

News & Views

Activity in the US housing market is declining sharply according to the sentiment index of the US National Association of Home Builders. The NAHB sentiment index tumbled from 40 to 34, the lowest reading YTD. Both the indices for current single family sales and future sales dropped substantially as was the case for prospective buyers traffic. Sentiment also dropped in three of the for regions under survey. However, the comments from NABH chief economist Robert Dietz were slightly more comforting that data of the survey as he was quoted that recent macro-economic data point to improving conditions for home construction in the coming months. ‘Given the lack of existing home inventory, somewhat lower mortgage rates will price-in housing demand and are likely to set the stage for improved further views of market conditions in December’ the NAHB was quoted.

According to comments from the officers of the Budget Committee of the German government, final deliberations on the German 2024 draft budget have been interrupted early in this morning. The halt in the deliberations comes after a ruling of the German constitutional court earlier this week. Due to the ruling, the government is facing a financing hole as the court judged that the government isn’t allowed to transfer €60 bln of funds that were made available during the pandemic to be redirected for initiatives that support the green transition and other industrial projects. Still, the government expects that final budget figures and new debt figures will be made public after a meeting next Thursday, instead of this week as planned earlier.

Oil: Race to the Bottom

This week could hardly be better in terms of economic, political, and geopolitical news. The US inflation slowed more than expected, the US politicians inked a short-term deal to avert a shutdown. On top, the US retail sales fell last month, but fell less than expected, the initial jobless claims rose, and the US unemployment benefits reached the highest level in almost two years, factory production fell more than expected and homebuilder sentiment fell to the lowest level for the year.

The US 2-year yield fell again to test the 4.80% level for the third time since the beginning of this month and the 10-year yield slipped below 4.50%, again. The S&P500 consolidated gains above the 4500 psychological level, and Nasdaq 100 remained bid a few points below the summer peak. Small stocks in the Russell 2000 however fell 1.50% yesterday, and the Chinese stocks couldn’t extend gains after the Biden-Xi summit. Nasdaq’s Golden Dragon China index spent just one day above its 50-DMA -thanks to fresh stimulus measures announced by China earlier in the week, then returned below this level.

Alibaba called off its much-expected cloud division spin off this week because the company serves Chinese tech and AI companies and needs advanced chips – the kind of chips that Nvidia makes – to compete with Amazon Web Services, or Microsoft’s Azure. And with the US chip export ban looming, it’s certainly not the best timing to take on a new challenge. Investors are not ready to go back to Chinese tech names in the middle of a chip war between the US and China.

FX and commodities

The US dollar index held ground at the 100-DMA, but remains offered near the major 38.2% Fibonacci retracement, as the softening Fed expectations increase bets against the greenback. The EURUSD consolidates gains after being propelled into the medium-term bullish consolidation zone. Earlier this week, the EU revised its 2023 growth forecast for Europe down to 0.6%, but it said that it sees growth return to the old continent by next year. Even Germany, which is suffering from a severe economic slowdown, could grow. Recession or not, the European Central Bank (ECB) is not expected to cut its interest rates until, at least, July next year. The ECB’s slight hawkish note could support a further rise to the 1.10 mark. Cable, on the other hand, returned below its 200-DMA after a softer-than-expected inflation report released earlier this week revived the Bank of England (BoE) doves as well.

In commodities, gold surfs on falling yields and high tensions in the Middle East. The yellow metal extended its gains to $1988 yesterday but should see resistance into the $2000 level in the absence of any major news.

American crude sank to $72pb yesterday, after having tested and failed to clear the $78/80 resistance earlier this week. The 3.6-mio-barrel increase in the US inventories last week served as a good excuse to sell the top, along with the rising worries of global slowdown. No one cares about the Middle East carnage or OPEC cuts. At the current levels, oil is oversold, and we could see another correction attempt, but gains will likely remain limited.

Could OPEC do anything about it? Yes, but not now. The market focus has heavily shifted to the weakening demand outlook from tightening supply If Saudi announces further supply cuts, and if the market doesn’t react, its finances will take a bigger hit. As such, the selloff could extend below the $70 mark. Key support stands at $63.50, the May dip.

Oil Trading Heavy

Market movers today

In Sweden, the October LFS labour market report will give some clues about the severity of underlying trends in the labour market. Recent seasonally adjusted data shows a drop in employment, a corresponding rise in unemployed people while at the same time there was a decline in the non-labour force. This suggests that at least partially, a rising number of job seekers may be the reason for the rise in the unemployment rate rather than it being a direct consequence of firms starting to shed work force to protect profits.

In the euro area, we get the final version of the already published October inflation (2.9% y/y for core HICP). There are rarely significant revisions, but we will get more details on the drivers.

ECB President Lagarde will give a keynote speech at the Frankfurt European Banking Congress.

US housing starts and building permits data for October are due. This is interesting to watch for signs that high interest rates are finally dampening housing investment, although that is not the expectation for today.

San Francisco Fed President Daly speaks. She is not a voter on the FOMC currently but will be in 2024.

The 60 second overview

Markets and economic data releases. The amount of market-moving news out yesterday was generally quite limited. Yields fell after the release of higher-than-expected US claims data and worse-than-expected industrial production figures in the afternoon, while the upbeat Philly-Fed for November received less market attention.

Michael Barr, vice chair for supervision at the Fed, in a speech yesterday warned about the basis trade in the treasury market, which has risen substantially in size since the turn of the year. Barr warned about the risks of the treasury market functioning due to the high degree of leverage that hedge funds typically apply in the trade.

In Europe, ECB chief Lagarde expressed some caution on the outlook for financial stability in the Eurozone, as higher funding costs and lower lending volumes are gradually putting more pressure on the banking sector. Additionally, policymakers should pay extra attention to the impact on non-performing loans stemming from the combination of weak growth and higher rates.

Oil. Oil prices dropped yesterday and Brent slipped back below USD 80/bbl. More weak US data put an end to the rebound at the beginning of the week. As we have noted before, we think oil prices could potentially be a bellwether for a deterioration of global aggregate demand. The fact that a weaker USD, geopolitical risk and low OPEC+ production has failed to keep up oil prices supports this view. If the sell-off continues we will keep a watch-out for comments from Saudi Arabia about a further extension of the 1mb/d voluntary output cut, and from the US about resumption of buying of oil for its strategic reserves. Both factors would help floor oil prices.

FI: Global yields drifted gradually lower in yesterday's session, reversing Wednesday's move up. The Bund curve bull-steepened, with the 10Y tenor declined by 6bp throughout the day. The move was quite gradual for most of the day, but the weaker-than-expected US claims data accelerated the move in the afternoon. The 10Y BTP-Bund spread ended down by 3bp at 175bp, the lowest level since the end of August. The 5y5y EUR inflation swap rate continued declining in line with energy prices throughout the day. The current 2.36% is the lowest level seen since the end of March. Long UST yields were down by 8bp throughout the session.

Equities calmed on Thursday. Yields lower was not enough to trigger further buying, but US closed up a mild 0.1% while Europe pulled back -0.7%. We see this breather as good news as volatility comes down. However, pundits may claim that this is the start of weak data no longer being perceived as good news, as it was weakening job data that triggered the rebound lower in yields. The best performers lately retreated, including small caps or regional banks. Quality sectors outperformed, including utilities, tech and communication. Value cyclicals were at the bottom. US futures are unchanged this morning.

FX: Oil and commodity currencies have come under renewed pressure amid the decline in oil and commodity prices broadly. Especially NOK traded heavy in yesterday's session with EUR/NOK back close to the 11.90 mark. EUR/USD ended the session at close to unchanged levels after having surged on weaker US data releases. EUR/GBP hovers around the 0.8750 mark while USD/JPY has fallen back a full figure to 150.50.

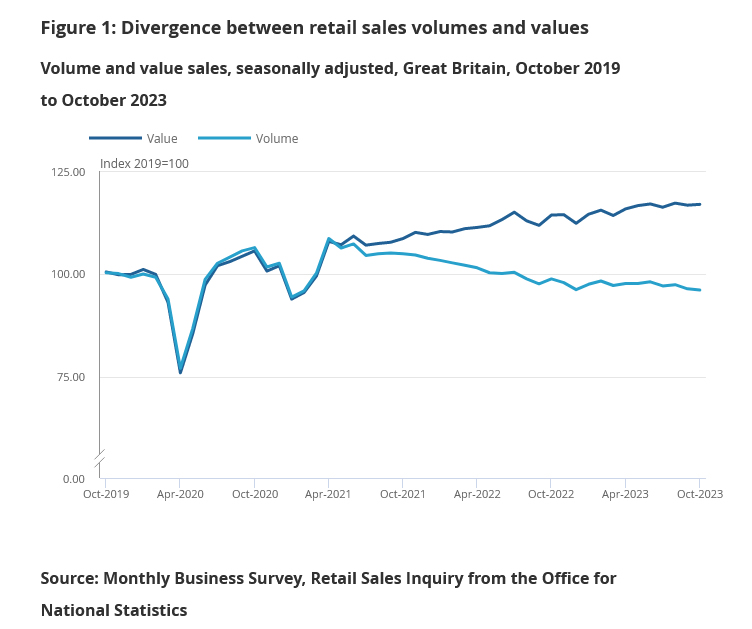

UK retail sales volume down -0.3% mom in Sep, sales value down up 0.1% mom

UK retail sales volume fell -0.3% mom in September, much worse than expectation of 0.3 mom rise. Ex-automotive fuel sales volume fell -0.1% mom.

Looking broader, sales volumes (include and excluding fuel) fell by -1.1% in the three months to October 2023 when compared with the previous three months.

In value term, retail sales rose 0.1% mom while ex-fuel sales was flat 0.0% mom.

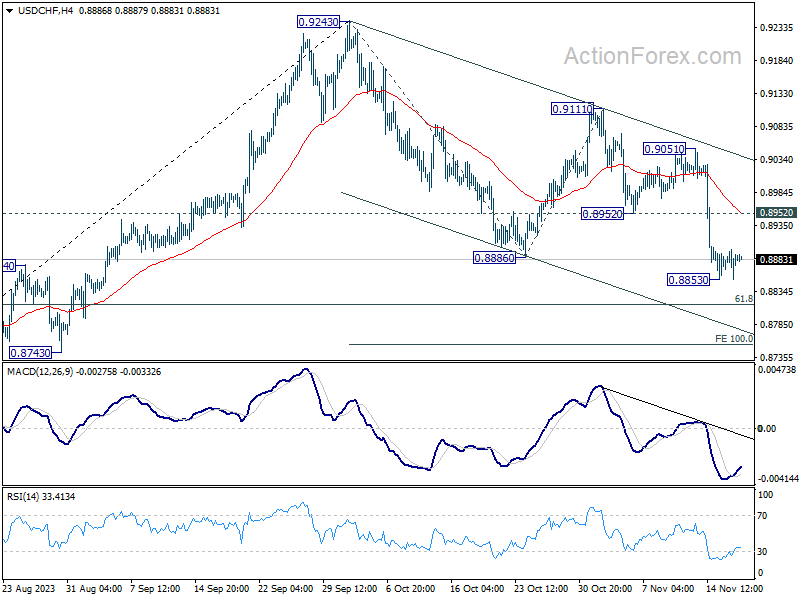

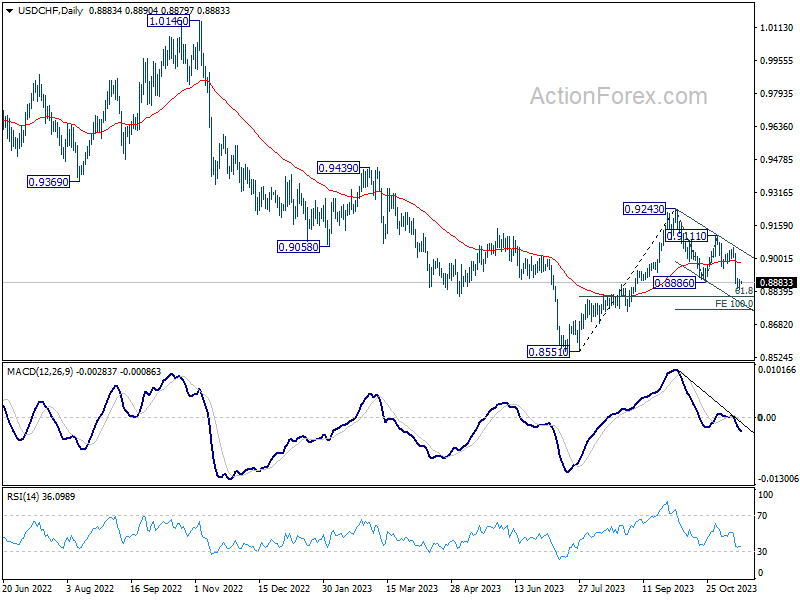

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8837; (P) 0.8933; (R1) 0.8988; More....

A temporary low is formed at 0.8853 and intraday bias in USD/CHF is turned neutral for consolidations. Stronger recovery cannot be ruled out. But upside should be limited by 0.8952 support turn resistance to bring another fall. Break of 0.8852 will resume the decline from 0.9243 to 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754.

In the bigger picture, price actions from 0.8551 are currently seen as a correction to the decline from 1.0146. Fall from 0.9243 is seen as the second leg for now. Deeper fall would be seen to 61.8% retracement of 0.8551 to 0.9243 at 0.8815. Sustained break there will bring retest of 0.8551 low. For now, this will remain the favored case as long as 0.9111 resistance holds.

Forex Markets in a Lull, Gold Extending Rally, Oil Tumbles

As the trading week draws to a close, the forex markets are experiencing a period of relative calm in today's Asian session. Key developments include Euro's attempted resurgence against Dollar overnight, which, despite initial signs of a rally, lost its momentum and settled back into familiar range. This pattern of indecisiveness is mirrored by Swiss Franc, which, after a period of gains against Dollar, is now in a similar phase of consolidation, aligning with other European majors. Commodity currencies displaying a softer stance overall. However, Australian Dollar stands out for its resilience.

For the week, Dollar remains the weakest performer overall. However, it's noteworthy that Dollar is managing to stay above the previous week's low against most currencies, except for Euro and Swiss Franc. This observation suggests that Dollar is still in the process of digesting its recent losses. Canadian Dollar and Japanese Yen follow as the next weakest, whereas Australian Dollar stands out as the strongest for the week. However, Aussie's position is somewhat precarious, as it hasn't surpassed last week's high against other rivals, indicating a lack of strong buying momentum. Euro and the British Pound are trailing as the next strongest, while Swiss Franc shows mixed performance.

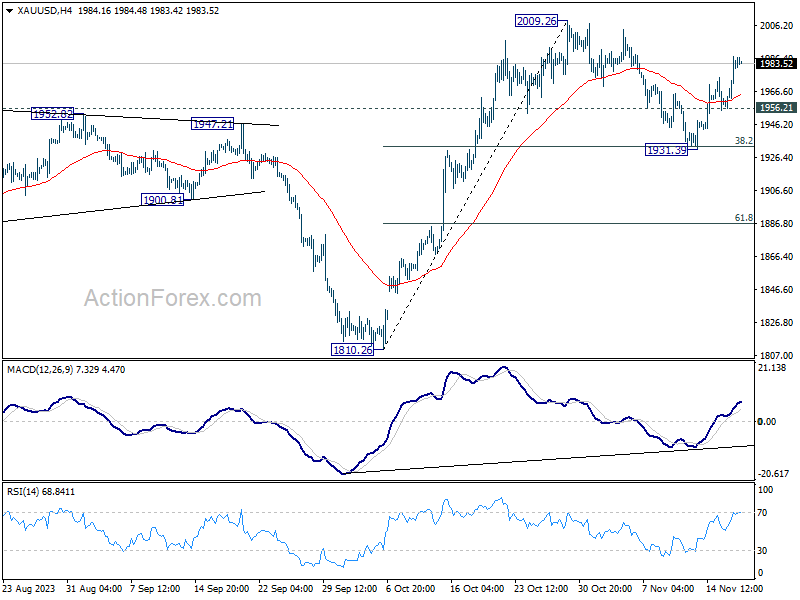

Technically, Gold's rally from 1931.39 is still in progress. Correction from 2009.26 should have completed after drawing support from 38.2% retracement of 1810.26 to 2009.26 at 1933.24. Further rise is expected as long as 1956.21 support holds. Retest of 2009.26 should be seen next. Firm break there will resume whole rally from 1810.26 to key resistance zone at 2062/74.

In Asia, Nikkei closed up 0.48%. Hong Kong HSI is down -1.98%. China Shanghai SSE is down -0.03%. Singapore Strait Times is down -0.39%. Japan 10-year JGB yield is down -0.030 at 0.761. Overnight, DOW dropped -0.13%. S&P 500 rose 0.12%. NASDAQ rose 0.07%. 10-year yield dropped -0.090 to 4.445.

Fed's Cook: Soft landing is possible but not assured

Fed Governor Lisa Cook addressed the delicate balance between sustaining economic growth and managing inflation in her conference remarks overnight. Cook acknowledged the possibility of achieving a "soft landing" for the US. economy, highlighting the ongoing disinflationary trends and robust labor market conditions. However, she was quick to note that such an outcome is not guaranteed.

"A 'soft landing' is possible, with continued disinflation and a strong labor market, but it is not assured," Cook stated. She elaborated on the complexities noting, "I see risks as two-sided, requiring us to balance the risk of not tightening enough against the risk of tightening too much."

She also pointed out the current economic resilience, saying, "The economy is still growing and consumers are still spending," which could potentially maintain demand-driven pressures in the market. Such momentum, according to Cook, could keep the economy and labor market tight, consequently slowing the disinflation process.

However, Cook also expressed concern over the potential negative impacts of aggressive policy measures, adding, "But I am also attuned to the risk of an unnecessarily sharp decline in economic activity and employment."

Mester's perspective from Fed's crow's nest: Disinflation progress made, yet more evidence needed

In a CNBC interview overnight, Cleveland Fed President Loretta Mester acknowledged, "We're making progress on inflation, discernible progress. We need to see more of that."

But she also highlighted the necessity of observing more concrete data to confirm that inflation is indeed on a timely path back to the desired level.

In her metaphorical reference to the "crow's nest", a vantage point on a ship used for spotting distant objects, Mester likened Fed's current position.

"We're at the crow's nest. What does the crow's nest let you do? It lets you look out on the horizon and see where the data is coming in, where the economy is evolving."

As for her personal stance on the direction of monetary policy, "I haven't assessed that yet. Where I think we are right now is we're basically in a very good spot for policy."

BoE's Ramsden signals extended period of restrictive monetary policy ahead

BoE's Deputy Governor Dave Ramsden emphasized the need for a prolonged phase of restrictive monetary policy to achieve the central bank's inflation target. Speaking on the future direction of the BoE's approach, Ramsden stated, "Monetary policy is likely to need to be restrictive for an extended period of time."

Ramsden further elaborated on the Monetary Policy Committee's stance, noting, "The MPC have communicated that monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term."

Additionally, Ramsden, who oversees BoE's quantitative tightening program, discussed the uncertainty surrounding the optimal size of the central bank's balance sheet. The ongoing assessment of the necessary reserves supply aims to meet both monetary policy objectives and ensure financial stability.

"We continue to work towards assessing what our future steady state reserves supply looks like, both to meet our monetary policy objectives through quantitative tightening, while ensuring our financial stability objective is also supported," he explained.

BoJ's Ueda reiterates patience in maintaining ultra-loose policy

BoJ Governor Kazuo Ueda has once again underscored the central bank's commitment to maintaining its ultra-loose monetary policy, emphasizing the need for patience in the face of uncertain inflation dynamics.

Speaking to the parliament, Ueda noted, "Trend inflation is likely to gradually accelerate toward our 2% inflation target through fiscal 2025. But this needs to be accompanied by a positive wage-inflation cycle."

"Uncertainty on whether Japan will see such a positive wage-inflation cycle is high," he added.

Addressing the behavior of 10-year JGB yields, Ueda expressed that he does not foresee a sharp rise above the 1% reference level, even under upward pressure.

Looking ahead, Ueda clarified the bank's position on potentially ending its Yield Curve Control and negative interest rate policies, stating, "We will consider ending YCC, negative rate if we can expect inflation to stably, and sustainably hit the price target."

He added that the order of adjustments to the policy would be contingent on various factors, including economic conditions, price movements, and market developments.

WTI crude oil nosedives to four-month low, more downside ahead

WTI crude oil experienced a significant tumble this week, dropping around -5% yesterday and reaching its lowest point in four months, marking a trajectory for its fourth consecutive week of decline. This marks the commodity's potential fourth consecutive week of decline.

Despite OPEC and IEA's predictions of supply tightness in Q4, a confluence of disappointing global economic data and a surge in US crude inventories, coupled with sustained record-level production, has fueled the sharp selloff.

From a technical analysis perspective, the bearish sentiment was cemented earlier this week when WTI failed to reclaim psychological level. The ongoing decline from 95.50 is now expected to continue to 161.8% projection of 95.50 to 81.77 from 91.07 at 68.85. However, we anticipate significant support emerging in 63.67/66.94 support zone, which to trigger reversal.

Overall, WTI is seen as encapsulated in a long-term range-bound pattern, oscillating between the 63/64 and 95/96 zones.

Looking ahead

UK retail sales is the main highlight in European session, while Eurozone will release CPI final. Later in the day, Canada will release IPPI and RMPI. US will release building permits and housing starts.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8837; (P) 0.8933; (R1) 0.8988; More....

A temporary low is formed at 0.8853 and intraday bias in USD/CHF is turned neutral for consolidations. Stronger recovery cannot be ruled out. But upside should be limited by 0.8952 support turn resistance to bring another fall. Break of 0.8852 will resume the decline from 0.9243 to 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754.

In the bigger picture, price actions from 0.8551 are currently seen as a correction to the decline from 1.0146. Fall from 0.9243 is seen as the second leg for now. Deeper fall would be seen to 61.8% retracement of 0.8551 to 0.9243 at 0.8815. Sustained break there will bring retest of 0.8551 low. For now, this will remain the favored case as long as 0.9111 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | PPI Input Q/Q Q3 | 1.20% | 0.20% | -0.20% | |

| 21:45 | NZD | PPI Output Q/Q Q3 | 0.80% | 0.40% | 0.20% | |

| 07:00 | GBP | Retail Sales M/M Oct | 0.30% | -0.90% | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Sep | 20.3B | 27.7B | ||

| 10:00 | EUR | Eurozone CPI Y/Y Oct F | 2.90% | 2.90% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct F | 4.20% | 4.20% | ||

| 13:30 | CAD | Industrial Product Price M/M Oct | 0.20% | 0.40% | ||

| 13:30 | CAD | Raw Material Price Index Oct | -2.00% | 3.50% | ||

| 13:30 | USD | Building Permits Oct | 1.45M | 1.47M | ||

| 13:30 | USD | Housing Starts Oct | 1.36M | 1.36M |