Sample Category Title

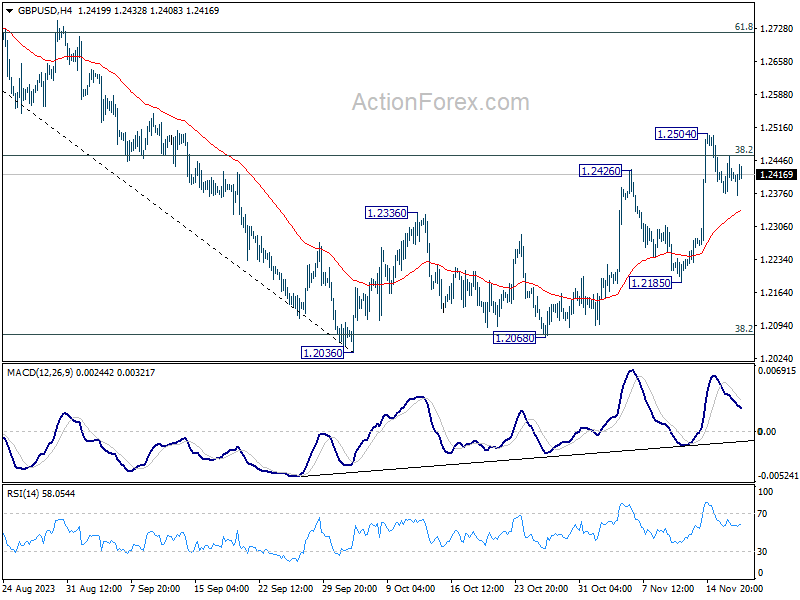

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2375; (P) 1.2416; (R1) 1.2454; More...

GBP/USD is still extending the consolidation from 1.2504 and intraday bias stays neutral at this point. Deeper retreat could be seen, but downside should be contained by 55 4H EMA (now at 1.2341) to bring another rally. On the upside, break of 1.2504 will resume the whole rebound from 1.2036. Sustained trading above 38.2% retracement of 1.3141 to 1.2036 at 1.2458 will pave the way to 61.8% retracement at 1.2716.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 will argue that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

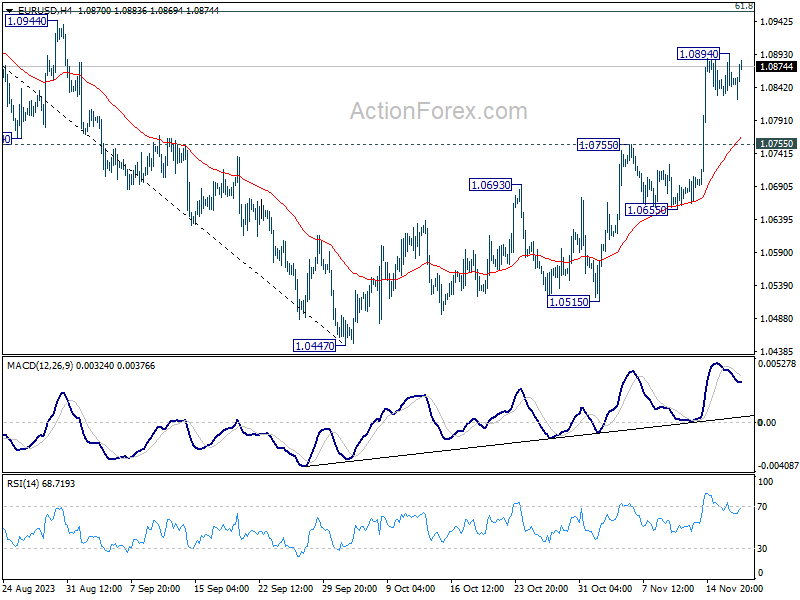

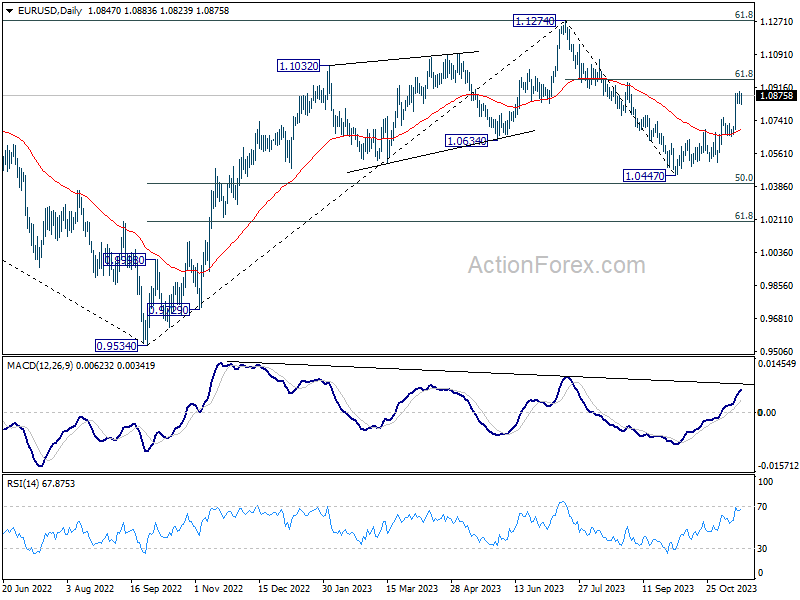

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0823; (P) 1.0860; (R1) 1.0889; More...

Intraday bias in EUR/USD stays neutral at this point, as consolidation continues below 1.0984. In case of deeper retreat, downside should be contained by 1.0755 resistance turned support to bring another rally. On the upside, above 1.0894 will resume the rebound from 1.0447 to 61.8% retracement of 1.1274 to 1.0447 at 1.0958 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. However, break of 1.0447 will resume the fall to 61.8% retracement of 0.9543 to 1.1274 at 1.0199.

Yen’s Sharp Rebound Amid Global Yield Dip: Central Bank Rate Cut Bets in Focus

Japanese Yen surged sharply in European session, bolstered by significant dips in Germany's 10-year government bond yield, which reached its lowest level since early September. Concurrently, US 10-year yield also briefly fell below 4.4% mark.

This movement in the bond markets reflects an aggressive stance by traders betting on rate cuts by major central banks in the upcoming year. Traders had been speculating about a full percentage point cut in interest rates by both ECB and Fed by the end of 2024. However, as the market regained its composure and yields recovered, Yen's rally also lost some of its initial momentum.

Despite the market's anticipatory stance, it seems premature to heavily bet on rate cuts just yet. Central bankers are still leaving the door open for further rate hikes. For instance, Bundesbank President Joachim Nagel stated today, "Are we there yet? Have we seen the peak in interest rates? That is not clear yet." Similarly, ECB Governing Council member Robert Holzmann suggested that it might be "somewhat early" for a rate cut in the second quarter .

In the broader forex markets, most major pairs and crosses are trading within the ranges set yesterday. Dollar is showing some softness alongside Sterling and New Zealand Dollar. Australian Dollar and Canadian Dollar are faring better, though Yen currently overshadows them.

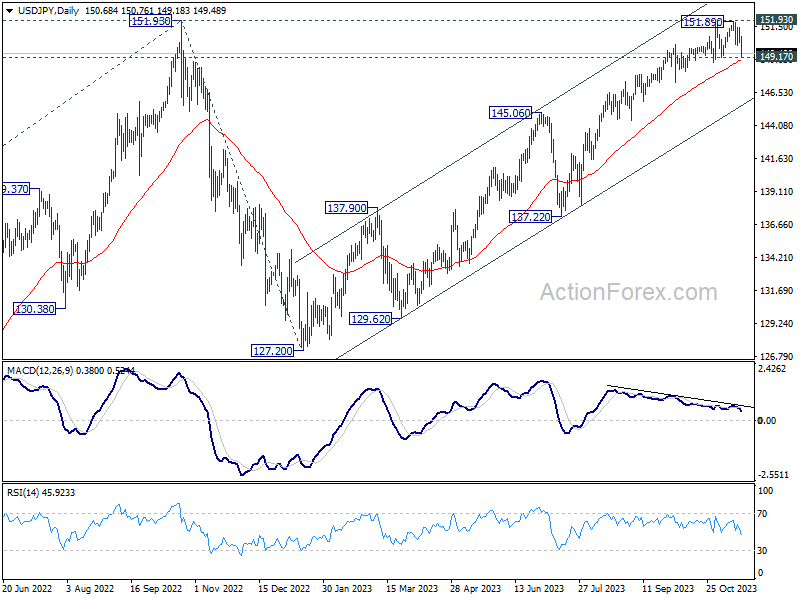

From a technical standpoint, USD/JPY is now pressing 149.17 support with today's steep fall. Firm break there should confirm rejection by 151.93 key resistance, and bring deeper decline towards medium term channel support (now at around 145.71). As the week draws to a close, it remains to be seen whether Yen can achieve this significant breakthrough.

In Europe, at the time of writing, FTSE is up 1.00%. DAX is up 0.86%. CAC is up 0.92%. Germany 10-year yield is down -0.015 at 2.583. Earlier in Asia, Nikkei rose 0.48%. Hong Kong HSI dropped -2.12%. China Shanghai SSE rose 0.11%. Singapore Strait Times dropped -0.27%. Japan 10-year JGB yield dropped -0.043 to 0.748.

Eurozone CPI finalized at 2.9% yoy in Oct, core at 4.2% yoy

Eurozone CPI was finalized at 2.9% yoy in October, down from September's 4.3% yoy. CPI core (excluding energy, food, alcohol & tobacco) was finalized at 4.2% yoy, down from previous reading of 4.5% yoy. The highest contribution came from services (+1.97%), followed by food, alcohol & tobacco (+1.48%), non-energy industrial goods (+0.90%) and energy (-1.45%).

EU CPI was finalized at 3.6% yoy, down from prior month's 4.9% yoy. The lowest annual rates were registered in Belgium (-1.7%), the Netherlands (-1.0%) and Denmark (-0.4%). The highest annual rates were recorded in Hungary (9.6%), Czechia (9.5%) and Romania (8.3%). Compared with September, annual inflation fell in twenty-two Member States and rose in five.

UK retail sales volume down -0.3% mom in Sep, sales value down up 0.1% mom

UK retail sales volume fell -0.3% mom in September, much worse than expectation of 0.3 mom rise. Ex-automotive fuel sales volume fell -0.1% mom. Looking broader, sales volumes (include and excluding fuel) fell by -1.1% in the three months to October 2023 when compared with the previous three months.

In value term, retail sales rose 0.1% mom while ex-fuel sales was flat 0.0% mom.

BoJ's Ueda reiterates patience in maintaining ultra-loose policy

BoJ Governor Kazuo Ueda has once again underscored the central bank's commitment to maintaining its ultra-loose monetary policy, emphasizing the need for patience in the face of uncertain inflation dynamics.

Speaking to the parliament, Ueda noted, "Trend inflation is likely to gradually accelerate toward our 2% inflation target through fiscal 2025. But this needs to be accompanied by a positive wage-inflation cycle."

"Uncertainty on whether Japan will see such a positive wage-inflation cycle is high," he added.

Addressing the behavior of 10-year JGB yields, Ueda expressed that he does not foresee a sharp rise above the 1% reference level, even under upward pressure.

Looking ahead, Ueda clarified the bank's position on potentially ending its Yield Curve Control and negative interest rate policies, stating, "We will consider ending YCC, negative rate if we can expect inflation to stably, and sustainably hit the price target."

He added that the order of adjustments to the policy would be contingent on various factors, including economic conditions, price movements, and market developments.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0823; (P) 1.0860; (R1) 1.0889; More...

Intraday bias in EUR/USD stays neutral at this point, as consolidation continues below 1.0984. In case of deeper retreat, downside should be contained by 1.0755 resistance turned support to bring another rally. On the upside, above 1.0894 will resume the rebound from 1.0447 to 61.8% retracement of 1.1274 to 1.0447 at 1.0958 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. However, break of 1.0447 will resume the fall to 61.8% retracement of 0.9543 to 1.1274 at 1.0199.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | PPI Input Q/Q Q3 | 1.20% | 0.20% | -0.20% | |

| 21:45 | NZD | PPI Output Q/Q Q3 | 0.80% | 0.40% | 0.20% | |

| 07:00 | GBP | Retail Sales M/M Oct | -0.30% | 0.30% | -0.90% | -1.10% |

| 09:00 | EUR | Eurozone Current Account (EUR) Sep | 31.2B | 20.3B | 27.7B | 30.8B |

| 10:00 | EUR | Eurozone CPI Y/Y Oct F | 2.90% | 2.90% | 2.90% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct F | 4.20% | 4.20% | 4.20% | |

| 13:30 | CAD | Industrial Product Price M/M Oct | -1.00% | 0.20% | 0.40% | |

| 13:30 | CAD | Raw Material Price Index Oct | -2.50% | -2.00% | 3.50% | 3.90% |

| 13:30 | USD | Building Permits Oct | 1.49M | 1.45M | 1.47M | |

| 13:30 | USD | Housing Starts Oct | 1.37M | 1.36M | 1.36M |

Euro Drifting as Eurozone Inflation Falls to 2.9%

- Eurozone inflation confirmed at 2.9%

The euro is trading quietly on Friday. In the European session, EUR/USD is trading at 1.0870, up 0.17%. The US dollar sustained sharp losses after a soft inflation report on Tuesday, and the euro took advantage with a massive gain of 1.68% the same day. Since then, the euro has been relatively calm.

Eurozone inflation confirmed at 2.9%

Eurozone inflation came in at 2.9% y/y in October, confirming the initial report. This was down sharply from 4.3% in September and matched the consensus estimate. The print was the lowest since July 2021 and was driven by a decline in energy and food prices. Monthly, inflation eased to 0.1%, down from 0.3% in September and matching the consensus estimate. The core rate, which remains well above the headline figure, showed a modest decrease, dropping from 4.5% to 4.2%, matching the consensus estimate.

The ECB held rates at 4.0% in October after 10 successive rate hikes and with inflation continuing to fall, expectations are that the central bank will prolong its hold on rates, barring an unexpected upswing in inflation. The economic picture is not pretty, as the eurozone economy is stagnating and Germany, once a global powerhouse, has become a deadweight on the eurozone with its weak economy. Lagarde said last week that the ECB will not be trimming rates in the “next couple of quarters” while acknowledging that “inflation has come down massively” and hinting that rates may have peaked.

In the US, there were further signs this week that the economy is losing steam. Inflation was lower than expected at 3.2% and retail sales surprised to the downside with a 0.1% decline. As well, unemployment claims hit a three-month high at 231,000. US Treasury yields fell on Thursday to 4.45%, down from 4.53%, as speculation continues to rise that the Fed has ended or is very close to ending the current rate-tightening cycle. The markets widely expect a pause at the final rate meeting of the year in December and have priced in a rate cut as early as May 2024.

EUR/USD Technical

- There is resistance at 1.0926 and close by at 1.0943

- EUR/USD tested support at 1.0842 earlier. Below, there is support at 1.0799

Australian Dollar Takes a Breather After Wild Week

- Markets see 60% chance of RBA rate hike in H1 of 2024

- US Treasury yields fall to 4.35%

The Australian dollar has bounced back on Friday after losses a day earlier. In the European session, AUD/USD is trading at 0.6487, up 0.24%.

It has been a wild week for the Australian dollar, which soared 2% on Tuesday, courtesy of a softer-than-expected US inflation print. The Aussie climbed as high as 0.6525 on Wednesday, its highest level since August 10th and has climbed 1.9% this week.

Is the RBA done with tightening?

The Reserve Bank of Australia has been aggressive with its rate hikes, bringing the cash rate to 4.35%. The RBA hiked by a quarter-point earlier this month but is widely expected to pause at the December meeting. Thursday’s employment report was much stronger than expected, with a gain of 55,000 jobs compared to the market consensus of 20,000. The release didn’t have much effect on the RBA rate odds, as the lion’s share of the increase in jobs were part-time positions.

As for 2024, investors aren’t sure what to expect from the RBA after December. The markets have priced in about a 60% chance of a quarter-point hike in the first half of 2024, and key releases such as inflation and employment will play major factors in the RBA’s upcoming rate decisions. Goldman Sachs is more dovish, as it projection that inflation to fall below 3% in late 2024 and isn’t expecting any further rate hikes.

In the US, there were further signs this week that the economy is slowly cooling. Inflation was lower than expected at 3.2% and retail sales surprised to the downside with a 0.1% decline. As well, unemployment claims hit a three-month high at 231,000. US Treasury yields fell on Thursday to 4.45%, down from 4.53%, as speculation continues to rise that the Fed has ended or is very close to ending the current rate-tightening cycle.

AUD/USD Technical

- AUD/USD is testing resistance at 0.6476. Above, there is resistance at 0.6526

- 0.6408 and 0.6351 are providing support

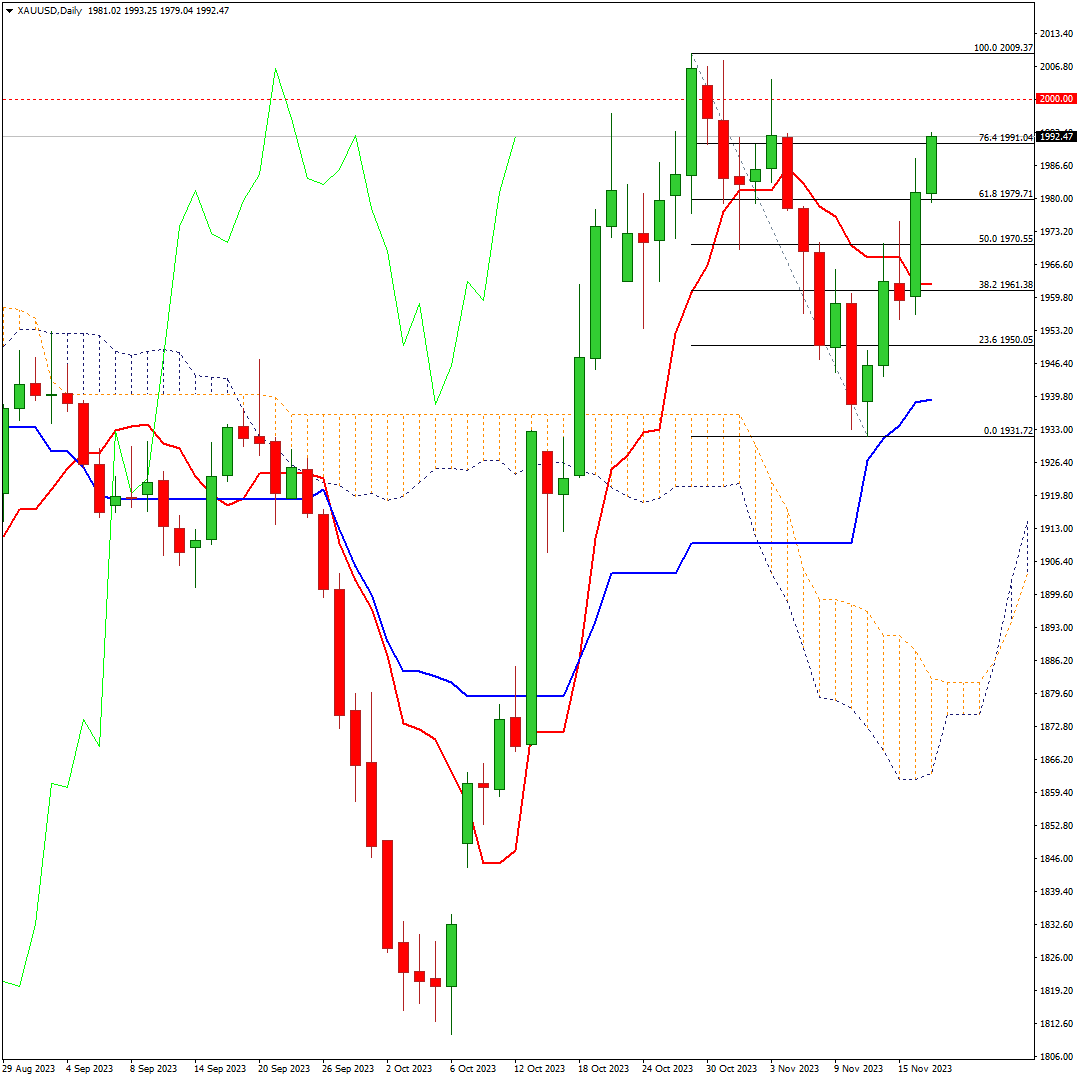

XAU/USD: Gold Extends Recovery Towards $2000 Barrier

Gold rose to ten-day high on Friday and almost fully retraced last week’s 2.7% drop, driven by growing demand on hopes that the Fed’s tightening cycle is close to its end.

Fresh extension on Friday cracked Fibo barrier at $1991 (76.4% of $2009/$1931), confirming bullish signal generated on close above 20DMA ($1974) and signaling that corrective phase from $2009 (Oct 27 peak) is likely over.

Bulls eye psychological $2000 barrier, where increased headwinds could be expected as daily studies are overbought, with limited dips to ideally find firm ground above $1980 zone (broken Dibo 61.8%) and offer better levels to re-enter bullish market for another probe through $2000.

Only return and close below 20DMA would weaken near-term structure and signal recovery stall.

Res: 2000; 2004; 2009; 2021.

Sup: 1987; 1979; 1974; 1970.

Can JPY Reach New Lows By the End of 2023?

Speculation persists regarding the Bank of Japan's potential departure from negative interest rates, yet the USD/JPY maintains its position within a 150–152 range for seven consecutive sessions. Caution is warranted due to a weaker-than-expected Q3 GDP, a slump in imports, and a more moderate increase in exports, despite inflation remaining elevated. While other central banks approach the conclusion of their rate hike cycles, signals indicate the likelihood of impending Yen strength. BoJ Governor Kazuo Ueda suggests a forthcoming decisive policy move, eliminating the necessity for wage growth to tighten policy. Deputy Gov. Shinichi Uchida explores plans to encourage firms to increase wages, potentially providing forward guidance to break the yen from its current range.

USDJPY - D1 Timeframe

USDJPY on the Daily timeframe is currently trading within a channel right inside a weekly-timeframe supply zone. Even though the clear conclusion should be a bearish sentiment, I would consider this a two-way possibility until the break and retest of the trendline support, since it overlaps the 50-day moving average. My target, in the case of a breakout, would be the 100-day moving average support.

Analyst’s Expectations:

- Direction: Bearish

- Target: 146.600

- Invalidation: 152.039

AUDJPY - D1 Timeframe

AUDJPY on the daily timeframe has already been rejected from the supply zone, giving a clear indication of what the direction is expected to be - bearish! With this in mind, my target would be the demand zone as marked, since it aligns perfectly with the trendline support.

Analyst’s Expectations:

- Direction: Bearish

- Target: 96.211

- Invalidation: 97.780

CADJPY - D1 Timeframe

CADJPY is, in my opinion, a no-brainer. On the chart, we can clearly see the supply zone price is currently being rejected from, as well as the demand zone price is likely heading towards. This makes it quite easy to decipher the market sentiment as being bearish.

Analyst’s Expectations:

- Direction: Bearish

- Target: 108.469

- Invalidation: 109.672

CONCLUSION

The trading of CFDs comes at a risk. To succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

GBPJPY Recedes from New Highs

- GBPJPY starts a new brief bearish cycle after fresh highs

- Support at 185.60, but sellers need to drive deeper to change outlook

GBPJPY switched into corrective mode, erasing half of its weekly wins after almost approaching the November 15, 2015 peak of 188.80.

The doji candlestick, along with the negative reversals in the RSI and stochastic oscillator, indicate that the bears have an advantage in the short term.

A close below 185.60, where the 23.6% Fibonacci retracement of the latest upleg is placed, could extend the decline straight to the 20-day simple moving average (SMA) at 184.40. Then, the 181.95-183.15 trendline region, which encapsulates the 50-day SMA, might bring some stability before a potential downfall squeezes the price into the important 178.00-179.60 territory. A step lower from there would violate the broad positive trend, motivating more selling towards the 200-day SMA at 176.00.

In the opposite scenario, where the pair revives its uptrend above the key bar of 188.80, immediate resistance is expected to develop between the short-term ascending line from March 2023 and the long-term ascending line from October 2022, both seen within the 191.50-192.45 territory. A successful penetration higher might clear the way towards the 2015 ceiling of 195.30-195.87.

To sum up, the current pullback in GBPJPY could gain extra legs in the coming sessions, though any declines might not be worrisome and could be considered part of the broad uptrend unless the pair tumbles below 178.00.

GBP/USD Edges Lower on Soft UK Retail Sales

- UK retail sales decline unexpectedly

- GBP/USD edges lower

The British pound is trading lower on Friday. In the European session, GBP/USD is trading at 1.2381, down 0.27%.

The pound has shown sharp swings this week, notably a 1.78% jump on Tuesday after US inflation was weaker than expected, sending the US dollar sharply lower against the majors. The pound is up 1.28% this week.

UK retail sales decline

UK retail sales were expected to bounce back in October, after a revised decline of 1.1% m/m in September. Instead, retail sales declined by 0.3% m/m, missing the market consensus of 0.3%. This was the third decline in four months. Fuel sales were down and consumers are being more cautious in their spending. The wet weather has also dampened consumer spending.

On a yearly basis, retail sales slid by 2.7%, down from a revised 1.3% and much weaker than the market consensus of -1.5%. This marked a 19th straight decline, pointing to a dismal picture of consumer spending which could result in a contraction in fourth-quarter GDP.

Consumer confidence remains deeply pessimistic, as high interest rates and high inflation continue to batter consumers. Inflation has fallen to a two-year low of 4.6%, but consumers continue to see higher and higher prices, which has put a damper on consumer spending.

In the US, the latest economic data points to a gradual slowdown, as seen in this week’s inflation and retail sales prints. Thursday’s unemployment claims were further evidence of this trend, with claims rising to a three-month high at 231,000. US Treasury yields fell on Thursday to 4.45%, down from 4.53%, as speculation continues to rise that the Fed has ended or is very close to ending the current rate-tightening cycle. There are hopes for a soft landing for the US economy, as inflation is falling while growth remains strong, which is the so-called Goldilocks scenario.

GBP/USD Technical

- GBP/USD is putting pressure on support at 1.2374. Below, there is support at 1.2312

- 1.2476 and 1.2522 are the next resistance lines

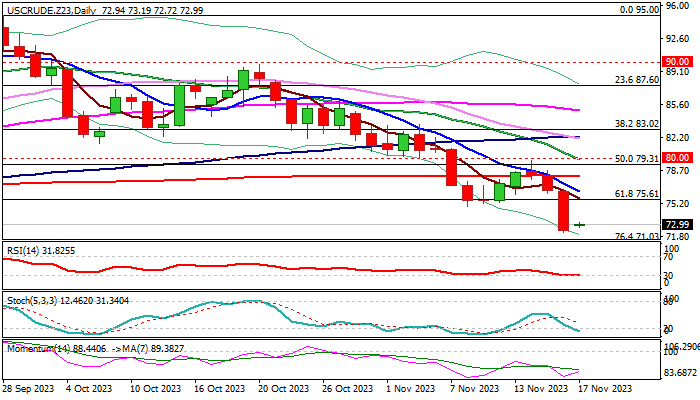

WTI Oil: Consolidation After 5.3% Fall on Thursday Likely to Precede Fresh Push Lower

WTI oil is holding within a narrow consolidation in early Friday after falling 5.3% previous day (the biggest one-day drop since Oct 4), being under increased pressure from growing demand concerns and strong supply.

Short-term price action is holding in a downward trajectory and on track for the fourth consecutive week of losses, since fears of output disruption in the Middle East faded, while demand is weaker and supply grows above expectations, which resulted in strong rise in US crude inventories.

The latest acceleration pushed the price to the lowest in over four months and below the base of thick weekly Ichimoku cloud.

Close below weekly cloud to add to bearish signals and open way towards targets at $71.03 and $70.00 (Fibo 76.4% of $63.63/$95.00 / psychological).

Meanwhile, bears are likely to pause for consolidation as daily studies are oversold and partial profit-taking at the end of the week may keep bears on hold.

Former low of Nov 11 ($74.92) and broken Fibo 61.8% ($75.61) reverted to solid resistances which should ideally cap upticks to keep bears intact and offer better selling opportunities.

Caution on lift above falling 10DMA ($76.51) which would increase risk of attack at upper pivot at $78.08 (200DMA).

Res: 74.47; 74.92; 75.61; 76.51.

Sup: 72.16; 71.73; 71.03; 70.00.