Sample Category Title

Canadian CPI Data in Center Stage in the Week Ahead

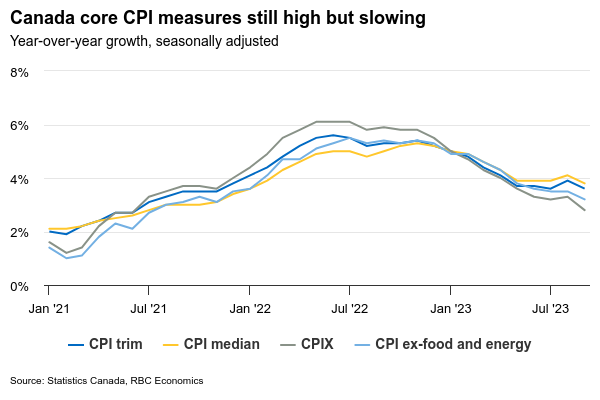

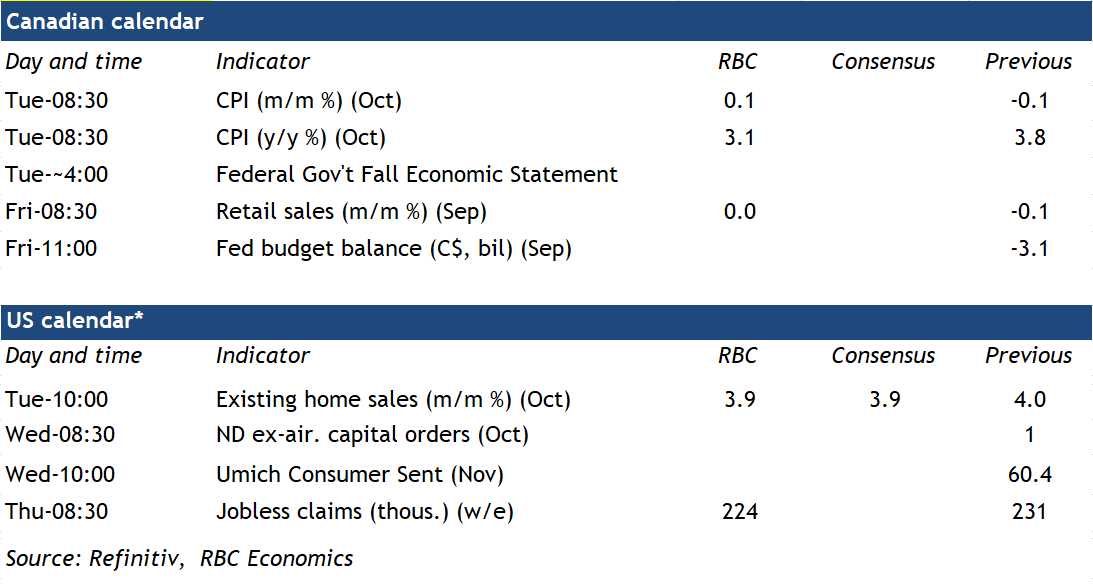

Canadian CPI data will be watched closely (including by Bank of Canada officials) in a week that will also include the federal government’s fall economic update and (we expect) more signs that the consumer spending backdrop is softening. Year-over-year CPI growth is expected to slow significantly to 3.1% in October (just above the top end of the BoC’s 1% to 3% inflation target range) from 3.8% in September. A drop in gasoline prices pushed energy costs lower and the lagged impact of easing supply chains and lower food commodity prices continue to slow grocery store price growth.

There is not much that the Bank of Canada can do to impact global commodity prices, and price growth excluding food and energy products is expected to be ‘stickier’, edging up to 3.3% year-over-year from 3.2% in September. Much of that growth is still coming from surging mortgage interest costs that are a direct result of Bank of Canada interest rate increases. Price growth excluding those costs has been slower – the so-called CPIX core measure that also excludes mortgage interest costs along with 7 other volatile price subcomponents has slowed to 2.8% year-over-year after hitting a peak of 6.1% in June 2022. Growth in the BoC’s current preferred median and trim core CPI components have still been running well above the 2% inflation objective but are expected to edge lower on both a year-over-year and 3-month rolling average basis in October.

Inflation pressures going forward are increasingly likely to slow with economic growth and labour markets looking softer. The advance estimate of September retail sales was unchanged from August, which would leave sales in volume terms down ~2 ½% at an annualized rate in Q3. And our own tracking of card transactions is also showing a slowdown in spending on discretionary services (alongside softer retail sales) into October.

Week ahead data watch

The federal government’s fall federal budget update will come alongside a slowing growth backdrop. Housing supply is expected to be a focus of the update with high rates of population growth stretching capacity. But a slower economic growth backdrop is also weighing on government purchasing power with the Parliamentary Budget Office estimating that the deficit for the current fiscal year will come in $6 billion wider than expected in in the last budget.

Has Dollar Rally Run Its Course?

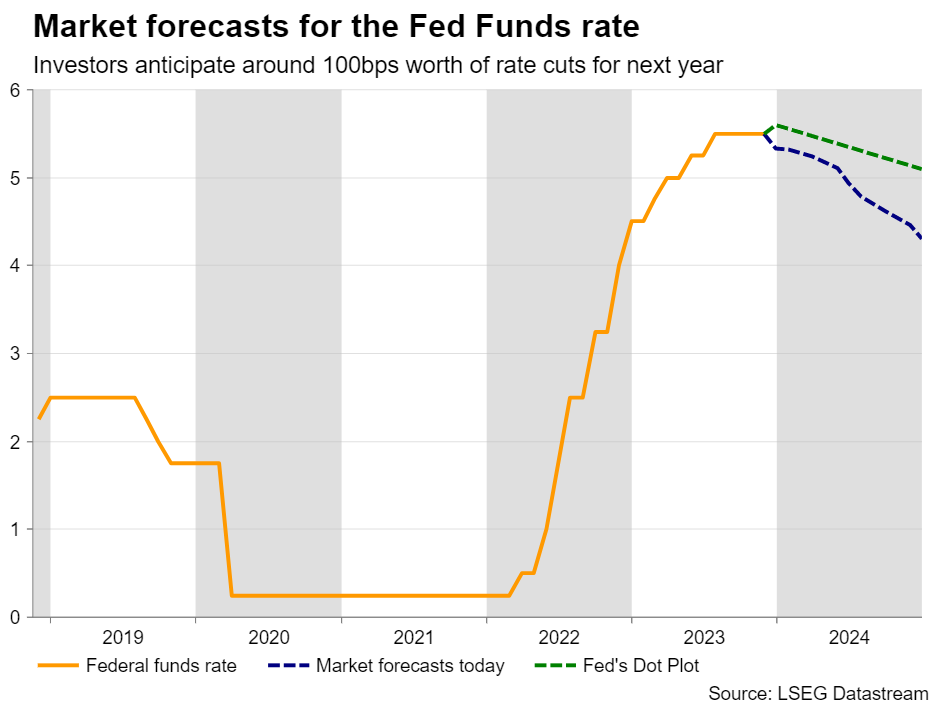

- Dollar slides as investors pencil in 100bps worth of Fed rate cuts

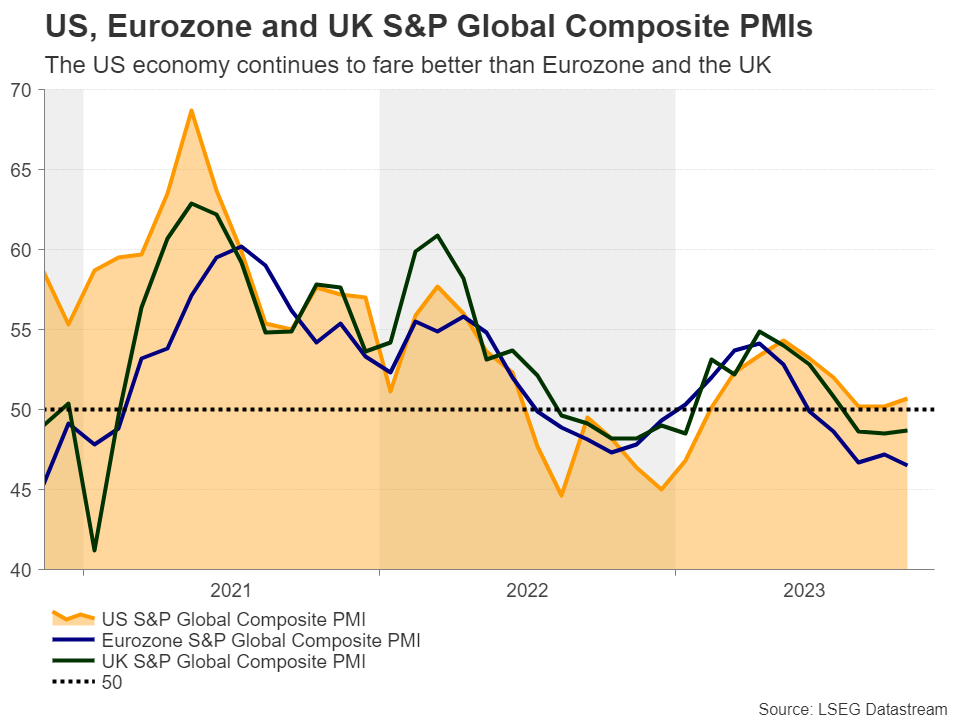

- US economy is expected to slow, but still fare better than its major peers

- Fed likely to begin rate reductions next year, but ECB may cut earlier

- Aussie the most likely candidate to outperform the greenback

Jobs and inflation data hurt the dollar

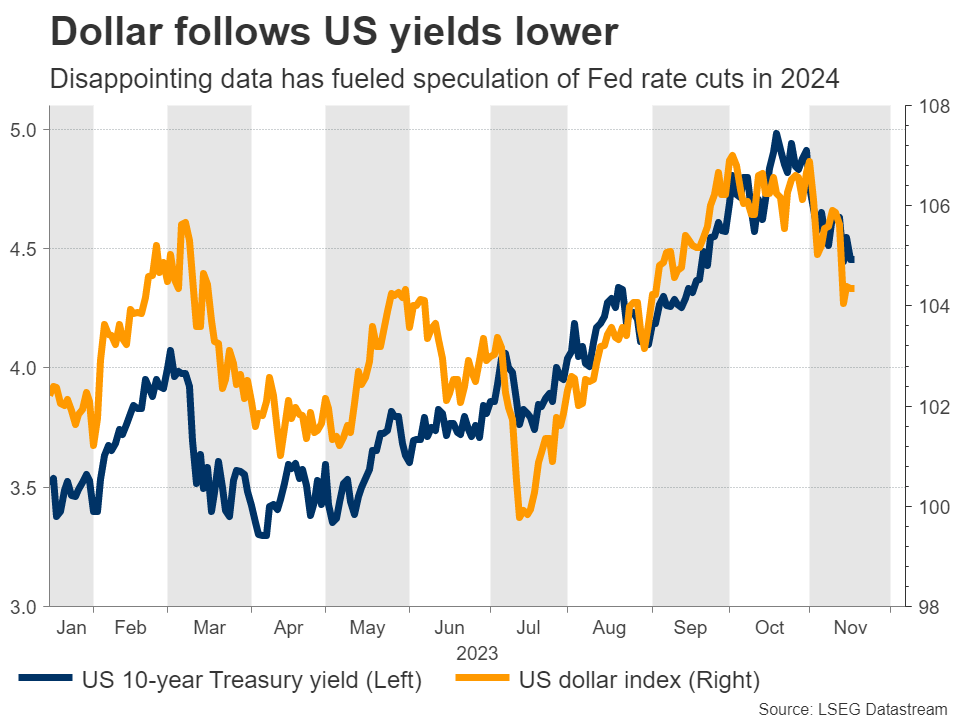

The US dollar suffered a major blow this week after the US CPI data revealed that inflation cooled by more than anticipated in October, adding credence to investors’ view that the end credits of the Fed’s tightening crusade have already rolled, despite Chair Powell and several of his colleagues pushing back against such expectations recently.

This was the second hit in less than two weeks for the US dollar, with the first one coming after the disappointing jobs report for the same month. Bearing in mind that the Fed is linking its monetary policy decisions to both inflation and the labor market, easing conditions on both fronts prompted market participants to price out any chance for another hike this year and to pencil in around 100bps worth of rate reductions for next year.

Fed to cut in 2024; but by how much?

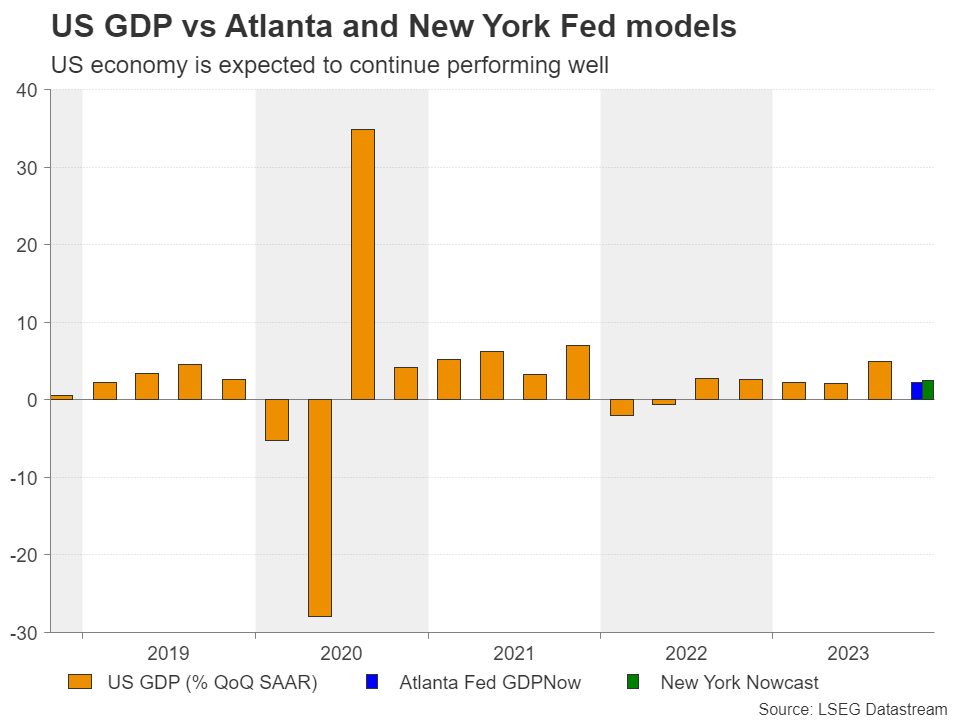

Nonetheless, there is no evidence yet supporting so many basis points worth of cuts for next year. Yes, the US economy is expected to have slowed in Q4, with the Atlanta Fed GDPNow and the New York Fed Nowcast models projecting growth rates of 2.2% and 2.5% respectively, but with interest rates at such high levels and the economy growing at the astounding pace of 4.9% in Q3, such a slowdown appears quite normal.

On the other hand, the Fed could start cutting rates and monetary policy would still stay tight, pushing inflation in the right direction. So, should data continue to suggest that inflation is drifting south faster than anticipated, then the Fed may be tempted to start cutting sooner than it currently anticipates, in order to avoid a more severe than forecast economic slowdown.

According to its September dot plot, the Committee is projecting one more hike and expects interest rates to end 2024 within the 5.00-5.25% range. In other words, it anticipates only 50bps worth cuts for next year, which is a decent deviation from what the market is currently pricing in. Therefore, the big question moving forward is: Who is right? The market or the Fed?

US economy seen slowing, but 100bps cuts not justified

The Fed’s own economic forecasts suggest that the economy could slow to 1.5% growth in 2024 and then reaccelerate to 1.8% in 2025, with inflation easing to 2.2% by the end of 2025 and hitting the 2% objective in 2025. Indeed, such projections do not justify 100bps worth of rate cuts and should incoming data continue to point to a US economy that is faring better than its major peers, investors may be eventually convinced to lift their implied path. Even if new rate hike bets do not resurface, market participants could scale back a decent amount of basis points worth of cuts, which could prove positive for long-dated Treasury yields, and thereby help the dollar rebound.

Although traders currently appear willing to sell the dollar more aggressively on anything confirming the ‘no more hikes’ narrative than on anything corroborating the Fed’s ‘higher for longer’ mantra, there is nothing suggesting that a bearish reversal is imminent. The Eurozone seems to be headed for its own recession, which could eventually prompt the ECB to start cutting its own rates before the Fed does. The UK economy is also in a bad shape and following the larger-than-expected slowdown in UK inflation during October and disappointing growth-related data, investors may be tempted to continue bringing forward their BoE cut bets. This could happen despite Governor Bailey arguing that it is too early to be thinking about rate cuts. Such thinking by investors is likely to leave the euro and the pound in a vulnerable position for a while longer.

Dollar could struggle against aussie, kiwi, and yen

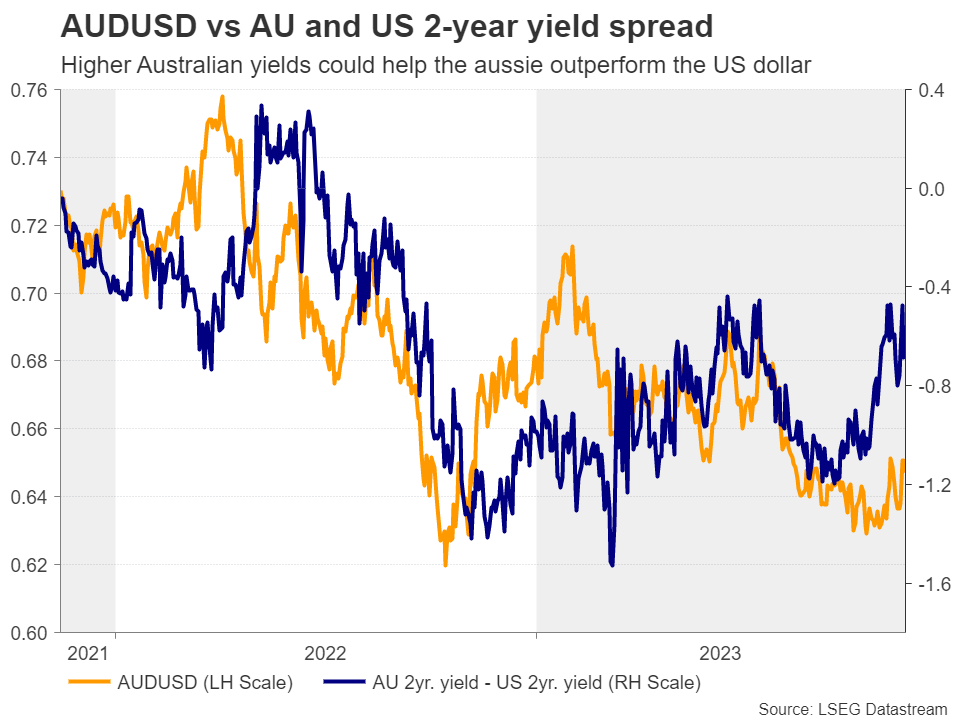

Currencies that have more chances in outperforming the dollar may be the risk-linked aussie and kiwi, as expectations of several rate cuts by the Fed have already been translated to increasing risk appetite, as made evident by the latest rally in Wall Street. What’s more, with investors not even pricing in a full 25bps cut by the RBA in 2024, the aussie could perform even better. That said, this may be a story for next year, when the Fed begins to cut rates and the slide in short-dated Treasury yields accelerates. The yen could also perform better than it did this year if the BoJ abandons its yield curve control (YCC) policy, although improving risk appetite is usually not a plus for this currency.

Week Ahead – Fed Minutes and Eurozone PMIs on the Menu

- Fed minutes on Tuesday will be scrutinized for clues on rate path

- Eurozone business surveys to shed some light on recession risks

- Japanese inflation stats also in focus as yen attempts to recover

Bruised dollar awaits FOMC minutes

It’s been a tough month for the US dollar. A string of disappointing data releases coupled with an announcement that the Treasury will shift its debt issuance towards shorter-dated maturities came together to engineer a heavy decline in US bond yields, which in turn has reduced the dollar’s interest rate advantage.

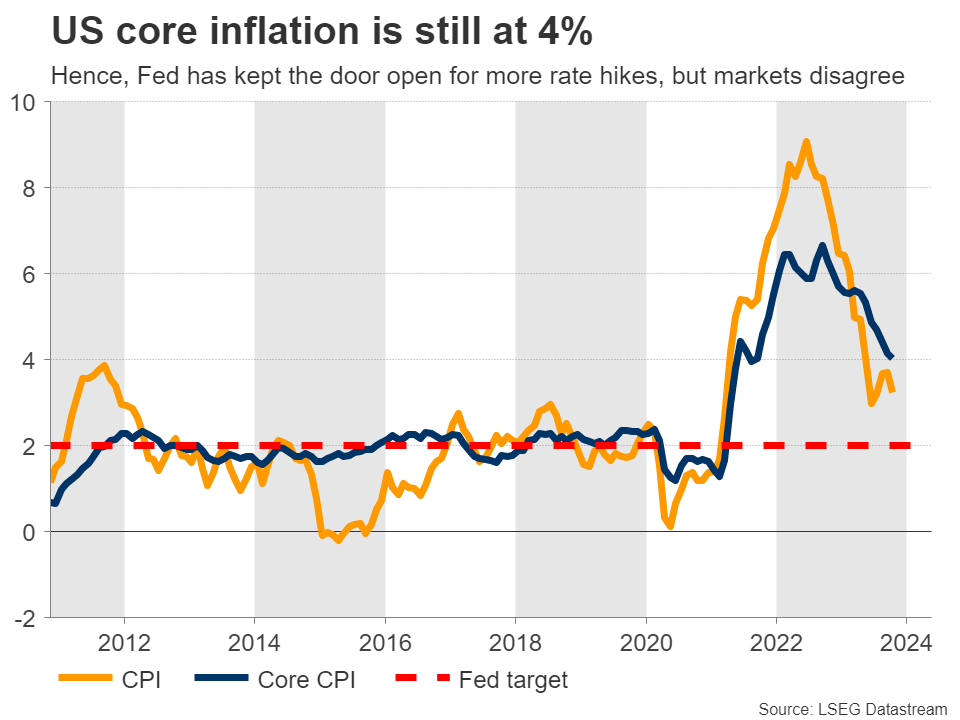

On the macro front, the labor market finally seems to be loosening. The unemployment rate has been grinding higher for several months now, providing some relief to Fed officials, as weaker employment conditions often translate into cooler inflation. Indeed, core inflation has declined steadily this year, but it remains elevated at 4%, so the Fed cannot declare victory yet.

With consumer spending also staying resilient, Fed officials have kept the prospect of another rate increase on the table. However, market pricing suggests the tightening cycle is already over and that the next move will be a rate cut, most likely in the second quarter of 2024. In light of this disparity, the upcoming FOMC meeting minutes could be crucial.

The minutes will be released on Tuesday, earlier than usual because Thursday is a public holiday in the United States. This was the meeting when the Fed kept rates unchanged and struck a neutral tone, highlighting that it is not certain whether rates are sufficiently high to bring inflation back under control.

Traders will dissect the minutes for any clues on the likelihood of further rate increases. However, even if the Fed provides such hints, it’s questionable whether markets will take them at face value, considering the series of disappointing data releases since this meeting. Hence, any upside reaction in the dollar from this release could be muted.

Beyond the minutes, there are several data releases on the agenda, including durable goods orders on Wednesday and the preliminary S&P Global PMIs for November on Friday.

All told, the question for FX traders heading into next year is which central banks will cut rates first and the deepest, since that will decide which currencies win or lose. That’s a setup that favors the dollar. The resilience of the US economy, especially when compared to Europe, suggests that the Fed might be among the last ones to launch an easing campaign.

Euro and sterling turn to PMI surveys

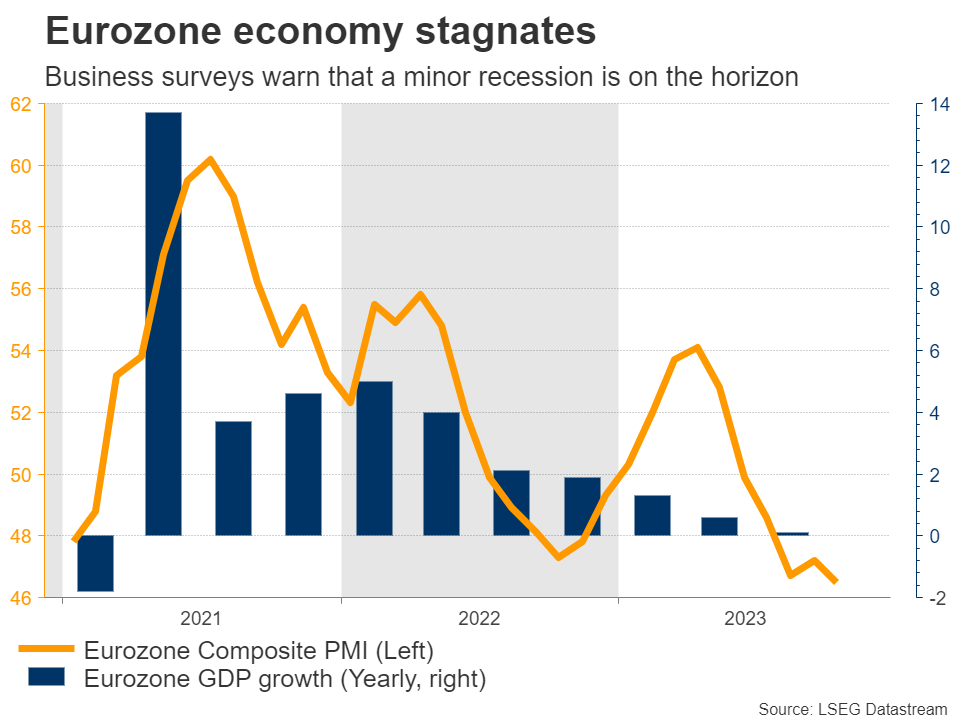

In the Eurozone and the United Kingdom, all eyes will fall on the latest round of business surveys on Thursday. Both economies are in similar shape, in the sense that economic growth has been stagnant for most of this year and might turn negative soon according to previous editions of these business surveys.

Europe seems to be entering a phase of stagflation, where the economy falls into a mild recession but inflationary pressures remain hot. That’s a nightmare scenario for any central bank, as cutting rates could refuel inflation but keeping them elevated could inflict more damage on the economy. This is particularly true in the UK, where core inflation is still running at 5.7%.

With all this in mind, the upcoming PMIs for November will provide an update on the health of these economies. Any further signs that the Eurozone and the UK are moving closer to a recession could dampen buying appetite in the euro and the pound, putting the brakes on the latest rebound.

Aside from the business surveys, the minutes of the latest European Central Bank meeting will also hit the markets on Thursday. This release is usually not a huge event for markets, but it could attract attention this time as traders attempt to decipher how quickly the ECB will start cutting rates. After that, the focus will turn to Germany’s Ifo survey on Friday.

Japanese inflation numbers coming up

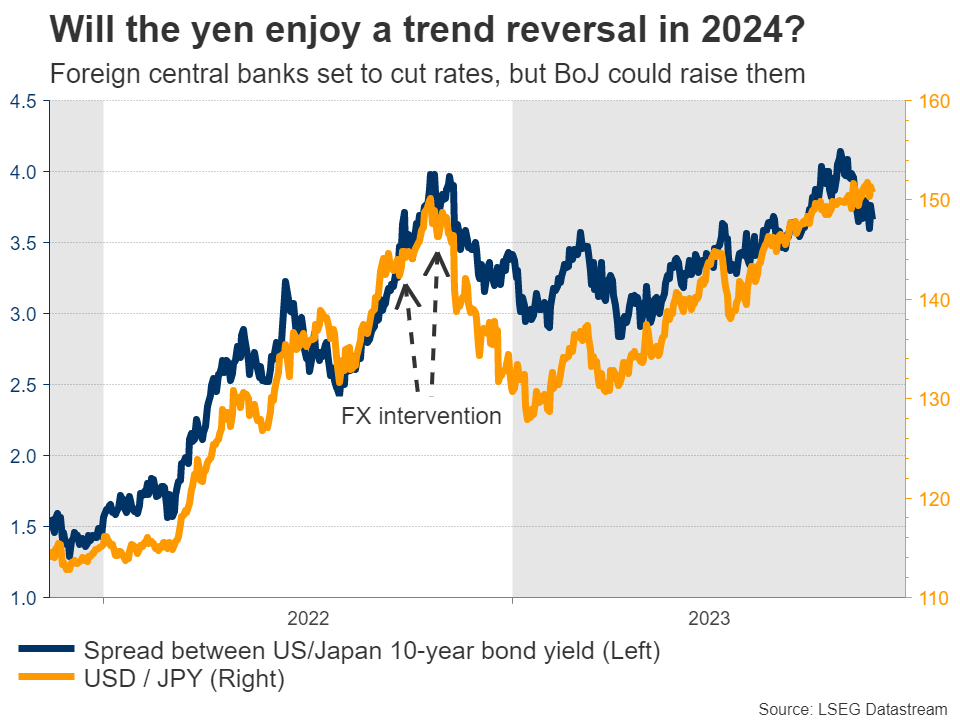

In the world’s third-largest economy, inflation stats for October will be released on Friday. The yen has been devastated this year, almost touching a three-decade low against the US dollar as interest rate differential widened against it.

Now, the question is whether the yen will get some relief next year, and perhaps even stage a trend reversal in an environment where foreign economies begin to cut interest rates while the Bank of Japan raises them. Market pricing suggests the BoJ will exit negative interest rates in the spring, helping to compress interest rate differentials.

Whether that happens or not will depend on the inflation outlook, which raises the importance of the upcoming data. Forecasts suggest that core inflation accelerated in October, something corroborated by a similar acceleration in Tokyo’s inflation that is considered a leading indicator of nationwide inflation. If this is the case, it could help the battered yen to recover some ground.

Meanwhile, inflation data will also be released in Canada on Tuesday, ahead of the latest edition of retail sales on Friday. Finally in Australia, the minutes of the latest RBA meeting are due out on Tuesday.

Weekly Focus – Inflation Pressures Easing But Too Early to Declare Victory

The big market mover this week was US CPI for October, which surprised to the downside with a rise in the core CPI inflation of 0.2% m/m versus a consensus estimate of 0.3% m/m. The number added to the picture that inflation pressures are easing. The October inflation print from the euro area showed a similar development earlier this month. However, it is still too early to declare victory over inflation. While goods price inflation has come down a lot, service price inflation is still too high. Labour markets remain tight sustaining high wage growth. We need to see more cooling of the economies to get further cooling of the labour markets and service inflation under control. Some Fed members during the week did warn that it was too early to declare victory and said higher rates could still be needed. San Francisco Fed's Daly said the data pointed to a deceleration in inflation but cautioned against prematurely calling for a "time out" on further hikes.

In the US retail sales for October was stronger than expected and still points to quite resilient private consumption. Hence we have yet to see consumers give in to the higher interest rates. However, we continue to see a further cooling of the labour market and consumption to kick in over the coming quarters implying that the Fed is done for now and can start lowering rates in the first half of 2024. The market is also convinced the Fed is done following the lower inflation print and bond yields moved much lower during the week and the USD weakened further. Stocks rallied on the positive signs of a soft landing.

In the euro area, it was a fairly quiet week. The German ZEW showed a rebound in November from -1.1 to 9.8. It tends to give a good signal on the Ifo business survey, which we get in the coming week. ECB's Kazak said it was premature to say we have reached the terminal rate and said there was no clear peak in wage growth yet. ECB's Guindos said he wouldn't prejudge further rate movements and future decisions will be data dependent. However, Centeno delivered more dovish comments saying inflation retreated faster than it went up and that real rates continue to rise as inflation comes down.

A decline in oil prices is providing additional help with easing inflation pressures. Brent oil dropped further this week below USD80 per barrel on concerns over weak demand and it is back to the levels seen in the summer months after hitting USD96 in late September. If the sell-off continues, we will likely see further supply cuts by OPEC and US resuming buying of oil for its strategic reserves. Both factors would help floor oil prices.

Turning to Asia, Japan's GDP growth for Q3 disappointed with a decline of 0.5% q/q (consensus -0.1% q/q). Chinese data for October showed positive surprises for retail sales and industrial production but housing remained a key concern with further declines in both house prices and home sales. On the geopolitical front leaders of the US and China, Joe Biden and Xi Jinping, met for the first time in a year. We see it as positive that the dialogue is back, which is key to managing the strained relationship and put up guard rails to avoid escalation into military conflict at some point. But the intense rivalry is likely to be with us in the years to come, see also our Geopolitical Radar released on Thursday.

Looking ahead to the coming week focus turns to Flash PMI's in the US and the euro area, German Ifo survey, Japan CPI and a Riksbank meeting in Sweden.

What To Expect from Gold In the upcoming week

Gold prices (XAU/USD) surged more than 1.0% on Thursday of this week, rebounding from a lackluster performance in the previous trading session. This upward momentum was driven by a notable retreat in U.S. Treasury yields, spurred by disappointing labor market data released earlier in the day. Key catalysts include higher-than-expected applications for unemployment benefits, recording 231,000 for the week ending November 11 against a forecast of 220,000. Continuing jobless claims also surpassed expectations, reaching 1,865,000, the highest in almost two years, indicating growing challenges in American employment. The combination of lackluster economic indicators and positive October CPI and PPI figures supports the perception that the Federal Reserve's tightening cycle is concluding, fostering expectations of future rate cuts, which has contributed to gold's upward trajectory amid a more dovish FOMC monetary policy outlook. But is this all there is to Gold? Read on to find out.

XAUUSD - W1 Timeframe

The weekly timeframe of XAUUSD shows price currently retesting a supply zone that is in very close proximity to the 76% of the Fibonacci zone. This on its own signifies that the upward rally has likely come to an end, and we may begin to see a reversal. We are not done yet though, so let’s see what the Daily timeframe indicates.

XAUUSD - D1 Timeframe

On the Daily timeframe of XAUUSD, we see that price has been rejected initially from the supply zone and seems to simply be heading back up in search of a supply zone from which its bearish momentum can be easily recovered.

XAUUSD - H4 Timeframe

This 4-Hour chart clarifies the entire prospects for Gold. Here, we can see price currently trading around the 76% level of the Fibonacci, and the supply zone. There is also a notable trendline resistance which serves as an additional confluence for a bearish sentiment.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1952.00

- Invalidation: 2010.00

CONCLUSION

The trading of CFDs comes at a risk. To succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

Sunset Market Commentary

Markets

Until about a month ago, market momentum for yields was to drift higher ‘by default’ at days with no market relevant news. A series of softer (or softly perceived) data since then triggered a 180-degree turn in market momentum. Central bankers’ ‘higher for longer mantra’ has been put aside. Key question for markets now is not if, but when the likes of the Fed, the ECB and even the Bank of England will start reversing part of the 2022/2023 hiking cycle even as inflation stays some distance away from (sustainably) reaching the 2.0% target. Markets now discount the ECB, the Fed and the ECB all cutting their policy rates by at least 25 bps at the June meetings at the latest. Central bankers’ comments pushing back against current market positioning (e.g. ECB Holzmann today) are simply ignored. German yields at some point this morning dropped another 7 bps (10-y), but momentum dwindled going into US trading. German yields currently are ceding between 1 bps (2-5y) and 3.5 bps (30-y). After a first attempt last week, German 2-y yield (2.94%) again holds below 3.0%. Near 2.55/58%, the 10-y yield is testing the lowest levels since mid-September. The jury is still out but question is how far long term yields still can decline from current levels, even if one subscribes current money market positioning on 2024 rate cuts. Easing global market conditions support some further intra-EMU spreads’ narrowing. The 10-y Italian spread versus German declines an additional 1-2 bps to 1.75% to be compared with levels of 2.0%+ last month. After the close of European markets, Moody’s will provide a review on Italy’s credit rating. The agency has the lowest score among major rating agencies (Baa3 with negative outlook), only one level above junk status. Looking at recent prices developments, markets don’t expected Moody’s to pull the trigger even as the Italian government scaled back its trajectory for fiscal consolidation. US yields reversed earlier intraday declines to currently trade between +3.5 bp (2-y) and minus 3.0 bps (30-y). Equities remain well bid. The EuroStoxx 50 gains + 0.85%. S&P opens little changed, but as such maintains a 2.0% weekly gain. Oil ($ 79 p/b) tries to regain some ground after yesterday’s tumbling.

On FX markets, the dollar remains in the defensive, even as recent lows in most cross rates were not extended. DXY (104.2 from 104.40) struggles not to fall below the 104 big figure. EUR/USD also gains modestly (1.087), but stays below the 1.0896 week top. The yen outperforms. The unwinding of standing yen short-positions is probably reinforcing some kind of self-feeding stops loss dynamics with USD/JPY (currently 149.7) testing the 149.20 area, compared to yesterday’s close at 150.73 and a YTD peak of 151.91 touched earlier this week. An unexpected decline in UK October retail sales (-0.3% M/M vs +0.4% expected) for sure won’t pass unnoticed at the BoE. Gilts outperform Bunds and Treasuries with yields ceding up to 6 bps (10-y). However, a constructive risk sentiment from now apparently prevents EUR/GBP forcing a sustained break beyond the 0.8755 area (for now?).

News & Views

ECB President Lagarde proposed to extend the powers of the European Securities & Markets Authority so that it more resembles the US’ Securities and Exchanges Commission. She noted that supervision of capital markets is largely a national competence with the ESMA not having broad enforcement powers similar to the ECB’s bank supervision arm. Yet, the bloc needs investor capital flows to finance an economic overhaul aimed to address challenges coming from deglobalization, demographics and decarbonization. In the eurozone and unlike in the US, banks play a more significant financing role compared to capital markets. But according to Lagarde, the upcoming financing needs outstrip banks’ lending capacity.

The Swedish Riksbank started selling foreign currency from its reserves on September 25 to hedge against currency risk. The plan is to sell $8bn and €2bn for Swedish krones within four to six months. With each selling operation, the Riksbank enters into FX swaps in order to maintain the size of its FX reserves. In the week starting October 30, the central bank sold $690 million dollar and no euros. This brings the running total amount to $3.4bn and €309 million. In other news, the central bank meets next week (Nov 23). Analysts polled by Bloomberg are split in a 6-5 vote in favour for a 25 bps hike to 4.25%. Money markets are betting that the Riksbank’s tightening cycle is over.

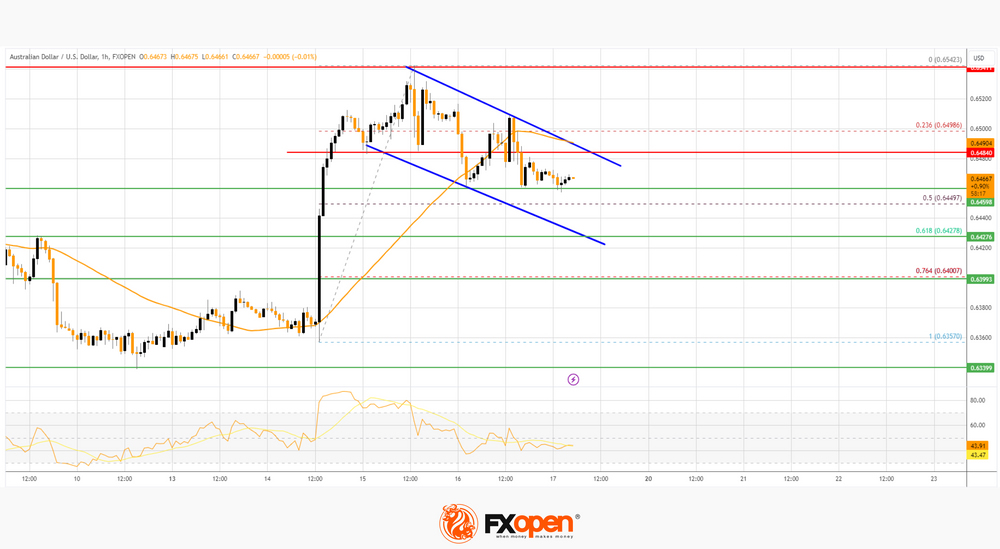

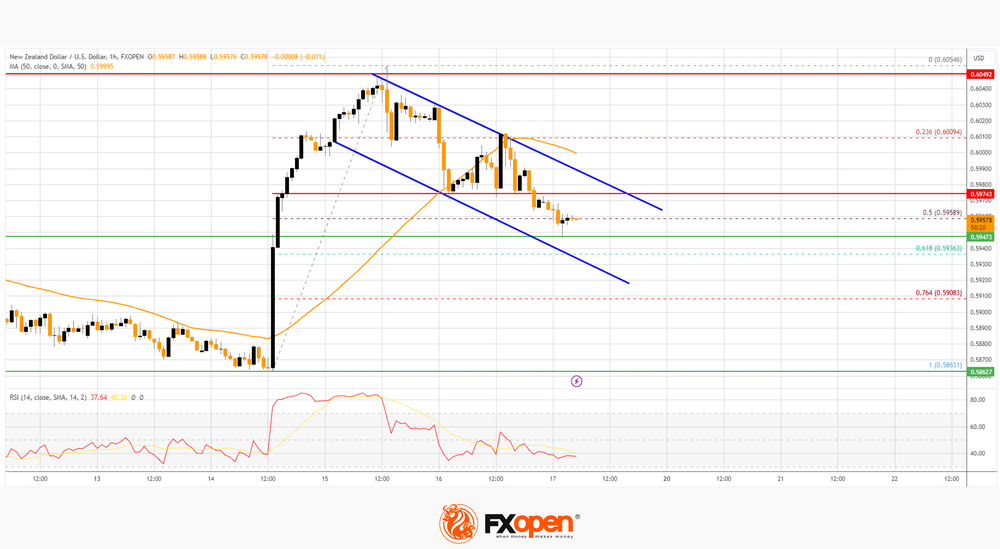

AUD/USD and NZD/USD Dips Could Be Attractive

AUD/USD is correcting gains from the 0.6540 zone. NZD/USD is also moving lower and might attempt a fresh increase from 0.5920.

Important Takeaways for AUD USD and NZD USD Analysis Today

- The Aussie Dollar started a downside correction from 0.6540 against the US Dollar.

- There is a key declining channel forming with resistance at 0.6480 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD is also moving lower below the 0.5980 support zone.

- There is a major declining channel forming with resistance near 0.5975 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair started a fresh increase from the 0.6340 support. The Aussie Dollar was able to clear the 0.6450 resistance to move into a positive zone against the US Dollar.

There was a close above the 0.6500 resistance and the 50-hour simple moving average. Finally, the pair tested the 0.6540 zone. A high is formed near 0.6542 and the pair is now correcting gains.

There was a move below the 0.6500 level. The pair declined below the 23.6% Fib retracement level of the upward move from the 0.6357 swing low to the 0.6542 high. There is also a key declining channel forming with resistance at 0.6480.

On the downside, initial support is near the 50% Fib retracement level of the upward move from the 0.6357 swing low to the 0.6542 high at 0.6450.

The next support could be 0.6420. If there is a downside break below the 0.6420 support, the pair could extend its decline toward the 0.6400 level. Any more losses might signal a move toward 0.6340. On the upside, the AUD/USD chart indicates that the pair is now facing resistance near 0.6480.

The first major resistance might be 0.6500. An upside break above the 0.6500 resistance might send the pair further higher. The next major resistance is near the 0.6540 level. Any more gains could clear the path for a move toward the 0.6600 resistance zone.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair started a steady increase from the 0.5860 level. The New Zealand Dollar broke the 0.5950 resistance to start the recent increase against the US Dollar.

The pair settled above 0.6000 and the 50-hour simple moving average. It tested the 0.6050 zone and is currently correcting gains. The pair corrected lower below the 0.6000 level. The pair also spiked below the 50% Fib retracement level of the upward wave from the 0.5863 swing low to the 0.6054 high.

The NZD/USD chart suggests that the RSI is still below 50 and signaling more downsides. There is also a major declining channel forming with resistance near 0.5975.

On the downside, there is major support forming near 0.5945. The next major support is near the 61.8% Fib retracement level of the upward wave from the 0.5863 swing low to the 0.6054 high at 0.5935.

If there is a downside break below the 0.5935 support, the pair might slide toward the 0.5880 support. Any more losses could lead NZD/USD in a bearish zone to 0.5860.

On the upside, the pair might struggle near 0.5975. The next major resistance is near the 0.6000 level. A clear move above the 0.6000 level might even push the pair toward the 0.6050 level. Any more gains might clear the path for a move toward the 0.6120 resistance zone in the coming days.

Trade global forex with the Innovative Broker of 2022*. Choose from 50+ forex markets 24/5. Open your FXOpen account now or learn more about trading forex with FXOpen.

* FXOpen International, Innovative Broker of 2022, according to the IAFT

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

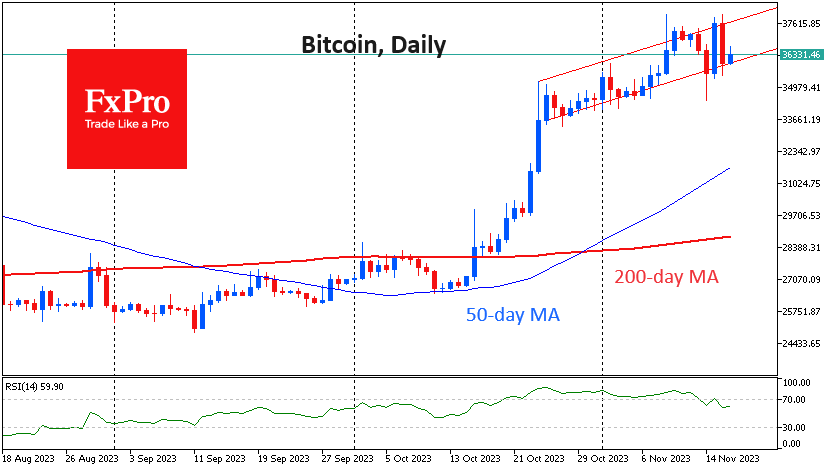

Bitcoin’s Volatility Within An Uptrend

Market picture

The crypto market has lost 1.5% over the past 24 hours, to $1.39 trillion. The sustained pressure has been in place since the start of the day on Thursday and looks like profit-taking from the impressive rally since the middle of last month. The correction is not as deep as it could have been, as it is primarily offset by demand for risk assets.

Tactically, we focus on the increased volatility of Bitcoin, which has fallen below 34500 since the beginning of the week, then rebounded sharply to 38000 and is trading near the midpoint of that range at 36500 at midday on Friday. Despite the volatility, bitcoin has remained in an uptrend since late October, while the volatility is clearing overbought conditions and making room for further gains.

News background

The SEC delayed a decision on Hashdex’s application to launch a spot ETF based on digital gold until 1 January 2024. At the same time, the SEC also postponed a decision on Grayscale’s application to launch an ETF based on Ethereum futures.

According to Bloomberg Intelligence, Grayscale’s application to launch ETFs based on Ethereum ETH futures is needed to advance the decision to launch spot funds on the second cryptocurrency.

SkyBridge Capital CEO Anthony Scaramucci said the Fed’s rate cut early next year will lead to another bull cycle in the cryptocurrency and equity markets. In addition, approving spot Bitcoin ETFs and halving BTC will create a “huge demand” for Bitcoin.

Tether, which issues the most popular stablecoin USDT, plans to invest $500 million in bitcoin mining over the next six months.

US presidential candidate Vivek Ramaswamy pledged to support bitcoin, cryptocurrencies, and decentralised finance (DeFi) in every way possible if he wins the presidential election.

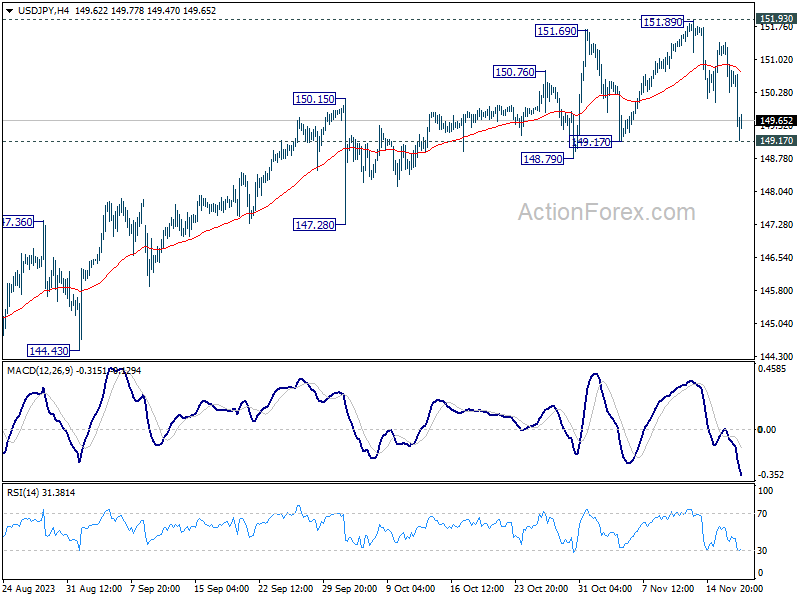

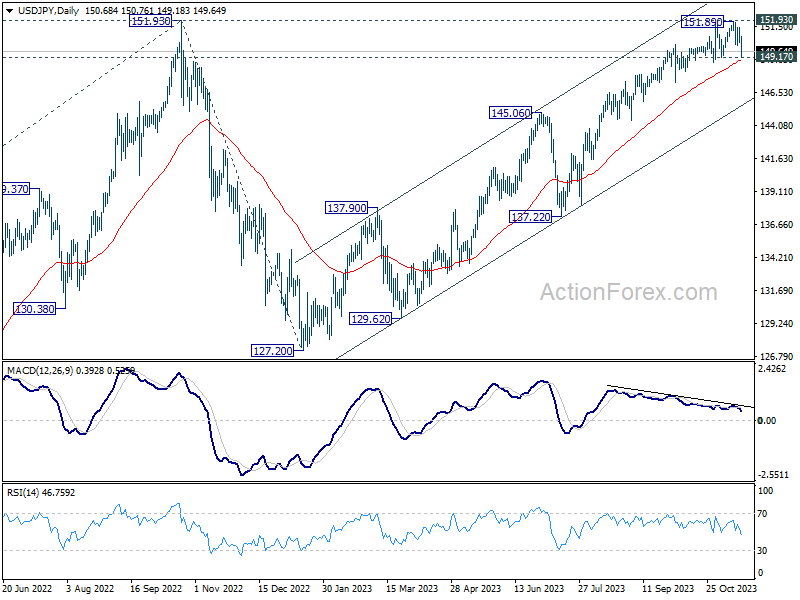

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.20; (P) 150.82; (R1) 151.34; More...

While USD/JPY falls steeply today, it's still holding above 149.17 support. Intraday bias remains neutral for the moment. On the upside, decisive break of 151.93 resistance will confirm resumption of long term up trend. However, firm break of 149.17 will be a sign of bearish reversal and bring deeper fall to 147.28 support first.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 (2021 low) to 151.93 from 127.20 at 157.69.

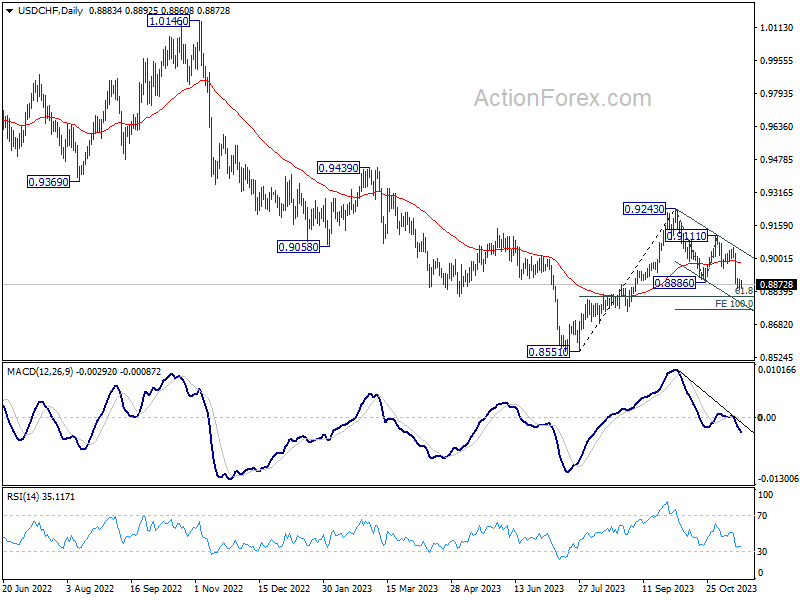

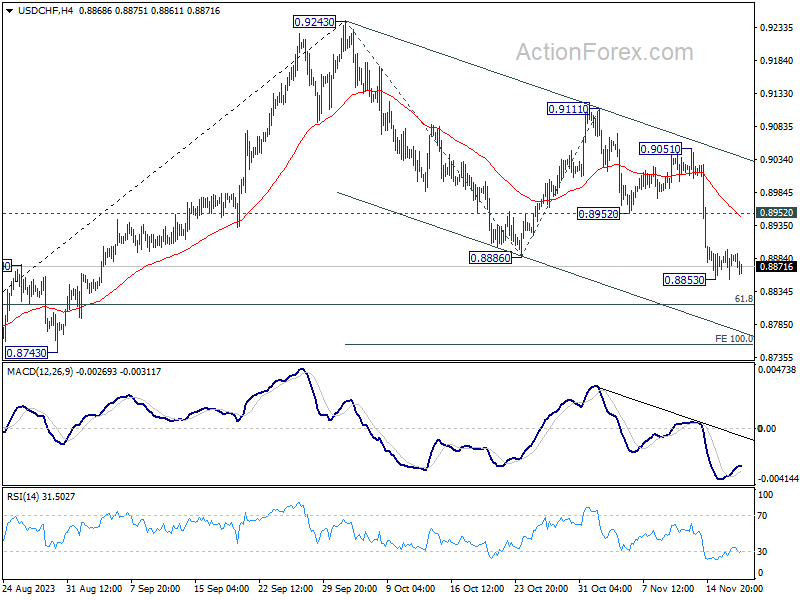

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8837; (P) 0.8933; (R1) 0.8988; More....

Intraday bias in USD/CHF remains neutral for consolidation above 0.8853 temporary low. Stronger recovery cannot be ruled out. But upside should be limited by 0.8952 support turn resistance to bring another fall. Break of 0.8852 will resume the decline from 0.9243 to 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754.

In the bigger picture, price actions from 0.8551 are currently seen as a correction to the decline from 1.0146. Fall from 0.9243 is seen as the second leg for now. Deeper fall would be seen to 61.8% retracement of 0.8551 to 0.9243 at 0.8815. Sustained break there will bring retest of 0.8551 low. For now, this will remain the favored case as long as 0.9111 resistance holds.