Sample Category Title

AUD/USD Weekly Report

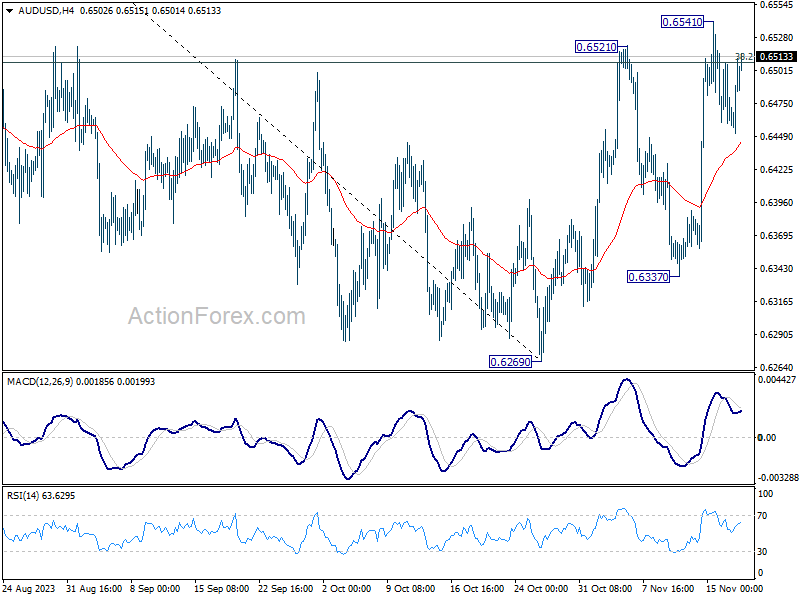

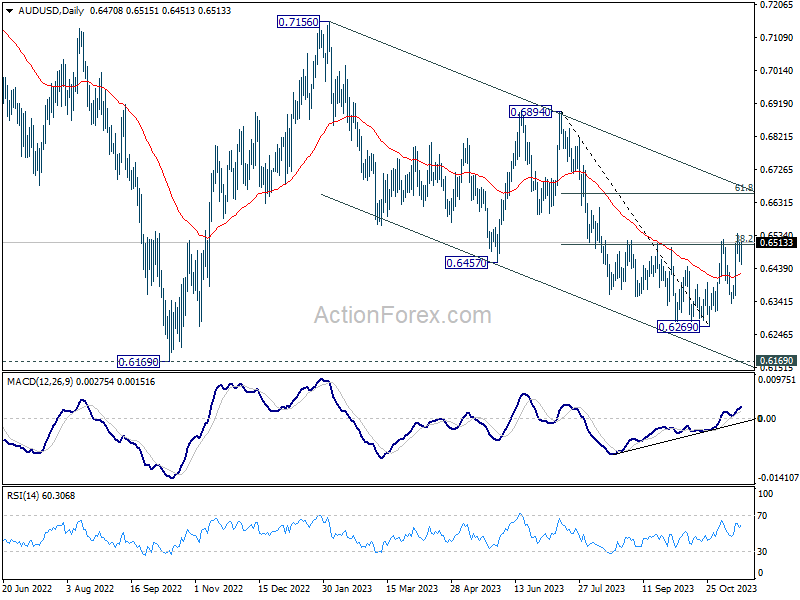

AUD/USD's rebound from 0.6269 resumed last week and hit 0.6541. But subsequent retreat suggested that a temporary top was formed. Initial bias stays neutral this week for more consolidations. On the upside, break of 0.6541, and sustained trading above 38.2% retracement of 0.6894 to 0.6269 at 0.6508, will argue that whole corrective fall from 0.7156 has completed with three waves down to 0.6269. Stronger rally should seen to falling channel resistance (now at 0.6676) next.

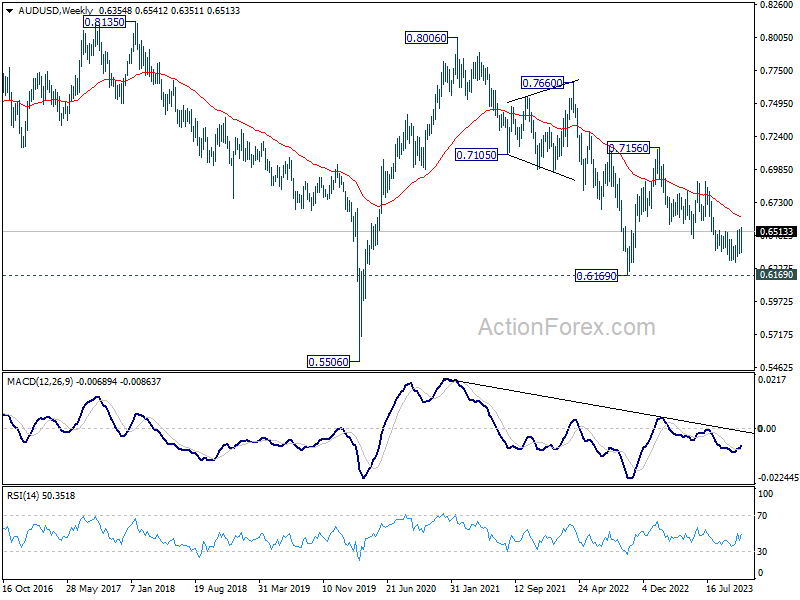

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of the corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

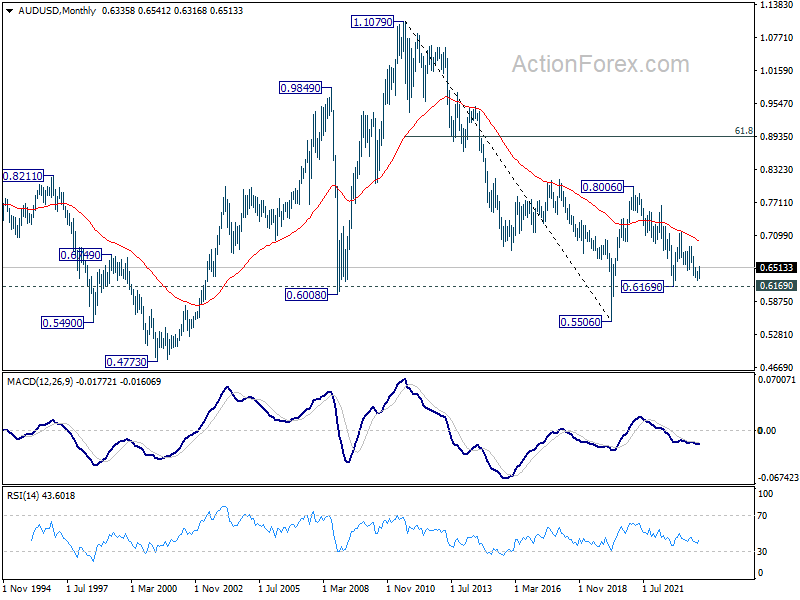

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506(2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen the second leg of the pattern. Hence, in case of deeper decline, downside strong support should emerge above 0.5506 to bring reversal.

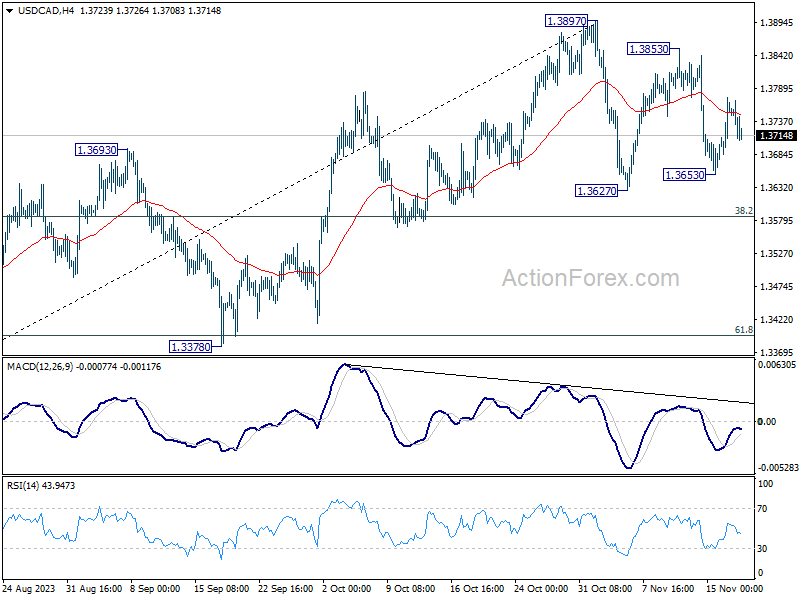

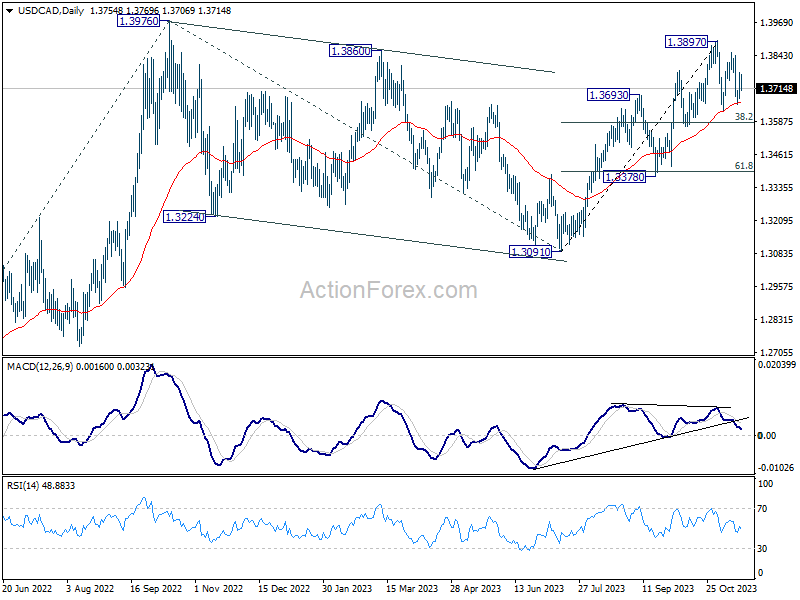

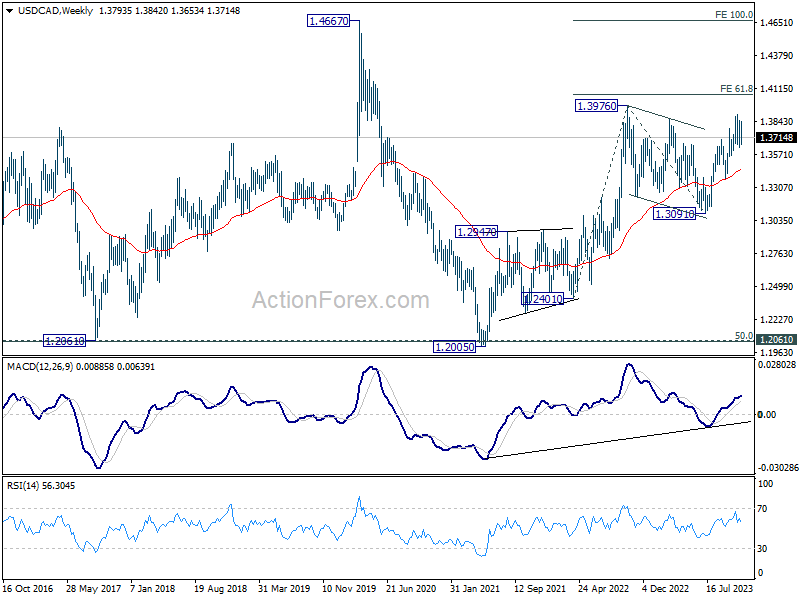

USD/CAD Weekly Outlook

USD/CAD continued to engage in sideway trading last week and outlook is unchanged. Initial bias remains neutral this week first. While another fall cannot be ruled out, downside should be contained by 38.2% retracement of 1.3091 to 1.3897 at 1.3589 to bring rebound. Break of 1.3897 is expected at a later stage to resume larger rally.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will remain the favored case as long as 1.3378 support holds.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern only, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as 55 M EMA (now at 1.3132) holds.

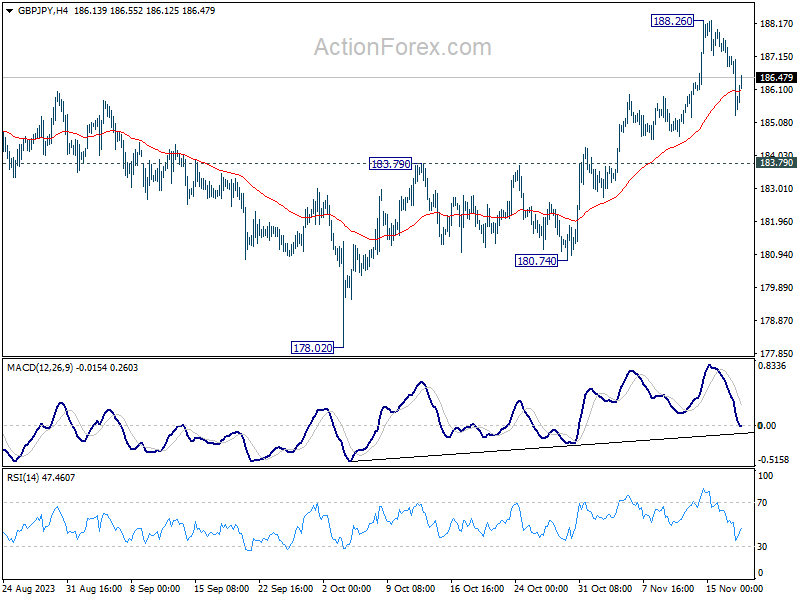

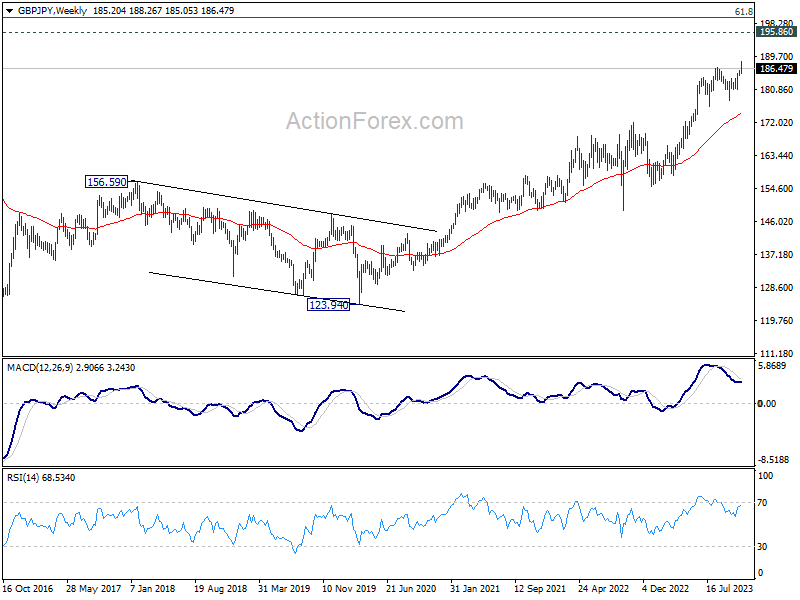

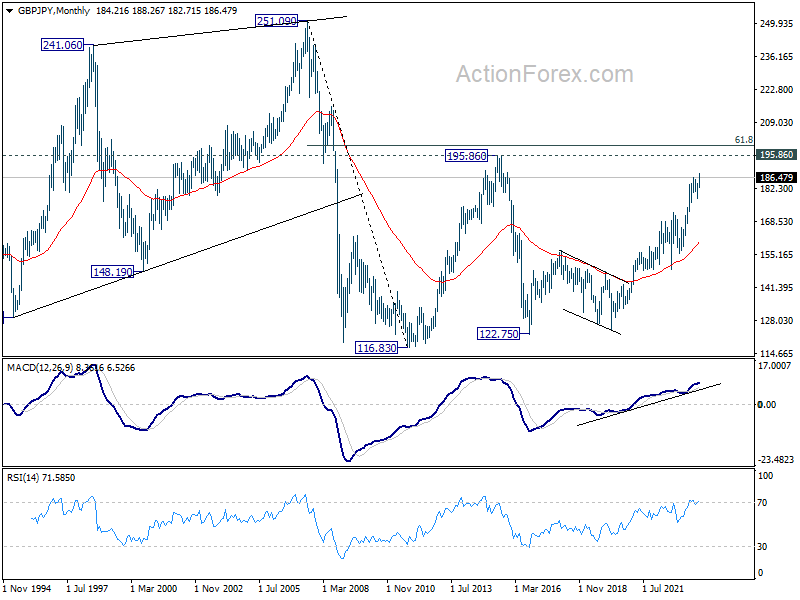

GBP/JPY Weekly Outlook

GBP/JPY's rally resumed last week and hit as high as 188.26, before retreating. Initial bias is now neutral this week for consolidations first. Another rally will remain in favor as long as 183.79 support turned resistance holds. Break of 188.26 will resume larger up trend.

In the bigger picture, as long as 180.74 support holds, larger up trend from 123.94 (202 low) should still be in progress, next target is 195.86 (2015 high). However, firm break of 180.74 will now argue that a medium term top is formed, possibly in bearish divergence condition in D MACD, and bring deeper fall back to 178.02 support.

In the longer term picture, rise from 122.75 (2016 low) in still in progress but started losing upside momentum as seen in W MACD. Further rise will remain in favor, though, as long as 177.02 support holds, to retest 195.86 (2015 high).

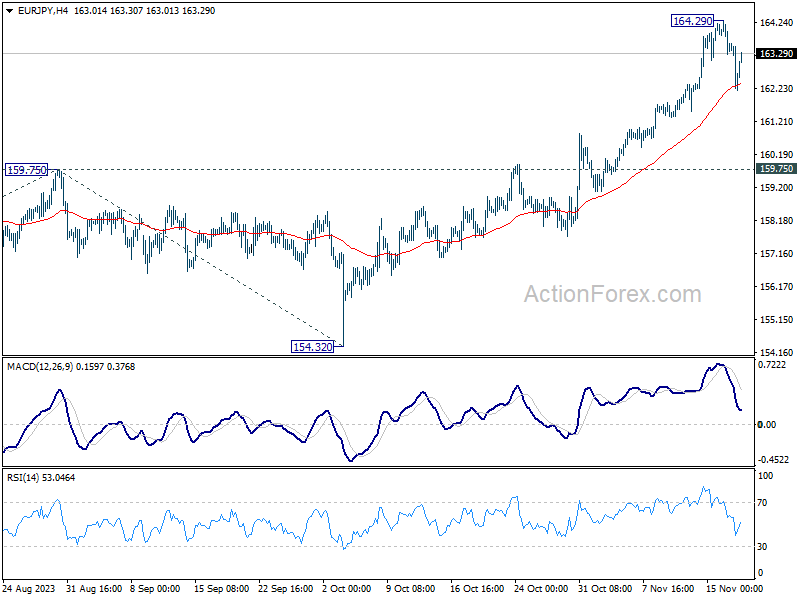

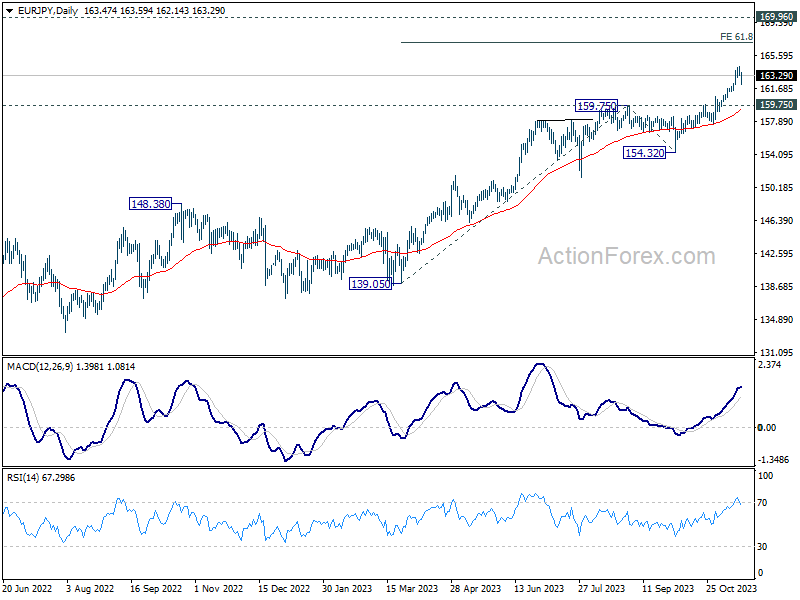

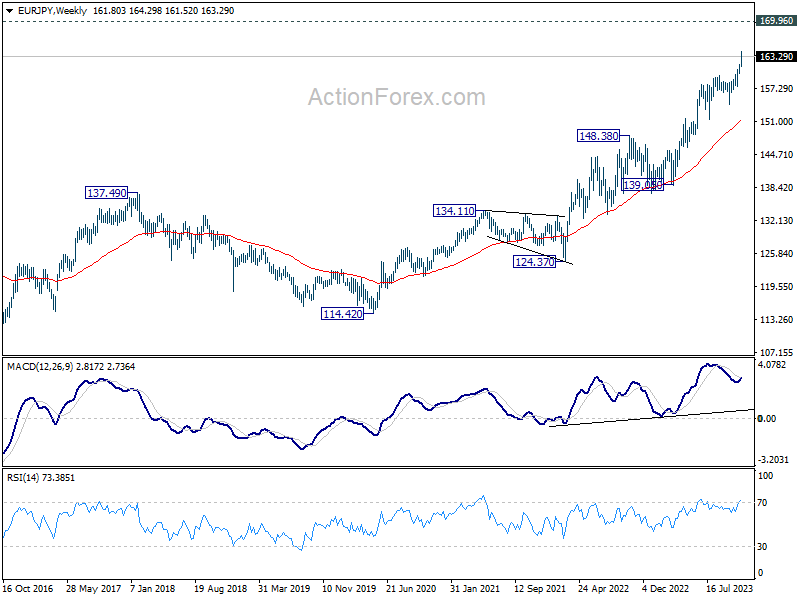

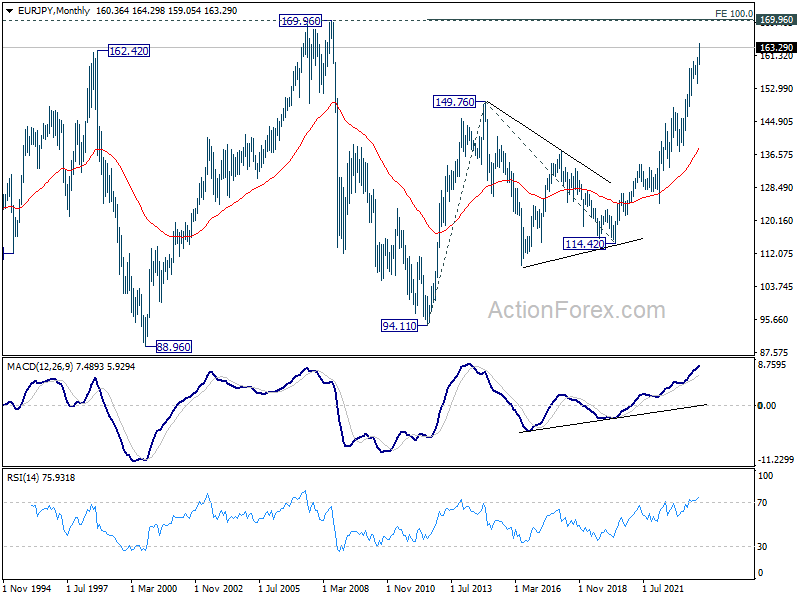

EUR/JPY Weekly Outlook

EUR/JPY's up trend continued to as high as 164.29 last week but retreated since then. Initial bias stays neutral this week first, and some more consolidations could be seen. Downside of retreat should be contained well above 159.75 resistance turned support to bring another rally. On the upside, break of 164.29 will resume larger up trend to 61.8% projection of 139.05 to 159.75 from 154.32 at 167.11.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 169.96 (2008 high). On the downside, break of 159.75 resistance turned support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish even in case of deep pullback.

In the long term picture, rise from 109.03 (2016 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high).

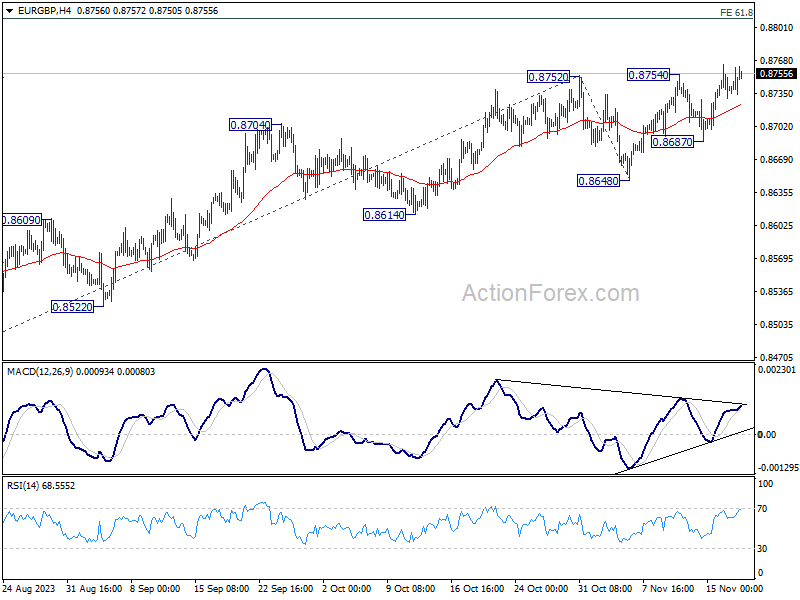

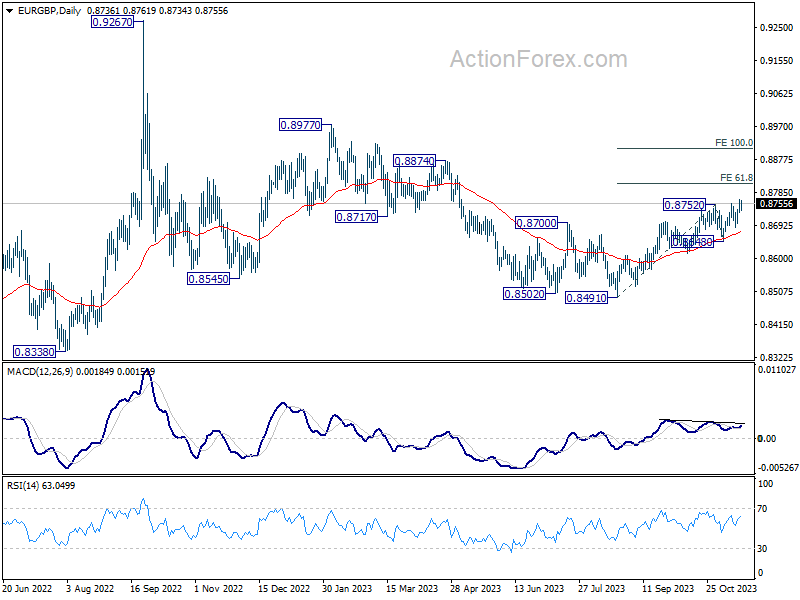

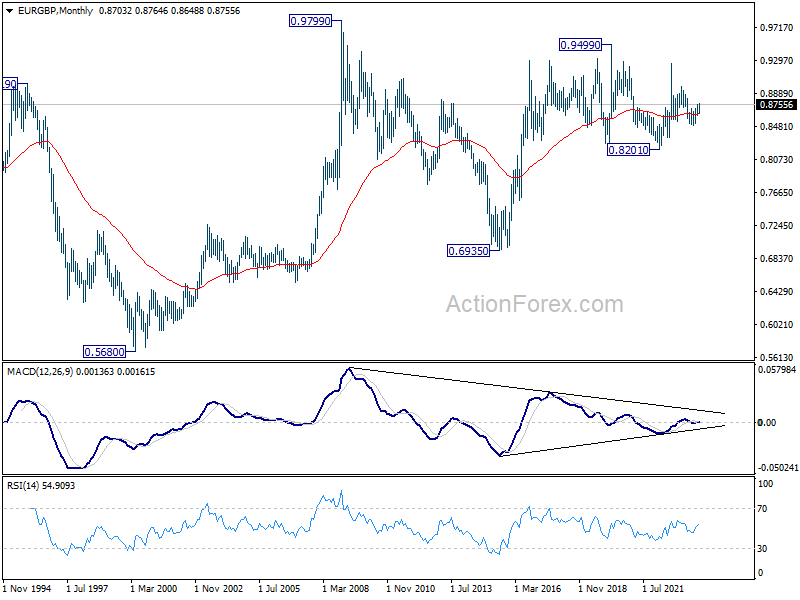

EUR/GBP Weekly Outlook

EUR/GBP's rise from 0.8491 resumed last week by breaching 0.8752 resistance. Initial bias stays on the upside this week for 61.8% projection of 0.8491 to 0.8752 from 0.8648 at 0.8809. On the downside, break of 0.8687 support is needed to indicate short term topping. Otherwise, further rally remains in favor in case of retreat.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. This will remain the favored case as long as 0.8648 support holds.

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to resume at a later stage, to 0.9799 (2009 high).

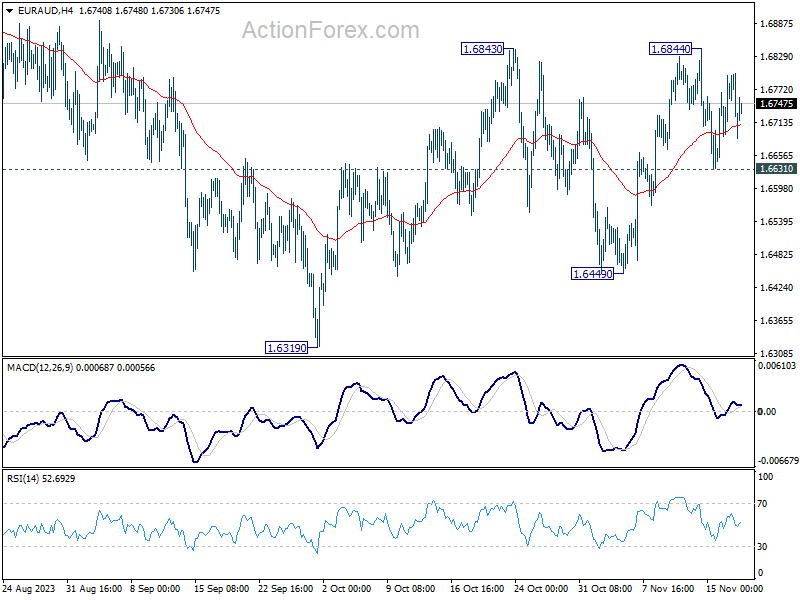

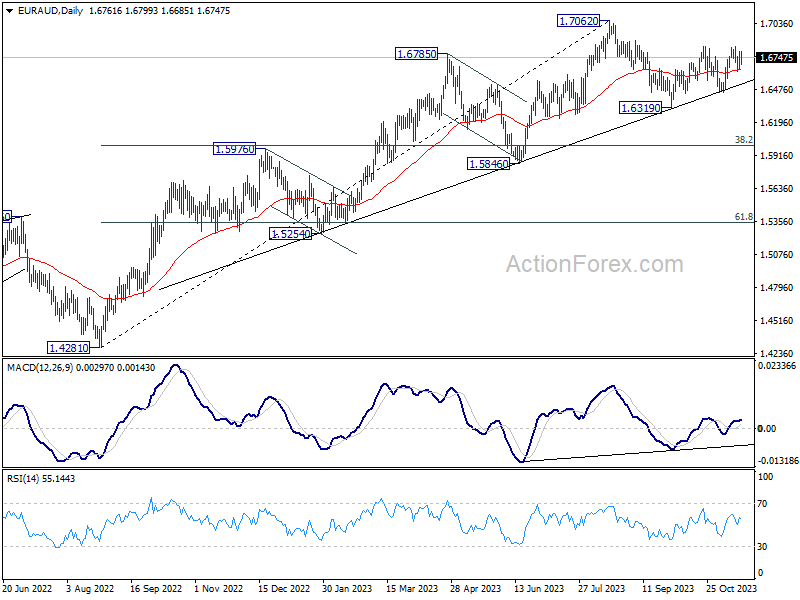

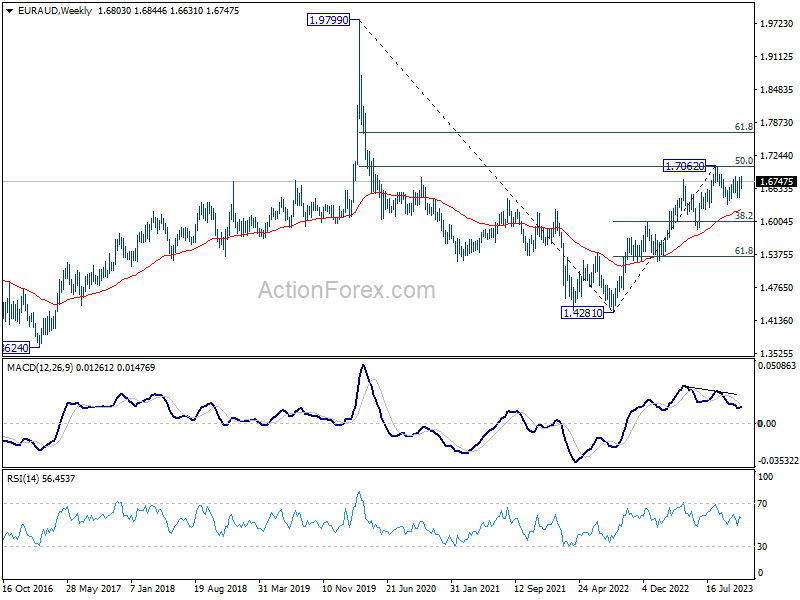

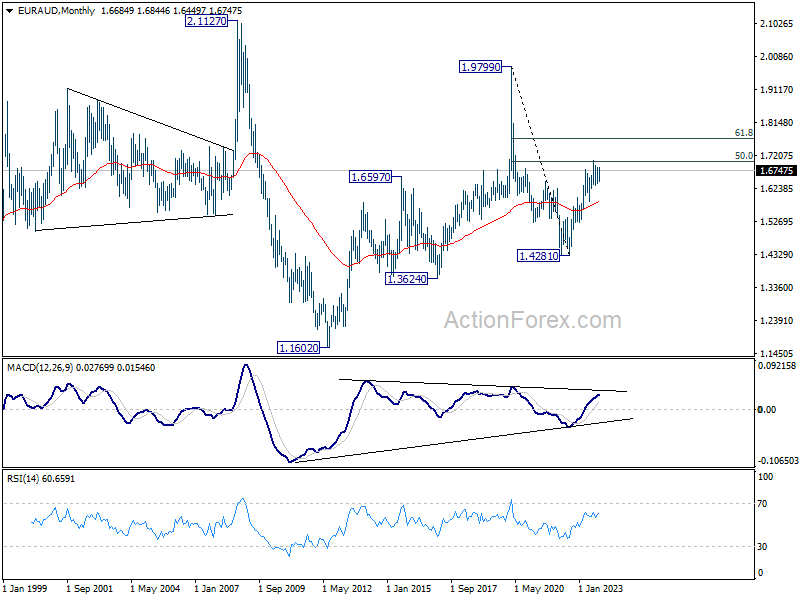

EUR/AUD Weekly Outlook

EUR/AUD failed to break through 1.6843 resistance decisively last week and retreated. Initial bias stays neutral this week for some more consolidations first. On the upside, sustained break of 1.6843/4 will resume the rebound from 1.6319 for retesting 1.7062 high next. On the downside, however, below 1.6631 minor support will turn bias back to the downside for 1.6449 support instead.

In the bigger picture, while 1.7062 is a medium term top, there is no clear sign of trend reversal as EUR/AUD continues to draw strong support from the medium term trend line. Break of 1.7062 will resume the larger up trend from 1.4281 (2022 low) to 1.7691 fibonacci level. Nevertheless, break of 1.6449 support will argue that deeper correction is underway to 38.2% retracement of 1.4281 to 1.7062 at 1.6000.

In the longer term picture, loss of upside momentum as seen in 55 W MACD at this stage argues that rise from 1.4281 (2022 low) is more likely a corrective move. Further rise could still be seen as long as 1.5846 support holds. But upside will likely be limited by 61.8% retracement of 1.9799 to 1.4281 at 1.7691. Firm break of 1.5846 support will argue that the rise has completed, and another medium term down leg has started.

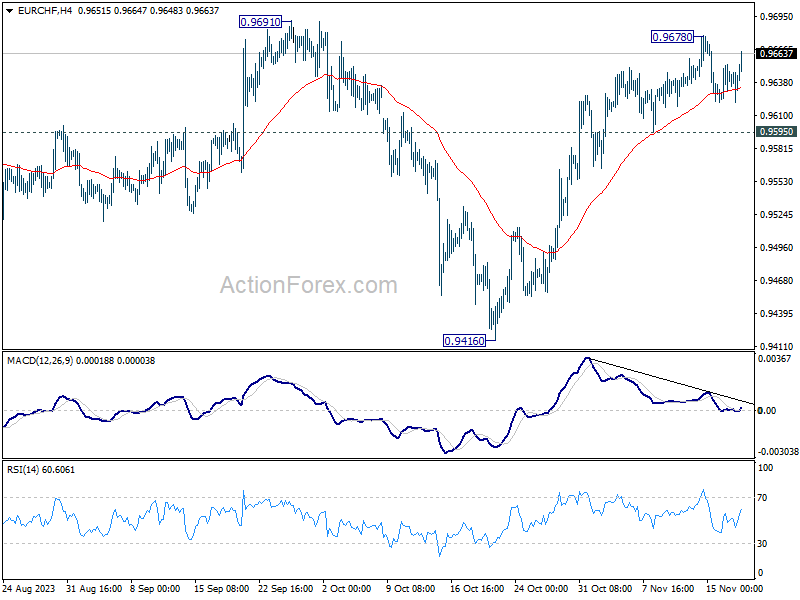

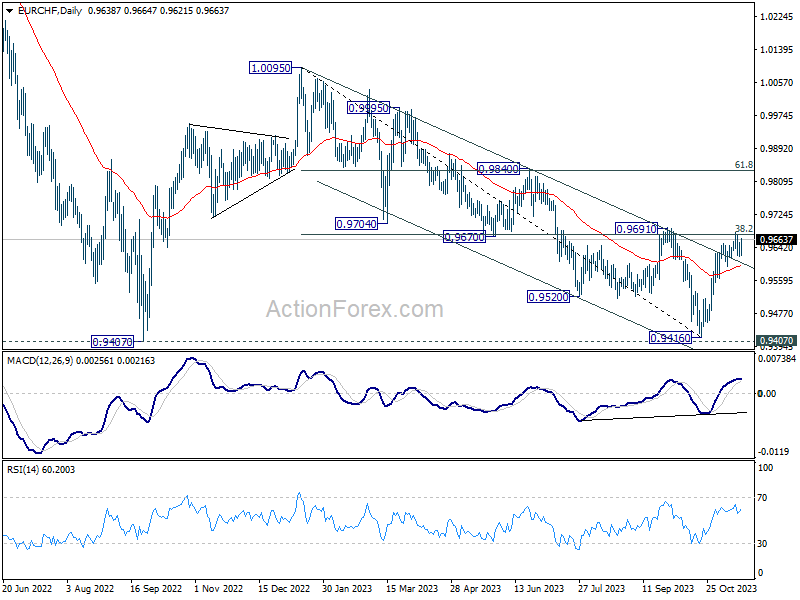

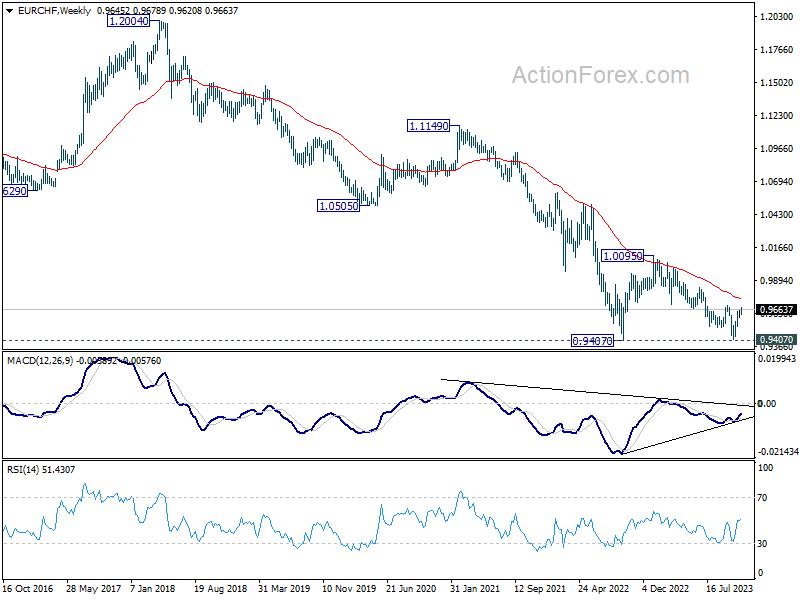

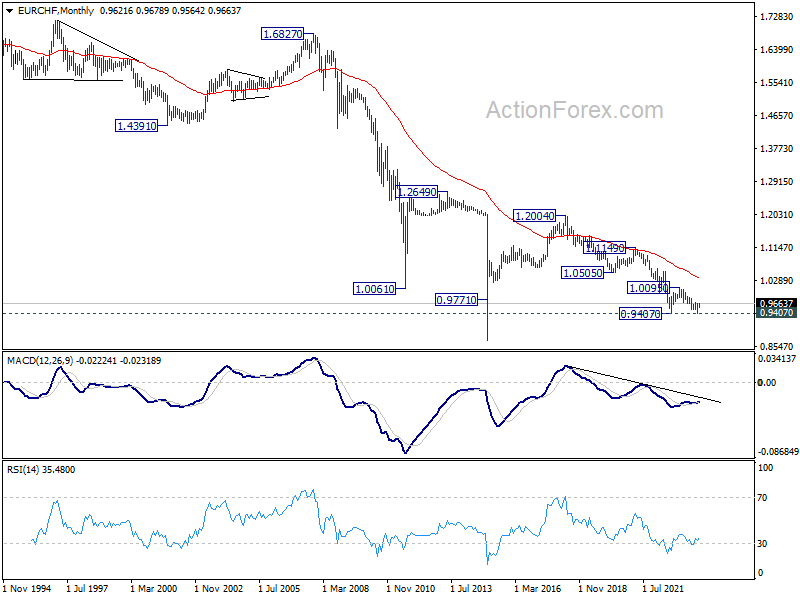

EUR/CHF Weekly Outlook

EUR/CHF edged higher to 0.9678 last week but turned retreated since then. Initial bias stays neutral this week for consolidations first. Further rally is expected as long as 0.9595 support holds. Firm break of 0.9678/91 resistance zone will carry larger bullish implication. Nevertheless, break of 0.9595 support will indicate short term topping, and turn bias back to the downside for deeper pull back.

In the bigger picture, fall from 1.0095 (2023 high) might have completed at 0.9416, just ahead of 0.9407 support (2022 low). Sustained break of 0.9691 cluster resistance (38.2% retracement of 1.0095 to 0.9416 at 0.9675) will pave the way to 61.8% retracement at 0.9836 and above. However, rejection by 0.9691 will maintain medium term bearishness for another test on 0.9407 at least.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0341). Price actions from 0.9407 are viewed as a three-wave consolidation pattern first. Larger down trend from 1.2004 (2018 high) might still resume through 0.9407 at a later stage. Break of 1.0095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

Summary 11/20 – 11/24

Monday, Nov 20, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | EUR | Germany PPI M/M Oct | -0.10% | -0.20% |

| 07:00 | EUR | Germany PPI Y/Y Oct | -11.00% | -14.70% |

| 11:00 | EUR | German Buba Monthly Report | ||

| 21:45 | NZD | Trade Balance (NZD) Oct | -1150M | -2329M |

| 21:45 | NZD | Imports Oct | $7.2B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | EUR | Germany PPI M/M Oct | |

| Forecast: -0.10% | Previous: -0.20% | ||

| 07:00 | EUR | Germany PPI Y/Y Oct | |

| Forecast: -11.00% | Previous: -14.70% | ||

| 11:00 | EUR | German Buba Monthly Report | |

| Forecast: | Previous: | ||

| 21:45 | NZD | Trade Balance (NZD) Oct | |

| Forecast: -1150M | Previous: -2329M | ||

| 21:45 | NZD | Imports Oct | |

| Forecast: | Previous: $7.2B | ||

Tuesday, Nov 21, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | RBA Meeting Minutes | ||

| 07:00 | CHF | Trade Balance (CHF) Oct | 5.87B | 6.32B |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Oct | 21.0B | 13.5B |

| 13:30 | CAD | New Housing Price Index M/M Oct | 0.00% | -0.20% |

| 13:30 | CAD | CPI M/M Oct | 0.20% | -0.10% |

| 13:30 | CAD | CPI Y/Y Oct | 3.20% | 3.80% |

| 13:30 | CAD | CPI Core M/M Oct | -0.10% | |

| 13:30 | CAD | CPI Median Y/Y Oct | 3.60% | 3.80% |

| 13:30 | CAD | CPI Trimmed Y/Y Oct | 3.60% | 3.70% |

| 13:30 | CAD | CPI Common Y/Y Oct | 4.30% | 4.40% |

| 15:00 | USD | Existing Home Sales Oct | 3.91M | 3.96M |

| 19:00 | USD | FOMC Minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | RBA Meeting Minutes | |

| Forecast: | Previous: | ||

| 07:00 | CHF | Trade Balance (CHF) Oct | |

| Forecast: 5.87B | Previous: 6.32B | ||

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Oct | |

| Forecast: 21.0B | Previous: 13.5B | ||

| 13:30 | CAD | New Housing Price Index M/M Oct | |

| Forecast: 0.00% | Previous: -0.20% | ||

| 13:30 | CAD | CPI M/M Oct | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 13:30 | CAD | CPI Y/Y Oct | |

| Forecast: 3.20% | Previous: 3.80% | ||

| 13:30 | CAD | CPI Core M/M Oct | |

| Forecast: | Previous: -0.10% | ||

| 13:30 | CAD | CPI Median Y/Y Oct | |

| Forecast: 3.60% | Previous: 3.80% | ||

| 13:30 | CAD | CPI Trimmed Y/Y Oct | |

| Forecast: 3.60% | Previous: 3.70% | ||

| 13:30 | CAD | CPI Common Y/Y Oct | |

| Forecast: 4.30% | Previous: 4.40% | ||

| 15:00 | USD | Existing Home Sales Oct | |

| Forecast: 3.91M | Previous: 3.96M | ||

| 19:00 | USD | FOMC Minutes | |

| Forecast: | Previous: | ||

Wednesday, Nov 22, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Westpac Leading Index M/M Oct | 0.10% | |

| 13:30 | USD | Initial Jobless Claims (Nov 17) | 225K | 231K |

| 13:30 | USD | Durable Goods Orders Oct | -3.20% | 4.60% |

| 13:30 | USD | Durable Goods Orders ex-Transport Oct | 0.20% | 0.40% |

| 15:00 | USD | Michigan Consumer Sentiment Index Nov F | 61.1 | 60.4 |

| 15:00 | EUR | Eurozone Consumer Confidence Nov P | -18 | -18 |

| 15:30 | USD | Crude Oil Inventories | 3.6M | |

| 17:00 | USD | Natural Gas Storage | 60B | |

| 22:00 | AUD | Manufacturing PMI Nov P | 48.2 | |

| 22:00 | AUD | Services PMI Nov P | 47.9 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Westpac Leading Index M/M Oct | |

| Forecast: | Previous: 0.10% | ||

| 13:30 | USD | Initial Jobless Claims (Nov 17) | |

| Forecast: 225K | Previous: 231K | ||

| 13:30 | USD | Durable Goods Orders Oct | |

| Forecast: -3.20% | Previous: 4.60% | ||

| 13:30 | USD | Durable Goods Orders ex-Transport Oct | |

| Forecast: 0.20% | Previous: 0.40% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Nov F | |

| Forecast: 61.1 | Previous: 60.4 | ||

| 15:00 | EUR | Eurozone Consumer Confidence Nov P | |

| Forecast: -18 | Previous: -18 | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 3.6M | ||

| 17:00 | USD | Natural Gas Storage | |

| Forecast: | Previous: 60B | ||

| 22:00 | AUD | Manufacturing PMI Nov P | |

| Forecast: | Previous: 48.2 | ||

| 22:00 | AUD | Services PMI Nov P | |

| Forecast: | Previous: 47.9 | ||

Thursday, Nov 23, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 08:15 | EUR | France Manufacturing PMI Nov P | 43.2 | 42.8 |

| 08:15 | EUR | France Services PMI Nov P | 45.7 | 45.2 |

| 08:30 | EUR | Germany Manufacturing PMI Nov P | 41.3 | 40.8 |

| 08:30 | EUR | Germany Services PMI Nov P | 48.5 | 48.2 |

| 09:00 | EUR | Eurozone Manufacturing PMI Nov P | 43.4 | 43.1 |

| 09:00 | EUR | Eurozone Services PMI Nov P | 48.0 | 47.8 |

| 09:30 | GBP | Manufacturing PMI Nov P | 45.0 | 44.8 |

| 09:30 | GBP | Services PMI Nov P | 49.5 | 49.5 |

| 12:30 | EUR | ECB Meeting Accounts | ||

| 21:45 | NZD | Retail Sales Q/Q Q3 | -0.80% | -1.00% |

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q3 | -1.50% | -1.80% |

| 23:30 | JPY | National CPI Y/Y Oct | 3% | |

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Oct | 3.00% | 2.80% |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Oct | 4.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 08:15 | EUR | France Manufacturing PMI Nov P | |

| Forecast: 43.2 | Previous: 42.8 | ||

| 08:15 | EUR | France Services PMI Nov P | |

| Forecast: 45.7 | Previous: 45.2 | ||

| 08:30 | EUR | Germany Manufacturing PMI Nov P | |

| Forecast: 41.3 | Previous: 40.8 | ||

| 08:30 | EUR | Germany Services PMI Nov P | |

| Forecast: 48.5 | Previous: 48.2 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Nov P | |

| Forecast: 43.4 | Previous: 43.1 | ||

| 09:00 | EUR | Eurozone Services PMI Nov P | |

| Forecast: 48.0 | Previous: 47.8 | ||

| 09:30 | GBP | Manufacturing PMI Nov P | |

| Forecast: 45.0 | Previous: 44.8 | ||

| 09:30 | GBP | Services PMI Nov P | |

| Forecast: 49.5 | Previous: 49.5 | ||

| 12:30 | EUR | ECB Meeting Accounts | |

| Forecast: | Previous: | ||

| 21:45 | NZD | Retail Sales Q/Q Q3 | |

| Forecast: -0.80% | Previous: -1.00% | ||

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q3 | |

| Forecast: -1.50% | Previous: -1.80% | ||

| 23:30 | JPY | National CPI Y/Y Oct | |

| Forecast: | Previous: 3% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Oct | |

| Forecast: 3.00% | Previous: 2.80% | ||

| 23:30 | JPY | National CPI ex Food Energy Y/Y Oct | |

| Forecast: | Previous: 4.20% | ||

Friday, Nov 24, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Nov | -27 | -30 |

| 00:30 | JPY | Manufacturing PMI Nov P | 48.8 | 48.7 |

| 00:30 | JPY | Services PMI Nov P | 51.6 | |

| 07:00 | EUR | Germany GDP Q/Q Q3 F | -0.10% | -0.10% |

| 09:00 | EUR | Germany IFO Business Climate Nov | 87.5 | 86.9 |

| 09:00 | EUR | Germany IFO Current Assessment Nov | 89.4 | 89.2 |

| 09:00 | EUR | Germany IFO Expectations Nov | 85.7 | 84.7 |

| 13:30 | CAD | Retail Sales M/M Sep | 0.00% | -0.10% |

| 13:30 | CAD | Retail Sales ex Autos M/M Sep | -0.30% | 0.10% |

| 14:45 | USD | Manufacturing PMI Nov P | 49.8 | 50 |

| 14:45 | USD | Services PMI Nov P | 50.4 | 50.6 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Nov | |

| Forecast: -27 | Previous: -30 | ||

| 00:30 | JPY | Manufacturing PMI Nov P | |

| Forecast: 48.8 | Previous: 48.7 | ||

| 00:30 | JPY | Services PMI Nov P | |

| Forecast: | Previous: 51.6 | ||

| 07:00 | EUR | Germany GDP Q/Q Q3 F | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 09:00 | EUR | Germany IFO Business Climate Nov | |

| Forecast: 87.5 | Previous: 86.9 | ||

| 09:00 | EUR | Germany IFO Current Assessment Nov | |

| Forecast: 89.4 | Previous: 89.2 | ||

| 09:00 | EUR | Germany IFO Expectations Nov | |

| Forecast: 85.7 | Previous: 84.7 | ||

| 13:30 | CAD | Retail Sales M/M Sep | |

| Forecast: 0.00% | Previous: -0.10% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Sep | |

| Forecast: -0.30% | Previous: 0.10% | ||

| 14:45 | USD | Manufacturing PMI Nov P | |

| Forecast: 49.8 | Previous: 50 | ||

| 14:45 | USD | Services PMI Nov P | |

| Forecast: 50.4 | Previous: 50.6 | ||

The Weekly Bottom Line: Extended Fed Pause Looking Increasingly Likely

U.S. Highlights

- Consumer Price Index (CPI) inflation printed lower than expected in October, fueling a rally in equities and a sharp pullback in longer-term Treasury yields.

- A government shutdown was averted this week, as Congress passed another short-term funding bill that maintains current spending levels through mid-January.

- Retail sales data showed a moderation in spending activity in October, while higher frequency credit card spend data suggests the weakness has extended into November.

Canadian Highlights

- Next week’s Canadian inflation report is likely to show easing price growth, in line with this week’s U.S. CPI print. The latter was the spark behind a rally in Canadian bonds and equities.

- The fall federal update is also slated for next week, with policymakers promising action on housing supply. On this front, housing starts remained highly elevated in October, though more needs to be done to tackle affordability challenges.

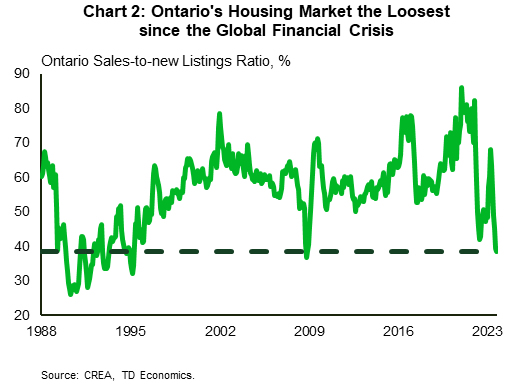

- Given the elevated rates backdrop, Canadian home sales and prices unsurprisingly dropped in October. In Ontario, housing markets are the loosest they’ve been since the Financial Crisis.

U.S. – Extended Fed Pause Looking Increasingly Likely

Market sentiment was decisively in the risk-on camp this week, as a softer reading on October inflation and signs of slowing consumer spending fueled expectations of a longer Fed pause. Also providing a lift to equities was Congress acting to pass yet another short-term funding bill that avoids an immediate government shutdown by extending current levels of spending through mid-January. The S&P 500 is shaping up to end the week 2% higher – extending its winning streak to three-consecutive weeks. Longer-term yields traded lower, with the 10-year Treasury ending the week down 18 basis-points to 4.43%.

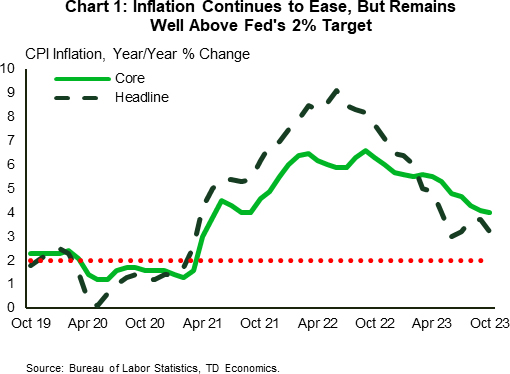

Turning to the Consumer Price Index (CPI) report, both headline and core inflation came in below market expectations. Falling energy and goods prices, a further easing on housing costs and some deceleration in the ‘supercore’ measure all contributed to last month’s softer print. On a twelve-month basis, core inflation is down 2.6 percentage points from last year’s high but, at 4%, remains well above the Fed’s 2% inflation target (Chart 1). As noted in our commentary, the challenge for the Fed going forward is that much of the low hanging fruit on the dis-inflation front has now been picked. With supply-chain issues largely resolved, it is unlikely that falling goods prices will continue to exert as much of a drag on inflation going forward. Ultimately, this means a more pronounced slowing in consumer spending will be required to sustain continued downward pressure on inflation.

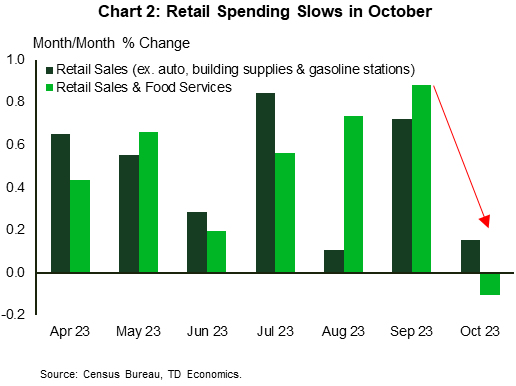

Retail sales data out this week showed that spending activity moderated in October. Although some of the weakness was attributed to a pullback in vehicle sales (possibly impacted by the UAW strike), the less volatile components still showed a meaningful deceleration in spending relative to prior months (Chart 2). Moreover, higher frequency credit card spend data reported through the first week of November has shown that spending activity has continued to moderate into the holiday shopping season.

At this point, the tailwinds for the consumer seem to be fading. Over two-thirds of the excess savings accumulated during the pandemic have now been exhausted, with most of the remaining savings likely residing with higher income households who tend to have a lower marginal propensity to consume. This is happening at a time when 27 million borrowers have started to make regular student loan repayments amidst a backdrop of deteriorating consumer sentiment and expectations of a cooling labor market.

To that end, recent readings on initial jobless claims have already turned higher over the past month, as have continued claims – recently touching a near two-year high. This suggests that not only are more workers losing their jobs but it’s also becoming a bit harder to find another. Ultimately, the labor market remains very tight by historical standards, but the recent drift higher in claims data suggests underlying conditions are easing on the margin. Although the Fed will need to see further evidence of cooling in the months ahead to rule out another rate hike next year, the recent data flow favors the FOMC holding rates steady in December.

Canada – Supply, Supply, Supply

Canadian bond yields were down this week. However, as is often the case, developments south of the border were the driver. Markets seemed to breathe a collective sigh of relief after a softer-than-expected U.S. CPI report offered some hope that the Federal Reserve wouldn't be taking their policy rate higher in the near-term. This prospect also supported a rally in Canadian equities, even as oil prices continued to drop on demand concerns and a larger-than-expected inventory build. It also helped prop up the Canadian dollar, although at around 0.73 U.S. cents, the loonie continues to fly low compared to its U.S. counterpart.

Next week features the release of the Canadian inflation report for October. U.S. all-items inflation trends have historically been a good guide for overall Canadian CPI, so the good showing stateside this week bodes well for the Canadian print. Specifically, markets expect all-items inflation to have cooled to 3.2% year-on-year in October, a marked deceleration from the heated pace observed during much of the summer. As in the U.S., energy prices should lead the inflation deceleration. However, policymakers will be keying in on core inflation, which is also expected to show some modest cooling in year-on-year terms. Notably, U.S. core inflation (i.e., ex-food and energy) eased a touch in October although the correlation between it and the equivalent Canadian measure isn't nearly as tight as it is for overall inflation.

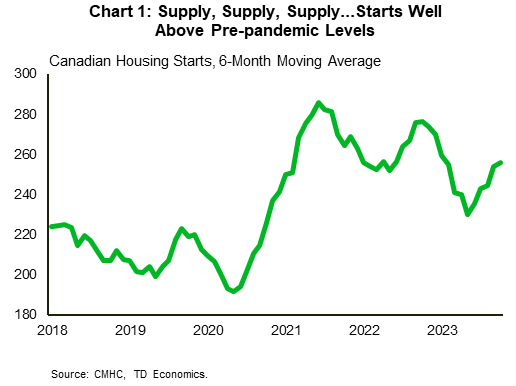

The fall federal fiscal update is also on tap for next week, and the government has telegraphed its intentions. As Minister Freeland noted in a speech this week, the focus will be on housing "supply, supply, supply", amid Canada's affordability crisis. Builders are certainly doing their part to respond to this challenge, with this week's report on housing starts showing them rising to a highly elevated level of 275k units, which is not too far off the record pace hit in early 2021. On a six-month average basis, starts are sitting at a very healthy 253k units (Chart 1), with the largest contributions coming from condos and purpose-built rental construction. While these are good trends indeed, the time it takes to complete a housing project in Canada is on the rise, and even these lofty levels of homebuilding may not be enough to prevent a housing shortage from accumulating given very robust population growth.

From a near-term residential investment and GDP growth perspective, last month's modest gain in housing starts should provide some offset to the 5% month-on-month decline in October's Canadian home sales. As expected, average and benchmark home prices pulled back last month, as did new listings. Arguably the most eye-catching aspect of the report was the decline in Ontario's sales-to-new listings ratio, which hit its lowest level since the Global Financial Crisis (Chart 2). This is a strong signal that more home price declines may be on the way.

Weekly Economic & Financial Commentary: Downside Surprises For G10 Economic Data

Summary

United States: Slew of Data to Binge On

- This week brought fresh reads on an array of macro data, and the underlying details continue to paint a picture of an economy that is gradually losing momentum in Q4. While retail and industrial activity were stronger than the headline data suggest, there are also some signs of weakening.

- Next week: LEI (Mon.), Existing Home Sales (Tue.), Durable Goods Orders (Wed.)

International: Downside Surprises For G10 Economic Data

- This week's reports pointed to slowing growth and slowing inflation among the economies. After solid growth during the first half of the year, Japan's Q3 GDP shrank by 2.1% quarter-over-quarter annualized, a larger than expected decline. U.K. October inflation slowed sharply to 4.6% year-over-year.

- Next week: Canada CPI (Tue.), Eurozone PMIs (Thu.), Japan CPI (Fri.)

Interest Rate Watch: Yields Fall on Slowing Inflation

- U.S. Treasury yields fell this week as markets digested slower-than-expected inflation data for October. As we go to print, the yield on the 10-year Treasury note is 4.45%, down from 4.65% one week ago. This week's inflation reports reinforced our view that the FOMC is done hiking rates.

Credit Market Insights: Credit Card Delinquencies Creep Up in Q3

- The Federal Reserve Bank of New York released its quarterly Household Debt and Credit Report last week. Not only did each major category of household debt rise during the quarter, but delinquency rates also moved higher. Credit card debt delinquency rates, in particular, have climbed above their pre-pandemic average.

Topic of the Week: Not-So-Free Bird: Thanksgiving Related Inflation Decelerates, Though Still Elevated

- Consumers have faced price pressures over the past few years that have continued to gobble up their wallets, and this Thanksgiving will be no different. Though price hikes for most items on the Thanksgiving menu have eased considerably from a year ago, the cost of Thanksgiving staples are still broadly elevated relative to a few years ago.