Sample Category Title

Sunset Market Commentary

Markets

It all boiled down to October US inflation figures today. Headline inflation was flat compared to September (vs +0.1% M/M forecast) resulting in a slightly bigger than anticipated drop from 3.7% Y/Y to 3.2% Y/Y. Energy prices were down 2.5% M/M with gasoline dropping 5% compared with September. Core inflation rose by 0.2% M/M (vs 0.3% M/M) with the Y/Y-figure a tad softer at 4% (from 4.1%), matching the lowest levels since August and September of 2021. The Bureau of Labour Statistics indicated that the shelter index was the largest factor in the monthly increase in core inflation (0.3% M/M). The market reaction was heavy despite the minor miss with investors taking the possibility of a December rate (14% by yesterday’s close) completely off the table and pulling forward the timing of a first Fed rate cut one meeting (from May to March). Daily changes on the US yield curve range between -15 bps (30-yr) and -22 bps (5-yr) at the moment. From a technical point of view, the 2-yr yield is back below the psychologic 5% mark with the November low at 4.80% serving as first support (4.84% live). The US 5-yr yield loses 4.50% with the November low at 4.43% (4.44% live). The US 10-yr yield is effectively losing the November low at 4.47% (4.45% live) with the 30-yr yield testing that barrier (4.61%). German Bunds rally in sympathy with yields 7 to 9 bps lower on the day and the belly of the curve outperforming the wings. The German 10-yr yield is closing in on the November low as well (2.62% vs 2.61%). Loss of interest rate support hurt the dollar. The trade-weighted greenback currently tests the November low at 104.85 from an open at 105.65. EUR/USD pierces through that technical reference, exchanging hands above 1.08 for the first time since early September (1.0820 from 1.07). Today’s figures and USD weakness even give some reprieve to USD/JPY with the pair declining from 151.80 to 150.80. European stock markets extend their recent bullish, gaining up to 1.5% for the German Dax. The EuroStoxx 50 breaks with the ruling sell-on-upticks pattern after easily taking out the previous high at 4237. US stock markets open with significant gains of up to 2% for the Nasdaq.

News & Views

Hungary and Poland reported a first estimate of Q3 GDP growth. Activity in Hungary rebounded 0.9% compared to the April-June quarter. Growth in the second quarter was also upwardly revised from -0.3% to 0.0%. The Hungarian economy posted negative quarterly growth figures since the third of last year. Even after the Q3 growth economic Hungarian activity was still 0.4% lower compared the same quarter last year. Over the first three quarters of the year, activity was 1.2% lower compared to 2022. The Hungarian Statistical office gave no exact data on the composition of the GDP, but indicated that the decrease in economic performance compared to last year was mostly owing to falls in industry and market services, with the latter mainly in wholesale and retail trade as well as scientific, technical and administrative activities. A good performance of agriculture eased the decline. The decrease in services added value was partly offset by a significant growth in section human health and social work activities. A second estimate of Q3 GDP will be published on December 01. According to flash estimate published by Statistics Poland, Q3 GDP rose 1.5% Q/Q and was 0.4% higher compared to the same quarter last year. The Statistical office also signaled a substantial upward revision of Q2 growth (0.3% from -2.2%). A first revision will be published on November 30.

Sentiment among US small business as measured by the NFIB confidence index remains sluggish. The headline indicator of the National Federation of Independ business declined from 90.8 to 90.7, touching the lowest level in five months. Firms turned more negative on recent sales and a growing number of firms reported an earnings decline over the previous three months. US smaller companies remained negative on the expected development of the economy (-43%) and see negative future earnings (-32%). The number of companies expecting better sales ‘improved’ from -13% to -10%, but still shows a bigger part of the companies seeing a deterioration. The NFIB uncertainty index declined slightly from 79 to 76. With respect to inflation, companies see higher selling prices, extending the uptrend since July (30% from 29% and 25% in July). In this respect NFIB assessed that ‘Labor costs, energy costs, and everything else small business owners pay for to operate their business are not falling, so firms continue to raise selling prices to keep up’.

BoE’s Pill prepared to raise rates if necessary

BoE Chief Economist Huw Pill emphasized today the readiness of the Bank to raise interest rates further if the situation demands, but also indicated that further rate hikes are not a necessity at the current juncture.

Pill highlighted today's wage growth data, noting, "We did have this morning the latest official data on pay growth in the UK with pay growing at 7.7%... But actually over the summer pay growth has remained very strong and we certainly wouldn't see pay growth of that rate as consistent with achieving the 2% inflation target on an ongoing basis."

BoE is closely monitoring the upcoming October CPI data, anticipating a decline to "around 5%." However, Pill acknowledges that even this level is significantly higher than the target, remarking, "But nonetheless, 5% is still much too high."

Pill also expressed concerns about the persistence of inflation, partly attributed to ongoing supply issues. He stressed the importance of maintaining a consistent policy approach, stating, "We need to meet inflation persistence with persistent restrictiveness in policy."

US October CPI: No Spooky Surprises

Summary

October's softer-than-expected CPI print is an encouraging development for the FOMC and reinforces our view that the FOMC has ended its hiking cycle. But, we do not see the latest data as a game-changer for inflation's path ahead. With inflation in October held down by volatile components like gasoline, travel services and autos, we expect inflation's return to 2% will continue to be a slow grind.

Inflation Reprieve

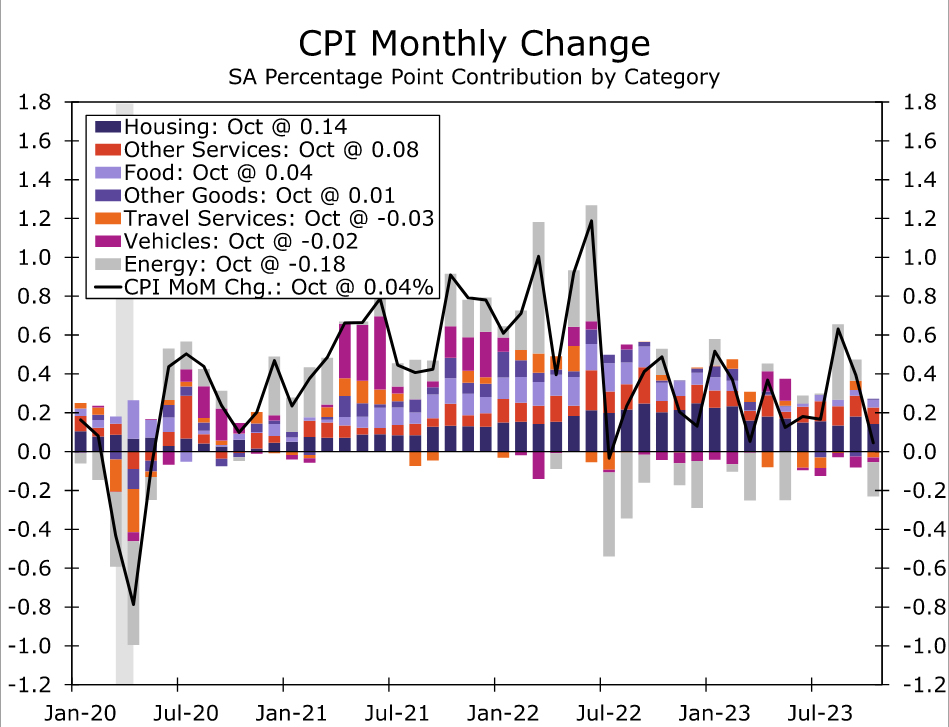

The consumer price index was unchanged in October, the first time monthly inflation was flat since July 2022. The Bloomberg consensus expected a 0.1% increase in the CPI, so this reading was a bit cooler than anticipated. As was the case in July 2022, a large drop in gasoline prices was the main contributor to the soft monthly reading. Gas prices fell 5.0% in October, more than reversing the 2.1% increase that occurred in September. Energy services prices, which includes electricity and utility gas, rose 0.5% in the month. Food prices increased 0.3% in October with food away from home inflation (+0.4%) outpacing the increase in prices at the grocery store (0.3%).

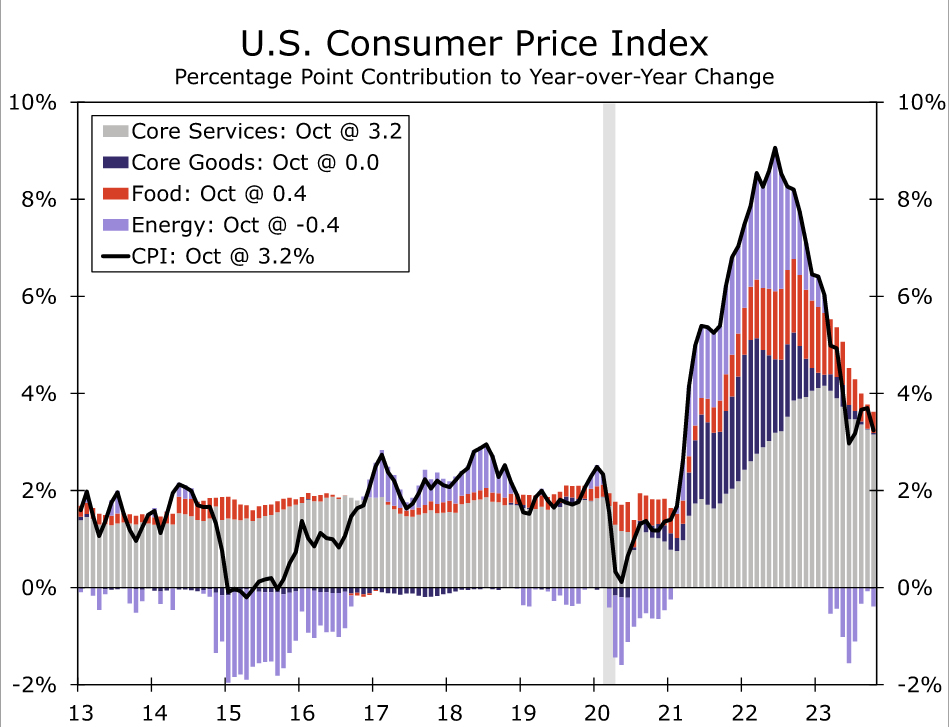

Compared to one year ago, the headline CPI has increased 3.2% (chart). Although this is still about a percentage above the pace that prevailed before the pandemic, it is well below the 9.1% peak that occurred in the summer of 2022. An outright decline in energy prices and much slower increases for food prices have put downward pressure on year-over-year inflation, although core price growth also has slowed to 4.0% from over 6% this time last year.

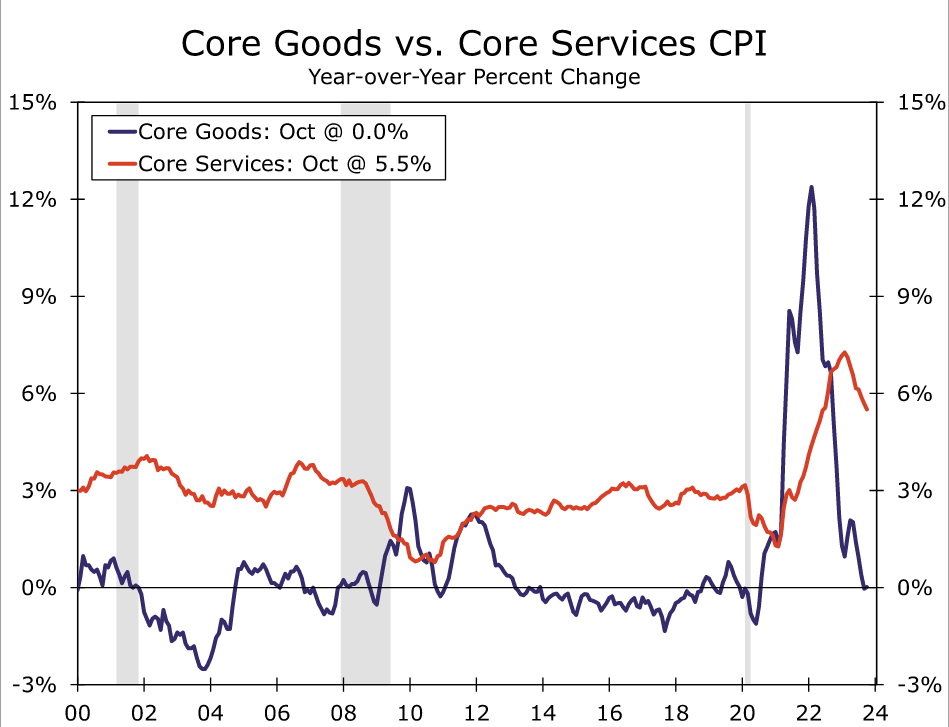

Excluding food and energy, consumer prices rose 0.2% in October, which was a touch softer than expected. The sharp run-up in goods prices since the pandemic continued to unwind in October. Core goods prices fell 0.1% in October, helped along by another drop in used vehicle prices (-0.8%) and a slight giveback in new vehicle prices (-0.1%). Elsewhere, goods prices were little changed over the month, as declines in education & communication equipment and motor vehicle parts offset small increases in apparel, medical and recreation goods. After peaking at a year-over-year rate of more than 12% last February, core goods price are unchanged from a year ago (chart).

Services inflation continues to ease as well, although progress remains slower than in the goods sector. Core services rose 0.3% in October, bringing the one-year change down to 5.5% from 6.7% this time last year. After a surprise 0.6% leap in September, owners' equivalent rent growth slowed in October (+0.4%), while the monthly change in rent of primary residences was little changed at 0.5%. We expect to see shelter inflation to continue to moderate in the months ahead, although the steady rate of primary rent inflation cautions that the slowdown might not be as sharp as private sector measures have implied.

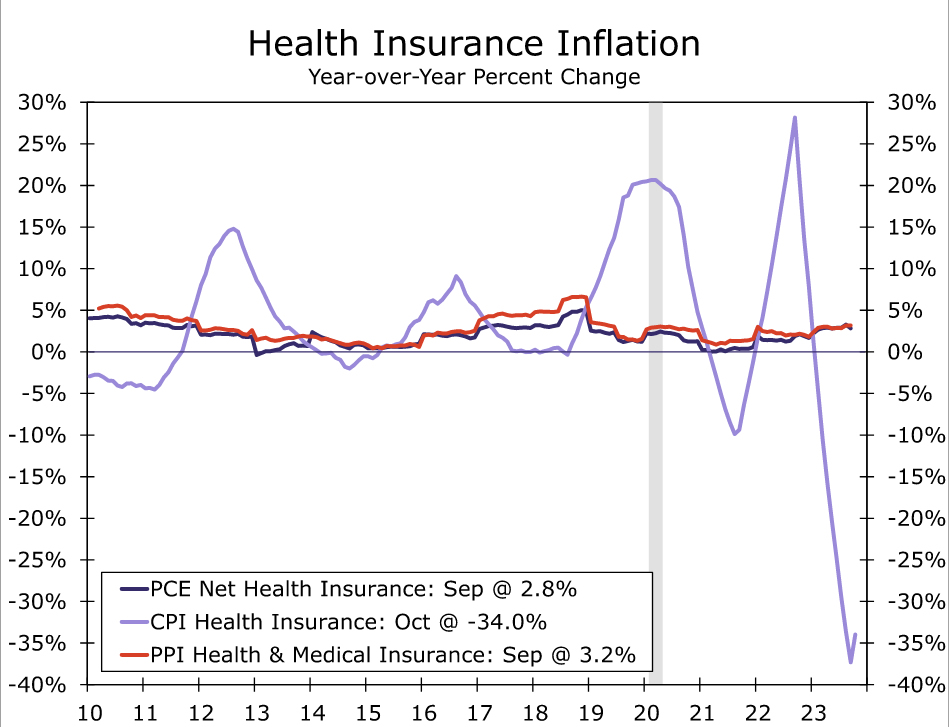

October's softer print in core services came despite a renewed rise in health insurance prices. After falling an average of 3.8% per month over the past year, the health insurance index rose 1.1% in October. "Prices" in this category are measured indirectly by the industry's retained earnings and are rather backward looking, with 2022 data incorporated with this release. Notably, the rise will not feed through to the PCE deflator, the Fed's preferred gauge of inflation, where health insurance inflation is measured differently and is up a rather-unremarkable 2.8% over the past year (chart).

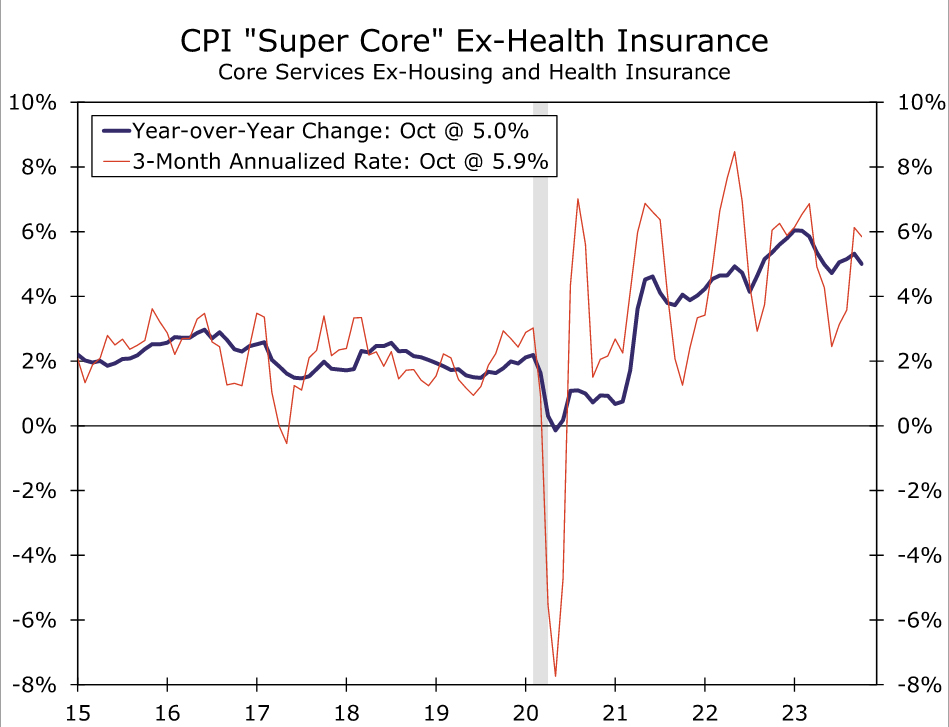

With the con of throwing yet another measure of "core" inflation into the mix, core services less primary shelter and health insurance, i.e., the CPI "super core" with the additional exclusion of health insurance, rose 0.2% in October after a 0.6% rise the prior month. Declines in both airfare (-0.9%) and hotel prices (-2.9%), two of the most volatile components of services, take some of the shine off the services slowdown, as they will be hard to repeat on a consistent basis. Through the large swings in travel-related services, the trend in CPI super core less health insurance is little improved over the past year, underscoring that despite the improvement for goods and housing, the fight against inflation is far from over (chart).

Focus To Turn from Future Rate Hikes to Future Rate Cuts

Today's CPI report further reinforces our view that the last rate hike of this tightening cycle is behind us. We will not receive the October data for the Fed's preferred measure of inflation, the PCE deflator, until November 30. That said, today's CPI data signal that inflation took another step forward on its long road back to 2%. The FOMC's job is not finished. Inflation is not yet back to 2%, and the Committee likely will need to feel confident that 2% inflation can be sustained before it begins to loosen its restrictive stance of monetary policy. Furthermore, the Committee will remain diligently on the lookout for any shocks that could disrupt the disinflationary trends that are currently in place. That said, as 2023 draws to a close and 2024 comes into view, we suspect the debate next year will focus squarely on when rate cuts and the end of quantitative tightening will occur.

US: Lower Prices at the Pump Cool Headline Inflation, and Cooler Core Inflation Provides Reassurance

The Consumer Price Index (CPI) was flat in October, marking a deceleration from September's 0.4% month-on-month (m/m) gain, and below consensus expectations. On a twelve-month basis, headline inflation cooled further to 3.2%.

Energy prices helped hold back headline inflation, dropping 2.5% m/m, driven by a drop in gasoline prices (-5.3% m/m). Food prices added upward pressure to inflation on a monthly basis (+0.3% m/m), but at 3.3% year-on-year, are no longer providing the lift to headline inflation they were last year.

There was good news on core inflation, which rose 0.2% m/m, below market consensus. Core inflation was up 4% on a year-on-year basis in October, down a tick from September.

Core goods prices have been a downward force on inflation for five months now, with prices down 0.1% m/m in October. Even services price gains cooled, up 0.3% m/m after a string of hotter readings over the past few months.

Shelter costs have been a key factor pushing service costs higher, and rose a more modest 0.3% m/m in October. Shelter inflation eased on both a 2.5% m/m drop in lodging away from home, and a cooling in owners' equivalent rent (rising by 0.4% m/m from 0.6% m/m in September).

- Non-housing services (aka the CPI measure of 'supercore') also decelerated in October, rising 0.3% m/m (from 0.6% m/m in September). However, hotter readings in recent months have left the twelve-month pace unchanged at 3.7%.

Key Implications

Well that is more like it. October's CPI inflation report showed encouraging progress towards the Fed's 2% target. Core inflation is still well above a pace consistent with the Fed's target, so it remains way too early for the Fed to declare victory, but policymakers likely just exhaled a bit. On a three-month annualized basis core inflation was 3.4% in October – still too high but pointing to further deceleration ahead.

The challenge for the Fed is much of the low hanging fruit on dis-inflation has been picked. Resolution of supply chain snarls that were keeping prices elevated, and other pandemic re-opening pain points, have already exerted a downward influence on inflation, and now we need to see consistently softer prices pressures due to weaker demand to get back to target. So far, consumer demand has kept up, but we will be watching tomorrow's retail sales figures for October closely for signs of fatigue. If we don't start to see greater cooling, the Fed will likely need to raise rates again.

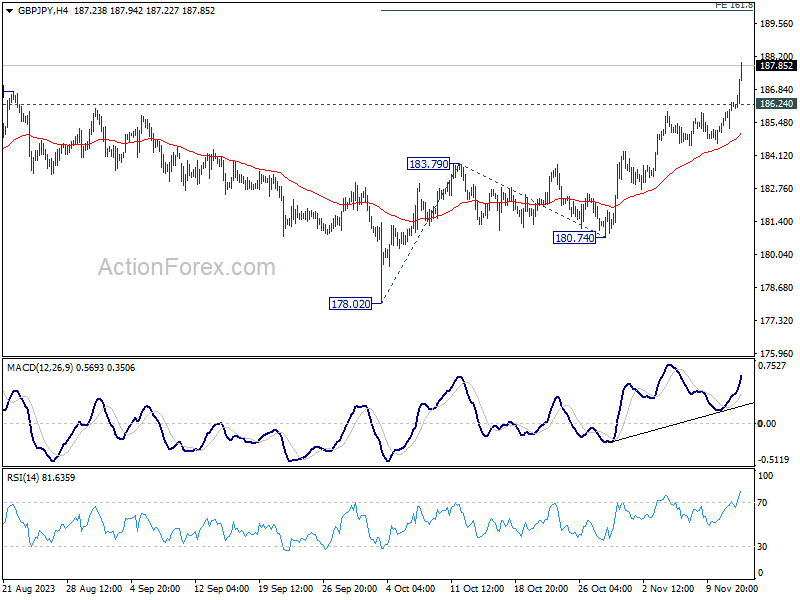

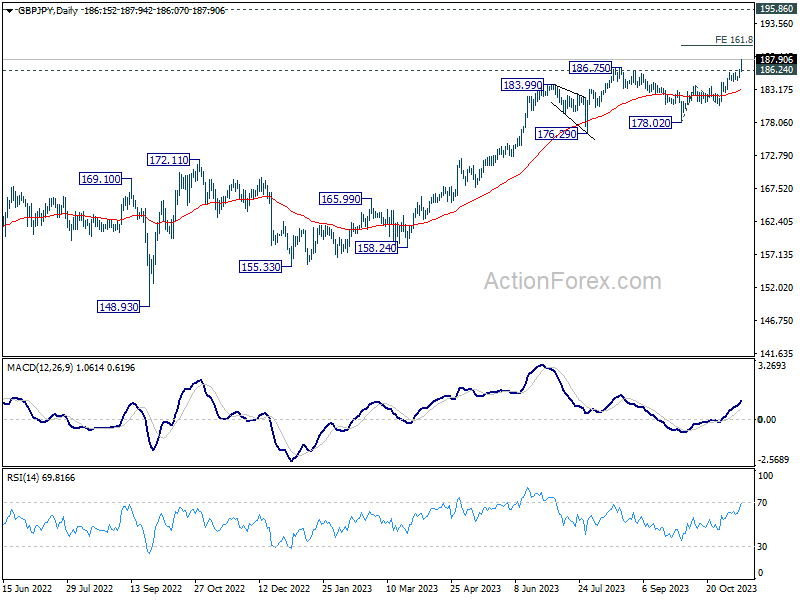

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 185.42; (P) 185.87; (R1) 186.75; More...

GBP/JPY accelerates to as high as 187.91 so far. The break of 186.75 resistance confirms larger up trend resumption. Intraday bias stays on the upside for 161.8% projection of 178.02 to 183.79 from 180.74 at 190.07. On the downside, below 186.24 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, as long as 178.02 support holds, larger up trend from 123.94 (202 low) should still be in progress, next target is 195.86 (2015 high). For now, outlook will stay bullish as long as 178.02 support holds, in case of deep pullback.

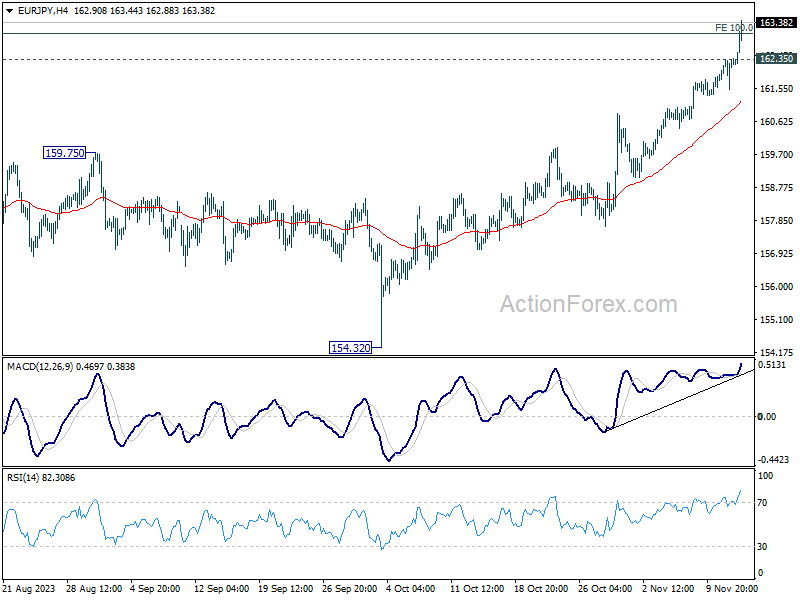

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 161.78; (P) 162.08; (R1) 162.61; More....

EUR/JPY's rally accelerates to as high as 163.44 so far. 163.06 projection is taken out already and there is no sign of topping. Intraday bias stays on the upside . Next target is 169.96 long term resistance. On the downside, below 162.35 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, rise from 114.42 (2020 low) is in progress. sustained trading above 100% projection of 124.37 to 148.38 from 139.05 at 163.06 will target 169.96 (2008 high). On the downside, break of 159.75 resistance turned support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish even in case of deep pullback.

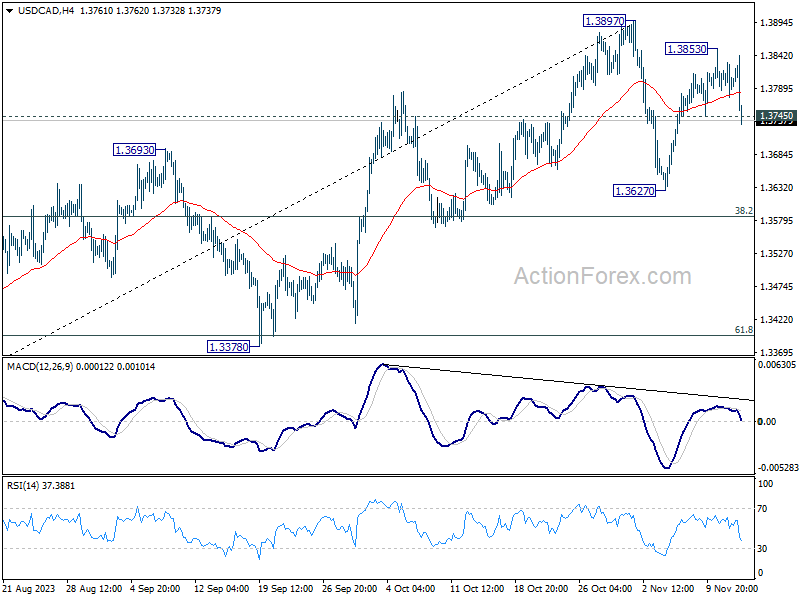

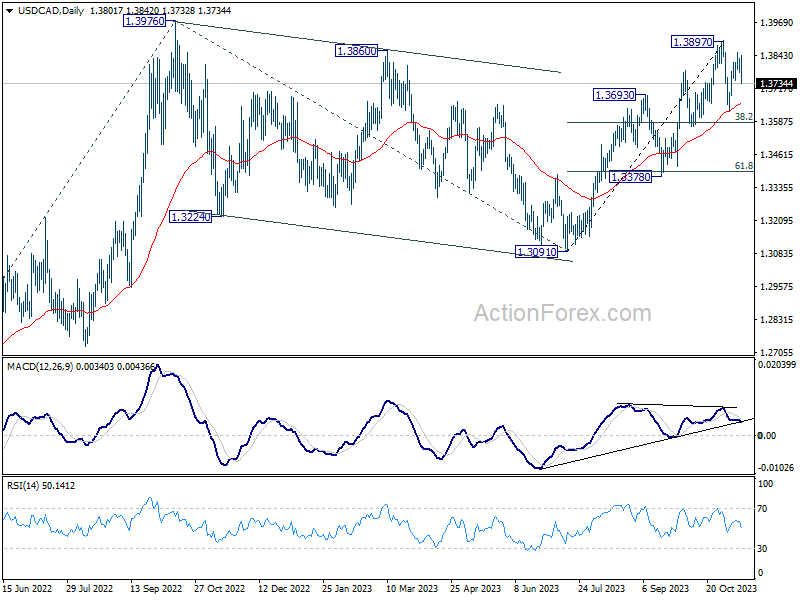

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3779; (P) 1.3805; (R1) 1.3834; More...

Break of 1.3745 minor support suggests that USD/CAD's rebound from 1.3627 has completed at 1.3853 already. Intraday bias is back on the downside for 1.3627 support and possibly below, to extend the corrective pattern from 1.3897. Strong support should be seen from 38.2% retracement of 1.3091 to 1.3897 at 1.3589 to bring rebound. On the upside, above 1.3853 will bring retest of 1.3897 instead.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will remain the favored case as long as 1.3378 support holds.

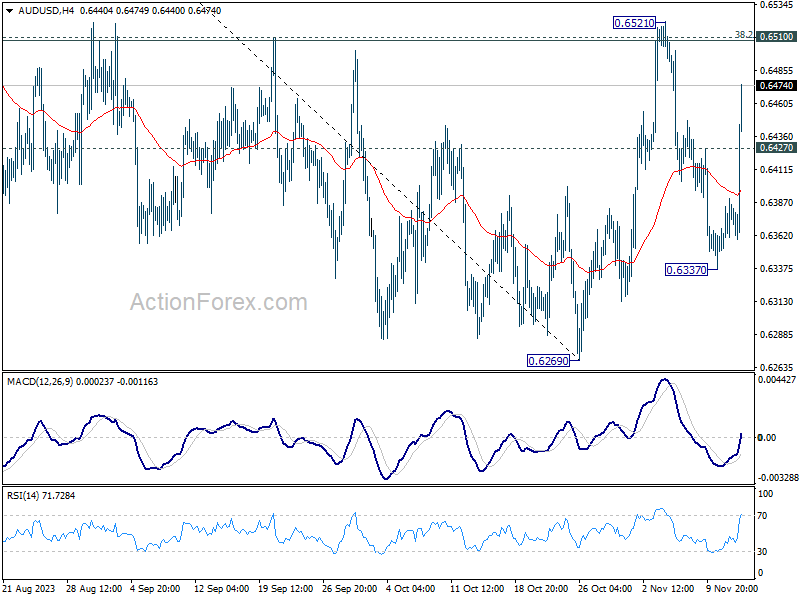

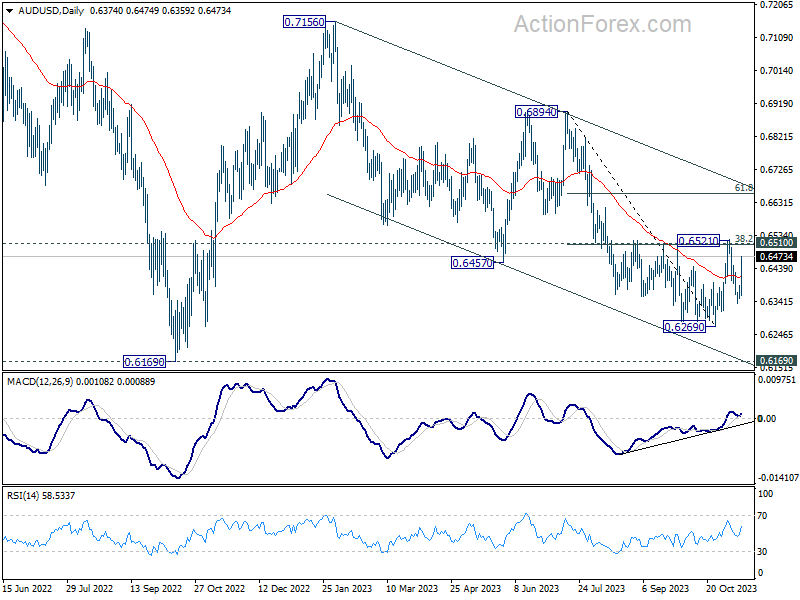

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6355; (P) 0.6374; (R1) 0.6395; More...

Break of 0.6247 minor resistance argues that AUD/USD's pull back from 0.6521 has completed at 0.6337 already. Intraday bias is back on the upside for 0.6510 cluster resistance (38.2% retracement of 0.6894 to 0.6269 at 0.6508). Decisive break there will carry larger bullish implication and turn outlook bullish. Nevertheless, break of 0.6337 will bring retest of 0.6269 support instead.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of the corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

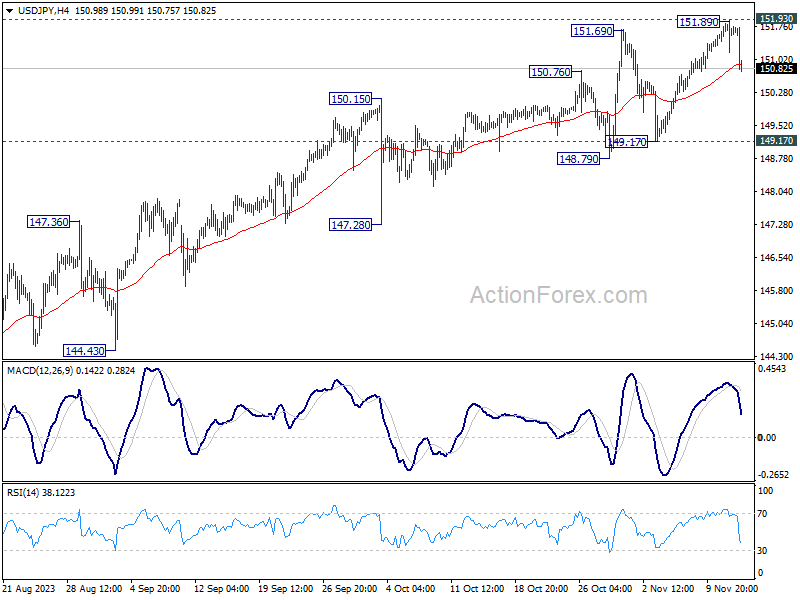

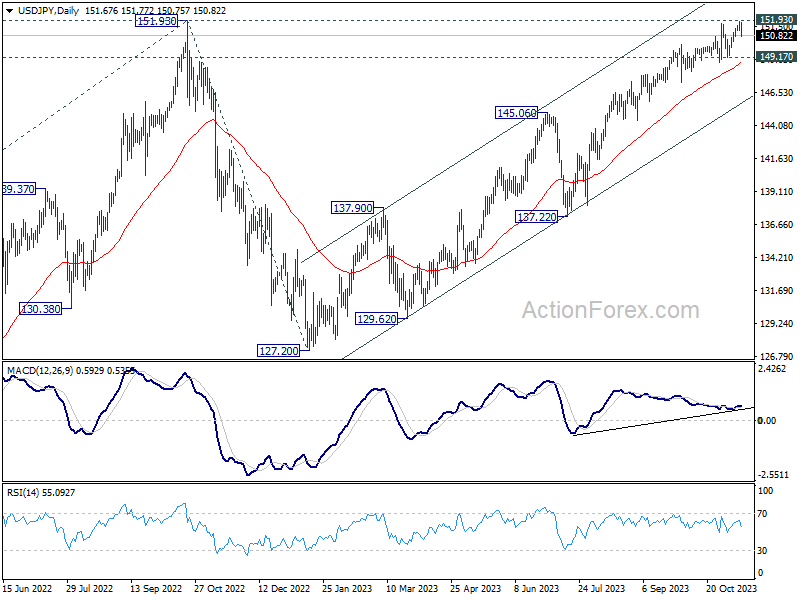

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.31; (P) 151.61; (R1) 152.02; More...

While USD/JPY dips notably, it's holding well above 149.17 support. Intraday bias remains neutral at this point, and another rally is in favor. On the upside, decisive break of 151.93 resistance will confirm resumption of long term up trend. Next target will be 157.69 projection level. However, firm break of 149.17 will be a sign of bearish reversal and bring deeper fall to 147.28 support first.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 (2021 low) to 151.93 from 127.20 at 157.69.

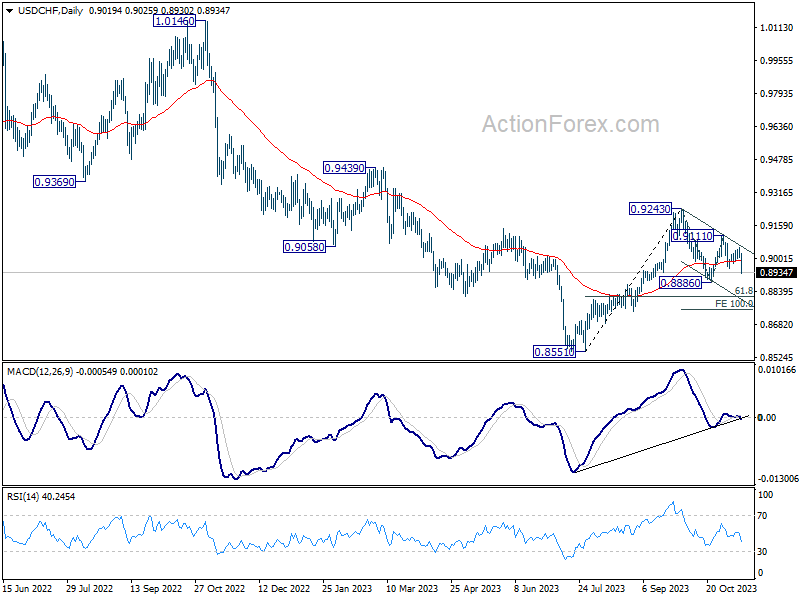

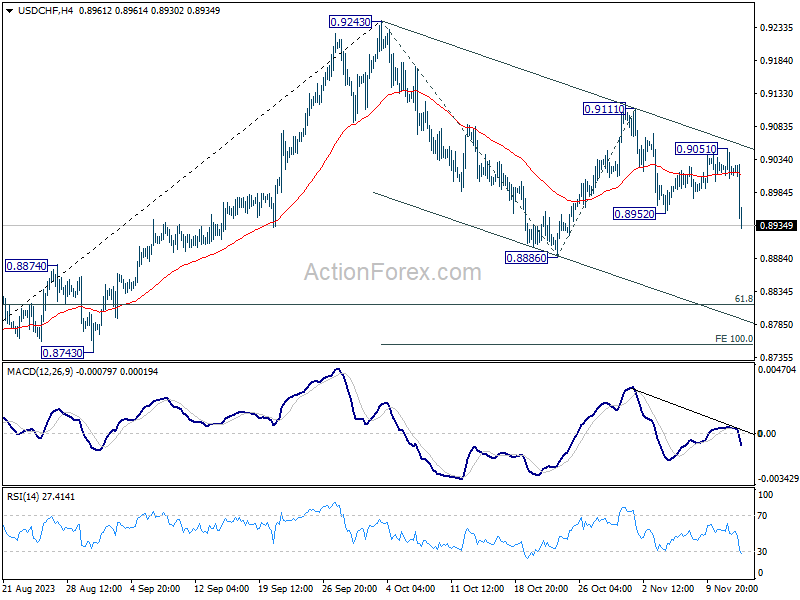

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8998; (P) 0.9025; (R1) 0.9044; More....

Break of 0.8952 support indicates resumption of fall from 0.9111. Intraday bias is back on the downside for 0.8886 support first. Firm break there will also resume the whole decline from 0.9243, and target 100% projection of 0.9243 to 0.8886 from 0.9111 at 0.8754. For now, risk will stay on the downside as long as 0.9051 resistance holds, in case of recovery.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.