Sample Category Title

UK payrolled employment rose 33k in Oct, unemployment rate unchanged at 4.2% in Sep

UK payrolled employment rose 33k, or 0.1% mom in October. Over the year, payrolled employment rate 398k or 1.3% yoy. Median monthly pay rose 5.9% yoy, down from prior month's 6.0% yoy. Claimant count rose 17.8k, above expectation of 15.0k.

In the three months to September, unemployment rate was unchanged at 4.2%, matched expectations. Average earnings including bonus rose 7.9% yoy, above expectation of 7.4%, slowed from prior 8.2%. Average earnings excluding bonus rose 7.7% yoy, matched expectations, slowed from prior month's 7.8%.

Key Inflation Data Due in the US and Sweden

Market movers today

US CPI for October is the highlight of this week in terms of data releases. We expect headline at 0.1 m/m and core at 0.3% m/m in line with consensus but with uncertainty coming from the auto worker's strike which might have temporarily raised car prices, as well as from technical factors related to the calculation of health insurance premiums. If there is an upside surprise related to those issues, the market should see through it.

In Sweden the October inflation numbers will be released at 8:00 CET. We expect a slight uptick in CPIF inflation to 4.5% YoY (from 4% in September), and a decrease in CPIF excl. energy to 6.3% YoY (from 6.9% in September). Looking at the Riksbank's latest forecast, their trajectory shows a 0.4 percentage point lower CPIF YoY estimate and CPIF excl. Energy print that is some 0.3 p.p YoY below our own forecast. We judge today's outcome to potentially be decisive for next week's policy decision by the Riksbank. We judge our call for an unchanged policy rate by the Riksbank next week to remain in play, should today's inflation outcome be in line (or below) our own forecast.

German ZEW increased more than expected in October which, together with the IFO survey, gave a small ray of hope for the German economy, so it could be interesting to see today's November figure. Second release today of euro area GDP, but still without details.

In the UK, we get the labour market report where focus will be on developments in wage growth, which has remained stubbornly elevated the past months, while the data on unemployment and employment continues to be published on an experimental basis given the poor data quality.

We get Chinese industrial production, retail sales and home sales early Wednesday morning. Especially home sales will be interesting but retail sales as well. Service PMI was soft in October so expectations are pretty low. We might also get a Chinese rate cut Wednesday.

Japanese Q3 GDP growth also early Wednesday will likely print close to zero as foreign demand has slowed.

The 60 second overview

Markets. It has been a quiet start to the week amid markets awaiting key data releases in not least today's US CPI print. European equities have generally outperformed peers, yields and the USD are little changed and commodity prices are generally a little higher to start the week.

US inflation expectations. Yesterday's release of New York Fed inflation expectations was a slight source of relief for markets following last week's surprise rise in the University of Michigan motheasure. B the 1Y and 5Y inflation expectations declined in the New York Fed measure to 3.57% and 2.72%, respectively.

Oil prices. After a series of weekly declines the oil price has rebounded somewhat since the bottom last Wednesday completing a four day consecutive rally - the longest rally in two months. Brent crude is now back close to the USD 83/bbl mark after having traded below USD 80/bbl last week. While it is difficult to pinpoint one single driver it does seem a slight improvement to the cyclical mood in markets alongside some hawkish OPEC comments have contributed to the rise.

UK politics. Yesterday, UK Prime Minister Rishi Sunak reshuffled his Cabinet ahead of the Autumn Statement, which is scheduled for 23 November. As expected, Chancellor Jeremy Hunt remains in place but in a more surprising move, former PM David Cameron was appointed foreign secretary. While the return of the former PM is not expected to be universally popular, his significant international standing is valuable with the Conservatives firmly behind in the polls. At present, Labour is set to win by a majority in the next general election, which is due to be held by January 2025 at the latest.

Equities: Equities were in wait-and-see mode yesterday ahead of the US inflation release today. Market movers were few, leaving US equities struggling for direction while Europe rose about 1% in a catch-up move from Friday. Little differences between sectors or styles in a classic wait-and-see manner but if any a slight preference for defensive momentum. Hesitancy continues this morning with US futures unchanged.

FI: It was a trading session with very limited volatility, while markets await today's US CPI release. 10y Bunds ended virtually unchanged at the 2.71%, where it started the day. The European curves twist-flattens as the short end ended higher 2bp while the long end ended by a similar amount lower.

FX: It has been a quiet start to the week in global markets including FX. Yesterday's session saw very limited moves with most notably NOK and SEK enjoying green equity markets and a move higher in oil prices as we head into this morning's Swedish CPI release.

Credit: Credit markets were in wait-and-see mode ahead of the important US inflation data release today. The tilt was, however, slightly risk seeking, with Itrax Main tightening 1.2bp to close at 74.4bp, while Itrax Xover tightened 5.2bp to close at 405.6bp. Primary markets were fairly active in both financials and corporates, with among others, S-Bank and Heidelberg materials, launching EUR bench-mark deals.

Inflation Jitters and Rate Cut Riddles

Investors are on the edge of their seats, waiting for the latest scoop on US inflation data to take a fresh direction in both stock and bond markets. The dollar index remains offered, the US political risks are casting shadows, and there's a rising chorus of opinions playing the guessing game on when and how much the Fed might trim the rates next year.

The S&P500 consolidated on Monday after a 7.5% rally since end of October, while Nasdaq 100 eased 0.30% following an almost 10% rally. The US 10-year yield steadied a touch above the 4.60% level.

According to the consensus of analysts on a Bloomberg survey, the US inflation may have slowed to 3.3% last month, from 3.7% printed a month earlier. Core inflation is seen unchanged at 4.1%. The waning supply chain disruptions, the loosening US jobs market, a further fall in gasoline prices and the expectation of a decline in rents are among the major factors that could help inflation ease – after a more than 1.5-year aggressive policy tightening from the Fed of course.

But not all indicators are in green. An uptick in health insurance costs could give a slight boost to October inflation figures, while the latest US consumer survey, released last Friday, showed that the US consumers expect inflation to climb at an annual rate of 3.2% over the next 5 to 10 years. In contrast, economists see inflation fall to 2.5% in the next five years and down to 2.2% in the next 5 to 10 years, and the bond prices imply a CPI of 2.36% in the period of 5 to 10 years from now.

For today, an inflation read in line with expectations, or ideally softer than expected, should give further support to the Federal Reserve (Fed) doves, cement the idea that the Fed is done hiking the interest rates and boost the rate cut expectations for next year. A read above expectations should bring Fed hawks back to the market and increase the bets of a rate hike in December. But activity on Fed funds futures gives around 85% chance for a no rate hike in the Fed’s December meeting, and the inflation numbers must look very bad to reverse that expectation.

And anyway, what investors are interested in right now is not whether the Fed will hike one more time or not – because they are convinced that it won’t. Instead, what everyone is trying to figure out right now is: when will the Fed start cutting rates, and by how much will it cut rates next year. Goldman Sachs doesn’t expect a rate cut from the Fed until this time next year. Morgan forecasts two deep rate cuts next year starting from June, and UBS’ Investment Bank anticipates the first rate cut as early as in March and a 275bp cut in 2024.

If inflation continues to ease and the US jobs market and the economy starts slowing – which is our base case scenario for the next 12 months – the Fed should start lowering rates. But given how reactive the Fed has been to mounting inflation, the rate cuts shouldn’t start before September, but when they start the loosening should be rapid.

Ceteris paribus, the US 2-year yield should hover around the 5% mark, the 10-year yield will remain appetizing approaching the 5% mark – and could hardly go above this level unless there is an economic shock, or a political turmoil, and a potential rating downgrade.

The US dollar index remains offered at the 50-DMA and could further extend losses with the sight of a sufficiently soft inflation report, while the USDJPY was sold near the 152 level. There are different rumours regarding the nature of the sudden jump in the yen on Monday. It could be a direct FX intervention, or it could be the result of options positioning. But in both cases, selling the yen at the current levels means taking the risk of a sudden reversal, either because of a broadly softer US dollar, or because of a direct intervention.

Technical Outlook and Review

DXY:

The DXY chart currently has a bearish overall momentum, suggesting the potential for a bearish continuation towards the 1st support level.

1st support at 105.40 is identified as an overlap support, and it also coincides with the 50% Fibonacci Retracement level. This level indicates that there could be a significant level of support, and traders may expect the price to find buying interest or a pause in the bearish movement around this area.

The 2nd support at 104.95 is considered a multi-swing low support, further reinforcing its potential as a support level. Multi-swing lows often indicate areas where buyers have stepped in previously, making it a relevant support level.

On the resistance side, the 1st resistance at 105.95 is categorized as an overlap resistance and also coincides with the 50% Fibonacci Retracement level. This level suggests that there could be selling interest in this area, potentially acting as a barrier to further upward movement.

The 2nd resistance at 106.46 is noted as a pullback resistance, indicating another potential level where the price may encounter selling pressure during its bearish continuation.

EUR/USD:

The EUR/USD chart currently has a bearish overall momentum, suggesting the potential for a bearish reaction off the 1st resistance level and a drop towards the 1st support.

1st support at 1.0664 is identified as an overlap support, and it also coincides with the 38.20% Fibonacci Retracement level. This level suggests that there could be a significant level of support, and traders may expect the price to find buying interest or a pause in the bearish movement around this area.

The 2nd support at 1.0606 is considered a pullback support and coincides with the 61.80% Fibonacci Retracement level. This level reinforces its potential as a support level. Fibonacci retracement levels are often watched by traders for potential reversal points.

On the resistance side, the 1st resistance at 1.0712 is categorized as a multi-swing high resistance. This level indicates that there could be selling interest in this area, potentially acting as a barrier to further upward movement.

The 2nd resistance at 1.0758 is also noted as a multi-swing high resistance, adding to the potential areas where the price might find resistance during its bearish reaction.

EUR/JPY:

The EUR/JPY chart currently suggests a bearish momentum, indicating a potential bearish reaction off the first resistance at 162.33, with a subsequent drop towards the first support at 161.73.

The first support at 161.73 is identified as a pullback support, indicating a level where the price might find some buying interest. Additionally, the second support at 160.99 is recognized as another pullback support, reinforcing the potential strength of the support zone.

On the resistance side, the first resistance at 162.33 represents a point of multi-swing high resistance, marking a crucial level where the price might face selling pressure. Furthermore, the second resistance at 162.86 is characterized as a swing high resistance, suggesting another level where the price might encounter obstacles within its downward movement.

EUR/GBP:

The EUR/GBP chart currently demonstrates a bullish momentum, suggesting a potential bullish bounce off the first support at 0.8713, with the potential to head towards the first resistance at 0.8730.

The first support at 0.8713 is identified as a swing low support, providing a foundational level for potential price rebounds. Additionally, the second support at 0.8697 is recognized as a multi-swing low support, reinforcing the potential strength of the support zone.

On the resistance side, the first resistance at 0.8730 represents a point of pullback resistance, coinciding with the 50% Fibonacci Retracement level. Furthermore, the second resistance at 0.8746 is identified as a multi-swing high resistance, demonstrating Fibonacci confluence with the 78.60% Fibonacci Retracement and the 61.80% Fibonacci Projection. This indicates a significant potential hurdle for the price and reinforces the importance of this resistance level.

GBP/USD:

The GBP/USD chart currently has a bullish overall momentum, suggesting the potential for a bullish continuation towards the 1st resistance.

1st support at 1.2214 is identified as an overlap support, and it also coincides with the 61.80% Fibonacci Retracement level. This level suggests that there could be a significant level of support, and traders may expect the price to find buying interest or a pause in the bullish movement around this area.

The 2nd support at 1.2104 is considered a multi-swing low support, further reinforcing its potential as a support level. Multiple swing lows indicate an area where buyers have previously stepped in, making it a significant support zone.

On the resistance side, the 1st resistance at 1.2303 is categorized as a multi-swing high resistance. This level coincides with the 50% Fibonacci Retracement level, which adds to its significance. This area may act as a barrier to further upward movement, where sellers could be active.

The 2nd resistance at 1.2400 is noted as a swing high resistance, indicating another potential level where the price may encounter obstacles in its upward movement.

GBP/JPY:

The GBP/JPY chart currently exhibits a bullish momentum, suggesting a potential bullish continuation towards the first resistance at 186.63.

The first support at 185.77 is identified as a pullback support, providing a potential foundation for the price to bounce higher. Additionally, the second support at 184.64 is recognized as a multi-swing low support, further reinforcing the potential strength of the support zone.

On the upside, the first resistance at 186.63 represents a point of swing high resistance, indicating a significant level where the price might face resistance or potential reversals within its upward movement. This level is crucial for traders to monitor as it could influence the continuation of the bullish trend.

USD/CHF:

The USD/CHF chart exhibits a bearish overall momentum, indicating the potential for a continuation of the bearish trend. Here are the key levels to watch:

1st support at 0.8982: This level is considered an overlap support, which means it has previously acted as a support level and could attract buying interest or act as a barrier to further downside.

2nd support at 0.8945: This support level gains significance as it coincides with the 78.60% Fibonacci Retracement level. Fibonacci retracement levels often act as potential reversal or support levels in the market.

1st resistance at 0.9041: This level is categorized as a multi-swing high resistance, indicating that it has historically been a point where price faced selling pressure and reversed lower.

2nd resistance at 0.9070: This is an overlap resistance, suggesting it has previously served as a resistance level and could continue to do so.

Intermediate support at 0.9006: This level is identified as an overlap support, adding to its potential significance as a support zone.

USD/JPY:

The USD/JPY chart currently shows a bullish overall momentum, indicating the potential for further upside movement. Here are the key levels to watch:

1st support at 150.54: This level is considered a pullback support, suggesting that it has previously acted as a level where buyers stepped in. It could provide a base for price to bounce higher.

2nd support at 149.83: This is another pullback support, indicating that it has historical significance as a level of buying interest.

1st resistance at 151.71: This level is categorized as a swing high resistance, which means it has previously acted as a barrier to further upside movement.

2nd resistance at 152.42: This resistance level is significant as it aligns with the 127.20% Fibonacci Extension, suggesting it could act as a strong barrier to price advancement.

USD/CAD:

The USD/CAD chart currently shows a bearish overall momentum, indicating the potential for further downside movement. Here are the key levels to watch:

1st support at 1.3739: This level is considered an overlap support and aligns with the 50% Fibonacci Retracement, suggesting that it has previously acted as a level where buyers entered the market. It could provide a base for price to potentially bounce higher.

2nd support at 1.3640: This is a swing low support, indicating historical significance as a level of buying interest.

1st resistance at 1.3823: This level is categorized as a multi-swing high resistance, which means it has previously acted as a barrier to further upside movement.

2nd resistance at 1.3870: This resistance level is significant as it aligns with a pullback resistance, suggesting it could act as a strong barrier to price advancement.

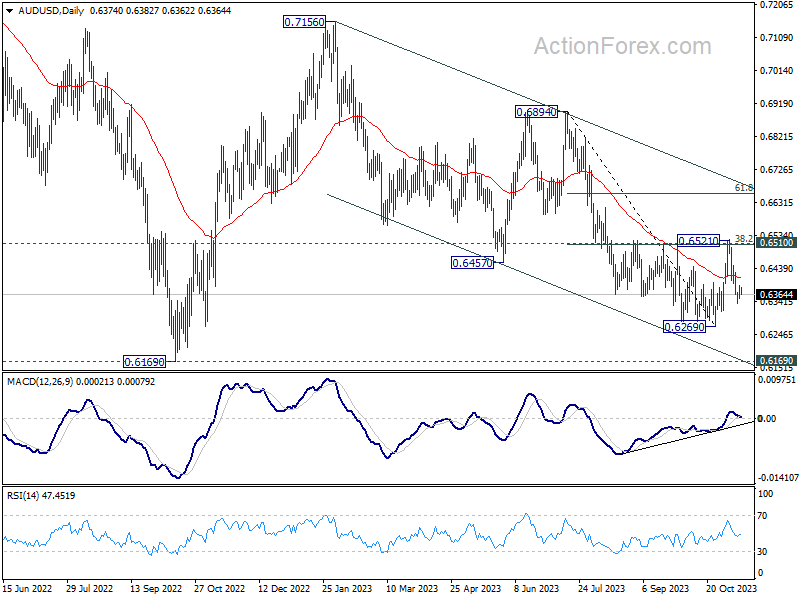

AUD/USD:

The AUD/USD chart currently exhibits a bearish overall momentum, suggesting the potential for further downward movement. Here are the key levels to watch:

1st support at 0.6324: This level is considered an overlap support and coincides with the 78.60% Fibonacci Retracement. It indicates a historical level where buyers have previously stepped in, potentially providing support and causing a bounce.

2nd support at 0.6275: This level is a swing low support, indicating its historical significance as a level of buying interest.

1st resistance at 0.6392: This level is categorized as an overlap resistance and may act as a barrier to further upside movement.

2nd resistance at 0.6436: This resistance level aligns with a 50% Fibonacci Retracement, suggesting that it could serve as a strong resistance level.

NZD/USD

The NZD/USD chart currently exhibits a bullish overall momentum, suggesting the potential for further upward movement. Here are the key levels to watch:

1st support at 0.5860: This support level is considered a pullback support and coincides with the 61.80% Fibonacci Retracement, indicating a historical level where buyers have previously stepped in. It suggests potential support and a possible bounce from this level.

2nd support at 0.5798: This level is categorized as a swing low support, signifying its historical significance as a level of buying interest.

1st resistance at 0.5919: This resistance level is considered a pullback resistance and may act as a barrier to further upside movement.

2nd resistance at 0.5941: This resistance level aligns with a multi-swing high resistance, indicating its potential strength as a barrier to further bullish movement.

DJ30:

The DJ30 chart is currently showing a bearish momentum, indicating a potential bearish continuation towards the first support level at 34195.24. This support is particularly significant as it is an overlap support, demonstrating Fibonacci confluence with both the 61.80% Fibonacci Projection and the 38.20% Fibonacci Retracement.

Additionally, the second support at 33866.72 is identified as another overlap support, further reinforcing the potential strength of this support zone.

On the resistance side, the first resistance at 34392.35 is recognized as an overlap resistance, suggesting a potential area where the price might face hurdles or reversals within its downward movement. Furthermore, the second resistance at 34726.35 is marked as a swing high resistance, indicating another level of significance where the price might encounter resistance.

GER40:

The GER40 chart is currently displaying a bearish momentum, suggesting a potential bearish reaction off the first resistance level at 15361.30, with a subsequent drop towards the first support at 15253.40. This support level is significant as it represents a multi-swing low support, and it aligns with the 61.80% Fibonacci Retracement and the 61.80% Fibonacci Projection, indicating a strong area of potential support.

Furthermore, the second support at 15174.70 is identified as an overlap support, adding to the potential strength of the support zone.

On the resistance side, the first resistance at 15361.30 is noted as an overlap resistance, suggesting a crucial point where the price might face resistance or a potential reversal. Additionally, the second resistance at 15424.50 is recognized as another overlap resistance, emphasizing its significance as a level where the price might encounter obstacles within its downward movement.

US500

The US500 chart is currently indicating a bearish momentum, suggesting a potential bearish reaction off the first resistance level at 4414.4, leading to a drop towards the first support at 4394.7. This support is identified as an overlap support, coinciding with the 38.20% Fibonacci Retracement, indicating a significant area for potential price support.

Additionally, the second support at 4369.9 is noted as a pullback support, associated with the 61.80% Fibonacci Retracement level, further strengthening its potential as a crucial support zone.

On the resistance side, the first resistance at 4414.4 represents a point of multi-swing high resistance, indicating a significant hurdle for the price. Furthermore, the second resistance at 4436.3 is characterized as a pullback resistance, marking another level where the price might face resistance within its downward movement.

BTC/USD:

The BTC/USD chart is currently exhibiting a bullish momentum, with one of the contributing factors being that the price is above the bullish Ichimoku cloud. There’s a potential scenario where the price could make a bullish bounce off the first support level at 36367, which is identified as a multi-swing low support, and subsequently head towards the first resistance at 37197.

The second support at 35628 is recognized as a pullback support, adding to the potential strength of the support zone. On the resistance side, the first resistance at 37197 represents a point of multi-swing high resistance, indicating a significant level where the price might face hurdles. Additionally, the second resistance at 37987 is characterized by its significance as a swing high resistance, marking another potential level where the price might encounter resistance within its upward movement.

ETH/USD:

The ETH/USD chart currently displays a bullish momentum, with one of the contributing factors being that the price is above the bullish Ichimoku cloud. There’s a potential scenario where the price could make a bullish bounce off the first support level at 2037.29, identified as a pullback support, and subsequently head towards the first resistance at 2129.57.

The second support at 1906.05 is also noted as a pullback support, reinforcing the potential strength of the support zone. On the resistance side, the first resistance at 2129.57 represents a point of multi-swing high resistance, indicating a significant level where the price might encounter hurdles or reversals within its upward movement.

WTI/USD:

The WTI (West Texas Intermediate) chart currently shows a bullish overall momentum, suggesting the potential for further upward movement. Here are the key levels to watch:

1st support at 78.09: This support level is considered a pullback support, indicating a historical level where buyers have previously stepped in. It suggests potential support and a possible bounce from this level.

2nd support at 75.34: This level is categorized as a swing low support, signifying its historical significance as a level of buying interest.

1st resistance at 80.05: This resistance level is considered a pullback resistance and may act as a barrier to further upside movement.

2nd resistance at 83.01: This resistance level is categorized as an overlap resistance, suggesting potential strength as a barrier to further bullish movement.

XAU/USD (GOLD):

The XAUUSD (Gold/USD), the overall momentum on the chart is currently bearish. Here are the key support and resistance levels to watch:

1st support at 1932.61: This support level is considered significant as it aligns with an overlap support and the 38.20% Fibonacci retracement level. It may act as a potential area for price to find support.

2nd support at 1904.32: This support level is also notable, as it corresponds to an overlap support and the 50% Fibonacci retracement level.

1st resistance at 1946.32: This resistance level is categorized as an overlap resistance, suggesting it could serve as a barrier to upward movement.

2nd resistance at 1964.32: Similar to the 1st resistance, this level is an overlap resistance and may also act as a significant barrier.

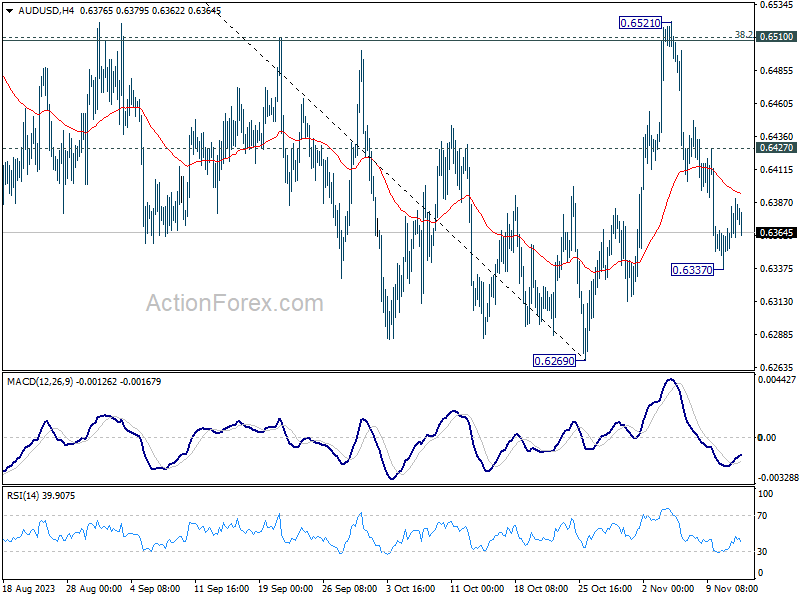

AUD/USD Daily Report

Daily Pivots: (S1) 0.6355; (P) 0.6374; (R1) 0.6395; More...

Intraday bias in AUD/USD is turned neutral first with current recovery. Some consolidations could be seen above 0.6337 temporary low. But deeper decline is expected as long as 0.6427 resistance holds. Below 0.6337 will resume the fall from 0.6521 and target 0.6269 support next. Firm break there will resume larger fall from 0.7156, to retest 0.6169 low. Nevertheless, above 0.6427 will bring stronger rebound back to 0.6510 cluster resistance (38.2% retracement of 0.6894 to 0.6269 at 0.6508).

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of a corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

US CPI to Dictate Dollar’s Path, GBP/JPY Poised Ahead of UK Employment Figure

The financial markets are intently focused on the upcoming US CPI report, a key indicator that could influence Fed's next steps. Expectations are leaning towards further slowdown in headline inflation to 3.3%, while core inflation rate is projected to remain steady at 4.1%. However, there's a growing consensus among economists about the potential for upside risks in this data release, especially concerning slower goods disinflation and stubborn shelter inflation.

Given Fed Chair Jerome Powell's recent admission of lacking confidence in the effectiveness of the current monetary policy to bring inflation back to target, any deviation above the forecast in today's CPI data could solidify the rationale for additional rate hikes. Presently, the likelihood of a rate increase in December is pegged at 14.3%, with January's odds slightly higher at 26.7%, according to fed funds futures.

A stronger-than-anticipated inflation report could trigger a surge in Dollar, not only by raising the probability of a Fed hike but also through inducing a wave of risk aversion in the markets.

As for currency performance this week so far, New Zealand Dollar emerges as the weakest for now, closely followed by the Canadian Dollar and Yen. Sterling stands out as the strongest, but upcoming UK job data and CPI figures will be crucial tests. Australian Dollar and Euro are showing strength too, yet they appear increasingly vulnerable. Dollar, in the meantime, remains in a state of flux, awaiting decisive cues from CPI data.

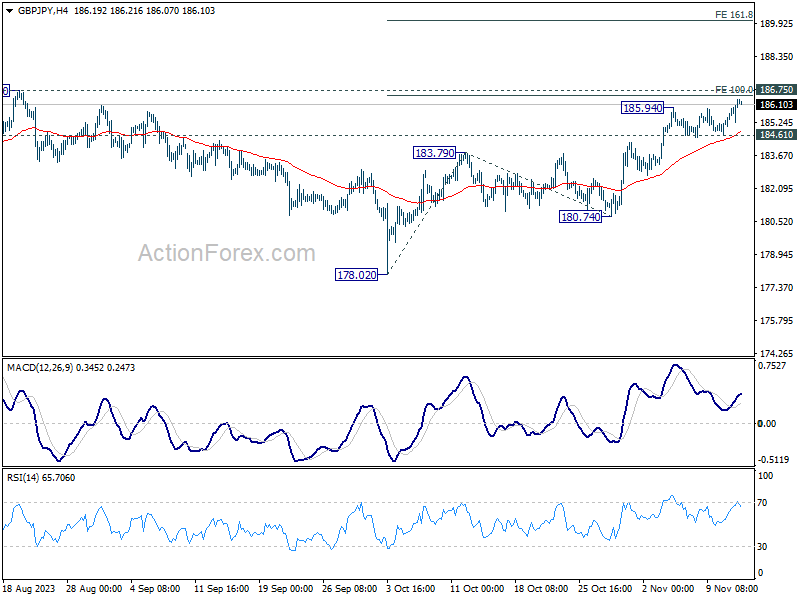

Technically, GBP/JPY's rally from 178.02 resumed by breaking through 185.94 resistance yesterday. Further rise is now expected as long as 184.61 support holds. Immediate focus is now on 186.75 resistance. Decisive break there will confirm larger up trend resumption. Next near term target will be 161.8% projection of 178.02 to 183.79 from 180.74 at 190.07.

In Asia, at the time of writing, Nikkei is up 0.45%. Hong Kong HSI is down -0.12%. China Shanghai SSE is up 0.07%. Singapore Strait Times is down -0.40%. Japan 10-year JGB yield is down -0.0172 at 0.859. Overnight, DOW rose 0.16%. S&P 500 dropped -0.08%. NASDAQ dropped -0.22%. 10-year yield rose 0.004 to 4.632.

Japan's Suzuki emphasizes balancing positives and negatives of weak Yen

As Japanese Yen continues to hover near multi-decade lows against Dollar after yesterday's selloff, Japan's Finance Minister Shunichi Suzuki reiterated the government's commitment to addressing the currency's movements. In his latest remarks, Suzuki avoided any direct mention of intervening in the currency markets, focusing instead on a strategy to balance the impact of the Yen's weakness.

Suzuki stated, "What's important is to maximize positive effects from the weak yen while mitigating negatives." His comments come as the Japanese government faces the challenges of managing economic implications of Yen's prolonged decline. While a weaker Yen can benefit Japan's export-driven economy, it also raises concerns about increased import costs, especially in the context of global inflationary pressures.

Suzuki's emphasis on maximizing the benefits and reducing the drawbacks of the weak Yen highlights the delicate balancing act the Japanese authorities must perform in the current economic environment. His statement suggests a cautious approach from the government, possibly hinting at measured responses rather than abrupt market interventions.

Australia's consumer sentiment plummets post RBA rate hike

Australia's Westpac Consumer Sentiment Index saw a significant decline in November, dropping by -2.6% mom to 79.9, reflecting a deepening pessimism among consumers.

Westpac attributed this drop to the recent RBA rate hike, noting a -6% decrease in confidence during the survey period. Despite the overarching pessimism, labor market confidence and housing-related sentiment remained relatively stable.

Westpac further commented, "The Reserve Bank Board next meets on December 5. The November Consumer Sentiment survey highlights the weak and uneven conditions across Australia's consumer sector. How this plays out for wider domestic demand in the context of strong population growth is something the Board will need to consider as it acts to ensure inflation returns to target."

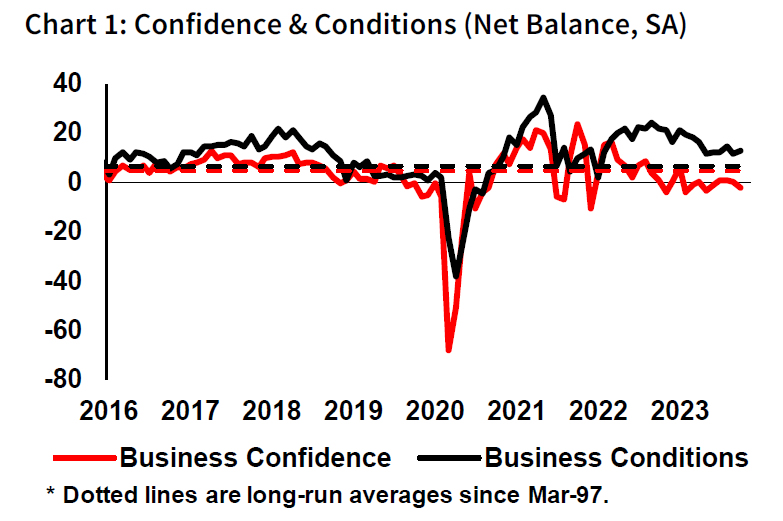

Australia NAB business confidence dips to -2, conditions resilient

In Australia, NAB reported a dip in Business Confidence for October, falling from 0 to -2. However, Business Conditions saw a slight improvement, rising from 12 to 13. Notably, trading conditions increased from 18 to 20, and profitability conditions improved from 9 to 12, while employment conditions slightly decreased from 9 to 8.

NAB Chief Economist Alan Oster commented, "Business conditions remain healthy, picking up in October and still well above average. Still, business confidence remained soft in the month, still well below average at -2 index points." He highlighted the persistent gap of 10-15 index points between current conditions and the more forward-looking confidence indicator, emphasizing that "Businesses clearly remain cautious about the outlook for the economy despite the resilience we are seeing."

The report also noted a slowdown in price and cost growth. Labour cost growth eased to 1.8% in quarterly equivalent terms, and purchase cost growth declined to 1.8%. Retail price growth remained stable at 1.9%, while overall price growth eased to 1.0%, marking the slowest rate since July 2020.

Oster added, "The Q3 CPI showed inflation had been persistent through the middle of the year and the survey suggests this remained the case heading into Q4. We still expect to see gradual moderation over time but it will be a protracted process, especially given the resilience of domestic demand thus far."

Looking ahead

UK employment, Swiss PPI, Eurozone GDP revision and German ZEW economic sentiment are the main focuses in European session. Later in the day, US CPI is the highlight.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6355; (P) 0.6374; (R1) 0.6395; More...

Intraday bias in AUD/USD is turned neutral first with current recovery. Some consolidations could be seen above 0.6337 temporary low. But deeper decline is expected as long as 0.6427 resistance holds. Below 0.6337 will resume the fall from 0.6521 and target 0.6269 support next. Firm break there will resume larger fall from 0.7156, to retest 0.6169 low. Nevertheless, above 0.6427 will bring stronger rebound back to 0.6510 cluster resistance (38.2% retracement of 0.6894 to 0.6269 at 0.6508).

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of a corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Nov | -2.60% | 2.90% | ||

| 00:30 | AUD | NAB Business Conditions Oct | 13 | 11 | 12 | |

| 00:30 | AUD | NAB Business Confidence Oct | -2 | 1 | 0 | |

| 07:00 | GBP | Claimant Count Change Oct | 15.0K | 20.4K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Sep | 4.20% | 4.20% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Sep | 7.40% | 8.10% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Sep | 7.70% | 7.80% | ||

| 07:30 | CHF | Producer and Import Prices M/M Oct | 0.10% | -0.10% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Oct | -1.00% | |||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | -0.10% | -0.10% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 P | 0.20% | 0.20% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Nov | 4.9 | -1.1 | ||

| 10:00 | EUR | Germany ZEW Current Situation Nov | -75.5 | -79.9 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | 6.1 | 2.3 | ||

| 13:30 | USD | CPI M/M Oct | 0.10% | 0.40% | ||

| 13:30 | USD | CPI Y/Y Oct | 3.30% | 3.70% | ||

| 13:30 | USD | CPI Core M/M Oct | 0.30% | 0.30% | ||

| 13:30 | USD | CPI Core Y/Y Oct | 4.10% | 4.10% |

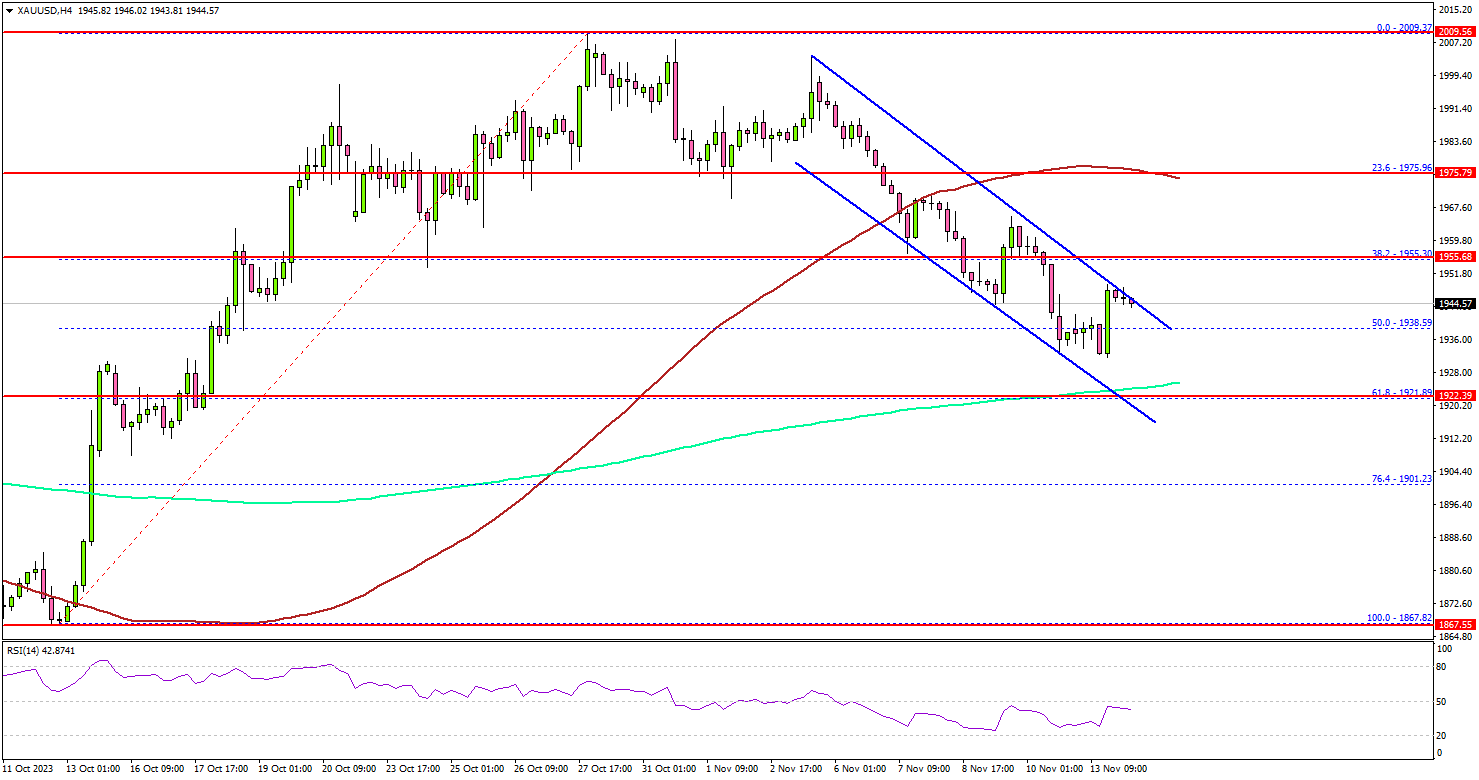

Gold Price Starts Correction, US CPI Next

Key Highlights

- Gold prices started a downside correction from the $2,010 zone.

- A major declining channel is forming with resistance near $1,945 on the 4-hour chart.

- Crude oil prices are attempting a recovery wave from the $75.00 zone.

- The US Consumer Price Index could decline from 3.7% to 3.3% in Oct 2023 (YoY).

Gold Price Technical Analysis

Gold rallied further and surpassed the $2,000 level amid the ongoing Israeli–Hamas war. The price traded as high as $2,009 before the bears appeared.

The 4-hour chart of XAU/USD indicates that the price started a downside correction below the $2,000 level. There was a drop below the $1,980 level and the 100 Simple Moving Average (red, 4 hours).

The price spiked below the 50% Fib retracement level of the upward move from the $1,867 swing low to the $2,009 high. The price is now consolidating near the $1,945 zone. There is also a major declining channel forming with resistance near $1,945 on the same chart.

Immediate resistance is near the $1,945 level. The first major resistance is $1,955. An upside break above the $1,955 level could send the price soaring toward the $1,965 resistance. The next major resistance is near the $1,972 level, above which Gold could test $1,985.

On the downside, the first major support is near the $1,938 level. The main support sits near the $1,920 level and the 200 Simple Moving Average (green, 4 hours). It is close to the 61.8% Fib retracement level of the upward move from the $1,867 swing low to the $2,009 high. Any more losses might call for a move toward the $1,900 level.

Looking at crude oil prices, the bulls appeared near the $75 zone and the price is now attempting a recovery wave.

Economic Releases to Watch Today

- UK Claimant Count Change for Oct 2023 – Forecast 3.0K, versus 20.4K previous.

- UK ILO Unemployment Rate Feb 2023 (3M) – Forecast 4.2%, versus 4.2% previous.

- Euro Zone Gross Domestic Product for Q3 2023 (Prelim) (QoQ) - Forecast -0.1%, versus -0.1% previous.

- US Consumer Price Index for Oct 2023 (MoM) – Forecast +0.1%, versus +0.4% previous.

- US Consumer Price Index for Oct 2023 (YoY) – Forecast +3.3%, versus +3.7% previous.

Silver (XAGUSD) Ended Correction and Turned Higher

Silver (XAGUSD) cycle from 10.3.2023 low is in progress as an impulse. Up from 10.3.2023 low, wave (1) ended at 23.69 and pullback in wave (2) is proposed complete at 21.86. Down from wave (1), wave W ended at 22.52 and rally in wave X ended at 23.3. Internal subdivision of wave X unfolded as a zigzag structure. Up from wave W, wave ((a)) ended at 23.12, wave ((b)) ended at 22.57, and wave ((c)) ended at 23.3. This completed wave X in higher degree.

The metal then extended lower in wave Y. Down from wave X, wave ((a)) ended at 22.28, and wave ((b)) rally ended at 22.98. Wave ((c)) lower ended at 21.86 which also completed wave Y of (2) in higher degree. The metal has turned higher in wave (3). A break above wave (1) at 23.69 will confirm this view. Up from wave (2), expect wave (i) to end soon, then it should pullback in wave (ii) to correct the rally in wave (i) before the metal resumes higher again. Near term, as far as pivot at 21.86 low stays intact, expect pullback to find support in 3, 7, 11 swing for further upside.

Silver 60 Minutes Elliott Wave Chart

Silver (XAGUSD) Elliott Wave Video

https://www.youtube.com/watch?v=2GQjm0x9wkU

Japan’s Suzuki emphasizes balancing positives and negatives of weak Yen

As Japanese Yen continues to hover near multi-decade lows against Dollar after yesterday's selloff, Japan's Finance Minister Shunichi Suzuki reiterated the government's commitment to addressing the currency's movements. In his latest remarks, Suzuki avoided any direct mention of intervening in the currency markets, focusing instead on a strategy to balance the impact of the Yen's weakness.

Suzuki stated, "What's important is to maximize positive effects from the weak yen while mitigating negatives." His comments come as the Japanese government faces the challenges of managing economic implications of Yen's prolonged decline. While a weaker Yen can benefit Japan's export-driven economy, it also raises concerns about increased import costs, especially in the context of global inflationary pressures.

Suzuki's emphasis on maximizing the benefits and reducing the drawbacks of the weak Yen highlights the delicate balancing act the Japanese authorities must perform in the current economic environment. His statement suggests a cautious approach from the government, possibly hinting at measured responses rather than abrupt market interventions.

Australia NAB business confidence dips to -2, conditions resilient

In Australia, NAB reported a dip in Business Confidence for October, falling from 0 to -2. However, Business Conditions saw a slight improvement, rising from 12 to 13. Notably, trading conditions increased from 18 to 20, and profitability conditions improved from 9 to 12, while employment conditions slightly decreased from 9 to 8.

NAB Chief Economist Alan Oster commented, "Business conditions remain healthy, picking up in October and still well above average. Still, business confidence remained soft in the month, still well below average at -2 index points." He highlighted the persistent gap of 10-15 index points between current conditions and the more forward-looking confidence indicator, emphasizing that "Businesses clearly remain cautious about the outlook for the economy despite the resilience we are seeing."

The report also noted a slowdown in price and cost growth. Labour cost growth eased to 1.8% in quarterly equivalent terms, and purchase cost growth declined to 1.8%. Retail price growth remained stable at 1.9%, while overall price growth eased to 1.0%, marking the slowest rate since July 2020.

Oster added, "The Q3 CPI showed inflation had been persistent through the middle of the year and the survey suggests this remained the case heading into Q4. We still expect to see gradual moderation over time but it will be a protracted process, especially given the resilience of domestic demand thus far."