Sample Category Title

GBP/USD Calm ahead of UK Job Report

- UK employment data expected to soften

- UK will release inflation report on Wednesday

The British pound has edged higher on Monday. In the European session, GBP/USD is trading at 122.48, up 0.18%. The pound is coming off a nasty week, in which it declined 1.2%.

UK employment data expected to cool

The UK labour market has been resilient despite the Bank of England’s aggressive tightening, but is showing some cracks. We’ll get a look at key employment numbers on Wednesday. Job growth is expected to fall by 80,000 in the three months to September, after a massive loss of 207,000 in the previous release. Average earnings including bonuses are expected to slow to 7.4% in the three months to August, down from 8.1%. The BoE will be keeping a close look at wage growth, which is a significant driver of inflation.

The UK releases the inflation report on Wednesday, with the markets expecting CPI to have fallen sharply in October from 6.7% to 4.8%. If inflation falls below 5%, it would mark a milestone in the government’s tough battle with inflation, although the 2% target remains far, far away. Core CPI, which excludes food and energy, is expected to show a modest drop to 5.8%, down from 6.1% in September.

The BoE is projecting that inflation will fall back to the 2% target at the end of 2025, six months later than the previous forecast. Governor Bailey has been stressing that inflation remains too high, but the BoE nevertheless voted to hold rates at this month’s meeting after 14 consecutive hikes. Another pause at the December meeting would be the central bank’s preferred plan of action, but that will depend on the data.

GBP/USD Technical

- There is resistance at 1.2287 and 1.2344

- 1.2183 and 1.2091 and are providing support

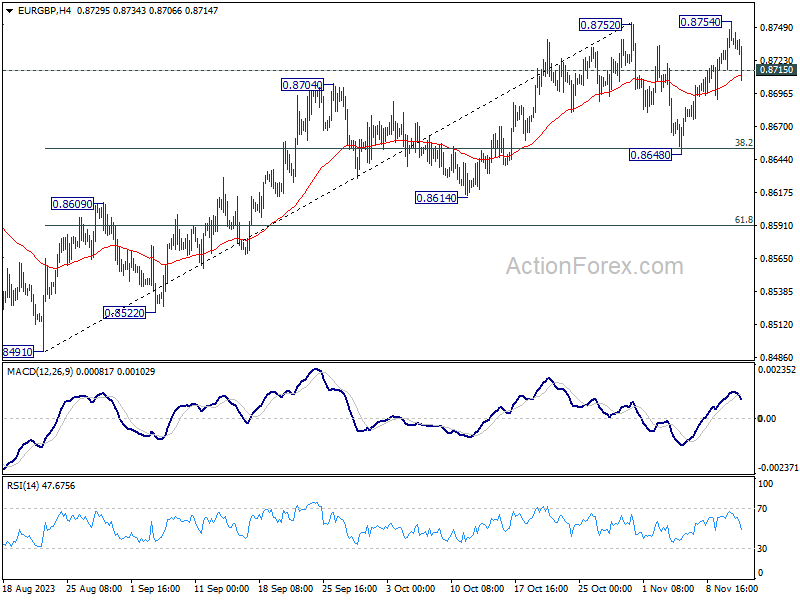

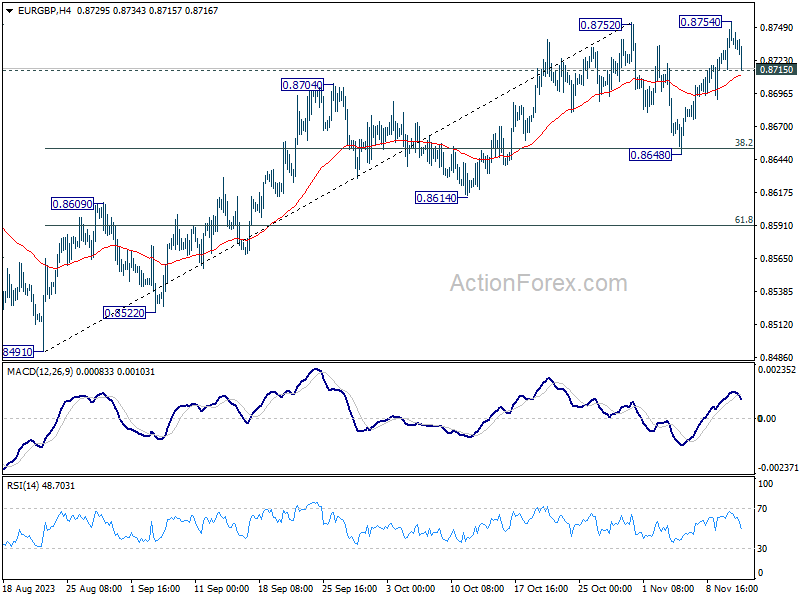

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8718; (P) 0.8737; (R1) 0.8758; More....

EUR/GBP's break of 0.8715 minor support argues that rebound from 0.8648 has completed after rejection by 0.8752 resistance. Intraday bias is back on the downside. Fall from 0.8754 is seen as the third leg of the consolidation pattern from 0.8752, and should target 0.8648. But strong support should be seen around there to complete the consolidation. On the upside, decisive break of 0.8752/4 will resume whole rise from 0.8491 to 0.8874 resistance next.

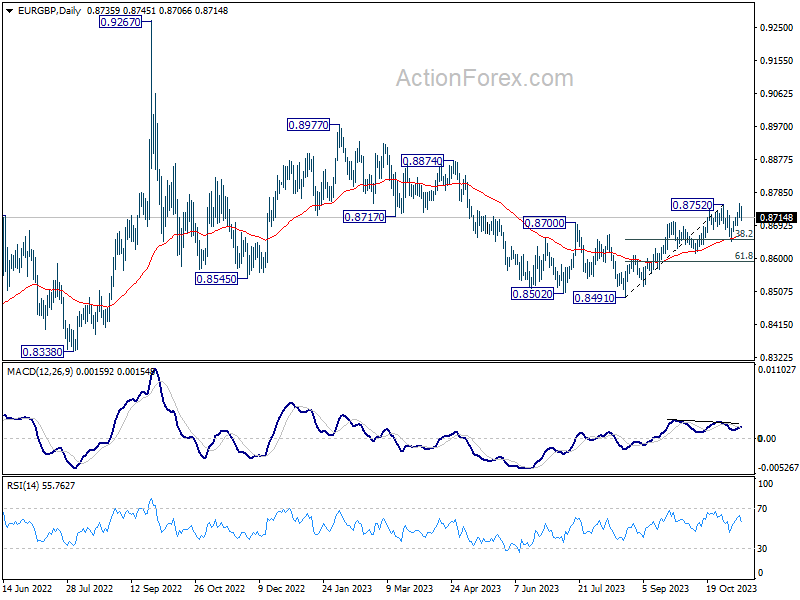

In the bigger picture, current development suggests that whole down trend from 0.9267 (2022 high) has completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. This will remain the favored case as long as 0.8614 support holds.

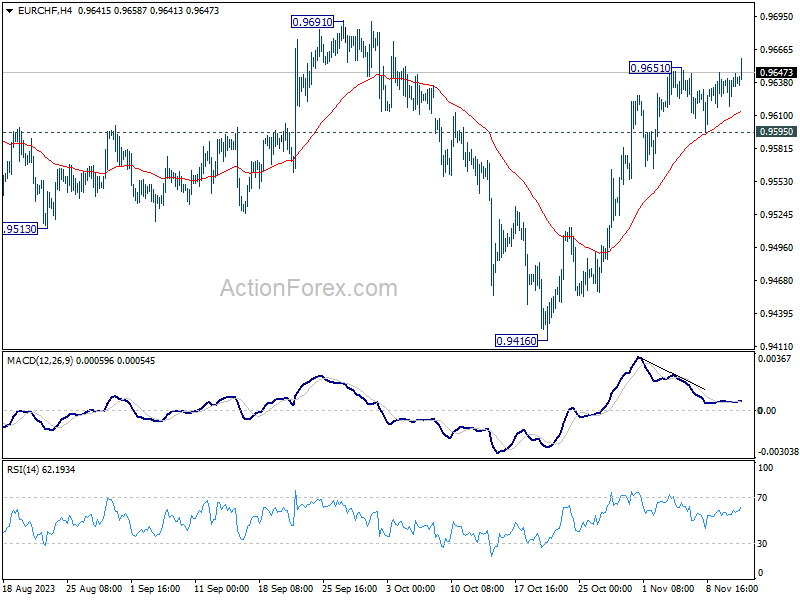

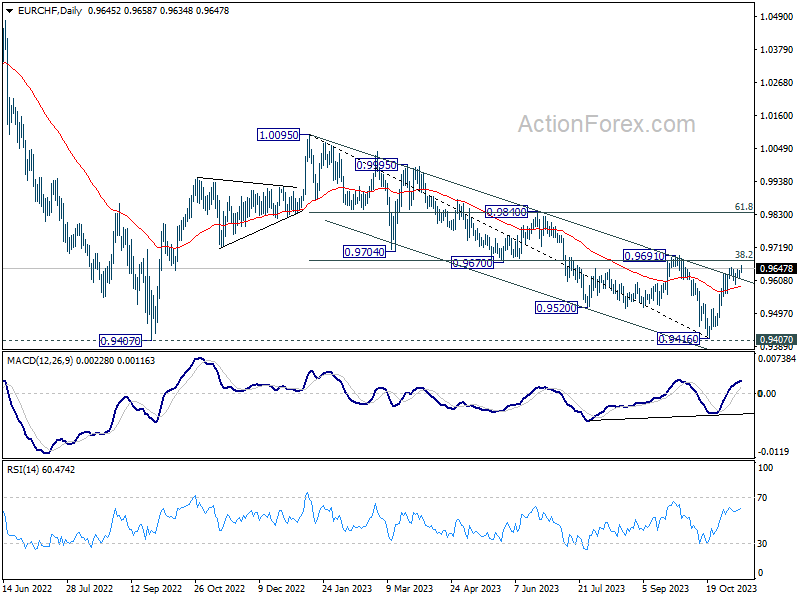

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9621; (P) 0.9633; (R1) 0.9646; More...

Intraday bias in EUR/CHF is back on the upside as rebound form 0.9416 resumes. Further rise should be seen to 0.9691 resistance. Firm break there will argue that whole decline from 1.0095 has completed at 0.9416, just ahead of 0.9407 support (2022 low). Nevertheless, break of 0.9595 support will indicate short term topping, and turn bias back to the downside for deeper pull back.

In the bigger picture, fall from 1.0095 (2023 high) might have completed at 0.9416, just ahead of 0.9407 support (2022 low). Sustained break of 0.9691 cluster resistance (38.2% retracement of 1.0095 to 0.9416 at 0.9675) will pave the way to 61.8% retracement at 0.9836 and above. However, rejection by 0.9691 will maintain medium term bearishness for another test on 0.9407 at least.

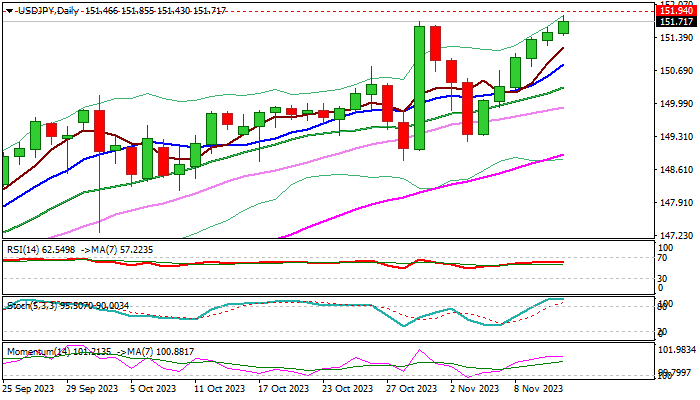

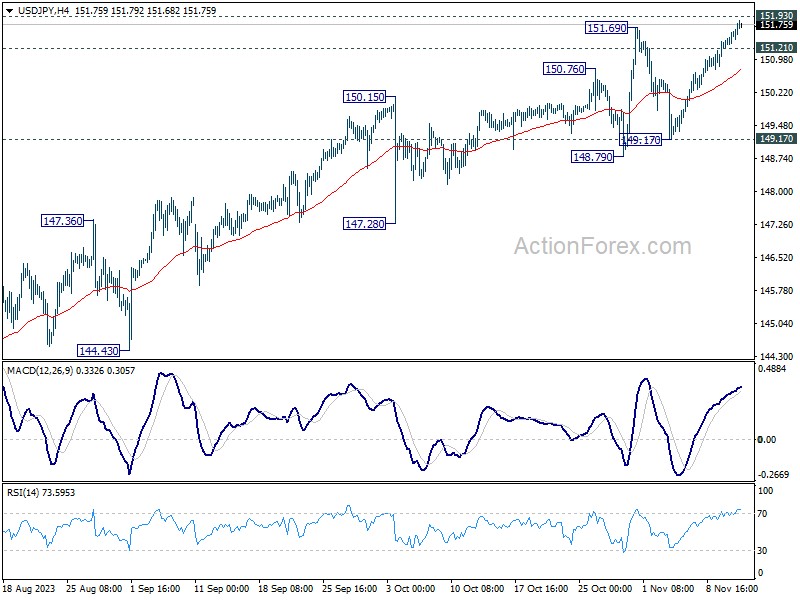

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.30 (P) 151.45; (R1) 151.68; More...

Intraday bias in USD/JPY stays on the upside at this point. Immediate focus is on 151.93 key resistance. Decisive break there will confirm resumption of long term up trend. Next target will be 157.69 projection level. On the downside, below 151.21 minor support will turn intraday bias neutral first. But near term outlook will stay bullish as long as 149.17 support holds, even in case of deep retreat.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 (2021 low) to 151.93 from 127.20 at 157.69.

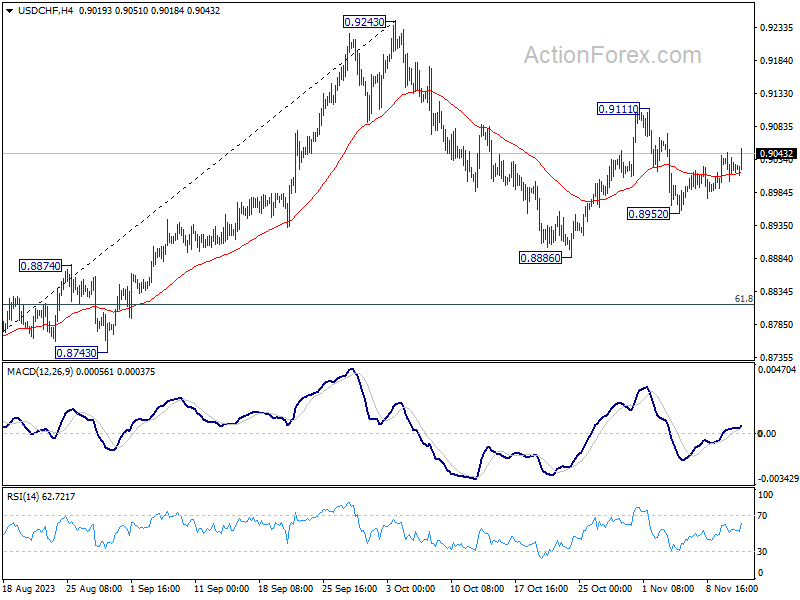

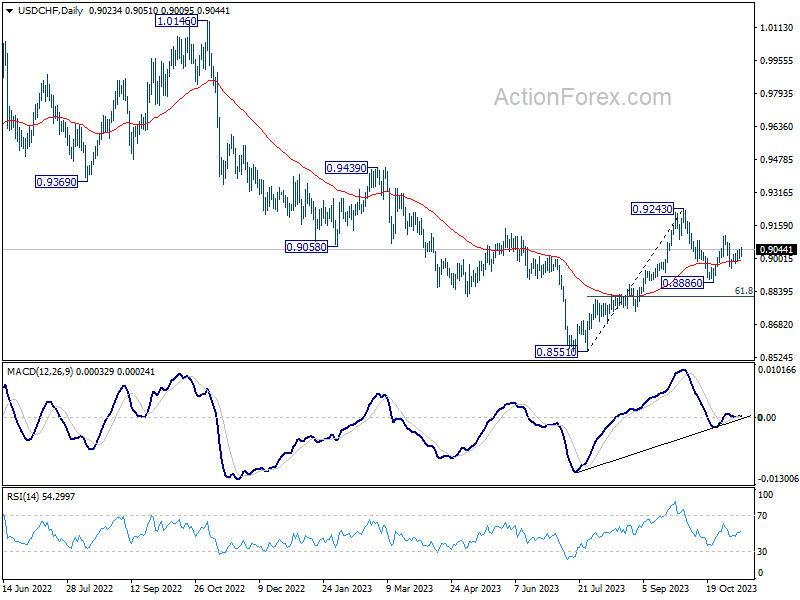

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8997; (P) 0.9021; (R1) 0.9040; More....

Intraday bias in USD/CHF stays neutral at this point, as range trading continues. On the downside, below 0.8952 will target a test on 0.8886 support first. Break there will resume whole decline from 0.9243 to 0.8815 fibonacci level. However, break of 0.9111 will resume the rebound from 0.8886 instead, and target 0.9243 resistance.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.

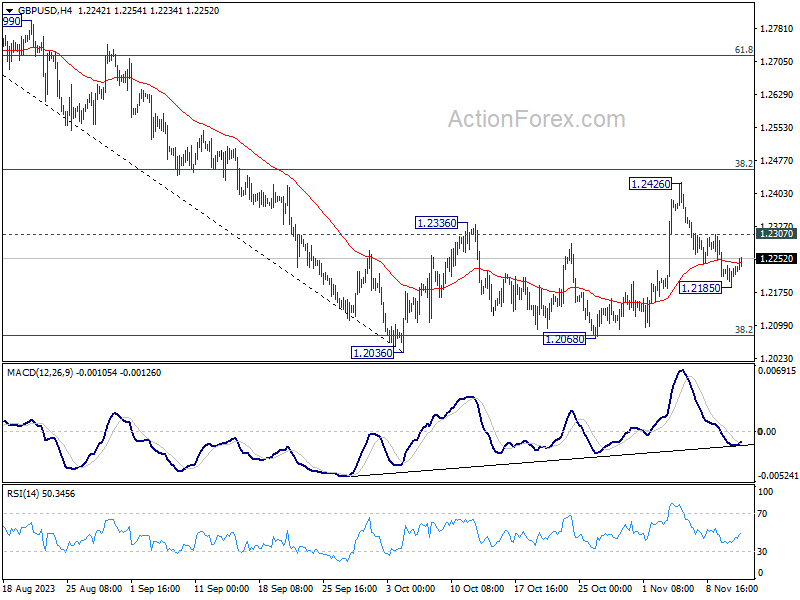

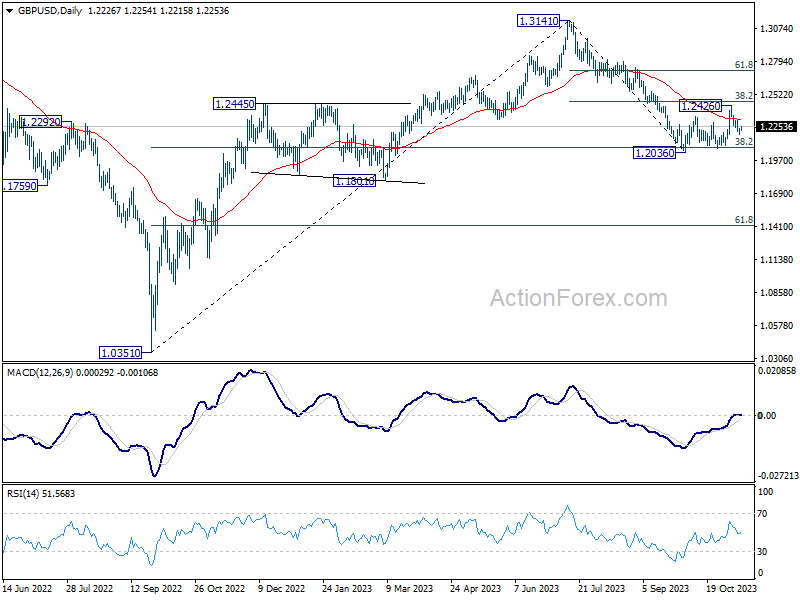

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2197; (P) 1.2217; (R1) 1.2248; More...

Intraday bias in GBP/USD is turned neutral with current recovery. But outlook is unchanged that corrective rebound from 1.2036 should have completed with three waves up to 1.2426. Below 1.2185 will bring deeper fall to retest 1.2036/68 support zone next. Firm break there will resume larger down trend from 1.3141. However, firm break of 1.2307 will dampen this view and bring stronger rise back to 1.2426 resistance.

In the bigger picture, rejection by 38.2% retracement of 1.3141 to 1.2036 at 1.2458, suggests fall from 1.3141 is still in progress. Sustained break of 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 will bring deeper decline to 61.8% retracement at 1.1417, even just as a corrective move.

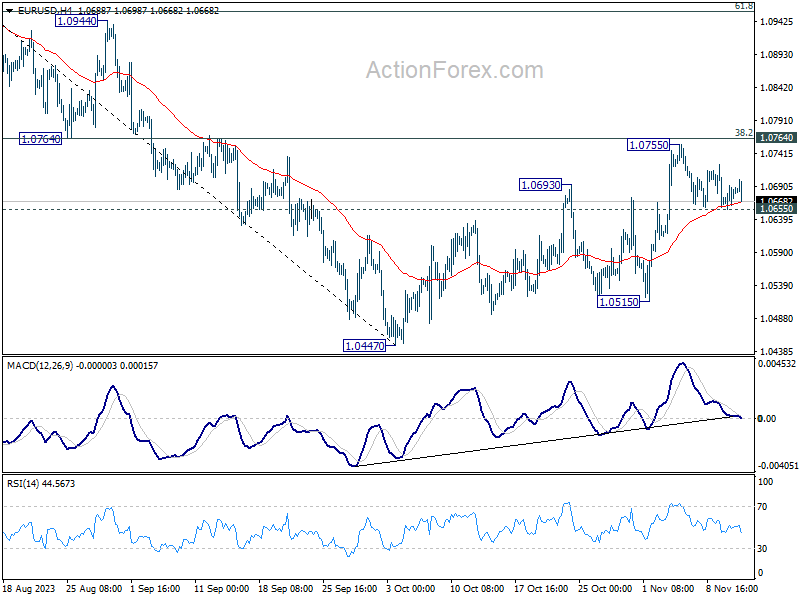

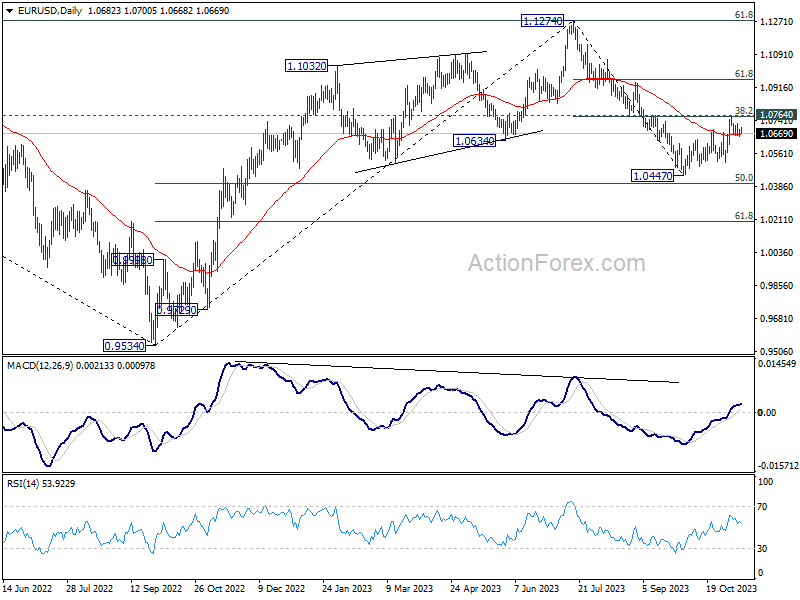

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0663; (P) 1.0678; (R1) 1.0700; More...

Intraday bias in EUR/USD stays neutral at this point. On the downside, break of 1.0655 minor support, and sustained trading below 55 4H EMA (now at 1.0664), will argue that the rebound from 1.0447 has completed with three waves up to 1.0755. That came after rejection by 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763). In this case, intraday bias will be turned back to the downside for 1.0447/0515 support zone. Nevertheless, strong bounce from current level, followed by decisive break of 1.0764, will bring stronger rally to 61.8% retracement at 1.0958 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. However, break of 1.0447 will resume the fall to 61.8% retracement of 0.9543 to 1.1274 at 1.0199.

Sterling and Aussie Bounce Back from Recent Lows, Euro Sees Downside Risk

There's a noticeable lack of a unifying theme in the forex markets today, largely attributed to an empty economic calendar across European and North American regions. Both Australian Dollar and British Pound are seeing a rebound from their recent downturns, particularly noticeable in currency crosses. However, the continuation of this momentum hinges significantly on impending economic data releases. Key reports to watch include Australian consumer and business confidence, along with UK employment data set to be unveiled tomorrow.

Dollar is trailing closely behind as the third strongest currency for the day. Meanwhile, Japanese Yen has seen a slight stabilization from its earlier steep selloff. However, Yen's recovery is relatively modest and is confined to a select few currencies. The Japanese currency still seems poised to challenge its multi-decade low against Dollar, but market participants may reserve their major trading decisions on USD/JPY until release of US CPI data tomorrow.

Swiss Franc finds itself at the bottom of the performance chart today, facing additional downward pressure due to the resumed rally in EUR/CHF. Similarly, New Zealand Dollar and Canadian Dollar are also among the weaker performers, further weighed down by Aussie's rebound against them. Euro, in contrast, presents a mixed picture, showing signs of vulnerability in several pairings except against Swiss Franc.

Technically, EUR/GBP is worth some attention in this quiet session. Firm break of 0.8715 minor support will argue that rebound from 0.8648 has completed after rejection by 0.8752 resistance. Fall from 0.8754 would then be seen as the third leg of the corrective pattern from 0.8752, and target 0.8648 support again. Nevertheless, in this case, strong support should emerge around 0.8648 to contain downside to complete the consolidation, and finally bring resumption of whole rise from 0.8491.

In Europe, at the time of writing, FTSE is up 0.63%. DAX is up 0.19%. CAC is up 0.29%. Germany 10-year yield is down -0.0221 at 2.697. Earlier in Asia, Nikkei rose 0.05%. Hong Kong HSI rose 1.30%. China Shanghai SSE rose 0.25%. Singapore Strait Times dropped -0.91%. Japan 10-year JGB yield rose 0.0192 to 0.877.

ECB's de Guindos foresees temporary inflation rebound, December forecasts crucial for policy assessment

In a speech today, ECB Vice President Luis de Guindos said the central bank expects "a temporary rebound" in inflation in the coming months as base-effect drops out of calculations. However, he emphasized that ECB foresees the overall disinflationary process to continue over the medium term.

De Guindos highlighted the unpredictability surrounding energy prices due to geopolitical tensions and fiscal policy impacts, along with the potential upward pressure on food prices resulting from adverse weather events and the broader climate crisis.

Despite a marked decrease in inflation, de Guindos warned that it is expected to remain high for an extended period, with persistent domestic price pressures. "We will therefore ensure that our policy rates will be set at sufficiently restrictive levels for as long as necessary," he affirmed.

Emphasizing the ECB's data-dependent approach, de Guindos stated, "Our future decisions on policy rates will continue to be taken on a meeting-by-meeting basis." He added that the ECB's December meeting, armed with fresh macroeconomic projections and additional data, will be crucial for reassessing the inflation outlook and necessary policy actions.

Japan's wholesale inflation eases to 0.8% yoy, continued downward trend

Japan's corporate goods price index, a key indicator of wholesale inflation, exhibited a significant slowdown in October, underscoring a continued trend of easing price pressures.

The index increased by just 0.8% yoy, falling short of the anticipated 0.9% yoy and marking its first dip below 1% since February 2021. This latest figure also represents the 10th consecutive month of slowing wholesale inflation.

The deceleration in the CGPI can be largely attributed to decreases in the prices of specific commodities. Notably, costs for wood, chemical, and steel products experienced declines, reflecting the broader impact of reduced global commodity prices.

Export price index saw an uptick from 0.5% yoy to 1.0% yoy. Import price index showed a lesser decline, moving from -15.5% yoy to -12.5% yoy.

RBA's Kohler warns of bumpy road ahead in tackling inflation

In a speech, Marion Kohler, Acting Assistant Governor of RBA, remarked that decline in inflation is expected to be a "more gradual process than previously thought."

This outlook stems from the current economic environment characterized by "still-high level of domestic demand" and "strong labour" alongside other cost pressures. These factors contribute to the prediction that inflation will hover just below 3% by the end of 2025.

The Assistant Governor pointed out that the recent trend of declining inflation has primarily been "driven by lower goods price inflation." In stark contrast, "domestically sourced inflation" – especially in the services sector – has shown resilience, being "widespread and slow to decline."

Kohler also underscored the nuanced challenges in the next phase of controlling inflation, which she anticipates to be "more drawn out than the first." This outlook aligns with experiences in other advanced economies that have faced similar inflationary patterns.

Furthermore, she cautioned about the potential for unforeseen challenges, citing the recent increase in fuel prices as an example of supply shocks that could unpredictably influence headline inflation.

Kohler emphasized the uncertain nature of the journey ahead in managing inflation, stating, "the road ahead could be bumpy."

New Zealand BNZ services fell to 48.9, contraction with economic angst

New Zealand's BusinessNZ Performance of Services Index experienced a notable dip in October, falling from 50.6 to 48.9, a level indicative of contraction in the sector. This decline also positions the index well below its long-term average of 53.5.

Activity and sales experienced a significant drop, moving from 50.9 to 47.4. There was also a downturn in employment, which decreased from 50.5 to 49.3. New orders and business fell as well,from 53.9 to 51.9. On a more positive note, stocks and inventories saw an increase, rising from 48.0 to 51.1, and supplier deliveries edged up slightly from 49.7 to 49.8.

Despite these declines, the proportion of negative comments in October decreased to 58.2%, a reduction from 61.8% in September and 63.9% in August, indicating a slight improvement in business sentiment.

BNZ Senior Economist Craig Ebert said that "combined, the PSI (48.9) and PMI (42.5) paint a picture of economic angst. This counsels caution around GDP for Q3, after it posted a surprising gain of 0.9% in Q2".

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0663; (P) 1.0678; (R1) 1.0700; More...

Intraday bias in EUR/USD stays neutral at this point. On the downside, break of 1.0655 minor support, and sustained trading below 55 4H EMA (now at 1.0664), will argue that the rebound from 1.0447 has completed with three waves up to 1.0755. That came after rejection by 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763). In this case, intraday bias will be turned back to the downside for 1.0447/0515 support zone. Nevertheless, strong bounce from current level, followed by decisive break of 1.0764, will bring stronger rally to 61.8% retracement at 1.0958 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. However, break of 1.0447 will resume the fall to 61.8% retracement of 0.9543 to 1.1274 at 1.0199.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Oct | 48.9 | 50.7 | ||

| 23:50 | JPY | PPI Y/Y Oct | 0.80% | 0.90% | 2.00% | 2.20% |

| 06:00 | JPY | Machine Tool Orders Y/Y Oct P | -20.60% | -11.20% |

Aussie Ends Nasty Slide, Confidence Data Next

- Australian dollar breaks five-day losing streak

- Business, consumer confidence will be released on Tuesday

The Australian dollar has edged higher on Monday. In the European session, AUD/USD is trading at 0.6376, up 0.27%. The Aussie has snapped a five-day losing streak in which it declined 2.35%.

Australian dollar eyes business, consumer confidence

Australia will release consumer and business confidence data on Tuesday. Consumers remain deeply pessimistic, although the Westpac Consumer Sentiment index climbed 2.9% in October to 82, its highest level in six months. The 100 level separates pessimism from optimism. Consumers have been squeezed by stubbornly high inflation and elevated interest rates. The market consensus for November is 0.7%, which would raise the index slightly to 82.6.

Business confidence remains well below average and the NAB Business Confidence index is expected to remain unchanged at 1 in October. The zero level separates pessimism from optimism. Business conditions are in better shape but fell from 14 to 11 in September.

Is the Reserve Bank of Australia done with its tightening cycle? The central bank raised rates last week after four consecutive pauses but the Australian dollar fell sharply after the move. The markets were of the view that the RBA had raised the bar to further hikes, even though the RBA statement noted that inflation was still too high.

The RBA quarterly monetary policy statement, released on Friday, warned of risks to the upside for inflation, and the hawkish tone may have helped the Aussie stabilize today after a miserable week. The RBA meets next on December 5th and the October inflation report a week earlier could play a key role as to whether the RBA pauses or raises rates at the final meeting of 2023.

In the US, the Michigan Consumer Sentiment index, released on Friday, eased to 60.4 in November, down from 63.8 in October and shy of the market consensus of 63.7. Confidence fell as consumers’ long-term inflation expectations rose from 3.0% to 3.2% in November, the highest level since 2011. The Fed is in a pickle as inflation expectations are rising while consumer confidence is falling, which is likely to translate into weaker consumer spending.

AUD/USD Technical

- AUD/USD is putting pressure on support at 0.6351. Below, there is support at 0.6292

- 0.6408 and 0.6476 are the next resistance lines

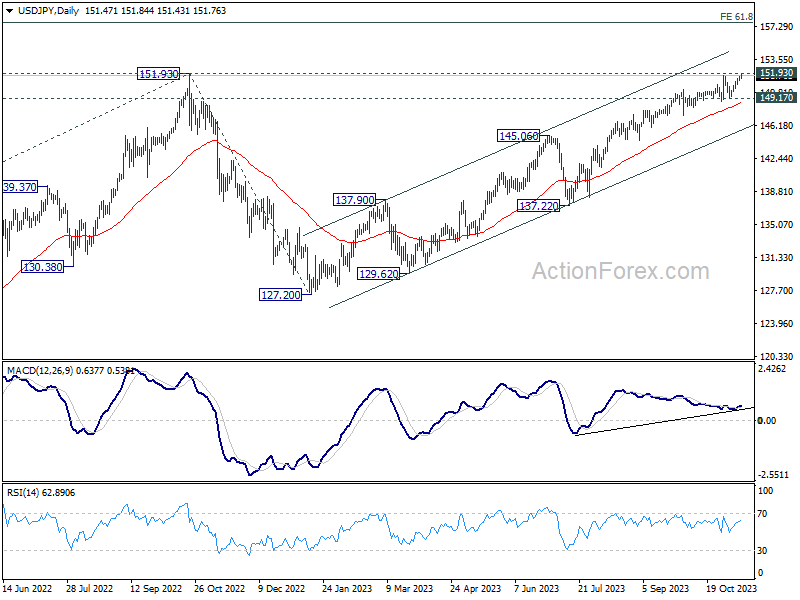

USD/JPY: Bulls Pressure Key 2022 Peak

USDJPY keeps firm bullish tone and extends gains, after 1.4% advance last week and hit new 2023 high on Monday.

Rally extends into sixth consecutive day and came just ticks ahead of 2022 peak (151.94, the highest in over three decades) with break of pivotal 152 zone to signal continuation of a larger uptrend from Dec 2011 low (75.55), interrupted by 151.94/127.22 correction.

Fibo projections of the upleg from 149.19 (Nov 3 higher low) mark immediate targets at 152.69 (138.2%), 153.29 (161.8%) and 154.26 (200%).

Full bullish setup of daily studies supports the action, though headwinds cannot be ruled out on overbought conditions and persisting intervention threats.

Friday’s low at 151.22 marks initial support, followed by Thursday’s low at 150.77, with dips to be contained by rising daily Tenkan-sen (150.52), guarding lower pivot at 150.00 (psychological/daily Kijun-sen) loss of which would sideline bulls.

Res: 151.85; 151.94; 152.69; 153.29.

Sup: 151.22; 150.77; 150.52; 150.00.