Sample Category Title

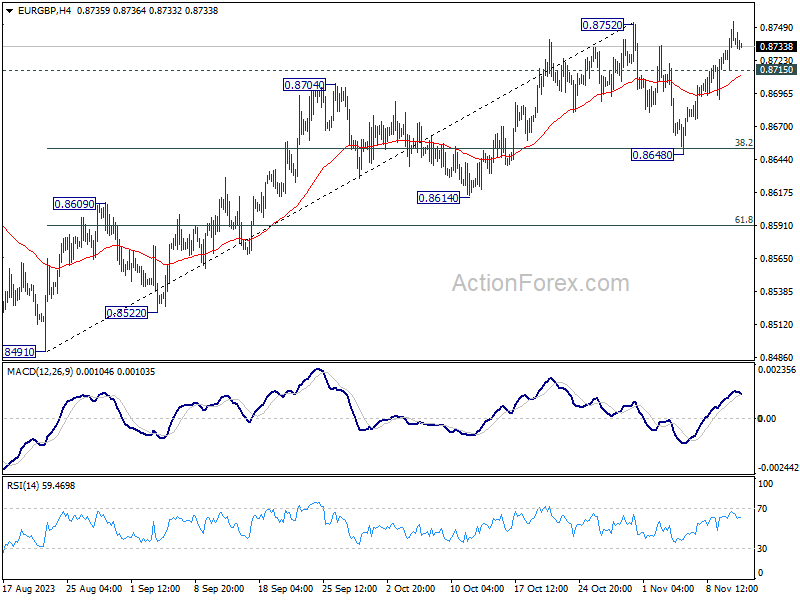

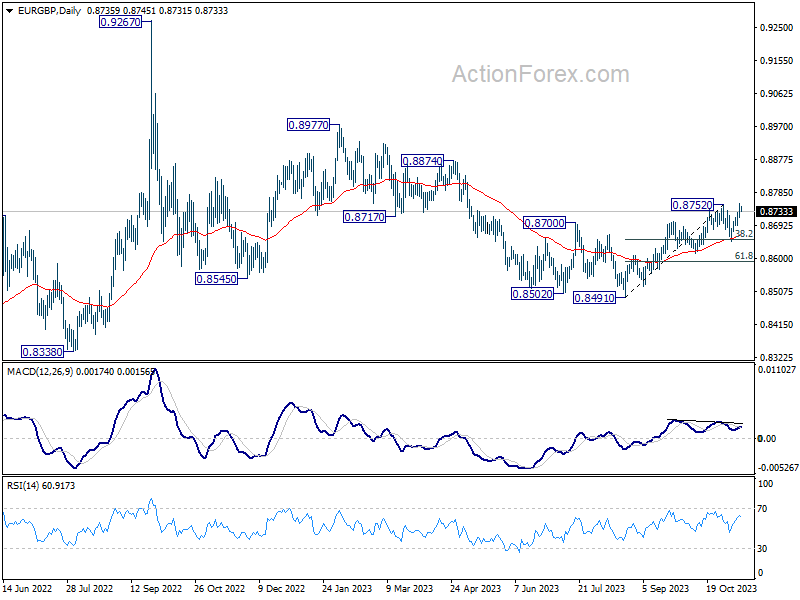

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8718; (P) 0.8737; (R1) 0.8758; More....

Focus stays on 0.8752 resistance in EUR/GBP. Decisive break there will resume larger up trend and target 0.8874 resistance next. On the downside, below 0.8715 minor support will extend the corrective pattern from 0.8752 with another falling leg before completion. But in this case, downside should be contained by 0.8648 support.

In the bigger picture, current development suggests that whole down trend from 0.9267 (2022 high) has completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. This will remain the favored case as long as 0.8614 support holds.

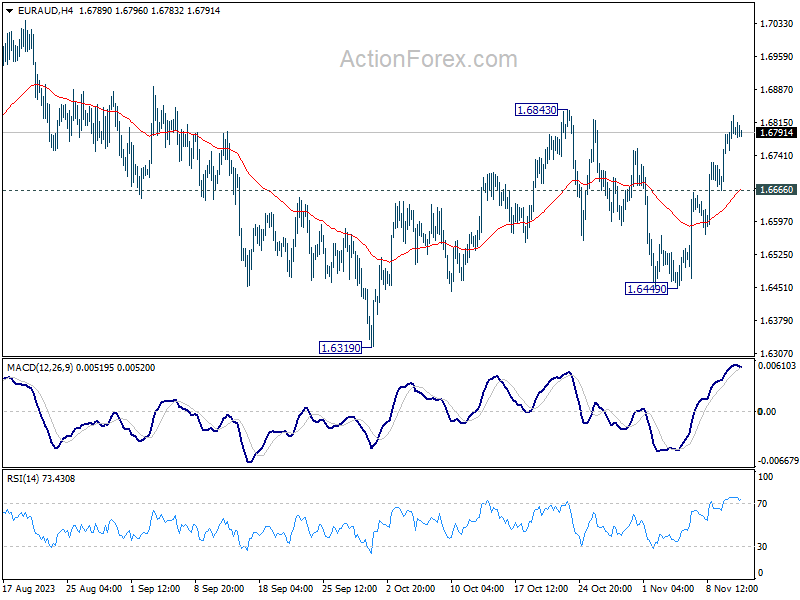

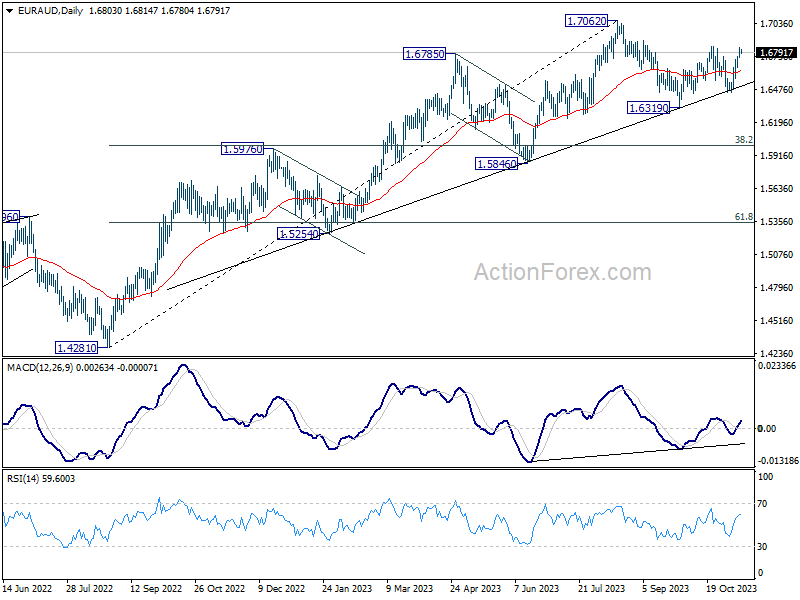

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6751; (P) 1.6792; (R1) 1.6840; More...

Immediate focus stays on 1.6843 resistance in EUR/AUD. Decisive break there will resume the rebound from 1.6319 for retesting 1.7062 high next. On the downside, however, below 1.6666 minor support will turn bias back to the downside for 1.6449 support instead.

In the bigger picture, while 1.7062 is a medium term top, there is no clear sign of trend reversal as EUR/AUD continues to draw strong support from the medium term trend line. Break of 1.7062 will resume the larger up trend from 1.4281 (2022 low) to 1.7691 fibonacci level. Nevertheless, break of 1.6449 support will argue that deeper correction is underway to 38.2% retracement of 1.4281 to 1.7062 at 1.6000.

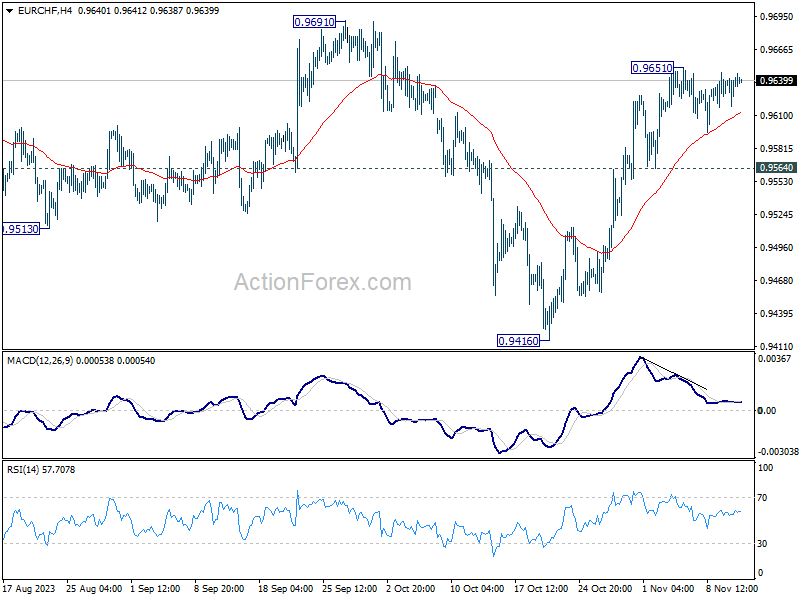

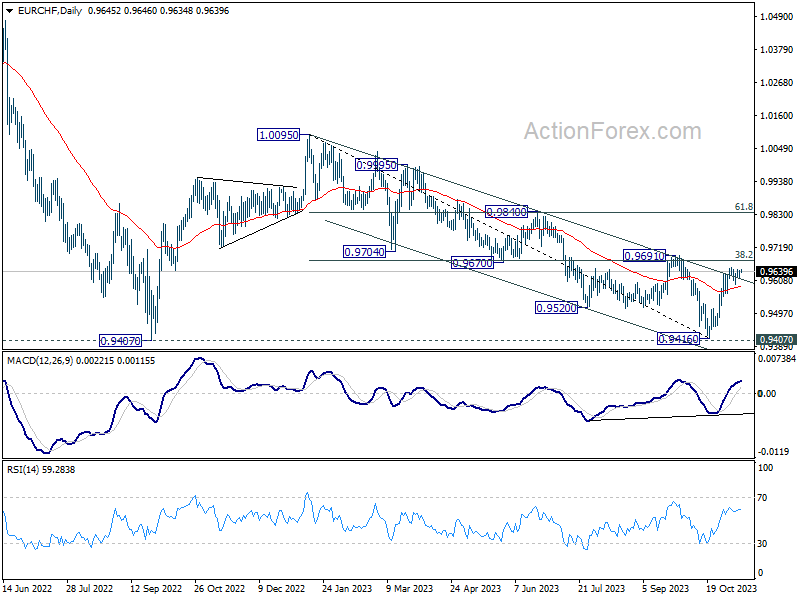

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9621; (P) 0.9633; (R1) 0.9646; More...

Intraday bias in EUR/CHF stays neutral as range trading continues below 0.9651. Another dip cannot be ruled out. But downside should be contained by 0.9564 support to bring another rally. On the upside, break of 0.9651 will resume the rise from 0.9416 to 0.9691 resistance first. Firm break there will argue that whole decline from 1.0095 has completed at 0.9416, just ahead of 0.9407 support (2022 low).

In the bigger picture, fall from 1.0095 (2023 high) might have completed at 0.9416, just ahead of 0.9407 support (2022 low). Sustained break of 0.9691 cluster resistance (38.2% retracement of 1.0095 to 0.9416 at 0.9675) will pave the way to 61.8% retracement at 0.9836 and above. However, rejection by 0.9691 will maintain medium term bearishness for another test on 0.9407 at least.

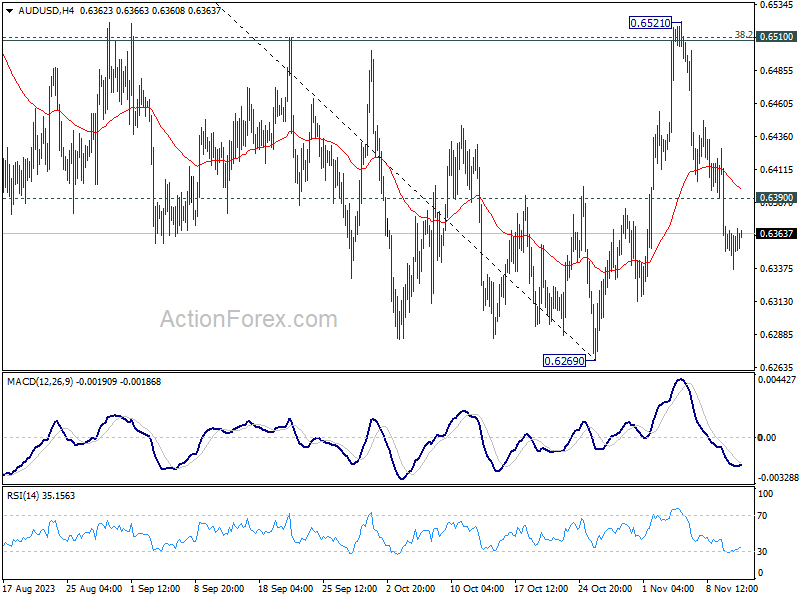

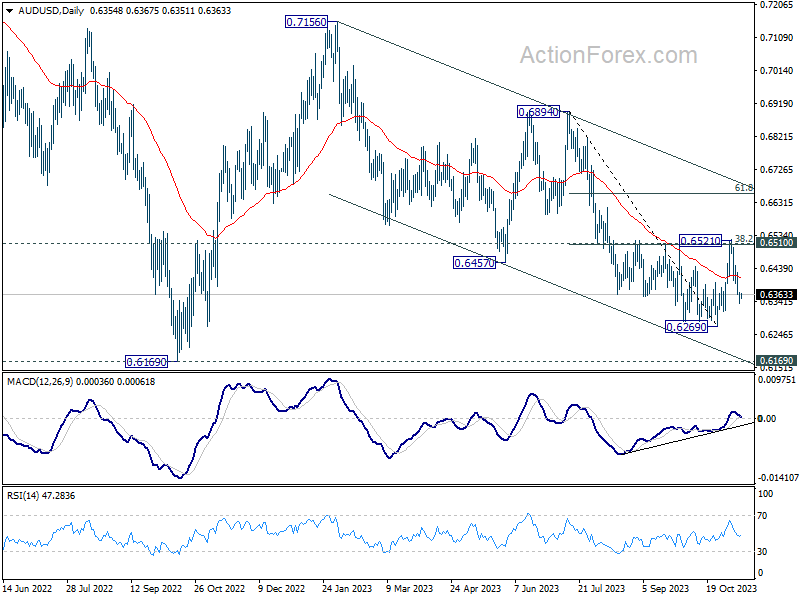

AUD/USD Daily Report

Daily Pivots: (S1) 0.6343; (P) 0.6357; (R1) 0.6376; More...

Intraday bias in AUD/USD stays on the downside at this point. Deeper fall should be seen back to retest 0.6269. Firm break there will resume larger fall from 0.7156, to retest 0.6169 low. On the upside, above 0.6427 minor resistance will turn intraday bias neutral first. Overall, outlook will stay bearish as long as 0.6510 cluster resistance (38.2% retracement of 0.6894 to 0.6269 at 0.6508) holds.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of a corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

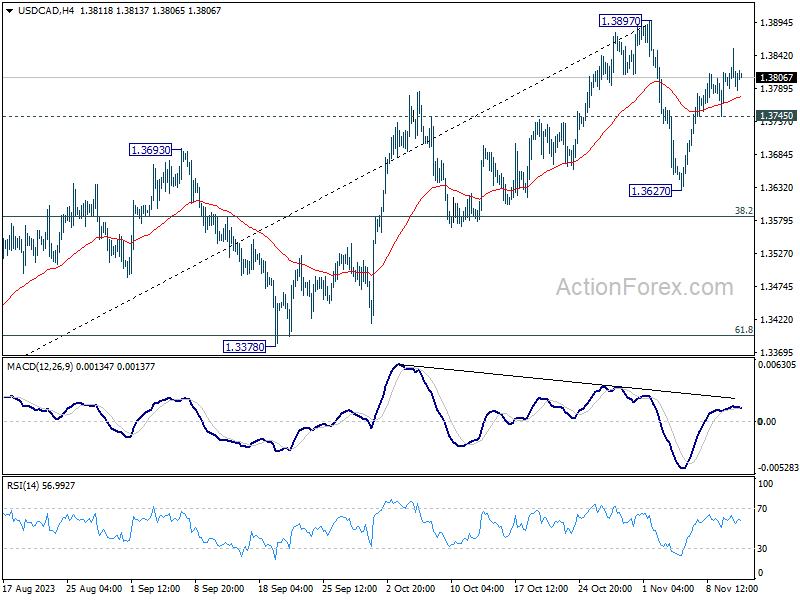

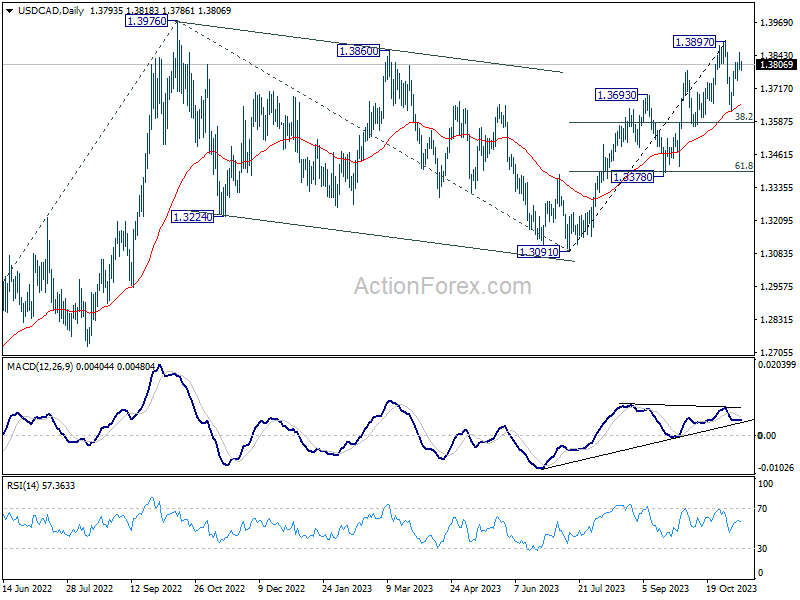

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3774; (P) 1.3814; (R1) 1.3837; More...

Intraday bias in USD/CAD remains mildly on the upside for retesting 1.3897. Strong resistance could be seen there to limit upside on first attempt. On the downside, break of 1.3745 will turn bias to the downside to extend the corrective pattern from 1.3897 with another falling leg. In this case, strong support should be seen from 38.2% retracement of 1.3091 to 1.3897 at 1.3589 to bring rebound.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will remain the favored case as long as 1.3378 support holds.

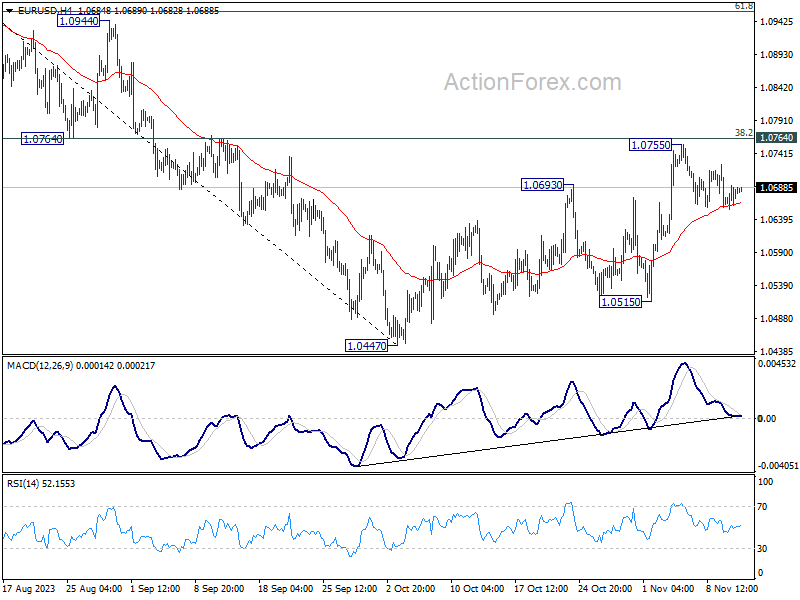

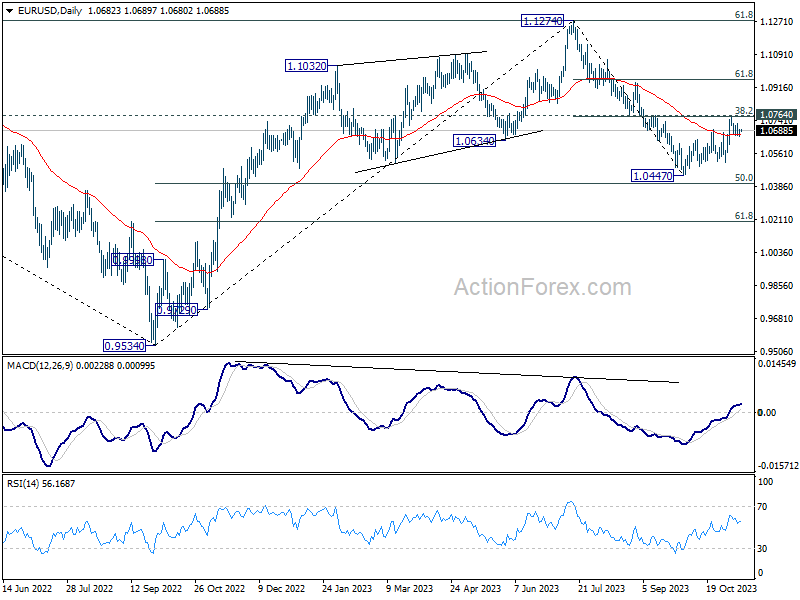

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0663; (P) 1.0678; (R1) 1.0700; More...

Intraday bias in EUR/USD remains neutral for the moment. On the upside, decisive break of 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763) will extend the rise from 1.0447 to 61.8% retracement at 1.0958 next. However, sustained break of 55 4H EMA (now at 1.0664) will argue that the rebound has completed, and turn bias back to the downside for 1.0447/0515 support zone instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. However, Break of 1.0447 will resume the fall to 61.8% retracement of 0.9543 to 1.1274 at 1.0199.

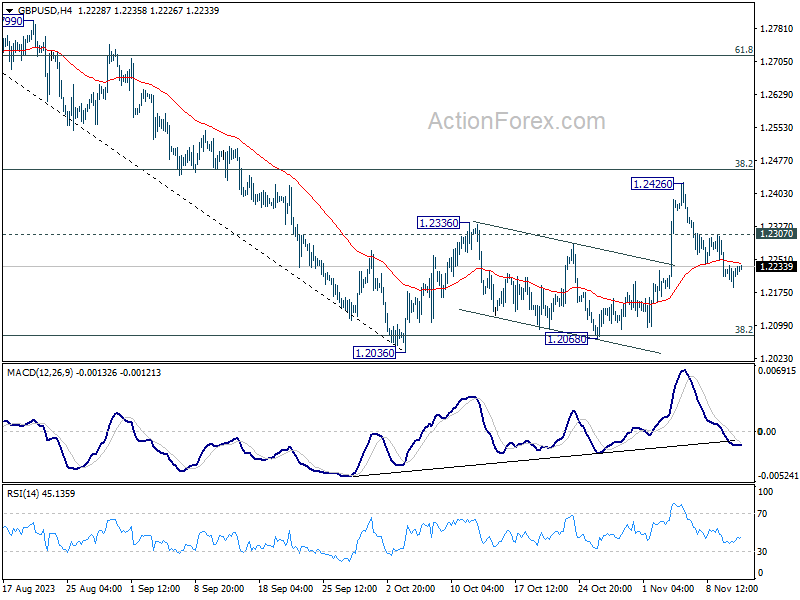

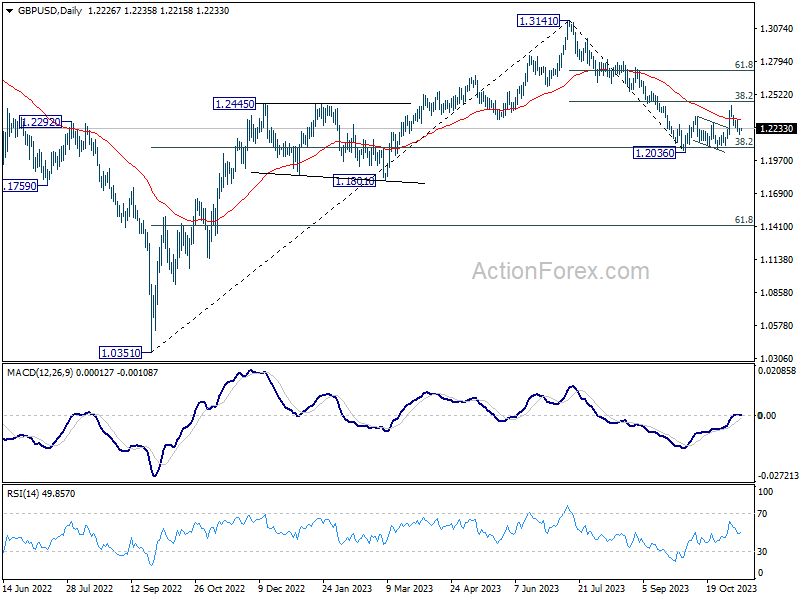

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2197; (P) 1.2217; (R1) 1.2248; More...

Intraday bias in GBP/USD remains mildly on the downside at this point. Corrective rebound from 1.2036 should have completed with three waves up to 1.2426. Deeper fall should be seen to retest 1.2036/68 support zone next. Firm break there will resume larger down trend from 1.3141. On the upside, above 1.2307 minor resistance will turn intraday bias neutral first.

In the bigger picture, rejection by 38.2% retracement of 1.3141 to 1.2036 at 1.2458, suggests fall from 1.3141 is still in progress. Sustained break of 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 will bring deeper decline to 61.8% retracement at 1.1417, even just as a corrective move.

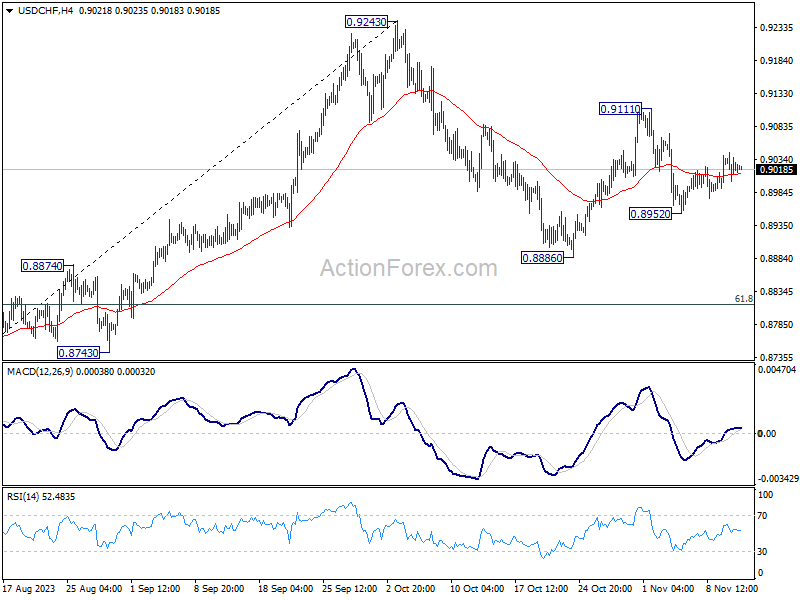

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8997; (P) 0.9021; (R1) 0.9040; More....

Intraday bias in USD/CHF remains neutral as range trading continues. On the downside, below 0.8952 will target a test on 0.8886 support first. Break there will resume whole decline from 0.9243 to 0.8815 fibonacci level. However, break of 0.9111 will resume the rebound from 0.8886 instead, and target 0.9243 resistance.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.

US CPI Week

Market movers today

There are no major data releases planned for today.

The most important release this week will likely be US CPI for October on Tuesday, which is extra uncertain this month due to possible effects from the auto workers' strike as well as technical factors relating to health insurance premiums. Also worth watching is US retail sales on Thursday after the very strong September-print. The week also features a long-expected Xi-Biden meeting on Wednesday along with a string of Chinese data and a possible Chinese rate cut, and UK job and inflation reports.

The 60 second overview

Market focus and overnight: Following a series of weeks this autumn where the market-narrative has shifted considerably amid new economic data releases, last week was rather uneventful when in terms of new global macro information for markets to trade on. The week was initially characterised by a decline in global yields but towards the end of last week we did see a slight reversal of the rally in fixed income with yields moving back higher. First, a few hawkish remarks from prominent Federal Reserve board members including Chair Powell halted the decline. Then Friday's release of University of Michigan inflation expectations showed a surprise rise in the 1Y measure from 4.2% to 4.4% (expected 4.0%) but more importantly the 5-10Y expectations also rose from 3.0% to 3.2% (expected 3.0%). Both drivers sent USD rates higher in a move that flattened the curve. We still think that we have hit the peak in Fed policy rates and do not envision a December rate hike. Also we still see the case for the first Fed rate cut to come as early as March.

It has been fairly quiet overnight with market sentiment turning slightly sour despite little new information and despite a late equity rally during the US session on Friday. On the data front Japanese producer prices were slightly lower than expected. Otherwise market focus is not least on US CPI this week and on US-China relations but also a seeming decline in geopolitical tensions in the Middle East is getting attention.

Oil. The oil market could be worth following in the coming weeks for a bellwether for the global business cycle. Oil prices dropped to the lowest level since July last week despite a severe Middle East crisis, Saudi Arabia hanging on to unilateral output cuts and a weaker USD. If the oil market does not reverse the recent losses global oil demand has likely deteriorated on the back of a drop in global economic growth.

Norway inflation surprise. On Friday, Norwegian core inflation for October surprised significantly to the topside. Core inflation rose to 6.0% y/y (expected: 5.6%) in annual terms while the (seasonally-adjusted) 3-month price growth rose from 2.9% to 4.9% . The details show that, somewhat surprisingly, there was a significant rebound in food prices. The prices of furniture/household equipment, air tickets, and hotel/restaurant services also rose more than expected, so the rise was quite broad-based. The release was a game changer in terms of the signals from previous months which had otherwise indicated a disinflationary trend. While Norwegian inflation releases are notoriously volatile the surprise rise in the October figures does challenge our narrative that underlying inflation clearly was in the process of decreasing. Given Norges Bank's rhetoric at the monetary policy meeting on 3 November this sharply lifts the probability of a 25bp rate hike in December - although we do not see it as a done deal. Indeed if we are right in expecting a sharp downward correction in the November CPI figures and in the growth picture weakening (GDP, regional network, etc.) we would expect markets to question the outlook for a final Norwegian rate hike.

Equities: Global equities were higher on Friday as the US market rallied into the late hour of trading and secured yet another positive week for equities. The rally was led by cyclicals taking 5 days in a row last week and outperforming defensives by almost 3%. It is worth noting that small-caps have been left out of recent rallies as investors see the recession fear as a bigger concern for small-caps compared to large-caps. Energy made a small comeback on Friday but that does not change the fact of an almost 8% underperformance versus tech last week. In the US on Friday: Dow +1.2%, S&P 500 +1.6%, Nasdaq +2.1% and Russell 2000 +1.1%. Asian markets are mostly lower this morning with Taiwan being the bright spot. European futures are flat while US futures are somewhat lower.

FI: European rates were mainly trading sideways on Friday in the 5y+ segment, while the short end sold off by 2-4bp amid ECB president Lagarde saying that a rate cut is not coming 'in the coming quarters' and given spill-overs from the USD curve.

FX: Last week, FX markets were characterised by a setback to commodity currencies in the likes of AUD, NZD and ZAR. While NOK initially had a poor week, Friday's Norwegian inflation surprise gave some support to the NOK returning EUR/NOK back below the 11.90 mark. EUR/USD was range-bound for the most part of last week although the final rise in short-end USD yields did contribute to sending EUR/USD below 1.07 on Friday. EUR/SEK remains close to the 11.65 area while EUR/GBP is back close to the 0.8750-mark.

Credit: Friday was a quiet day in the corporate bond market without significant news. iTraxx Main was 1bp wider at 76bp while iTraxx X-over was 4bp wider at 412bp.

Nordic macro

The only thing happening in Sweden is that vice Governor Aino Bunge will give the last speech of the Riksbank's executive board before the blackout period starts up to their rate decision on 22 November.

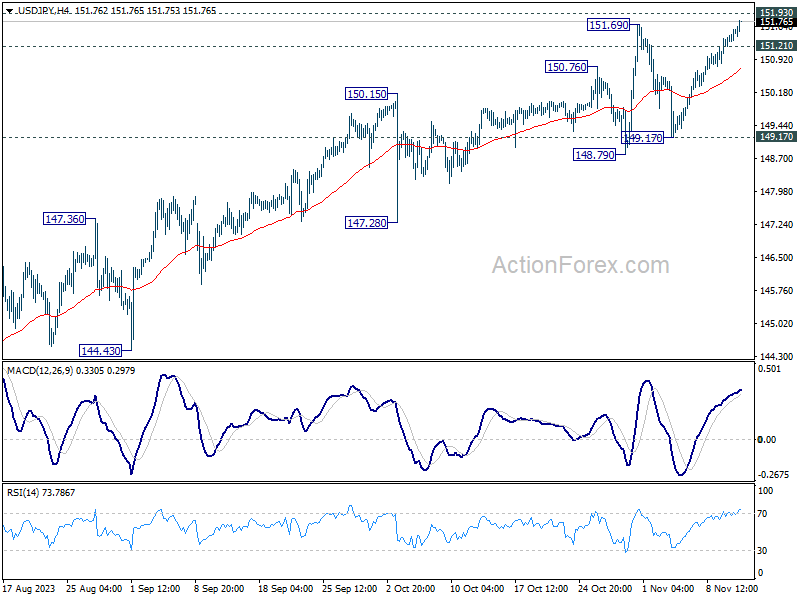

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.30 (P) 151.45; (R1) 151.68; More...

As USD/JPY's rise from 149.17 extends, immediate focus is now on 151.93 key resistance. Decisive break there will confirm resumption of long term up trend. Next target will be 157.69 projection level. On the downside, below 151.21 minor support will turn intraday bias neutral first. But near term outlook will stay bullish as long as 149.17 support holds, even in case of deep retreat.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 (2021 low) to 151.93 from 127.20 at 157.69.