Sample Category Title

EUR/GBP Weekly Outlook

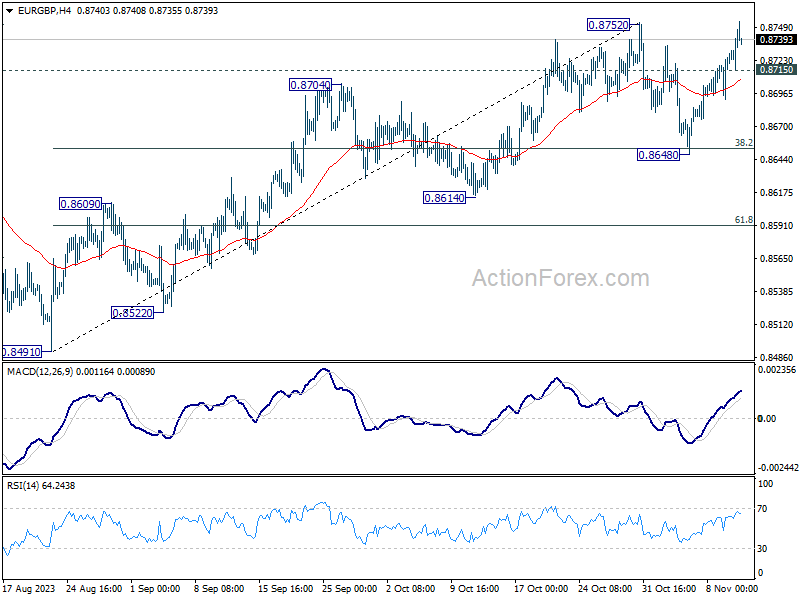

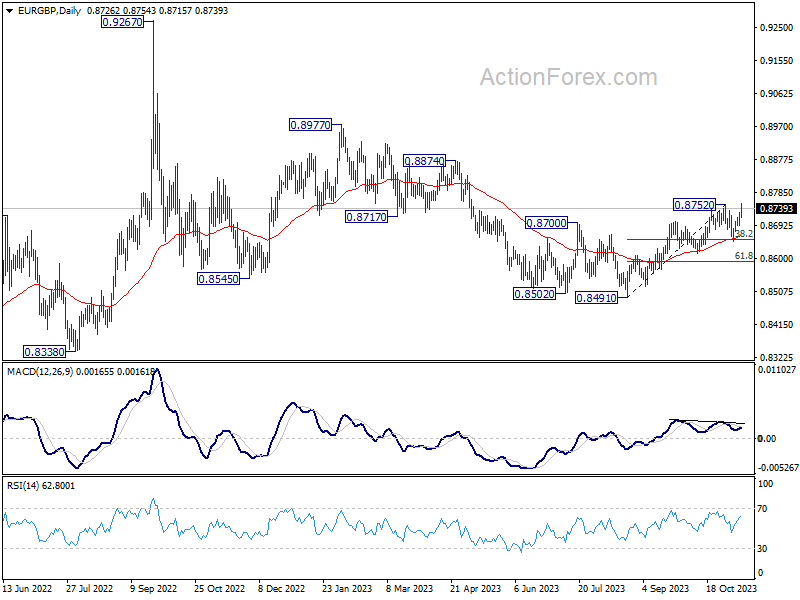

EUR/GBP's strong rebound last week suggests that correction from 0.8752 has completed at 0.8648, after hitting 38.2% retracement of 0.8491 to 0.8752 at 0.8652. Initial focus is on 0.8752 resistance this week. Decisive break there will resume larger up trend and target 0.8874 resistance next. On the downside, below 0.8715 minor support will extend the corrective pattern with another falling leg before completion.

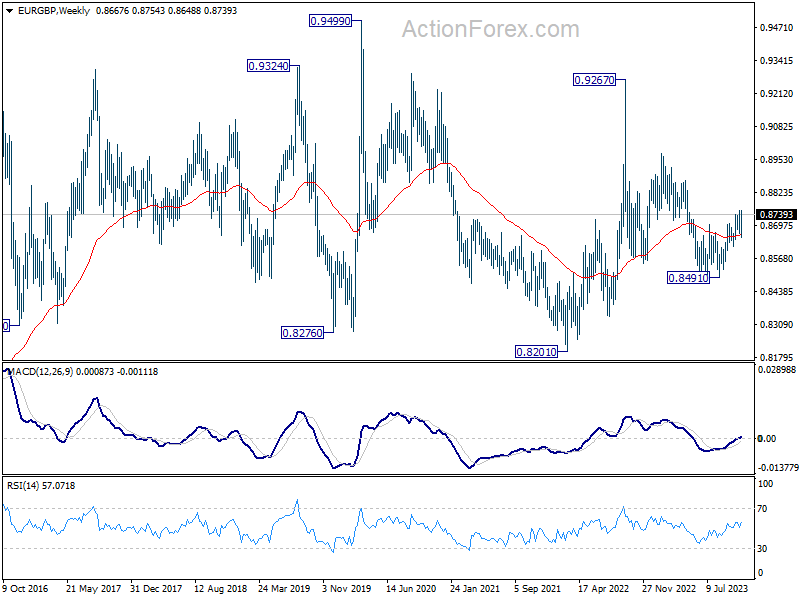

In the bigger picture, current development suggests that whole down trend from 0.9267 (2022 high) has completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. This will remain the favored case as long as 0.8614 support holds.

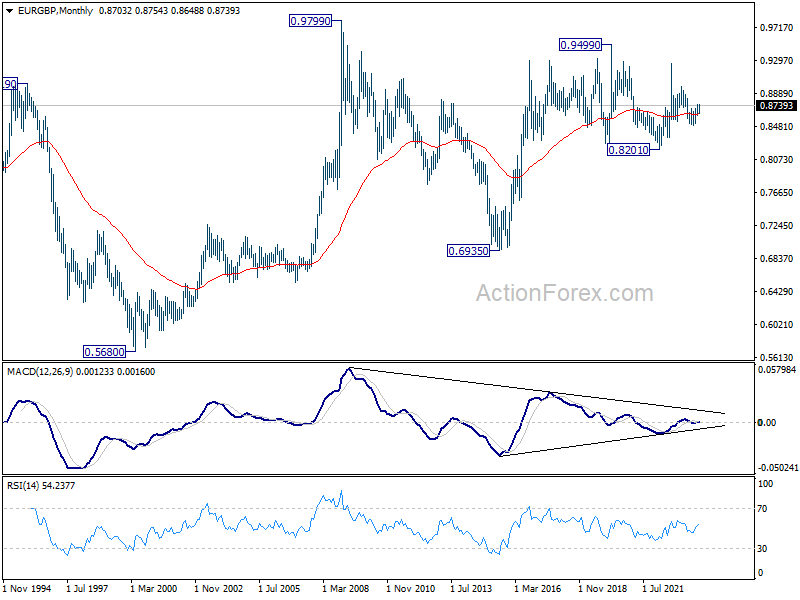

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to resume at a later stage, to 0.9799 (2009 high).

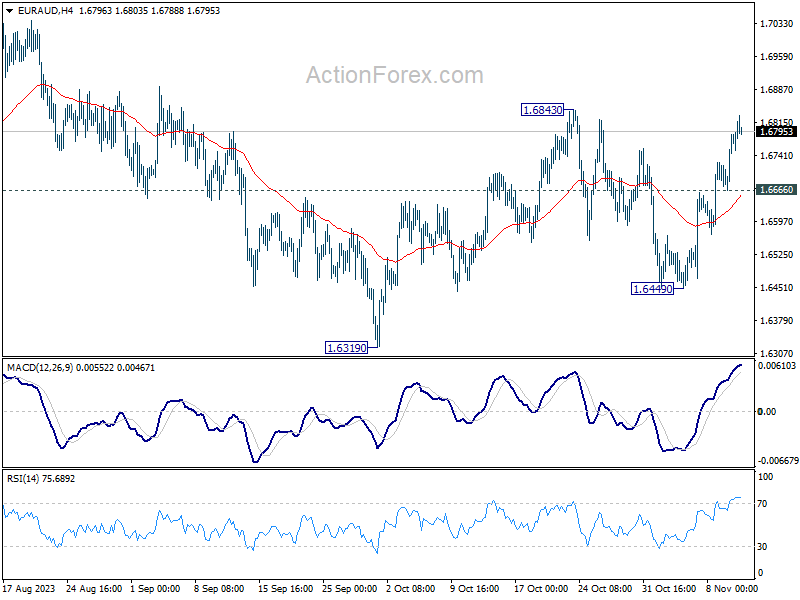

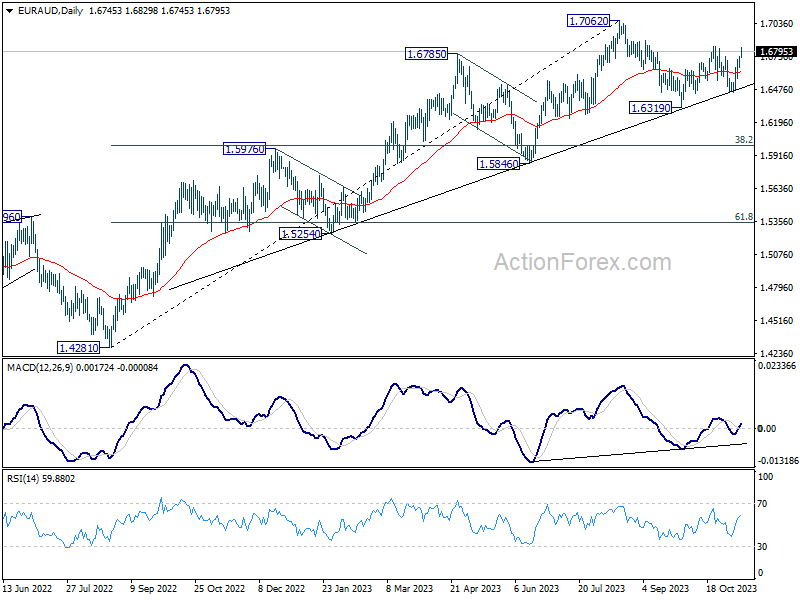

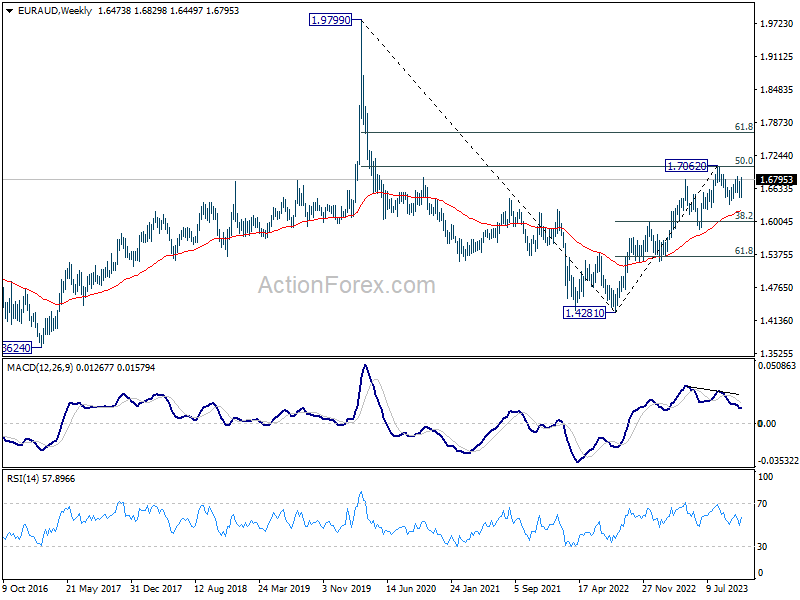

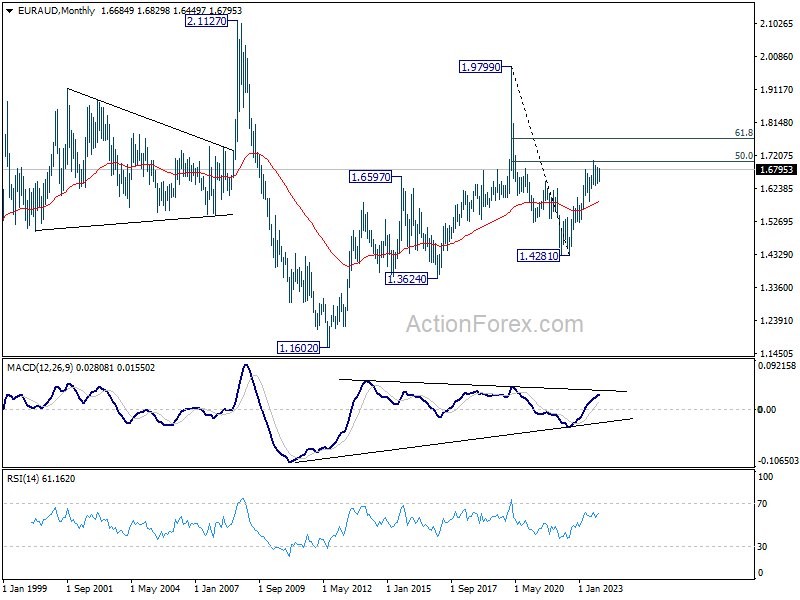

EUR/AUD Weekly Outlook

EUR/AUD's strong rebound last week revived near term bullishness. Immediate focus is on 1.6843 resistance this week. Firm break there will resume the rebound from 1.6319 for retesting 1.7062 high next. On the downside, however, below 1.6666 minor support will turn bias back to the downside for 1.6449 support instead.

In the bigger picture, while 1.7062 is a medium term top, there is no clear sign of trend reversal as EUR/AUD continues to draw strong support from the medium term trend line. Break of 1.7062 will resume the larger up trend from 1.4281 (2022 low) to 1.7691 fibonacci level. Nevertheless, break of 1.6449 support will argue that deeper correction is underway to 38.2% retracement of 1.4281 to 1.7062 at 1.6000.

In the longer term picture, loss of upside momentum as seen in 55 W MACD at this stage argues that rise from 1.4281 (2022 low) is more likely a corrective move. Further rise could still be seen as long as 1.5846 support holds. But upside will likely be limited by 61.8% retracement of 1.9799 to 1.4281 at 1.7691. Firm break of 1.5846 support will argue that the rise has completed, and another medium term down leg has started.

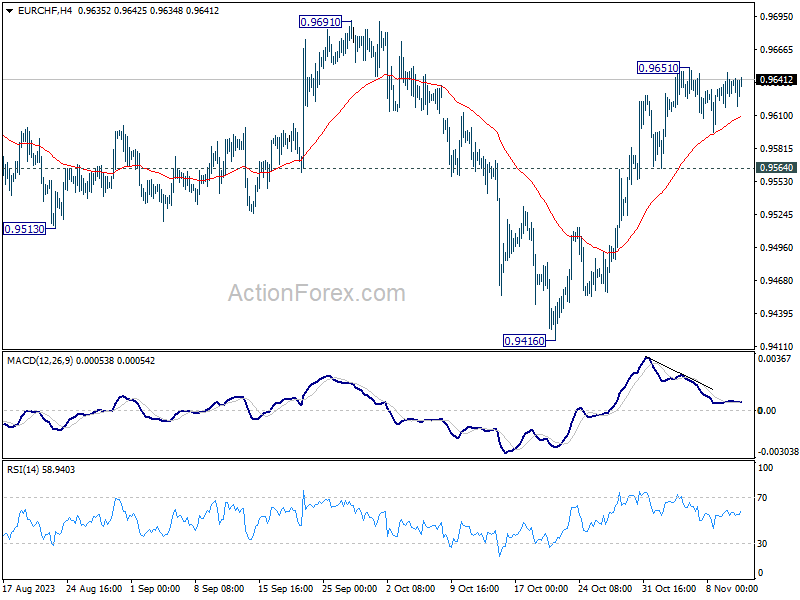

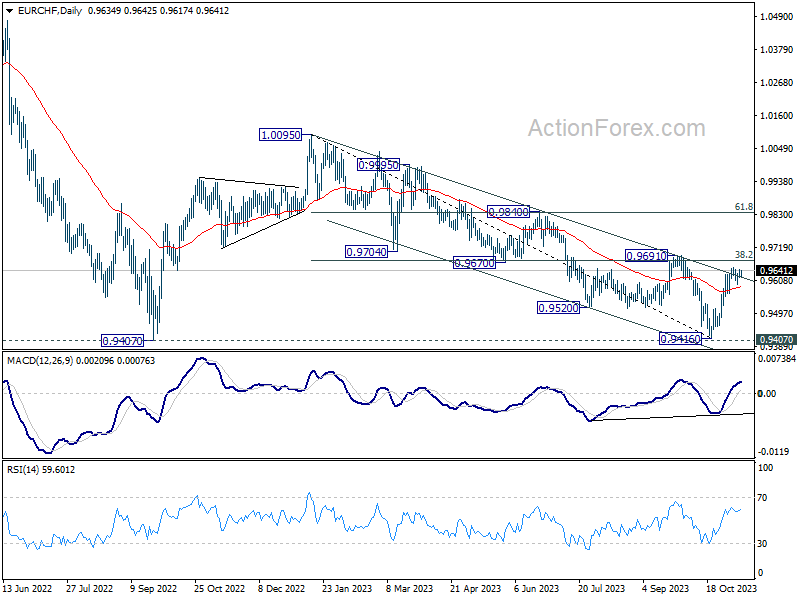

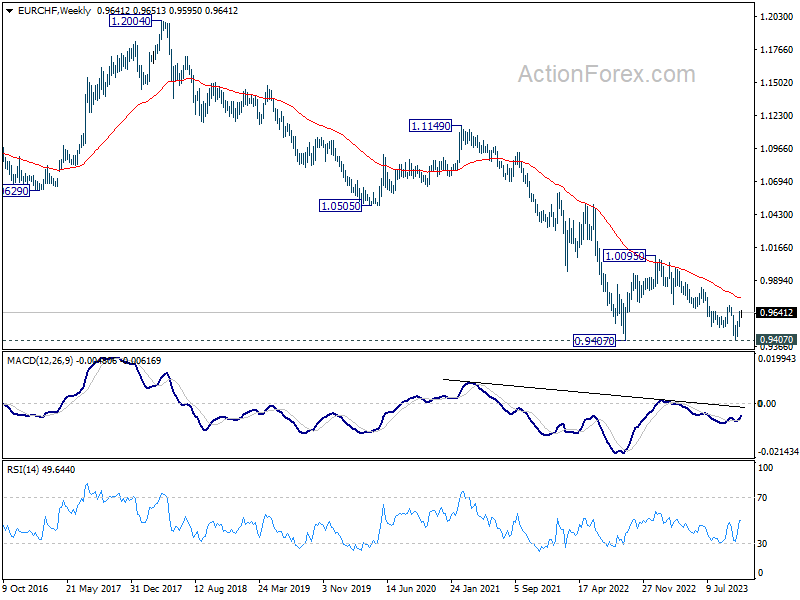

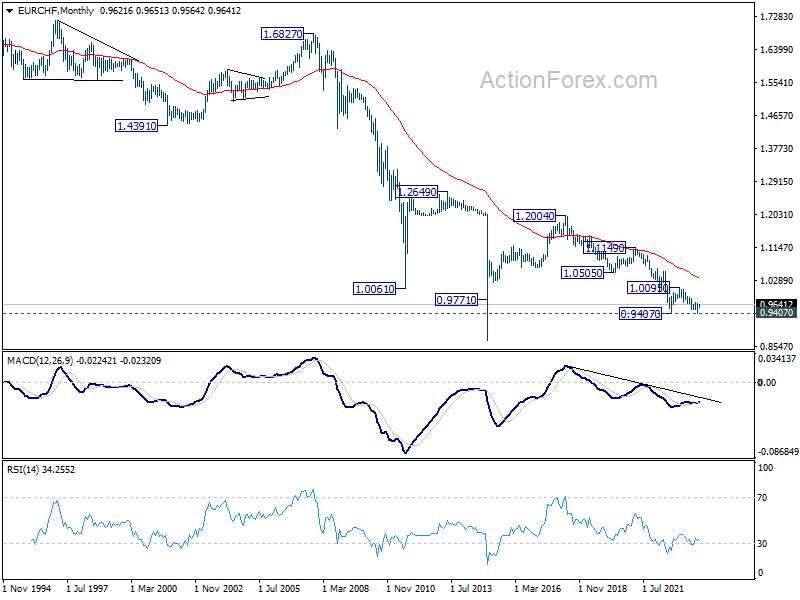

EUR/CHF Weekly Outlook

EUR/CHF edged higher to 0.9651 last week but turned into sideway consolidation then. Initial bias stays neutral this week first. Another dip cannot be ruled out. But downside should be contained by 0.9564 support to bring another rally. On the upside, break of 0.9651 will resume the rise from 0.9416 to 0.9691 resistance first. Firm break there will argue that whole decline from 1.0095 has completed at 0.9416, just ahead of 0.9407 support (2022 low).

In the bigger picture, fall from 1.0095 (2023 high) might have completed at 0.9416, just ahead of 0.9407 support (2022 low). Sustained break of 0.9691 cluster resistance (38.2% retracement of 1.0095 to 0.9416 at 0.9675) will pave the way to 61.8% retracement at 0.9836 and above. However, rejection by 0.9691 will maintain medium term bearishness for another test on 0.9407 at least.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0341). Price actions from 0.9407 are viewed as a three-wave consolidation pattern first. Larger down trend from 1.2004 (2018 high) might still resume through 0.9407 at a later stage. Break of 1.0095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

Weekly Economic & Financial Commentary: Long and Variable Lags Evident in Credit Availability

Summary

United States: Long and Variable Lags Evident in Credit Availability

- Ben Franklin famously said, “If you would know the value of money, try to borrow some.” Amid a light calendar for economic data, we focus this week on how lenders tightened standards for most loan types in Q3 even as demand for loans weakened, according to the Federal Reserve's Senior Loan Officer Opinion Survey (SLOOS).

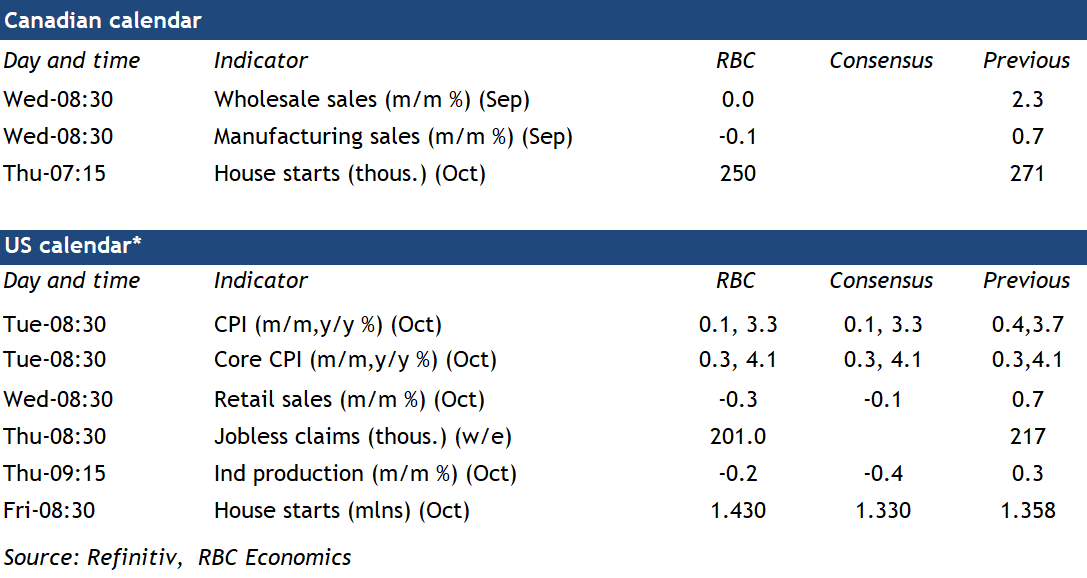

- Next week: CPI (Tue.), Retail Sales (Wed.), Housing Starts (Fri.)

International: British Economy Stalls During the Third Quarter

- The U.K. economy stalled during the third quarter, as Q3 GDP registered a flat quarter-over-quarter outcome. While that was better than the consensus forecast for a small decline, the details of the report were less encouraging. Consumer spending, government spending and business investment all fell during the quarter, indicative of very weak domestic demand. We still expect the U.K. to fall into a mild recession through late 2023 and into early 2024.

- Next week: Japan GDP (Wed.), China Industrial Production & Retail Sales (Wed.), U.K. CPI (Wed.)

Interest Rate Watch: Reserve Bank of Australia Resumes Rate Hikes

- While the Federal Reserve and many of the world's other major central banks are currently on hold, a few central banks are continuing to nudge interest rates higher. One such institution is the Reserve Bank of Australia (RBA), which, after remaining on pause since July, resumed its monetary tightening cycle this week with a 25 bps policy rate increase to 4.35%.

Topic of the Week: Census Projects Population Dip in 2080

- This week, the U.S. Census Bureau released its first population projections incorporating the results of the 2020 Census. The projections, stretching into 2100, show population growth plateauing over the next few decades. The population is expected to peak at 370 million in 2080 before contracting in the following years.

The Weekly Bottom Line: ‘Higher for Longer’ is the BoC’s Winning Strategy

U.S. Highlights

- The risk of a government shutdown has returned as Congress has one week left before the continuing resolution passed on September 30th expires.

- The Federal Reserve’s Senior Loan Officer Opinion Survey showed that banks continued to tighten credit standards in the third quarter, as credit demand weakened further.

- Consumer credit growth eased in the third quarter as an acceleration in revolving credit growth (i.e. credit cards) was offset by a contraction in nonrevolving credit (i.e. student loans).

Canadian Highlights

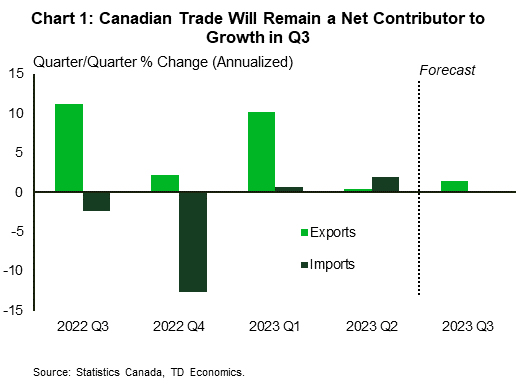

- Merchandise trade data out this week showed a further widening in Canada’s trade surplus in September, suggesting net trade will make a positive contribution to Q3 growth.

- The minutes from the Bank of Canada’s policy discussions showed that “lack of downward momentum” on the inflation front remained the top concern for policymakers and was behind the difference in opinion on whether more hikes are needed.

- The Senior Deputy Governor Carolyn Rogers delivered an update on the Financial Systems Review where she warned households and businesses to prepare for a “new normal”, where the cost of borrowing is likely to remain elevated over the medium-term.

U.S. – Government Shutdown Risk Redux

After last week’s busy slate markets took a breather to digest last week’s Federal Reserve policy decision and prepare for the risk of another potential government shutdown next Friday. On the data front, the Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) and consumer credit report both showed credit conditions remained tight and demand continues to wane.

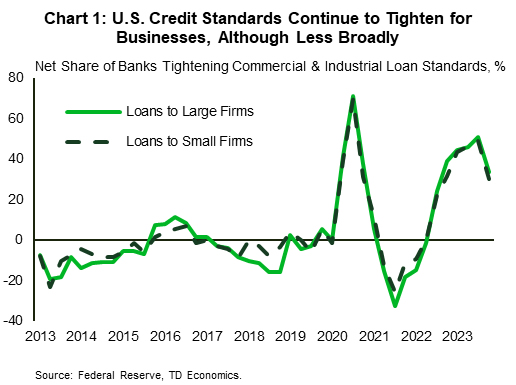

Monday’s release of the SLOOS showed that banks continued to tighten credit standards across loan categories in the third quarter and report weaker business and consumer demand for loans (see here). Although this came as little surprise considering Treasury yields rose by roughly 100 basis-points in Q3, the share of banks reporting tighter standards for commercial and industrial loans actually declined relative to the second quarter (Chart 1). This also held true for consumer credit cards and auto loans, although personal and mortgage loans each saw broader tightening relative to the second quarter. Despite the modest narrowing of credit tightening in the third quarter, the Federal Reserve’s continued signaling of rates staying higher for longer means a material loosening of credit standards likely remains a way off.

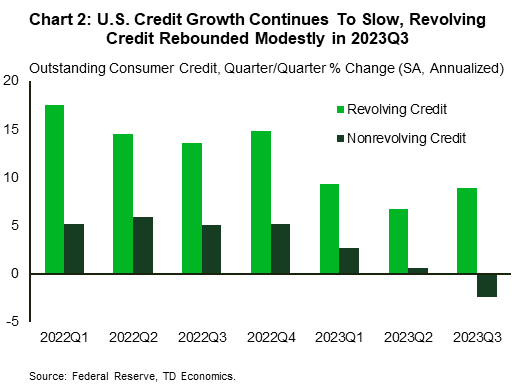

Easing consumer demand for loans was also evident in the Federal Reserve’s consumer credit data release on Tuesday which showed outstanding credit growth slowed notably relative to the second quarter. Outstanding revolving credit loans, which includes credit cards, saw accelerating growth in the third quarter of 8.6% while non-revolving credit growth, which includes student loans, declined by 2.4% (Chart 2). Under the weight of higher prices many consumers are increasingly relying on revolving credit to support spending, particularly as the moratorium on student loan repayment ends. Next week’s retail sales data will show whether the past six months of real sales growth, aided by consumer credit, continued into October despite the growing headwinds facing consumers.

In addition, updated CPI data out next week is expected to show continued easing in aggregate price pressures, supported by cooling energy prices. While this would undoubtedly be positive news, core inflation, which excludes food and energy prices, is expected to persist well above the Federal Reserve’s 2% target. A majority of FOMC members have noted that their current pause is conditional on sustained disinflation progress, with Chair Powell stating on Thursday that “if it becomes appropriate to tighten policy further, we will not hesitate to do so”.

Rounding out the coming week is the return of the risk of a potential government shutdown (see here) as the continuing resolution passed on September 30th expires on Friday, November 17th. Of the twelve appropriation bills that need to be passed to fund the federal government, the House has passed seven and the Senate has passed three with no consolidated bill managing to pass both chambers of Congress. This means that another continuing resolution may be used as a stopgap once again, but markets are likely to become increasingly apprehensive as Friday’s deadline approaches.

Canada – 'Higher for Longer' is the BoC's Winning Strategy

This week was sparse on economic data but rich on remarks from the Central Bank. Neither had a significant impact on the markets, with the TSX largely building on the dynamics across global equity markets, and finishing the week slightly lower. Volatility in the bond market returned by Thursday, reflecting the anxiety south of the border where weak demand in the 30-year auction helped to push the term premium higher. The only sigh of relief came from oil prices, although the decline in crude was driven largely by expectations for slowing global demand rather than peace in the Middle East.

On the macro front, Statistics Canada reported September's data on merchandise trade, which recorded a second consecutive month of trade surplus, with exports gaining slightly more than imports. This offset the negative impact from the B.C. port strike and Nova Scotia floods, observed earlier in the quarter. Exports also outperformed imports in volume terms, which means trade will be a net contributor to Q3 growth.

Looking ahead, the minutes from the Bank of Canada's policy discussions indicated an anticipated slowdown in exports, attributed to a decrease in global demand. But it was concerns of the disinflationary process stalling that remained the top concern for the Governing Council. Higher global oil prices, rising cost of rent and other housing-related costs, driven by demand-supply imbalances, have been the primary factors leading to the recent stalling in disinflationary dynamics. Moreover, despite the ongoing easing in the labour market, wage growth remains in a range that's higher than is needed to help push inflation down towards the BoC's target. This 'lack of downward momentum' was behind the difference in opinion on whether more hikes are needed.

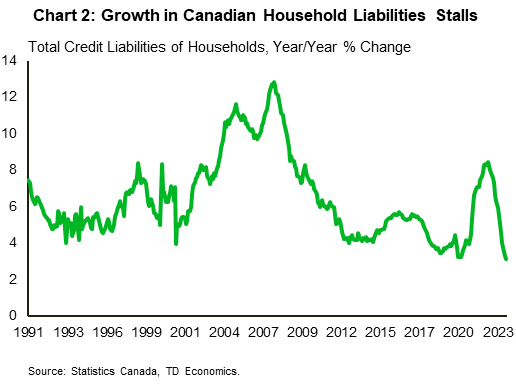

Despite these concerns, members observed that the 475 basis points in rate hikes have helped to rebalance the economy. Consumer spending and household credit growth are both showing signs of slowing, as households continue to adjust to higher borrowing costs (Chart 2). This message was echoed by the Senior Deputy Governor Carolyn Rogers who delivered an update on the Financial Systems Review. She reiterated that servicing debt is getting harder for some households, which can be observed through higher consumer delinquency rates and a rising share of accounts with utilization rates above 90%.

Rogers also pushed back on the expectations for lower rates and advised households and businesses to prepare for a 'new normal', where the cost of borrowing is likely to remain elevated. 'Higher for longer' rhetoric remains the winning strategy for the Bank as it keeps financial conditions tight without adjusting the policy rate. With little hard data to mull over, markets are likely to remain in 'wait and see' mode until the CPI report on November 21st. Next week, we'll get the most recent reading on existing home sales, which will provide an update on whether recent weakness gained more traction in October alongside the sharp uptick in yields. Stay tuned!

Softer Canadian Production and Lower US Inflation on Tap Next Week

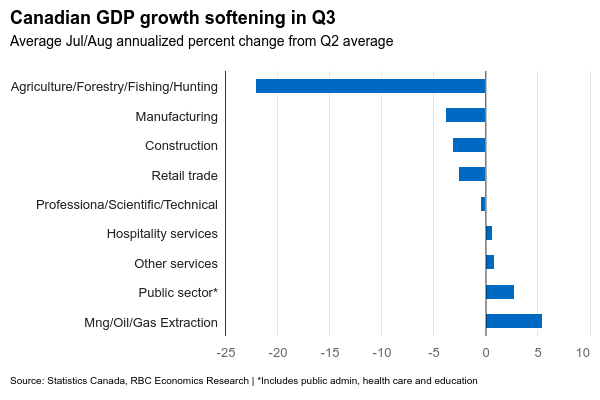

The advance estimate from Statistics Canada was that September Canadian manufacturing sales edged down 0.1% from August, despite another monthly surge in petroleum and coal prices. Manufacturing prices were up ~1% in September on a seasonally adjusted basis by our count, implying the volume of sales (excluding price impacts) declined even more after already contracting 0.7% in August. Indeed, economic growth in Canada is starting to look substantially softer. Consumer related sectors have weakened significantly – retail sales are tracking below Q2 levels to-date in Q3 and hospitality services (like restaurants and hotels) have flatlined. But cooling demand globally is also filtering down supply chains and slowing manufacturing output with the broader economy on track for another small quarterly decline in Q3.

Across the border, spending among US consumers has been much more resilient. Retail sales grew at an average pace of 0.5% per month in Q3, almost double the rate in pre-pandemic 2019. Next week’s October data will be among the first indications of how much of that momentum carried into Q4 (and the important holiday shopping period). We continue to expect strength in consumer spending to wane. October marked the restart of the student loan repayment program, and labour market conditions in the U.S. are starting to deteriorate. Employment growth has remained positive, but the rise in the unemployment rate over the last three months is similar to what has usually been seen at the start of a downturn in labour markets. The U.S. Fed will be watching next week’s October U.S. CPI report closely. Inflation pressures ticked higher in September – breaking a string of softer price growth readings. But a drop in gasoline prices should push headline year-over-year CPI growth lower in October. Core CPI in September was propped up by a larger increase in the owner’s equivalent rent index but that was not expected to be repeated this month. As indicated by Powell in his speech at the IMF yesterday, the Fed is still willing to hike interest rates further if needed. But we continue to expect slower consumer spending and deteriorating labour market conditions will keep the central bank on the sidelines, before pivoting to gradual rate cuts in the second quarter of next year.

Week ahead data watch

Canadian manufacturing sales likely inched down 0.1% in September, primarily driven by lower sales in metal and transportation equipment subsectors and despite a sharp price-led increase in petroleum sales.

Core wholesale sales are expected to remain unchanged from the prior month, in line with Statistics Canada’s early estimate. The preliminary estimate showed sales in auto and food subsectors with the largest increases, offsetting a pullback from machinery and equipment sales.

We anticipate U.S. retail sales to edge down 0.3% in October. Gasoline station sales likely fell on lower prices.

We look for a pullback in industrial production (-0.2%), with lower outputs in manufacturing and utility sectors.

Summary 11/13 – 11/17

Monday, Nov 13, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Oct | 50.7 | |

| 23:50 | JPY | PPI Y/Y Oct | 0.90% | 2.00% |

| 06:00 | JPY | Machine Tool Orders Y/Y Oct P | -11.20% | |

| 10:00 | EUR | EU Economic Forecasts | ||

| 23:30 | AUD | Westpac Consumer Confidence Nov | 2.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Oct | |

| Forecast: | Previous: 50.7 | ||

| 23:50 | JPY | PPI Y/Y Oct | |

| Forecast: 0.90% | Previous: 2.00% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Oct P | |

| Forecast: | Previous: -11.20% | ||

| 10:00 | EUR | EU Economic Forecasts | |

| Forecast: | Previous: | ||

| 23:30 | AUD | Westpac Consumer Confidence Nov | |

| Forecast: | Previous: 2.90% | ||

Tuesday, Nov 14, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | NAB Business Conditions Oct | 11 | |

| 00:30 | AUD | NAB Business Confidence Oct | 1 | |

| 07:00 | GBP | Claimant Count Change Oct | 15.0K | 20.4K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Sep | 4.20% | 4.20% |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Sep | 7.40% | 8.10% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Sep | 7.70% | 7.80% |

| 07:30 | CHF | Producer and Import Prices M/M Oct | 0.10% | -0.10% |

| 07:30 | CHF | Producer and Import Prices Y/Y Oct | -1.00% | |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | -0.10% | -0.10% |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 P | 0.20% | 0.20% |

| 10:00 | EUR | Germany ZEW Economic Sentiment Nov | 4.9 | -1.1 |

| 10:00 | EUR | Germany ZEW Current Situation Nov | -75.5 | -79.9 |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | 6.1 | 2.3 |

| 13:30 | USD | CPI M/M Oct | 0.10% | 0.40% |

| 13:30 | USD | CPI Y/Y Oct | 3.30% | 3.70% |

| 13:30 | USD | CPI Core M/M Oct | 0.30% | 0.30% |

| 13:30 | USD | CPI Core Y/Y Oct | 4.10% | 4.10% |

| 23:50 | JPY | GDP Q/Q Q3 P | -0.10% | 1.20% |

| 23:50 | JPY | GDP Deflator Y/Y Q3 P | 4.80% | 3.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | NAB Business Conditions Oct | |

| Forecast: | Previous: 11 | ||

| 00:30 | AUD | NAB Business Confidence Oct | |

| Forecast: | Previous: 1 | ||

| 07:00 | GBP | Claimant Count Change Oct | |

| Forecast: 15.0K | Previous: 20.4K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Sep | |

| Forecast: 4.20% | Previous: 4.20% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Sep | |

| Forecast: 7.40% | Previous: 8.10% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Sep | |

| Forecast: 7.70% | Previous: 7.80% | ||

| 07:30 | CHF | Producer and Import Prices M/M Oct | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Oct | |

| Forecast: | Previous: -1.00% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 P | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Nov | |

| Forecast: 4.9 | Previous: -1.1 | ||

| 10:00 | EUR | Germany ZEW Current Situation Nov | |

| Forecast: -75.5 | Previous: -79.9 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | |

| Forecast: 6.1 | Previous: 2.3 | ||

| 13:30 | USD | CPI M/M Oct | |

| Forecast: 0.10% | Previous: 0.40% | ||

| 13:30 | USD | CPI Y/Y Oct | |

| Forecast: 3.30% | Previous: 3.70% | ||

| 13:30 | USD | CPI Core M/M Oct | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 13:30 | USD | CPI Core Y/Y Oct | |

| Forecast: 4.10% | Previous: 4.10% | ||

| 23:50 | JPY | GDP Q/Q Q3 P | |

| Forecast: -0.10% | Previous: 1.20% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q3 P | |

| Forecast: 4.80% | Previous: 3.50% | ||

Wednesday, Nov 15, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Wage Price Index Q/Q Q3 | 1.30% | 0.80% |

| 02:00 | CNY | Industrial Production Y/Y Oct | 4.50% | 4.50% |

| 02:00 | CNY | Retail Sales Y/Y Oct | 7.00% | 5.50% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Oct | 3.10% | 3.10% |

| 04:30 | JPY | Industrial Production M/M Sep F | 0.20% | 0.20% |

| 07:00 | GBP | CPI M/M Oct | 0.20% | 0.50% |

| 07:00 | GBP | CPI Y/Y Oct | 4.70% | 6.70% |

| 07:00 | GBP | RPI M/M Oct | 0.50% | |

| 07:00 | GBP | RPI Y/Y Oct | 6.60% | 8.90% |

| 07:00 | GBP | PPI Input M/M Oct | 0.10% | 0.40% |

| 07:00 | GBP | PPI Input Y/Y Oct | -2.60% | |

| 07:00 | GBP | PPI Output M/M Oct | 0.10% | 0.40% |

| 07:00 | GBP | PPI Output Y/Y Oct | -0.10% | |

| 07:00 | GBP | PPI Core Output M/M Oct | 0.00% | |

| 07:00 | GBP | PPI Core Output Y/Y Oct | 0.70% | |

| 07:00 | GBP | Core CPI Y/Y Oct | 5.80% | 6.10% |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | 12.3B | 11.9B |

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | -0.90% | 0.60% |

| 13:30 | CAD | Manufacturing Sales M/M Sep | 0.80% | 0.70% |

| 13:30 | CAD | Wholesale Sales M/M Sep | 1.40% | 2.30% |

| 13:30 | USD | Empire State Manufacturing Index Nov | -2.6 | -4.6 |

| 13:30 | USD | Retail Sales M/M Oct | -0.30% | 0.70% |

| 13:30 | USD | Retail Sales ex Autos M/M Oct | -0.20% | 0.60% |

| 13:30 | USD | PPI M/M Oct | 0.10% | 0.50% |

| 13:30 | USD | PPI Y/Y Oct | 2.20% | |

| 13:30 | USD | PPI Core M/M Oct | 0.20% | 0.30% |

| 13:30 | USD | PPI Core Y/Y Oct | 2.70% | |

| 15:00 | USD | Business Inventories Sep | 0.30% | 0.40% |

| 15:30 | USD | Crude Oil Inventories | ||

| 23:50 | JPY | Trade Balance (USD) Oct | -0.71T | -0.43T |

| 23:50 | JPY | Machinery Orders M/M Sep | 0.90% | -0.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Wage Price Index Q/Q Q3 | |

| Forecast: 1.30% | Previous: 0.80% | ||

| 02:00 | CNY | Industrial Production Y/Y Oct | |

| Forecast: 4.50% | Previous: 4.50% | ||

| 02:00 | CNY | Retail Sales Y/Y Oct | |

| Forecast: 7.00% | Previous: 5.50% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Oct | |

| Forecast: 3.10% | Previous: 3.10% | ||

| 04:30 | JPY | Industrial Production M/M Sep F | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 07:00 | GBP | CPI M/M Oct | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 07:00 | GBP | CPI Y/Y Oct | |

| Forecast: 4.70% | Previous: 6.70% | ||

| 07:00 | GBP | RPI M/M Oct | |

| Forecast: | Previous: 0.50% | ||

| 07:00 | GBP | RPI Y/Y Oct | |

| Forecast: 6.60% | Previous: 8.90% | ||

| 07:00 | GBP | PPI Input M/M Oct | |

| Forecast: 0.10% | Previous: 0.40% | ||

| 07:00 | GBP | PPI Input Y/Y Oct | |

| Forecast: | Previous: -2.60% | ||

| 07:00 | GBP | PPI Output M/M Oct | |

| Forecast: 0.10% | Previous: 0.40% | ||

| 07:00 | GBP | PPI Output Y/Y Oct | |

| Forecast: | Previous: -0.10% | ||

| 07:00 | GBP | PPI Core Output M/M Oct | |

| Forecast: | Previous: 0.00% | ||

| 07:00 | GBP | PPI Core Output Y/Y Oct | |

| Forecast: | Previous: 0.70% | ||

| 07:00 | GBP | Core CPI Y/Y Oct | |

| Forecast: 5.80% | Previous: 6.10% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | |

| Forecast: 12.3B | Previous: 11.9B | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | |

| Forecast: -0.90% | Previous: 0.60% | ||

| 13:30 | CAD | Manufacturing Sales M/M Sep | |

| Forecast: 0.80% | Previous: 0.70% | ||

| 13:30 | CAD | Wholesale Sales M/M Sep | |

| Forecast: 1.40% | Previous: 2.30% | ||

| 13:30 | USD | Empire State Manufacturing Index Nov | |

| Forecast: -2.6 | Previous: -4.6 | ||

| 13:30 | USD | Retail Sales M/M Oct | |

| Forecast: -0.30% | Previous: 0.70% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Oct | |

| Forecast: -0.20% | Previous: 0.60% | ||

| 13:30 | USD | PPI M/M Oct | |

| Forecast: 0.10% | Previous: 0.50% | ||

| 13:30 | USD | PPI Y/Y Oct | |

| Forecast: | Previous: 2.20% | ||

| 13:30 | USD | PPI Core M/M Oct | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 13:30 | USD | PPI Core Y/Y Oct | |

| Forecast: | Previous: 2.70% | ||

| 15:00 | USD | Business Inventories Sep | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Trade Balance (USD) Oct | |

| Forecast: -0.71T | Previous: -0.43T | ||

| 23:50 | JPY | Machinery Orders M/M Sep | |

| Forecast: 0.90% | Previous: -0.50% | ||

Thursday, Nov 16, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Nov | 4.80% | |

| 00:30 | AUD | Employment Change Oct | 22.8K | 6.7K |

| 00:30 | AUD | Unemployment Rate Oct | 3.70% | 3.60% |

| 04:30 | JPY | Tertiary Industry Index M/M Sep | -0.10% | -0.10% |

| 13:15 | CAD | Housing Starts Y/Y Oct | 255K | 270K |

| 13:30 | USD | Initial Jobless Claims (Nov 10) | 222K | 217K |

| 13:30 | USD | Import Price Index M/M Oct | -0.30% | 0.10% |

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Nov | -11 | -9 |

| 14:15 | USD | Industrial Production M/M Oct | -0.40% | 0.30% |

| 14:15 | USD | Capacity Utilization Oct | 79.40% | 79.70% |

| 15:00 | USD | Natural Gas Storage | ||

| 21:45 | NZD | PPI Output Q/Q Q3 | 0.20% | |

| 21:45 | NZD | PPI Input Q/Q Q3 | -0.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Nov | |

| Forecast: | Previous: 4.80% | ||

| 00:30 | AUD | Employment Change Oct | |

| Forecast: 22.8K | Previous: 6.7K | ||

| 00:30 | AUD | Unemployment Rate Oct | |

| Forecast: 3.70% | Previous: 3.60% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Sep | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 13:15 | CAD | Housing Starts Y/Y Oct | |

| Forecast: 255K | Previous: 270K | ||

| 13:30 | USD | Initial Jobless Claims (Nov 10) | |

| Forecast: 222K | Previous: 217K | ||

| 13:30 | USD | Import Price Index M/M Oct | |

| Forecast: -0.30% | Previous: 0.10% | ||

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Nov | |

| Forecast: -11 | Previous: -9 | ||

| 14:15 | USD | Industrial Production M/M Oct | |

| Forecast: -0.40% | Previous: 0.30% | ||

| 14:15 | USD | Capacity Utilization Oct | |

| Forecast: 79.40% | Previous: 79.70% | ||

| 15:00 | USD | Natural Gas Storage | |

| Forecast: | Previous: | ||

| 21:45 | NZD | PPI Output Q/Q Q3 | |

| Forecast: | Previous: 0.20% | ||

| 21:45 | NZD | PPI Input Q/Q Q3 | |

| Forecast: | Previous: -0.20% | ||

Friday, Nov 17, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | GBP | Retail Sales M/M Oct | 0.30% | -0.90% |

| 09:00 | EUR | Eurozone Current Account (EUR) Sep | 20.3B | 27.7B |

| 10:00 | EUR | Eurozone CPI Y/Y Oct F | 2.90% | 2.90% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct F | 4.20% | 4.20% |

| 13:30 | CAD | Industrial Product Price M/M Oct | 0.40% | |

| 13:30 | CAD | Raw Material Price Index Oct | 3.50% | |

| 13:30 | USD | Building Permits Oct | 1.45M | 1.47M |

| 13:30 | USD | Housing Starts Oct | 1.36M | 1.36M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | GBP | Retail Sales M/M Oct | |

| Forecast: 0.30% | Previous: -0.90% | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Sep | |

| Forecast: 20.3B | Previous: 27.7B | ||

| 10:00 | EUR | Eurozone CPI Y/Y Oct F | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct F | |

| Forecast: 4.20% | Previous: 4.20% | ||

| 13:30 | CAD | Industrial Product Price M/M Oct | |

| Forecast: | Previous: 0.40% | ||

| 13:30 | CAD | Raw Material Price Index Oct | |

| Forecast: | Previous: 3.50% | ||

| 13:30 | USD | Building Permits Oct | |

| Forecast: 1.45M | Previous: 1.47M | ||

| 13:30 | USD | Housing Starts Oct | |

| Forecast: 1.36M | Previous: 1.36M | ||

Sunset Market Commentary

Markets

Fed Chair Powell’s comments at the IMF’s annual research conference echoed through today’s trading session amid an empty eco calendar. He provided several hawkish accents to the same underlying message from the early November policy meeting. In doing so, he managed to push back against the (rate) correction that followed so far this month. First, he argued that the easy disinflation gains are over, warning that getting back inflation to the 2% target from current levels will be a much tougher challenge and “a long way to go”. This is a warning that policy rate cut bets in Q2 2024 seem premature. The Fed won’t be fooled by monthly head fakes, keeping policy restrictive until they are absolutely sure that inflation will return to the 2% target. Second, if it becomes appropriate to tighten policy further, the Fed will not hesitate to do so. The US central bank walks a tightrope between overtightening and doing too little in case of feeling too comfortable by a few months of good data. An additional rate hike doesn’t seem to the preferred scenario for the moment but the Fed is attentive to the risk that stronger growth could undermine further progress in restoring balance to the labour market and in bringing inflation down. Finally he touched on the topic of tighter financial conditions, Powell said that the Fed would not be ignorant to a significant tightening but that the effect on policy would largely depend on how long the market move lasted. German Bund yields had some catching up to do compared with yesterday’s US yield increases. They currently add 2.8 bps (30-yr) to 5.5 bps (5-yr) with the belly of the curve outperforming the wings. Intraday gains had been double these amounts though with momentum fading after 10-yr yields failed to take out the week tops in Germany (2.76%) and the US (4.67%). The trade weighted dollar’s comeback bumped into the 106 big figure with EUR/USD treading water near 1.0680. European stock market currently lose 0.5%-1%, but intraday losses had been bigger. From a technical point of view, both European (EuroStoxx50) and US (S&P 500, Nasdaq) indices failed to take out October tops and breaking the ruling sell-on-upticks pattern. Sterling initially avoided more weakness on a flat Q3 GDP print (vs -0.1% Q/Q), but details didn’t provide much comfort. Add the risk-off market climate and you and up with EUR/GBP testing the 0.8754 October top. We hold our view for a bullish break in the FX pair.

News & Views

Czech inflation jumped from 6.9% to 8.5% y/y in October. Given the mere 0.1% m/m increase, the reacceleration was exclusively due to last year’s low comparison base, when a sharp decline in prices for household electricity (energy savings tariff) was recorded. The monthly increase was mainly driven by seasonally more expensive clothing and higher food prices, while housing costs fell thanks to lower electricity, gas and heating prices. The headline figure topped the Czech National Bank’s 8.3% Autumn forecast but core inflation came in slightly lower than expected (4.3% vs 4.2% actual value). Commenting the numbers, the CNB said the latter reflected a “fading of growth in prices of foreign inputs and a cooling of domestic demand.” The CNB isn’t worried about this headline uptick. The aforementioned base effect drops out in January 2024 and will prompt a reading close to the 2% target. The Czech koruna initially extended minor gains before paring them again. EUR/CZK is currently trading slightly weaker around 24.52. Front end Czech swap yields rose in a kneejerk move but are now down 5 bps on the day. The numbers confirm KBC Economic’s view of the CNB starting the cutting cycle in December with a 25 bps move.

Price pressures in Hungary returned into the single digits for the first time since April 2022. The 9.9% y/y increase in October was a sharp drop from the 12.2% reading the month before and was helped lower by a negative 0.1% m/m outcome. Consensus stood at a 0.3% m/m and 10.4% rise. The Hungarian central bank (MNB) core inflation estimates eased too but all of them remained (well) above 10%, varying between 10.9% and 11.9%. The MNB recently lowered the policy rate by a more-than-expected 75 bps to 12.25%. Additional rate cuts will follow but their size is determined by the disinflationary process and the Hungarian forint. As the former went more swiftly and the latter even appreciated to the strongest level in three months after today’s numbers (EUR/HUF 377.3), there’s a real possibility the MNB is readying a 100 bps cut later this month. Money markets price in such a move at the two remaining policy meetings of the year. Hungarian swap yields tumble more than 10 bps at the front of the curve.

Week Ahead – US and UK Inflation Data to Take Center Stage

- US inflation numbers the next event to shake up Fed bets

- Pound traders lock gaze on CPIs after BoE’s hawkish hold

- Aussie awaits jobs report and Chinese data, Japan’s GDP also on tap

Can US CPIs convince investors about one more Fed hike

After taking a strong hit last Friday due to the disappointing US employment report, the dollar staged a shy recovery this week as several Fed officials noted that the stellar performance of the US economy keeps the door open to further rate increases. Just on Thursday, Fed Chair Powell said that they “are not confident” that interest rates are high enough to signal the end of their fight against inflation.

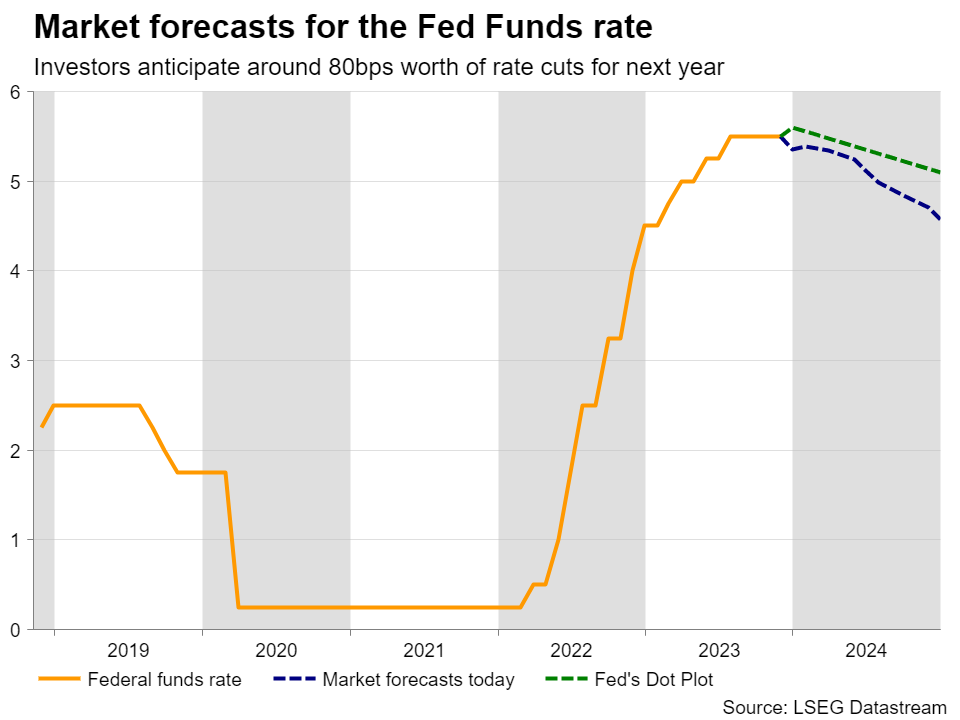

However, despite the recovery in the greenback, investors remained largely unconvinced that another hike may be on the table. According to Fed funds futures, they are assigning only a 20% probability for one last quarter-point increase by January, while pricing in around 80bps worth of rate cuts by the end of next year.

Maybe market participants expect inflation to pull back again, especially after the retreat in oil prices during October, and the economy to weaken going forward. Indeed, the Atlanta Fed GDPNow model estimates a 2.1% annualized growth rate for Q4, but in an environment of high interest rates and a stellar acceleration to 4.9% in Q3, this slowdown appears quite normal.

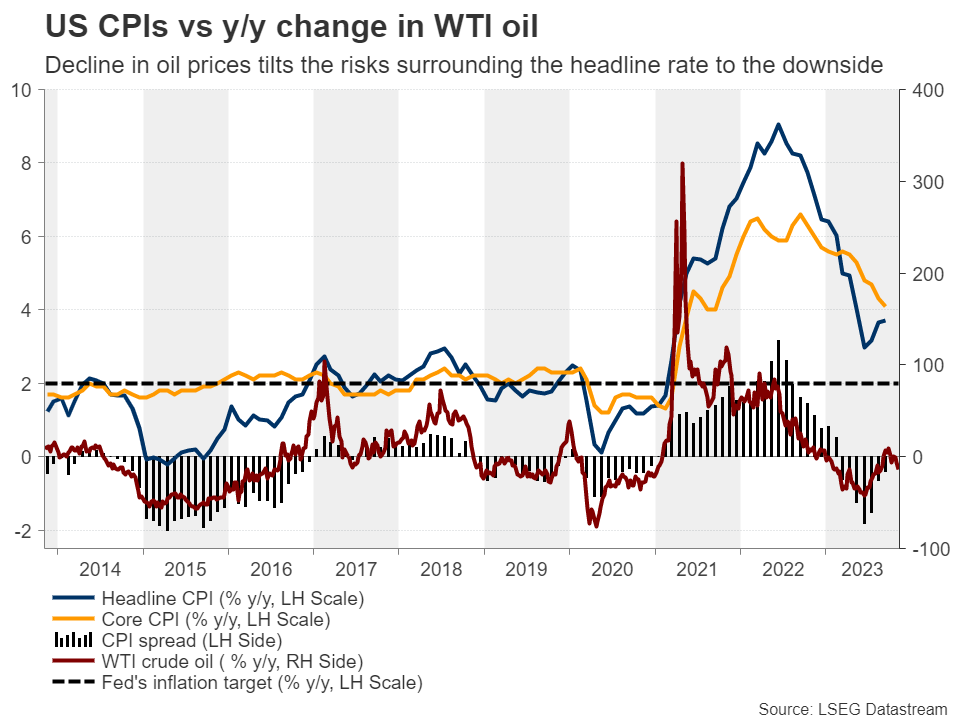

With all that in mind, next week, the spotlight is likely to turn to the US CPI data for October on Tuesday. The headline rate is expected to have pulled back to 3.3% y/y from 3.7% and the core one to have ticked down to 4.0% y/y from 4.1%. That said, considering that the PMIs for October suggested softer price pressures, the risks may be tilted to the downside, and with the y/y change in oil prices turning negative again, headline inflation could continue to soften going into year-end.

This could add credence to investors’ belief of no more rate hikes and several cuts for next year and perhaps hurt the dollar. However, as long as data relating to economic growth continues to suggest that the US economy is performing better than its major counterparts, any retreat in the greenback may just be a corrective phase. This could be confirmed if Wednesday’s retail sales and Thursday’s industrial production for October continue to point to a resilient US economy.

UK jobs and CPI data to affect the pound’s fate

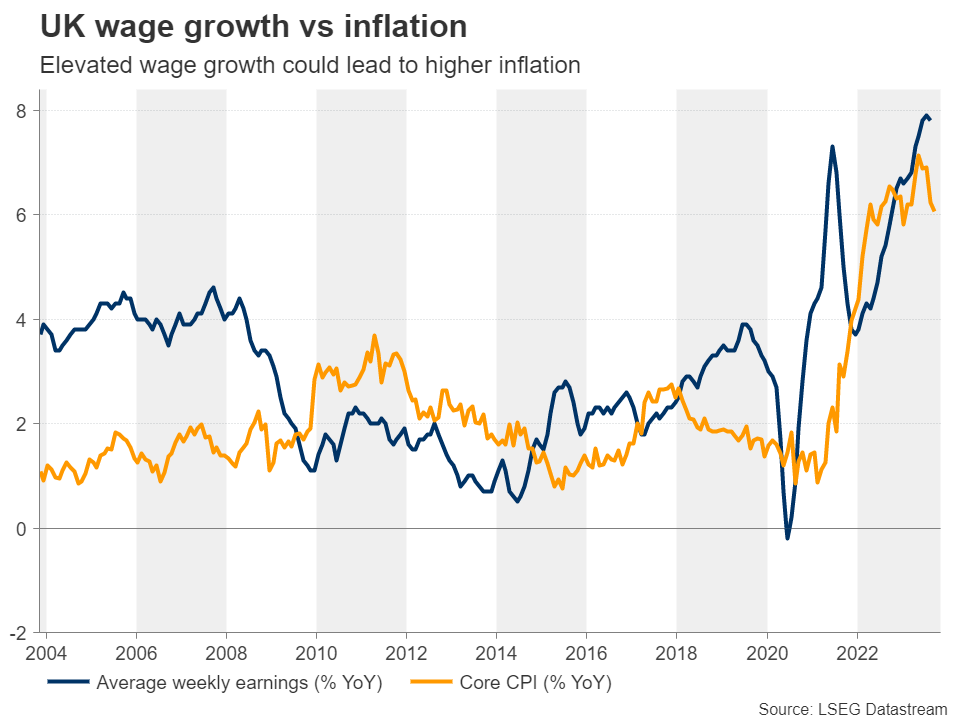

The UK also releases inflation data next week, on Wednesday. The headline CPI rate is anticipated to have slumped to 4.9% y/y from 6.7%, and the core one to have slid to 5.6% y/y from 6.1%. Nonetheless, according to the PMIs, prices charged by companies accelerated to a three-month high in October. Thus, in contrast to the US CPI data, there may be upside risks surrounding the UK numbers. Tuesday’s employment report for September could also be important as the average weekly earnings print may provide a glimpse of where inflation may be headed in upcoming months.

Last week, the BoE kept rates steady but noted that they remain willing to further raise them if there is evidence of more persistent inflationary pressures. Yet, investors see only a 15% probability of another hike. Ergo, data pointing to stickier-than-previously-expected inflation could boost that number, but even if they don’t, they may prompt investors to scale back some basis points worth of rate cuts anticipated for next year; not because of a brighter economic outlook but on fears that cutting massively to support the economy may result in inflation getting out of control, which could in turn lead to deeper economic wounds down the road. This, combined with cooler US inflation, could help Cable return above the key barrier of 1.2310 and perhaps emerge above its 200-day moving average. The nation’s retail sales for October are also coming out on Friday.

Aussie sets for volatility, Japan’s GDP to reveal contraction

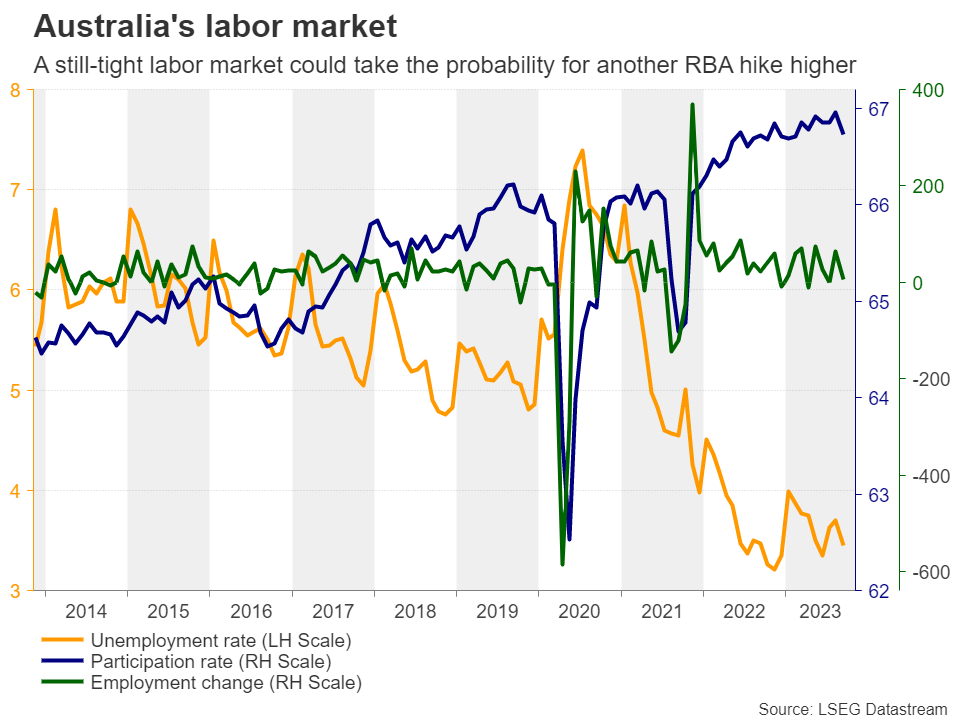

The aussie has been under pressure this week following the RBA’s dovish hike, as well as data and developments adding to concerns about China’s economic outlook. The probability of another hike at the December gathering is a coin toss, and thus traders may seek clarity in Australia’s employment numbers for October on Thursday. With the unemployment rate resting at historically low levels, labor conditions remain tight. The September data pointed to some cooling, but should next week’s numbers point to strength, the probability of a December hike may increase and the aussie could rebound.

However, any recovery could stay limited and short-lived if the Chinese numbers released the previous day add to the woes surrounding the world’s second largest economy. On Wednesday, investors will digest China’s industrial production, retail sales and fixed asset investment, all for October.

Japan’s preliminary GDP for Q3 is due to be released the same day. According to a Reuters poll, the Japanese economy likely shrank during the quarter, marking the first contraction in four quarters. Many analysts believe that the BoJ will phase out its ultra-loose policy next year, but a negative GDP figure could prove a challenge for the Bank’s plans and perhaps prompt traders to push the yen lower.

Weekly Focus – Maybe Not Quite So High for Quite So Long

The "higher for longer" narrative about interest rates was toned down in a week with little concrete news about the economy, based on recent indicators that inflation is coming down. Not least last Friday's US labour market report pointed in that direction, with job growth in October below expectations and downward revisions of the two preceding months, hourly earnings increasing just 0.2% in October, and private sector average working hours decreasing 0.3%. During the week, we have in general seen both a declining trend in bond yields and positive sentiment in equity markets. However, central banks have been eager to say that the inflation problem should not yet be considered solved, not least Fed Chairman Jerome Powell, who sent that message on Thursday, leading to a partial reversal of the previous market moves.

Helpful for the inflation outlook, oil prices have again dropped to around USD 80 per barrel. We see this as mostly another sign of markets becoming more convinced of a cooling world economy.

As central banks around the world emphasised during the week, it is still too soon to conclude that inflation has been vanquished. Wage growth in most Western countries remains above what is consistent with 2% inflation, including the US, by other measures than the hourly earnings from the job report. In the US this week, the Senior Loan Officer Opinion Survey showed that banks are not to the same extent as earlier experiencing declining credit demand, although it is clear that financial conditions are still a drag on activity and that credit standards are still being tightened. The Reserve Bank of Australia actually hiked its rates by 25bp to 4.35% for the Cash Rate as it saw especially services inflation being more persistent than anticipated. The Polish central bank had been expected to cut rates this week, but did not do.

In China, however, deflation talk has returned to the headlines after CPI declined 0.2% y/y in October. This was driven by a 30% decline in pork prices, and we do not expect deflation to persist, but core inflation is low at 0.6% y/y and more economic stimulus is likely. Already in the coming week, there is a chance of a rate cut on Wednesday when we will also be following the meeting between Presidents Xi and Biden for signs of improvement in China-US relations. Also on Wednesday, a range of interesting Chinese data is released, not least home and retail sales.

Globally, the most important data release in the coming week will likely be US CPI where we expect energy prices to pull headline inflation lower. We see the underlying price pressure as moderate if still to the high side of the Fed's target. However, the October number could be distorted by the auto workers' strike leading to temporarily higher car prices and the effect from health insurance premiums.

The UK labour market report will be watched for signs of easing in the stubbornly high wage growth. Data from this week showed a stronger than expected economy with GDP unchanged in Q3 and growing 0.2% in September. In principle, it will also be important to see how the labour market more broadly is developing, but the data for employment and unemployment is currently "experimental".