Sample Category Title

GBP/USD Remains in Bearish Trend after Hawkish “Powell”

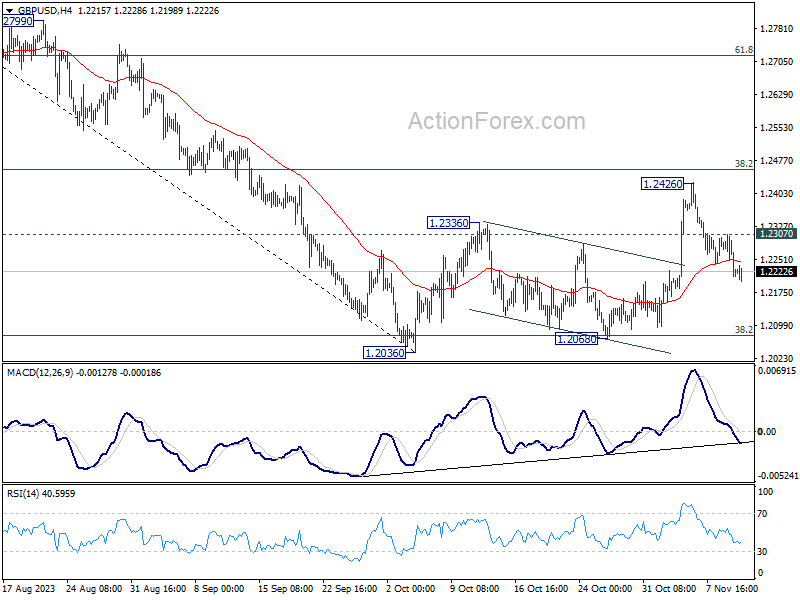

So, the USD turned up recently as investors again looking to sell it as Powell signaled that more hikes can be needed in the future, but it will depend on the data. As a result, US yields stabilized and stocks hit resistance while DXY comes higher and can still target the pre-NFP levels. This can be important short-term level; if it DXY goes above 106.40 then I think EUR and GBP will see more weakness. In fact, looking at the 4h time frame on cable and only three wave rally from the low, with wave (C) failing at the upper corrective channel, it appears that bearish trend is still here and ready to resume, especially if a price drops below 1.2190 bearish level. Then I think 1.2030 can come back in play.

ECB’s Lagarde cautions against complacency as swift disinflation phase may wane

ECB President Christine Lagarde, speaking at a Financial Times event, warned that the recent phase of quick disinflation might be nearing its end, with the potential for near-term inflation re-acceleration. This caution comes amid the possibility that the dampening effect of high energy prices on year-on-year comparisons may soon diminish.

Lagarde emphasized the need for vigilant monitoring of energy prices, suggesting that the current headline inflation figure of 2.9% shouldn't be taken for granted. "We should not assume that this respectable 2.9 headline number is something that should be taken for granted and for long," she stated.

Lagarde also alerted to the likelihood of seeing "a resurgence of probably higher numbers going forwards." She highlighted that even if energy prices stabilize, the dissipating base effect could lead to higher inflation figures in the early months of the coming year.

Despite these challenges, Lagarde reiterated her confidence in ECB's current interest rate policy. She believes that maintaining the current rate for a sufficient duration "will make a significant contribution to bringing inflation back to our 2% target."

However, she was quick to add a caveat, indicating that ECB's stance might need reevaluation in the face of major unforeseen shocks: "If major shocks come up, depending on the nature of the shocks, we'll have to revisit that."

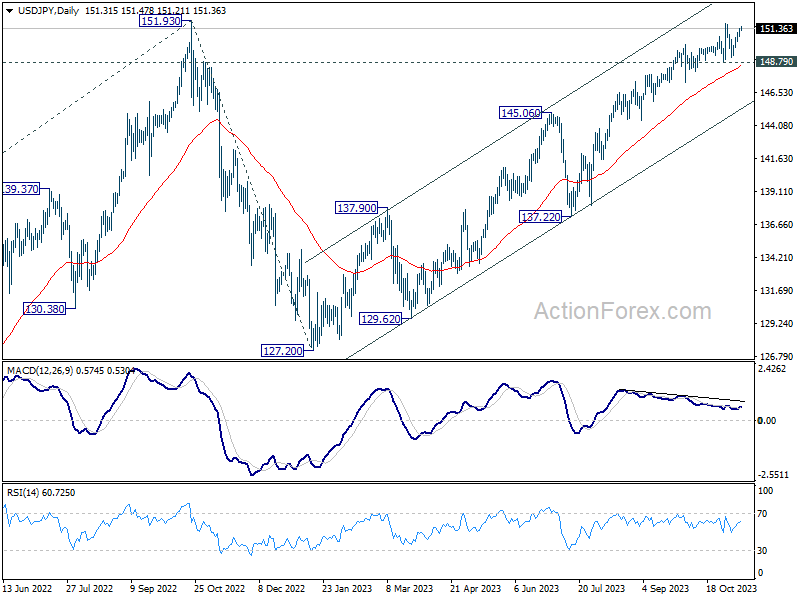

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.94; (P) 151.17; (R1) 151.56; More...

Range trading continues in USD/JPY and intraday bias remains neutral at this point. Another falling leg could be seen as consolidation from 151.69 extends, but further rally is expected as long as 148.79 support holds. Firm break of 151.69 high will resume larger up trend. However, decisive break of 148.79 will indicate rejection by 151.93 key resistance, and bring deeper fall through 147.28 support.

In the bigger picture, immediate focus is on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 to 151.93 from 127.20 at 157.69.

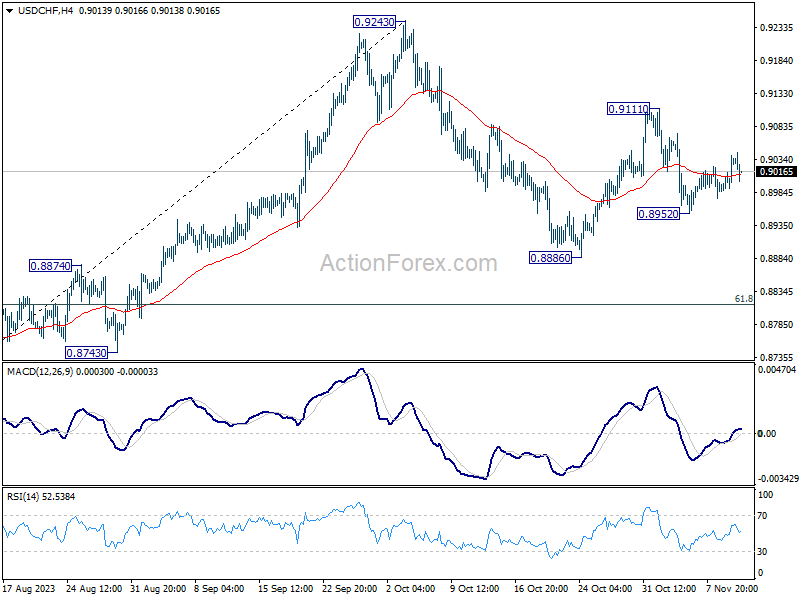

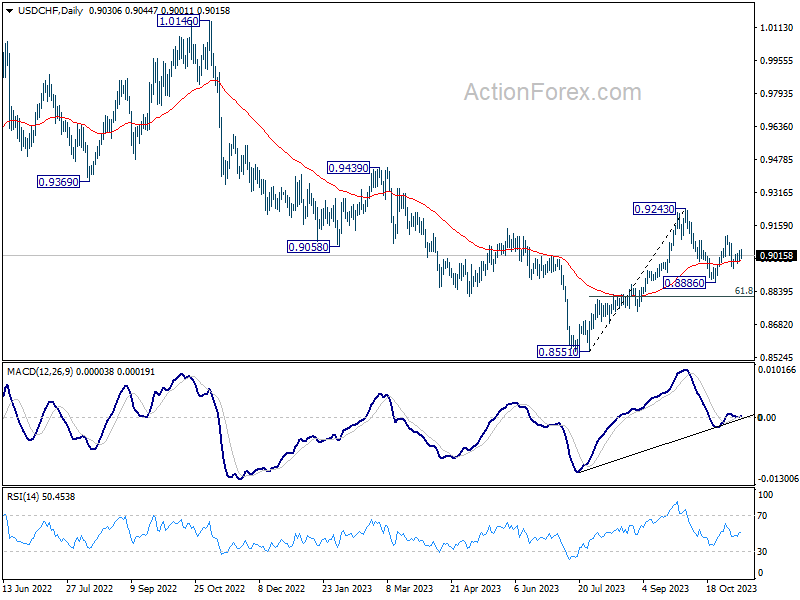

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8992; (P) 0.9017; (R1) 0.9053; More....

Intraday bias in USD/CHF stays neutral as range trading continues. On the downside, below 0.8952 will target a test on 0.8886 support first. Break there will resume whole decline from 0.9243 to 0.8815 fibonacci level. However, break of 0.9111 will resume the rebound from 0.8886 instead, and target 0.9243 resistance.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.

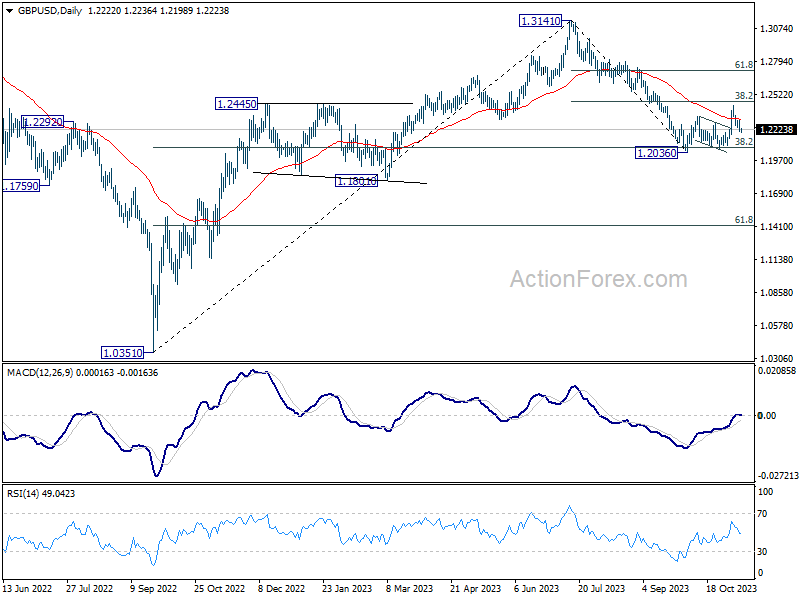

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2187; (P) 1.2248; (R1) 1.2283; More

Intraday bias in GBP/USD remains on the downside at this point. Corrective rebound from 1.2036 could have completed at 1.2426 already, just ahead of 38.2% retracement of 1.3141 to 1.2036 at 1.2458. Deeper fall would be seen back to retest 1.2036/68 support zone first. However, on the upside, break of 1.2307 minor resistance will dampen this bearish case, and turn intraday bias neutral first.

In the bigger picture, price actions from 1.3141 medium term top are seen as a correction to up trend from 1.3051 (2022 low). Strong rebound from 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will argue that it's a sideway pattern only. However, sustained break of 1.2036 will indicate that it's a deeper correction that would target 61.8% at 1.1417 before completion.

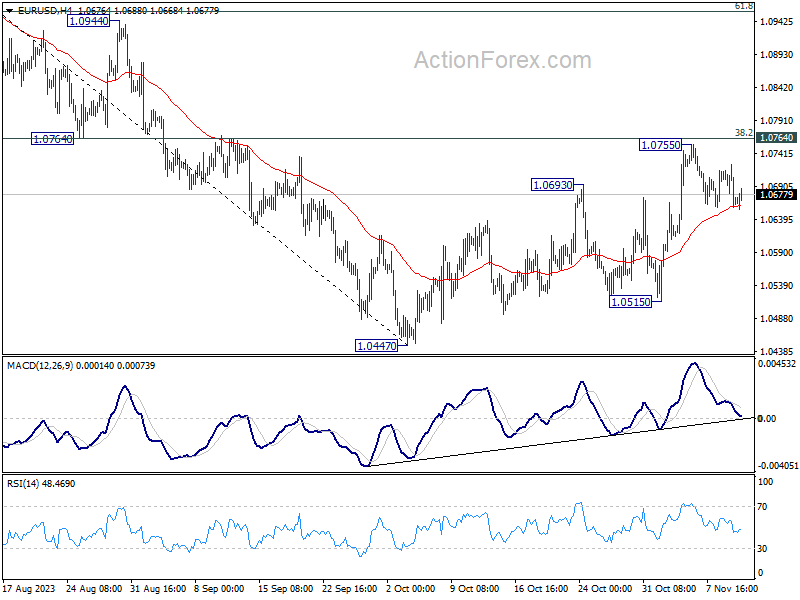

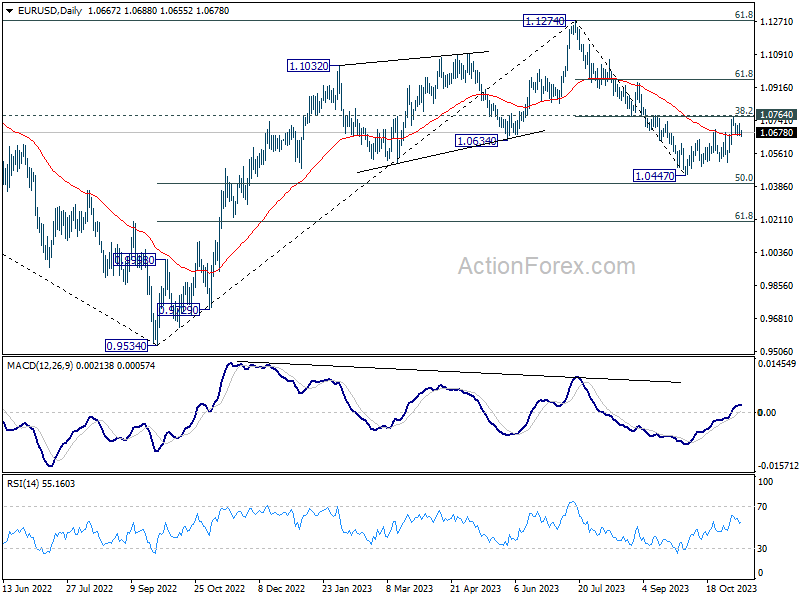

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0644; (P) 1.0685; (R1) 1.0709; More...

EUR/USD is trying to draw support from 55 4H EMA (now at 1.0657) and intraday bias remains neutral first. Further rise is in favor as long as this EMA holds. Decisive break of 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763) will extend the rise from 1.0447 to 61.8% retracement at 1.0958 next. However, sustained break of 55 4H EMA will argue that the rebound has completed, and target 1.0515 support, and then 1.0447 low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

Euro Gains Ground as Dollar Hesitates, Cryptos Surge

Today's currency market sees Euro gaining some traction, especially against Japanese Yen, which is underperforming alongside Australian Dollar. Despite RBA's hinting at a potential rate hike, Aussie is struggling, not only against major currencies but also against its commodity-linked counterparts. British Pound, too, is lagging behind despite UK reporting GDP figures marginally above expectations. Dollar is showing signs of firmness but is unable to muster a strong momentum to significantly build upon this week's recovery efforts.

In commodity markets, Gold is slipping below 1950 handle again. WTI crude oil is experiencing stagnation, hovering around 76 mark, following a notable decline earlier in the week. While US 10-year Treasury yield showcased an impressive bounce yesterday, it has not managed to maintain the upward trajectory, suggesting caution among bond investors.

A more optimistic note is seen in cryptocurrency market, where Bitcoin and Ethereum are showing significant bullish momentum. Bitcoin has successfully broken 37k mark, while Ethereum has powered through 2000 level, signaling intensifying investor interest in digital assets.

Technically, Ether now looks set to break through 2141.75 resistance to resume the whole rebound from 878.50. Key resistance level lies in 38.2% retracement of 4863.75 to 878.50 at 2400.85. (Bitcoin has already broken equivalent fibonacci resistance. Decisive break there could pave the way to 61.8% retracement at 3341.38 in the medium term. In any case, outlook will stay bullish as long as 1849.05 support holds.

In Europe, at the time of writing, FTSE is down -1.31%. DAX is down -0.68%. CAC is down -1.00%. Germany 10-year yield is up 0.0570 at 2.708. Earlier in Asia, Nikkei dropped -0.24%. Hong Kong HSI dropped -1.76%. China Shanghai SSE dropped -0.47%. Singapore Strait Times dropped -0.91%. Japan 10-year JGB yield rose 0.0153 to 0.857.

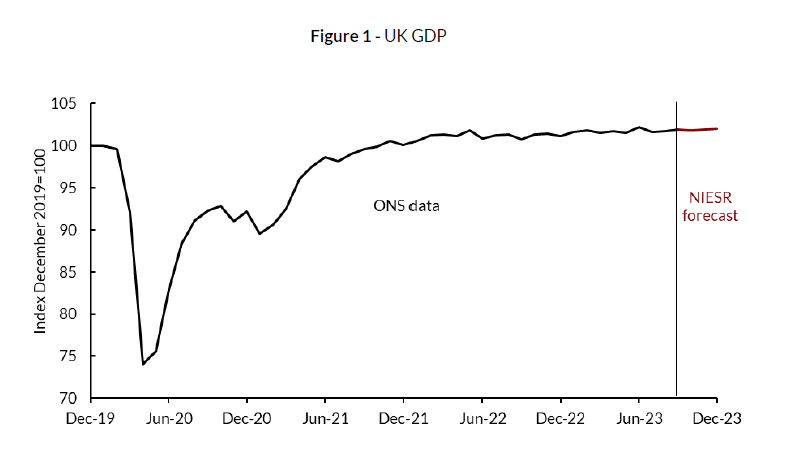

NIESR forecasts slight growth for UK economy, averting recession in 2023

According to NIESR's projections, UK economy is set to witness a marginal increase in GDP of 0.1% in the fourth quarter of this year. The institute's report highlighted, "Our central forecast does not expect a recession in 2023."

Delving into the specifics of the economic forecast, NIESR stated, "These forecasts remain broadly consistent with the longer-term trend of low, but stable economic growth in the United Kingdom."

Looking ahead to the next two years, NIESR expects the pace of growth to remain relatively subdued. The institute's report forecasts GDP growth of 0.6% for 2023, followed by further restrained growth of 0.5% in 2024. The primary cause for this muted growth, as per NIESR, is the ongoing productivity slump.

UK economy shows resilience: GDP up 0.2% mom in Sep, flat in Q3

UK's economy displayed unexpected resilience in today's data releases, GDP figures surpassed market expectations both on a monthly and quarterly basis.

In September, GDP grew by 0.2% mom, defying the stagnation prediction of 0.0% mom. This growth was primarily driven by a 0.2% increase in the services sector, a crucial component of the UK economy. Additionally, the construction sector contributed positively with a 0.4% mom= growth, while production remained steady with no significant change.

On a quarterly scale, GDP figures remained flat at 0.0%, which is a more favorable outcome compared to the anticipated contraction of -0.1% qoq. On a year-on-year basis, GDP registered a growth of 0.6% yoy, indicating a modest but steady recovery from the same quarter in the previous year.

The services sector experienced a slight contraction of -0.1% qoq, whereas construction saw a marginal growth of 0.1% qoq. The production sector's performance was broadly unchanged.

RBA's hawkish SoMP points to another rate hike

RBA's latest Statement on Monetary Policy presents a more hawkish picture than market observers anticipated, with upward revisions in both headline and underlying inflation projections, alongside stronger growth outlook.

More importantly, these projections rest on the assumption that cash rate will peak around 4.50%, comparing to the current 4.35%, suggesting another rate hike could be imminent.

RBA's heightened vigilance against inflation is clear: "The weight of recent information suggests that the risk of inflation remaining higher for longer has increased," the bank stated, highlighting domestic inflation persistence and possible global factors, such as energy market disruptions and food price hikes tied to El Niño effects.

Economic projections now show a year-average GDP growth expected to hit 2.00% in 2023, rising to 1.75% in 2024, and reaching 2.25% in 2025. These figures mark an upgrade from June's forecast of 1.50%, 1.25%, and 2.00% respectively, suggesting a resilient economy that could withstand tighter monetary policy.

Inflation forecasts have also been adjusted upward, with headline CPI inflation now seen at 4.50% at the year's end in 2023, followed by 3.50% in 2024, and softening to 3.00% in 2025. They are upgraded from 4.25%, 3.25% and 2.75% respectively.

The trimmed mean inflation follows a similar upward trajectory, projected to be at 4.50% in year-ended 2023, 3.25% in 2024, and 3.00% in 2025, up from prior forecast of 4.00%, 3.00%, and 2.75% respectively.

Underpinning these projections are technical assumptions of a cash rate peaking at around 4.50%, with a gradual decline to approximately 3.50% by the end of 2025, indicating a higher rate path than previously used.

NZ BNZ PMI fell to 42.5, manufacturing downturn reaches lowest point since 2009

October has marked a significant downturn for New Zealand's manufacturing sector, with BusinessNZ Performance of Manufacturing Index plummeting from 45.1 to 42.5. This figure not only represents the fifth consecutive month of declining activity but also stands as the lowest activity level for a month unaffected by COVID-19 restrictions since May 2009, deeply underscoring the sector's distress.

Delving into the components, the bleak picture becomes clearer: Production has taken a hit, sliding down from 44.3 to 41.5, and employment in the sector is also suffering, with a drop from 45.1 to 43.3. New orders barely held ground, marginally decreasing from 44.8 to 44.1. A significant retreat was seen in finished stocks, which contracted from 51.2 to 45.7, and deliveries were also on the downturn from 44.3 to 42.9.

Amidst these figures, the voice of the industry has tilted towards concern, with 65.1% of comments categorized as negative, albeit slightly less pessimistic than previous months, at 68.8% in September and 66.7% in August.

BNZ Senior Economist, Doug Steel, highlighted the potential ramifications for the broader economy: "Today's PMI is not a good look for GDP and employment growth," he noted. With the current forecasts including a downturn in manufacturing for the latter half of 2023, Steel warned, "There's a chance that decline is bigger than we think, if the PMI does not bounce in the final months of the year."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0644; (P) 1.0685; (R1) 1.0709; More...

EUR/USD is trying to draw support from 55 4H EMA (now at 1.0657) and intraday bias remains neutral first. Further rise is in favor as long as this EMA holds. Decisive break of 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763) will extend the rise from 1.0447 to 61.8% retracement at 1.0958 next. However, sustained break of 55 4H EMA will argue that the rebound has completed, and target 1.0515 support, and then 1.0447 low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Oct | 42.5 | 45.3 | 45.1 | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Oct | 2.40% | 2.40% | ||

| 00:30 | AUD | RBA Monetary Policy Statement | ||||

| 07:00 | GBP | GDP M/M Sep | 0.20% | 0.00% | 0.20% | 0.10% |

| 07:00 | GBP | GDP Q/Q Q3 P | 0.00% | -0.10% | 0.20% | |

| 07:00 | GBP | Manufacturing Production M/M Sep | 0.10% | 0.30% | -0.80% | -0.70% |

| 07:00 | GBP | Manufacturing Production Y/Y Sep | 3.00% | 3.10% | 2.80% | 3.00% |

| 07:00 | GBP | Industrial Production M/M Sep | 0.00% | -0.10% | -0.70% | -0.50% |

| 07:00 | GBP | Industrial Production Y/Y Sep | 1.50% | 1.10% | 1.30% | 1.50% |

| 07:00 | GBP | Goods Trade Balance (GBP) Sep | -14.3B | -15.3B | -16.0B | -15.5B |

| 09:00 | EUR | Italy Industrial Output M/M Sep | 0.00% | -0.10% | 0.20% | 0.30% |

| 12:00 | GBP | NIESR GDP Estimate (3M) Oct | 0.10% | -0.10% | 0.00% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Nov P | 63.6 | 63.8 |

NIESR forecasts slight growth for UK economy, averting recession in 2023

According to NIESR's projections, UK economy is set to witness a marginal increase in GDP of 0.1% in the fourth quarter of this year. The institute's report highlighted, "Our central forecast does not expect a recession in 2023."

Delving into the specifics of the economic forecast, NIESR stated, "These forecasts remain broadly consistent with the longer-term trend of low, but stable economic growth in the United Kingdom."

Looking ahead to the next two years, NIESR expects the pace of growth to remain relatively subdued. The institute's report forecasts GDP growth of 0.6% for 2023, followed by further restrained growth of 0.5% in 2024. The primary cause for this muted growth, as per NIESR, is the ongoing productivity slump.

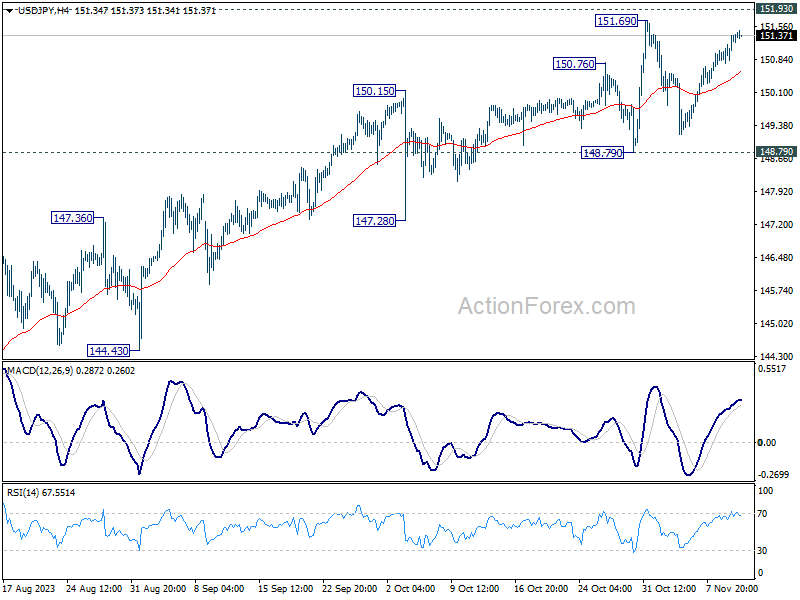

Japanese Yen Under Pressure After Dismal Week

- Fed’s Powell says interest rate hikes still on table

The Japanese yen is drifting on Friday. In the European session, USD/JPY is trading at 151.44, up 0.06%.

It has been a rough week for the Japanese yen, which is down 1.42%, its worst weekly showing since August.

Powell talks hawkish

The markets believe that interest rates have peaked and are looking ahead to rate cuts in 2024, but Fed Chair Powell continues to sound hawkish. Powell said on Thursday that he would not hesitate to raise rates if needed in order to contain inflation and stated that he was “not confident” that inflation would return to 2% under the current policy. The markets still expect a rate cut in mid-2024, but Powell’s remarks led to the markets repricing a cut in July rather than June. It seems that the US economy will have to show much sharper growth before the markets buy into the Fed’s stance that rate hikes remain on the table.

The Japanese yen fell to a one-year low of 151.72 against the dollar on 31 October. Not far off is 151.96, which was last year’s peak and the highest level in some 33 years. With the yen not far from these levels, there is concern that Japan’s Ministry of Finance (MOF) could intervene in the currency markets in order to prop up the ailing yen. The MOF has been jawboning, warning that it is alarmed by the yen’s sharp depreciation. Will this be enough to scare off speculators or will the MOF decide that action is needed to back up tough talk? If the yen continues to lose ground, the possibility of intervention will become more likely..

USD/JPY Technical

- USD/JPY is putting strong pressure on resistance at 151.56. Above, there is resistance at 152.87

- There is support at 151.12 and 150.51

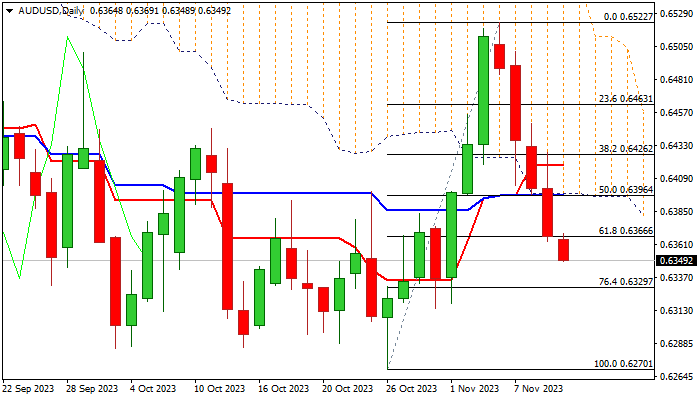

AUD/USD: On Track for Weekly Loss of Over 2%

AUDUSD remains firmly in red for the fifth straight day and on track for a weekly loss of over 2% which erased the most of previous week’s gains.

Aussie came under increased pressure from the Fed’s latest hawkish shift, which so far offsets renewed hawkishness from the RBA on growing fears that inflation will remain resilient, indicating possible further rate hikes.

Technical picture on daily chart weakened significantly as the price broke below thick daily cloud and MA’s turned to bearish setup, while 14-d momentum is trending lower but still holding in positive territory.

On the other hand, deeply oversold stochastic may slow bears for consolidation which should offer better selling opportunities if limited and keeping bears intact.

Initial resistance lays at 0.6366 (broken Fibo 61.8% / 20DMA), with extended upticks to stay below 0.6396 (daily cloud base / daily Kijun-sen)) and maintain bearish bias.

Res: 0.6366; 0.6396; 0.6408; 0.6426.

Sup: 0.6329; 0.6314; 0.6285; 0.6270.