Sample Category Title

Will US CPI Alter Fed’s Rate Path?

- US CPI inflation expected to pull lower in October

- Is the Fed's tightening strategy working?

- Dataset to be released on Tuesday at 13:30 GMT

Inflation remains a priority

The US dollar fell by 1% against six major currencies after traders saw a slowdown in hirings and concluded that the Fed won't raise rates again. At the same time, a group of investors became more confident that signs of economic weakness might motivate rate cut talks in 2024, although the Fed chief, Jay Powell, kept that scenario out of the radar during November’s FOMC policy meeting.

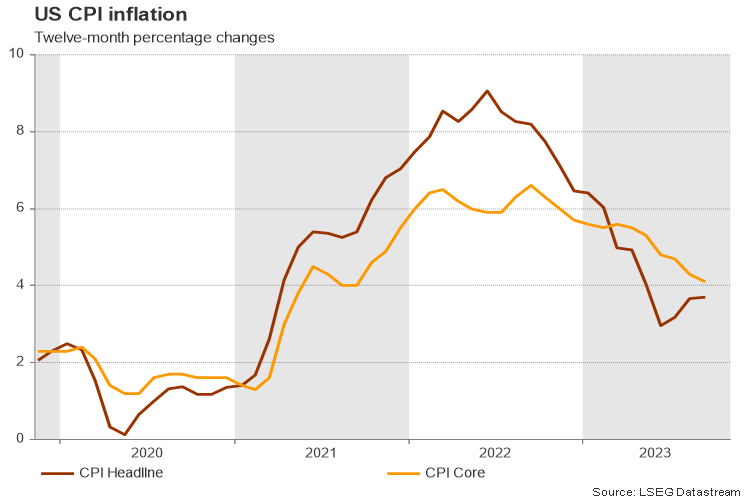

Monetary tightening to fight inflation has been a story for more than a year, and this may not change soon as the Fed is not convinced that inflation is on a sustainable path towards the central bank’s 2.0% target. Growth in consumer prices has eased significantly from the 2022 multi-year highs, falling as low as 3.0% y/y in June before edging up to stabilize around 3.7%. The next CPI update is scheduled to take place on Tuesday and investors will look at whether progress has halted particularly on the core measure, which is a better proxy of the general inflation trend.

According to forecasts, the monthly headline CPI change is expected to slow down to 0.1% from 0.3% previously, while the core CPI is forecast to stay steady at 0.3% m/m.

The core CPI inflation, which excludes food and energy prices, has been slowly decreasing over the past six months and reached a two-year low of 4.1% in September. In October, the ISM services PMI survey found that price pressures remained within the expansion territory, with businesses stating that increased labor costs were the main cause of elevated prices.

Is additional tightening necessary?

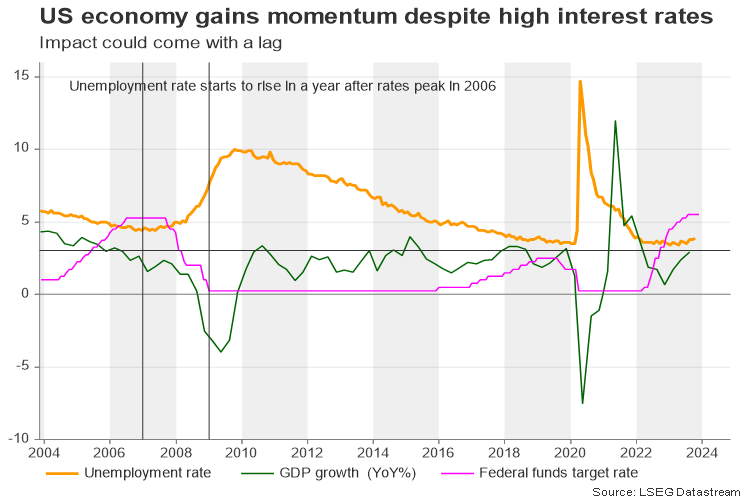

Additional tightening may be the easiest way to cool inflation, but its impact on the economy and price pressures has been a puzzle so far.

Rising personal consumption, a low unemployment rate, and low savings indicate that higher interest rates didn't dampen demand. Of course, this does not mean that monetary tightening was not necessary. Otherwise, inflation would have been a bigger headache as a weak dollar would have made import prices more painful to consumers.

Nevertheless, effects from monetary tightening will apparently become more obvious at some point, perhaps with a bigger lag if real wage growth turns positive in the coming months and consumers remain confident that their jobs are secured.

Meanwhile, supply-side effects might keep adding pressure on inflation, especially in the housing sector. If the Fed shuts the door to additional rate hikes but retains its higher for longer guidance, demand for loans and therefore for houses would probably decline, likely causing a negative spiral in prices.

The Fed’s latest economic projections for 2024 pointed to a softer GDP growth of 1.5% and a weaker inflation of 2.6%.

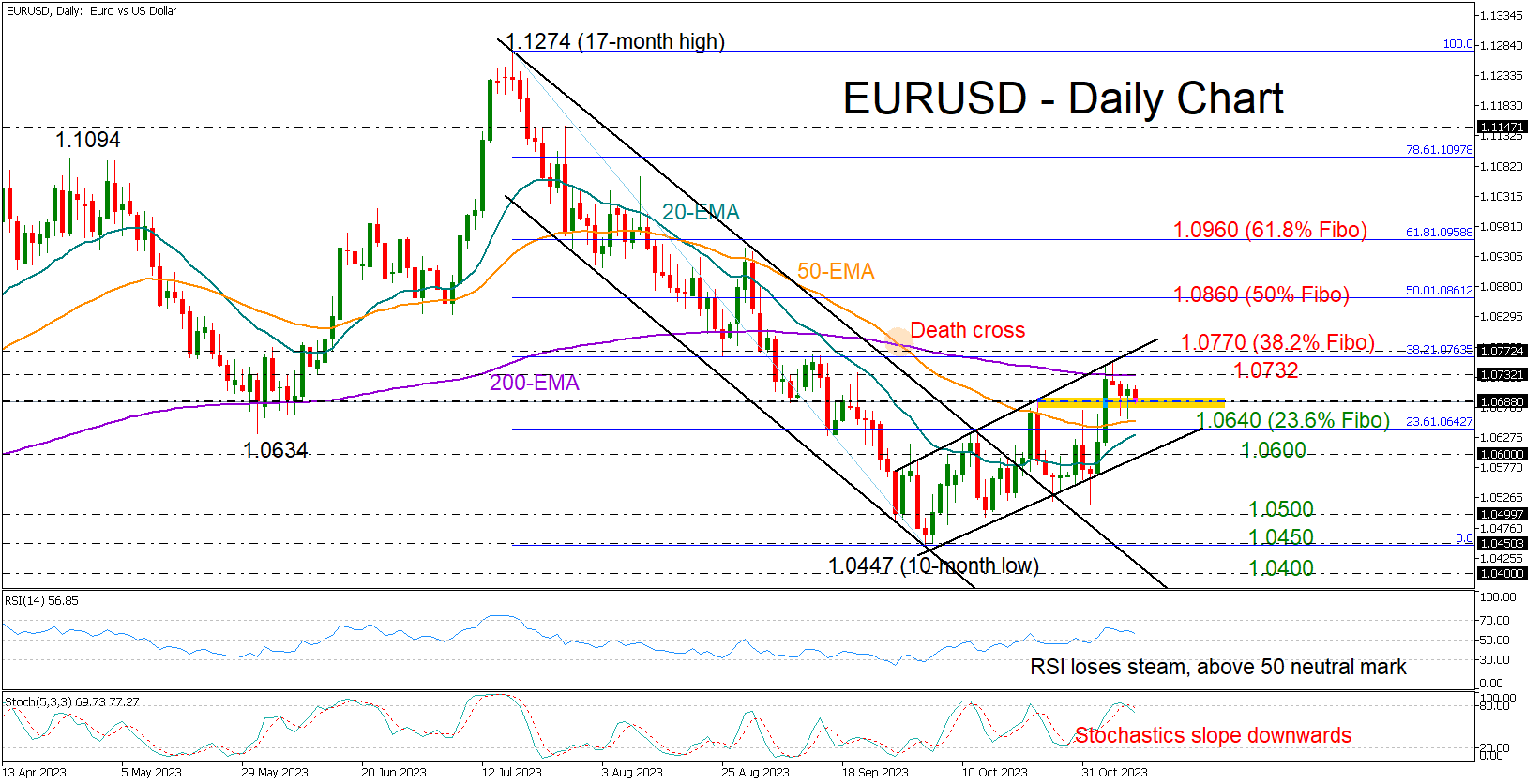

EURUSD levels to watch

As regards the impact on the US dollar, traders could sell the currency if CPI measures resume downleg, boosting confidence the Fed has reached the terminal rate. Looking at EURUSD, the pair might attempt to crawl above its 200-day exponential moving average (EMA) at 1.0730 and pierce the bullish channel on the upside at 1.0763.

Alternatively, if inflation keeps trending up, suggesting the battle for price stability might be trickier, investors might see another rate hike on the horizon. EURUSD could correct lower on the back of a stronger dollar, though only a slide below 1.0600 would violate the positive trend in the short-term picture.

BTCUSD Jumps to Fresh 18-month Peak; Looks Overbought

- BTCUSD touches 37,000 for the first time since May 5, 2022

- Momentum indicators remain deep in overbought zones

- These oscillators warn of an impending pullback

BTCUSD (Bitcoin) has experienced a massive rally driven by speculation around the approval of spot-Bitcoin ETFs, which has sent the price to a fresh 18-month high of 37,029 on Thursday. However, the latest advance seems substantially overstretched as both the RSI and stochastics are within their overbought zones for more than two weeks.

Given that the price is currently within overbought conditions, the bears could attempt a reversal towards the February 2022 low of 34,320. Sliding beneath that floor, the leading crypto could face the previous resistance of 31,827, which also held strong in June 2022. A violation of the latter could turn the spotlight to the 30,000 psychological mark.

On the flipside, if the price resumes its persistent advance, initial resistance could be met at the inside swing low of 37,500 registered in May 2022. Further upside attempts may then cease around 40,500, which acted both as support and resistance in the first half of 2022. Even higher, the April 2022 resistance of 42,980 could prove to be a tough obstacle for the price to overcome.

Overall, BTCUSD has been in a steep uptrend since early October, posting consecutive multi-month highs. However, traders should not rule out a downside correction as Bitcoin seems largely overbought at current levels.

Silver Prices Edge Lower, Trapped Under Trendline

- Silver remains in a downtrend, after recovery runs out of fuel

- Prices trading below trendline and key moving averages

- Break above 23.60 or below 22.20 could signal next move

Silver prices remain trapped in a downtrend, with a clear structure of lower highs and lower lows in place since May. The market is also trading below a trendline drawn from the May peak, as well as below the 50- and 200-day simple moving averages (SMAs), all of which suggests that the technical outlook is negative.

That said, momentum oscillators point to some stabilization in the market. The RSI is slightly below 50 but seems to be flattening, while the MACD is near its neutral levels, almost painting a picture of a directionless market.

Another wave of selling could bring the 22.20 region back into play. This obstacle halted several selloffs this year, so it’s quite important. If sellers manage to pierce through it, then the next major battle could take place near the October low of 20.65.

On the other hand, if buyers manage to regain control, the first resistance barrier for them to overcome might be the 23.60 area. The downtrend line is just above and can be considered part of the same area. A successful break could see scope for further upside extensions towards 24.30, which has served both as resistance and support this year.

Summarizing, the broader picture seems negative as long as the downtrend line remains valid.

NZD/USD Edges Higher Ahead of Manufacturing PMI

- China inflation misses estimate

- NZ manufacturing PMI expected to decline

The New Zealand dollar is in positive territory on Wednesday. In the European session, NZD/USD is trading at 0.5926, up 0.26%.

NZ Manufacturing PMI expected to decelerate slightly

New Zealand’s manufacturing sector has been in decline for seven consecutive months and little change is expected from the October PMI, which will be released on Friday. The market consensus stands at 45.0, compared to 45.3 in September, which marked a 2-year low. Business activity in the manufacturing sector has been dampened by weak global demand and elevated borrowing costs have exacerbated the prolonged slump.

China has been struggling with a significant slowdown, which is bad news for the New Zealand economy, as China is New Zealand’s number one trading partner. China is grappling with deflationary pressures, and the October inflation report was softer than expected due to a sharp decline in the price of pork.

Inflation in China fell by 0.2% y/y in October, down from 0.0% in September and lower than the market consensus of -0.1%. Monthly, CPI declined by 0.2%, versus a 0.2% rise in September and below the market consensus of 0.0%. If deflation continues, it could cause a downturn in inflation expectations that could dampen consumer spending.

Federal Reserve Chair Jerome Powell didn’t discuss monetary policy in public remarks on Wednesday, and the markets will again be listening carefully as Powell speaks later today. Earlier this week, two Fed members sounded hawkish about inflation.

On Wednesday, Philadelphia Fed President Harker said he expected rates to stay higher for longer and there were no signs of rate cuts in the near term. This followed Dallas Fed President Logan, who said that inflation remains too high and looks to be trending towards 3% rather than the Fed’s 2% inflation target. Logan warned that the Fed would have to maintain tight financial conditions in order to bring inflation back to target.

NZD/USD Technical

- NZD/USD continues to test support at 0.5929. The next support line is 0.5858

- There is resistance at 0.5996 and 0.6069

Dollar’s Recovery Meets Quiet Markets, GBP/AUD in Focus

As US session unfolds, the Dollar is showing signs of rally, buoyed by recovery in benchmark treasury yield. This modest uplift comes despite a general lack of direction owing to a sluggish risk sentiment across markets. Euro is losing momentum as its earlier recovery falters, whereas other European majors are also on the back foot. Commodity currencies seem to garner strength while Yen is mixed.

The market is bracing for potential volatility with key economic releases on the horizon. RBA's Statement on Monetary Policy is poised to unveil new economic projections, which market participants will scrutinize for the economic outlook and indications of future policy direction. This comes after Australian Dollar faced selling pressure following the RBA's rate hike earlier in the week.

In the UK, investors and BoE will be turning their attention to the upcoming GDP data to gauge the economic climate and evaluate the necessity of further interest rate adjustments. These forthcoming insights have the potential to catalyze movements in Sterling, which is presently in a wait-and-see mode alongside other major currencies.

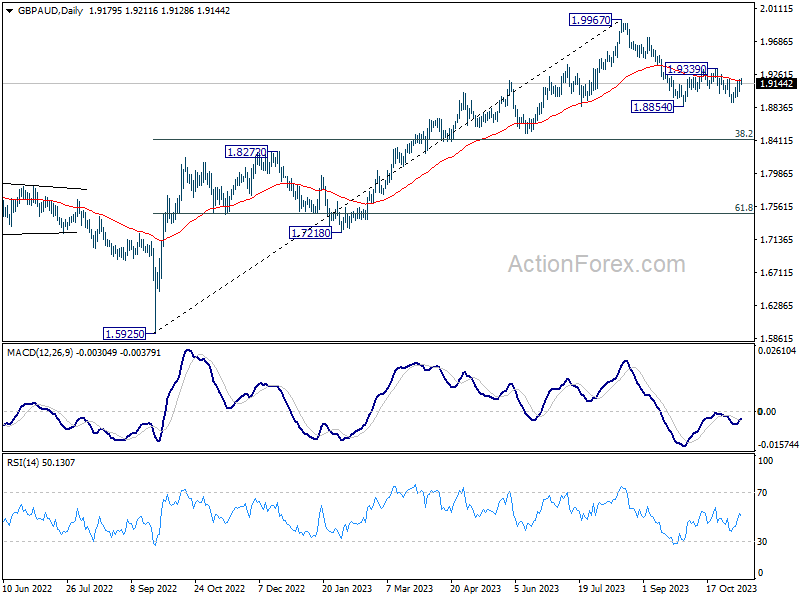

Technically, GBP/AUD is staying in the consolidation pattern above 1.8854. Some more sideway trading cannot be ruled out. But fall from 1.9967 is expected to continue after the consolidation completes. Break of 1.8854 will target 38.2% retracement of 1.5925 (2022 low) to 1.9967 at 1.8423.

In Europe, at the time of writing, FTSE is up 0.58%. DAX is up 0.57%. CAC is up 0.83%. Germany 10-year yield is up 0.0354 at 2.658. Earlier in Asia, Nikkei rose 1.49%. Hong Kong HSI dropped -0.33%. China Shanghai SSE rose 0.03%. Singapore Strait Times rose 0.18%. Japan 10-year JGB yield dropped -0.0072 to 0.842.

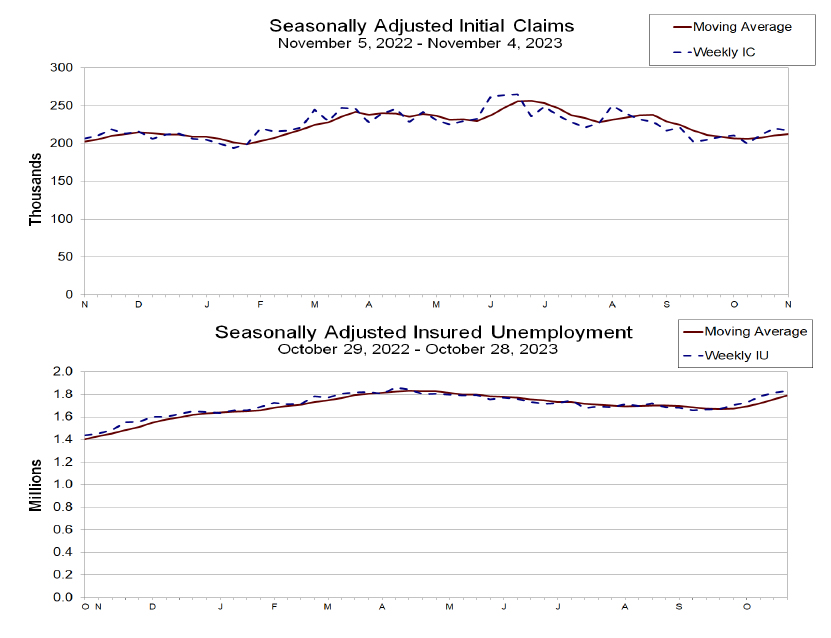

US initial jobless claims fell to 217k, above expectations

US initial jobless claims fell -3k to 217k in the week ending November 4, above expectation of 210k. Four-week moving average of initial claims rose 1.5k to 212k.

Continuing claims rose 22k to 1834k in the week ending October 28. Four-week moving average of continuing claims rose 32k to 1789k.

Fed's Goolsbee cautions on long-term yield impact

In an interview with The Wall Street Journal, Chicago Fed President Austan Goolsbee emphasized the necessity for Fed to closely monitor long-term bond yields.

"A sustained rise in long-term rates can have a very substantial effect on real economic performance," he warned.

In the ongoing debate on the future of interest rates, Goolsbee stated, "It's too soon to say whether or when the central bank would turn its focus to lowering rates."

Despite the challenging economic environment, Goolsbee projected an optimistic scenario: "The US economy can stay on the golden path in which inflation declines closer to the Fed's 2% target without a significant rise in unemployment."

ECB de Guindos: Growth more negative than projected, inflation align closely

ECB Vice President Luis De Guindos said in an interview that by holding interest rates steady "at their current level", ECB anticipates a significant impact on taming inflation to target of 2%.

This comes as a positive sign for the markets that have seen inflation rates soar over the past year, with a peak above 10% that has since eased to 2.9%. With core inflation also showing signs of moderation, ECB's tightening campaign seems to be bearing fruit.

However, de Guindos emphasized a "prudent and cautious" approach because of "risks around the outlook for inflation over the next few months." This underlies ECB's stance to consider interest rate decisions on a "meeting-by-meeting" basis, guided by unfolding economic data.

De Guindos also pointed out that "leading indicators point to the growth outlook being somewhat more negative than we previously projected." Nonetheless, he believes that inflation may align closely with their September projections.

BoE's Pill: Maintaining restrictive rates, not hikes, essential for tackling inflation

BoE Chief Economist Huw Pill highlighted today that the existing policy rate, deemed restrictive, is sufficient to dampen inflationary pressures without necessitating further hikes.

"Having established monetary policy in restrictive territory, it's not the case that we need to raise rates in order to bear down on inflation," he said in a speech to the Institute of Chartered Accountants in England and Wales.

"Sustaining rates at their current restrictive level will continue to bear down on inflation," he affirmed "It is that maintaining of the restrictive stance that is key to achieving the inflation target."

Pill also acknowledged the role of global economic developments in the inflation outlook but was keen to point out the influence of BoE's actions. "That tightening of monetary policy is bearing down on inflation and contributing to this decline," he stated.

Despite these measures, Pill expressed caution, noting that inflation, especially in the service sector, has displayed more tenacity than anticipated, without a "decisive turning point" in sight.

Moreover, wage growth is proving to be more persistent, signaling that it may take longer to align with the 2% inflation target than previously projected by models.

BoJ Ueda awaits wage trends before altering policy

In today's parliamentary session, BoJ Governor Kazuo Ueda emphasized a cautious stance on Japan's monetary policy, acknowledging the need for more evidence before making any adjustments.

"We expect trend inflation to gradually approach 2 percent. But we'd like to wait until we have more conviction that sustained achievement of our price target comes into sight," Ueda said.

Highlighting the significance of wage trends, Governor Ueda noted, "Whether wage hikes will broaden and become embedded in society, firms begin to hike prices on prospects of rising wages, will be key to judging whether inflation target will be met sustainably."

He reaffirmed the Bank's current strategy: "Until then, we will maintain negative interest rates and the yield curve control framework."

The Summary of Opinions from the BoJ's October meeting, released separately, showed a notable stance from one member suggested optimism about wage growth, "It's highly possible that wage growth to be agreed in next year's base pay negotiations will exceed that agreed this year," and added that "achievement of the BoJ's price target is coming into sight."

One member went further to suggest that the chances of meeting the inflation target have increased, proposing that "It's therefore necessary for the BOJ to gradually adjust the degree of monetary easing down from its maximum level."

Another member's opinion highlighted that adjustments in yield controls are not just a mitigation of side-effects but also pave the way for future policy normalization.

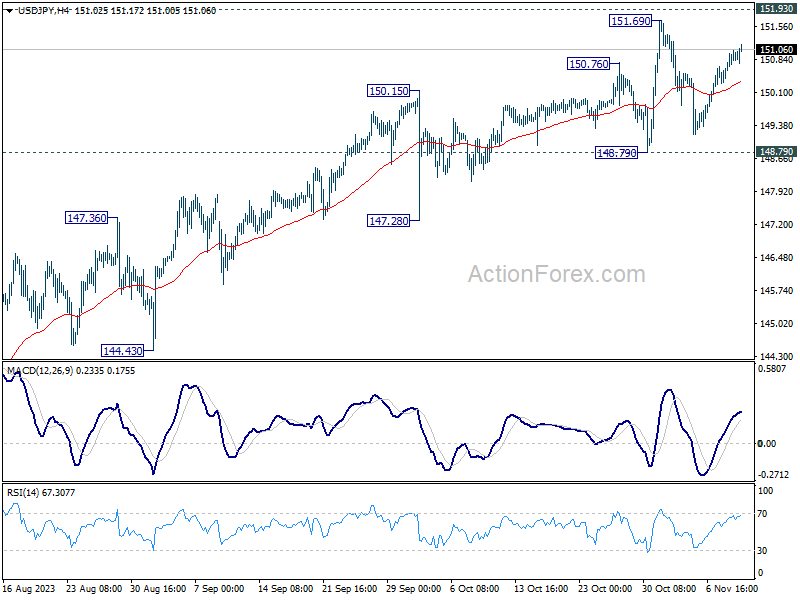

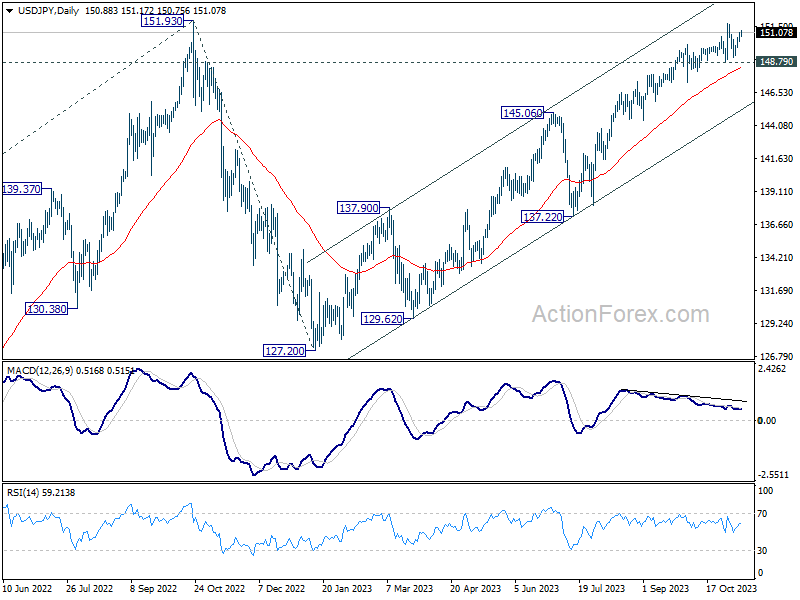

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.51; (P) 150.79; (R1) 151.25; More...

No change in USD/JPY's outlook as consolidation from 151.69 is extending. Intraday bias stays neutral at this point. Further rally is expected as long as 148.79 support holds. Firm break of 151.69 high will resume larger up trend. However, decisive break of 148.79 will indicate rejection by 151.93 key resistance, and bring deeper fall through 147.28 support.

In the bigger picture, immediate focus is on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 to 151.93 from 127.20 at 157.69.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Current Account (JPY) Sep | 2.01T | 2.27T | 1.63T | 1.50T |

| 00:01 | GBP | RICS Housing Price Balance Oct | -63% | -65% | -69% | |

| 01:30 | CNY | CPI Y/Y Oct | -0.20% | -0.20% | 0.00% | |

| 01:30 | CNY | PPI Y/Y Oct | -2.60% | -2.70% | -2.50% | |

| 05:00 | JPY | Eco Watchers Survey: Current Oct | 49.5 | 50.2 | 49.9 | |

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 13:30 | USD | Initial Jobless Claims (Nov 3) | 217K | 210K | 217K | 220K |

US initial jobless claims fell to 217k, above expectations

US initial jobless claims fell -3k to 217k in the week ending November 4, above expectation of 210k. Four-week moving average of initial claims rose 1.5k to 212k.

Continuing claims rose 22k to 1834k in the week ending October 28. Four-week moving average of continuing claims rose 32k to 1789k.

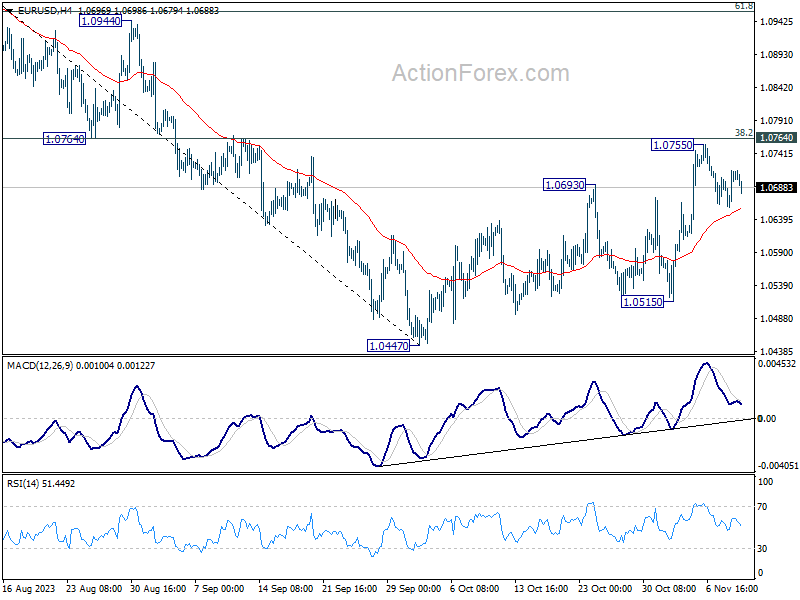

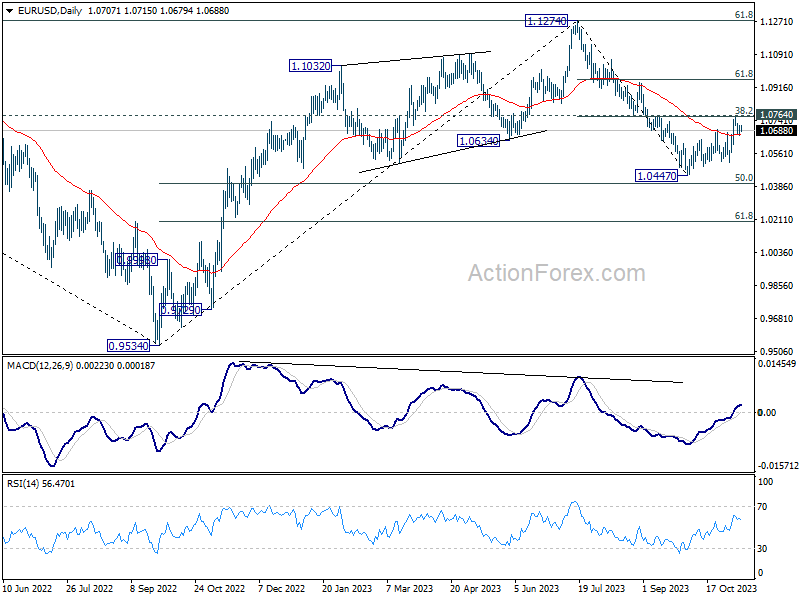

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0673; (P) 1.0695; (R1) 1.0730; More...

Range trading continues in EUR/USD and intraday bias stays neutral. Further rally is in favor as long as 55 4H EMA (now at 1.0657) holds. Decisive break of 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763) will extend the rise from 1.0447 to 61.8% retracement at 1.0958 next. However, sustained break of 55 4H EMA will argue that the rebound has completed, and target 1.0515 support, and then 1.0447 low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

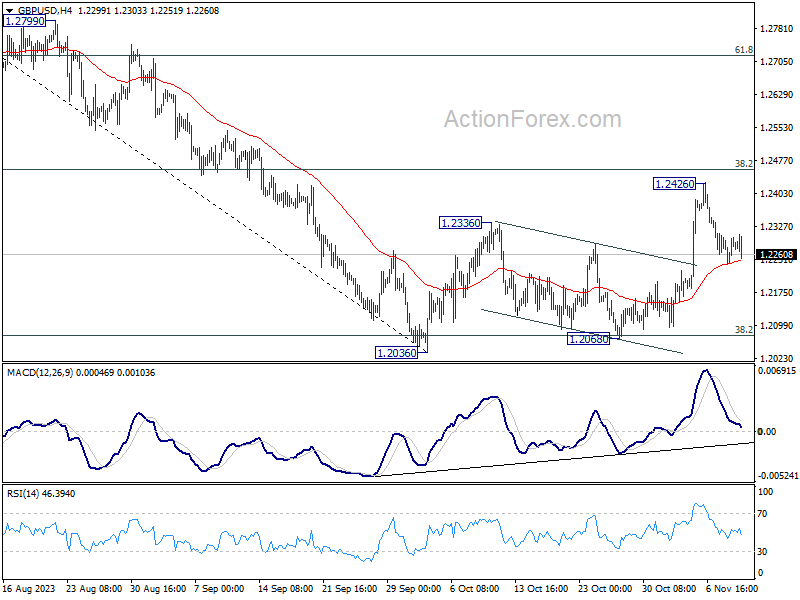

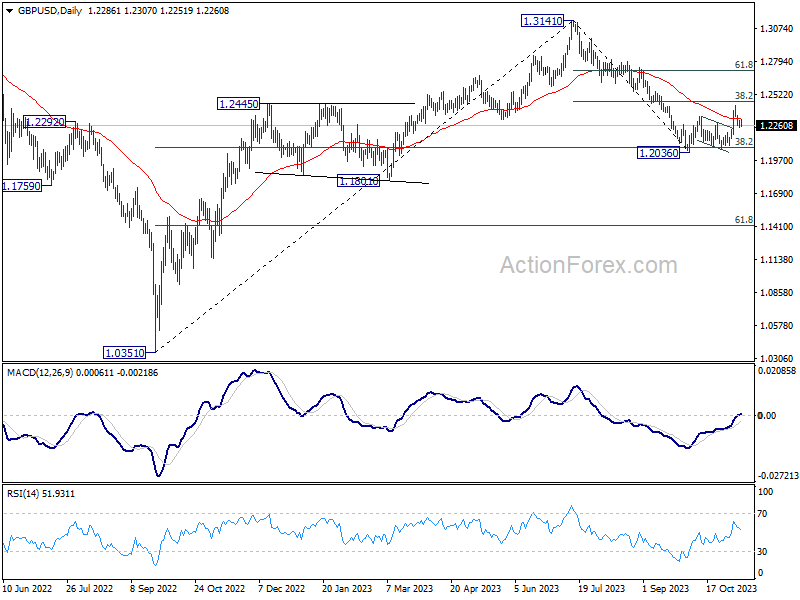

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2250; (P) 1.2277; (R1) 1.2313; More

Intraday bias in GBP/USD stays neutral at this point. Strong rebound from 55 4H EMA (now at 1.2248) will maintain near term bullishness for another rise to 38.2% retracement of 1.3141 to 1.2036 at 1.2458. However, sustained break of 4H 55 EMA will revive near term bearishness and bring retest of 1.2036 low instead.

In the bigger picture, the strong rebound from 38.2% retracement of 1.0351 to 1.3141 at 1.2075 argues that price action from 1.3141 are merely a correction to rise from 1.0351 (2022 low). Current rally from 1.2036 is tentatively seen as the second leg of the pattern. Hence, while further rally is in favor, upside should be limited by 1.3141 to start the third leg.

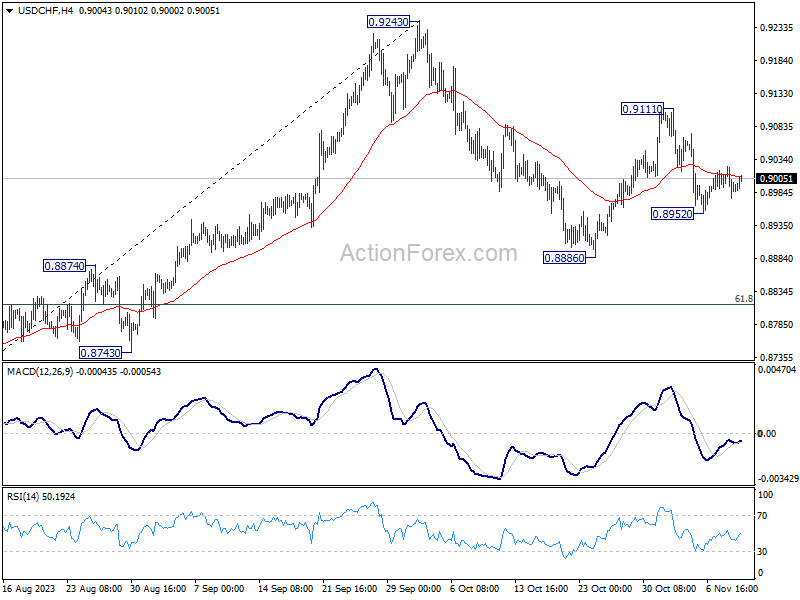

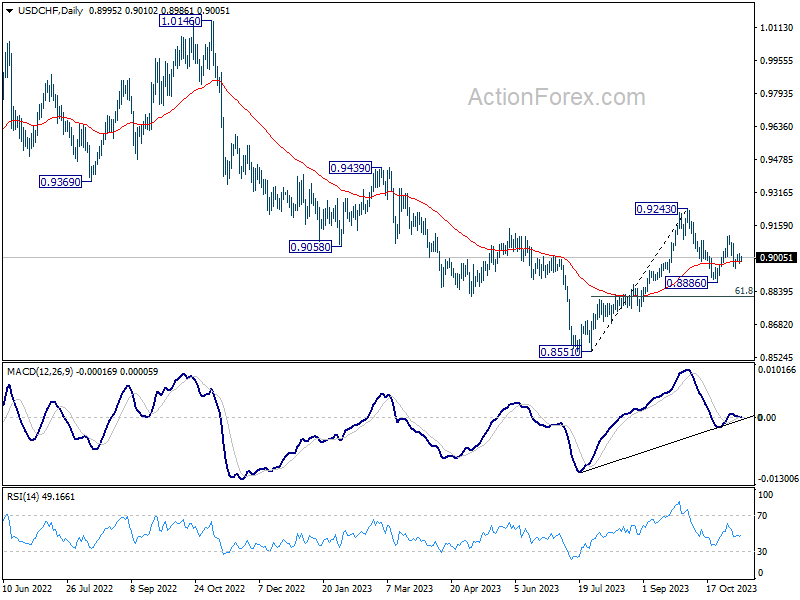

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8973; (P) 0.8998; (R1) 0.9020; More....

Intraday bias in USD/CHF stays neutral as consolidations continue above 0.8952 temporary low. On the downside, below 0.8952 will target a test on 0.8886 support first. Break there will resume whole decline from 0.9243 to 0.8815 fibonacci level. However, break of 0.9111 will resume the rebound from 0.8886 instead, and target 0.9243 resistance.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.51; (P) 150.79; (R1) 151.25; More...

No change in USD/JPY's outlook as consolidation from 151.69 is extending. Intraday bias stays neutral at this point. Further rally is expected as long as 148.79 support holds. Firm break of 151.69 high will resume larger up trend. However, decisive break of 148.79 will indicate rejection by 151.93 key resistance, and bring deeper fall through 147.28 support.

In the bigger picture, immediate focus is on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 to 151.93 from 127.20 at 157.69.