Sample Category Title

Fed’s Goolsbee cautions on long-term yield impact

In an interview with The Wall Street Journal, Chicago Fed President Austan Goolsbee emphasized the necessity for Fed to closely monitor long-term bond yields.

"A sustained rise in long-term rates can have a very substantial effect on real economic performance," he warned.

In the ongoing debate on the future of interest rates, Goolsbee stated, "It's too soon to say whether or when the central bank would turn its focus to lowering rates."

Despite the challenging economic environment, Goolsbee projected an optimistic scenario: "The US economy can stay on the golden path in which inflation declines closer to the Fed's 2% target without a significant rise in unemployment."

Can the Upcoming UK Data Revive Bets of Another BoE Hike?

- Despite hawkish BoE, investors don’t expect more hikes

- Friday’s GDP data expected to reveal slight contraction

- Employment and CPI data to follow next week

- Accelerating inflation may be the pound’s only hope

Investors don’t buy BoE’s hawkish hold

Last week, the Bank of England decided to keep interest rates unchanged via a 6-3 vote, with the three dissenters favoring a 25bps hike. In the accompanying statement, officials noted that policy must stay restrictive for an extended period, and that further tightening may be required if there is evidence of more persistent inflationary pressures. At the press conference, Governor Bailey said that inflation is still too high and that they are determined to take it all the way down to 2%, adding to the decision’s hawkish flavor.

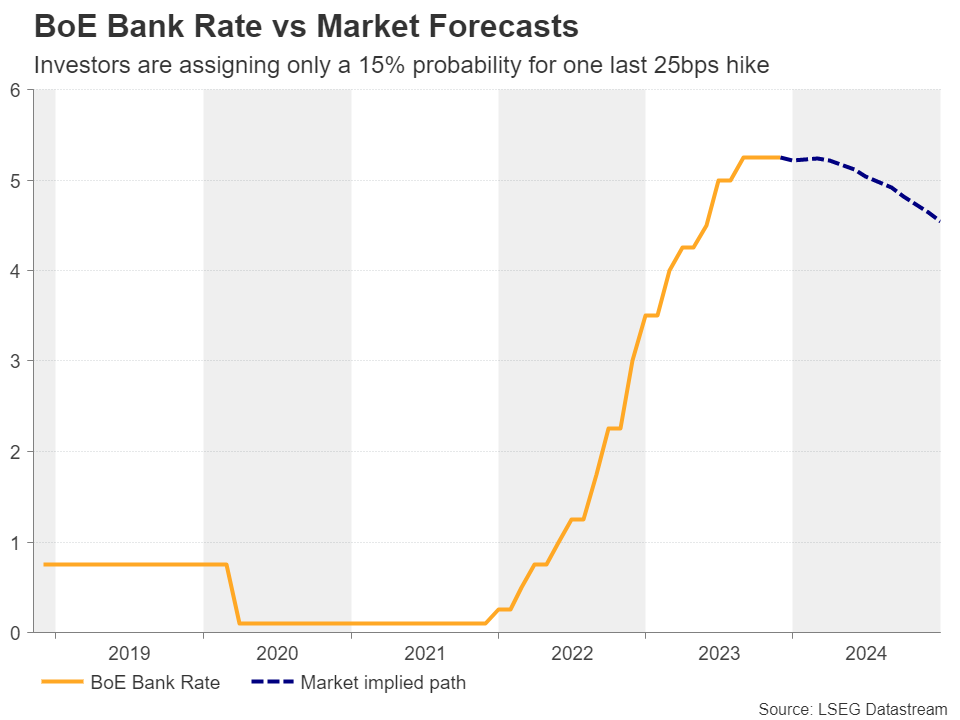

That said, even after the BoE’s ‘higher for longer’ message, investors continue to see only a 15% probability for another quarter point hike by February and around 70bps worth of rate cuts by the end of next year.

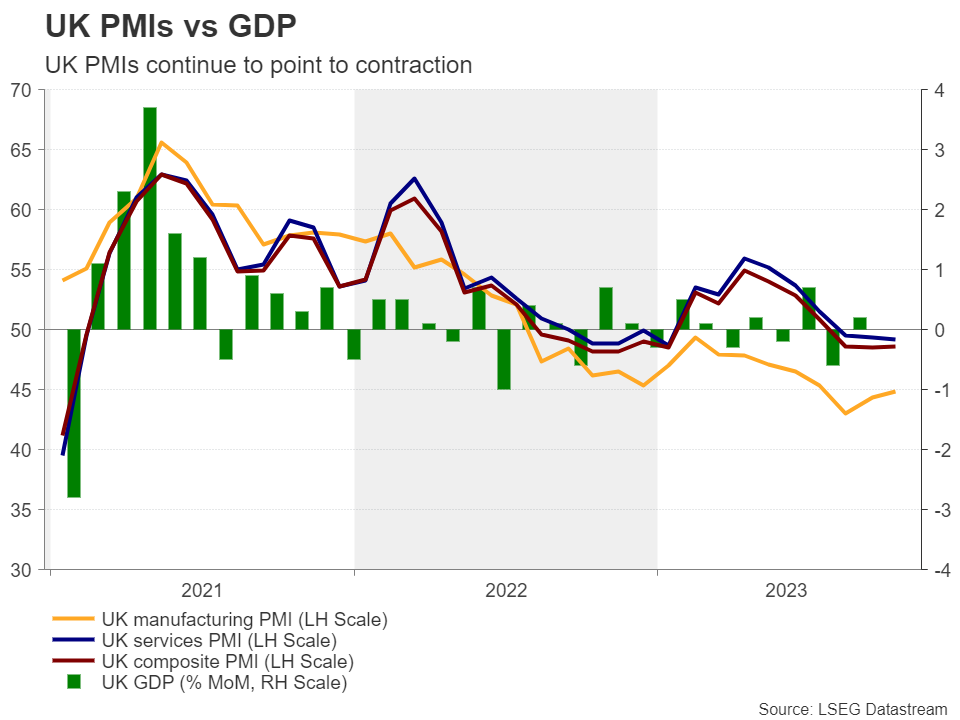

Did the UK economy contract in Q3?

With the Bank estimating flat economic growth for Q3 this year, Friday’s official GDP data for the quarter may attract special interest. Expectations are for the economy to have shrunk 0.1% q/q after growing 0.2% q/q in Q2, with a contraction supported by the UK composite PMI, which fell from 50.8 in July to 48.6 in August and then to 48.5 in September.

A negative growth rate could confirm the market’s view that BoE policymakers may be forced to press the cut button earlier than they currently believe, bringing the pound under selling interest. That said, the British currency may not suffer huge losses if the contraction is mild as traders may decide to save ammunition for next week’s employment and inflation data, on Tuesday and Wednesday respectively. For investors to sell the pound and forget next week’s releases, the GDP growth rate may need to miss the forecast by a decent margin.

Risks surrounding inflation tilted to the upside

Given that Governor Bailey said after last week’s meeting that whether GDP growth is slightly negative or slightly positive will not impact monetary policy, next week’s data may prove more important in shaping expectations about the Bank’s future plans if indeed the GDP figure comes in at -0.1%.

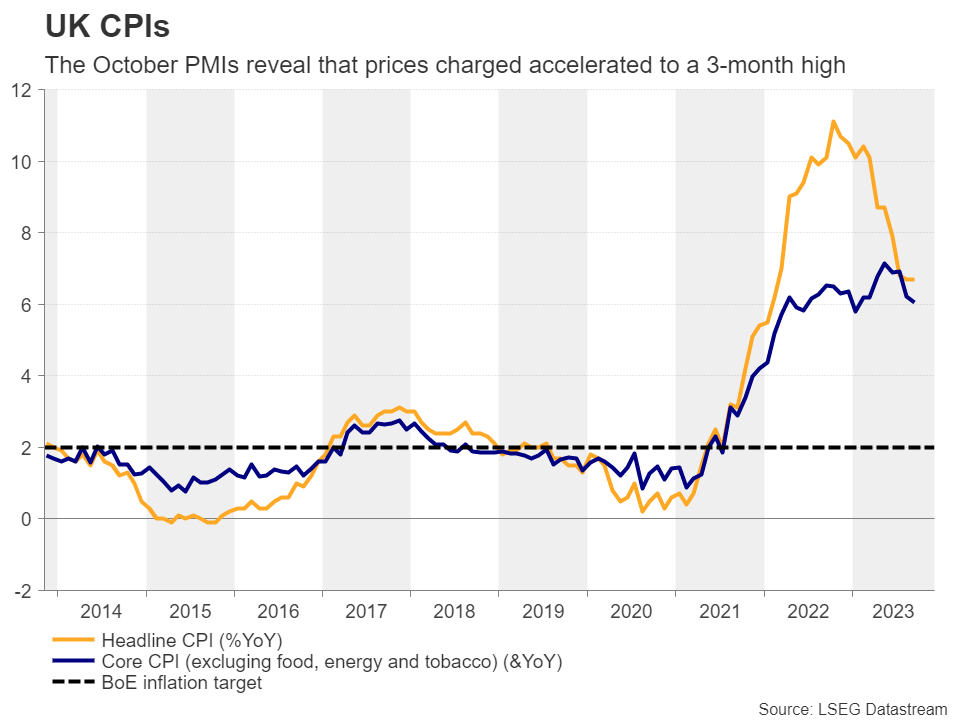

Both the headline and core CPI rates are more than three times the BoE’s target of 2%, which means that policymakers’ mission is far from accomplished and that indeed some further tightening may be needed, despite market participants not sharing that view. According to the UK PMIs for the month, prices charged by companies accelerated to a three-month high in October, tilting the risks surrounding the CPI report to the upside.

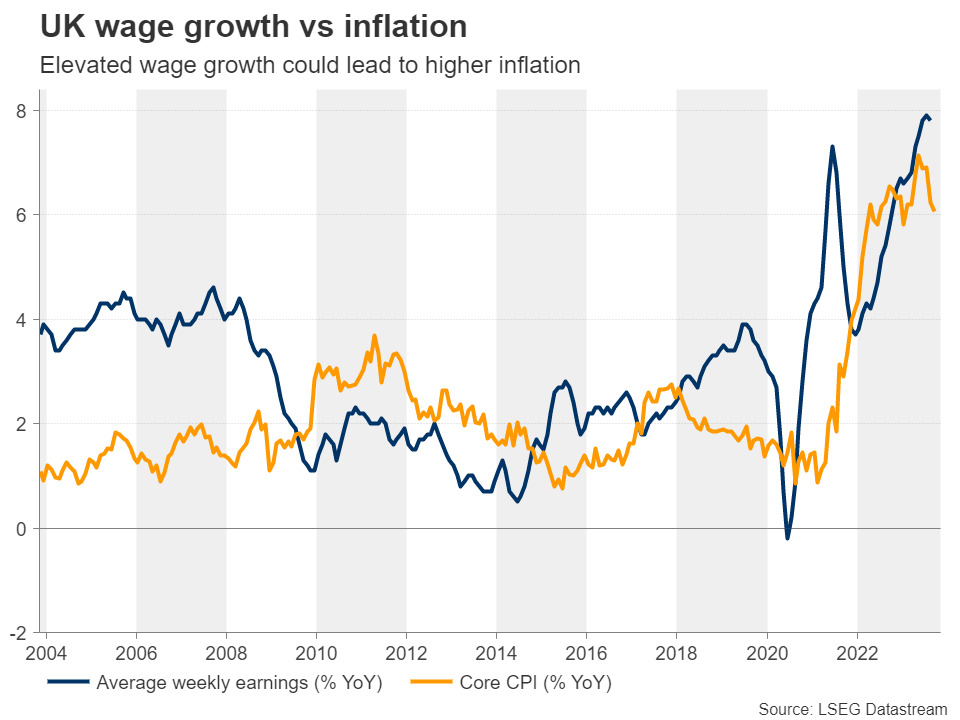

Wage growth to be monitored as well

On the other hand, the KPMG and REC UK report on jobs pointed to a further easing of overall pay growth, which means that Tuesday’s data may reveal a slowdown in average weekly earnings. Having said that, a small slowdown in the excluding bonuses rate from 7.8% is unlikely to be a reason for complacency. For investors to maintain a low probability for another rate hike by the BoE and keep several rate cuts for next year on the table, the CPIs on Wednesday may need to reveal a slowdown as well, or the wage growth rate may need to slide to levels that will raise speculation of lower inflation in future months, even if Wednesday’s CPI rate sees as small rebound.

Pound’s technical outlook remains cautiously bearish

Cable rallied on Friday following the disappointing US employment report, but with the US dollar staging a shy comeback this week, the pair returned below the key territory of 1.2310. If the GDP data suggests that the economy contracted by more than anticipated, the pair is likely to continue drifting south, especially if wages slow as well next Tuesday. However, whether the slide will extend to reach the round figure of 1.2000 may depend on Wednesday’s CPI data.

For the pair to return above 1.2310 and perhaps violate its 200-day moving average, even if economic growth and wages slow somewhat, the inflation data may need to reveal a rebound in both the headline and core rates. In such a case, the bulls may feel confident to climb towards the 1.2600 zone.

Aussie Halts Slide, RBA Statement Next

- China’s inflation misses estimate

- RBA to release monetary policy statement on Friday

The Australian dollar is unchanged on Thursday and is trading at 0.6401. This follows a three-day slide, in which AUD/USD has fallen 1.7%.

RBA Monetary Policy Statement eyed

The Reserve Bank of Australia will release its quarterly monetary policy statement on Friday. Investors will be looking for insights about the RBA’s rate policy, after the central bank increased rates on Tuesday by a quarter point to 4.35%, a 12-year high. It was the first rate hike by Governor Michelle Bullock and came after four consecutive pauses.

The RBA statement after the meeting noted that inflation remained too high and “the risk of inflation remaining higher had increased”, but investors focused on the fact that the statement did not mention that further tightening might be required, unlike the October statement. This raised expectations that the RBA is done with tightening and the Australian dollar plunged over 1% in the aftermath of the rate hike.

The markets will now focus on third-quarter wage growth, which will be released on 15 November. If wages rise sharply, we will likely see an increase in the odds of a second straight hike at the RBA’s next meeting on 5 December.

The Australian dollar is sensitive to Chinese data, as China is Australia’s largest trading partner. Inflation in China fell by 0.2% y/y in October, down from 0.0% in September and lower than the market consensus of -0.1%. Monthly, CPI declined by 0.2%, versus a 0.2% rise in September and below the market consensus of 0.0%. The downturn in inflation was driven by a sharp decline in the price of pork, as supply has outstripped demand.

The sharp slowdown in China has resulted in persistent disinflation and further support measures will be needed to avoid a downturn in inflation expectations that could dampen consumer spending.

AUD/USD Technical

- There is resistance at 0.6431 and 0.6526

- 0.6351 and 0.6256 are providing support

Bitcoin is tired of consolidation

Market picture

The crypto market continues to climb, rising 3.4% in the last 24 hours to $1.38 trillion. Bitcoin was again the driver, adding 3.8%. Altcoins are moving slower but up, adding between 1.7% (BNB) and 7.7% (Polygon).

Bitcoin has broken out of a long consolidation range and is approaching the next round level of $37K. The technical implementation of this pattern suggests a rise to $41-45K, depending on which point we choose as the start of the last impulse. The upper limit looks like a suitable target with a pivot point close to it. Near it, in April 2022, the corrective rebound ended, and the most relentless phase of the sell-off began.

Despite Bitcoin’s strong recovery since the beginning of the year, the supply of coins is extremely limited due to the actions of hoarders. Many metrics that characterise “bitcoin inactivity” have reached historic highs, Glassnode noted.

News background

The significant increase in Open Interest in bitcoin futures creates conditions for the price of digital gold to continue rising, according to YouTube analyst CredibleCrypto.

The European Banking Authority has launched a public consultation on capital and liquidity requirements for issuers of stablecoins and other digital tokens.

According to Bloomberg, USDC stablecoin issuer Circle Internet Financial is considering an IPO in early 2024.

Swiss cryptocurrency bank SEBA received a licence from the Hong Kong Securities and Futures Commission, allowing it to provide digital asset-related services to residents.

Exchange Binance announced the launch of Web3 Wallet, available to users via the platform’s mobile app. The utility uses Multi-Party Computing technology, which splits private keys into three parts and stores them on different servers.

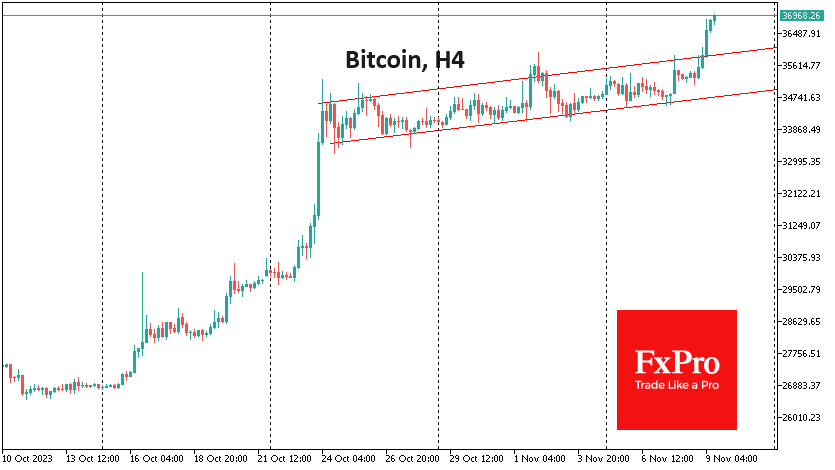

BTC/USD Analysis: New High of the Year

The bitcoin rate exceeded USD 36,500 per coin for the first time in 2023.

This is fueled by pending approval of Bitcoin ETF applications pending before the SEC. According to the latest information, SEC representatives are in contact with the Grayscale fund, one of those who submitted applications. This increased confidence that applications would be approved. Moreover:

- → applications can be approved all together and then several ETFs will start working simultaneously, making it possible that potentially billions of dollars will be directed to the purchase of bitcoins;

- → this can happen before January 10, 2024.

The creation of ETFs will open up new opportunities for a wide range of investors to easily invest in the main cryptocurrency, while reducing the risks associated with opening an account on a crypto exchange, hacked wallets, or sanctions from regulators.

The BTC/USD chart today shows that the price of bitcoin broke through the USD 36,000 level on an expanding candle, indicating the strength of demand.

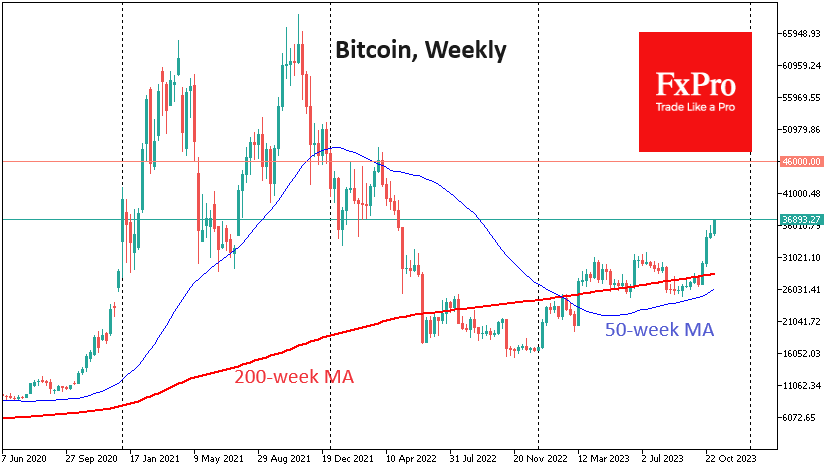

How far can the bitcoin rate go up?

Let's consider the situation in 2023, taking into account the periods of supply and demand balances that developed in those zones where the canal lines are located.

- Period A: Buyers and sellers found equilibrium in the spring below USD 30,000.

- Period B: Another balance near the median line, but above USD 30,000.

- Period C: Balance near the bottom line with an average price around USD 27,000.

- Period D: Another balance near the median line, now around USD 35,000.

If news related to the approval of the ETF heats up the market even more, the next balance may develop near the upper border of the channel — that is, around USD 44,000. Has the bitcoin Santa Rally begun?

On the other hand, if the news turns out to be fake or there are negative comments from the SEC, this may cause the price to roll back to the median line.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

EUR/JPY Analysis: New High of the Year

For the first time since 2008, the rate exceeded the level of 161 yen per euro.

The strength of the euro and the weakness of the yen are contributed to by different policies of central banks.

The European Central Bank's chief economist said on Wednesday that he had not seen enough progress in curbing inflation. This may mean a continuation of the ECB's tight monetary policy and the “expensive euro”. The head of Ireland's central bank said on Wednesday that further interest rate hikes should not be ruled out, while the Bundesbank president said the "last mile" to the inflation target could be the hardest.

At the same time, in Japan, interest rates are effectively negative, making the yen fundamentally weak against the euro. The uptrend channel on the EUR/JPY pair (shown in blue) dates back to 2022. The stability of the trend is also evidenced by the upward-directed MA (100) — the rate is stably above it.

Wherein:

- the psychological level of 160 yen worked as an important resistance in 2023, but in November the price consolidates higher;

- yesterday, the bulls broke through the level of 161 yen per euro;

- The RSI rises into the overbought zone, making the market vulnerable to a pullback.

At the same time, it is acceptable to assume that the yen may strengthen as a result of statements by representatives of the Japanese authorities (former or even current) about changing the monetary policy. As such, signals are increasingly broadcast through the media, 2024 could be the period when the yen situation changes from verbal interventions to real actions (including rate hikes).

Taking into account the above, one should not exclude the scenario of a return to the level of 160 yen per dollar, especially taking into account the fact that this level was not clearly tested after the bullish breakout.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

ECB de Guindos: Growth more negative than projected, inflation align closely

ECB Vice President Luis De Guindos said in an interview that by holding interest rates steady "at their current level", ECB anticipates a significant impact on taming inflation to target of 2%.

This comes as a positive sign for the markets that have seen inflation rates soar over the past year, with a peak above 10% that has since eased to 2.9%. With core inflation also showing signs of moderation, ECB's tightening campaign seems to be bearing fruit.

However, de Guindos emphasized a "prudent and cautious" approach because of "risks around the outlook for inflation over the next few months." This underlies ECB's stance to consider interest rate decisions on a "meeting-by-meeting" basis, guided by unfolding economic data.

De Guindos also pointed out that "leading indicators point to the growth outlook being somewhat more negative than we previously projected." Nonetheless, he believes that inflation may align closely with their September projections.

BoE’s Pill: Maintaining restrictive rates, not hikes, essential for tackling inflation

BoE Chief Economist Huw Pill highlighted today that the existing policy rate, deemed restrictive, is sufficient to dampen inflationary pressures without necessitating further hikes.

"Having established monetary policy in restrictive territory, it's not the case that we need to raise rates in order to bear down on inflation," he said in a speech to the Institute of Chartered Accountants in England and Wales.

"Sustaining rates at their current restrictive level will continue to bear down on inflation," he affirmed "It is that maintaining of the restrictive stance that is key to achieving the inflation target."

Pill also acknowledged the role of global economic developments in the inflation outlook but was keen to point out the influence of BoE's actions. "That tightening of monetary policy is bearing down on inflation and contributing to this decline," he stated.

Despite these measures, Pill expressed caution, noting that inflation, especially in the service sector, has displayed more tenacity than anticipated, without a "decisive turning point" in sight.

Moreover, wage growth is proving to be more persistent, signaling that it may take longer to align with the 2% inflation target than previously projected by models.

Price of Gold Drops Below $1,950

This happened for the first time since mid-October, when gold was rapidly rising in price on fears related to the escalation of the military conflict in the Middle East.

At the same time, the psychological level of USD 2,000 per ounce demonstrated its importance.

Notice the volatility spikes around it — the bulls were active in the attacks, noticeable on the 4-hour chart, but all the progress made on the upward impulses was almost immediately canceled out by the bears.

The graph shows:

- formation of a reversal pattern SHS (head-and-shoulders). With some subjectivity, we can assume that the “neck” level is around USD 1,970. But it has already been broken after a weak rebound;

- the price dropped below EMA (100).

The price can be supported by a trend line drawn at the highs of August-September. After a bullish breakout, it could serve as market support in the area of USD 1,915 per ounce. In the same area is the 50% Fib level of the upward momentum from the October lows to the peak above USD 2,000. If the price falls to the USD 1,910-1,920 zone, it could serve as a support for the bulls to try to resume the bullish trend, if the news background also contributes to this.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

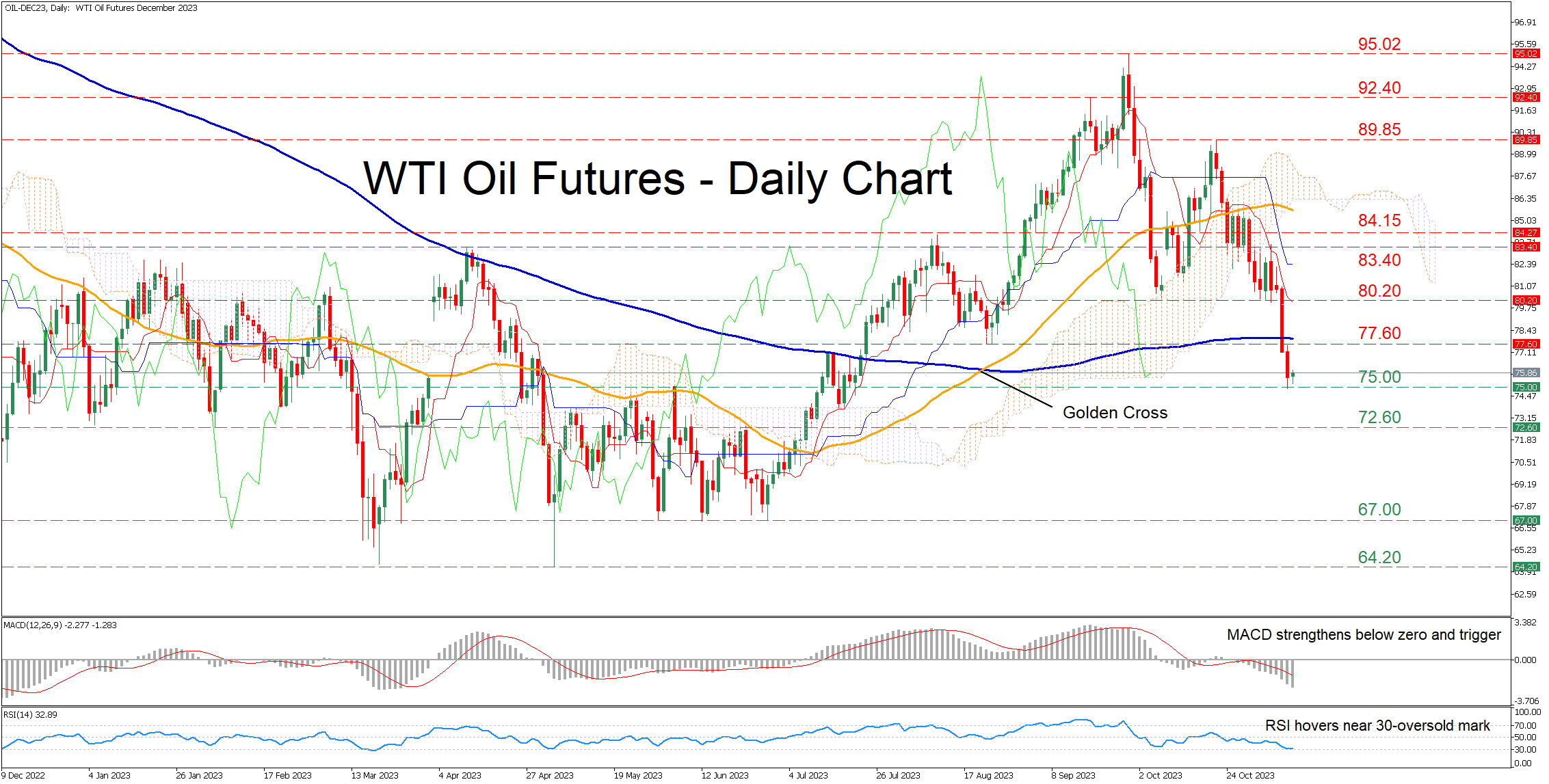

WTI Oil Futures Collapse to a Fresh 3-month Low

- WTI futures decline sharply below the 200-day SMA

- Drop to the lowest level since July 20, but find their feet at the 75.00 handle

- Momentum indicators touch oversold levels, hinting at potential bounce

WTI oil futures (December delivery) have been on the retreat since their October peak of 89.85, breaking aggressively below historical support zones. On Tuesday, the price dropped more than 4.5%, sliding beneath the crucial 200-day simple moving average (SMA) before recording a fresh three-month low on the following day.

Should selling pressures persist, the price could revisit the recent three-month bottom of 75.00, which also served as resistance in June. Failing to halt there, oil futures could descend towards 72.60, a level that held its ground both in January and February of 2023. A break below that zone could set the stage for the triple bottom of 67.00.

On the flipside, if the price attempts to stage a recovery, initial advances could encounter resistance at the August support of 77.60, which coincides with the 200-day SMA. Violating that territory, oil could challenge the 80.20 hurdle. Even higher, the April peak of 83.40 may prove to be a tough obstacle for the bulls to overcome.

In brief, WTI oil futures remain under relentless downside pressure, recording consecutive lower lows. However, traders should not rule out a bounce to the upside as the short-term oscillators are dangerously approaching oversold conditions.