Sample Category Title

JPY Weakness

Market movers today

With no market movers in the calendar focus will be on central bank comments as both Lagarde and Powell will speak this evening.

The 60 second overview

China: Chinese economies remains on the brink of deflation after CPI inflation dropped to -0.2% y/y in October and thus back to negative territory. The drop was slightly bigger than expected by consensus.

Japan: Bank of Japan chair Ueda reiterated that the central bank will keep easy policy until inflation target is in sight, while adding that the order of the normalisation process for the yield curve control and negative interest rate policies had not been decided yet.

Oil: Oil prices fell further yesterday with Brent dropping below USD80/bbl. With no oil specific news to report, it may be that the oil market has started to price a bigger downturn in global economic growth, which would likely hit global oil demand along the way.

Equities: Global equities were almost unchanged yesterday. Relatively big regional differences with Asia trailing especially Europe. It is maybe worth nothing that Denmark was outperforming because of mostly well received earnings. On that note, it is rare to see 4 stocks up almost 10% and 1 down 12% in just one day for the OMXC25 index. Globally, energy was again lagging the rest as the oil price continues to drop. Elsewhere the preference for cyclical growth is still dominating with yields ticking lower. In the US: Dow -0.1%, S&P 500 +0.1%, Nasdaq +0.1%, Russell 2000 -1.1%. Asian markets are catching up this morning, mostly driven by the renewed appetite for tech and cyclical stocks. Futures in Europe and US are roughly unchanged.

FI: Yesterday was mostly about lower rates, lower inflation (with 5y5y EUR swap touching 2.43%, lowest since June) and flattening of the euro curves from the long end. We saw a number of ECB hawks on the wires, not least Wunsch pointing to downside risks to growth and upside risks to inflation, yet they were largely ignored by markets. Similar was the tier2 releases yesterday, captured by the ECB's Consumer expectations survey, ticked higher for the 12m ahead.

FX: The persistent JPY weakness is a bit of a puzzle to us. The combined drop in US yields and the oil price would normally provide tailwind for JPY, but USD/JPY still hovers above 150. Scandies performed somewhat yesterday, where in particular we note that the slide in NOK came to a halt. On the news front, the Polish central bank surprisingly kept interest rates unchanged, which led to a bounce in PLN.

Credit: A positive tone in the corporate bond market supported by overall risk-on sentiment. Yesterday iTraxx Main was 2bp tighter at 75bp while iTraxx X-over was 6bp tighter at 410bp. The positive tone led to a number of new issues including Heineken, Swedavia and Sandoz. Notably UBS came to the bond market with two USD denominated bonds (including AT1's) for USD3.5bn in total. The combined order book was more than USD36bn according to Bloomberg! According to Bloomberg the UBS AT1 issue contains a mechanism that would allow the bonds to be converted into ordinary shares once the bank's articles of association are amended to provide enough conversion capital. In March 2023 Credit Suisse AT1 holders were left with a complete write-down of outstanding AT1's while the bank's shareholders managed to retain some value. The equity trigger in the newly issued UBS AT1's would cushion potential investor losses.

Nordic macro

Statistics Norway will publish wage and employment figures for Q3. Please note that the wage growth will probably be above 6 % y/y in Q3, partly due to the effects from the central wage negotiations in the spring. The figure will still be well in line with Norges Bank's estimate from the September MPR at 5.5 % for 2023. Any signs of employment stalling could be more important to Norges Bank, as this will indicate that the output gap is falling.

Riksbank releases the second Financial Stability Report this year 09.30 CET, press conference at 11.00 CET with Governor Thedeén. He later presents the report at a meeting 17.00 CET at the Swedish Bankers' Association. The previous June Report concluded that the Swedish financial system works well despite high inflation and rising rates, but at the same time acknowledged vulnerabilities in the form of high debt burden at real estate companies and banks' high exposure to this sector. We expect a similar message this time.

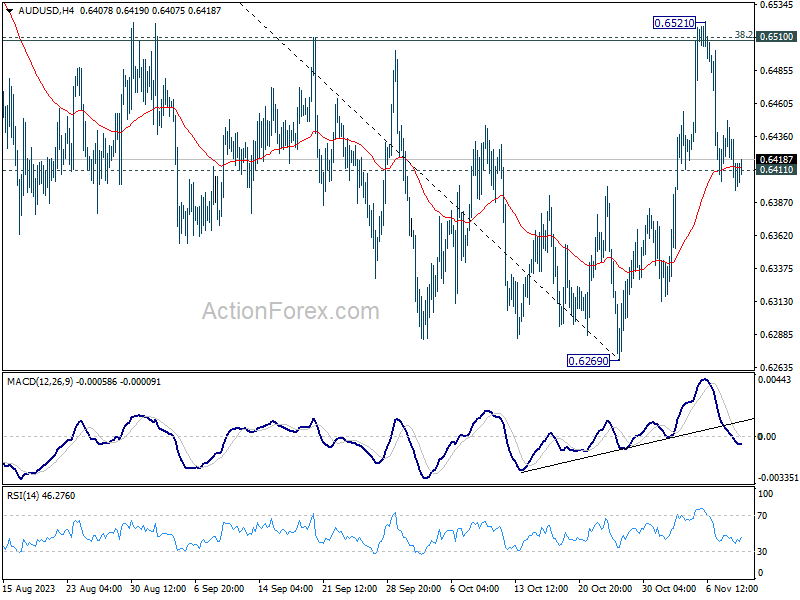

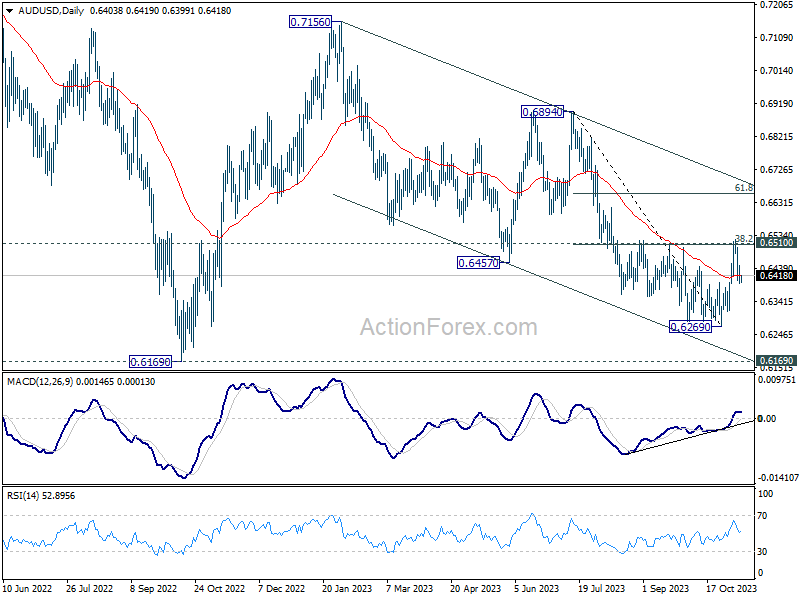

AUD/USD Daily Report

Daily Pivots: (S1) 0.6384; (P) 0.6417; (R1) 0.6435; More...

Intraday bias in AUD/USD stays neutral with focus on 0.6411 support and 55 4H EMA. On the downside, firm break of 0.6411 will indicate rejection by 0.6510 cluster resistance (38.2% retracement of 0.6894 to 0.6269 at 0.6508) , and turn bias back to the downside for retesting 0.6269 low. Nevertheless, decisive break of 0.6508/10 will argue that whole decline from 0.7156 might be completed with three waves down to 0.6269. Stronger rally should then be seen to medium term trend line resistance (now at 0.6700).

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of a corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

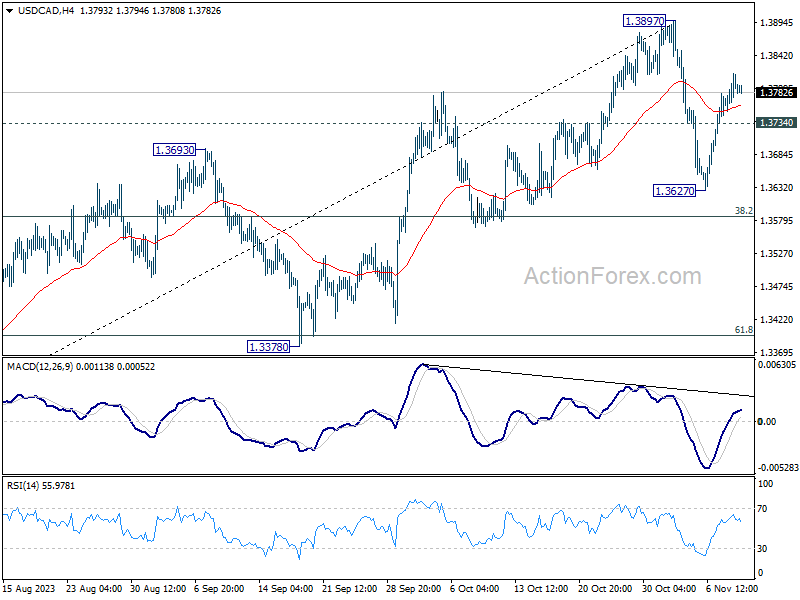

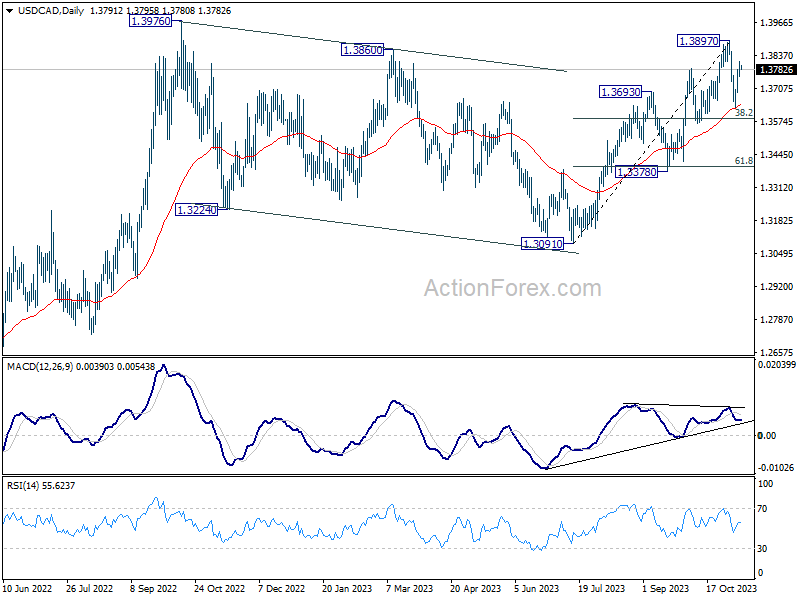

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3760; (P) 1.3787; (R1) 1.3820; More...

Intraday bias in USD/CAD remains mildly on the upside at this point. Rebound from 1.3627 is in progress for retesting 1.3897 resistance. On the downside, below 1.3734 minor support will turn bias back to the downside, to extend the corrective pattern from 1.3897 with another leg. But in this case, strong support should be seen from 38.2% retracement of 1.3091 to 1.3897 at 1.3589 to bring rebound.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). This will now remain the favored case as long as 1.3378 support holds. However, firm break of 1.3378 will argue that the pattern from 1.3976 is indeed still extending.

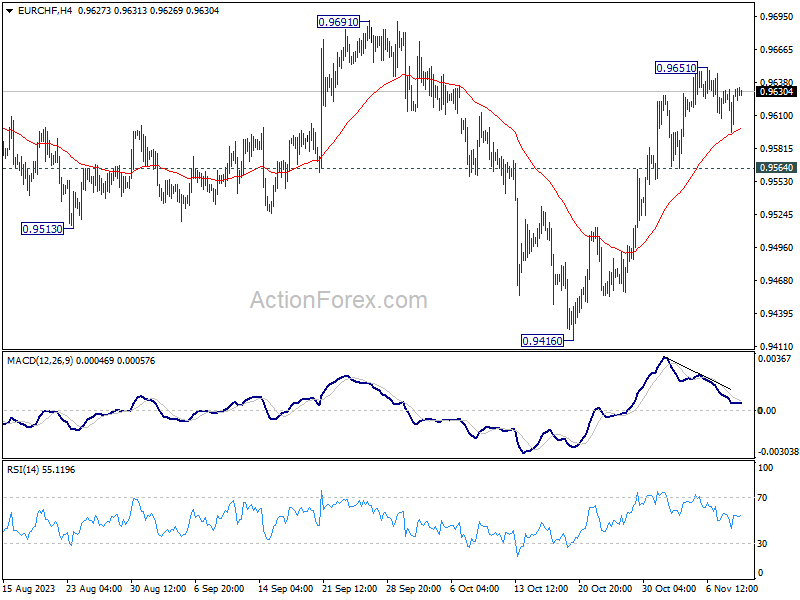

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9607; (P) 0.9621; (R1) 0.9645; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 0.9651 is extending. Further rally is in favor as long as 0.9564 minor support holds. Above 0.9651 will resume the rebound form 0.9416 to 0.9691 resistance first. Firm break there will argue that whole decline from 1.0095 has completed at 0.9416, just ahead of 0.9407 support (2022 low). Nevertheless, break of 0.9564 will turn bias back to the downside for deeper fall.

In the bigger picture, as long as 1.0095 resistance holds, price actions from 0.9407 are viewed as a three-wave consolidation pattern first. Current rise from 0.9416 might be the third leg. That is, larger down trend from 1.2004 (2018 high) might still resume through 0.9407 at a later stage. However, decisive break of 1.0095 will argue that the long term down trend is reversing.

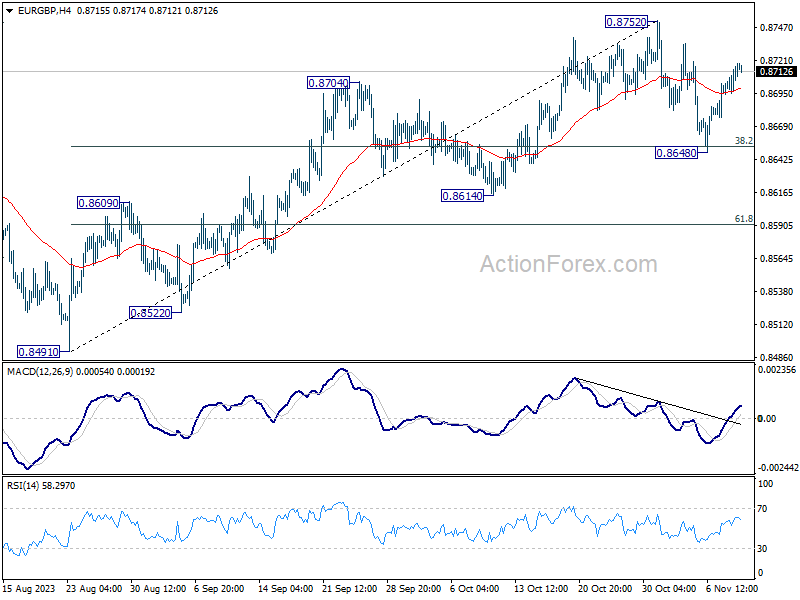

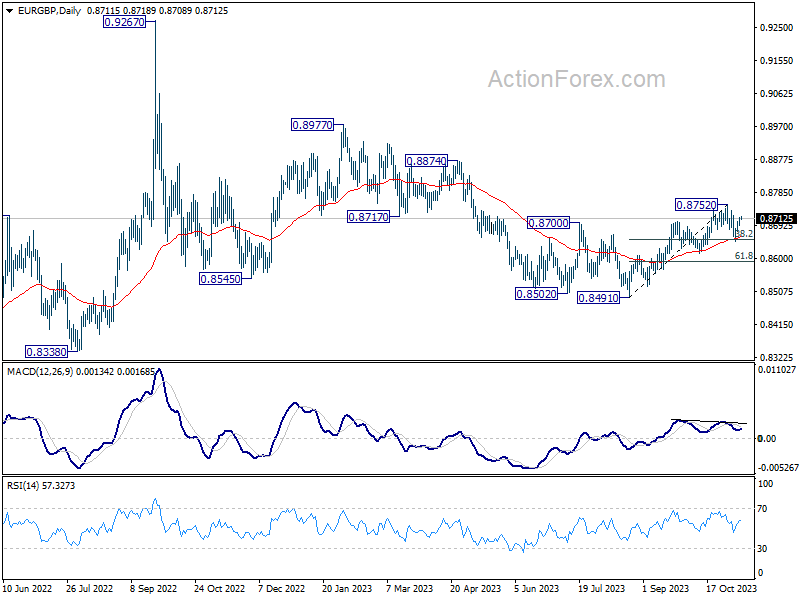

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8698; (P) 0.8708; (R1) 0.8727; More....

Intraday bias in EUR/GBP stays neutral for the moment. Consolidation from 0.8752 could extend with another falling leg. But in that case, downside should be contained by 0.8614 support to bring rebound. Break of 0.8752 resistance to resume the rally from 0.8491 is expected at a later stage.

In the bigger picture, current development suggests that whole down trend from 0.9267 (2022 high) has completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. This will remain the favored case as long as 0.8614 support holds.

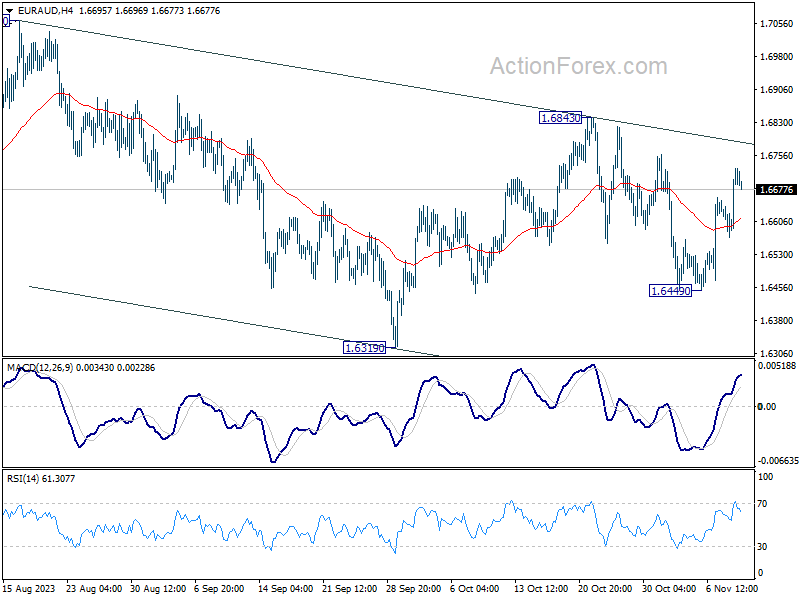

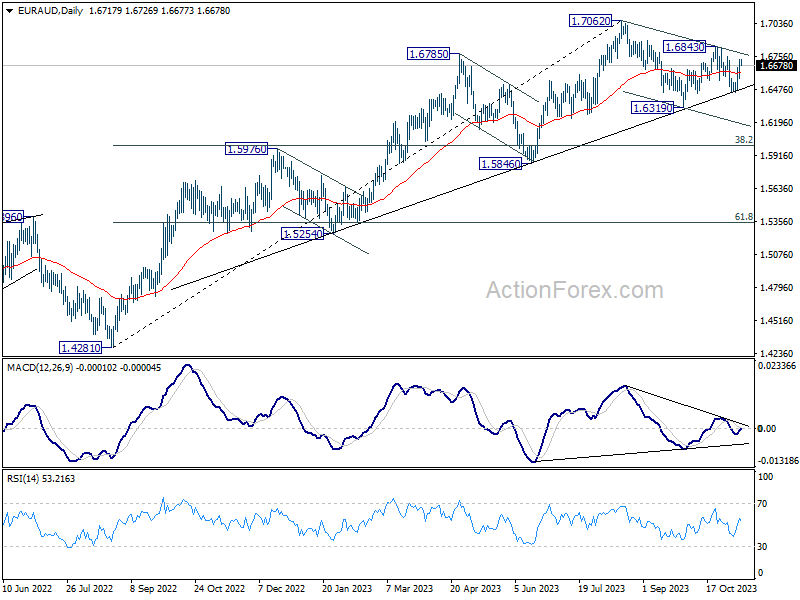

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6622; (P) 1.6676; (R1) 1.6781; More...

While EUR/AUD's rebound from 1.6449 extends, it's capped below 1.6843 resistance so far. Near term outlook is mixed and intraday bias stays neutral. On the downside, break of 1.6449 will target 1.6319 support first. Firm break there will resume the whole decline from 1.7062. However, above 1.6843 will resume the rebound from 1.6319 towards 1.7062 resistance instead.

In the bigger picture, current development suggests that 1.7062 is already a medium term top. Fall from there is seen as a correction to the up trend from 1.4281 (2022 low). While deeper decline might be seen, strong support should emerge from 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to contain downside. On the other hand, break of 1.6843 resistance will revive medium term bullishness that larger up trend is still in progress.

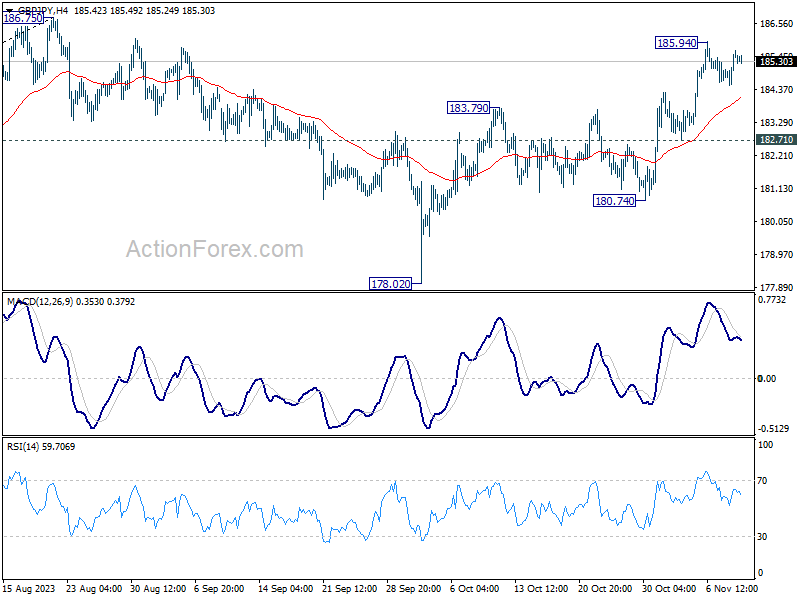

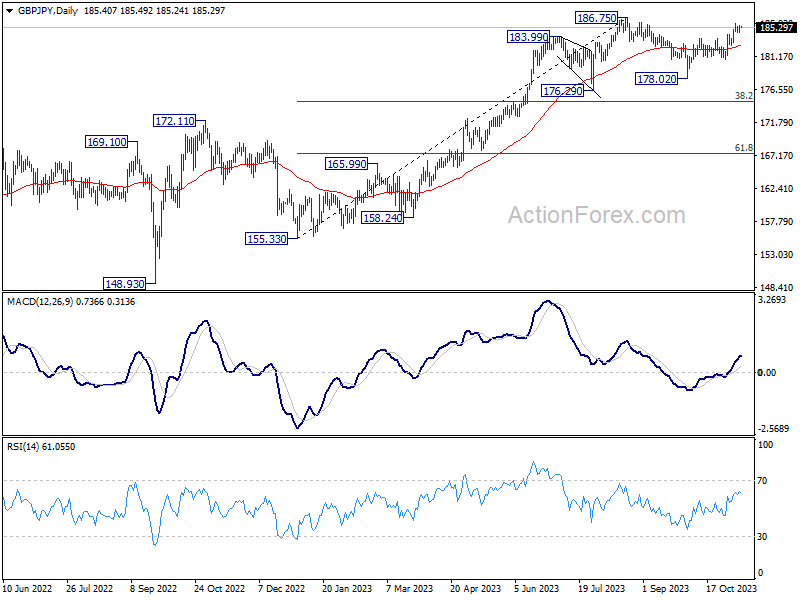

GBP/JPY Daily Outlook

Daily Pivots: (S1) 184.79; (P) 185.23; (R1) 185.92; More...

Intraday bias in GBP/JPY remains neutral and some more consolidations could be seen below 185.94 temporary top. But further rally is expected as long as 182.71 support holds. Above 185.94 will resume the rebound from 178.02 to retest 186.76 resistance first. Decisive break there will resume larger up trend.

In the bigger picture, as long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and bring lengthier and deeper consolidations.

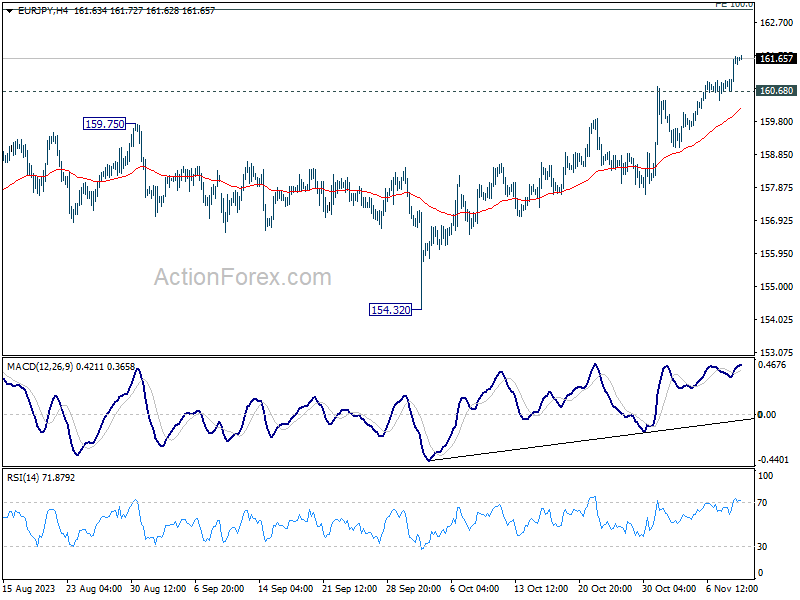

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.01; (P) 161.37; (R1) 162.04; More....

EUR/JPY's rally is still in progress and hits as high as 161.71 so far. Intraday bias stays on the upside for 163.06 projection level next. On the downside, below 160.68 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 139.05 at 163.06. On the downside, break of 154.32 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish even in case of deep pullback.

Euro Strengthens Amid Market Quietude, Bitcoin’s Rally Poses Tailwind for Tech

Euro is showing signs of fortitude in relatively subdued market conditions today. The overnight rebounds in EUR/USD and EUR/CHF indicate that bearish traders are hesitating to drive the market, while EUR/JPY continues its upward stride. On the other hand, Dollar is engaged in a tight contest with Euro, mostly reversing its losses from the previous week. Investors were left wanting more after Federal Reserve Chair Jerome Powell's recent speech, which skirted around pivotal topics such as interest rate changes and the economic forecast, focusing instead on forecasting.

For the current week so far, Dollar, Euro, and Swiss Franc are shaping up to be the frontrunners, while Australian Dollar, New Zealand Dollar, and Canadian Dollar lag behind. British Pound finds itself in a state of limbo, neither excelling nor trailing significantly.

In the equity domain, major US stock indices are encountering resistance, stalling at crucial levels—34147 for DOW, 4393 for S&P 500, and 13714 for NASDAQ. However, the crypto market, spearheaded by Bitcoin breakthrough above 36k mark, might provide a supportive breeze for the tech-heavy NASDAQ if the cryptocurrency continues to gather pace.

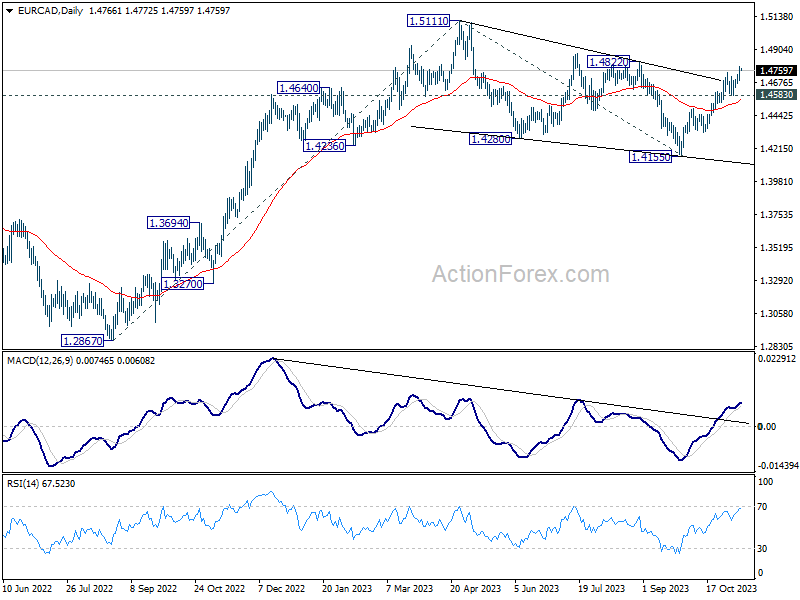

Technically, EUR/CAD's rally from 1.4155 resumed overnight and hit as high as 1.4787 so far. Outlook is unchanged that corrective fall from 1.5111 might have completed with three waves down to 1.4155 already. Further rally is expected as long as 1.4583 support holds. Decisive break of 1.4822 resistance will argue that larger up trend is ready to resume through 1.5111 high.

In Asia, Nikkei closed up 1.57%. Hong Kong HSI is down -0.33%. China Shanghai SSE is down -0.03%. Singapore Strait Times is up 0.25%. Japan 10-year JGB yield is down -0.0067 at 0.843. Overnight, DOW dropped -0.12%. S&P 500 rose 0.10%. NASDAQ rose 0.08%. 10-year yield dropped -0.048 to 4.523.

BoC minutes reflect division on path forward for interest rate

The latest deliberations within BoC have revealed a divide among officials over the course of monetary policy, as they confront the challenge of reigning in inflation without further rate hikes. At the heart of the debate is whether the current 5.00% policy rate will suffice in guiding inflation back to the targeted 2%.

The minutes from the October 25 meeting, where BoC maintained the interest rate, reflect this uncertainty. A faction within the bank is leaning towards additional tightening measures. "Some members felt that it was more likely than not that the policy rate would need to increase further to return inflation to target," the minutes read, highlighting concerns that the current policy stance may not be enough to temper rising prices.

On the flip side, there is a sense of cautious optimism among other members, who believe that maintaining the current rate might achieve the desired effect over time. "Others viewed the most likely scenario as one where a five per cent policy rate would be sufficient to get inflation back to the two per cent target, provided it was maintained at that level for long enough," the minutes elaborated.

This divergence in views has culminated in a consensus to adopt a "patient" approach, reflecting a strategy of watchful waiting while assessing incoming data. "They agreed to revisit the need for a higher policy rate at future decisions with the benefit of more information," according to the documented discussions.

BoJ Ueda awaits wage trends before altering policy

In today's parliamentary session, BoJ Governor Kazuo Ueda emphasized a cautious stance on Japan's monetary policy, acknowledging the need for more evidence before making any adjustments.

"We expect trend inflation to gradually approach 2 percent. But we'd like to wait until we have more conviction that sustained achievement of our price target comes into sight," Ueda said.

Highlighting the significance of wage trends, Governor Ueda noted, "Whether wage hikes will broaden and become embedded in society, firms begin to hike prices on prospects of rising wages, will be key to judging whether inflation target will be met sustainably."

He reaffirmed the Bank's current strategy: "Until then, we will maintain negative interest rates and the yield curve control framework."

The Summary of Opinions from the BoJ's October meeting, released separately, showed a notable stance from one member suggested optimism about wage growth, "It's highly possible that wage growth to be agreed in next year's base pay negotiations will exceed that agreed this year," and added that "achievement of the BoJ's price target is coming into sight."

One member went further to suggest that the chances of meeting the inflation target have increased, proposing that "It's therefore necessary for the BOJ to gradually adjust the degree of monetary easing down from its maximum level."

Another member's opinion highlighted that adjustments in yield controls are not just a mitigation of side-effects but also pave the way for future policy normalization.

Bitcoin breaks key fibonacci resistance amid ETF speculation

In a notable surge, Bitcoin has pierced through a key Fibonacci resistance level, stirring the market as whispers of a wave of Bitcoin ETF approvals by US SEC enhance investor optimism. The digital currency's leap forward comes amid speculations that the SEC could, within an eight-day window that started today, green-light up to 12 spot Bitcoin ETF filings. Despite the buzz, the market consensus still eyes January 10 as the likely date for concrete decisions.

Technically, near term outlook will now stay bullish as long as 33373 support holds. Next target is 100% projection of 15452 to 31815 from 24896 at 41259.

For the medium term, the break of 38.2% retracement of 68986 to 15452 at 35902 now opens the door to further rally to 61.8% retracement at 48536. The structure and momentum of the current rise will be monitor to assess whether rise form 15452 is a medium term corrective move, or the start of a long term up trend.

Looking ahead

ECB monthly economic bulletin is a highlight of the empty European calendar. US will release jobless claims later in the day.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.01; (P) 161.37; (R1) 162.04; More....

EUR/JPY's rally is still in progress and hits as high as 161.71 so far. Intraday bias stays on the upside for 163.06 projection level next. On the downside, below 160.68 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 139.05 at 163.06. On the downside, break of 154.32 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Current Account (JPY) Sep | 2.01T | 2.27T | 1.63T | 1.50T |

| 00:01 | GBP | RICS Housing Price Balance Oct | -63% | -65% | -69% | |

| 01:30 | CNY | CPI Y/Y Oct | -0.20% | -0.20% | 0.00% | |

| 01:30 | CNY | PPI Y/Y Oct | -2.60% | -2.70% | -2.50% | |

| 05:00 | JPY | Eco Watchers Survey: Current Oct | 49.5 | 50.2 | 49.9 | |

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 13:30 | USD | Initial Jobless Claims (Nov 3) | 210K | 217K |

Bitcoin breaks key fibonacci resistance amid ETF speculation

In a notable surge, Bitcoin has pierced through a key Fibonacci resistance level, stirring the market as whispers of a wave of Bitcoin ETF approvals by US SEC enhance investor optimism. The digital currency's leap forward comes amid speculations that the SEC could, within an eight-day window that started today, green-light up to 12 spot Bitcoin ETF filings. Despite the buzz, the market consensus still eyes January 10 as the likely date for concrete decisions.

Technically, near term outlook will now stay bullish as long as 33373 support holds. Next target is 100% projection of 15452 to 31815 from 24896 at 41259.

For the medium term, the break of 38.2% retracement of 68986 to 15452 at 35902 now opens the door to further rally to 61.8% retracement at 48536. The structure and momentum of the current rise will be monitor to assess whether rise form 15452 is a medium term corrective move, or the start of a long term up trend.