Sample Category Title

Nikkei 225 Technical: An Imminent Potential Minor Corrective Pull-Back

- The prior four days of the rally have reached an extreme overbought condition.

- Odds have increased for a minor pull-back scenario reinforced by the latest reading from the 4-hour RSI momentum indicator.

- Watch the 32,760 key short-term pivotal resistance with an immediate support zone at 32,120/31,620.

In the past week, the Japan 225 Index (a proxy for the Nikkei 225 futures) has indeed staged the expected bullish reversal after a retest close to its 200-day moving average and 30,490/320 medium-term pivotal support zone.

It rallied by +6.85% to print an intraday high of 32,823 on 3 November and notched its best weekly return since March 2022.

Overstretched rally

Fig 1: Japan 225 minor short-term trend as of 7 Nov 2023 (Source: TradingView, click to enlarge chart)

The past four days of bullish impulsive moves have now reached an extreme overbought condition as depicted by the 4-hour RSI momentum indicator with a reading of 82.84 printed yesterday, 6 November, its highest level since 17 May 2023.

Right now, the RSI indicator has just exited from its overbought which increases the odds of a minor pull-back towards the 20 and 50-day moving average region.

Watch the 32,760 key short-term pivotal resistance

If the 32,760 pivotal resistance (also the minor swing highs area of 25 September/12 October 2023) is not surpassed to the upside, the price actions of the Japan 225 Index may undergo a minor corrective pull-back towards the immediate support zone of 32,120/31,620 (50% Fibonacci retracement of the recent swift up move from 30 October low to 4 November 2023 high & the 20-day moving average) before a potential new bullish impulsive up move sequence unf0lds.

However, a clearance above 32,760 opens up scope to see the next intermediate resistance coming in at 33,410 in the first step (the medium-term descending trendline in place since the 19 June 2023 high).

China’s export decline deepens while imports rebound

China's export figures have taken a sharper downturn than anticipated in October, contracting by -6.4% yoy to USD 274.8B, exceeding market predictions of -3.1% yoy. This downturn marks the sixth consecutive month where China's exports have receded.

In contrast, imports defied expectations with a 3.0% yoy increase, a significant departure from the forecasted -5.4% yoy decline, and putting an end to an 11-month streak of contraction.

The culmination of these trade activities resulted in a considerable narrowing of the trade surplus, which shrunk from USD 77.7B to USD 56.5B. This is a stark contraction compared to the anticipated figure of USD 84.2B.

RBA hikes to 4.35%, future path hinges on evolving data

RBA announced an increase in cash rate target by 25 bps to 4.35%, aligning with market anticipations. Accompanying this move, RBA signaled a shift to a neutral policy stance, indicating that "whether further tightening of monetary policy is required... will depend upon the data and the evolving assessment of risks ."

In the statement, RBA said inflation is "still too high" and is proving "more persistent than expected a few months ago". A rate hike was was warranted today to be "more assured" that inflation would return to target in a "reasonable timeframe".

The central bank's outlook is tempered by "significant uncertainties," particularly regarding the persistence of services inflation which has been notably resilient internationally and could mirror in the Australian market.

The effectiveness of monetary policy changes and the response of wage settings and pricing decisions amid a slowdown in economic growth are areas of unpredictability, especially given the current tightness of the labor market. Household consumption prospects are also veiled with uncertainty, too. T

Looking abroad, RBA's statement brought to light the ongoing global uncertainties, notably the economic trajectory of China and the far-reaching consequences of international conflicts, adding further dimensions to the central bank's considerations.

(RBA) Statement by Michele Bullock, Governor: Monetary Policy Decision

At its meeting today, the Board decided to raise the cash rate target by 25 basis points to 4.35 per cent. It also increased the interest rate paid on Exchange Settlement balances by 25 basis points to 4.25 per cent.

Inflation in Australia has passed its peak but is still too high and is proving more persistent than expected a few months ago. The latest reading on CPI inflation indicates that while goods price inflation has eased further, the prices of many services are continuing to rise briskly. While the central forecast is for CPI inflation to continue to decline, progress looks to be slower than earlier expected. CPI inflation is now expected to be around 3½ per cent by the end of 2024 and at the top of the target range of 2 to 3 per cent by the end of 2025. The Board judged an increase in interest rates was warranted today to be more assured that inflation would return to target in a reasonable timeframe.

The Board had held interest rates steady since June following an increase of 4 percentage points since May last year. It had judged that higher interest rates were working to establish a more sustainable balance between supply and demand in the economy. Furthermore, it had noted that the impact of the more recent rate rises would continue to flow through the economy. It had therefore decided that it was appropriate to hold rates steady to provide time to assess the impact of the increase in interest rates so far. In particular, the Board had indicated that it would be paying close attention to developments in the global economy, trends in household spending, and the outlook for inflation and the labour market.

Since its August meeting, the Board has received updated information on inflation, the labour market, economic activity and the revised set of forecasts. The weight of this information suggests that the risk of inflation remaining higher for longer has increased. While the economy is experiencing a period of below-trend growth, it has been stronger than expected over the first half of the year. Underlying inflation was higher than expected at the time of the August forecasts, including across a broad range of services. Conditions in the labour market have eased but they remain tight. Housing prices are continuing to rise across the country.

At the same time, high inflation is weighing on people's real incomes and household consumption growth is weak, as is dwelling investment. Given that the economy is forecast to grow below trend, employment is expected to grow slower than the labour force and the unemployment rate is expected to rise gradually to around 4¼ per cent. This is a more moderate increase than previously forecast. Wages growth has picked up over the past year but is still consistent with the inflation target, provided that productivity growth picks up.

Returning inflation to target within a reasonable timeframe remains the Board's priority. High inflation makes life difficult for everyone and damages the functioning of the economy. It erodes the value of savings, hurts household budgets, makes it harder for businesses to plan and invest, and worsens income inequality. And if high inflation were to become entrenched in people's expectations, it would be much more costly to reduce later, involving even higher interest rates and a larger rise in unemployment. To date, medium-term inflation expectations have been consistent with the inflation target and it is important that this remains the case.

There are still significant uncertainties around the outlook. Services price inflation has been surprisingly persistent overseas and the same could occur in Australia. There are uncertainties regarding the lags in the effect of monetary policy and how firms' pricing decisions and wages will respond to the slower growth in the economy at a time when the labour market remains tight. The outlook for household consumption also remains uncertain, with many households experiencing a painful squeeze on their finances, while some are benefiting from rising housing prices, substantial savings buffers and higher interest income. And globally, there remains a high level of uncertainty around the outlook for the Chinese economy and the implications of the conflicts abroad.

Whether further tightening of monetary policy is required to ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks. In making its decisions, the Board will continue to pay close attention to developments in the global economy, trends in domestic demand, and the outlook for inflation and the labour market. The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome.

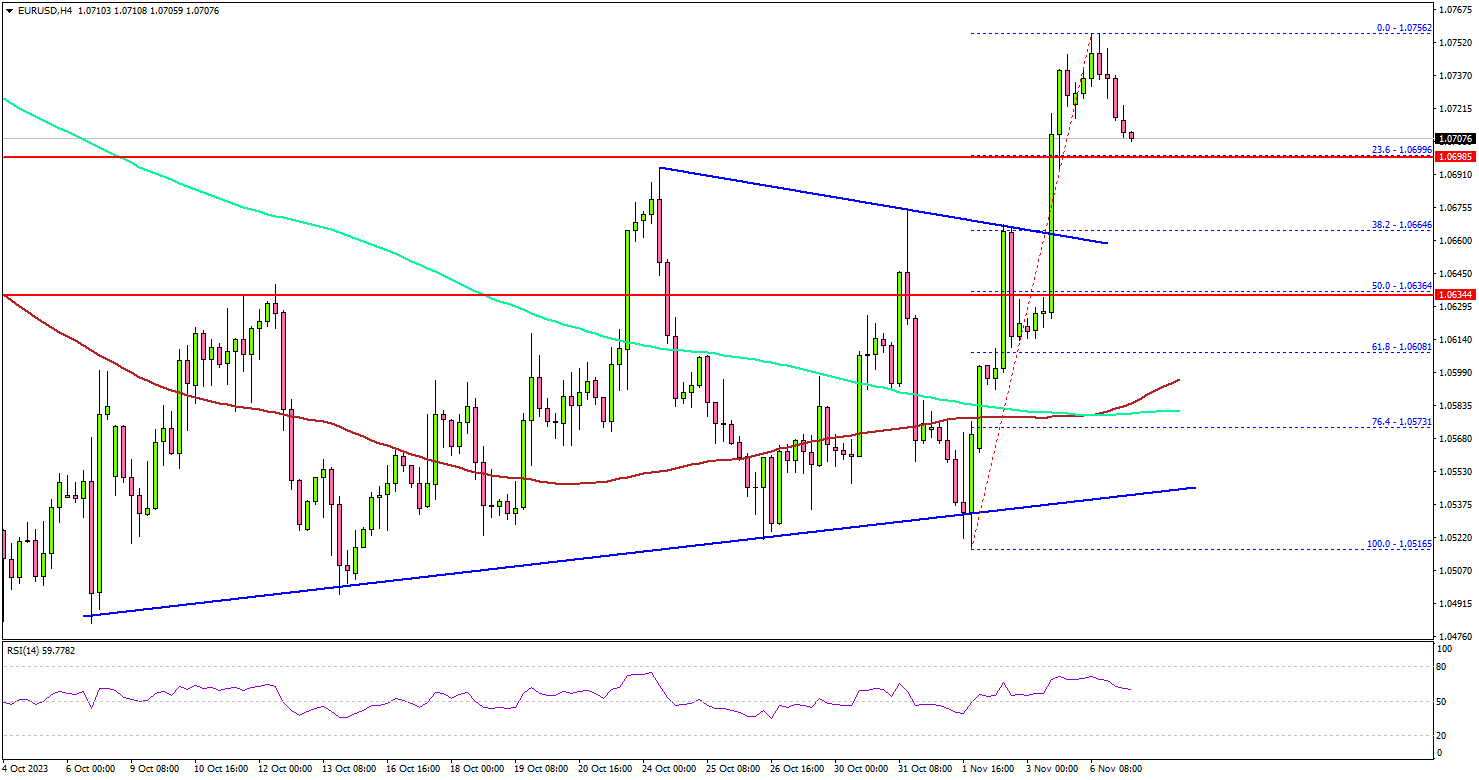

EUR/USD Regains Strength As Dollar Takes Back Seat

Key Highlights

- EUR/USD started a recovery wave above the 1.0650 resistance.

- It broke a key contracting triangle with resistance near 1.0665 on the 4-hour chart.

- GBP/USD surged above the 1.2300 resistance zone.

- Ethereum and XRP extended their rally with strong bullish moves.

EUR/USD Technical Analysis

The Euro formed a base and started a recovery wave above 1.0600 against the US Dollar. EUR/USD cleared many hurdles near 1.0620 to move into a positive zone.

Looking at the 4-hour chart, the pair broke a key contracting triangle with resistance near 1.0665. It even settled above the 1.0700 level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

Finally, it tested the 1.0750 resistance. If the bulls remain in action, there could be more upsides toward the 1.0800 level. Any more gains might send it toward the 1.0880 level.

If there is a downside correction, the pair might find bids near the 1.0700 level. The first major support is now forming near the 1.0665 level, below which the pair could test the 1.0635 pivot level in the near term.

The main support sits near the 1.0580 level and the 100 simple moving average (red, 4 hours). A downside break below the 1.0580 level might spark a sharp decline. The next key support sits at 1.0500.

Looking at GBP/USD, the pair found support near the 1.2070 level and recently started a strong increase above the 1.2300 level.

Economic Releases

- US Goods and Services Trade Balance for Sep 2023 - Forecast $-60.2B, versus $-58.3B previous.

Japan’s labor cash earnings up 1.2% yoy, but real wages down for 18th month

Japan reported a modest increase in nominal labor cash earnings in September, with 1.2% yoy rise that slightly exceeded market expectations of 1.0% yoy gain. This uptick, an improvement from the previous month's 0.8%, may seem like a positive indicator at first glance, with base salary growth also marking an increase to 1.4% yoy from August's 1.2% yoy.

However, not all components of earnings showed strength. Special payments, often a volatile category, continued to decline by -6.0% yoy , albeit a less severe contraction than -6.3% yoy reported in August. Meanwhile, overtime pay exhibited a marginal increase, rising 0.7% yoy, suggesting a modest uptick in extra working hours.

The nuanced picture of Japan's wage situation becomes more concerning when adjusted for inflation. Real wages, which reflect the purchasing power of income, fell sharply by -2.4% yoy compared to the same month last year, marking the 18th consecutive month of decline. This persistent slide in real wages points to the squeeze on household income as inflation outpaces nominal wage growth.

In line with the strain on incomes, household spending dipped by -2.8% yoy , although the figure is marginally better than the anticipated -3.0% yoy fall. This marks the seventh straight month of decline, underscoring the ongoing reticence of Japanese consumers to open their wallets amid economic uncertainties.

On a more positive note, on a seasonally adjusted basis, household spending saw an unexpected increase of 0.3% mom, defying expectations of a -0.4% mom decline.

BoE’s Pill suggests rate cuts by mid-2024 “not totally unreasonable”

In an online event overnight, BoE Chief Economist Huw Pill acknowledged the slower pace of reduction compared to global counterparts. The UK has also seen inflation climbed higher. Despite this lag, he expressed confidence that "We're going to see the UK get down to levels more comparable to what we're seeing in the rest of the world."

Pill's remarks came amid the backdrop of market expectations that have priced in a potential rate cut as early as August 2024. He finds this timing "not totally unreasonable," highlighting it's a period when the Bank might reassess its stance, albeit with the usual caveat that economic conditions are fluid and subject to change.

Moreover, Pill tempered expectations of a return to the ultra-low interest rate environment seen pre-pandemic, indicating that future rates are more likely to find a middle ground. This perspective reinforces the notion that the era of zero interest rates was an anomaly rather than a standard monetary condition.

Fed’s Kashkari signals preference for stronger policy action to tame inflation target

Minneapolis Federal Reserve President Neel Kashkari expressed concern over the consequences of insufficient tightening in a WSJ interview, saying, "Under-tightening will not get us back to 2% in a reasonable time." He favored a stance that leans toward an aggressive policy rather than a cautious one.

In a subsequent conversation with Fox News, Kashkari drew attention to the economy's endurance despite Fed's recent rounds of rate increases. "The economy has proved to be really resilient even though we've raised interest rates a lot over the past couple of years. That's good news," he said. This resilience suggests that the economy might be better positioned to handle further rate hikes, should they be deemed necessary.

However, Kashkari was clear that the Fed's job is far from over, as inflation remains a critical challenge. "We need to let the data keep coming to us to see if we really have got the inflation genie back in the bottle so to speak," he conveyed, emphasizing the need for ongoing vigilance. He added, "We haven't completely solved the inflation problem. We still have more work ahead of us to get it done."

AUDUSD Wave Analysis

- AUDUSD reversed from resistance level 0.6500

- Likely to fall to support level 0.6450

AUDUSD currency pair recently reversed down from the pivotal resistance level 0.6500 (former strong support from May, which has been reversing the pair from the end of August).

The resistance level 0.6500 was strengthened by the upper daily Bollinger Band and by the 38.2% Fibonacci correction of the previous downward impulse from July.

Given the predominant daily downtrend, AUDUSD can be expected to fall further toward the next support level 0.6450.

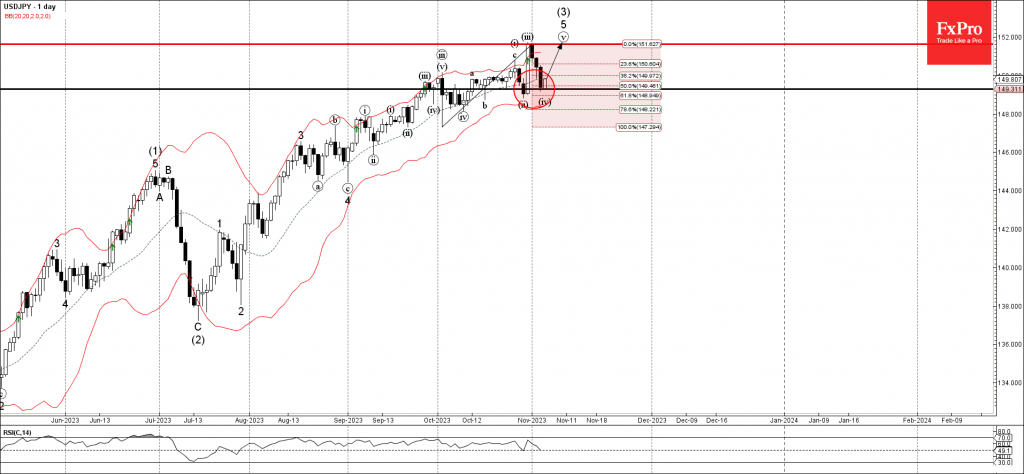

USDJPY Wave Analysis

- USDJPY reversed from support level 149.30

- Likely to rise to resistance level 152.00

USDJPY currency pair recently reversed up from the key support level 149.30 (which has been reversing the pair from the middle of October as can be seen below).

The support level 149.30 was strengthened by the 50% Fibonacci correction of the previous sharp upward impulse from the start of last month.

Given the strength of the active uptrend, USDJPY can be expected to rise further toward the next resistance level 152.00 (top of wave iii and the target for the completion of the active impulse wave v).