Sample Category Title

BoE’s Pill suggests rate cuts by mid-2024 “not totally unreasonable”

In an online event overnight, BoE Chief Economist Huw Pill acknowledged the slower pace of reduction compared to global counterparts. The UK has also seen inflation climbed higher. Despite this lag, he expressed confidence that "We're going to see the UK get down to levels more comparable to what we're seeing in the rest of the world."

Pill's remarks came amid the backdrop of market expectations that have priced in a potential rate cut as early as August 2024. He finds this timing "not totally unreasonable," highlighting it's a period when the Bank might reassess its stance, albeit with the usual caveat that economic conditions are fluid and subject to change.

Moreover, Pill tempered expectations of a return to the ultra-low interest rate environment seen pre-pandemic, indicating that future rates are more likely to find a middle ground. This perspective reinforces the notion that the era of zero interest rates was an anomaly rather than a standard monetary condition.

Fed’s Kashkari signals preference for stronger policy action to tame inflation target

Minneapolis Federal Reserve President Neel Kashkari expressed concern over the consequences of insufficient tightening in a WSJ interview, saying, "Under-tightening will not get us back to 2% in a reasonable time." He favored a stance that leans toward an aggressive policy rather than a cautious one.

In a subsequent conversation with Fox News, Kashkari drew attention to the economy's endurance despite Fed's recent rounds of rate increases. "The economy has proved to be really resilient even though we've raised interest rates a lot over the past couple of years. That's good news," he said. This resilience suggests that the economy might be better positioned to handle further rate hikes, should they be deemed necessary.

However, Kashkari was clear that the Fed's job is far from over, as inflation remains a critical challenge. "We need to let the data keep coming to us to see if we really have got the inflation genie back in the bottle so to speak," he conveyed, emphasizing the need for ongoing vigilance. He added, "We haven't completely solved the inflation problem. We still have more work ahead of us to get it done."

AUDUSD Wave Analysis

- AUDUSD reversed from resistance level 0.6500

- Likely to fall to support level 0.6450

AUDUSD currency pair recently reversed down from the pivotal resistance level 0.6500 (former strong support from May, which has been reversing the pair from the end of August).

The resistance level 0.6500 was strengthened by the upper daily Bollinger Band and by the 38.2% Fibonacci correction of the previous downward impulse from July.

Given the predominant daily downtrend, AUDUSD can be expected to fall further toward the next support level 0.6450.

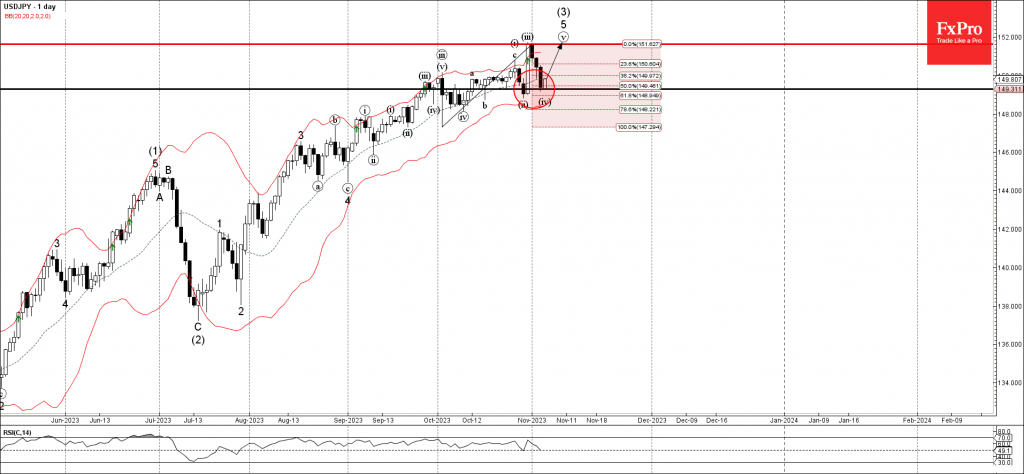

USDJPY Wave Analysis

- USDJPY reversed from support level 149.30

- Likely to rise to resistance level 152.00

USDJPY currency pair recently reversed up from the key support level 149.30 (which has been reversing the pair from the middle of October as can be seen below).

The support level 149.30 was strengthened by the 50% Fibonacci correction of the previous sharp upward impulse from the start of last month.

Given the strength of the active uptrend, USDJPY can be expected to rise further toward the next resistance level 152.00 (top of wave iii and the target for the completion of the active impulse wave v).

Aussie Soars to 3-Month High, RBA Expected to Hike

- AUD/USD climbs after soft US nonfarm payrolls

- RBA rate decision a 50/50 toss-up

The Australian dollar has edged lower on Monday, after huge gains on Friday. In the North American session, AUD/USD is trading at 0.6499, down 0.21%.

On Friday, the Aussie posted spectacular gains, rising 1.22% and hitting its highest level since August 10th. The US dollar retreated against the majors on Friday, suffering sharp losses after a softer-than-expected nonfarm payrolls report.

Nonfarm payrolls fell to 150,000 in October, down from a downwardly revised 297,000 in September and shy of the consensus estimate of 170,000. The reading wasn’t a massive miss of the forecast, but investors jumped all over the soft reading as expectations jumped that the Fed could be done with tightening. The Fed rate odds of a hike in December have fallen to 10%, compared to 24% just a week ago, according to the CME Fed Watch Tool. We can expect to hear the markets talk more and more about a rate cut sometime in 2024.

The RBA meets on Tuesday and we’ve seen a remarkable swing in the RBA rate odds. Just a few weeks ago, the probability of a pause was close to 100%, but that has changed dramatically. According to the ASX RBA rate tracker, the odds of a hike are now 50/50, making it a live meeting that could see significant volatility from the Australian dollar.

RBA policy makers have a tough call to make after holding rates four straight times. Inflation has been falling slowly but the current level of 5.4% is much higher than the 2% target. Inflation expectations remain high and the RBA wants to see these expectations remain anchored; otherwise, the battle with inflation will become even more difficult.

AUD/USD Technical

- AUD/USD is putting pressure on resistance at 0.6523. Above, there is resistance at 0.6582

- 0.6449 and 0.6379 are providing support

Sunset Market Commentary

Markets

Markets got some reprieve today after last week’s heavy correction amid an empty eco calendar. These conditions will remain at play throughout the week, rerouting market focus to things like US supply, central bank speeches, risk sentiment or just underlying momentum. Technical considerations come in to play as well. Core bonds drifted lower with German yields adding 3.4 bps (2-yr) to 6.5 bps (30-yr) and US yields increasing by 2.9 bps (30-yr) to 4.2 bps (5-yr). The German 10-yr yield tries to regain/retain the 2.68% neckline of a double top formation. The US 10-yr yield bounced off first support at 4.51%. European stock markets failed to build on Friday’s WS gains (up to +1.4% for Nasdaq) or this morning’s Asian rally (huge Korean outperformance on short selling ban). Key indices currently lose up to 0.5% while Wall Street opens with small gains. Brent crude bounces off the $85/b support area after Saudi Arabia and Russia confirmed their commitment to additional output cuts ($1.3mn/day combined) until the end of the year amid weakening demand and tensions in the Middle-East. The trade-weighted dollar stabilizes around the sell-off lows just above 105, but doesn’t make any additional ground, staying below the lost neckline of a triple top formation (105.55). The same goes for EUR/USD at 1.0740. USD/JPY is rising back to the 150-mark following comments by BoJ governor Ueda who signaled a low probability of ending negative rates before year-end. The likelihood of realizing the outlook for achieving the 2% price stability target is nevertheless rising, suggesting the gentle BoJ normalization path will continue. There are many ECB/Fed members scheduled to speak later this week, including ECB Lagarde and Fed Powell on Thursday, but for now we have to do with comments by former vice Fed chair and current director of the national Economic council, Brainard. She said that the US economy is coming to the point of sustainable growth with most forecasters taking recession calls off the table. EUR/GBP treads water at 0.8670. This week’s UK agenda contains a BoE Bailey speech (Thursday) and Q3 GDP data (Friday).

News & Views

The ECB in a research publication finds that large euro area companies are relocating production across the world more actively than they used to do. They’ve come to that conclusion through a survey of corporations that combined represent about 5% of the euro zone’s economic output. The respondents cited rising geopolitical risks as a driver that’s increasingly competing with traditional motivations for outsourcing that include cutting costs or improving efficiency. The pandemic and the energy crisis thereafter served as a wake-up call to the fragility of global supply chains, prompting a preference for more resilience and independence. This does not only include moving operations back into the European bloc. Companies also plan to diversify more outside the EU, for example where they source inputs. Many of them identified China as the “dominant source of critical inputs” while mentioning the country the most in terms of perceived risks.

Britain’s “big five” – the leading business groups – are calling on UK finance minister Hunt to cut business taxes, improve the power grid and address skill shortages to unlock private investment in and as such lift the economy. They are seeking, amongst others, a permanent 100% tax relief on capital spending and want the government to allow for more immigration. Hunt unveils a package of economic measures on November 22 but has downplayed expectations for big handouts with inflation still well above the 2% target. In addition, within the limited fiscal headroom he has, Hunt faces a dilemma between either heeding the group’s call (and caving to growing pressure from within the Tory party) or going for more popular initiatives such as cutting inheritance taxes. The latter should be seen against the backdrop of Hunt’s Tory party lagging Labour opposition in the polls by some 20 points. The UK has to hold general elections no later than January 2025.

Weekly Technical Outlook – EURGBP, AUDUSD, USDJPY

- UK GDP in focus this week; pound could significantly benefit from a strong print

- RBA meeting and Chinese data could push aussie even higher against the US dollar

- USDJPY could break below its upward trending channel if Japanese data improve

UK GDP Q3 print -> EURGBP

The Bank of England kept its main bank rate unchanged at last week’s meeting despite the inflation rate remaining at a very high level. Bailey et al kept the door open to further tightening if needed – 3 members actually voted for a 25bps rate move at this meeting – but concerns about the growth outlook appear to be multiplying. In this context, on Friday we will get the preliminary GDP print for the third quarter of 2023. Market expectations point to a negative figure with strong downside risk.

A weak set of data releases this week, especially Friday’s GDP print, could accelerate the current rally in euro-pound, potentially allowing euro bulls to test the 0.8794-0.8815 area. On the flip side, a plethora of upside surprises this week could help the pound bulls recover part of their recent losses. A strong move below the busy 0.8615-0.8647 looks plausible.

RBA meeting and Chinese data -> AUDUSD

The Reserve Bank of Australia will wrap up the current round of central bank meetings. There are very strong expectations, especially from analysts, for a 25bps rate hike from the RBA on Tuesday after pausing for three consecutive meetings. The market is assigning a more modest probability for a rate hike announcement, potentially opening the door for a surprise reaction in the FX market if the RBA indeed decides to hike and maintains its hawkish rhetoric.

China is another key driver of the aussie, and there is a busy data schedule this week. The key releases will come out on Thursday when the October CPI is expected to show a negative yearly change, raising concerns about the level of domestic consumer demand.

The aussie has been rallying against the US dollar since testing the November 3, 2022 low at 0.6271 in late October, partly due to expectations of an RBA rate hike. It is now trading at a 3-month high. A combination of a hawkish rate hike from the RBA and an upside surprise in Chinese inflation could accelerate the current upleg, potentially towards the 200-day simple moving average (SMA) at 0.6609.

On the other hand, a dovish rate hike by RBA, or even a decision to pause, along with weaker Chinese data will probably put a dent in the current bullish sentiment in aussie-dollar. A move towards the 50-day SMA could take place, partly reversing the recent bullish move.

Japanese earnings data and BoJ minutes -> USDJPY

With the market feeling somewhat disappointed by the recent Bank of Japan meeting and its change in the yield curve control mechanism, the focus now turns to the weekly earnings data and the first draft of minutes from the aforementioned gathering. BoJ members have been quite vocal about the importance of earnings growth in their attempt to start curtailing the current very accommodative BoJ stance. Recent earnings prints have not been optimistic but maybe this trend will change this week.

In addition, the Summary of Opinions published on Thursday could offer more insight into the internal discussion that led to the YCC framework change and the overall assessment of the current state of the Japanese economy from the policy board.

Amidst these developments and with the market digesting the recent Fed meeting, US dollar-yen is testing the lower boundary of its upward trending channel. Stronger earnings data and hawkish minutes could result in a repeat of the July downwards breakout. On the flip side, weaker data releases and the dovish minutes could potentially allow the dollar-yen pair to retest its recent high

Rally Running on Fumes after Fed and NFP Boost

It's been a relatively subdued start to trading on Monday and the US is eyeing a similar open, with stock markets struggling to maintain the momentum from the second half of last week.

Investors got everything they wanted from the Federal Reserve and the jobs report. Chair Jerome Powell and his colleagues adopted a slightly less hawkish tone for the meeting while maintaining its extremely cautious position on inflation and interest rates.

The jobs report, meanwhile, brought a miss on the NFP number - alongside downward revisions totaling another 101,000 jobs from prior releases - and arguably more important, a miss on the wages component meaning two of the last three reports have produced 0.2% monthly readings. If repeated, this could be a game changer.

The Fed is desperate to take some heat out of the labor market as it believes it's required to get inflation sustainably back to 2%. But if wage growth continues to fall, 2% inflation may be achievable without too much disruption. I'm not sure that's the likely outcome at the moment, but it's certainly a positive development.

That said, the response in the second half of the week didn't look particularly sustainable. It was arguably over the top under the circumstances but investors have been eagerly awaiting the turning point in the data. Perhaps they've been premature on this occasion but data over the coming weeks may prove otherwise.

Oil choppy as Saudi and Russia recommit to end of year cuts

Oil prices remain very choppy and are trading a little over 1% higher on Monday. Russia and Saudi Arabia once again reaffirmed their commitment to output restrictions until the end of the year which isn't surprising under the circumstances and it's not new information as it aligns with what they've said previously.

Weaker economic expectations have weighed on crude prices recently which has contributed to prices pulling off their highs and, arguably, once again justified the positions of OPEC+ nations in cutting supply. It's not a question of whether the two countries keep to end-of-year targets, but whether they extend them.

Gold struggling to break $2,000

Gold rallied above $2,000 for the fourth time in six days on Friday and, just as it did on the previous three occasions, failed to capitalize on the breakout before falling back below. That's not a particularly bullish signal and suggests the rally over the last month is running on fumes. We may still see a break above $2,000 but another bullish catalyst may be required.

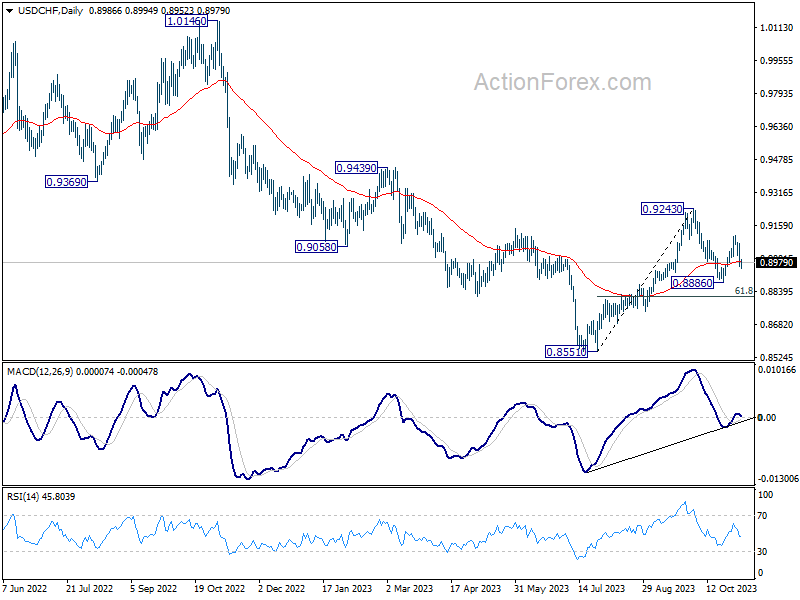

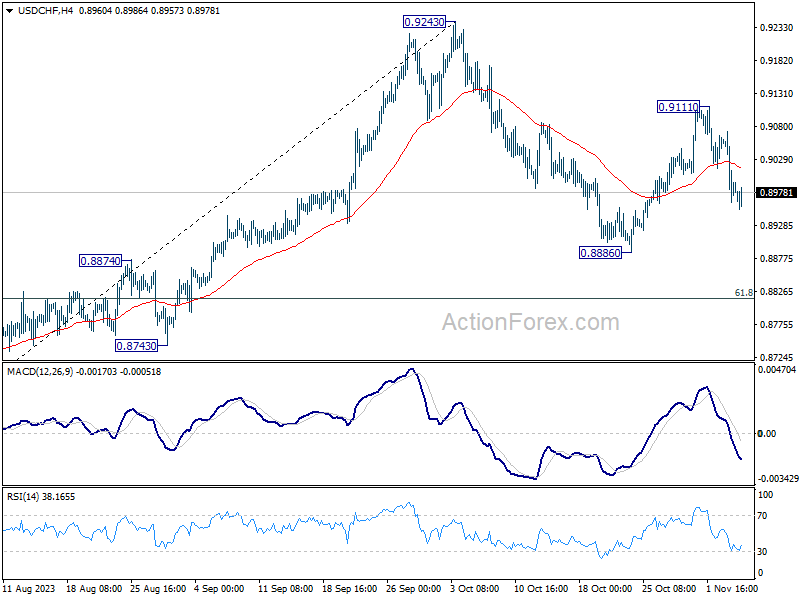

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8949; (P) 0.9011; (R1) 0.9057; More....

No change in USD/CHF's outlook and intraday bias stays on the downside for 0.8886 support first. Break there will resume whole decline from 0.9243 to 0.8815 fibonacci support. For now, risk will be on the downside as long as 0.9111 resistance holds, in case of recovery.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.