Sample Category Title

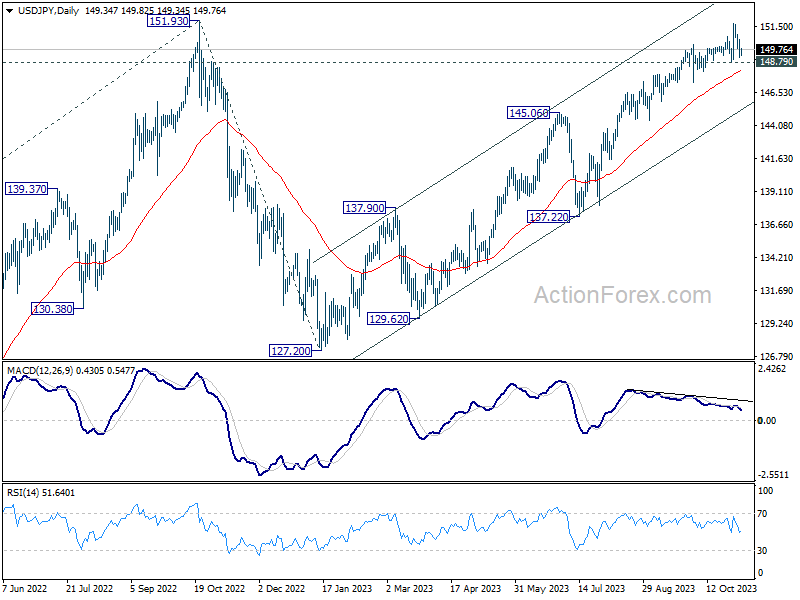

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.89; (P) 150.43; (R1) 151.02; More...

Outlook in USD/JPY is unchanged and intraday bias stays neutral. Price actions from 151.69 could still be seen as a consolidation pattern only. However, firm break of 148.79 will indicate rejection by 151.93 key resistance, and bring deeper fall through 147.28 support.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 to 151.93 from 127.20 at 157.69.

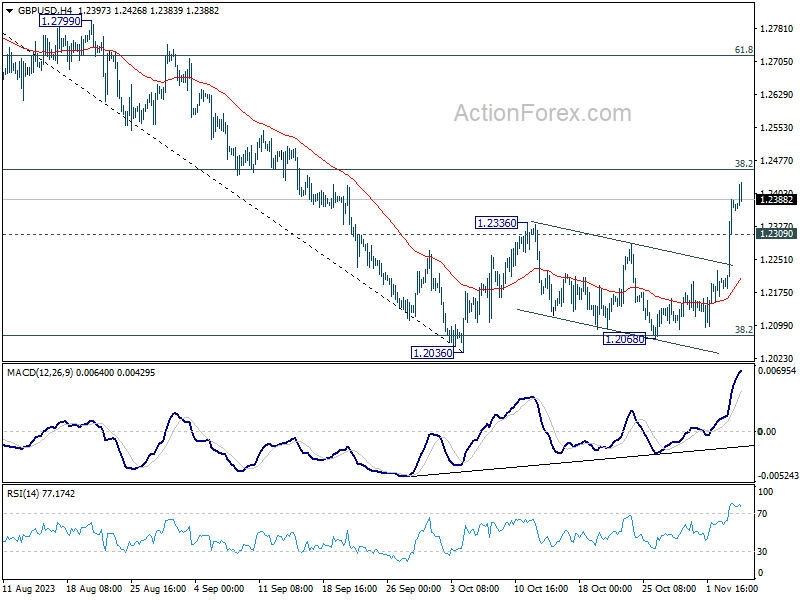

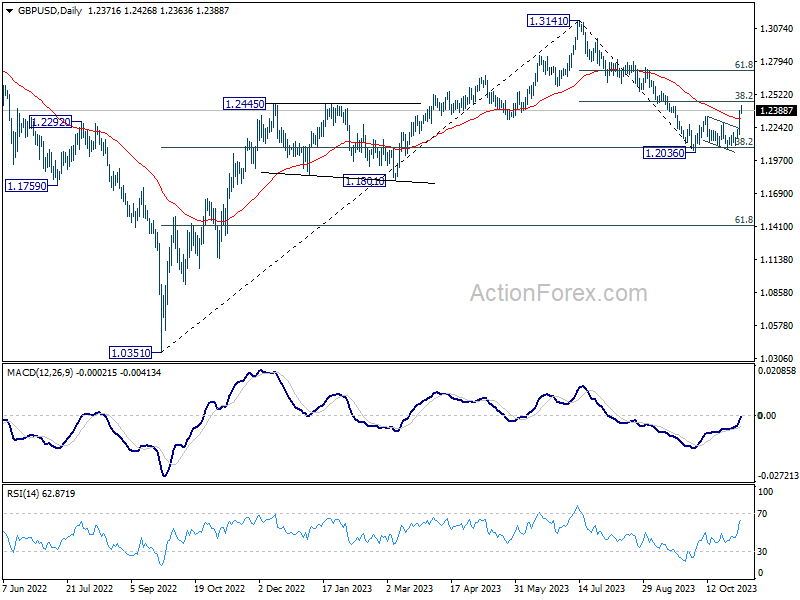

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2247; (P) 1.2318; (R1) 1.2452; More

Intraday bias in GBP/USD remains on the upside as rise from 1.2036 is in progress. Further rally should be seen to 38.2% retracement of 1.3141 to 1.2036 at 1.2458. Sustained break there will pave the way to 61.8% retracement at 1.2783. On the downside, below 1.2309 minor support will turn intraday bias neutral first.

In the bigger picture, the strong rebound from 38.2% retracement of 1.0351 to 1.3141 at 1.2075 argues that price action from 1.3141 are merely a correction to rise from 1.0351 (2022 low). Current rally from 1.2036 is tentatively seen as the second leg of the pattern. Hence, while further rally is in favor, upside should be limited by 1.3141 to start the third leg.

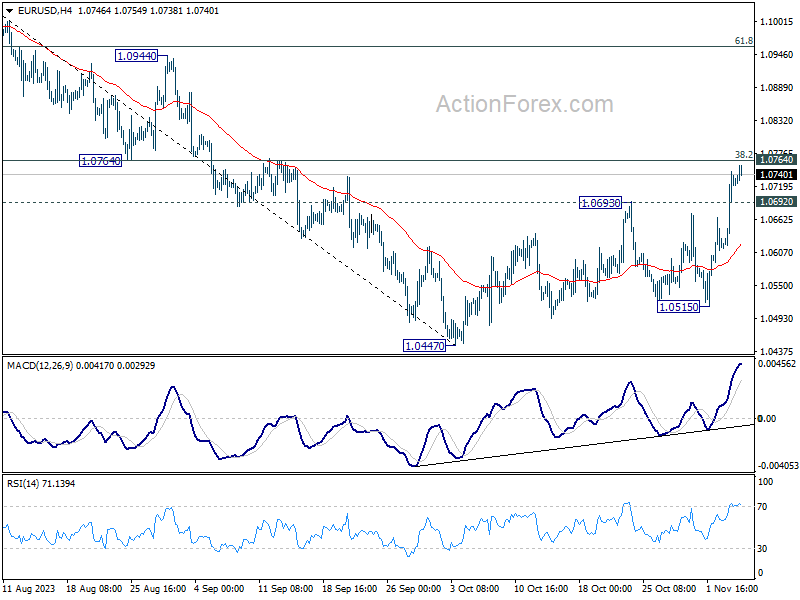

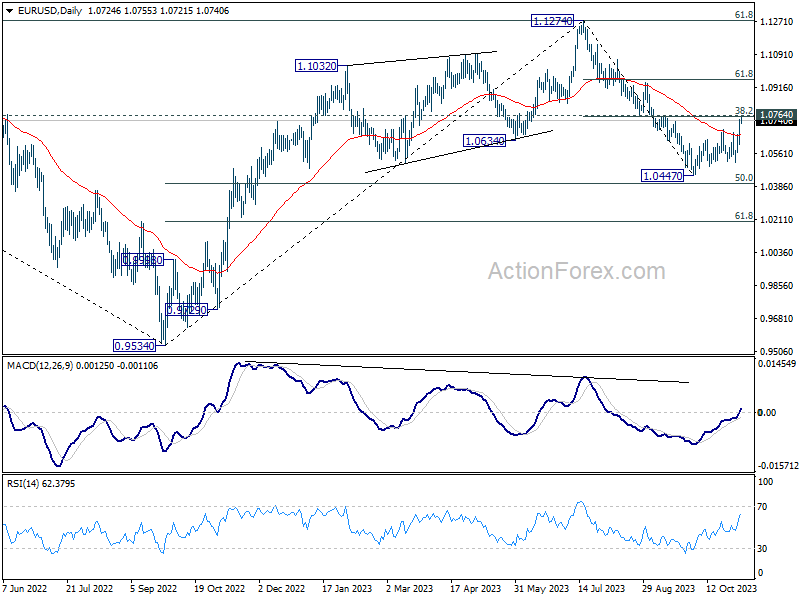

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0648; (P) 1.0698; (R1) 1.0780; More...

No change in EUR/USD's outlook and intraday bias remains on the upside. Decisive break of 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763) will extend the rise from 1.0447 to 61.8% retracement at 1.0958 next. On the downside, below 1.0666 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

European Majors Show Strength after Sentix Data, Aussie Consolidates

European majors are maintaining their upward momentum against the Dollar, leveraging last week's rally and finding additional support in the unexpectedly positive Eurozone investor confidence data. Yet, while the data provided a glimmer of positivity, the market remains guarded, unwilling to fully commit to the narrative of an economic rebound.

Meanwhile, Australian and New Zealand Dollars are surrendering some of their recent gains as traders pivot their attention to the upcoming RBA interest rate decision. With the central bank expected to hike rates, traders are holding their bets in anticipation of volatility. Yen, on the other hand, finds itself on softer footing following dovish remarks from BoJ Governor.

Across other markets, European stocks have shown signs of hesitancy, and US futures are hovering without a clear course, as investors seem to be on standby for a stronger signal. On the commodities front, Gold struggles to find direction as it lingers around the pivotal 2000 psychological resistance. Bitcoin consolidates, maintaining its position near 35k mark. Crude oil has seen a slight uplift as OPEC heavyweights Saudi Arabia and Russia reaffirm supply cuts, possibly hinting at a tighter oil market ahead.

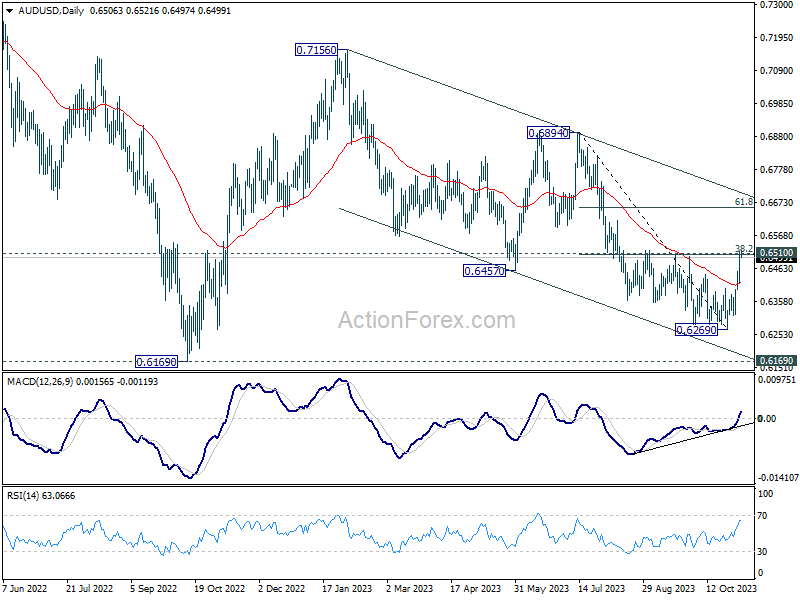

From a technical standpoint, pressing an important cluster resistance at 0.6510 (38.2% retracement of 0.6894 to 0.6269 at 0.6508). Decisive break there will raise the chance that whole down trend from 0.7156 has completed with three waves down to 0.6269. That would open up further near term rise to trend line resistance at around 6.7. However, rejection by 0.6510 will retain near term bearishness for another fall through 0.6269 at a later stage. With the RBA's rate decision on the near horizon, the currency pair's response will be telling, possibly setting the tone for its near-term direction.

In Europe, at the time of writing, FTSE is down -0.05%. DAX is down -0.19%. CAC is down -0.37%. Germany 10-year yield is up 0.0660 at 2.714. Earlier in Asia, Nikkei rose 2.37%. Hong Kong HSI rose 1.71%. China Shanghai SSE rose 0.91%. Singapore Strait Times rose 1.17%. Japan 10-year JGB yield is down -0.0419 at 0.874.

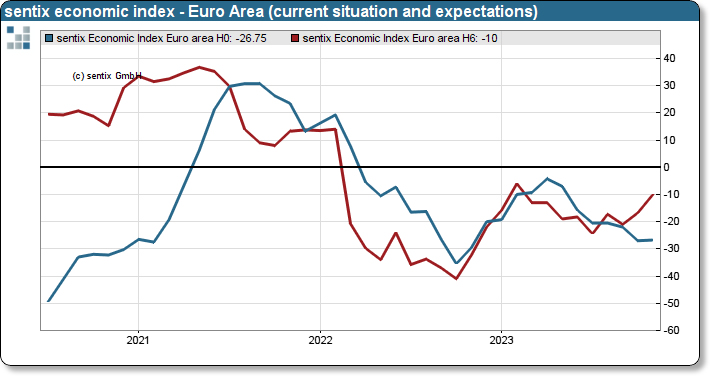

Eurozone Sentix rose to -18.6 as inflation worries ease

Eurozone's Sentix Investor Confidence Index rose from -21.90 to -18.6 in November, marking the highest level since June and surpassing analysts' expectations of -22.5.

The details of the report are also encouraging, with Current Situation Index marginally improving from -27.0 to -26.8. Expectations Index leaped towards optimism, reaching the highest point since February at -10.0, up from -16.8.

However, it is critical to acknowledge that expectations remain in negative terrain. "The decrease in negative momentum is an initial sign of improvement," according to the Sentix report, "but the all-clear can only be given if expectations turn positive."O

ne notable development is the rise in the Sentix "Inflation" theme index, which has crossed into positive territory for the first time since early 2020, suggesting that inflation may be diminishing as a key concern. The index now stands at +6.5 points, a development that could potentially reduce ECB's urgency to act.

Eurozone PMI services finalized at 47.8, stagflation concerns mount

Eurozone PMI Services slumped to 47.8 (final reading) from September's 48.7. PMI Composite index, which tracks both manufacturing and services, descended to a 35-month low of 46.5 from 47.2. The rate at which new business is falling has reached levels not seen since 2012, with the exception of the pandemic period.

This downturn is evident across key Eurozone economies, with member states reporting troubling metrics. Spain hit a 2-month low at the brink of stagnation with PMI Composite of 50.0, while Ireland descended to an 11-month low at 49.7. Italy and Germany both reported figures suggesting continuing contraction in service sector activity, with PMIs at 47.0 and 45.9 respectively. France, although at a 2-month high, still sits in a contractionary phase at 44.6.

Cyrus de la Rubia of HCOB offers a stark analysis: "The Eurozone service sector appears to be struggling at the onset of Q4, continuing a three-month trend of decline. A steep decrease in new business intake is a worrying harbinger for future activity. Although there is a slight uptick in future expectations, they still linger well below the historical average."

The economic situation seems paradoxical, with prices rising without the typical accompanying demand, pointing to a condition of "stagflation". De la Rubia questions how long this "odd stagflation zone" will persist, a query that also plagues ECB. With PMI data suggesting no quick exit from these conditions, it appears ECB is not in a position to lower interest rates just yet, as it balances the dual threats of sluggish growth and persistent inflation.

BoJ Governor Ueda affirms commitment to easing amid uncertain inflation-wage dynamics

BoJ Governor Kazuo Ueda reaffirmed today the central bank's commitment to its accommodative stance.

"We're seeing more positive signs than before in corporate wage and price-setting behavior," Ueda stated, acknowledging the nascent signs of a healthier inflation-wage cycle. However, he also underscored the prevailing uncertainties, admitting, "there's still uncertainty on whether the positive cycle will strengthen, as we predict."

With an eye on supporting economic activity, Ueda emphasized the central bank's resolve, "We will patiently maintain monetary easing," indicating no immediate shift from BoJ's long-standing dovish position.

Last week's decision to relax the 1% cap on 10-year JGB yield, allowing greater movement in long-term borrowing costs, was a nod to flexibility in BoJ's approach. Today, Ueda elaborated, "We will conduct nimble market operations when interest rates rise, depending on the level and speed of moves of long-term rates."

Ueda also sought to temper market expectations regarding the potential for sharp rises in long-term yields. "Even if long-term rates come under upward pressure, don't expect the 10-year JGB yield to sharply exceed 1%," he stated.

The Governor's comments reflect a deep consideration of the "real" interest rate, which factors in inflation expectations. He explained, "Long-term rates may rise somewhat but what's important is to look at the real interest rate that takes into account inflation expectations."

He reassured markets, "Even if long-term rates rise, real interest rates will move in negative territory so monetary conditions will be sufficiently accommodative."

Japan's PMI services finalized at 51.6, growth is on the wane

Japan's PMI Services was finalized at 51.6 in October, down from previous month's 53.8. PMI Composite figure similarly declined to 50.5 from September's 52.1.

Andrew Harker of S&P Global Market Intelligence highlighted the subdued performance: "While the PMI data continue to make positive reading for the Japanese service sector, the recent trends suggest that growth is on the wane."

He elaborates that the slowdown is notably marked by the softest increases in activity and new orders witnessed since the year's inception, which could herald a persistent deceleration as we edge closer to the year's end.

This softening expansion has raised concerns regarding the service sector's capacity to buoy the broader economy, particularly as manufacturing continues to lag. Harker notes the stagnation of new orders in October, halting an eight-month stretch of growth and presenting a cautionary backdrop for the upcoming months.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0648; (P) 1.0698; (R1) 1.0780; More...

No change in EUR/USD's outlook and intraday bias remains on the upside. Decisive break of 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763) will extend the rise from 1.0447 to 61.8% retracement at 1.0958 next. On the downside, below 1.0666 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | ||||

| 00:00 | AUD | TD Securities Inflation M/M Oct | -0.10% | 0.00% | ||

| 07:00 | EUR | Germany Factory Orders M/M Sep | 0.20% | -1.40% | 3.90% | 1.90% |

| 08:45 | EUR | Italy Services PMI Oct | 47.7 | 48.5 | 49.9 | |

| 08:50 | EUR | France Services PMI Oct | 45.2 | 46.1 | 46.1 | |

| 08:55 | EUR | Germany Services PMI Oct | 48.2 | 48 | 48 | |

| 09:00 | EUR | Eurozone Services PMI Oct | 47.8 | 47.8 | 47.8 | |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Nov | -18.6 | -22.5 | -21.9 | |

| 09:30 | GBP | Construction PMI Oct | 45.6 | 46.2 | 45 | |

| 15:00 | CAD | Ivey PMI Oct | 54 | 53.1 |

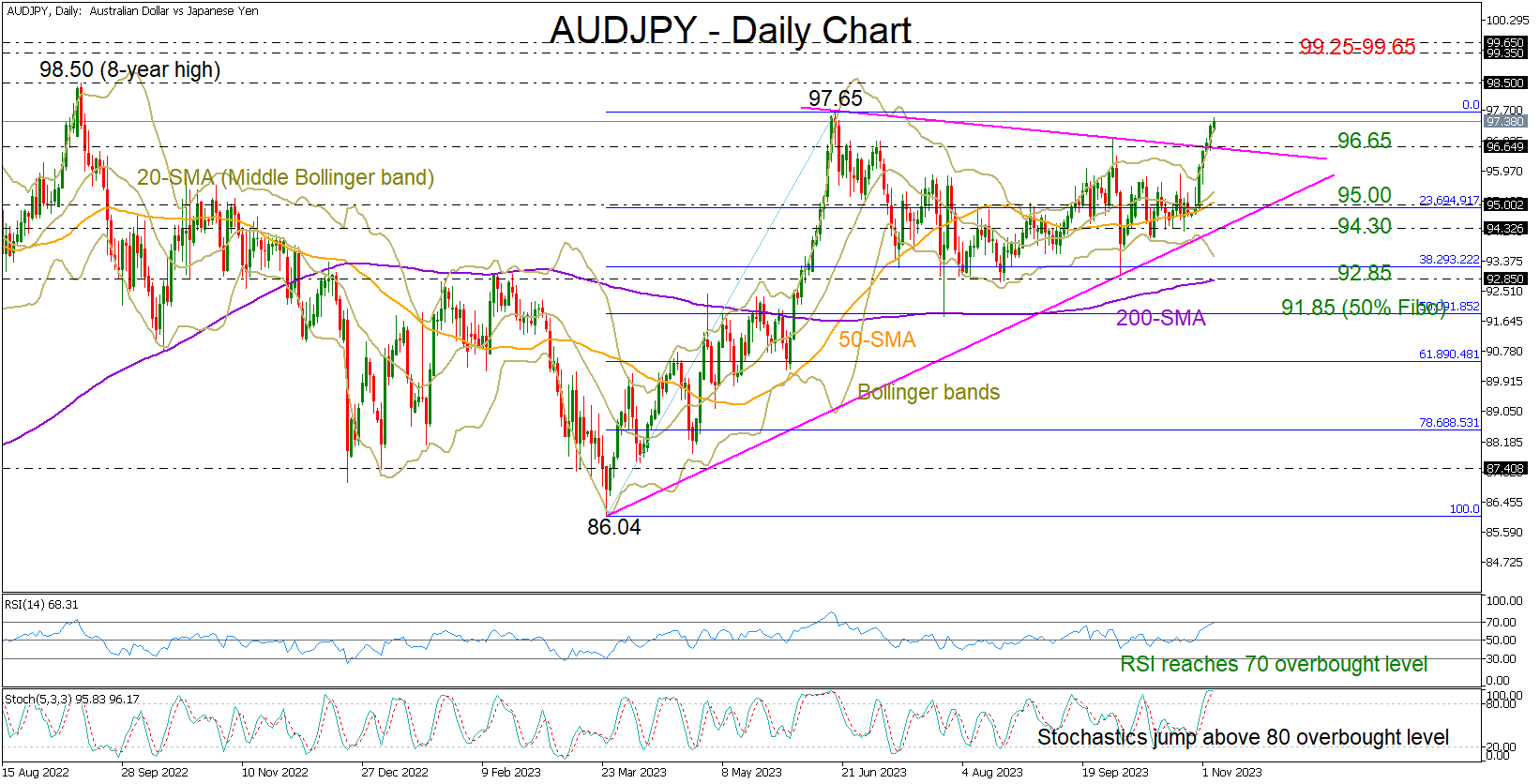

AUDJPY in Overbought Waters; RBA Rate Decision Looms

- AUDJPY enjoys fastest weekly growth since June

- Risk skewed to the upside, but gains could be limited

- RBA policy announcement due on Tuesday at 03:30 GMT

AUDJPY has turned its eyes back to June’s peak of 97.65 after a constructive week of strong gains.

The RSI and the stochastic oscillator are warning that the latest rapid upturn may not be durable, as the indicators are already testing their overbought levels. Note that the price has been constantly closing above the upper Bollinger band over the past few days. Yet, if it manages to stay above 96.65, the bulls might attempt to crawl up to the 2022 top of 98.50. Even higher, the next stop could be within the constraining zone of 99.25-99.65.

Should the price tumble below 96.65, it may find support somewhere between its simple moving averages (SMAs) and the tentative ascending line at 94.30. The 23.6% Fibonacci retracement of the 84.06-97.65 upleg is within the same region. Hence, a close lower could motivate more selling, likely bringing the 92.85 floor and the 200-day SMA under examination. If that proves fragile too, the pair may slide to 91.85.

In brief, AUDJPY seems to be at risk of a bearish correction, but any downside movements could appear limited if it manages to set a strong footing around 96.65.

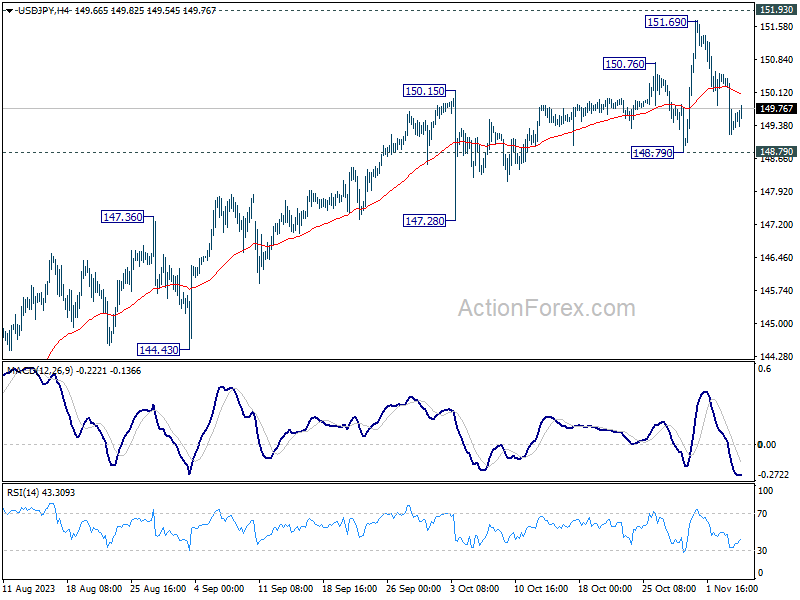

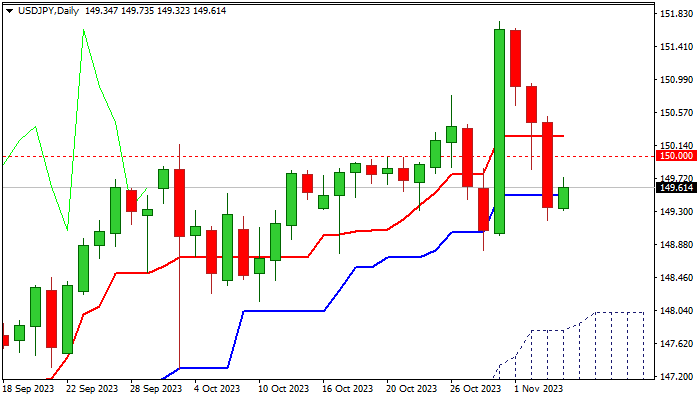

USD/JPY: Remains Biased Lower But Fresh Bearish Signals Need Further Confirmation

USDJPY is consolidating after a three-day pullback from new multi-month high (151.72) resulted in another failure to register weekly close above psychological 150 barrier (basically the pair last time closed the week above 150 level in September 1990).

This points to the strength of 150 resistance and also to strong headwinds that larger bears face here, mainly due to persisting fears that firm break higher would spark intervention by Japanese authorities.

Technical picture on daily chart is weakening as the latest pullback broke and closed below daily Tenkan-sen / Kijun-sen (requires another close below Kijun-sen to verify signal) and 14-momentum broke into negative territory.

This warns of further weakness, although fresh bears need to clear another pivotal supports at 148.80 (Oct 30 higher low) and 148.42 (rising 55DMA) to confirm top and spark fresh acceleration lower and test of next strong support at 147.88 (top of rising and thick daily Ichimoku cloud).

Near-term bias is expected to remain with bears while the price action stays under daily Tenkan-sen (150.26).

On the other hand, bounce and close above this barrier would sideline immediate bears, but rather for extended sideways mode than for significant gains, as the dollar remains weighed by the recent economic data and Fed’s stance, along with looming intervention.

Res: 150.00; 150.26; 150.93; 151.11.

Sup: 149.19; 148.80; 148.30; 147.88.

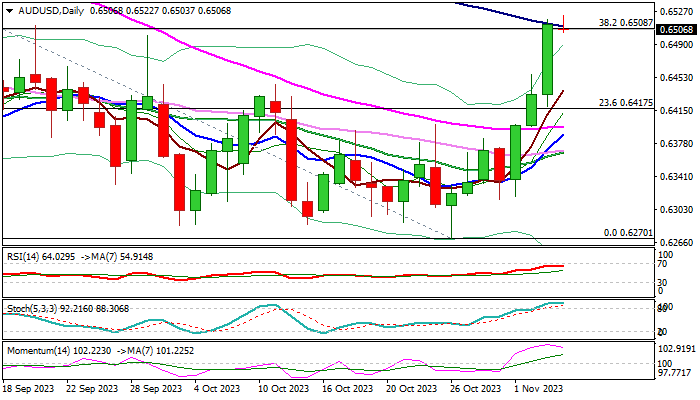

AUD/USD: Bulls Hold Grip But Look for Fresh Direction Signal from RBA’s Decision

AUDUSD remains constructive and consolidating around 0.65 level on Monday, after 2.8% surge on Friday, sparked by weaker than expected US labor data which deflated US dollar on fading prospects of further rate hikes and holding high borrowing cost for longer period.

The pair closed marginally above 0.65 barrier on Friday, registering the first weekly close above this level since late May (0.65 also marks Fibo 38.2% retracement of 0.6894/0.6270 bear-leg and is reinforced by falling 100DMA which adds to significance of the barrier).

Daily technical studies are improving, but near-term action needs firm break above 0.6500 zone to confirm signal and spark fresh acceleration higher, targeting 0.6582/89 (50% retracement / daily cloud top) and 0.6617 (200DMA) in extension.

Overbought conditions suggest that bulls may take a breather and consolidate ahead of key event – RBA policy meeting-due early Tuesday.

Aussie dollar may rise further as markets widely expect the central bank to deliver another 25 basis points hike, though the focus will be on the post-meeting statement which needs to be hawkish to confirm signal.

Conversely, dovish hike or decision to stay on hold would sour the sentiment and deflate Australian currency.

Res: 0.6521; 0.6589; 0.6617; 0.6696.

Sup: 0.6490; 0.6445; 0.6417; 0.6397.

S&P 500 Analysis: Best Week of the Year, Despite Bad News from Labour Market

According to Friday's data, in the US:

→ the unemployment rate rose to 3.9% (expected = 3.8%). The last time the level was this high was in February 2022.

→ the number of workers employed in the non-agricultural sector increased over the month by only 150k (+178k expected). The last time the figure was below 150k was in February 2021.

Published negative data clearly indicate a cooling of the labour market. Why then did the E-mini S&P-500 futures price end the week up about 5.5%, marking the best week of 2023?

The point is that market participants are increasingly convinced that the Fed will no longer tighten monetary policy. That is, interest rates have peaked, the next step should be to ease them, which will allow companies to grow.

The 4-hour chart of the S&P 500 shows that the index price:

→ has reached the upper border of the descending channel, above which there is a resistance line from the October highs;

→ the RSI indicates severe overbought.

That is, the market is in a vulnerable position for the formation of a rollback from current price levels. If the price goes into a pullback, it will be an important test for the current positive interpretations of statistical data — is rising unemployment really a good thing for the stock market?

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

US Economic Conundrum: Will Rising Interest Rates Affect Spending or the Job Market First?

It is a classic economic puzzle akin to the chicken-and-egg dilemma: as interest rates reach their highest levels in over two decades, which vital component of the economy will give way first—spending or employment?

When consumers tighten their purse strings, businesses experience a drop in revenue, and this, in turn, can lead to layoffs as profits dwindle. Conversely, when companies reduce their workforce, individuals find themselves with less money to spend. It is a delicate dance, and the intricacies of this relationship remain a subject of much debate among economists.

For now, it appears that spending remains robust, and businesses continue their hiring spree. The key question is why? Some contend that the robust job market is driving consumer spending, while others argue that strong consumer demand enables employers to maintain a solid hiring pace.

Consumer spending plays a pivotal role in the US economic landscape, contributing to approximately 70% of the nation's economic output. Consequently, it acts as a litmus test for the overall health and trajectory of the American economy.

Determining which will weaken first—spending or hiring—entails consideration of various nuances. Factors such as the lingering effects of pandemic-era savings, varying degrees of pent-up demand for specific goods and services, and the ever-evolving economic landscape across different business cycles all come into play.

Although the US labour market's meteoric rise in 2021 and 2022 has slowed, it remains robust. In recent months, it has exhibited signs of cooling, as underscored by the latest jobs report released on a recent Friday.

The report indicated the addition of 150,000 jobs in the previous month, slightly below expectations but still a notable increase in employment opportunities. While October's job growth may have lagged behind the previous month's performance, it comfortably exceeded the minimum job gain required to match population growth—estimated to be between 70,000 and 100,000. Unemployment rates remain low, and job vacancies are at historically high levels.

A moderation in the labour market's growth trajectory can result in income deceleration and diminished consumer confidence in their employment prospects. This tends to affect consumer spending and may ultimately lead to layoffs.

However, a counter argument posits that there have been instances in which spending faltered before the job market.

A prime example is the housing market crash of 2008, which precipitated the Great Recession and, in turn, led to a slump in consumer spending.

Indicative pricing only

The performance of the EURUSD pair has been notably intriguing in recent days. The euro has made significant gains against the US dollar, with a notable surge occurring during Friday's trading session.

As interest rates continue to shape the economic landscape, the outcome of the spending versus employment dilemma remains an issue that economists, policymakers, and market participants will closely monitor.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Eurozone Sentix rose to -18.6 as inflation worries ease

Eurozone's Sentix Investor Confidence Index rose from -21.90 to -18.6 in November, marking the highest level since June and surpassing analysts' expectations of -22.5.

The details of the report are also encouraging, with Current Situation Index marginally improving from -27.0 to -26.8. Expectations Index leaped towards optimism, reaching the highest point since February at -10.0, up from -16.8.

However, it is critical to acknowledge that expectations remain in negative terrain. "The decrease in negative momentum is an initial sign of improvement," according to the Sentix report, "but the all-clear can only be given if expectations turn positive."O

ne notable development is the rise in the Sentix "Inflation" theme index, which has crossed into positive territory for the first time since early 2020, suggesting that inflation may be diminishing as a key concern. The index now stands at +6.5 points, a development that could potentially reduce ECB's urgency to act.