Sample Category Title

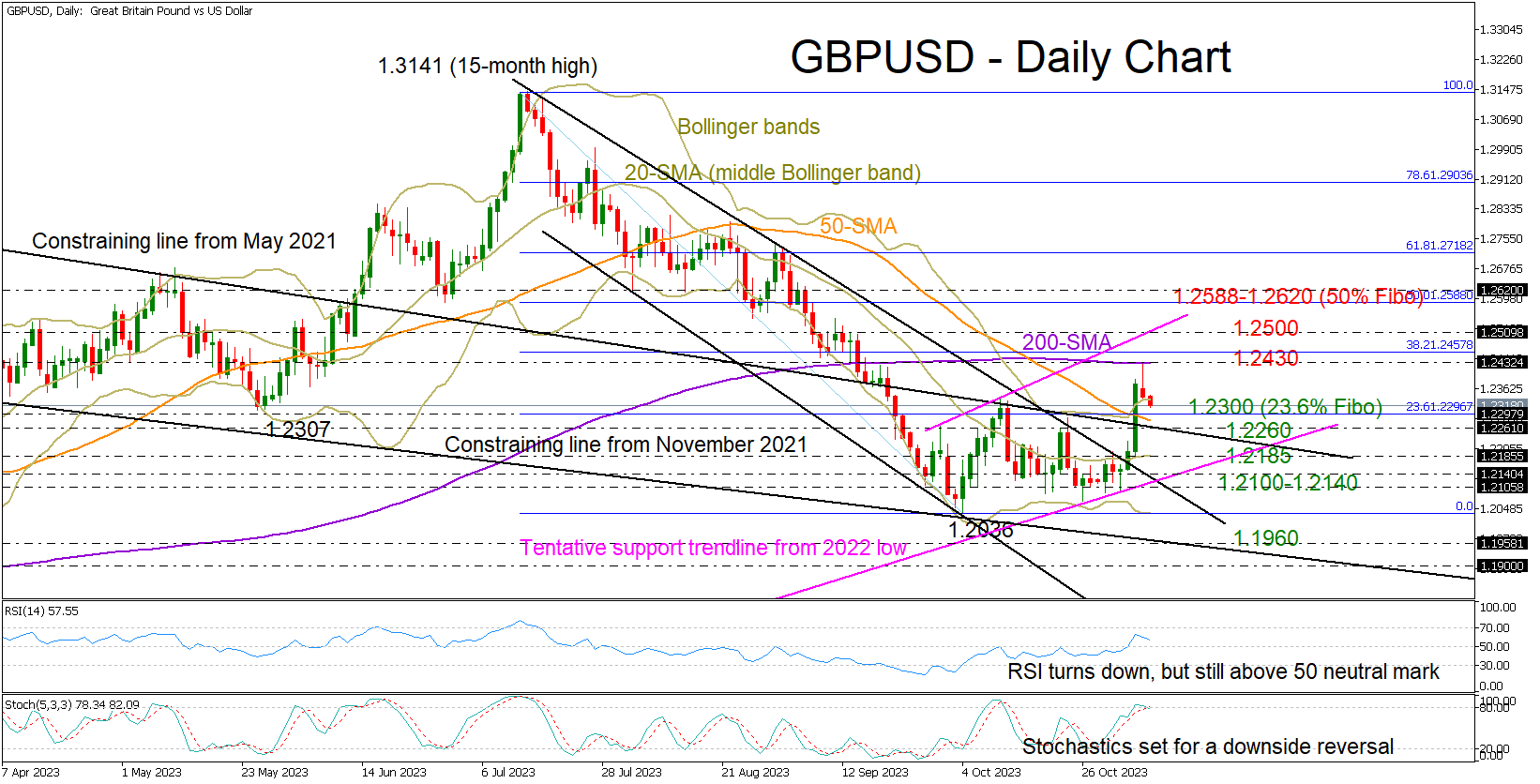

Did GBPUSD Get Caught in a False Breakout?

- GBPUSD trims gains after rejection from 200-SMA

- Buying appetite falls; support at 1.2260-1.2300

GBPUSD could not find enough buyers to expand Friday’ bull run above its 200-day simple moving average (SMA), closing with marginal losses within the 1.2300 area on Monday.

Given the current negative momentum in the price, the question now is whether the pair will stay resilient above the 1.2260-1.2300 key region. A clear step below it and beneath the 50-day SMA would wipe out Friday’s boost, pressing the price back to the 20-day SMA. Slightly lower, the tentative ascending line from the 2022 low at 1.2140 and the upper band of the broken bearish channel at 1.2100 could prevent a drop towards October’s low of 1.2036. If not, the sell-off might stretch towards the falling support line from November 2021 at 1.1960.

Technically, the short-term risk is leaning to the downside. The price has closed above the upper Bollinger band, while the stochastic oscillator seems to have peaked above its 80 overbought level, both suggesting that the latest spike in the price is overdone.

Nevertheless, the RSI is still some distance above its 50 neutral mark, raising speculation that the bulls still have the power to stage a rebound. In this case, traders will wait for a close above the 200-day SMA at 1.2430, and more importantly, beyond the 1.2500 mark to upgrade their outlook. Then, the next battle could take place somewhere between the 50% Fibonacci retracement of the previous downleg at 1.2588 and the 1.2620 barrier.

To sum up, the latest spike in GBPUSD has not excited traders yet. An extension above the 200-day SMA and the 1.2500 number is still required to make the upturn look more credible. Note that the death cross between the 50- and 200-day SMAs is intact.

Asian Markets Return to Risk-off Mode

Markets

The new trading week yesterday started with a countermove on last week’s overall easing in financial conditions. Maybe the market has been running a bit ahead of itself in declaring an end to the Fed’s tightening cycle or at least it was too early to pencil in rate cuts before the summer of next year. Contrary to what was the case last week, there was little economic news to ‘explain’ the move. Technical levels probably played a role, with US yields end last week testing key support levels (e.g. 4.50% for the 10-y). Upcoming supply maybe also was a good reason for investors to turn more cautious to further rush into bonds (US Treasury refinancing starting today). Whatever the driver, US yields yesterday rebounded between 9.6 bps (2-y) and 4.2 bps (30-y). At 4.635%, the 10-y US yield again created some breathing space compared to the 4.50% reference. Overnight, Minneapolis Fed governor Kashkari joined yesterday’s market mood as he warned that it’s too soon to declare victory on inflation. More data are needed to be sure that ‘the inflation genie’ is back in the bottle, he assessed. EMU/German yields followed the broader rise but as was the case on Friday, the curve move again was a bit different from the US (bear steepening, 2-y +6.2 bps; 10-y +9.4 bps). ECB’s Holzmann, admittedly a notable hawk, came with a similar conclusion as did Kashkari (not declaring victory yet). Doubts on the room for early (Fed) easing also blocked that rebound in equities. US indices finished with limited gains (Dow +0.1%, Nasdaq +0.3%). First key resistance levels (Dow 34148, S&P 4394, Nasdaq 13714) are under test or within reach, but not recovered yet. This also applies for the Eurostoxx50 (+0.38%, ST top at 4.234). Oil ($ 85 p/b) hardly gained even as Russia and Saudi Arabia extended production cuts. The dollar halted Friday’s sell-off, but its performance remained unconvincing (DXY 105.21 from 105.02, EUR/USD 1.0718 from 1.073). Sterling underperformed both the dollar (cable close 1.2344) and the euro (EUR/GBP close 0.8682).

This morning, Asian markets return to risk-off mode. China October trade data show a mixed picture exports (USD -6.4% Y/Y) disappointed. Imports rose more than expected (+6.4%Y/Y). US Treasuries gain marginally as does the dollar (DXY 105.4). Later today, eco data (US trade balance, German production) probably won’t have a lasting impact on trading. Interest rate markets will keep a close eye at the $ 48 bln sale of 3-y Treasury Notes. Still, technical trading might again prevail. On interest rate markets, yesterday’s price action suggests that a sustained decline below last week’s lows won’t be that evident. On FX markets we look out whether the dollar will be able to profit more from a global risk-off than was the case of late. Sterling (EUR/GBP 0.868) this morning hardly reacts to mediocre BRC October retail sales (+2.5% Y/Y from 2.8%).

News & Views

The Reserve Bank of Australia hiked its policy rate by 25 bps to 4.35%, interrupting a four-meeting pause during which it judged that higher interest rates were balancing the economy and that some tightening impact was yet to be felt. Today, however, it concluded that the progress in CPI declining towards target is slower than in the August forecasts expected. The latest reading “indicates that while goods price inflation has eased further, the prices of many services are continuing to rise briskly.” Inflation is seen at around 3.5% by end 2024 and at the top of the 2-3% target by end 2025. The risk of inflation (expectations) being higher for longer against the background of a stronger than expected economy and still tight labour market thus warranted another rate increase. The RBA said uncertainties around the outlook are significant and often two-sided. Further tightening in such circumstances will depend upon the data and the evolving assessment of risks, it said. The Australian dollar’s attempt to rise on the not fully discounted rate hike was shortlived. After touching AUD/USD 0.65, the pair turned south to trade around 0.648 currently. Australian government bond yields ease 2.9-3.3 bps.

The Fed’s Q3 Senior Loan Officer Opinion Survey (SLOOS) yesterday showed how lending standards tightening across all kinds of loans. In the business segment, survey respondents reported tighter standards and weaker demand for commercial and industrial loans to firms of all sizes. Tighter standards and weaker demand also prevailed for all commercial real estate loan categories. Consumer lending tightened and demand weakened across all categories of residential real estate. The same applied for credit card, auto and other consumer loans.

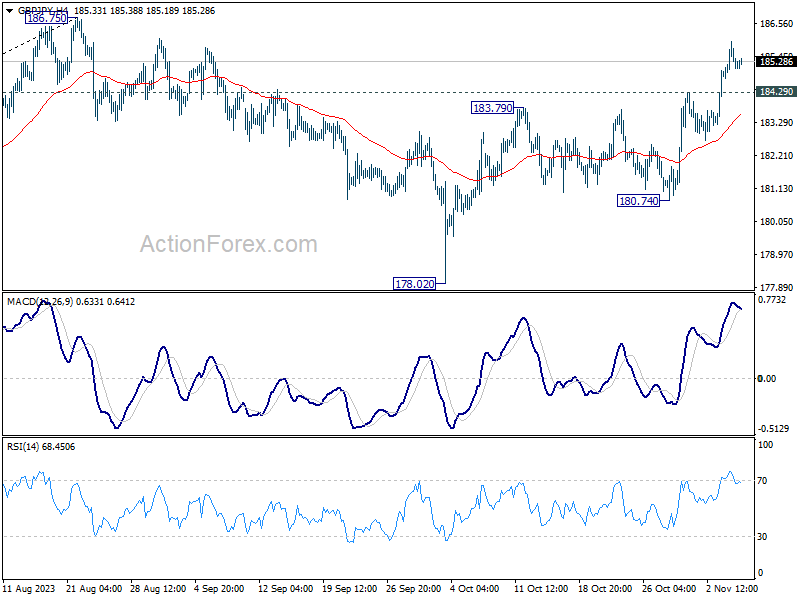

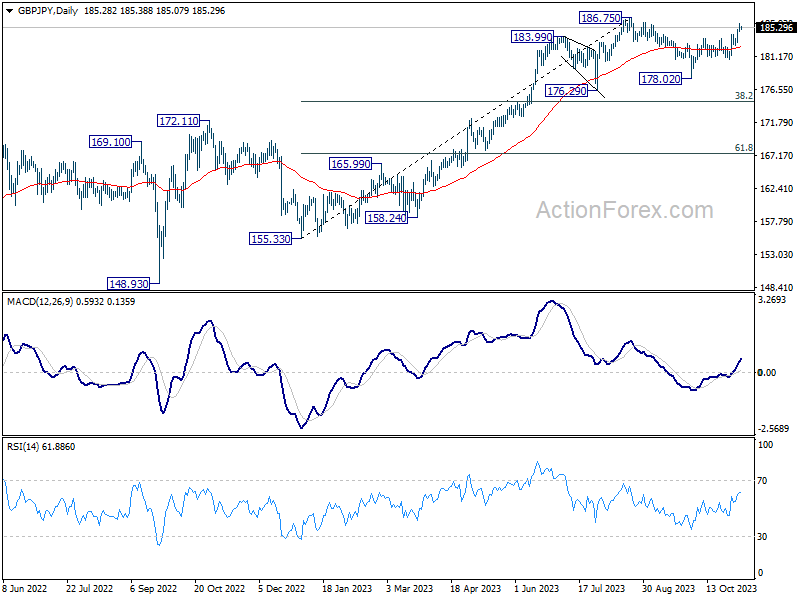

GBP/JPY Daily Outlook

Daily Pivots: (S1) 184.66; (P) 185.32; (R1) 185.90; More...

Intraday bias in GBP/JPY remains on the upside for the moment. Current rise from 178.02 should target a retest of 186.76 resistance. Decisive break there will resume larger up trend. On the downside, below 184.29 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, as long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and bring lengthier and deeper consolidations.

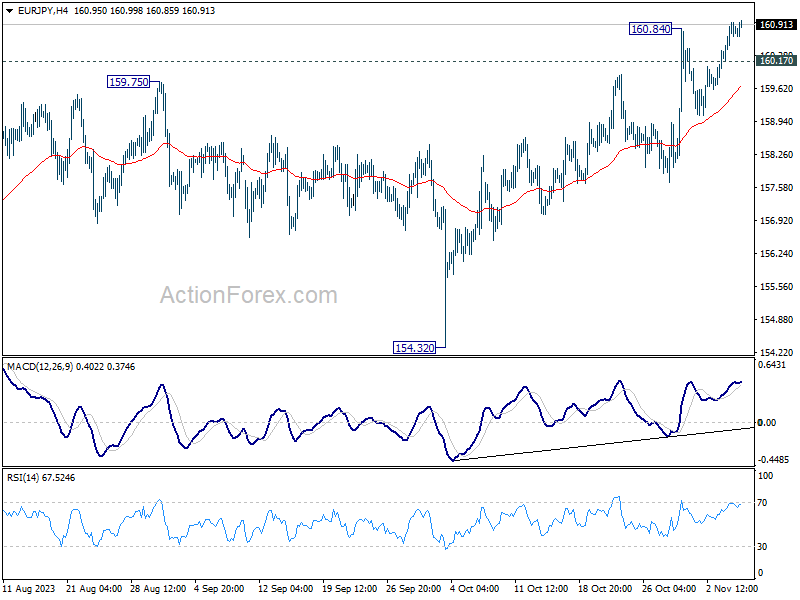

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.32; (P) 160.65; (R1) 161.17; More....

Break of 160.84 resistance indicates resumption of larger up trend in EUR/JPY. Intraday bias is back on the upside for 163.06 projection level next. On the downside, break of 160.17 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 139.05 at 163.06. On the downside, break of 154.32 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish even in case of deep pullback.

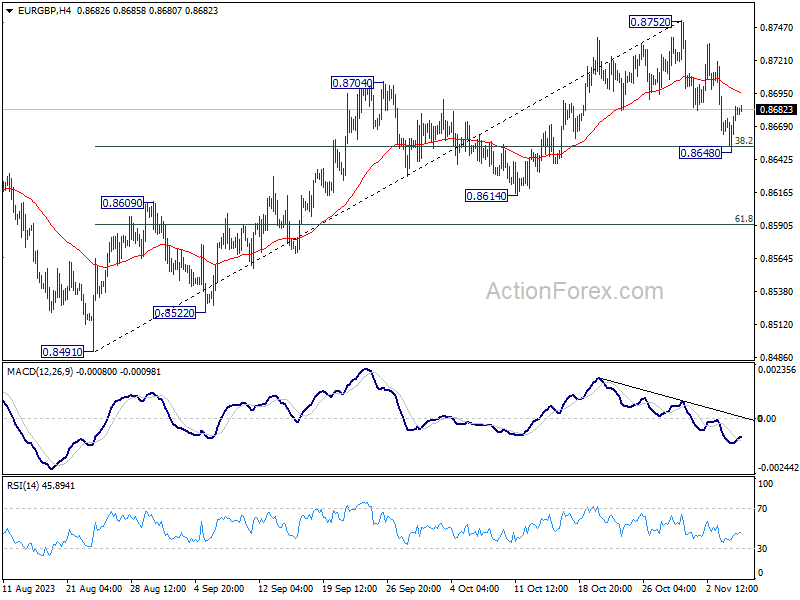

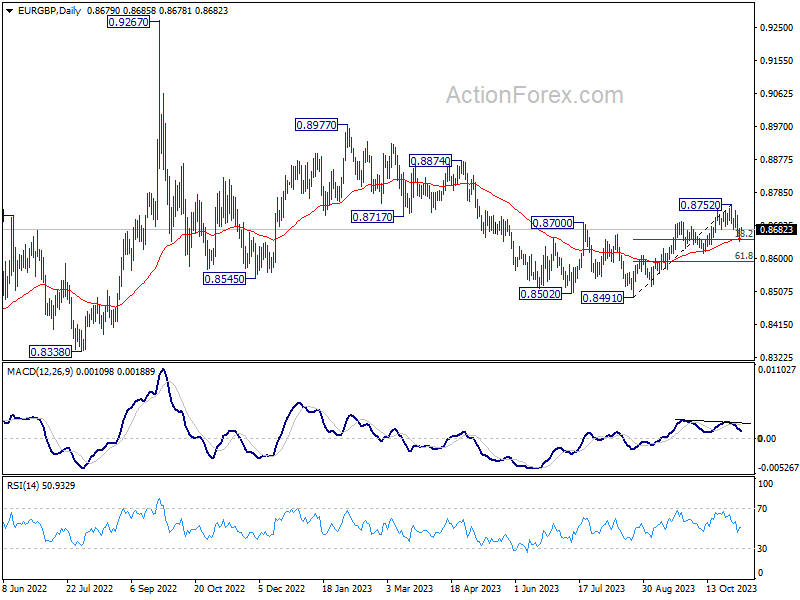

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8659; (P) 0.8673; (R1) 0.8696; More....

EUIR/GBP recovered after drawing support from 38.2% retracement of 0.8491 to 0.8752 at 0.8652 and intraday bias is turned neutral first. Pull back from 0.8752 could still extend lower, but downside should be contained by 0.8614 support to bring rebound. Break of 0.8752 resistance to resume the rally from 0.8491 is expected at a later stage.

In the bigger picture, current development suggests that whole down trend from 0.9267 (2022 high) has completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. This will remain the favored case as long as 0.8614 support holds.

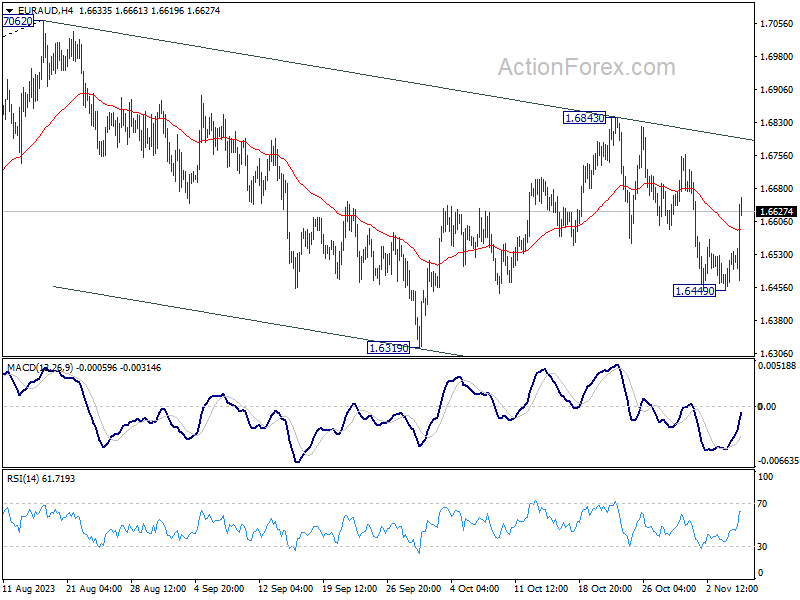

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6450; (P) 1.6492; (R1) 1.6518; More...

Intraday bias in EUR/AUD is turned neutral first with current recovery. On the downside, break of 1.6449 will target 1.6319 support first. Firm break there will resume the whole decline from 1.7062. However, above 1.6843 will resume the rebound from 1.6319 towards 1.7062 resistance instead.

In the bigger picture, current development suggests that 1.7062 is already a medium term top. Fall from there is seen as a correction to the up trend from 1.4281 (2022 low). While deeper decline might be seen, strong support should emerge from 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to contain downside. However, sustained break of 1.6000 will raise the chance of bearish tend reversal.

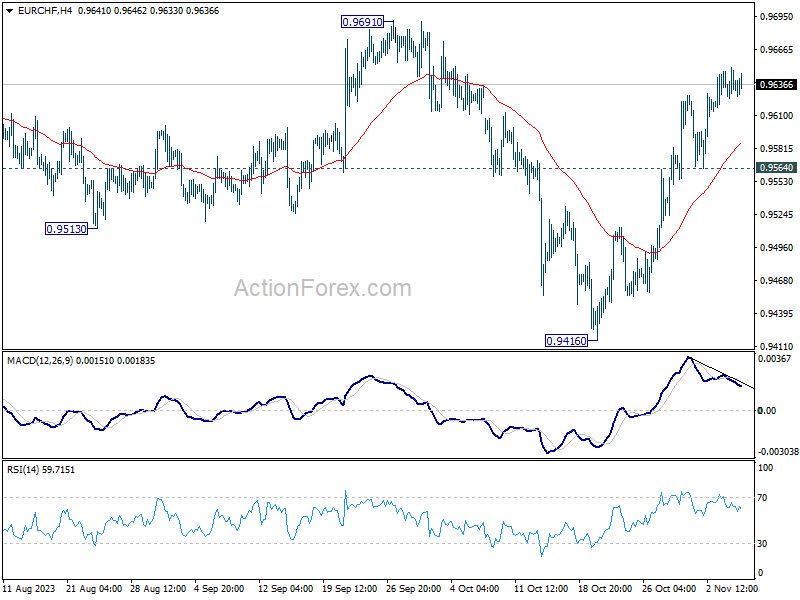

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9626; (P) 0.9639; (R1) 0.9653; More...

While EUR/CHF is losing upside momentum as seen in 4H MACD, further rise is still expected with 0.9564 support holds. Current rebound from 0.9416 should target 0.9691 resistance first. Firm break there will argue that whole decline from 1.0095 has completed at 0.9416, just ahead of 0.9407 support (2022 low). Further rally would be seen to 0.9840 resistance.

In the bigger picture, as long as 1.0095 resistance holds, price actions from 0.9407 are viewed as a three-wave consolidation pattern first. Current rise from 0.9416 might be the third leg. That is, larger down trend from 1.2004 (2018 high) might still resume through 0.9407 at a later stage. However, decisive break of 1.0095 will argue that the long term down trend is reversing.

AUD/USD Technical: RBA Hike Already Priced In, Minor Corrective Decline in Progress

- RBA hiked the official cash rate by 25 bps to 4.35% as expected.

- Revised up slightly projected year-end 2024 Australia CPI inflation to be around 3.5% from 3.25% previously forecasted in August.

- AUD/USD has declined by -64 pips intraday from yesterday, 6 November high of 0.6523.

- Short-term momentum has turned bearish as depicted by the hourly RSI.

- Watch the key short-term pivotal resistance at 0.6520 on the AUD/USD with intermediate support coming in at 0.6395/6370.

On the contrary, the AUD/USD did not shape the residual push down and staged a bullish breakout from the medium-term “Descending Wedge” bullish reversal configuration as highlighted in our previous report.

The recent bullish outburst of the AUD/USD in the past week has been reinforced by an increased odd that the Australian central bank, RBA may choose to restart its interest rate hike cycle today after four consecutive pauses on its policy cash rate to maintain it at 4.1%.

Based on the pricing from the ASX 30-day interbank cash rate futures as of yesterday, 6 November, the data has implied that there is a 50% chance of a 25 basis points (bps) hike in today’s RBA’s monetary policy meeting to bring the cash rate to 4.35% due to the recent hawkish vibes from the new RBA Governor Bullock and the recent uptick in the monthly CPI number for October.

At the risk of undergoing minor pull-back after a swift up move

Fig 1: AUD/USD medium-term trend as of 7 Nov 2023 (Source: TradingView, click to enlarge chart)

Fig 2: AUD/USD minor short-term trend as of 7 Nov 2023 (Source: TradingView, click to enlarge chart)

As seen on the short-term 1-hour chart, momentum has turned bearish on the AUD/USD as depicted by the breakdown seen in the hourly RSI momentum indicator.

If the 0.6520 short-term pivotal resistance (also the minor swing high areas of 30 August/1 September 2023) is not surpassed to the upside, the AUD/USD may see a further potential minor corrective decline towards the intermediate supports of 0.6420 and 0.6395/6370 (also the 20 and 50-day moving averages & the pull-back of the former “Descending Wedge” resistance) before a new potential bullish impulsive up move sequence unfolds.

However, a clearance above 0.6520 invalidates the corrective pull-back scenario for a squeeze-up to see the next intermediate resistance coming in at 0.6595 (also the 200-day moving average) in the first step.

RBA Board Has Responded to Material Increase in Inflation Outlook

As we expected, the RBA Board raised the cash rate target by ¼ percentage point to 4.35%. Their inflation outlook is stronger, and so is their outlook for the labour market. But follow-up increases in rates are far from assured.

At its November meeting, the RBA Board raised the cash rate target by ¼ percentage point to 4.35%. This is a break from the run of meetings where it was comfortable to hold steady and monitor the evolving situation. Given its low tolerance for upside surprises, a stronger inflation outlook and some unexpected resilience in the real economy has induced the Board to act.

As we noted last month, the CPI release for the September quarter tipped the balance in favour of raising the cash rate further. The Governor’s statement noted that inflation “is proving more persistent than expected a few months ago” and that “progress looks to be slower than earlier expected”. The considerably rewritten statement was noteworthy for the detailed explanation of what the Board had previously believed, and how things have changed since the RBA’s last forecast round in August.

Services inflation has remained sticky and there are some concerning signs in housing-related inflation and the prices of some retail goods. The Governor’s statement highlighted that many services prices “are continuing to rise briskly”. The language of the statement shows that the Board is increasingly concerned that inflation will not decline on the trajectory it is aiming for, and so it has decided to take out more insurance to achieve the desired result. That is despite the reduced risk of a price–wage spiral that the Board called out in the October minutes.

The RBA’s forecast for inflation over 2024 have been revised up, from 3.3% to 3½% now. More detail will be made available on Friday with the release of the November Statement on Monetary Policy. Our own forecasts have also been revised up over the past month. Also noteworthy is that the RBA’s unemployment forecast for end-2025 has been revised down from 4.5% to 4¼%. We will know more on Friday, but this seems like a nod to the signs of unexpected resilience in parts of the real economy.

We do not expect that the RBA will follow up with another rate increase in December. The last paragraph of the statement contained a shift in language from “Some further tightening of monetary policy may be required” used in the October media release to “Whether further tightening of monetary policy is required”. This reads as the Board hoping not to have to raise rates again, but being very willing to do so if things change. There is not enough new information between now and the December meeting to drive a change in view. Given the upgraded inflation forecasts and lower unemployment forecast, though, they are likely to have even less tolerance for upside surprises than they indicated in recent communication. So while a December move is unlikely, it is more likely that February meeting would become ‘live’ if the inflation outlook continues to lift.

Next year the RBA Board moves to a timetable of eight meetings per year, rather than the traditional eleven. This means that all meetings will follow significant data releases, including either the quarterly CPI or the national accounts. Enough new information will be able to be accumulated between each meeting that the RBA’s view of the outlook could shift. From the new year, all Board meetings should therefore be considered potentially ‘live’ in a way that was not the case in the past.

The RBA’s decision stands in contrast to the recent decisions of the FOMC, ECB and Bank of England to hold rates at their recent meetings. At a deeper level, though, all of these central banks are facing similar decisions. They have already raised policy rates a lot, and monetary policy is now restrictive in all these economies. Each central bank is watching the data unfold for signs that they need to do more. Countries such as the United States are further along the disinflation journey, just as they were earlier to experience the surge in inflation. They also would have more confidence in that the disinflation will unfold as expected. The RBA Board has not yet achieved that level of comfort.

AUD Weakens after RBA Hike, Oil Downbeat

The US bond yields rebounded, and the equity rally slowed on Monday. The US 10-year rebound from last Friday low, and the S&P500 consolidate gains near three-week highs. There are divergent opinions regarding whether last week’s risk rally is on sufficiently solid ground to extend into a Santa rally, or it would simply fade away. And it all depends on what matters the most for investors. The softening Federal Reserve (Fed) and other central bank expectations and falling sovereign yields are positive for stock valuations, but the chatter of potentially higher-for-longer rates, growing signs of slowing global economy and the rising recession odds don’t offer a bright outlook for equities into the year end. Seasonally speaking, November and December are known to be good months for the S&P500 stocks. In the past, the S&P500 stocks gained, on average, 1.8% in November and 0.9% in December. But this year, the picture is overshadowed by a lot of weak guidance and revenue warnings.

The chatter of weak demand and profit warnings are not great for equities but the worst news would be sticky inflation despite slowing growth and a persistently long period of high interest rates. For now, the Fed is perceived as being ‘done’ with interest rate hikes. But Powell is due to speak this week and he will probably leave the door open for a rate hike… otherwise he knows that all the past 1.5-year’s efforts will be instantaneously thrown out of the window with everyone rushing to US treasuries – which would pull the yields lower and loosen the financial conditions and eventually boost growth and inflation. This is something the Fed doesn’t want.

And despite a series of no rate hike news that we received over the past few weeks from major central banks including the Fed, the ECB and the BoE, the Reserve Bank of Australia (RBA) raised its rates by 25bp, as broadly expected, today. The RBA hike came as a sour reminder that there is no rule that says that a bank can’t hike rates after pausing for four meetings. Interestingly, the AUDUSD fell after the decision, along with the Australian stock markets. Today’s rate hike revived fears of economic slowdown more than appetite for higher Aussie yields – while a broad-based recovery in the US dollar and weak Chinese trade data certainly didn’t help.

Speaking of weakness

The Chinese exports which are a good gauge of global economic health, are down for the 6th consecutive month and Iranian oil exports fell for the 2nd straight month to 1.43mbpd as demand in Asia weakened. That’s certainly why we haven’t seen oil prices react to the news of escalation tensions in the Middle East and the news that Saudi and Russia will keep their oil production curbs in place during the weekend. The barrel of crude is trading a touch above the $80pb psychological mark this morning. We revise our medium-term outlook for crude oil from neutral to negative. Last week’s persistent selloff despite a broad-based risk rally, oil bulls’ unresponsiveness to normally price-positive geopolitical developments and the fact that the market focus is shifting from supply to demand side hint that a fall below the $80pb is increasingly possible, and a verbal intervention from Saudi or OPEC won’t prevent a deeper decline in the short run. Iran’s implication in the Gaza war could be a game changer but the American crude is now in the medium-term bearish consolidation zone, and will remain downbeat below $81.50, the major 38.2% Fibonacci retracement on this summer’s rally.