Sample Category Title

Could Surprise Indices Explain Market Movements?

- Surprise indices are an easy way of mapping the current state of an economy

- Our index confirms that the US economy has been losing steam the past few weeks

- Could EURUSD moves be explained by our surprise indices?

Theory states that the price of financial assets should reflect the underlying economic conditions in the respective region. While this tends to occur from a long-term perspective, a good chunk of the movements occurring in the short-term are dictated by sentiment and the impact of surprises by economic data releases.

Without aiming to steal the thunder from more established surprises indices, we created economic surprise indices for the US, the UK and Germany; the latter one is used as a proxy for the euro area. Our intention is to (a) identify the current state of economic surprises in each region, (b) compare the different regions, and (c) examine whether these indices confirm or even lead the performance of key financial assets.

We have used economic releases since 2013 and have assigned different weights to the more market-moving data. For example, the preliminary release of PMIs surveys has a greater weight in the index compared to other smaller and less market-moving business surveys. Similarly, data releases with no market forecast have the lowest possible impact on the surprise indices. It is worth noting that by surprise we refer to any economic data release significantly diverging from the economists’ forecast; thus a surprise could be positive and negative.

US, UK and German surprise indices – interesting findings

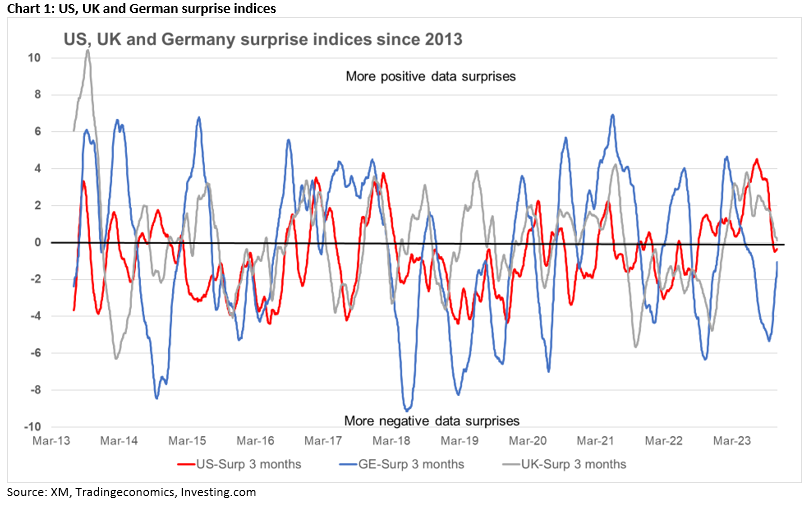

Our brand-new surprise indices, using a 3-month rolling period of economic data releases, are presented in Chart 1 below. According to our findings, only the UK index is in positive territory. This means that over the past 3 months data releases in the UK have mostly been stronger than their previous prints, and that data surprises have been more positive than negative. However, this trend appears to have changed lately, as the UK index is on a downward path with the negative surprises multiplying.

The same kind of worsening is more evident in the US surprise index. As seen in Chart 1, the US economy was at its strongest position during the summer. However, it peaked on July 17, and it has been aggressively moving lower since then. It is currently a tad below the zero line, as the recent data releases have been worsening and producing marginally more negative surprises compared to expectations.

Similarly, the German surprise index is currently hovering at a low level. However, since mid-September this index has been on an aggressive upward trend, pointing to an improvement in data releases despite the bleak short-term economic forecasts from various German think tanks.

We have to highlight the fact that economists tend to become more optimistic especially when the economy is assumed to be progressing well. This potentially gives rise to more negative surprises. This attitude is also shared by central banks when examining their forecasting record. For example, the ECB tends to produce inflation projections that show that the Bank is close to its target at the end of the forecasting window examined, despite its recent dismal record.

Euro/dollar and the surprise indices

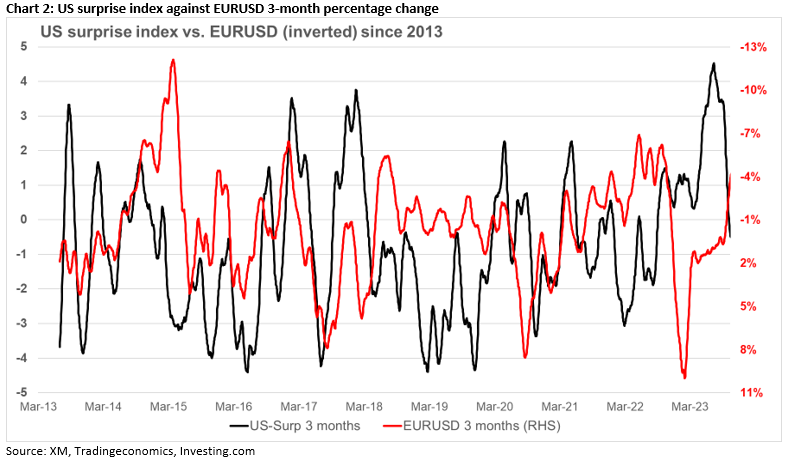

The key motivation for the creation of surprise indices is to unmask any possible correlation with key market assets. Therefore, we tried to tie up the recent trend of the surprise indices with the performance of instruments like the EURUSD. Interestingly, the progressive and significant divergence of the US and the German surprise indices over the summer, seen quite clearly in Chart 1 above, can explain to a certain degree the strong bearish move recorded in EURUSD during the July-September period. More recently, the converging US and the German surprise indices are bound to have played a role in the EURUSD upleg registered since early October.

The long-term relationship between the US surprise index and EURUSD is presented in Chart 2 below and, at times, the negative correlation tends to be rather strong. Interestingly, since the start of 2023 this correlation has been strengthening as strong US data releases fueled the sell-off in EURUSD. A growing US economy, especially when other developed economies are going through a rough patch, tends to attract global investor interest. This situation increases demand for the US dollar, as investors want to take advantage of investment opportunities. However, since early September, this relationship turned positive, potentially pointing to other factors being behind the recent EURUSD move.

S&P 500 cash index driven by the surprise indices?

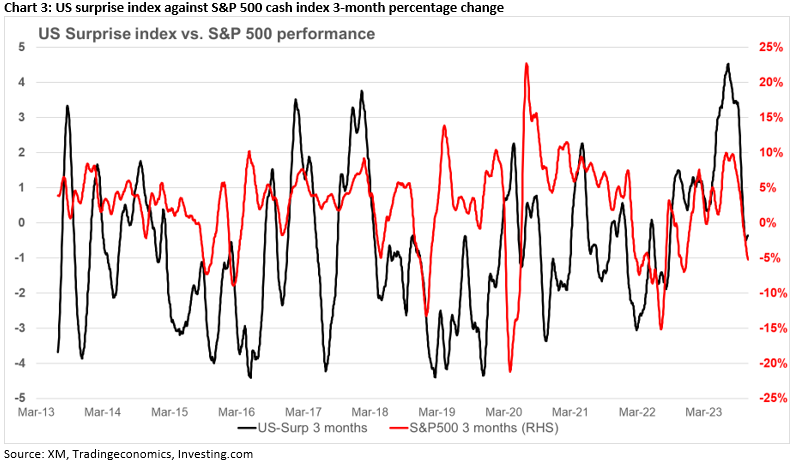

Like EURUSD, there appears to be a strong relationship between the S&P 500 cash index and the US surprise index. Since early-2023 this relationship has been getting stronger with the current correlation being very close to 1, the strongest possible positive correlation. This situation is expected as the stock market, at normal times, reflects the current economic conditions and the market participants’ expectations about the future. Therefore, we can assume that the S&P 500 rally during 2023 was fueled by consistent upside surprises in US data.

To sum up, our first attempt to create surprise indices for the three key developed economies has produced some interesting findings. The UK appears to record the best economic surprise score at this stage with Germany still hovering at negative territory and the US recently experiencing an aggressive weakening in its economic data prints. This difference between the US and the German surprise indices can explain at a great length the EURUSD performance during the until late September. Finally, in terms of equities, the US surprise index is currently very strongly positively correlated with the S&P 500 cash index.

GBPUSD Wave Analysis

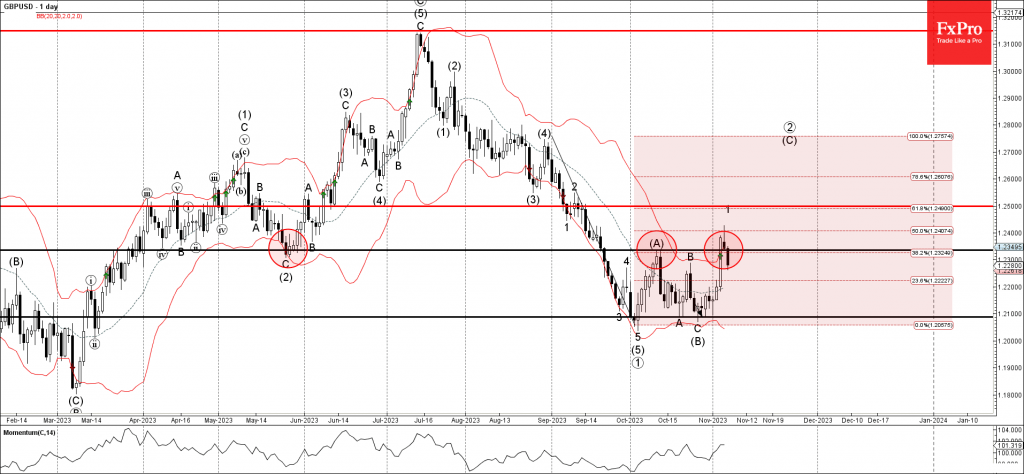

- GBPUSD reversed from key resistance level 1.2335

- Likely to fall to support level 1.2200

GBPUSD currency pair recently reversed down with the daily Shooting Star from the key resistance level 1.2335 (former strong support from May).

The resistance level 1.2335 was strengthened by the upper daily Bollinger Band and by the 50% Fibonacci correction of the downward impulse from august.

Given the strength of the resistance level 1.2335, GBPUSD can be expected to fall further toward the next support level 1.2200.

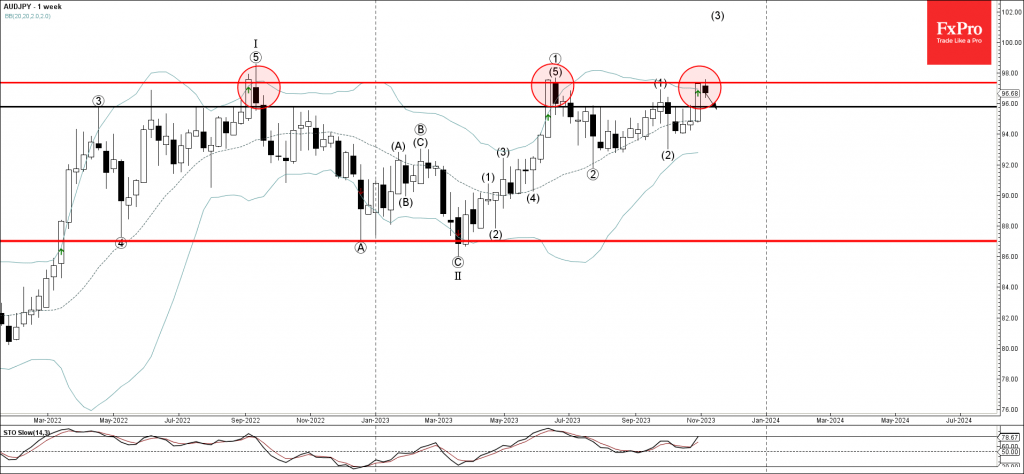

AUDJPY Wave Analysis

- AUDJPY reversed from resistance level 97.35

- Likely to fall to support level 96.00

AUDJPY currency pair recently reversed down from the major resistance level 97.35 (which has been reversing the pair from September of 2022).

The resistance level 97.35 was strengthened by the upper daily and weekly Bollinger Bands.

Given the strength of the resistance level 97.35 and the overbought daily Stochastic, AUDJPY can be expected to fall further toward the next support level 96.00.

Fed’s Goolsbee: Job market getting into better balance

Chicago Fed President Austan Goolsbee, in recent comments to CNBC, noted that the job market is "getting into better balance," a sign that the central bank's policies may be having the desired effect without tipping the economy into a sharp downturn.

The Chicago Fed head also mentioned the need for a shift in focus from the height of rate hikes to the duration for which these elevated rates might need to be maintained.

"As long as we're making progress," he remarked, "the moment of arguing how high should the rate go is going to fade to how long should we keep rates at this level as inflation is coming down."

Fed’s Kashkari sees inflation battle far from over

In a recent interview with Bloomberg TV, Minneapolis Fed President Neel Kashkari underscored Fed's commitment to reining in inflation, stressing the importance of reducing the inflation rate to Fed's target of 2% over a "reasonable period of time."

However, he also candidly expressed that the exact measures required to achieve this goal are still uncertain, as the economic response will guide future actions.

"We have to get inflation back down to 2% over a reasonable period of time," Kashkari stated, adding, "Ultimately, the economy will tell us how much is needed to get there. And I just don't know."

Kashkari's remarks come at a time when the economy is displaying resilience in the face of aggressive monetary tightening, with economic indicators not showing signs of significant weakening. "I'm not seeing a lot of evidence that the economy is weakening,"

Despite Fed's aggressive rate hikes aimed at cooling inflation, Kashkari emphasized that policymakers have not declared victory yet. The fight against inflation is ongoing, and Fed is prepared to implement additional tightening measures if they are deemed necessary.

EURUSD Sustains Strength Near Six-Week Highs

The EUR/USD currency pair remains steadfast near 1.0710 on Tuesday, maintaining proximity to the six-week highs set the previous day.

The U.S. dollar has seen a tempered performance, influenced by recent U.S. labor market statistics for October and the resultant stock market adjustments. The data pointed to pockets of weakness in the employment sector, leading investors to infer that the cooling may be an effect of tighter credit and monetary policies. Consequently, there has been a recalibration of expectations regarding the trajectory of future Federal Reserve rate hikes.

In detail, the U.S. unemployment rate edged up to 3.9%, slightly higher than the previous 3.8%. Nonfarm payrolls showed an increase of 150 thousand, which was shy of the forecasted 178 thousand. Additionally, the average wage increment was a modest 0.2% month-over-month, missing the anticipated mark.

Market sentiment now appears to lean towards the belief that the current interest rates may represent the zenith of the present monetary tightening cycle.

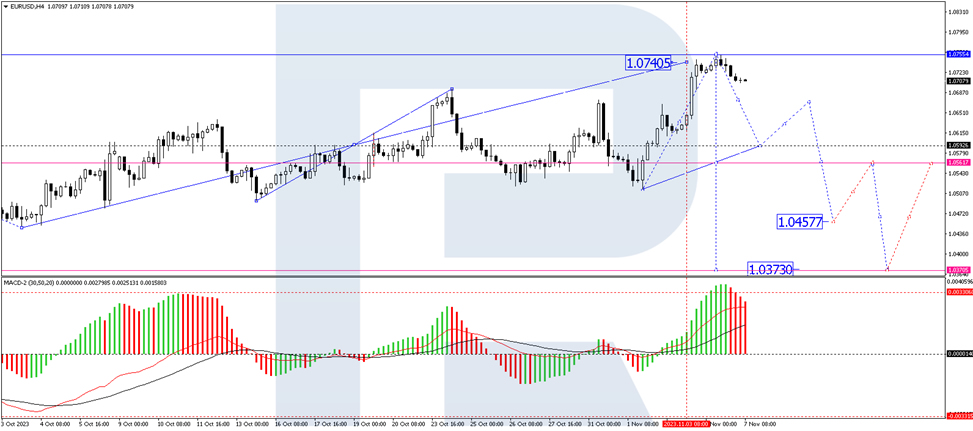

EUR/USD technical analysis

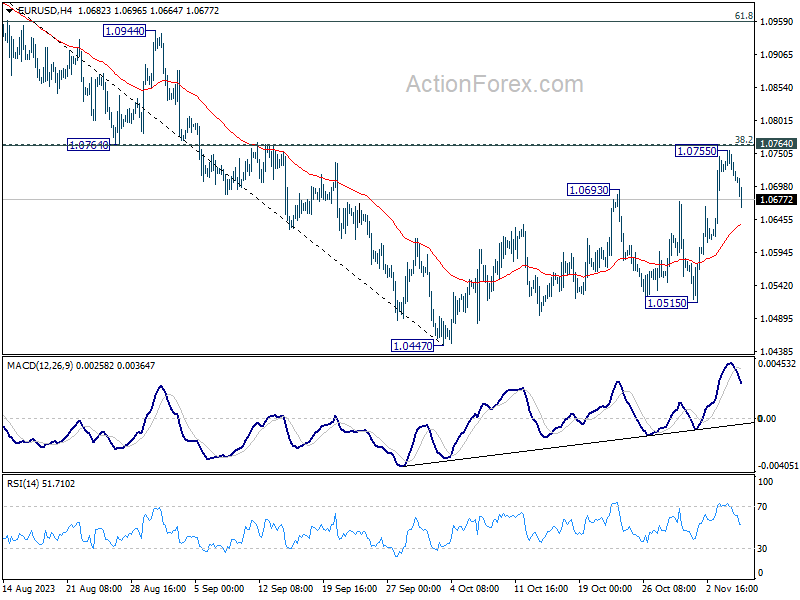

On the H4 chart for EUR/USD, the currency pair has attained the correctional target at 1.0755. The trend now seems to be tilting downwards, with a trajectory set towards the 1.0655 level. A consolidation phase around this mark is probable. A break below this consolidation could signal a further decline to 1.0633, and potentially, should this support give way, a fall to 1.0515 could be on the horizon. The MACD indicator suggests a peak formation, with its signal line at the highs and anticipating a downturn.

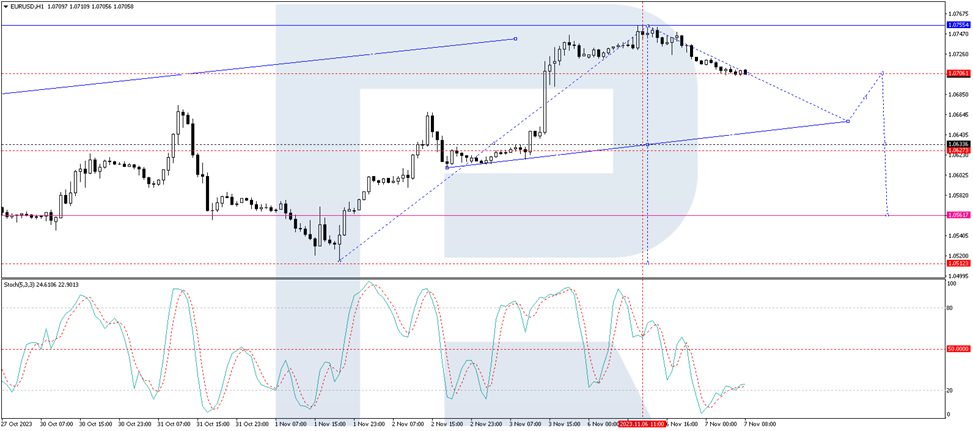

The H1 chart reveals a continuation of the downward wave targeting 1.0655. Should the pair touch this level, a corrective move upwards to around 1.0700 might ensue. Subsequent to this correction, the market may witness a renewed descent towards 1.0633. The Stochastic oscillator provides technical affirmation for this bearish outlook, with its signal line dropping below 50 and aiming for the 20 level.

Stock Markets Ease Further, RBA Hikes After Four-Meeting Hold

Stocks are trading a little lower in Europe on Tuesday and the US is shaping up for a similar open in an hour or so.

Lower bond yields enabled stocks to bounce back strongly in the second half of last week, aided by some less hawkish Fed commentary after the meeting and a softer jobs report. But with yields now stabilizing again, equities are also running low on energy and may require another boost from the data or central bank.

But Fed officials remain extremely cautious, fearing stopping too soon and suffering another onslaught of criticism for underestimating the inflationary pressures. And we're seeing that again, with Kaskari claiming it's too soon to declare victory and that doing too much is preferable to too little.

A raft of policymakers will be making appearances today and it will be interesting to see whether they take a similar approach in light of bond yields now cooling again. Policymakers can't afford to bounce between messaging depending purely on how bond yields are performing, especially when they are largely responsible for the moves, but they are clearly paying close attention to them.

RBA hikes after four-meeting hold

As they will what other central banks are doing, including the RBA which today ended a series of four rate pauses and hiked by another 25 basis points. While its decision-making is independent of the Fed's, the challenges it faces are similar, and the fact that it's needed to hike again after such a long time will only strengthen the Fed's position that it needs to maintain the higher for longer mantra, and potential for more, until the last minute.

The RBA may now refrain from warning about further hikes going forward but it will certainly leave the door ajar as it can no longer be confident that inflation won't stubbornly remain above target. As we've heard so much, the RBA is data-dependent, and future moves will be guided by it.

Oil slips further amid a weaker economic outlook

Oil prices declined again on Tuesday, with Brent now erasing the moves that followed the Hamas attack on Israel. Traders will remain on high alert for signs of a wider conflict emerging in the region that could disrupt supplies but it seems those fears are subsiding.

That we're seeing data that confirms economies are struggling under the pressure of high interest rates which are not expected to decline soon may also have contributed to oil reversing its gains. It's no surprise then that Saudi Arabia and Russia remain committed to their end-of-year cuts, it's just a question of whether they will be extended. That they haven't already perhaps suggests there's some reluctance too, which may also be weighing on prices a little.

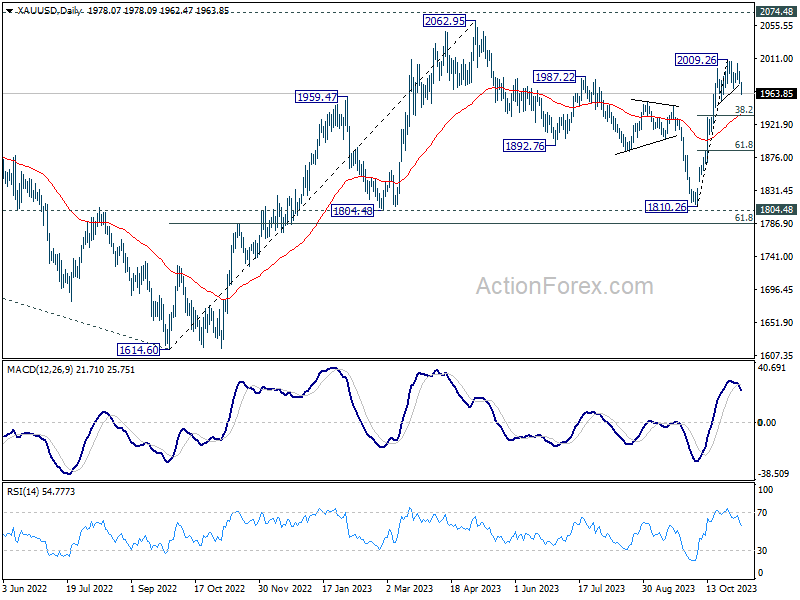

Gold struggles after repeated fails to hold above $2,000

Gold has broken lower today, appearing to enter into a correction phase after failing to significantly break above $2,000 on a number of occasions. Perhaps we're seeing an unwind of some of the geopolitical risk in the markets or just a technical correction in the rally over the last month but the last couple of sessions haven't been great.

It will be interesting to see how gold trades around $1,940 if it reaches that far as this roughly coincides with prior resistance, the 38.2% retracement of the previously mentioned rally, and the 200-day simple moving average.

Dollar Gains as Risk Aversion Spreads, Market Seeks Clarity Amid Global Economic Concerns

As markets across the globe confront a wave of cautious sentiment, Dollar finds itself in a position of strength, capitalizing on a shift in investor mood. European trading sessions have mirrored the apprehensive tone set by Asian markets, although early signs from US pre-markets suggest that the intense selling pressure may be subsiding.

Swiss Franc and Japanese Yen, traditionally seen as safe havens during tumultuous times, rise slightly too . Australian Dollar, however, has been less fortunate, trailing behind with New Zealand Dollar and British Pound. Canadian Dollar is also underperforming, albeit to a lesser extent. Euro stands somewhere in between, struggling to keep pace with its European counterparts.

At the core of the cautious turn in sentiment might be a combination of profit-taking activities, following the previous week's robust stock rally, and fresh concerns sparked by unsatisfactory economic data. Notably, Germany's industrial production has taken a sharper downturn than analysts predicted, shrinking by -1.4% mom. Additionally, persistent softness in China's export figures has contributed to the unease, though a clear driver behind the current mood shift remains elusive.

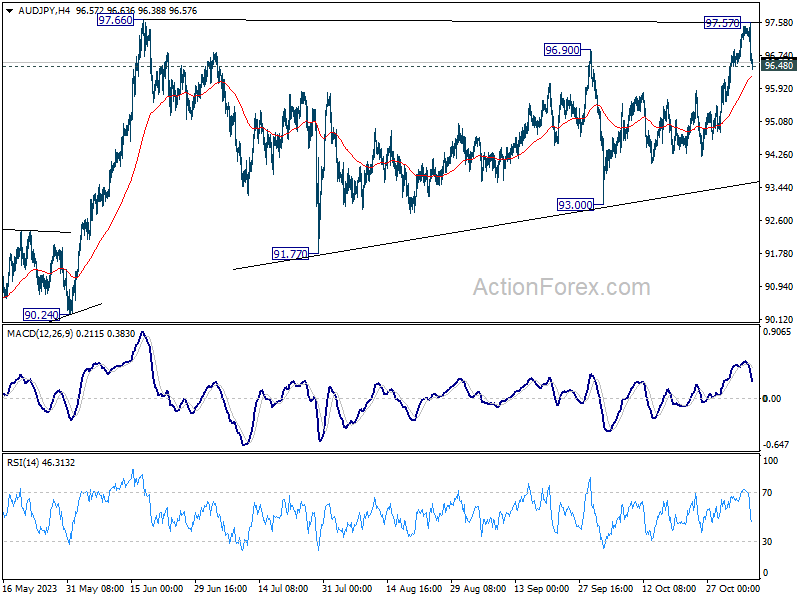

From a technical perspective, AUD/JPY's breach of 97.57 minor suggest is taken as an initial sign of rejection by 97.66 resistance. Sustained break of 55 4H EMA (now at 96.22) will argue that the consolidation pattern from 97.66 is extending with another falling leg. In this case, AUD/JPY would head lower towards lower trendline (now at 93.47).

In Europe, at the time of writing, FTSE is up 0.07%. DAX is down -0.14%. CAC is down -0.51%. Germany 10-year yield is down -0.053 at 2.694. Earlier in Asia, Nikkei dropped -1.34%. Hong Kong HSI dropped -1.65%. China Shanghai SSE dropped -0.04%. Singapore Strait Times dropped -0.21%. Japan 10-year JGB yield rose 0.0029 to 0.877.

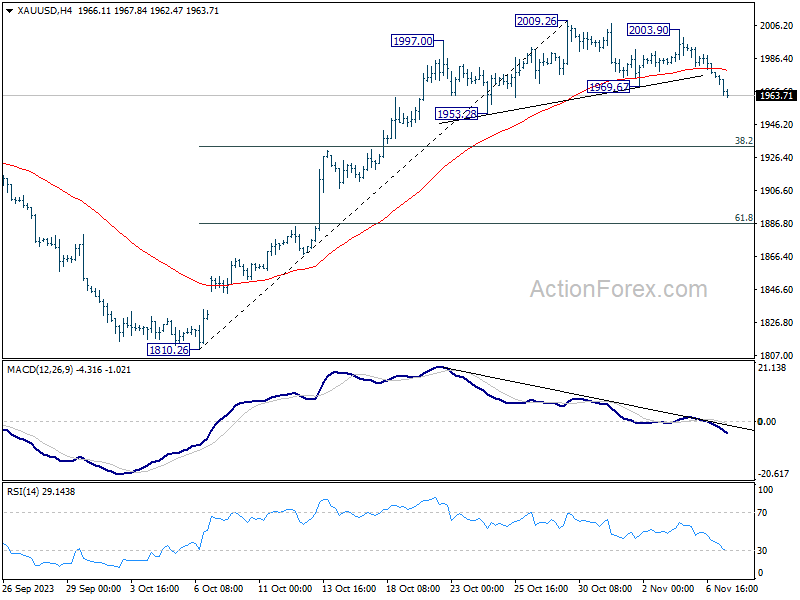

Gold completes head and shoulder top, how low will it go?

Gold's decline from 2009.26 continued today and the break of 1969.67 support completed a head and shoulder top pattern (ls: 1997.00, h: 2009.26, rs: 2003.90). The development suggests that it's already in correction to the whole rally from 1810.26. Further decline should be seen towards 38.2% retracement of 1810.26 to 2009.26 at 1933.24.

Overall outlook is unchanged that correction from 2062.95 has completed with three waves down to 1810.26. Hence, strong support should be seen from 1933.24, which is close to 55 D EMA (now at 1933.62), to contained downside. Another rally through 2009.26 to retest 2062.95 high should be seen sooner rather than later.

However, sustained break of 1933 support zone, will dampen this above bullish view, and open up deeper fall 61.8% retracement at 1886.27, and possibly below.

Eurozone's PPI at 0.5% mom, -12.4% yoy in Sep

Eurozone PPI came in at 0.5% mom, -12.4% yoy in September, versus expectation of 0.3% mom, -12.5% yoy. For the month, Industrial producer prices increased by 2.2% in the energy sector, while prices remained stable for capital goods and for durable consumer goods, and prices decreased by 0.2% for both intermediate goods and non-durable consumer goods. Prices in total industry excluding energy decreased by 0.1%.

EU PPI came in at -0.6% mom, -11.2% yoy. The biggest monthly increases in industrial producer prices were observed in Luxembourg (+28.5%), Romania (+2.6%) and Bulgaria (+2.1%), while the largest decreases were recorded in Finland (-0.9%), Cyprus and Poland (both -0.3%) and Germany (-0.2%).

RBA hikes to 4.35%, future path hinges on evolving data

RBA announced an increase in cash rate target by 25 bps to 4.35%, aligning with market anticipations. Accompanying this move, RBA signaled a shift to a neutral policy stance, indicating that "whether further tightening of monetary policy is required... will depend upon the data and the evolving assessment of risks ."

In the statement, RBA said inflation is "still too high" and is proving "more persistent than expected a few months ago". A rate hike was was warranted today to be "more assured" that inflation would return to target in a "reasonable timeframe".

The central bank's outlook is tempered by "significant uncertainties," particularly regarding the persistence of services inflation which has been notably resilient internationally and could mirror in the Australian market.

The effectiveness of monetary policy changes and the response of wage settings and pricing decisions amid a slowdown in economic growth are areas of unpredictability, especially given the current tightness of the labor market. Household consumption prospects are also veiled with uncertainty, too. T

Looking abroad, RBA's statement brought to light the ongoing global uncertainties, notably the economic trajectory of China and the far-reaching consequences of international conflicts, adding further dimensions to the central bank's considerations.

China's export decline deepens while imports rebound

China's export figures have taken a sharper downturn than anticipated in October, contracting by -6.4% yoy to USD 274.8B, exceeding market predictions of -3.1% yoy. This downturn marks the sixth consecutive month where China's exports have receded.

In contrast, imports defied expectations with a 3.0% yoy increase, a significant departure from the forecasted -5.4% yoy decline, and putting an end to an 11-month streak of contraction.

The culmination of these trade activities resulted in a considerable narrowing of the trade surplus, which shrunk from USD 77.7B to USD 56.5B. This is a stark contraction compared to the anticipated figure of USD 84.2B.

Japan's labor cash earnings up 1.2% yoy, but real wages down for 18th month

Japan reported a modest increase in nominal labor cash earnings in September, with 1.2% yoy rise that slightly exceeded market expectations of 1.0% yoy gain. This uptick, an improvement from the previous month's 0.8%, may seem like a positive indicator at first glance, with base salary growth also marking an increase to 1.4% yoy from August's 1.2% yoy.

However, not all components of earnings showed strength. Special payments, often a volatile category, continued to decline by -6.0% yoy , albeit a less severe contraction than -6.3% yoy reported in August. Meanwhile, overtime pay exhibited a marginal increase, rising 0.7% yoy, suggesting a modest uptick in extra working hours.

The nuanced picture of Japan's wage situation becomes more concerning when adjusted for inflation. Real wages, which reflect the purchasing power of income, fell sharply by -2.4% yoy compared to the same month last year, marking the 18th consecutive month of decline. This persistent slide in real wages points to the squeeze on household income as inflation outpaces nominal wage growth.

In line with the strain on incomes, household spending dipped by -2.8% yoy , although the figure is marginally better than the anticipated -3.0% yoy fall. This marks the seventh straight month of decline, underscoring the ongoing reticence of Japanese consumers to open their wallets amid economic uncertainties.

On a more positive note, on a seasonally adjusted basis, household spending saw an unexpected increase of 0.3% mom, defying expectations of a -0.4% mom decline.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0703; (P) 1.0730; (R1) 1.0743; More...

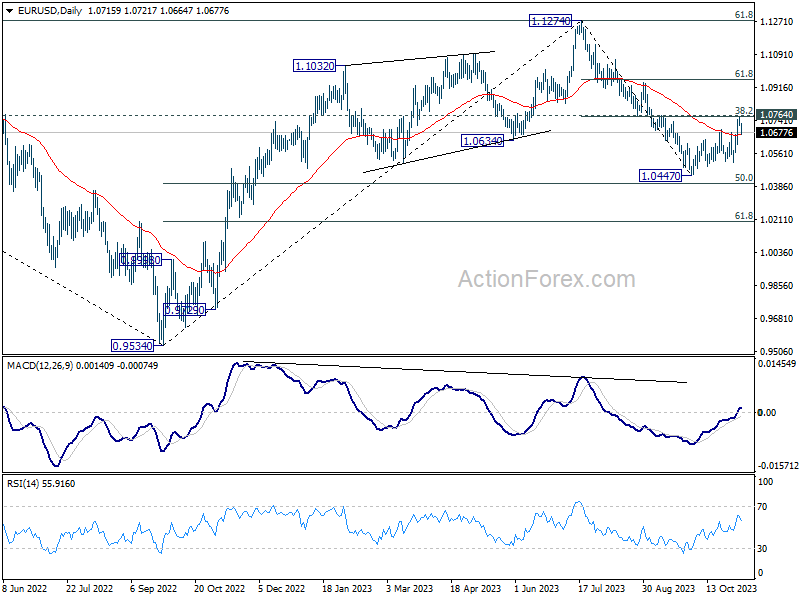

Intraday bias in EUR/USD stays neutral at this point. Further rally is in favor as long as 55 4H EMA (now at 1.0638) holds. Decisive break of 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763) will extend the rise from 1.0447 to 61.8% retracement at 1.0958 next. However, sustained break of 55 4H EMA will argue that the rebound has completed, and target 1.0515 support, and then 1.0447 low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Sep | 1.20% | 1.00% | 1.10% | 0.80% |

| 23:30 | JPY | Overall Household Spending Y/Y Sep | -2.80% | -3.00% | -2.50% | |

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Oct | 2.60% | 2.80% | ||

| 03:00 | CNY | Trade Balance (USD) Oct | 56.5B | 84.2B | 77.7B | |

| 03:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% | 4.10% | |

| 06:45 | CHF | Unemployment rate Oct | 2.10% | 2.10% | 2.10% | |

| 07:00 | EUR | Germany Industrial Production M/M Sep | -1.40% | -0.30% | -0.20% | |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Oct | 658B | 678B | ||

| 10:00 | EUR | Eurozone PPI M/M Sep | 0.50% | 0.30% | 0.60% | 0.70% |

| 10:00 | EUR | Eurozone PPI Y/Y Sep | -12.40% | -12.50% | -11.50% | |

| 12:30 | CAD | Trade Balance (CAD) Sep | 2.0B | 1.0B | 0.7B | |

| 13:30 | USD | Trade Balance (USD) Sep | -61.5B | -60.5B | -58.3B | -58.7B |

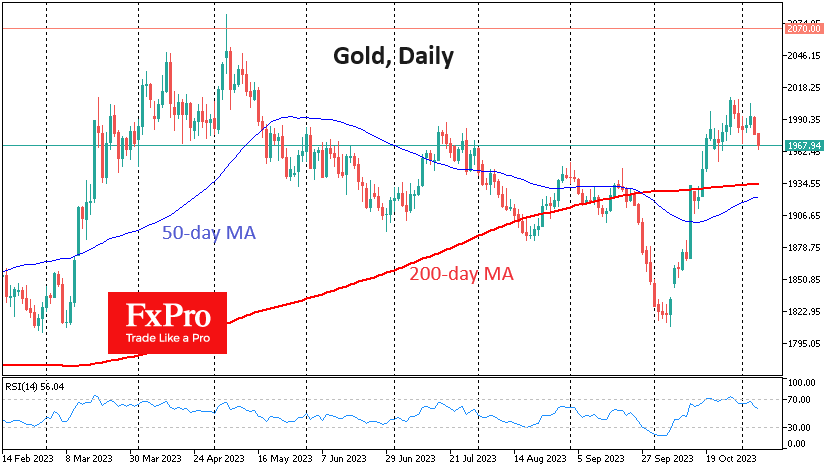

Gold in Correction

Gold came under pressure this week, losing around 1.4% and retreating to $1966. This drops below previous local lows, forming a short-term downtrend and fitting into a pattern of declines following local overbought conditions.

Gold has been in strong demand since October 7th, following the war in Gaza. However, technical patterns are still at work. We have seen that the entry into the overbought area on the Relative Strength Index on the daily timeframe caused the growth to stall, and more active selling began early last week. As a result, the RSI retreated from the overbought area, which is often a medium-term signal for the end of growth and, at the very least, the beginning of a full-blown correction.

According to the Fibonacci pattern, we should pay more attention to the price dynamics around $1960, which is 76.4% of the amplitude of the October move. With strong buying interest, gold could find support and return to growth. Such shallow corrections are common in strong bull markets.

But we see more potential in a more profound correction with a pullback to $1932. The 61.8% retracement level, a classic Fibonacci pattern marker, is concentrated at this level. In addition, the 200-day moving average passes through here.

The ability to hold above this level will keep the focus on sustaining the bull market in gold. If the sellers don’t stop here, the broader investment community could join in the selling. As in June 2022 or September 2023, a break below this line could be followed by a sharp decline. In the above cases, the price fell 8.5% and 6%, respectively, after a break below the 200-day average. Repeating this amplitude would wipe out October’s gains or the gains of the last 12 months.

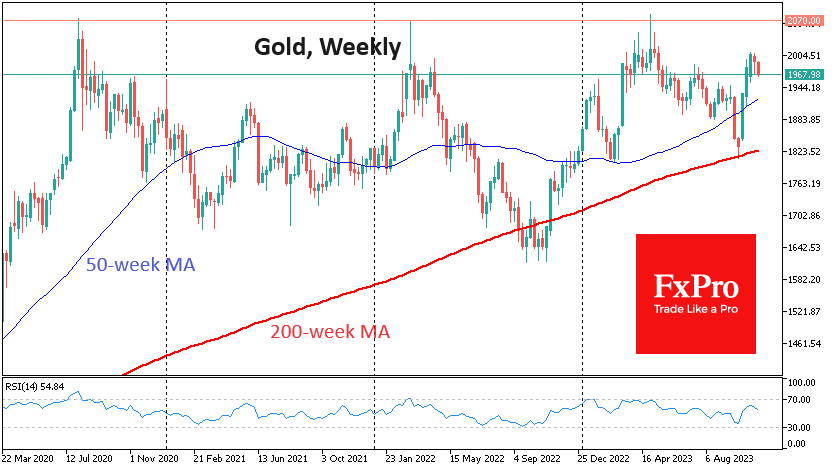

A fall back to near $1800 would take gold below the 200-week average, which it touched so nicely during the reversal in early October. However, it is rare to see such nice touches in gold. For example, a couple of them in 2017 failed to become a starting point for gold’s rally, and only a dip below the 200-week average in late 2018 revived buying interest.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0703; (P) 1.0730; (R1) 1.0743; More...

Intraday bias in EUR/USD stays neutral at this point. Further rally is in favor as long as 55 4H EMA (now at 1.0638) holds. Decisive break of 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763) will extend the rise from 1.0447 to 61.8% retracement at 1.0958 next. However, sustained break of 55 4H EMA will argue that the rebound has completed, and target 1.0515 support, and then 1.0447 low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.