Sample Category Title

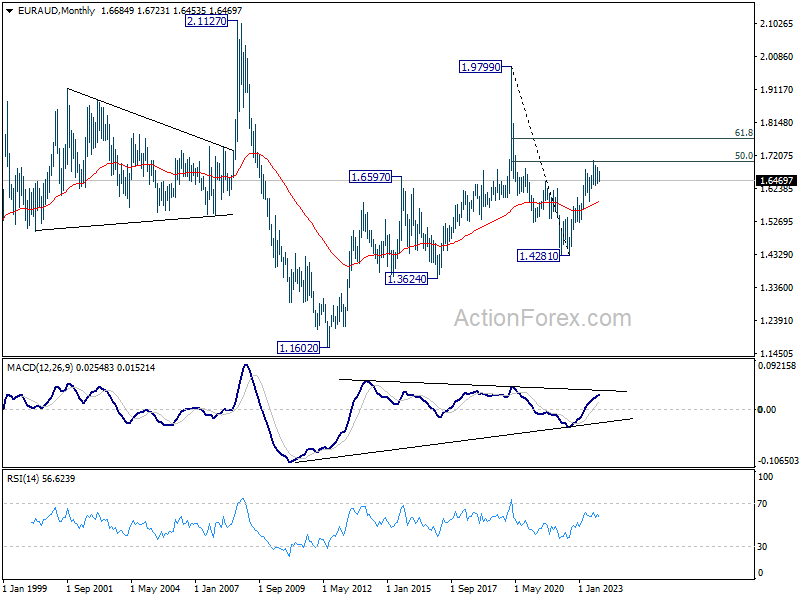

EUR/AUD Weekly Outlook

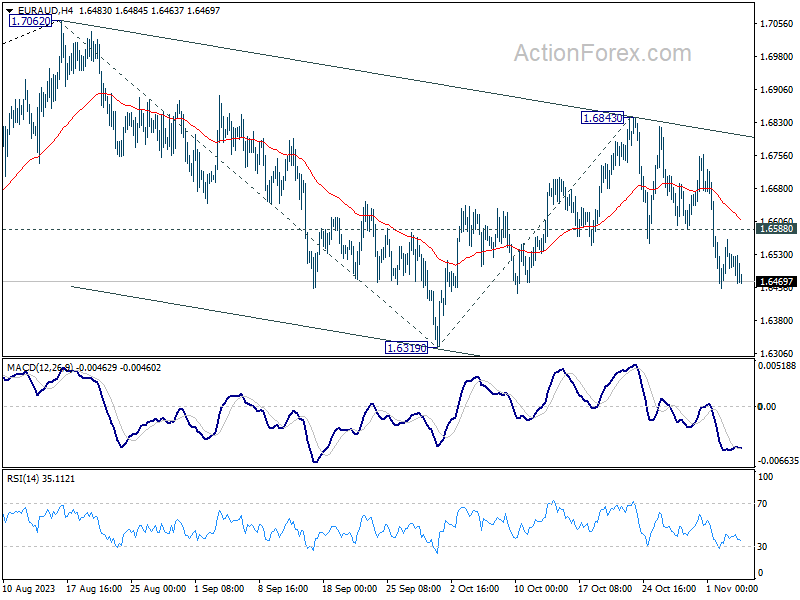

EUR/AUD's decline last week argues that corrective rebound from 1.6319 has completed at 1.6843 already. Initial bias stays on the downside this week for retesting 1.6319 support next. Sustained break there will target 100% projection of 1.7062 to 1.6319 from 1.6843 at 1.6100. On the upside, above 1.6588 minor resistance will turn intraday bias neutral first.

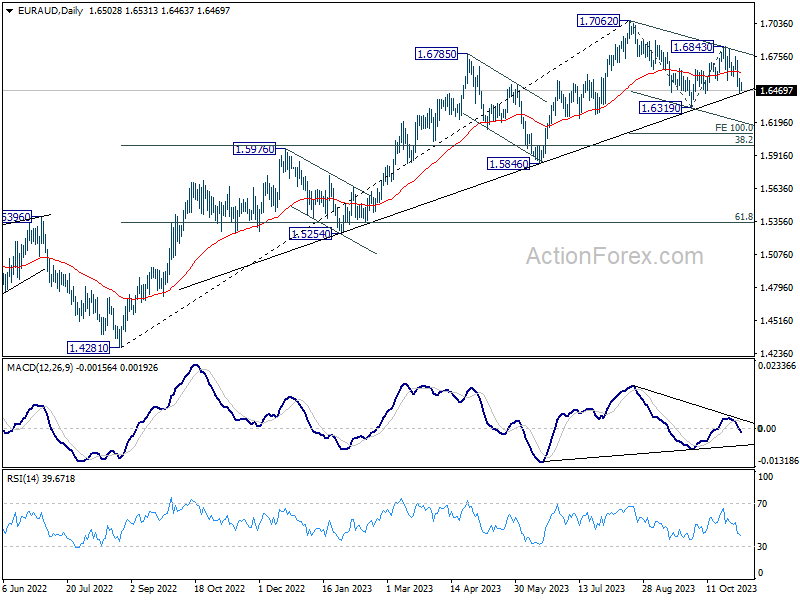

In the bigger picture, current development suggests that 1.7062 is already a medium term top. Fall from there is seen as a correction to the up trend from 1.4281 (2022 low). While deeper decline might be seen, strong support should emerge from 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to contain downside. However, sustained break of 1.6000 will raise the chance of bearish tend reversal.

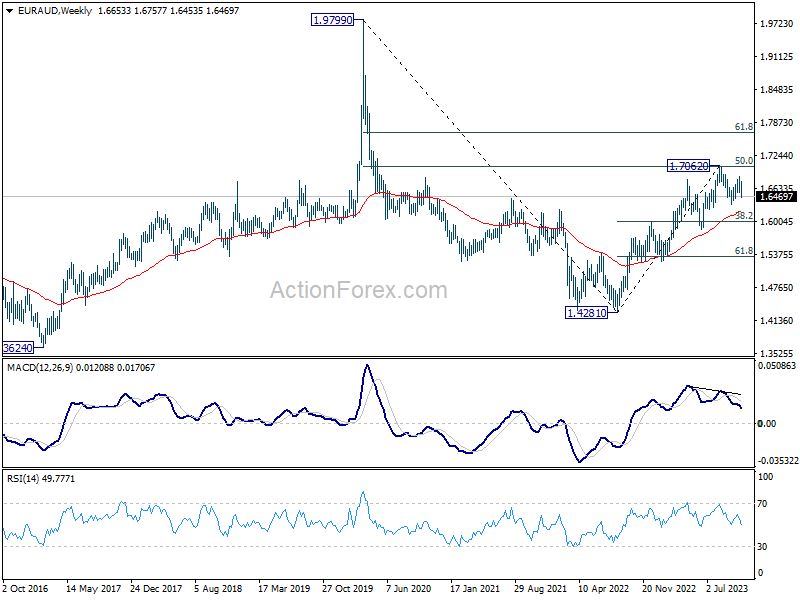

In the longer term picture, loss of upside momentum as seen in 55 W MACD at this stage argues that rise from 1.4281 (2022 low) is more likely a corrective move. Further rise could still be seen as long as 1.5846 support holds. But upside will likely be limited by 61.8% retracement of 1.9799 to 1.4281 at 1.7691. Firm break of 1.5846 support will argue that the rise has completed, and another medium term down leg has started.

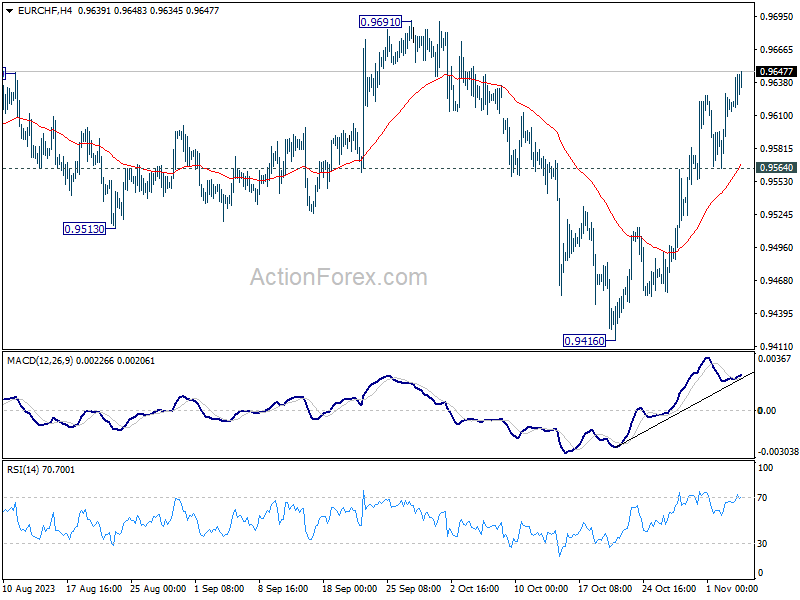

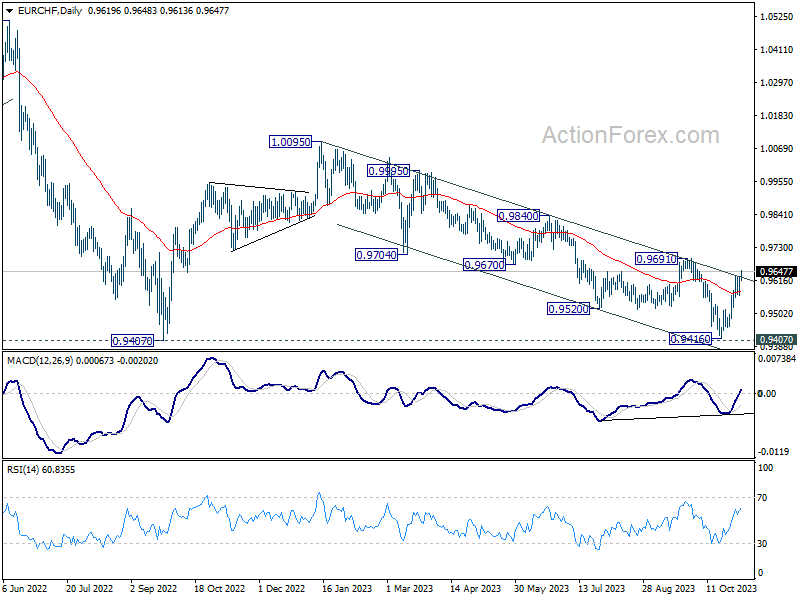

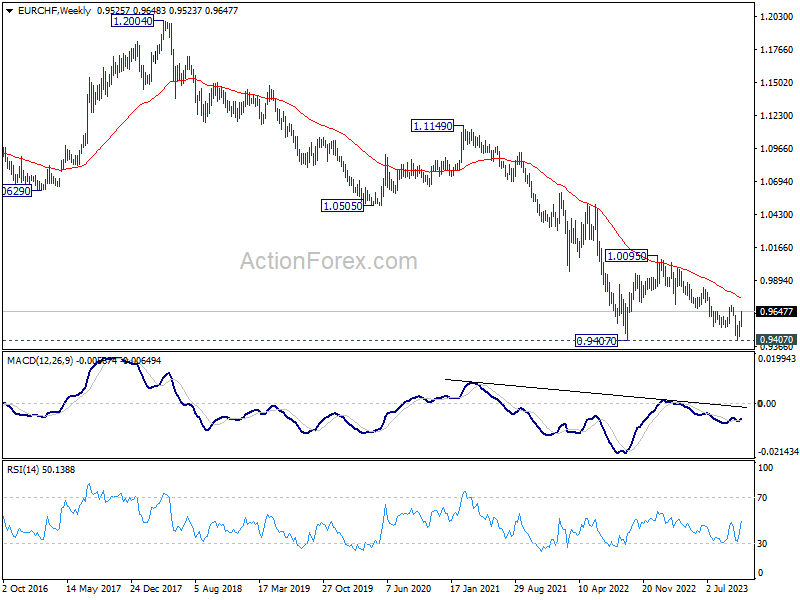

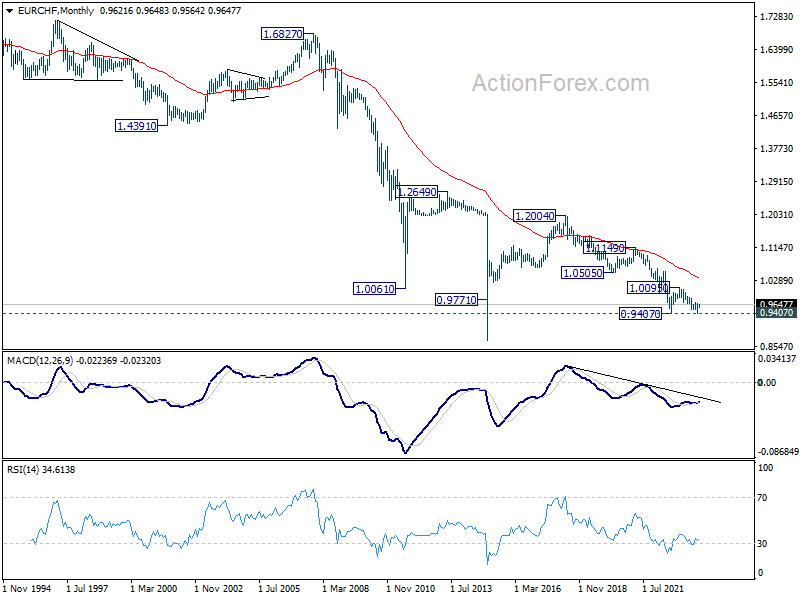

EUR/CHF Weekly Outlook

EUR/CHF's rise from 0.9416 continued last week and hit as high as 0.9648 despite interim retreat. Initial bias is on the upside this week for 0.9691 key structural resistance next. Firm break there will argue that whole decline from 1.0095 has completed at 0.9416, just ahead of 0.9407 support (2022 low). Further rally would be seen to 0.9840 resistance next. For now, break of 0.9564 support is needed to indicate short term topping. Otherwise, further rally will remain in favor in case of retreat.

In the bigger picture, as long as 1.0095 resistance holds, price actions from 0.9407 are viewed as a three-wave consolidation pattern first. Current rise from 0.9416 might be the third leg. That is, larger down trend from 1.2004 (2018 high) might still resume through 0.9407 at a later stage. However, decisive break of 1.0095 will argue that the long term down trend is reversing.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0362). Break of 1.0095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

Weekly Economic & Financial Commentary: Q4 Appears Off to a Slower Start

Summary

United States: Q4 Appears Off to a Slower Start

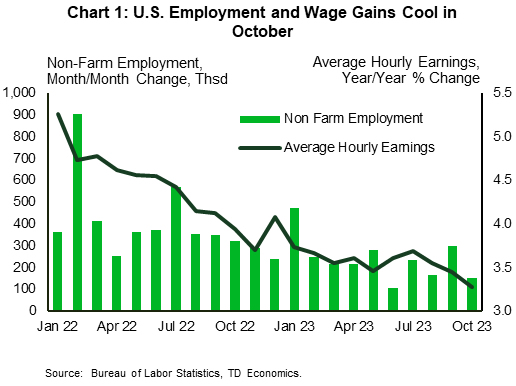

- This week delivered an onslaught of economic indicators that provided a first glimpse of economic activity during Q4. In short, the remarkable strength on display during Q3 looks to be fading as the year begins to wind to a close. The labor market was front and center. After September's surprising surge, nonfarm payrolls advanced at a more moderate pace in October, rising by 150,000 net new jobs during the month.

- Next week: Trade Balance (Tue.), Consumer Credit (Tue.), U. of Mich. Sentiment (Fri.)

International: Bank of Japan Continues Its Monetary Policy Tweaks

- The Bank of Japan delivered another monetary policy tweak this week. It held its policy rate and 10-year yield target steady at -0.10% and 0.00%, respectively, but said it would treat the 1.00% upper bound for 10-year yields as a "reference", rather than a "hard cap" as it had done previously. We believe the case for a more substantial policy adjustment is gradually building and expect a 10 bps policy rate hike at the central bank's April 2024 monetary policy meeting.

- Next week: Reserve Bank of Australia Policy Rate (Tue.), Mexico Policy Rate (Thu.), U.K. GDP (Fri.)

Interest Rate Watch: FOMC on "Hawkish Hold"

- For the third time in the past four policy meetings, the FOMC refrained from hiking its target range for the federal funds rate this week. Although the FOMC is keeping the door open to more policy tightening, we believe the bar to further rate increases is higher now than it was a few months ago.

Credit Market Insights: Households Grow More Pessimistic about Credit Conditions

- Earlier this month, the New York Fed released September data for its Survey of Consumer Expectations. The data revealed that inflation expectations held mostly steady, but households’ perceptions and expectations for credit conditions deteriorated slightly over the month.

The Weekly Bottom Line: The Fed’s Door is Still Open

U.S. Highlights

- The Federal Reserve’s policy statement took center stage this week. As expected, the Fed kept policy rates unchanged but preserved the option of hiking in the future.

- Hiring in the U.S. slowed in October, with wage gains decelerating and the unemployment rate edging up.

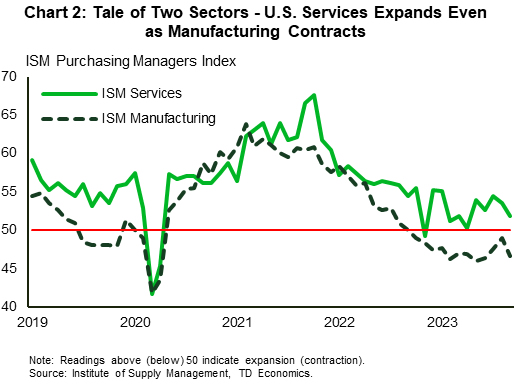

- Activity in the manufacturing sector continued to contract in October, in contrast to the continued expansion in the services sector (though at a slower rate).

Canadian Highlights

- GDP growth in the month of August and September is reigniting chatter around a Canadian recession. It’s too early to tell, but the Canadian economy is evidently slowing.

- Canada’s labour market continued to add jobs in October, but not enough to keep pace with labour force growth, pushing the unemployment rate higher.

- The Bank of Canada (BoC) likely welcomed this week’s developments. Their decision to hold the policy rate at 5.00% last meeting is shaping up to be the prudent move.

U.S. – The Fed’s Door is Still Open

The U.S. economic calendar was packed this week with a mix of key data, central bank meetings and even Treasury auction announcements. To start things off, the Treasury announced its financing requirements for the upcoming quarter. In the announcement, issuance is dominated by shorter dated securities (2-7 year), with planned 10-to-30-year range issuance less than most had expected. What’s more, Treasury’s projection that it will slow the recent flood of new long-dated debt, contributed to a rally in the bond market and a pullback in long-term yields.

The next key focus was the labor market, with varying reports giving snapshots of the state of this important sector. November’s nonfarm payrolls, the most important, showed that hiring in the U.S. economy has slowed. Additionally, the pace of wage growth has cooled (Chart 1). The unemployment rate also edged up slightly, bucking expectations for no change. The job opening and labor turnover survey (JOLTS) was slightly backward looking, covering September, and showed an increase in job openings, which was offset by a rise in the number unemployed, leaving the ratio of the two largely unchanged at 1.5. The pace of hiring also eased and the quit rate levelled off at its pre-pandemic rate. The employment cost index on the other hand showed that wage gains ticked up in the third quarter, but compensation growth still slowed from 4.5% to 4.3% on a year-on-year basis. Overall, the labor market metrics are consistent with what the Fed wants to see – a market that is slowly cooling with likely further deceleration in wage pressures ahead.

As widely expected, the Federal Reserve held interest rates steady at 5.25%-5.50% on Wednesday. This is the first time in the current tightening cycle that the Fed has paused for two consecutive meetings. However, the central bank still left the door wide open to potentially raising rates in the future if needed to keep the disinflation momentum going. October’s cooling in the labor market combined with expectations that economic activity will pullback in Q4, suggests that they may not need to walk through it before the year is done, but only time (and the data) will tell.

One sector of the economy that is not fairing very well is the manufacturing sector. Activity in the sector, as measured by the ISM sentiment survey, continued to contract in October, falling to its lowest level since July, on broad-based weakness. The silver lining, however, is that a pullback in raw materials prices is easing cost pressures, which should help to mitigate price pressures for consumer goods. The services side of the economy fared a bit better, with the ISM services index expanding again in October, though at a slower pace (Chart 2). Twelve out of eighteen industries reported growth; however, the softer-than-expected reading suggests that the Fed’s hiking campaign is influencing the services sector as well.

The takeaway from the week is that if the disinflationary trend remains intact, the Fed’s December decision is a tougher call. There will be several economic releases over the next six weeks that will influence the Fed’s decision. But, so far, consumer spending momentum has remained stronger than expected, risking an uptick in inflation. This still suggests that the Fed’s work is likely not done.

Canada – Proceeding With Caution

The "R" word has crept back into discussion this week. Could the Canadian economy already be in a recession? Technically speaking, maybe–but we won't know until official third quarter GDP readings land at the end of the month. GDP updates this week for August (no growth), combined with guidance for flat growth in September, suggests that third quarter GDP could have contracted by a very small 0.1% annualized rate. If so, that would mark a technical recession, given the narrow decline in economic activity in the quarter prior.

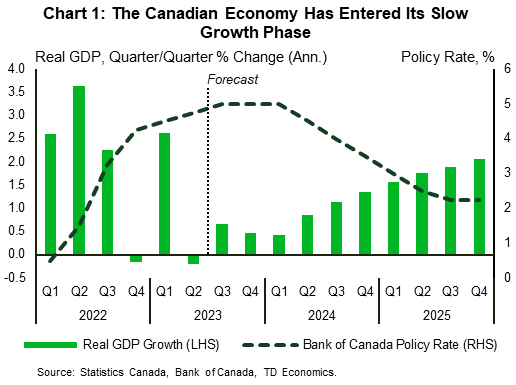

Technicalities still matter, but economic activity would be better characterized as flat over the last two quarters. On the one hand, this is impressive as the economy battled through significant wildfire activity, major strikes, and other idiosyncratic shocks concurrently with multi-decade high interest rates. On the flip side, this is clear evidence that the economy is cooling. From here, we expect a prolonged period of below-trend growth before activity picks up in the second half of next year, alongside interest rate cuts commencing around the mid-year mark (Chart 1).

The Canadian labour market is also slowing but hasn't fully ceded its strength. The Canadian economy added another 18k jobs in October, pulling the three-month trend in job gains slightly upward. The unemployment rate, however, has moved up seven-tenths since April, as labour force gains outpaced employment. The labour market is holding up relatively well at this point in the cycle, but the Bank of Canada (BoC) likely wants to see the market move further into balance. Notably, wage gains are still robust, potentially fanning future inflation fears and vacancies, while declining, are still at elevated levels.

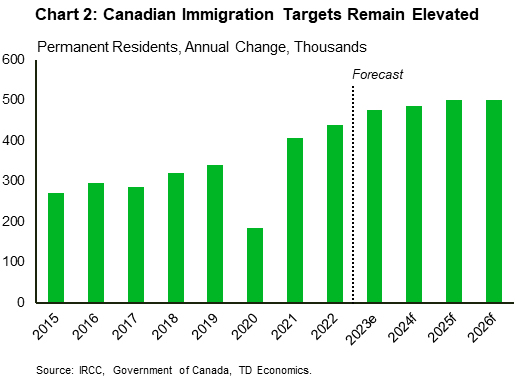

Strong labour force and employment growth in the last year were a function of the rapid population increase across the nation. Over the last 12 months, Canada added over one million people, which provided an impulse to hiring and spending. The Canadian government updated its immigration plan this week, targeting 485k, 500k, and 500k new permanent residents in 2024, 2025, and 2026, respectively (Chart 2). These targets suggest that population gains will remain durable, adding upward pressure to labour force growth as employment continues to moderate.

The BoC's mission is to get inflation back to its two-percent target. Governor Macklem and Deputy Governor Rogers reiterated the BoC's policy stance this week in two separate testimonies, nailing down a few key points. Firstly, further easing in inflation will take some time, but that if inflationary pressures exist, they are "prepared to raise the policy rate further to restore price stability". Secondly, just as we have highlighted above, the BoC has acknowledged that the Canadian economy is showing clear signs slowing and will continue to do so as higher interest rates curb consumer spending and rebalance supply and demand. Overall, developments this week should add a layer of comfort to the BoC's decision to stand pat on the 5.00% policy rate.

Canadian Imports Softening on Lower Consumer and Business Spending

The week ahead will be a lighter one for data releases after signs of decelerating Canadian GDP growth, a higher unemployment rate in both the U.S. and Canada , and the U.S. Federal Reserve foregoing an interest rate hike for a second consecutive meeting in the week past.

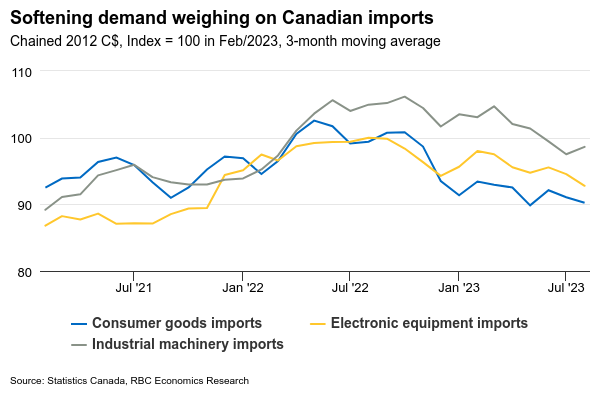

We expect Canada’s international goods trade surplus will widen with a 10% increase in oil prices boosting the value of net energy exports. Excluding price impacts, net trade is on track to add to GDP growth in Q3, but only as a result of an offsetting faltering in domestic demand. Lower imports of both consumer goods and equipment in the third quarter to-date are adding to signs that consumer spending and business investment are slowing. Canadian exports surged 5.7% in August, but largely due to a jump in gold shipments and higher oil prices. Excluding price impacts, exports of merchandise are tracking little changed in Q3 to-date.

As the economy loses steam, attention will also be on government finances with Quebec’s Economic and Fiscal Update set for release on November 7th. Canada’s provinces emerged from the pandemic in better fiscal positions than feared , thanks to rapidly rebounding economic growth. But provinces have yet to scale back expenditures even with pandemic support programs ended. Weaker economic growth, rising operating costs, and higher debt-servicing costs will continue to challenge provinces’ fiscal positions. Ontario’s Fall Economic Statement last week showed a larger $5.6 billion deficit for the current year, compared to the $1.3 billion deficit projected in the spring.

Week ahead data watch

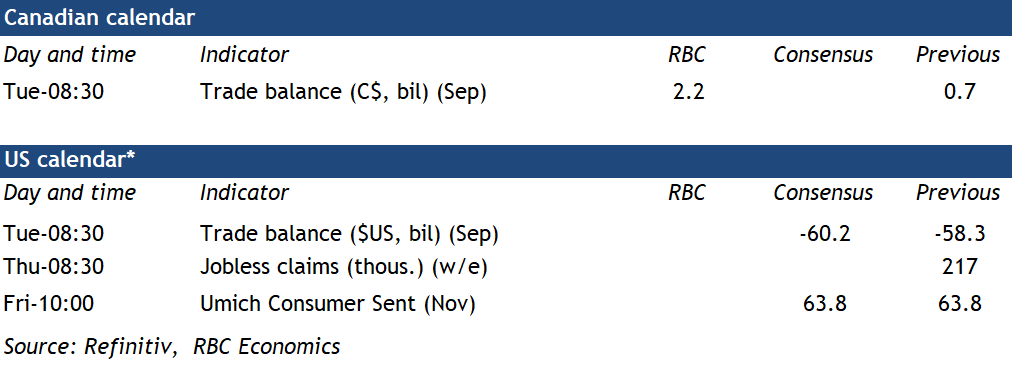

The U.S. trade deficit is expected to widen to -$59.3 billion in September from $58.3 billion in August, driven by a $1.1 billion deterioration in the advance estimate of the goods trade balance. Merchandise exports jumped 2.9% in the advance estimate, led by higher food (+10%) and consumer goods (+7%) shipments. Merchandise imports rose 2.4% on broadly-based gains.

Summary 11/6 – 11/10

Monday, Nov 6, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | ||

| 00:00 | AUD | TD Securities Inflation M/M Oct | 0% | |

| 07:00 | EUR | Germany Factory Orders M/M Sep | -1.40% | 3.90% |

| 08:45 | EUR | Italy Services PMI Oct | 48.5 | 49.9 |

| 08:50 | EUR | France Services PMI Oct | 46.1 | 46.1 |

| 08:55 | EUR | Germany Services PMI Oct | 48 | 48 |

| 09:00 | EUR | Eurozone Services PMI Oct | 47.8 | 47.8 |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Nov | -22.5 | -21.9 |

| 09:30 | GBP | Construction PMI Oct | 46.2 | 45 |

| 15:00 | CAD | Ivey PMI Oct | 54 | 53.1 |

| 23:30 | JPY | Labor Cash Earnings Y/Y Sep | 1.00% | 1.10% |

| 23:30 | JPY | Overall Household Spending Y/Y Sep | -2.60% | -2.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | |

| Forecast: | Previous: | ||

| 00:00 | AUD | TD Securities Inflation M/M Oct | |

| Forecast: | Previous: 0% | ||

| 07:00 | EUR | Germany Factory Orders M/M Sep | |

| Forecast: -1.40% | Previous: 3.90% | ||

| 08:45 | EUR | Italy Services PMI Oct | |

| Forecast: 48.5 | Previous: 49.9 | ||

| 08:50 | EUR | France Services PMI Oct | |

| Forecast: 46.1 | Previous: 46.1 | ||

| 08:55 | EUR | Germany Services PMI Oct | |

| Forecast: 48 | Previous: 48 | ||

| 09:00 | EUR | Eurozone Services PMI Oct | |

| Forecast: 47.8 | Previous: 47.8 | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Nov | |

| Forecast: -22.5 | Previous: -21.9 | ||

| 09:30 | GBP | Construction PMI Oct | |

| Forecast: 46.2 | Previous: 45 | ||

| 15:00 | CAD | Ivey PMI Oct | |

| Forecast: 54 | Previous: 53.1 | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Sep | |

| Forecast: 1.00% | Previous: 1.10% | ||

| 23:30 | JPY | Overall Household Spending Y/Y Sep | |

| Forecast: -2.60% | Previous: -2.50% | ||

Tuesday, Nov 7, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Oct | 2.80% | |

| 03:00 | CNY | Trade Balance (USD) Oct | 84.2B | 77.7B |

| 03:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.10% |

| 07:00 | EUR | Germany Industrial Production M/M Sep | -0.30% | -0.20% |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Oct | 678B | |

| 10:00 | EUR | Eurozone PPI M/M Sep | 0.30% | 0.60% |

| 10:00 | EUR | Eurozone PPI Y/Y Sep | -11.50% | |

| 12:30 | CAD | Trade Balance (CAD) Sep | 1.0B | 0.7B |

| 13:30 | USD | Trade Balance (USD) Sep | -60.5B | -58.3B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Oct | |

| Forecast: | Previous: 2.80% | ||

| 03:00 | CNY | Trade Balance (USD) Oct | |

| Forecast: 84.2B | Previous: 77.7B | ||

| 03:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 4.35% | Previous: 4.10% | ||

| 07:00 | EUR | Germany Industrial Production M/M Sep | |

| Forecast: -0.30% | Previous: -0.20% | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Oct | |

| Forecast: | Previous: 678B | ||

| 10:00 | EUR | Eurozone PPI M/M Sep | |

| Forecast: 0.30% | Previous: 0.60% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Sep | |

| Forecast: | Previous: -11.50% | ||

| 12:30 | CAD | Trade Balance (CAD) Sep | |

| Forecast: 1.0B | Previous: 0.7B | ||

| 13:30 | USD | Trade Balance (USD) Sep | |

| Forecast: -60.5B | Previous: -58.3B | ||

Wednesday, Nov 8, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 02:00 | NZD | RBNZ Inflation Expectations Q4 | 2.83% | |

| 05:00 | JPY | Leading Economic Index Sep P | 109.2 | |

| 07:00 | EUR | Germany CPI M/M Oct | 0.00% | 0.00% |

| 07:00 | EUR | Germany CPI Y/Y Oct | 3.80% | 3.80% |

| 07:45 | EUR | France Trade Balance (EUR) Sep | -8.1B | -8.2B |

| 09:00 | EUR | Italy Retail Sales M/M Sep | -0.20% | -0.40% |

| 10:00 | EUR | Eurozone Retail Sales M/M Sep | -0.20% | -1.20% |

| 12:30 | CAD | Building Permits M/M Sep | 1.20% | 3.40% |

| 15:00 | USD | Wholesale Inventories Sep F | 0.00% | 0.00% |

| 15:30 | USD | Oil Inventories | 0.774M | |

| 23:50 | JPY | BoJ Summary of Opinions | ||

| 23:50 | JPY | Current Account (JPY) Sep | 2.27T | 1.63T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 02:00 | NZD | RBNZ Inflation Expectations Q4 | |

| Forecast: | Previous: 2.83% | ||

| 05:00 | JPY | Leading Economic Index Sep P | |

| Forecast: | Previous: 109.2 | ||

| 07:00 | EUR | Germany CPI M/M Oct | |

| Forecast: 0.00% | Previous: 0.00% | ||

| 07:00 | EUR | Germany CPI Y/Y Oct | |

| Forecast: 3.80% | Previous: 3.80% | ||

| 07:45 | EUR | France Trade Balance (EUR) Sep | |

| Forecast: -8.1B | Previous: -8.2B | ||

| 09:00 | EUR | Italy Retail Sales M/M Sep | |

| Forecast: -0.20% | Previous: -0.40% | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Sep | |

| Forecast: -0.20% | Previous: -1.20% | ||

| 12:30 | CAD | Building Permits M/M Sep | |

| Forecast: 1.20% | Previous: 3.40% | ||

| 15:00 | USD | Wholesale Inventories Sep F | |

| Forecast: 0.00% | Previous: 0.00% | ||

| 15:30 | USD | Oil Inventories | |

| Forecast: | Previous: 0.774M | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Current Account (JPY) Sep | |

| Forecast: 2.27T | Previous: 1.63T | ||

Thursday, Nov 9, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | RICS Housing Price Balance Oct | -65% | -69% |

| 01:30 | CNY | CPI Y/Y Oct | -0.20% | 0.00% |

| 01:30 | CNY | PPI Y/Y Oct | -2.70% | -2.50% |

| 05:00 | JPY | Eco Watchers Survey: Current Oct | 50.2 | 49.9 |

| 09:00 | EUR | ECB Economic Bulletin | ||

| 13:30 | USD | Initial Jobless Claims (Nov 3) | 210K | 217K |

| 15:30 | USD | Natural Gas Storage | 79B | |

| 21:30 | NZD | Business NZ PMI Oct | 45.3 | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Oct | 2.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | RICS Housing Price Balance Oct | |

| Forecast: -65% | Previous: -69% | ||

| 01:30 | CNY | CPI Y/Y Oct | |

| Forecast: -0.20% | Previous: 0.00% | ||

| 01:30 | CNY | PPI Y/Y Oct | |

| Forecast: -2.70% | Previous: -2.50% | ||

| 05:00 | JPY | Eco Watchers Survey: Current Oct | |

| Forecast: 50.2 | Previous: 49.9 | ||

| 09:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 13:30 | USD | Initial Jobless Claims (Nov 3) | |

| Forecast: 210K | Previous: 217K | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 79B | ||

| 21:30 | NZD | Business NZ PMI Oct | |

| Forecast: | Previous: 45.3 | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Oct | |

| Forecast: | Previous: 2.40% | ||

Friday, Nov 10, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | RBA Monetary Policy Statement | ||

| 07:00 | GBP | GDP M/M Sep | 0.00% | 0.20% |

| 07:00 | GBP | GDP Q/Q Q3 P | -0.10% | 0.20% |

| 07:00 | GBP | Manufacturing Production M/M Sep | 0.30% | -0.80% |

| 07:00 | GBP | Manufacturing Production Y/Y Sep | 2.80% | |

| 07:00 | GBP | Industrial Production M/M Sep | -0.10% | -0.70% |

| 07:00 | GBP | Industrial Production Y/Y Sep | 1.10% | 1.30% |

| 07:00 | GBP | Goods Trade Balance (GBP) Sep | -15.3B | -16.0B |

| 09:00 | EUR | Italy Industrial Output M/M Sep | -0.10% | 0.20% |

| 12:00 | GBP | NIESR GDP Estimate (3M) Oct | -0.10% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Nov P | 63.6 | 63.8 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | RBA Monetary Policy Statement | |

| Forecast: | Previous: | ||

| 07:00 | GBP | GDP M/M Sep | |

| Forecast: 0.00% | Previous: 0.20% | ||

| 07:00 | GBP | GDP Q/Q Q3 P | |

| Forecast: -0.10% | Previous: 0.20% | ||

| 07:00 | GBP | Manufacturing Production M/M Sep | |

| Forecast: 0.30% | Previous: -0.80% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Sep | |

| Forecast: | Previous: 2.80% | ||

| 07:00 | GBP | Industrial Production M/M Sep | |

| Forecast: -0.10% | Previous: -0.70% | ||

| 07:00 | GBP | Industrial Production Y/Y Sep | |

| Forecast: 1.10% | Previous: 1.30% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Sep | |

| Forecast: -15.3B | Previous: -16.0B | ||

| 09:00 | EUR | Italy Industrial Output M/M Sep | |

| Forecast: -0.10% | Previous: 0.20% | ||

| 12:00 | GBP | NIESR GDP Estimate (3M) Oct | |

| Forecast: | Previous: -0.10% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Nov P | |

| Forecast: 63.6 | Previous: 63.8 | ||

Week Ahead – RBA Rate Decision and UK Growth on the Radar

- Reserve Bank of Australia could raise rates on Tuesday

- Chinese trade and inflation stats also in the spotlight

- UK economy likely contracted in Q3 - can sterling hold on?

RBA decision will be a close call

With most of the major central bank decisions in the rear-view mirror and volatility in bond markets coming down, a quieter week lies ahead for FX traders. Most of the focus will fall on the Reserve Bank of Australia's rate decision on Tuesday, where markets assign a 60% probability for a rate increase.

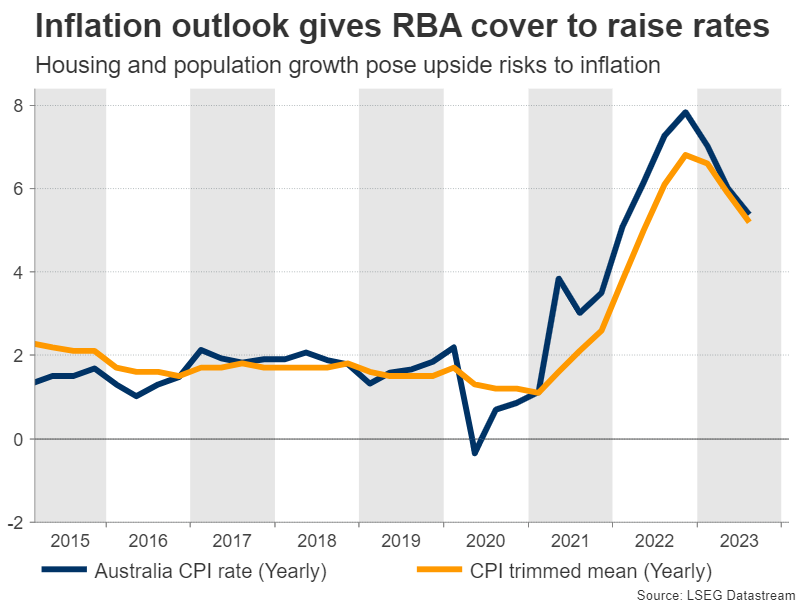

Recent developments in Australia certainly favor another rate increase. Last week, the RBA Governor stressed that her central bank will not hesitate to raise rates further “if there is a material upward revision to the outlook for inflation”. Directly after those comments, inflation data for the third quarter surprised on the upside.

Similarly, house prices continue to rise and almost touched a record high in October according to CoreLogic. That can also boost inflation, both by lifting rent prices and through the wealth effect, as higher home prices often translate into stronger household spending.

Even the IMF recently warned that the RBA needs to raise rates further to cool an economy that is running beyond full capacity, with a historically labor market and booming population growth reinforcing the risk that inflation might remain hot for some time.

Of course, not everything is rosy. For instance, the latest round of business surveys signaled that economic growth will probably slow heading into year-end, amid a decline in new orders. Likewise, the conflict in the Middle East raises uncertainty.

Most importantly, the global wave of rising bond yields has spilled into Australia. With Australian yields trading near their highest levels in a decade, the bond market has essentially done a lot of tightening for the RBA, reducing the need for further rate hikes.

Therefore, there are solid arguments both for raising rates and keeping them unchanged. That said, the case for a rate increase seems stronger based on the data pulse and RBA commentary. Considering that market pricing only implies a 60% chance for a hike, a decision to raise rates could help boost the Australian dollar.

Beyond the RBA decision, the longer-term trajectory for the Australian dollar will also be decided by global risk sentiment and any developments in China.

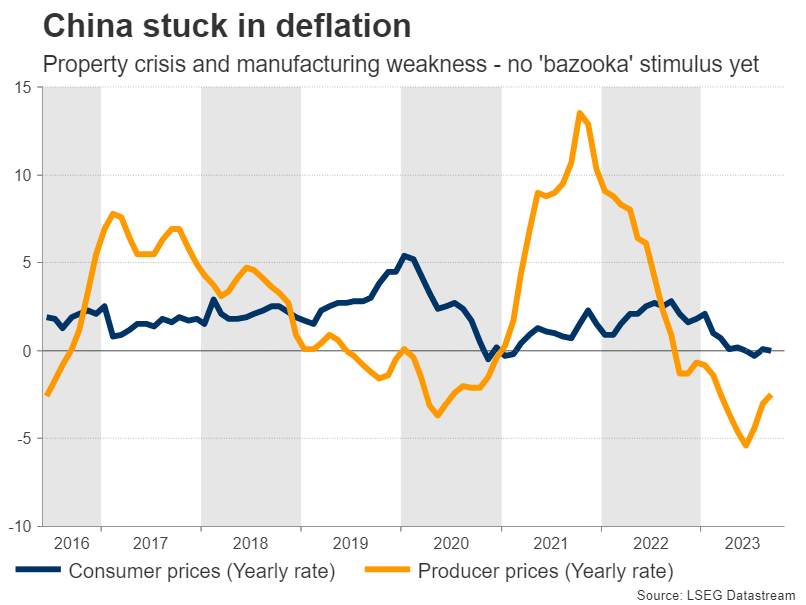

China awaits trade and inflation data

The Australian currency is sensitive to China news because of the close trading relationship between the two nations. Australia and New Zealand rely on Chinese demand to absorb their commodity exports, so the outlook for China directly influences the growth prospects of these economies.

This correlation helps explain why both currencies have been pummeled this year, amid an unfolding property crisis and a severe manufacturing slowdown in China. Investors have been waiting in agony for Beijing to roll out bigger stimulus measures, but so far, the policy response has been underwhelming.

China’s central government announced last week it would boost its budget deficit, approving 1 trillion yuan ($137 billion) in debt issuance. This was a signal that fiscal spending is coming. However, this support package only amounts to 0.8% of GDP, so it might lack the ‘firepower’ to truly kickstart the stalled economy.

In this sense, the upcoming releases will be closely monitored by investors. Trade data for October will hit the markets on Tuesday, ahead of inflation stats for the same month on Thursday. All these numbers are important, but markets often focus on exports and producer prices, which are seen as proxies of global factory demand.

Aside from the commodity-linked currencies, these releases could also impact global risk sentiment, driving stock markets in Asia and other regions accordingly.

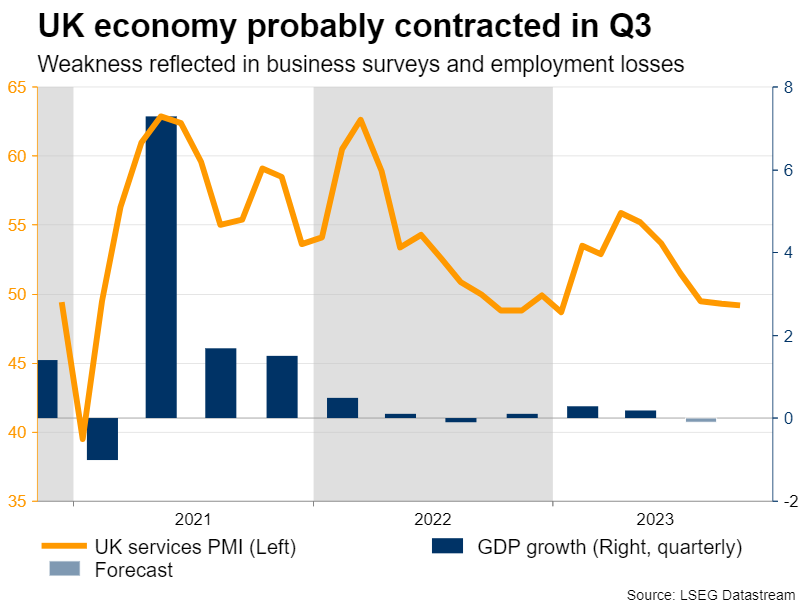

UK GDP could be ugly

Turning to the United Kingdom, the highlight will come on Friday in the form of quarterly GDP numbers. The British economy most likely fell into contraction in the third quarter, something reflected in the monthly GDP readings that have already been released and gloomy business surveys.

Even more worrisome, the UK economy is suffering job losses. The labor market started losing jobs back in June, and this pattern continued through September. Faced with weaker demand conditions and shrinking margins, UK businesses are scrambling to slash costs. One option is to fire workers.

Employment losses are how every recession begins, so this is a massive red flag. In turn, the prospects for sterling appear dim. Economic growth is rolling over while inflation continues to burn hot, painting a stagflationary picture of the UK economy.

On top of that, Cable continues to exhibit strong correlation with stock markets, which leaves it vulnerable in case equities turn lower again as the global economy loses power.

Finally in the euro area, the latest data on producer prices are out on Tuesday, ahead of retail sales on Wednesday.

Will RBA Confirm Rate Hike Expectations?

- RBA could announce a 25bps rate hike at its November meeting

- Hawkish bias could be maintained if quarterly forecasts revised higher

- Aussie/dollar’s current upleg could pick up speed after RBA meeting

- The meeting statement will be released on Tuesday at 03:30 GMT

RBA ready for action

The Reserve Bank of Australia is preparing for its 10th rate-setting meeting for 2023. It is shaping up to be the most interesting one in the current round of central bank meetings, as the RBA is widely expected to deliver a 25bps rate hike on Tuesday, raising its main cash rate to 4.35%.

The RBA was among the first central banks to pause in the current tightening cycle but, after three unchanged meetings, Governor Bullock et al look ready to hike again. To be fair, the RBA has been quite clear about its readiness to raise interest rates again and the minutes from the previous October 3 meeting supported this case. There was apparently a good discussion around another 25bps rate move at the last meeting but in the end most members agreed to wait for the early November gathering when new information on inflation and jobs would be available.

Quarterly inflation surprised on the upside

In this context, the incoming information since then has been on the stronger side. The inflation rate for the third quarter of 2023 came in at 5.4% YoY, slightly higher than anticipated, and the producer price index continues to show decent annual increases. Additionally, the comment that the “Board had low tolerance for a slower return of inflation to target”, which appeared in the last minutes, has also caught analysts' attention, fueling the current rate hike expectations.

Interestingly, most investment houses are expecting a rate hike on Tuesday. However, the same cannot be said for the market as it is assigning a meagre 56% probability for a November rate hike with the full 25bps rate move currently priced in by February 2024. It is quite rare for the market not to be fully onboard when analysts show a united front.

Quarterly RBA forecasts on Friday

Additionally, there is a strong possibility that the RBA could maintain its hawkish stance, even after announcing a rate hike. However, the degree of hawkishness will most likely depend on its quarterly forecasts. The last Statement on Monetary Policy published in August had 2025 inflation dropping to 2.8%.

While this is in line with the 2-3% inflation corridor targeted by the RBA, recent geopolitical developments and the decent consumer appetite could lead to an upwards revision in projected inflation. Should this be the case at Friday’s publication, the RBA could select to keep the door open for further rate hikes if needed going forward.

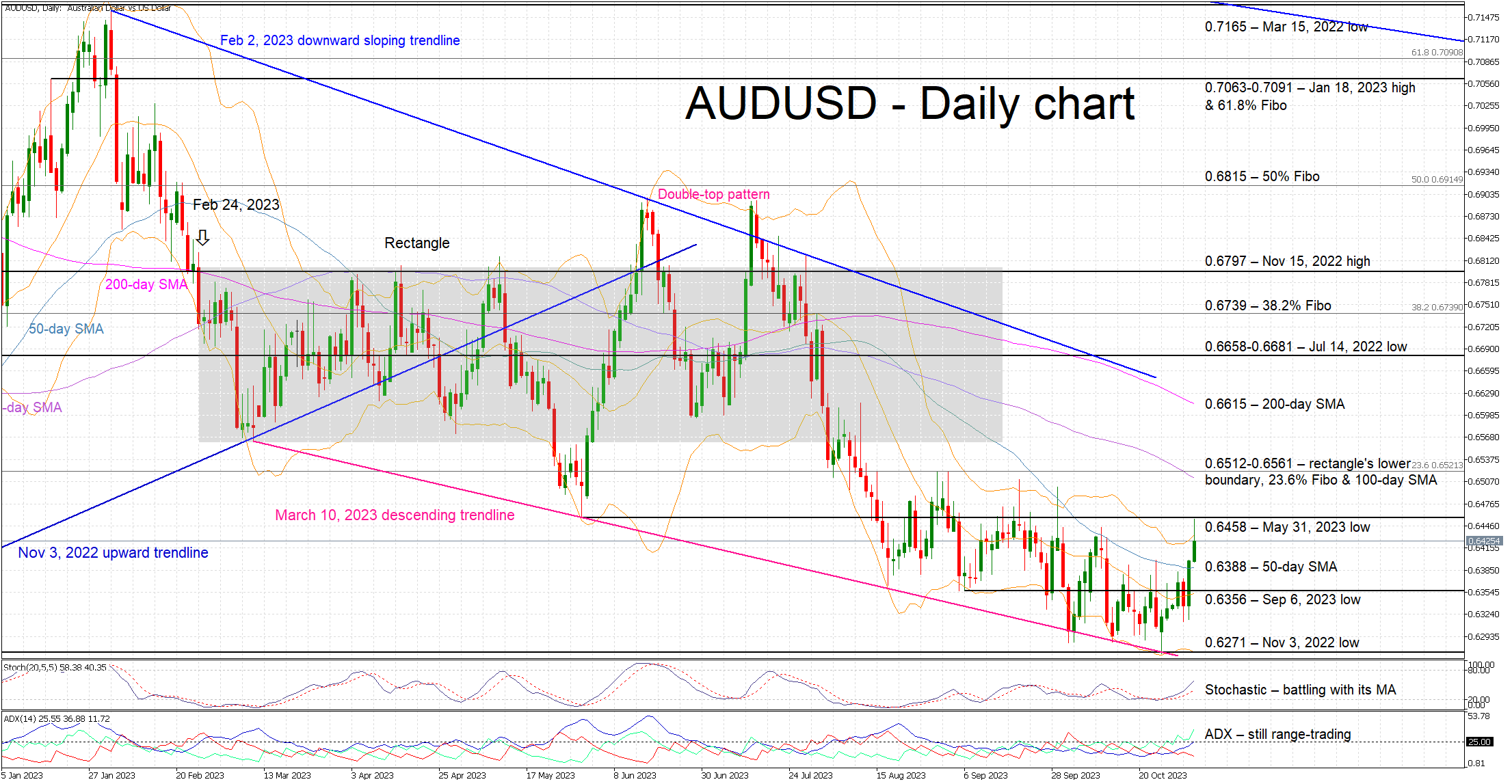

Aussie to benefit from a rate hike and a hawkish statement

The aussie has been under considerable pressure against the US dollar since the start of 2023. It recently traded at its lowest level for more than a year before the aussie bulls decided to stage a small upleg. The current move has stopped at the 0.6458 level but the combination of a 25bps rate and a hawkish statement could propel aussie/dollar towards the 0.6512-0.6561 area.

On the flip side, an RBA decision to postpone the rate hike for December could result in a stronger market reaction, with the aussie/dollar pair potentially dropping aggressively towards the November 3, 2022 low at 0.6271.

Weekly Focus – Halloween Did Not Spook Markets

Markets were not spooked by Halloween as equities climbed significantly higher while rates and the index of fear (the VIX) declined during the week. The market moves were driven by weaker US data, dovish market perceptions of the Fed, and a better outlook for the US treasury as it now expects to slow the pace of longer-term bonds issuance.

The Bank of Japan (BoJ) used Halloween to "trick or tweak" and tweaked its yield curve yield curve control policy (YCC) by redefining the 1% cap on 10-year JGB yields as a reference rather than a rigid bound. This was likely the last, step ahead of dismantling the YCC altogether. However, the BoJ still needs confirmation that inflation has sustainably moved above the 2% target before they are ready to take bigger steps to normalisation. They are slowly recognising higher inflation is not temporary and moved their inflation forecast significantly higher for the fiscal year 2024 to 2.8% from 1.9%.

Economic data from the US showed weaker than expected ISM manufacturing driven by lower new orders, production and employment, reversing some of the more positive signals seen over the past months. ADP employment change was also lower than expected, while JOLTs job openings continue to signal quite resilient labour markets. The latter was also visible in the Conference Board wage index that rose 1.2% in Q3 vs 1% in Q2.

The Federal Reserve decided, as expected, to keep the Fed Funds target range unchanged at 5.25-5.50%. Powell delivered a balanced message with dovish undertones. The recent strong labour market data that has lifted inflation expectations provided Powell an option to deliver a more hawkish message, but he did not consider it necessary and said that inflation expectations remain "in a good place".

In the euro area, inflation and GDP data corroborated the 'soft-landing' narrative. Headline inflation fell significantly again to 2.9% y/y from 4.3% and core inflation ticked down to 4.2% y/y from 4.5%. Base effects drove the yearly growth rate down but the underlying inflationary momentum again showed positive signs with core inflation increasing just 0.11% m/m s.a. from 0.17%. GDP growth in the third quarter was -0.1% q/q which is not a bad as one could fear given the significant monetary policy tightening.

In China, October PMIs from both NBS and Caixin disappointed. Manufacturing PMI fell to 49.5 (consensus 50.2) from 50.2 and service PMI dropped to 50.6 (consensus 52.0) from 51.7. The lower service PMIs raise concerns over the consumer engine in China.

Bank of England (BoE) left the bank rate unchanged at 5.25% in line with expectations. The BoE lowered growth and near-term inflation projections amid pushing back against market pricing of rate cuts. We continue to expect the peak in the Bank Rate to have been reached and see another rate hike as unlikely at this point.

Next week, focus is on comments from the Fed and the flash University of Michigan survey. In Japan, we look out for September wage figures while China releases trade data and CPI. The reserve bank of Australia meeting on Tuesday is interesting as market pricing is split 50/50 on the probability of a hike/ no hike. On Friday, we receive UK GDP.

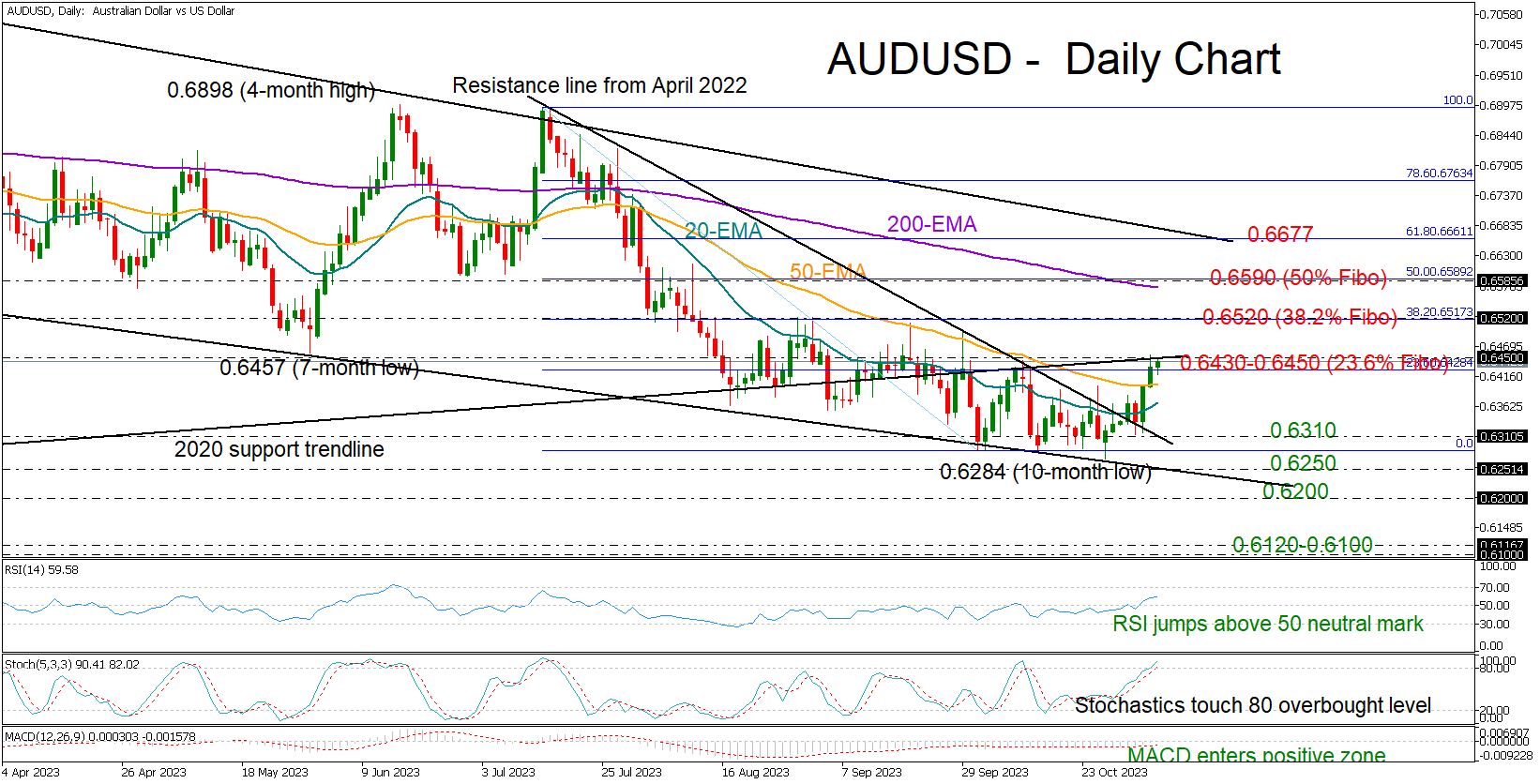

AUDUSD Overcomes Hurdles after NFP Miss

- AUDUSD breaks familiar resistance zone after dissapointing NFP data

- Technical signals improve, but some caution necessary

AUDUSD rose rapidly in the wake of a weaker-than-expected US jobs report, crossing above the long-term constraining line from the 2020 low at 0.6450 after a couple of failed attempts.

The RSI has finally advanced above its 50 neutral mark for the first time after three months, boosting optimism that the bulls could stay in play in the coming sessions. The rising MACD, which entered the positive area, is adding to the positive signals, but some caution is still necessary as the stochastic oscillator has already entered the overbought zone above 80, suggesting that the recent gains could be short-lived.

The 0.6520 zone, which overlaps with the 38.2% Fibonacci retracement of the latest downleg, is currently in target. Beyond that, the price could stabilize somewhere between its 200-day exponential moving average (EMA) and the 50% Fibonacci of 0.6590. Then, a more challenging battle could take place near the long-term resistance trendline from April 2022 at 0.6677.

In the event the bears squeeze the price back below the 0.6430-0.6450 area, the 20- and 50-day EMAs could immediately come to thre rescue ahead of the broken resistance trendline at 0.6310. Should selling forces persist, the price might next seek shelter around the protective falling line from March 2023 at 0.6250. A step lower could stabilize near the 0.6200 psychological mark or head for the 0.6120-0.6100 constraining zone.

Summing up, the latest upturn in AUDUSD is looking promising. An extension above the 0.6520 wall could add more fuel to the bull run.