Sample Category Title

Canada’s Labour Market Posts Modest Gain in October

The Canadian labour market added 17.5k positions in October, with full-time employment down 3.3k and part-time employment up 20.8k.

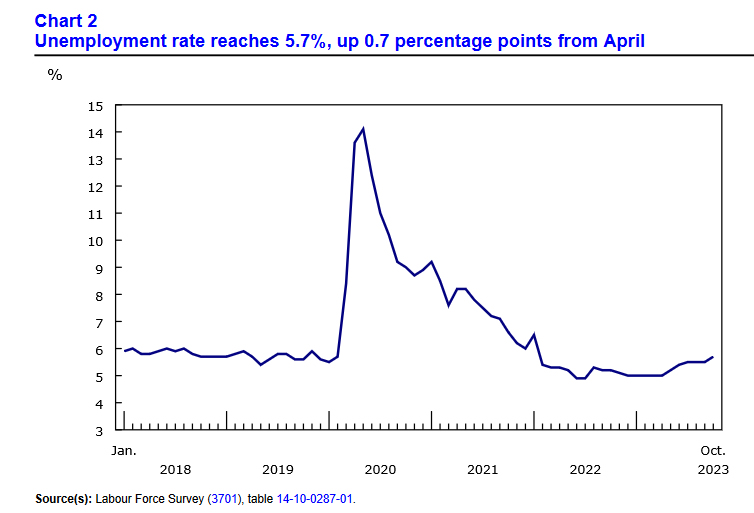

The unemployment rate rose 0.2 percentage points to 5.7% and the participation rate was unchanged at 65.6%.

Employment by sector showed gains in construction (+23k) and information, culture and recreation (+21) being offset by declines in wholesale and retail trade (-22k) and manufacturing (-19k).

Lastly, total hours worked were flat at 0.02% month-on-month and wages were up 4.8% year-on-year (versus 5.0% in September).

Key Implications

The Canadian jobs market is moving back towards balance following two strong monthly prints. The 18k monthly job gain once again failed to keep up with the 58k gain in the population-driven boost to the labour force. The "is this a recession?" debate will continue to swirl, with the unemployment rate rising by 0.7 percentage points since April. While this certainly isn't a recession as there is no depth, duration, or breadth, weakness is present. The number of unemployed workers keeps rising, while cyclically sensitive private sector hiring has been retreating for months.

When the Bank of Canada decided to hold rates at 5% last week, it did so because of a notable slowing in economic momentum. While this has been apparent in reduced consumer spending and a weakening housing market, the labour market left the BoC wanting more. But, given the rise in the unemployment rate and continued weakening in the underlying details, today's report is likely to make the BoC feel more comfortable about its decision to hold. Looking forward, we are expecting this employment trend to continue, while high rates and persistent inflation make the case for the BoC to remain on hold in December.

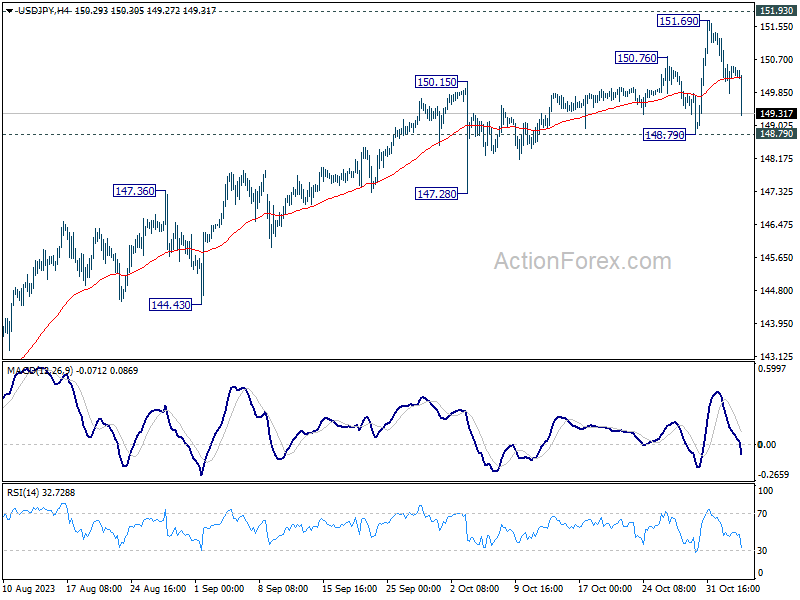

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.89; (P) 150.43; (R1) 151.02; More...

While USD/JPY's fall from 151.69 is extending, it's still holding above 148.79 support. Intraday bias remains neutral first. Price actions from 151.69 could still be seen as a consolidation pattern only. However, firm break of 148.79 will indicate rejection by 151.93 key resistance, and bring deeper fall through 147.28 support.

In the bigger picture, immediate focus is now on 151.93 resistance (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will argue that rise from 127.20 has completed, and turn outlook bearish for 137.22 support and below. However, sustained break of 151.93 will confirm resumption of long term up trend. Next target will be 61.8% projection of 102.58 to 151.93 from 127.20 at 157.69.

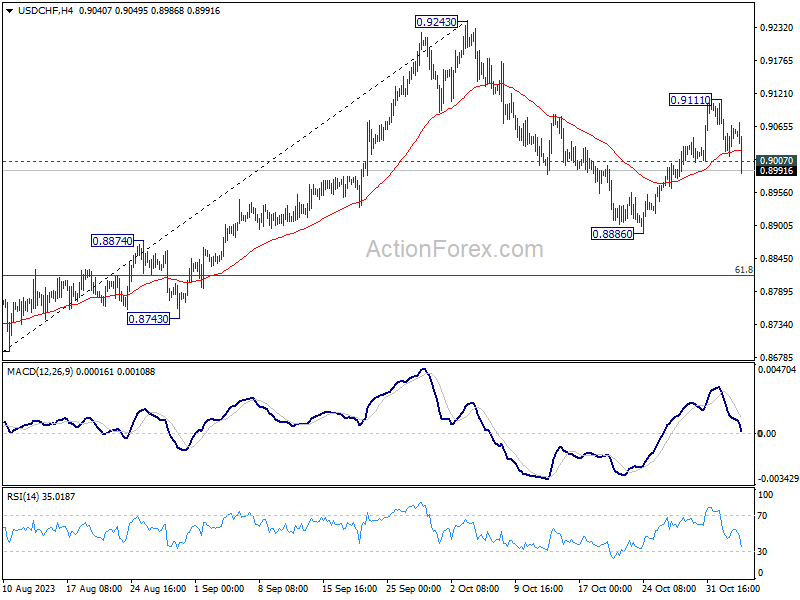

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9023; (P) 0.9054; (R1) 0.9089; More....

Break of 0.9005 support support argues that USD/CHF's rebound from 0.8886 has completed at 0.9111 already. Intraday bias is back on the downside for retesting 0.8886. Firm break there will resume whole fall from 0.9243 to 0.8815 fibonacci level. For now, risk will be on the downside as long as 0.9111 resistance holds, in case of recovery.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.9243. Yet there was no follow through selling after hitting 0.8886. On the upside, break of 0.9243 resistance will revive the case of medium term bottoming at 0.8851, and turn outlook bullish. However, sustained break of 61.8% retracement of 0.8551 to 0.9243 at 0.8815 will argue that larger decline from 1.0146 is ready to resume through 0.8551 low.

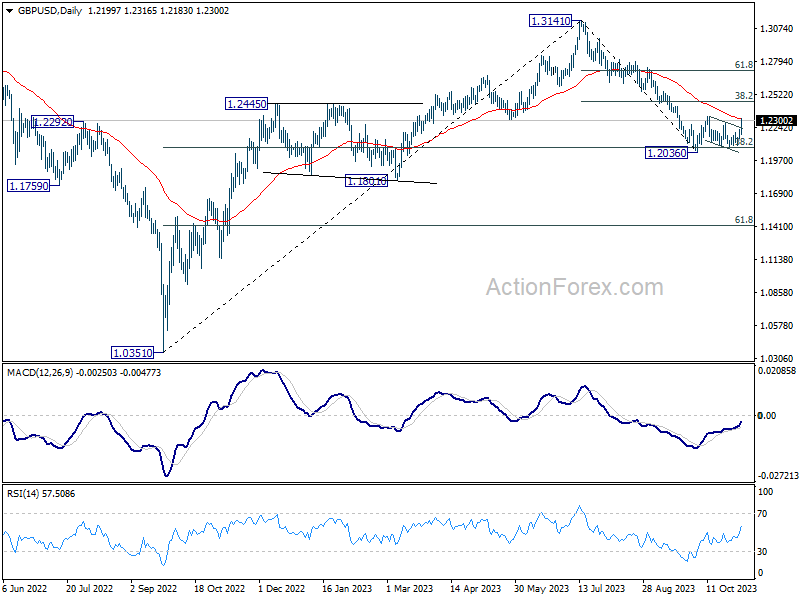

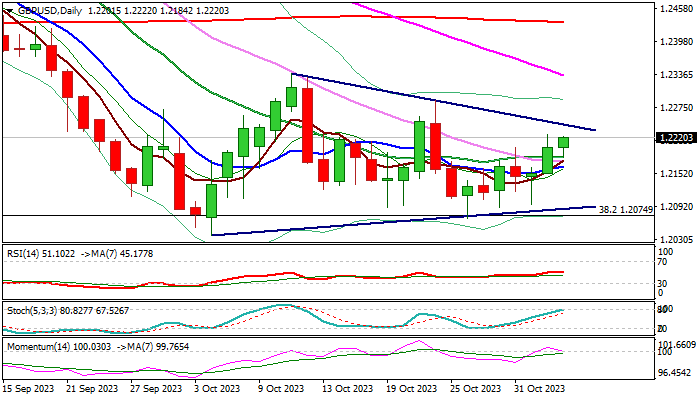

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2152; (P) 1.2189; (R1) 1.2240; More

Break of 1.2287 resistance argues that rebound from 1.2036 is resuming. Intraday bias is back on the upside for 1.2336 resistance first. Firm break there will target 38.2% retracement of 1.3141 to 1.2036 at 1.2458. On the downside, below 1.2184 minor support will turn intraday bias neutral first.

In the bigger picture, fall from 1.3141 medium term top could be viewed as part of a correction to rise from 1.0351 (2022 low). An interim bounce could be seen as the second leg of the pattern. But upside should be limited well below 1.3141 to start the third leg. Nevertheless, the pattern would be a range pattern as long as 38.2% retracement of 1.0351 to 1.3141 at 1.2075 holds.

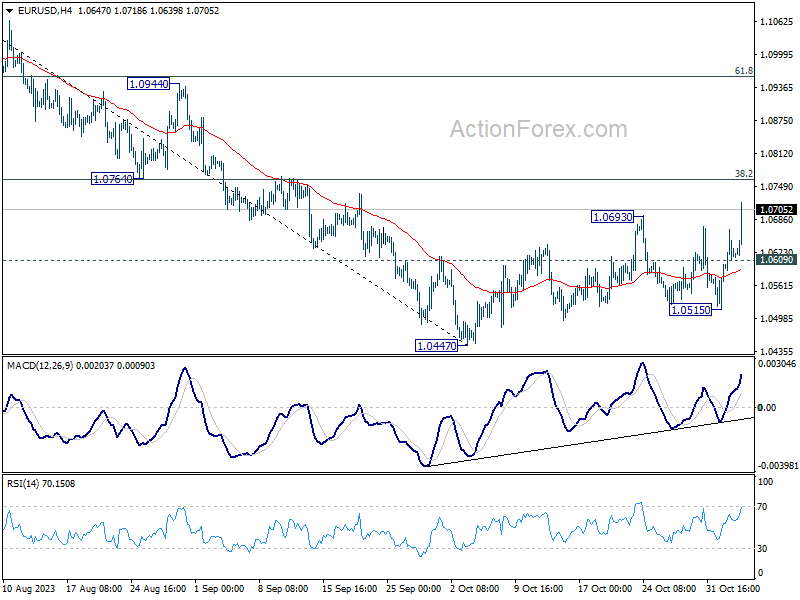

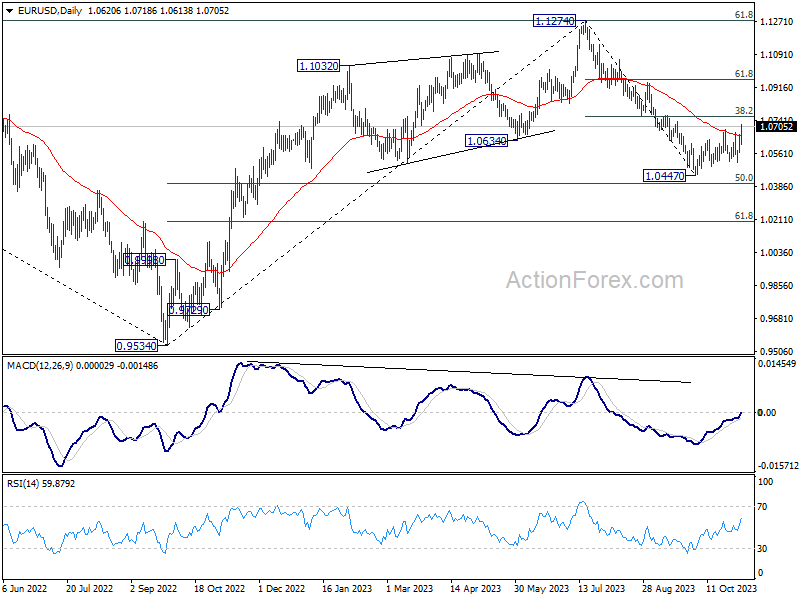

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0570; (P) 1.0619; (R1) 1.0672; More...

EUR/USD's rebound from 1.0447 resumed by breaking through 1.0693 resistance. Intraday bias is back on the upside for 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763). Decisive break there will pave the way to 61.8% retracement at 1.0958 next On the downside, below 1.0609 minor support will turn intraday bias neutral first.

In the bigger picture, fall from 1.1274 medium term top could be viewed part of a correction to rise from 0.9534 (2022 low). An interim bounce from current level, as the second leg of the pattern, cannot be ruled out. But upside should be limited well below 1.1274 resistance to start the third leg. The pattern would likely at least have a take on 61.8% retracement of 0.9534 to 1.1274 at 1.0199 before completion.

Disappointing NFP Data Fuels Market Optimism Dollar and Yields Tumble

Markets reacted with notable positivity to the latest US. non-farm payroll report, which showed weaker-than-expected growth in jobs, a higher unemployment rate, and subdued wage inflation. Stock futures leaped as the data appeared to assuage investor concerns about further tightening by Fed. In a sharp response, 10-year Treasury yield plunged through 4.55% level, exacerbating the week's precipitous decline and signalling a potential shift in investor expectations regarding the trajectory of interest rates. Dollar experienced a broad sell-off, intensifying its decline for the week.

While Canadian dollar was burdened by its own disappointing employment figures, it nevertheless surged against Dollar, reflecting the greenback's broad weakness. Meanwhile, New Zealand and Australian dollars emerged as the strongest performers for the day, buoyed not only by the narrowing yield differential but also by a surge in risk appetite.

Euro and Sterling capitalized on Dollar's weakness, with both currencies making substantial gains. Conversely, Yen and Swiss Franc were notable laggards in the currency markets, potentially due to their status as safe havens which are less attractive in an environment where risk sentiment is on the rise.

In Europe, at the time of writing, FTSE is down -0.02%. DAX is up 0.44%. CAC is up 0.15%. Germany 10-year yield is down -0.062 to 2.659. Earlier in Asia, Nikkei rose 1.10%. Hong Kong HSI rose 2.52%. China Shanghai SSE rose 0.71%. Singapore Strait Times rose 1.98%. Japan 10-year JGB yield dropped -0.0433 to 0.916.

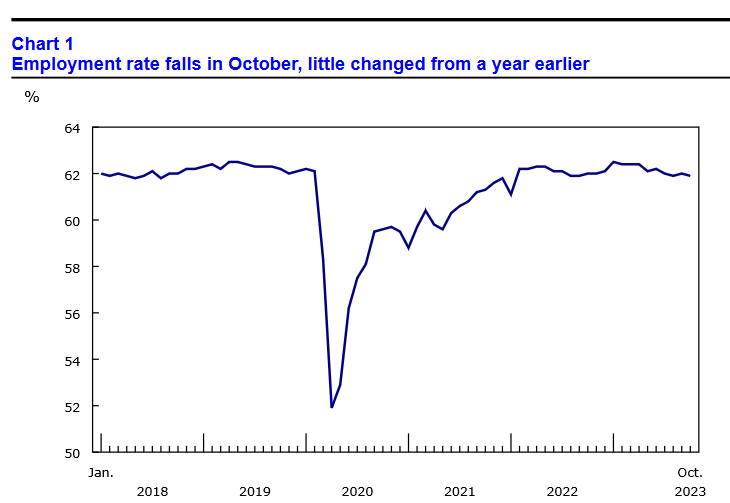

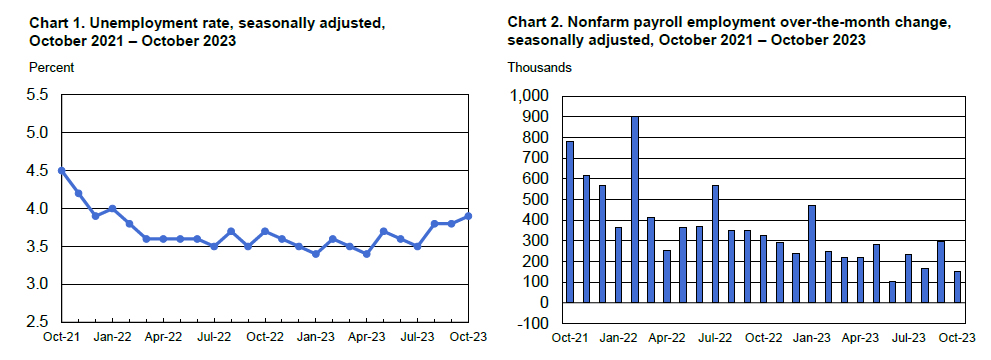

US NFP grows 150k, unemployment rate rose to 3.9%

US non-farm payroll employment grew 150k in October, below expectation of 172k. That's well below average monthly gain of 258k over the prior 12 months.

Unemployment rate rose from 3.8% to 3.9%, above expectation of being unchanged at 3.8%. Participation rate dropped from 62.8% to 62.7%.

Average hourly earnings rose 0.2% mom, below expectation of 0.3% mom. Over the 12 months, average hourly earnings rose 4.1% yoy.

Canada's employment grew 17.5k, unemployment rate rose to 5.9%

Canada's employment grew 17.5k in October, below expectation of 25.7.

Employment was up in construction (+23,000; +1.5%) and information, culture and recreation (+21,000; +2.5%) in October. This was offset by decreases in wholesale and retail trade (-22,000; -0.7%) and manufacturing (-19,000; -1.0%).

Unemployment rate rose from 5.7% to 5.9%, above expectation of 5.8%.

On a year-over-year basis, average hourly wages rose 4.8% yoy in October, following an increase of 5.0% yoy in September.

Eurozone unemployment rate rose to 6.5%, EU unchanged at 6.0%

Unemployment rate in Eurozone ticked up in September, rising to 6.5% from the previous month's 6.4%. This uptick defied market expectations that the unemployment rate would hold steady.

Despite the month-over-month increase, the broader picture shows a labor market that has seen a significant year-over-year improvement, with Eurozone unemployment shrinking by -212k compared to September 2022. However, the monthly rise in unemployment, with 69k more individuals without work in the Eurozone, suggests that the region's labor market might be facing new challenges as it enters the final quarter of the year.

The EU-wide unemployment rate remained constant at 6.0%, underscoring a more stable job market situation across the broader European Union. Nevertheless, the total number of unemployed persons in the EU rose by 95k month-over-month, bringing the number to approximately 13.026m, of which 11.017m are within the Eurozone.

UK PMI services finalized at 49.5, shallow downturn persists

UK PMI Services index was finalized at to 49.5 in October up fractionally from 49.3 in September, lingering in contraction territory for the third consecutive month. PMI Composite showed a minor improvement to 48.7 from an 8-month nadir of 48.5

Economics Director at S&P Global Market Intelligence, Tim Moore, highlighted, "A shallow downturn in UK service sector activity persisted in October as businesses struggled to make headway against a backdrop of worsening domestic economic conditions and stretched household budgets."

The outlook remains cautious at best. "Forward-looking survey indicators suggested that service providers will continue to skirt with recession," said Moore, noting that business optimism has dipped to its lowest point of the year.

On the brighter side, there was a silver lining with a slight uptick in new export sales. Furthermore, input cost inflation showed signs of easing, reaching its softest point in over two years due to reduced raw material prices and supplier discounting.

Nevertheless, this hasn't stopped businesses from hiking prices. "Higher wages and fuel bills were still passed on to clients, which resulted in the strongest increase in average prices charged inflation for three months," Moore explained.

China Caixin PMI services ticks to 50.4, composite fell to 50

China's service sector showed a glimmer of resilience in October, with Caixin PMI Services edging up marginally from 50.2 to 50.4, meeting expectations. However, this slight uptick could not buoy the overall PMI Composite, which leveled at the neutral 50.0 threshold, down from 50.9 in the previous month.

The slight uptick in the services sector was overshadowed by a dip in manufacturing (which fell from 50.6 to 49.5). The details reveal a mixed scenario: composite new business inched forward at its weakest pace in ten months. Service providers and goods producers alike witnessed decelerated growth in sales.

Employment trends also painted a picture of caution. There was a small overall decline in jobs, with manufacturing bearing the brunt through more pronounced job losses, while employment in the service sector hit a plateau.

On the pricing front, inflationary pressures were somewhat contained. Input costs across the combined sectors rose modestly, maintaining a muted pattern of cost escalation. Despite this, firms nudged their selling prices upwards, continuing a trend that could suggest confidence in passing on costs, albeit the rate of charge inflation was just marginally lower than the 18-month peak seen in September.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0570; (P) 1.0619; (R1) 1.0672; More...

EUR/USD's rebound from 1.0447 resumed by breaking through 1.0693 resistance. Intraday bias is back on the upside for 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763). Decisive break there will pave the way to 61.8% retracement at 1.0958 next On the downside, below 1.0609 minor support will turn intraday bias neutral first.

In the bigger picture, fall from 1.1274 medium term top could be viewed part of a correction to rise from 0.9534 (2022 low). An interim bounce from current level, as the second leg of the pattern, cannot be ruled out. But upside should be limited well below 1.1274 resistance to start the third leg. The pattern would likely at least have a take on 61.8% retracement of 0.9534 to 1.1274 at 1.0199 before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:45 | CNY | Caixin Services PMI Oct | 50.4 | 50.4 | 50.2 | |

| 07:00 | EUR | Germany Trade Balance (EUR) Sep | 16.5B | 16.3B | 16.6B | 17.7B |

| 07:45 | EUR | France Industrial Output M/M Sep | -0.50% | 0.00% | -0.30% | -0.10% |

| 09:30 | GBP | Services PMI Oct F | 49.5 | 49.2 | 49.2 | |

| 10:00 | EUR | Eurozone Unemployment Rate Sep | 6.50% | 6.40% | 6.40% | |

| 12:30 | USD | Nonfarm Payrolls Oct | 150K | 172K | 336K | 297K |

| 12:30 | USD | Unemployment Rate Oct | 3.90% | 3.80% | 3.80% | |

| 12:30 | USD | Average Hourly Earnings M/M Oct | 0.20% | 0.30% | 0.20% | 0.30% |

| 12:30 | CAD | Net Change in Employment Oct | 17.5K | 25.7K | 63.8K | |

| 12:30 | CAD | Unemployment Rate Oct | 5.70% | 5.60% | 5.50% | |

| 13:45 | USD | Services PMI Oct F | 50.9 | 50.9 | ||

| 14:00 | USD | ISM Services PMI Oct | 53.2 | 53.6 |

Canada’s employment grew 17.5k, unemployment rate rose to 5.9%

Canada's employment grew 17.5k in October, below expectation of 25.7.

Employment was up in construction (+23,000; +1.5%) and information, culture and recreation (+21,000; +2.5%) in October. This was offset by decreases in wholesale and retail trade (-22,000; -0.7%) and manufacturing (-19,000; -1.0%).

Unemployment rate rose from 5.7% to 5.9%, above expectation of 5.8%.

On a year-over-year basis, average hourly wages rose 4.8% yoy in October, following an increase of 5.0% yoy in September.

US NFP grows 150k, unemployment rate rose to 3.9%

US non-farm payroll employment grew 150k in October, below expectation of 172k. That's well below average monthly gain of 258k over the prior 12 months.

Unemployment rate rose from 3.8% to 3.9%, above expectation of being unchanged at 3.8%. Participation rate dropped from 62.8% to 62.7%.

Average hourly earnings rose 0.2% mom, below expectation of 0.3% mom. Over the 12 months, average hourly earnings rose 4.1% yoy.

GBP/USD: Cable Stands at the Front Foot ahead of US Labor Report

GBPUSD remains steady in European trading on Friday and attempts above 1.22 mark, in extension of Thursday’s rise, sparked by BOE’s decision, which markets saw as a hawkish hold.

Better than expected UK Oct Services PMI (although the sector contracts for the fourth consecutive month) added support to sterling as markets await release of key US labor report.

Non-farm payrolls are expected to rise by 180K in Oct compared to 336K new jobs added in Sep, average earning forecasted to tick up (Oct 0.3% m/m vs Sep 0.2%) and unemployment to stay unchanged at 3.8%.

Any stronger divergence of NFP numbers from forecasts would generate direction signal, with pound seen benefiting from weaker numbers, while jump above consensus would put the pair under pressure.

Initial support lays at 1.2175 (session low / 20DMA), followed by Thursday’s low (1.2152) and pivotal trendline support (1.2090) loss of which will be bearish.

Upper triangle boundary offers initial resistance at 1.2236, ahead of Oct 24 spike high at 1.2288 and Oct 11 top / falling 55DMA at 1.2337, violation of which to bring bulls fully in play.

Res: 1.2236; 1.2288; 1.2337; 1.2410.

Sup: 1.2175; 1.2152; 1.2080; 1.2069.

Research US – Bond Yields Headed Lower Towards 2024

Bond market outlook remains blurred by high issuance, debt sustainability worries as well as uncertainty over economic outlook and inflation. We continue to forecast lower long-end yields, but less than previously.

We see 10y UST yield at 4.20% in 12M horizon (from 3.70%). We also revise up our US GDP forecast to 2.4% for 2023 (from 2.1%) and 1.1% for 2024 (from 0.9%), reflecting stronger realized data but still weak outlook.

10Y UST yields have generally traded in the 4.80-5.00% range over the past weeks, but broke below the recent range following the November FOMC Meeting. Yields remain caught in crosswinds stemming from data, market dynamics and monetary policy. On the latter, Powell struck a rather balanced tone at the press conference following yesterday's FOMC meeting, emphasising that the committee sees progress on inflation/labour market data but is not yet convinced that financial conditions are sufficiently restrictive. Wage growth remains elevated, excess labour demand is still present and growth continues to surprise to the upside. The 'high for longer' narrative has clearly been adopted by markets.

Apart from data and monetary policy, bond markets remain highly impacted by supply/demand dynamics encapsulated in the move up in the Term Premium since the summer. The US debt outlook is in centre of these discussions, after the Treasury's sizeable upward revision of expected issuance in August. However, recent announcements on issuance have brought some calm to markets.

Earlier this week, the Treasury lowered its expected issuance for the remainder of the year, while signalling that the cash buffer (TGA) is now sufficiently refilled after being drained in the lead up to the debt ceiling resolution in June. According to the Quarterly Refunding Statement out Wednesday, issuance for the remainder of the year will mainly pick up at the belly of curve, while selling in the long-end will decline marginally in December and January. A continued high share of T-Bills in the issuance profile indicates, that the short end will continue to bear a significant share of US deficit burden. Markets had clearly feared a more significant amount of duration to accommodate in the short run.

On the demand side, investors still seems cautious to take on more duration risk in the current situation. Powell mentioned in his speech at The Economic Club of New York earlier this month that the FOMC is looking at the current positive bond/equity correlation as a potential driver of Term Premia. Bonds have become less useful for hedging risk. Bonds and equities share a common exposure to inflation, and historically the two have correlated positively in decades characterized by elevated price pressures as the 1970s and 1980s. As economic growth slows and inflationary risks dampen, the positive correlation will likely recede gradually from here.