Sample Category Title

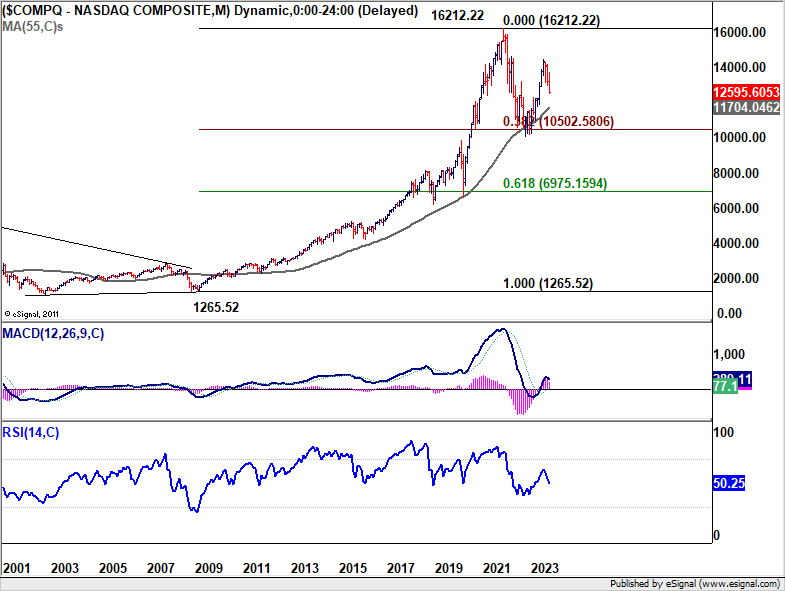

NASDAQ set for deeper selloff as key support shattered

US stocks underwent a marked decline overnight, with NASDAQ at the forefront, shedding -1.76% of its value. This follows closely on the heels of Wednesday's downturn, where the tech-driven index recorded its most significant single-day loss in eight months, plummeting by -2.5%. Notably, several pivotal technical support have been violated, hinting that we might be witnessing the onset of a medium-term downtrend in NASDAQ.

Interestingly, the strong US Q3 GDP figures released overnight did little to lift investor spirits. Paradoxically, these robust economic indicators are fueling concerns about Fed maintaining higher interest rates for an extended period, rather than providing reassurance to the markets.

On the technical front, NASDAQ has taken out both 38.2% retracement of 10088.82 to 14446.55 at 12781.89 and 55 W EMA (now at 12826.98). These developments lend notion to the hypothesis that the entire rally from 10088.82 has concluded. Additionally, the break of channel support suggests that the index may be entering a phase of downside acceleration. For the near term, outlook will stay bearish as long as 13170.39 resistance holds. Next target is 61.8% retracement at 11753.47.

In a broader context, rise from 10088.82 (2022 low) is seen as the second leg of the corrective pattern from 16212.22 (2021 high). In a less bearish scenario, the fall from 14446.55 could merely be a correction to rise from 10088.82. In this case, significant support might emerge around the 55 M EMA (now at 11704.04), close to the aforementioned fibonacci level, triggering a substantial bounce.

However, in a gloomier perspective, the decline from 14446.55 might represent the third leg of the corrective pattern from 16212.22. This would suggest a more significant and persistent decline, plummeting below 10088.82. While it's premature to definitively conclude, market's reaction around 11700 level should provide valuable insights into future trends.

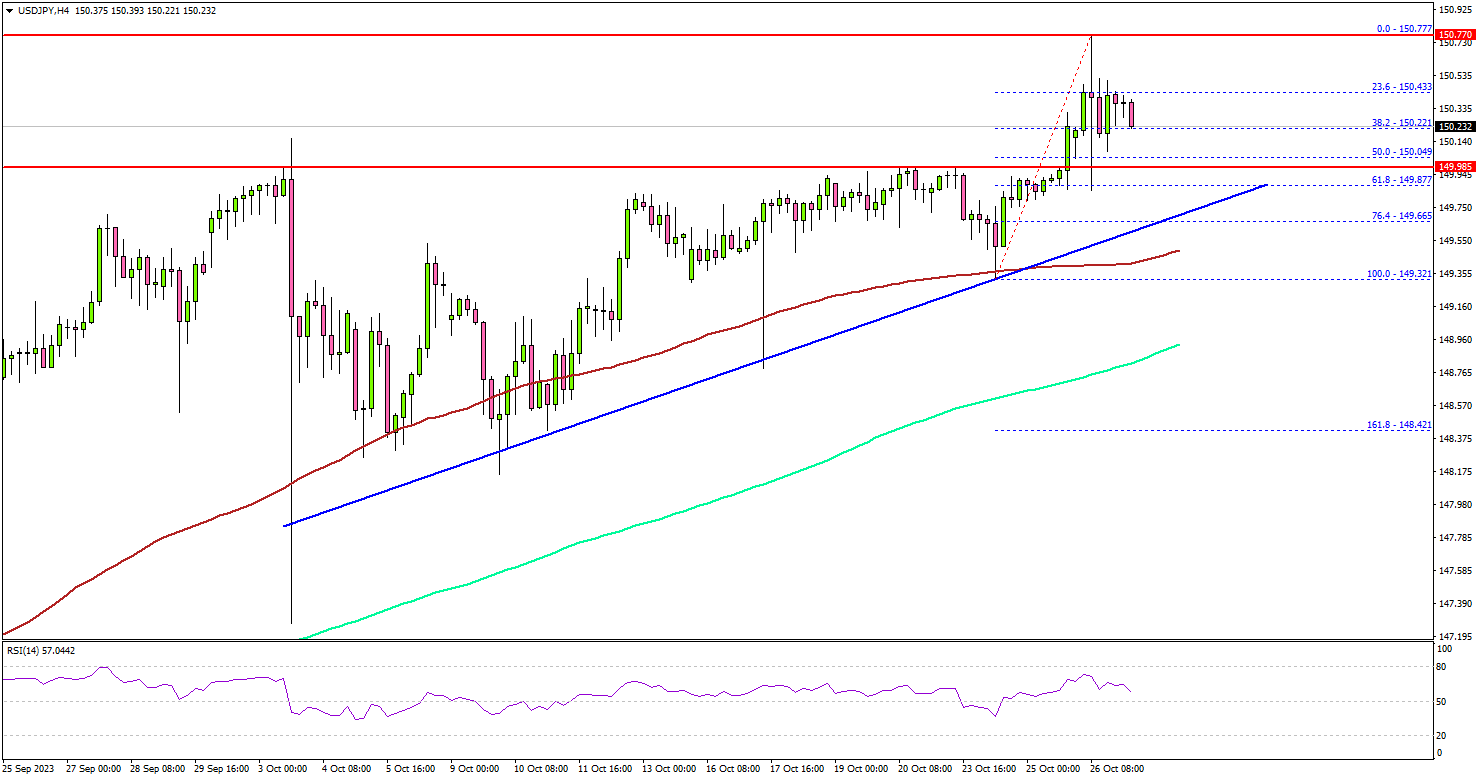

USD/JPY Targets Fresh ATH, US GDP Grows 4.9%

Key Highlights

- USD/JPY broke the 150.00 resistance and remains in a positive zone.

- A crucial bullish trend line is forming with support near 149.80 on the 4-hour chart.

- EUR/USD and GBP/USD turned lower and might extend losses.

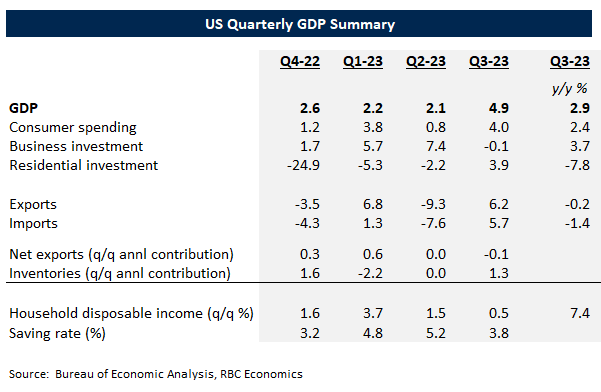

- The US GDP grew 4.9% in Q3 2023 (Prelim), more than the market forecast of 4.2%.

USD/JPY Technical Analysis

The US Dollar remained in a strong uptrend above the 148.50 level against the Japanese Yen. USD/JPY gained bullish momentum and broke the 150.00 resistance.

Looking at the 4-hour chart, the pair settled well above the 149.20 support, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

It traded as high as 150.77 before there were swing moves. However, the pair remained well supported above the 149.20 support. There is also a crucial bullish trend line forming with support near 149.80 on the same chart.

On the upside, the pair might face resistance near the 150.80 level. If there is a clear move above 150.80, the pair could rise toward the 151.40 resistance. The next key resistance is near 152.00, above which the pair could rise toward the 155.00 level.

If there is a fresh decline, the pair might find bids near 150.00. The next key support is seen near the trend line at 149.80, below which it could test the 100 simple moving average (red, 4 hours) at 149.20. Any more losses might send the pair toward the 148.80 level.

Looking at EUR/USD, the pair struggled to recover and remains at risk of more downsides below the 1.0500 support.

Fundamentally, the US Gross Domestic Product Annualized report was released by the US Bureau of Economic Analysis. The market was looking for a 4.2% rise in the GDP in Q3 2023 (Prelim).

The actual result surpassed the market expectations, as the US Gross Domestic Product grew 4.9% in Q3 2023, the first estimate showed on Thursday.

Economic Releases

- US Personal Income for Sep 2023 (MoM) - Forecast +0.4%, versus +0.4% previous.

Tokyo CPI signals rising inflation; BoJ likely to upgrade forecasts

In Japan, Tokyo's headline CPI unexpectedly accelerated from 2.8% yoy to 3.3% yoy in October. CPI core, which excludes the volatile prices of fresh food, also witnessed an acceleration, moving from 2.5% yoy to 2.7% yoy. On the other hand, CPI core-core, which strips out impact of both food and energy prices, marginally slowed from 3.9% yoy to 3.8% yoy, but remained elevated.

An important metric to note is acceleration in services prices, which went from 1.9% yoy 2.1% yoy. The continued uptick in services inflation indicates a more entrenched and broad-based price pressure scenario, suggesting that it could be a prolonged period before inflation retraces its steps back below BoJ's 2% target.

Considering that consumer inflation in Tokyo often sets the tone for national trends, the data bolsters the anticipation that BoJ might have to upgrade its inflation forecasts. Market participants are now keenly awaiting the fresh quarterly projections that are expected to be unveiled at BoJ's policy meeting next week.

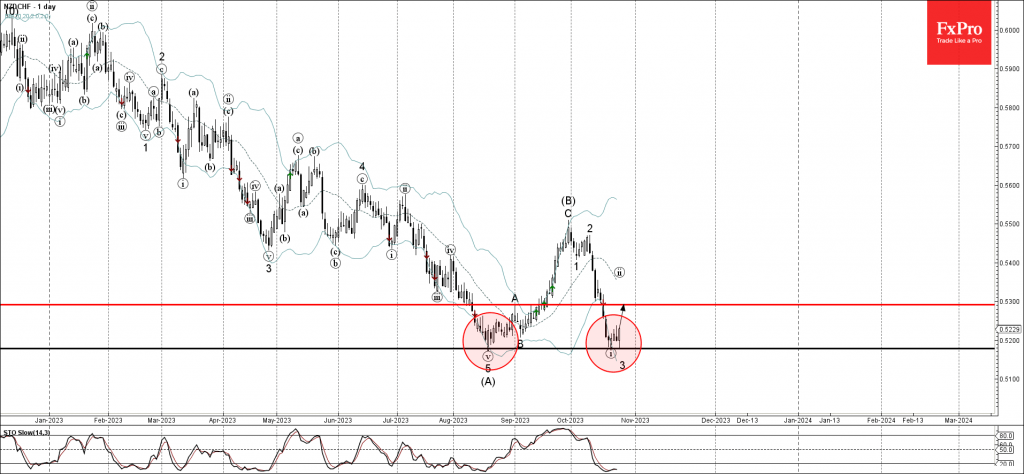

NZDCHF Wave Analysis

- NZDCHF reversed from key support level 0.5180

- Likely to rise to resistance level 0.5300

NZDCHF currency pair recently reversed up from the key support level 0.5180 (which stopped the prolonged daily downtrend in August as can be seen below).

The support level 0.5180 was further strengthened by the lower daily Bollinger Band.

Given the strength of the support level 0.5180 and the oversold daily Stochastic, NZDCHF currency pair can be expected to rise further toward the next resistance level 0.5300.

USDCAD Wave Analysis

- USDCAD broke key resistance level 1.3790

- Likely to rise to resistance level 1.3950

USDCAD previously broke above the key resistance level 1.3790 (which has been steadily reversing the pair from last October).

The breakout of the resistance level 1.3790 accelerated the active minor ABC correction 2 from the middle of July.

Given the continued USD bullishness, USDCAD can be expected to rise further toward the next resistance level 1.3950 (which stopped the daily uptrend in 2022, top of the active daily up channel).

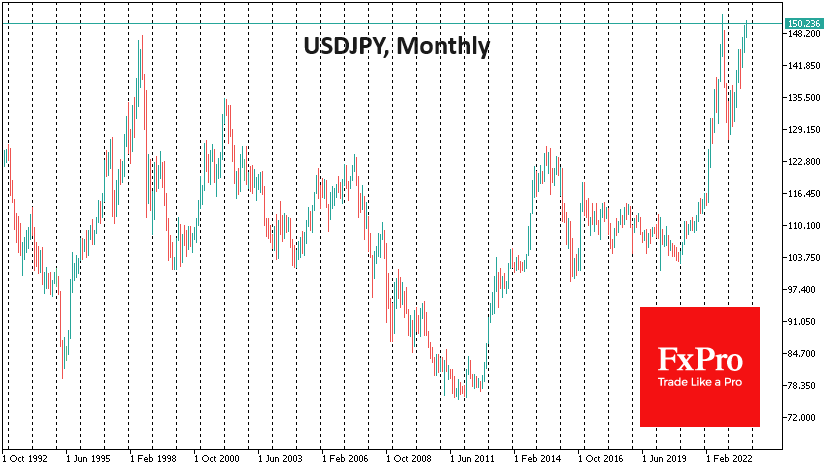

USDJPY Above 150, But Don’t Expect Repeat of Last Year’s Interventions

A strengthening US dollar pushed the USDJPY to 150.77 early Thursday. Except for just over 20 hours on 21 October 2022, the pair hasn’t traded higher since 1990.

Almost a year ago, a breach of the round 150 level triggered a decisive intervention by the Japanese Ministry of Finance, breaking the pair’s bullish trend and pushing it back below 128 less than three months later.

Considering this history, the market failed to break through this round level, approached in early October. There were many sharp spikes in Yen gains during the month, raising whether these were interventions initiated by the Japanese Ministry of Finance. In contrast to developments last year, the short-term spikes were not followed by a continuation, raising doubts about the authorities’ resolve.

There is a risk that it is not in Japan’s interest to repeat last year’s actions. The authorities are not targeting a specific level but are assessing volatility and the impact of the exchange rate on inflation. Sharp movements in the exchange rate undermine economic activity, forcing exporters and importers to postpone transactions to a point of equilibrium if possible. This is why we often hear from officials that large exchange rate movements are undesirable. However, intervention only increases this volatility.

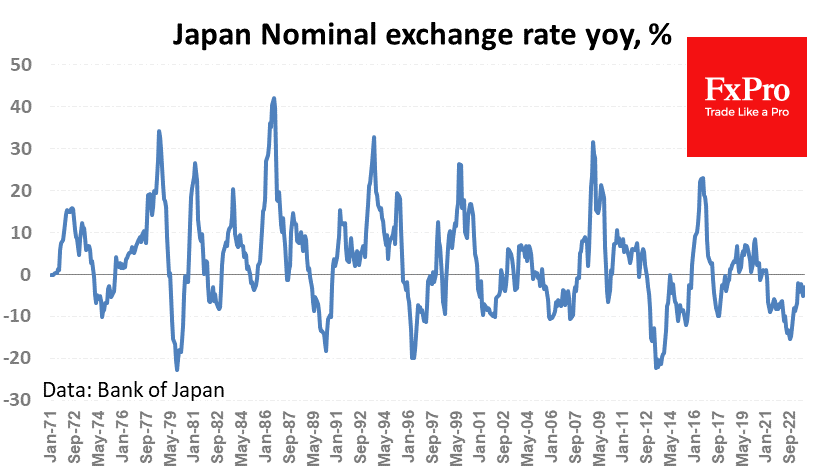

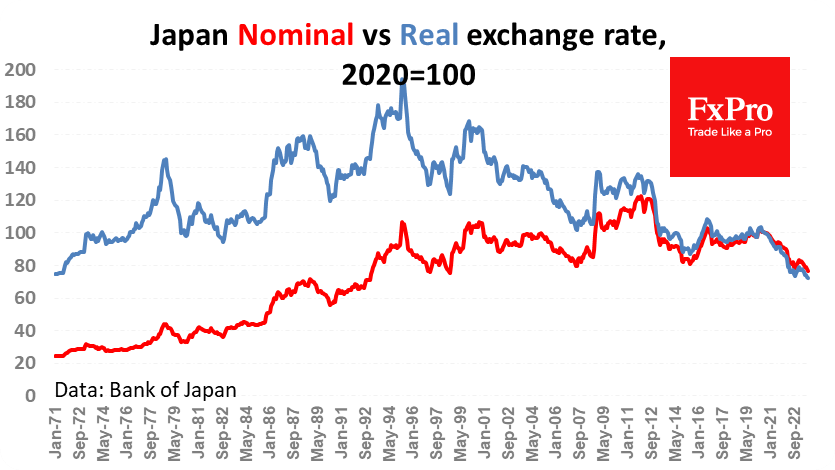

The impact on inflation is not the nominal yen exchange rate but the change compared with a previous period, such as a year ago. A year ago, the nominal yen exchange rate against a trade-weighted basket depreciated by 15% y/y; now, it is down by only 3% y/y, which means that its contribution to inflation is close to zero, although it is not an inflation-fighting regime.

So, it is possible that the enormous focus on the yen at 150 by traders and FX market commentators has not resonated in the hearts of Japan’s policymakers, who see no immediate need to intervene in the situation, especially as it is not free.

Unlike intervention to weaken the local currency, attempts to support the exchange rate are backed by the sale of foreign exchange reserves, depleting the country’s reserves. To make matters worse, the value of US government bonds (the most liquid instrument for intervention) has fallen sharply in recent months.

So, at current levels, it is safer to expect Japan’s MoF to turn the tide with intervention but will only limit USDJPY gains, even though the real effective yen exchange rate is at its lowest since 1970.

ECB Review: Not Rocking the Boat

- As expected, ECB kept policy rates unchanged at today's meeting and guided that they are done with additional rate hikes.

- Lagarde seemed to be on a mission not to rock the boat in terms of market pricing, she succeeded well and gave indications that this was a stock taking meeting only.

- Lagarde highlighted uncertainty about the economic outlook and remained confident that inflation would return to the target if rates were maintained for a sufficiently long duration at the current level, based on today's inflation. Surprisingly, no discussion took place today on advancing the full end to PEPP reinvestments.

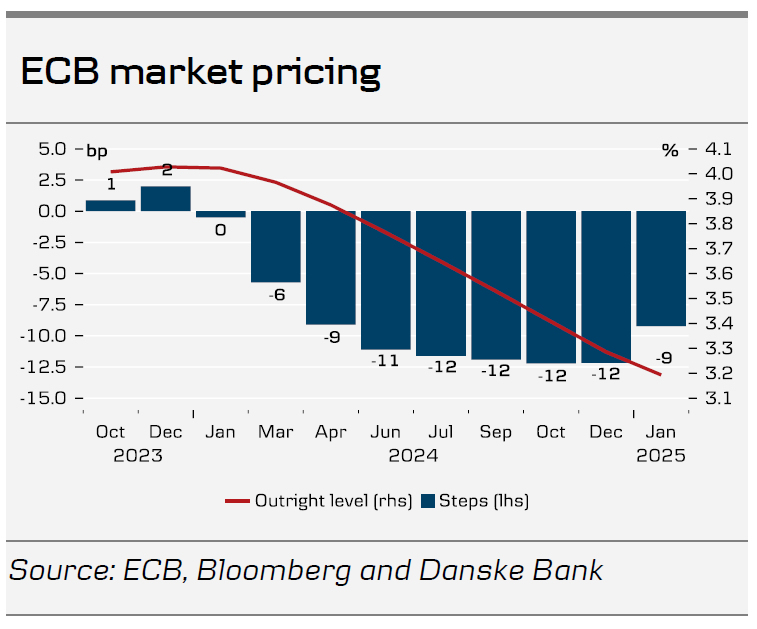

- The outcome was marginally on the dovish side of expectations and led to a minor dovish market reaction to the ECB decision and the press conference, which was supported by US data release along the way. Markets are pricing the first full rate cut in June next year.

Unchanged in uncertainty

For the first time since June last year, ECB decided to leave policy rates unchanged following their guidance in September. While ECB said that inflation is still expected to stay too high for too long and domestic price pressures remain strong, they nevertheless highlighted the inflation dropped 'markedly' in September due to base effects as well as underlying inflation pressures continue to ease. ECB guided that the inflation would return to target if rates were maintained at sufficiently restrictive levels. While Lagarde said that they do not rule out a further rate hike could come, she nevertheless made clear that such rate hike is not expected.

Stock taking meeting.

We conclude that today's meeting was more about stock taking that than sending new policy signals. Highlights were made on the transmission of the monetary policy to the real economy where not least the President Lagarde and VP de Guindos said that the recent rise in yields stemmed from outside the euro area and didn't reflect fundamentals and hence spill-overs and potential a fear of more coming needs to be taking into account.

Inflation is still expected to stay too high for too long

Lagarde acknowledged that the incoming data since the September meeting have been broadly as expected. Hence, the ECB has not changed its assessment of the economic situation and the inflation outlook since the last meeting. Lagarde characterised the current economic environment as weak especially due to the manufacturing sector. The labour market is currently supporting activity. Yet, there are signs that it is weakening also in the service sector. The service sector is weakening as industrial activity is spilling over and the higher interest rates are broadening out to the economy. The economic activity will remain weak the rest of the year and then likely recover, as household's real income increases (also on the back of lower inflation) and rising foreign demand will give strength to activity in the coming years.

Lagarde reiterated that risks to the economic outlook are tilted to the downside due to potentially stronger monetary policy transmission, weaker external demand, and geopolitical risks. Regarding inflation, the upside risks are higher than expected energy prices, wage increases and corporate profits. Overall, the higher than usual uncertainty surrounding the outlook prevails.

Muted FX reaction as expected

EUR/USD was more or less unaffected by the ECB decision, trading in the mid 1.0500- 1.0600 range. After the move just shy ahead of 1.0700 in the beginning of the week, the past couple of days the USD has regained strength on rising US yields, still remarkably strong US data and very weak euro area PMIs.

Overall, we make no changes to our long-term EUR/USD forecast and therefore, we maintain our strategic case for a lower EUR/USD based on relative terms of trade, real rates and relative unit labour costs. We forecast the cross at 1.06/1.03 in 6/12M. In the near-term, we stick to our topside risk call in EUR/USD. We expect a turnaround in the exceptional run of positive US economic data surprises to weigh on the USD. Additionally, we believe that peak policy rates, improvements in the struggling manufacturing sector, and a bottoming out of China-pessimism will provide some support to EUR/USD in the nearterm. The risks primarily consist of an escalation in the Middle East, leading to both a riskoff sentiment and higher energy prices, resulting in a stronger USD.

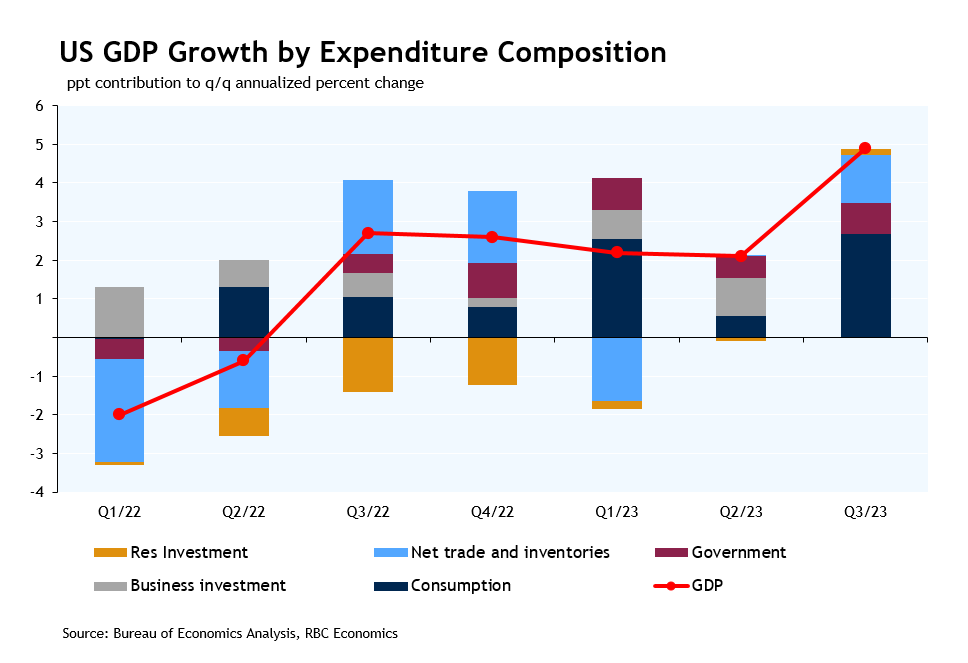

U.S. Economy Defied Gravity in Q3 with 4.9% GDP Gain

Third quarter U.S. GDP remained exceptionally strong, accelerating to an annualized rate of 4.9%. That was also the fifth consecutive increase since Q2/22 and largest since Q4/21.

A jump in the volatile inventory component accounted for about a quarter of the overall GDP gain. And residential investment surprised to the upside in Q3 (+3.9%), posting an increase after nine quarterly declines.

Consumer spending remained very strong, rising 4.0% in Q3, driven by broadly-based growth across goods (+4.8%) and services (+3.6%).

Still, household purchasing power showed further signs of deteriorating. Household after-inflation disposable income declined outright for the first time since Q3/23 and saving rate fell further below pre-pandemic levels. That is consistent with lower wage growth and slower hours worked growth over the summer.

Business investments on structures continued to climb higher, but at slower pace compared to the previous quarter, equipment investments declined by 3.8% in Q3. And net trade contributed little to growth.

Bottom line: Today’s GDP number indicates the U.S. economy still performed remarkably well in Q3, led by resilient household spending. Still, much of that strength came from another decline in remaining ‘excess’ savings accumulated during the pandemic – the household saving rate was still below pre-pandemic levels in Q3, and down from Q2. We continue to expect consumer spending to slow moving forward as higher interest rates and prices erode household purchasing power. Labour market conditions are also still exceptionally firm, but wage growth has ticked lower since June and lower job openings are flagging a pullback in hiring demand under the surface. We continue to expect the GDP growth backdrop to slow, and for that to keep the Federal Reserve from hiking interest rates further.

Sunset Market Commentary

Markets

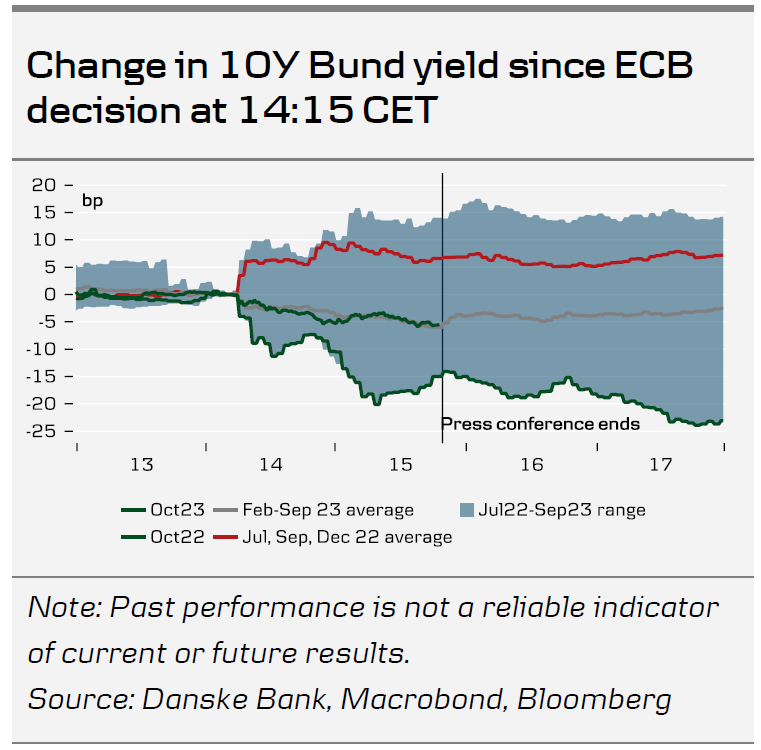

The ECB as expected paused the hiking cycle it started in July last year by leaving its deposit rate unchanged at 4% as recent information confirmed its assessment on the inflation outlook. Inflation is still seen staying too high for too long, but price rises dropped markedly. This was not only driven by base-effects but also by a slowdown in underlying inflation as previous hikes are affecting financial conditions. The MPC reiterates that ECB interest rates are at levels that, if maintained for sufficiently long, will make a substantial contribution to return inflation to 2% in a timely manner. The council maintains a data-dependent approach in determining the appropriate level and the duration of restriction. The ECB’s wait-and-see assessment was broadly as expected given recent growth and inflation data. The ECB kept ‘guidance’ unchanged that it intends to reinvest the proceeds of maturing assets from the PEPP program at least until the end of 2024. At the press conference ECB Chair Lagarde said that halting those reinvestments wasn’t discussed. This also applied for the renumeration of reserves. German yields opened higher at the start this morning, trading little changed at the time of the ECB decision. The intra-day ‘down move’ continued after the decision & during the press conference. German yields currently are ceding between 1.5 bps (30-y) and 4 bps (5-y). Lagarde indicated that any debate on the timing of rate cuts is totally premature.

The first estimate of US Q3 GDP printed at a strong 4.9% QoQa (from 2.1% and 4.5% expected). Private consumption (4%) and gross private investment (8.4%) were strong. As was government consumption (4.6%). Change in inventories also added 1.32% to overall growth. Net exports was marginally negative (-0.08% contribution). The price indicators were mixed (GDP price index 3.5% from 1.7%, core PCE deflator down to 2.4% from 3.7% Q/Q). Headline durable goods orders were very strong at 4.7%, but capital goods shipments stabilized. Weekly jobless claims rose marginally more than expected (210k) but remain low.US yields tentatively rose in the run-up to the data, but eased afterwards. Investors concluded that an important bout of strong data is now out of the way. US yields ease 3 bps (30-y) to 5 bps (5-y).

Other markets succeeded a modest risk-on rebound after the ECB decision and the US data. The EuroStoxx 50 reversed a 1%+ decline to currently lose only 0.35%. US indices opened with modest losses (S&P 500 -0.15%), but futures also showed bigger losses intraday. Modest moves also occurred in the major USD cross rates. EUR/USD touched the 1.0525 area but currently trades little changed at 1.056. USD/JPY after filling offers near 150.75 this morning eased back to 150.25. Sterling profited slightly from this afternoon’s risk rebound, with EUR/GBP easing back to the 0.871 area.

News & Views

The Turkish central bank (CBRT) raised its policy rate from 30% to 35% extending the stealth tightening cycle which started in the aftermath of Turkish elections in May (policy rate 8.5%). The strong course of domestic demand, the stickiness of services inflation, and the deterioration in inflation expectations continue to put upward pressure on inflation (61.53% Y/Y in September) . Upside risks stem from oil prices and the value of TRY. Monetary tightening will be further strengthened as much as needed in a timely and gradual manner until a significant improvement in inflation outlook is achieved. The CBRT also announced additional steps to increase the share of Turkish lira deposits and/or other liquidity-tightening measures suggesting that the pace of rate hikes will slow. EUR/TRY continues to trade near the all-time highs, just below 30.

Poland’s opposition leader Donald Tusk (Civic Platform party), who together with his allies secured a majority in Polish parliamentary elections earlier this month, suggested that gaining access to EU funds doesn’t depend on a lengthy legislative process. Improving relations with Europe is top of mind of likely future PM Tusk. Unblocking €35bn in EU funding could happen as soon as December if he’s able to form a government. The money was kept back on disputes with the outgoing Law & Justice party over rule of law infringements. EUR/PLN drops from 4.4825 towards 4.4575 today, but this is also might also be due to better risk sentiment intraday.