Sample Category Title

U.S. Consumer Spending Grows, Despite a Slowdown in Income in September

Personal income grew 0.3% month-on-month (m/m) in September, a deceleration from August's 0.4% and just below market expectations for 0.4% growth.

Accounting for inflation and taxes, real personal disposable income fell -0.1% m/m, following a similar decline in the previous month.

Personal consumption expenditures rose 0.7% m/m, accelerating from the 0.4% posted in August. September's reading came in above market expectations for 0.5% growth.

- Expenditures on services grew 0.8% m/m, reflecting higher spending on other services (international travel), housing and utilities, health care and transportation services (led by air transportation).

- There was also an increase in goods spending (up 0.7% m/m) reflecting a gain of 0.5% in non-durable goods spending (prescription drugs) and 1% in durable goods spending (led by new motor vehicles).

Adjusting for inflation, real spending grew 0.4% for the month, coming in just above consensus estimate for a 0.3% gain. In real terms, goods and services spending were up 0.5% and 0.3% respectively.

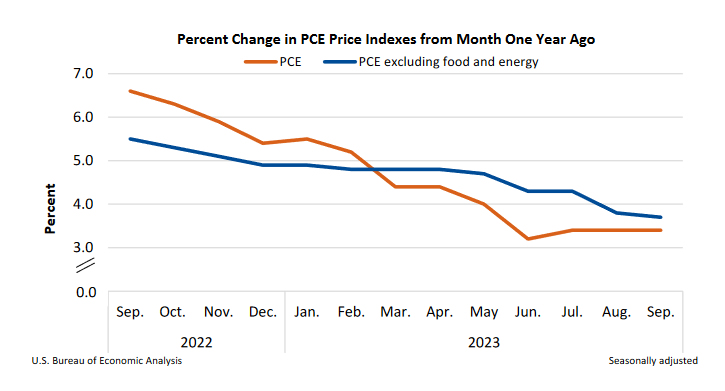

Headline personal consumption expenditure (PCE) inflation rose 0.4% m/m, and was steady at 3.4% on a year-on-year (y/y) basis. However, the core PCE price deflator (which excludes food and energy and is the Fed's preferred measure of inflation) accelerated to 0.3% m/m, from a soft 0.1% in August. However, on an annual basis, core PCE inflation decelerated to 3.7% from 3.8% the month prior, and on a three month annualized basis was 2.5% in September, suggesting core inflation should cool further in the coming months..

As spending growth outpaces income gains, the personal savings rate fell to 3.4% in September, down 0.6%-pts from August's 4% reading, and the lowest level this year.

Key Implications

U.S. consumer spending closed out the third quarter on solid footing. Despite mounting headwinds, the consumer more than did their part to buoy the economy with real consumption expenditure growth clocking in at 4.0% annualized for Q3. However, with real disposable income declining for three straight months and headwinds growing, the likelihood that the consumer will be able to keep up the same pace in Q4 is dubious. As such, a deceleration in consumer spending to below 2% is expected in the final quarter.

Turning to movements in prices, today's core PCE number headed in the right direction to support the Fed's current wait-and-see stance. The fact that our measure of non-housing service inflation (aka "supercore") held steady at 4.2% y/y was promising, though the jump in the 3-month annualized change to 4.2% (from 3.2%) was not. Nevertheless, the central bank is unlikely to have been surprised by the strength of consumer spending during the summer. The more relevant question is whether the trend can continue in coming quarters and its impact on inflation – a topic sure to be discussed at the upcoming FOMC meeting next week. Despite the bump in consumer spending (and GDP), with the Fed's preferred measure of inflation continuing to head lower in September, market pricing continues to favor the Fed holding rates steady next week.

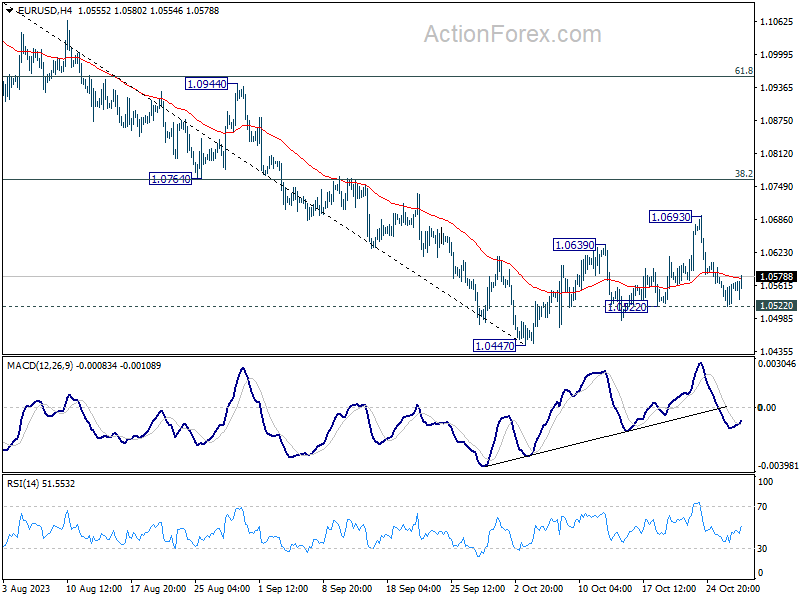

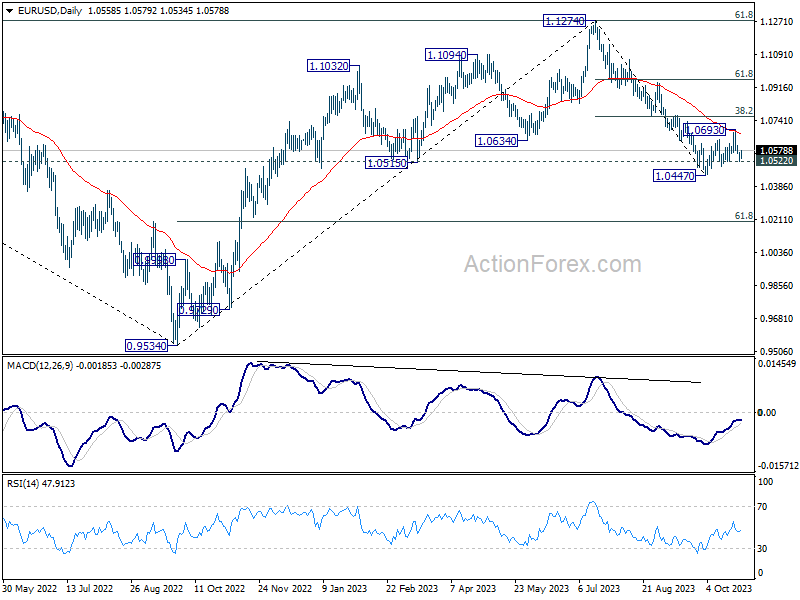

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0534; (P) 1.0554; (R1) 1.0584; More...

EUR/USD is recovering after hitting 1.0522 support, but stays well below 1.0693 resistance. Intraday bias stays neutral first. On the downside, break of 1.0522 support will confirm rejection by 55 D EMA, and retain near term bearishness. Intraday bias will be back on the downside for 1.0447. Break there will resume larger fall from 1.1274. On the other, strong bounce from current level, followed by break above 1.0693, rebound from 1.0447 to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763).

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0668) holds, in case of rebound.

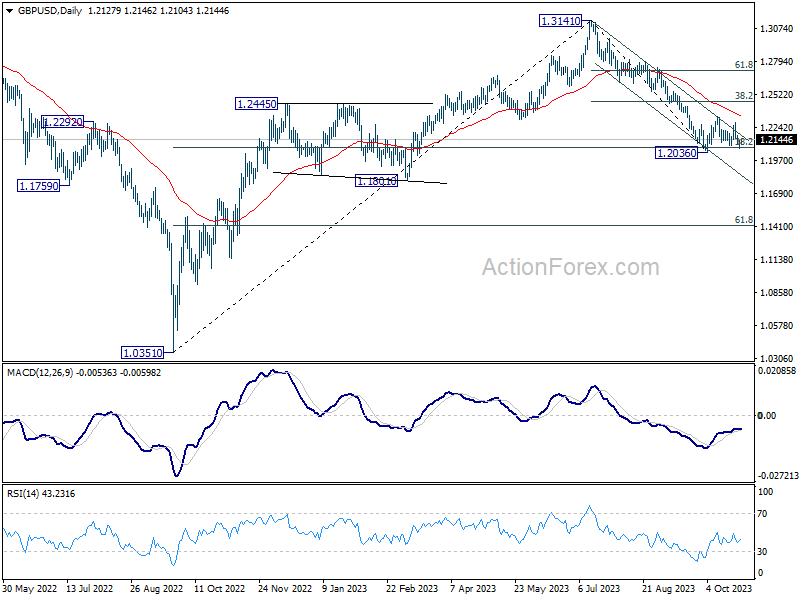

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2085; (P) 1.2112; (R1) 1.2155; More

No change in GBP/USD's outlook as consolidation from 1.2036 is still extending. Intraday bias remains neutral and further decline is in favor. On the downside, decisive break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next. However, break of 1.2336 will turn bias back to the upside for 38.2% retracement of 1.3141 to 1.2036 at 1.2458.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2346) holds, in case of rebound.

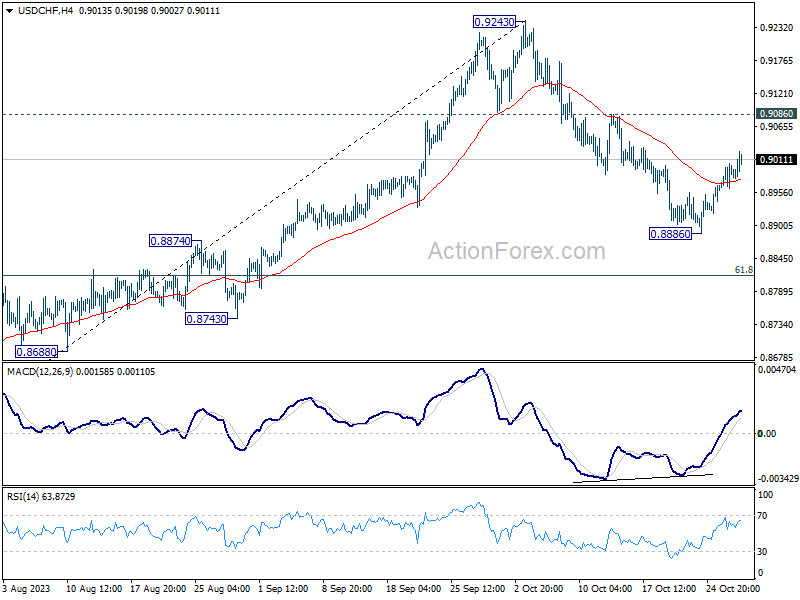

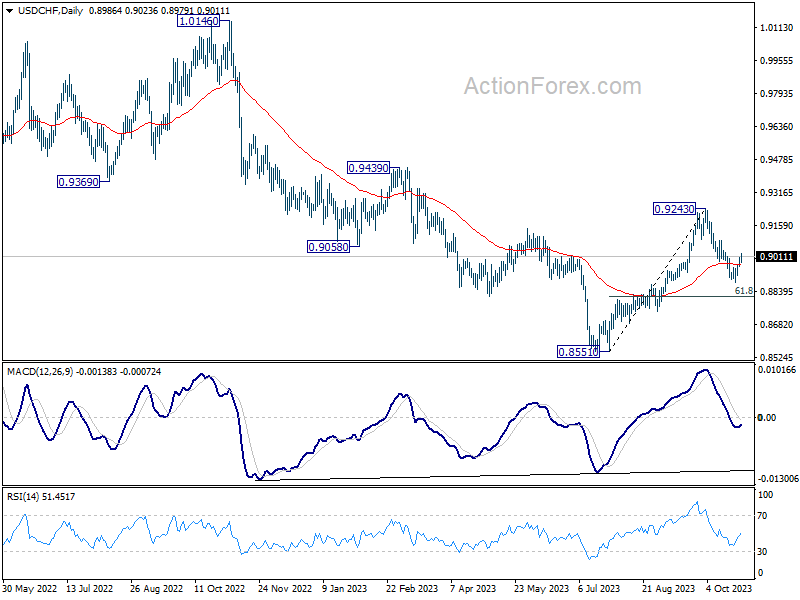

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8960; (P) 0.8983; (R1) 0.9011; More....

Break of 0.9000 minor resistance indicates short term bottoming at 0.8886. Intraday bias is back on the upside for 0.9086 resistance first. Firm break there will bring retest of 0.9243 high. On the downside, however, break of 0.8886 will resume the fall from 0.9243 to 61.8% retracement of 0.8551 to 0.9243 at 0.8815 next.

In the bigger picture, rebound from 0.8551 might be completed as a correction at 0.9243. In other words, larger fall from 1.0146 (2022 high) is possibly not over yet. Risk will now stay on the downside as long as 0.9243 resistance holds. Firm break of 0.8551 will confirm down trend resumption.

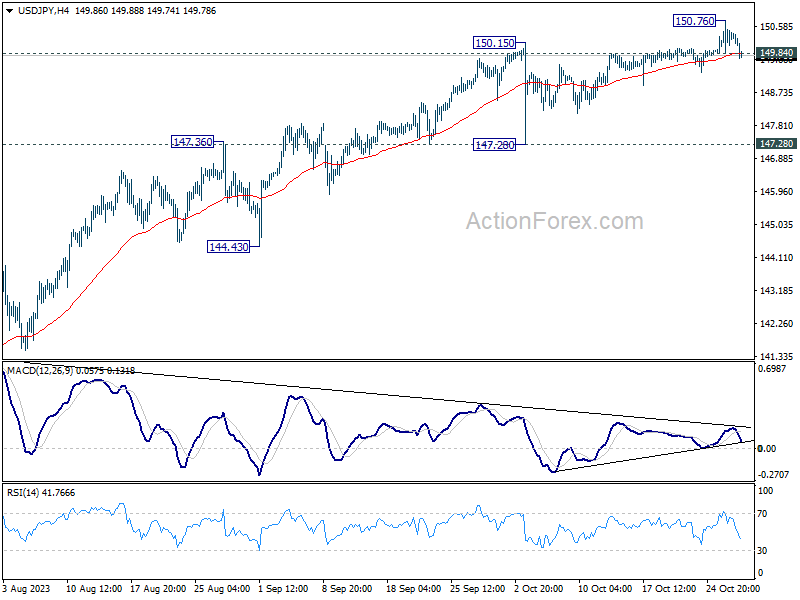

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.91; (P) 150.34; (R1) 150.85; More...

Intraday bias in USD/JPY is turned neutral with break of 149.84 minor support. Some consolidations would be seen first. But near term outlook will stay bullish as long as 147.28 support holds, even in case of deep retreat. On the upside, above 150.76 will resume larger rally to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Yen Seeks Revival as Dollar Shrugs PCE Data

As the week draws to a close, the Japanese Yen is exhibiting signs of a tentative comeback, with USD/JPY retreating back below the significant 150 mark. Dollar's response to the latest US personal income and outlays data was relatively subdued. Although the monthly headline PCE price index ticked slightly above forecasts, other inflation indicators aligned closely with market expectations. Notably, robust spending growth highlights the resilience of US consumers.

However, it appears Dollar traders are cautiously adjusting their positions in anticipation of next week's pivotal FOMC meeting and the upcoming non-farm payroll report. Similarly, Yen traders are vigilant, preparing for potential shifts stemming from BoJ's upcoming policy meeting.

Looking at the week in review, Australian and New Zealand Dollars have emerged among the top performers, sharing the stage with Dollar. On the flip side, Swiss Franc, Euro, and Canadian Dollar lagged behind. British Pound and Yen showcased a mixed performance.

In Europe, at the time of writing, FTSE is down -0.18%. DAX is up 0.25%. CAC is down -0.60%. Germany 10-year yield is down -0.023 at 2.845. Earlier in Asia, Nikkei rose 1.27%. Hong Kong HSI rose 2.08%. China Shanghai SSE rose 0.99%. Japan 10-year JGB yield dropped -0.0090 to 0.876.

US PCE inflation unchanged at 3.4% yoy, core slowed to 3.7% yoy

US personal income rose 0.3% mom or USD 77.8B in September, below expectation of 0.4%. Personal spending rose 0.7% mom or USD 138.7B, well above expectation of 0.4% mom.

PCE price index rose 0.4% mom, above expectation of 0.3% mom. Core PCE price index (excluding food and energy) rose 0.3% mom, matched expectations. Prices for goods increased 0.2% mom and prices for services increased 0.5% mom. Food prices increased 0.3% mom and energy prices increased 1.7% mom.

Annually, PCE price index was unchanged at 3.4% yoy, matched expectations. Core PCE price index slowed from 3.8% yoy to 3.7% yoy, matched expectations. Prices for goods increased 0.9% yoy and prices for services increased 4.7% yoy. Food prices increased 2.7% yoy and energy prices decreased by less than -0.1% yoy.

ECB survey indicates modest adjustments to growth and inflation forecasts

ECB's latest Survey of Professional Forecasters for Q4 presents marginal adjustments to economic outlook for the 2023-2025 period. Also, headline inflation expectations underwent minimal changes for these years.

Regarding the HICP, inflation forecast for 2023 has been adjusted upwards to 5.6% from its earlier 5.5% estimation. The projections for 2024 remain steady at 2.7%, whereas for 2025, it was slightly dialed back to 2.1% from the prior 2.2% prediction.

On the core inflation front, 2023 remains unchanged at 5.1%. However, the following years see a minor downward revision, with 2024 expectations set at 2.9% (down from earlier 3.1%) and 2025 set at 2.2% (down from 2.3%).

Turning to Real GDP growth, 2023 projections are adjusted downwards to 0.5% an prior 0.6%. 2024 now stands at 0.9%, a reduction from 1.1% previously forecasted. Growth projection for 2025 remains steady at 1.5%.

Tokyo CPI signals rising inflation; BoJ likely to upgrade forecasts

In Japan, Tokyo's headline CPI unexpectedly accelerated from 2.8% yoy to 3.3% yoy in October. CPI core, which excludes the volatile prices of fresh food, also witnessed an acceleration, moving from 2.5% yoy to 2.7% yoy. On the other hand, CPI core-core, which strips out impact of both food and energy prices, marginally slowed from 3.9% yoy to 3.8% yoy, but remained elevated.

An important metric to note is acceleration in services prices, which went from 1.9% yoy 2.1% yoy. The continued uptick in services inflation indicates a more entrenched and broad-based price pressure scenario, suggesting that it could be a prolonged period before inflation retraces its steps back below BoJ's 2% target.

Considering that consumer inflation in Tokyo often sets the tone for national trends, the data bolsters the anticipation that BoJ might have to upgrade its inflation forecasts. Market participants are now keenly awaiting the fresh quarterly projections that are expected to be unveiled at BoJ's policy meeting next week.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.91; (P) 150.34; (R1) 150.85; More...

Intraday bias in USD/JPY is turned neutral with break of 149.84 minor support. Some consolidations would be seen first. But near term outlook will stay bullish as long as 147.28 support holds, even in case of deep retreat. On the upside, above 150.76 will resume larger rally to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Oct | 3.30% | 2.80% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Oct | 2.70% | 2.50% | 2.50% | |

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Oct | 3.80% | 3.80% | 3.90% | |

| 00:30 | AUD | PPI Q/Q Q3 | 1.80% | 0.70% | 0.50% | |

| 00:30 | AUD | PPI Y/Y Q3 | 3.80% | 3.90% | ||

| 12:30 | USD | Personal Income M/M Sep | 0.30% | 0.40% | 0.40% | |

| 12:30 | USD | Personal Spending Sep | 0.70% | 0.40% | 0.40% | |

| 12:30 | USD | PCE Price Index M/M Sep | 0.40% | 0.30% | 0.40% | |

| 12:30 | USD | PCE Price Index Y/Y Sep | 3.40% | 3.40% | 3.50% | 3.40% |

| 12:30 | USD | Core PCE Price Index M/M Sep | 0.30% | 0.30% | 0.10% | |

| 12:30 | USD | Core PCE Price Index Y/Y Sep | 3.70% | 3.70% | 3.90% | 3.80% |

| 14:00 | USD | Michigan Consumer Sentiment Index Oct F | 63 | 63 |

US PCE inflation unchanged at 3.4% yoy, core slowed to 3.7% yoy

US personal income rose 0.3% mom or USD 77.8B in September, below expectation of 0.4%. Personal spending rose 0.7% mom or USD 138.7B, well above expectation of 0.4% mom.

PCE price index rose 0.4% mom, above expectation of 0.3% mom. Core PCE price index (excluding food and energy) rose 0.3% mom, matched expectations. Prices for goods increased 0.2% mom and prices for services increased 0.5% mom. Food prices increased 0.3% mom and energy prices increased 1.7% mom.

Annually, PCE price index was unchanged at 3.4% yoy, matched expectations. Core PCE price index slowed from 3.8% yoy to 3.7% yoy, matched expectations. Prices for goods increased 0.9% yoy and prices for services increased 4.7% yoy. Food prices increased 2.7% yoy and energy prices decreased by less than -0.1% yoy.

ECB survey indicates modest adjustments to growth and inflation forecasts

ECB's latest Survey of Professional Forecasters for Q4 presents marginal adjustments to economic outlook for the 2023-2025 period. Also, headline inflation expectations underwent minimal changes for these years.

Regarding the HICP, inflation forecast for 2023 has been adjusted upwards to 5.6% from its earlier 5.5% estimation. The projections for 2024 remain steady at 2.7%, whereas for 2025, it was slightly dialed back to 2.1% from the prior 2.2% prediction.

On the core inflation front, 2023 remains unchanged at 5.1%. However, the following years see a minor downard revision, with 2024 expectations set at 2.9% (down from earlier 3.1%) and 2025 set at 2.2% (down from 2.3%).

Turning to Real GDP growth, 2023 projections are adjusted downwards to 0.5% an prior 0.6%. 2024 now stands at 0.9%, a reduction from 1.1% previously forecasted. Growth projection for 2025 remains steady at 1.5%.

CHF/JPY Technical: At Risk of Multi-Day Corrective Decline

- Several key bearish technical elements have emerged on the CHF/JPY.

- The Tokyo-area inflationary data for October has surpassed expectations that revive a potential hawkish guidance from the Bank of Japan (BoJ)’s upcoming monetary policy decision next Tuesday, 31 October.

- Watch the short-term key resistance of 167.60 on CHF/JPY.

The price actions of CHF/JPY have staged the expected rally and hit the resistance levels of 166.60 and 167.90/168.30 as highlighted in our report. The cross pair printed an intraday high of 168.42 on 20 October 2023.

Through the lens of technical analysis, the price actions of highly liquid FX pairs such as CHF/JPY do not move in a vertical fashion, but rather oscillate or mean revert within a trending phase.

In the past week, there has been an emergence of key technical elements that advocate for a potential multi-day corrective decline for CHF/JPY within a major uptrend phase that is still in place since its 13 January 2023 low of 137.44.

Fundamentally, the ongoing down move seen in the CHF/JPY as it shed 58 pips intraday at this time of the writing has been the revival of inflationary pressures in the leading Tokyo area CPI data for October. Tokyo’s core-core inflation rate (excluding fresh food and energy) rose to 2.7% y/y and surpassed its August year-to-date peak of 2.6% y/y to hit a 31-year high.

This elevated set of inflationary numbers from Japan ahead of the Bank of Japan (BoJ) monetary policy decision and the release of its latest forecast of Japan’s key economic data (outlook report) on next Tuesday, 31 October has increased the odds of a hawkish guidance which in turn trigger a stronger JPY movement today.

Daily bearish reversal candlestick sighted

Fig 1: CHF/JPY major & medium-term trends as of 27 Oct 2023 (Source: TradingView, click to enlarge chart)

The CHF/JPY has formed a daily “Shooting Star” bearish reversal candlestick on 20 October 2023 before this current slide of -185 pips took form at this time of the writing. In conjunction, the daily RSI momentum indicator has exited from its overbought region (more than 70 level) thereafter and still has potential room to manoeuvre towards its oversold region.

These observations suggest that medium-term downside momentum is likely to have emerged which in turn increases the odds of a multi-day corrective decline in CHF/JPY.

Minor bearish breakdown from ascending channel

Fig 2: CHF/JPY minor short-term trend as of 27 Oct 2023 (Source: TradingView, click to enlarge chart)

In addition, as seen from the shorter time frame chart (1 hour), the price actions of CHF/JPY have broken down below the minor ascending channel support yesterday, 23 October.

Watch the 167.60 key short-term pivotal resistance for a further potential slide towards the next immediate support zone at 165.20/164.80 (also the 20 and 50-day moving averages). A break below 164.80 exposes the next support at 164.00/163.70 (the median line of the major ascending channel in place since 13 January 2023 low and congestion area from 24 July/October 2023).

On the flip side, a clearance above 167.60 invalidates the bearish tone to see a retest on the medium-term resistance level of 167.90/168.30.

USD/JPY Edges Lower, Tokyo Core CPI Rises

- Tokyo Core CPI climbs higher than expected

- US GDP jumps 4.9%

The Japanese yen has steadied after three straight days of losses. In the European session, USD/JPY is trading at 150.11, down 0.19%.

Strong Tokyo Core CPI puts the heat on BoJ

Tokyo Core CPI climbed 2.7% y/y in October, above 2.5% in September which was also the consensus estimate. The index, which excludes fresh food is a key indicator of inflation trends in Japan and is closely monitored by the Bank of Japan. Tokyo’s headline CPI also rose in October, from 2.8% to 3.3%.

The Bank of Japan will find it hard to ignore these hotter-than-expected inflation readings. The timing of these releases is awkward for the BoJ, which holds its policy meeting on Oct. 30-31. Underlying inflation is proving to be stickier than expected and BoJ policy makers may have to revise upwards their inflation outlooks for 2023 and 2024. High inflation is a risk to Japan’s recovery, putting pressure on the BoJ to make some kind of move at the meeting.

The central bank will have a busy agenda at next week’s meeting. Aside from stubbornly high inflation, the BoJ will have to decide whether to tweak its yield curve control (YCC) program and what to do about the falling yen. The Japanese currency breached the symbolic 150 line this week for the first time since October 3rd, raising speculation that the BoJ could shift its policy or even intervene in the currency markets. Tokyo has responded to the yen breaching 150 with the usual verbal intervention, warning investors not to sell the yen. The BoJ won’t be providing any advance warning about a currency intervention, so traders should remain on alert.

US GDP sizzles 4.9%

For those doubting US exceptionalism, the superb US GDP of 4.9% in the third quarter was proof in the pudding of a robust US economy. This was the fastest growth rate since Q4 of 2021, boosted by strong consumer spending in the third quarter. The sharp rise in growth hasn’t changed market expectations with regard to rates, which have priced in pauses at the November and December meetings.

USD/JPY Technical

- USD/JPY is testing support at 1.5017. Below, there is support at 149.67

- There is resistance at 1.5049 and 1.5099