Sample Category Title

The Weekly Bottom Line: Economic Resilience on Full Display in Third Quarter

U.S. Highlights

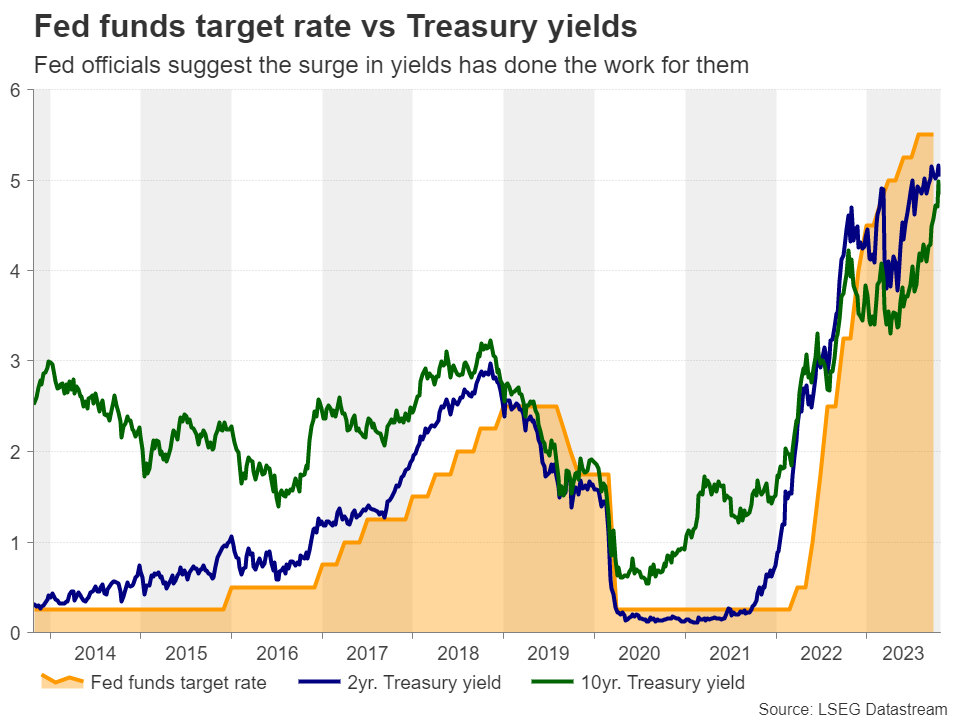

- The 10-year Treasury yield briefly surpassed 5% earlier this week. Though yields have since retraced, the 10-year looks to end the week at a still elevated 4.85%.

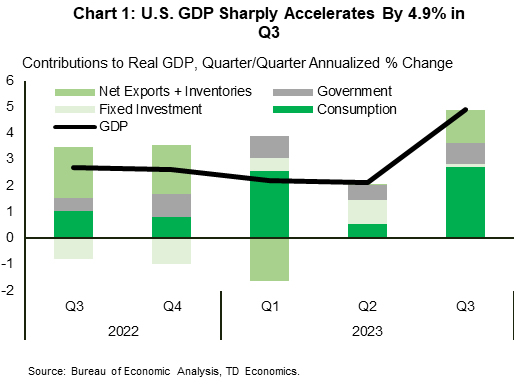

- The advance estimate of GDP showed the economy registered its strongest gain in nearly two years in the third quarter, with most major areas of spending recording gains.

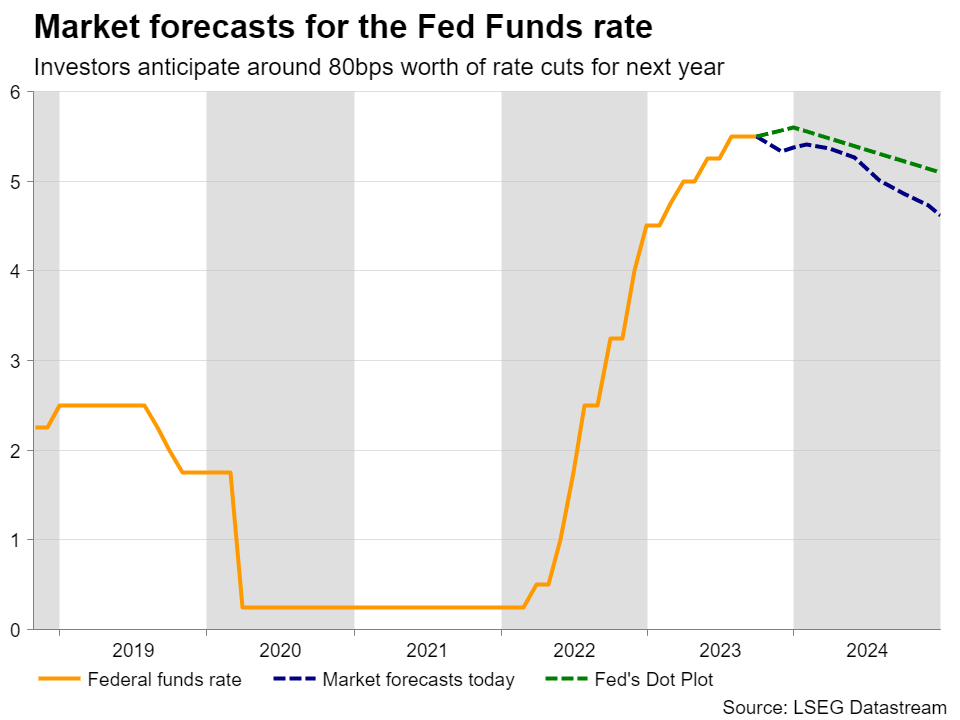

- The FOMC is expected to hold rates steady next week, but the uptick in September inflation along with any signs of continued labor market strength in next week’s data will tilt the scales in favor of another rate hike later this year.

Canadian Highlights

- Fears around what higher-for-longer rates might do to growth dominated markets this week. Equities were lower and yields fell. Meanwhile, easing concerns of a wider Middle East conflict weighed on oil.

- The Bank of Canada held the policy rate at 5% this week. Their Monetary Policy Report emphasized the economic toll from higher rates, consistent with no further hikes.

- However, policymakers retained a hawkish tone, given still robust wage growth, elevated inflation expectations and corporate pricing behaviour that’s yet to normalize.

U.S. – Economic Resilience on Full Display in Third Quarter

Longer-term Treasury yields continued to creep higher through the early portion of the week, as the looming threat of a mid-November government shutdown, increased Treasury issuance, and heightened geopolitical tensions remain key drivers pressuring the term-premia higher. After briefly surpassing 5% earlier this week, the 10-Year Treasury yield has since pared its gains and currently sits at a still elevated 4.85%. Meanwhile, equities edged lower for the second straight week – down 2% at the time of writing – but remain 8% higher on the year.

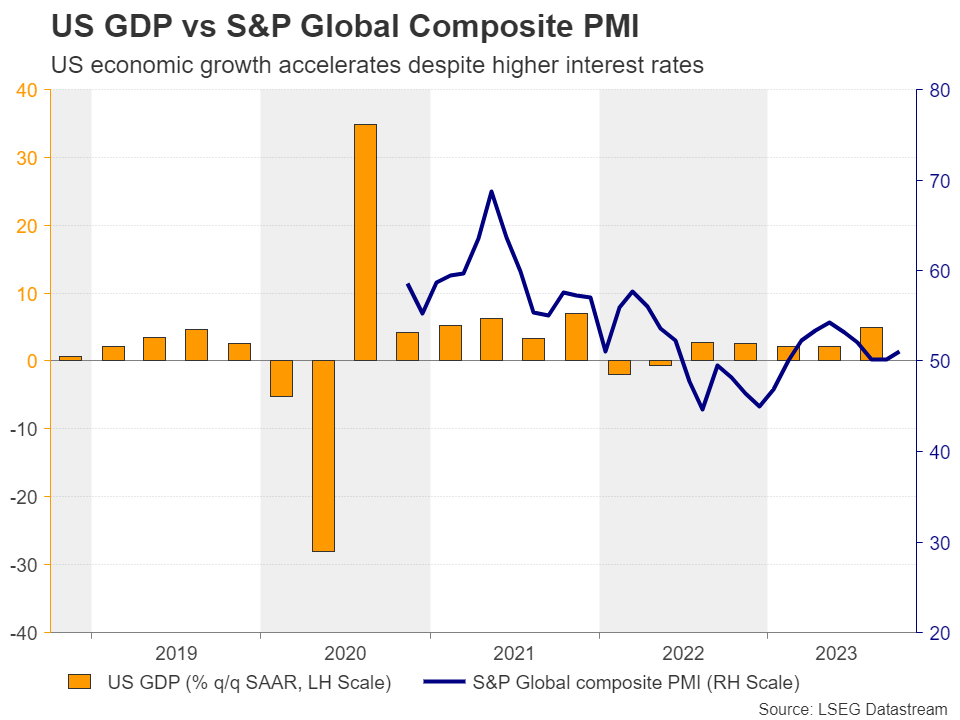

Turning to the economic data calendar, the Bureau of Economic Analysis (BEA) released its advance estimate of third quarter real GDP. The report showed economic activity accelerating at more than double the rate of expansion seen in Q2. The ongoing theme of economic resilience was on full display last quarter, with most major areas of spending recording gains. The strength in consumer spending was particularly eye-catching, jumping up 4.0% (Chart 1). The summer shopping spree was fueled by a resilient labor market and a further drawdown of the excess savings accumulated during the pandemic. Moreover, because many homeowners locked-in mortgages at ultra-low rates in 2020/21, the passthrough of higher interest rates to the consumer has been more muted relative to past tightening cycles.

Perhaps more concerning for policymakers is that spending momentum heated up at the end of the third quarter. September’s gain was the second strongest over the past eight months, and suggests consumers didn’t hold back last month, despite the looming headwind of student loan repayments restarting in October. At this point, we see Q3’s blowout numbers as the ‘last hurrah’ and expect a more tepid pace of consumer spending (1.5-2%) for Q4, before slipping sub-1% through the first half of next year.

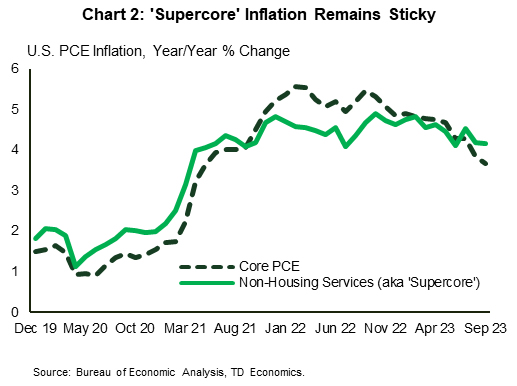

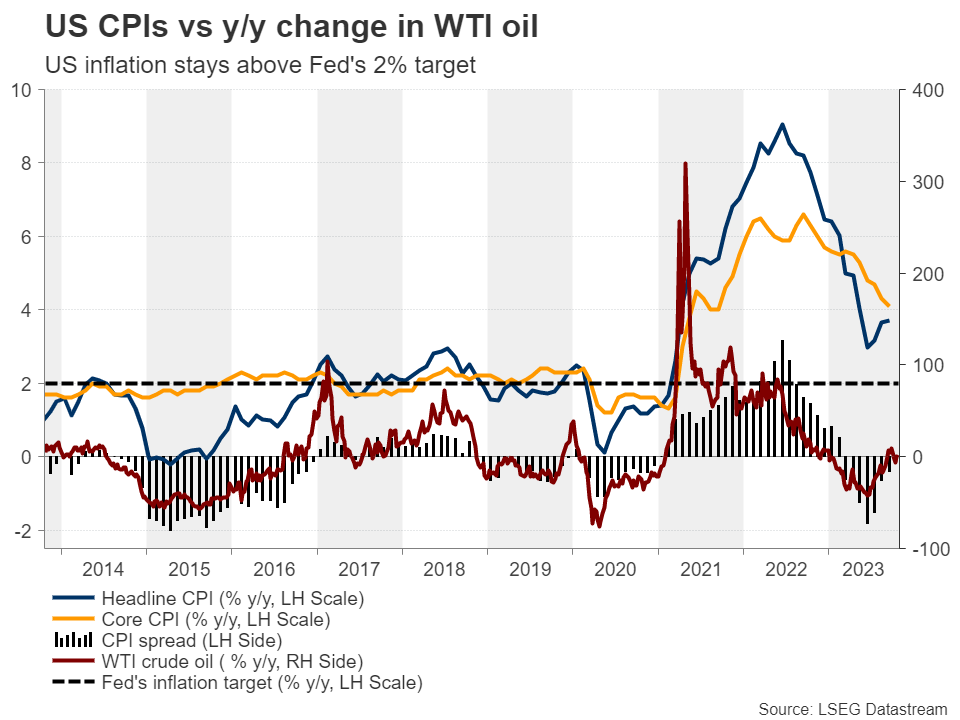

Should the consumer prove more resilient, that will spell trouble on the inflation front. In fact, core PCE inflation data for September has already telegraphed some evidence of progress stalling. Price growth picked up to 0.3% m/m (up from the 0.17% m/m gains averaged over the three prior months), with notable strength in Powell’s ‘supercore’ measure, which has barely budged from last year’s highs (Chart 2).

From the Fed’s perspective, nothing out this week will influence next week’s interest rate decision. At this point, markets are fully priced for the FOMC to hold rates steady, and only attach a 20% probability to another rate hike in December. However, that could quickly change over the next week should the FOMC statement and/or Powell’s press conference strike a more hawkish tone. Next week’s Employment Cost Index release for the third quarter is also important given it contains a measure of wage inflation that the Fed watches closely. As well, October’s employment figures out Friday will be closely scrutinized as usual. Unless these reports show a definitive sign that the labor market is cooling, which looks unlikely given the recent strength in higher frequency indictors including jobless claims and Indeed job posting data, another rate hike come December seems inevitable.

Canada – Holding the Line

The mood in financial markets was more dovish this week, on concerns on what higher-for-longer rates could mean for growth prospects. The North American benchmark WTI slid about $3 per barrel, greased by weaker-than-expected seasonal demand in the U.S. and (likely) some degree of assurance that the Israel/Hamas conflict would be regionally contained. This decline helped pull the TSX to its lowest level since October of last year. Even the sustained and severe upward march in bond yields observed over the past several months hit a pause this week, with yields down across the curve.

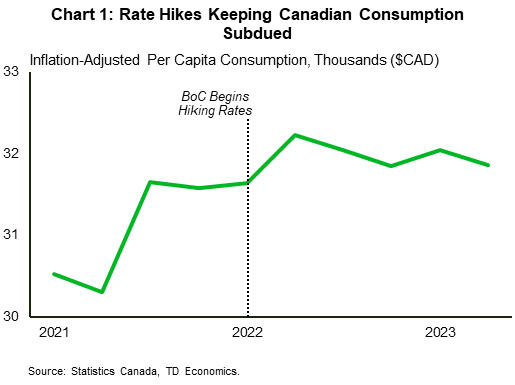

The pullback in yields doesn't change the fact that they remain near-multi year highs and are exerting a braking force on the Canadian economy. The Bank of Canada hammered this point home in this week's interest rate announcement. The Bank stood pat on rates, and the accompanying Monetary Policy Report (MPR) even included a special section detailing the impact of rates on economic activity. Policymakers noted that inflation-adjusted per capita consumption has stalled since the Bank started hiking rates (Chart 1), weighed down (to varying degrees) by both rate-sensitive and non-rate-sensitive goods and services.

The impact of higher rates also shows up in the Bank's near-term growth projections, where they are forecasting (annualized) gains of 0.8% for GDP in both the third and fourth quarters of this year. While we wouldn't quibble too much with these projections, monthly GDP data suggests some modest downside risk to the Bank's Q3 forecast. Preliminary estimates had pointed to a 0.1% month-on-month gain in August, although we'll receive confirmation of that (alongside an early read on September) when the monthly GDP data is released next week.

While softer growth would certainly be consistent with our view that the Bank is done hiking rates this year, we can't necessarily close the book on that possibility. The Bank upgraded its inflation forecast for this year and next, while making pains to emphasize their concern that core inflation is not cooling as rapidly as expected. They also noted that inflation expectations are far from normal while corporate pricing behaviour also has yet to normalize.

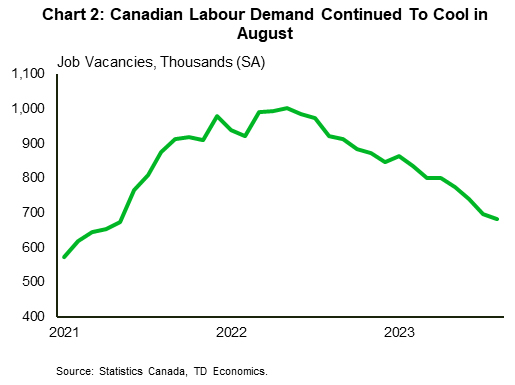

In addition to these factors, the Bank remains concerned that a tight job market is keeping wage growth in the 4-5% range, which is simply too strong to move inflation to their 2% target, especially given Canada's poor productivity. Our view is that wage growth will likely cool moving forward amid robust population growth and an economy that's struggling to keep its head above water. Notably, this week's Survey of Employment Payrolls and Hours showed some cooling in wage growth, declining payroll employment and falling job vacancies for the month of August (Chart 2). Next week, all eyes will be on Friday's Labour Force Survey release, which will offer the latest temperature reading on wage growth.

Weekly Economic & Financial Commentary: Remarkable Resilience

Summary

United States: Remarkable Resilience

- The U.S. economy expanded at a stronger-than-expected pace in Q3, with real GDP increasing at a robust 4.9% annualized rate. Data on consumer spending, durable goods, initial claims and new home sales also continued to show remarkable resilience, given higher interest rates and tightening credit conditions.

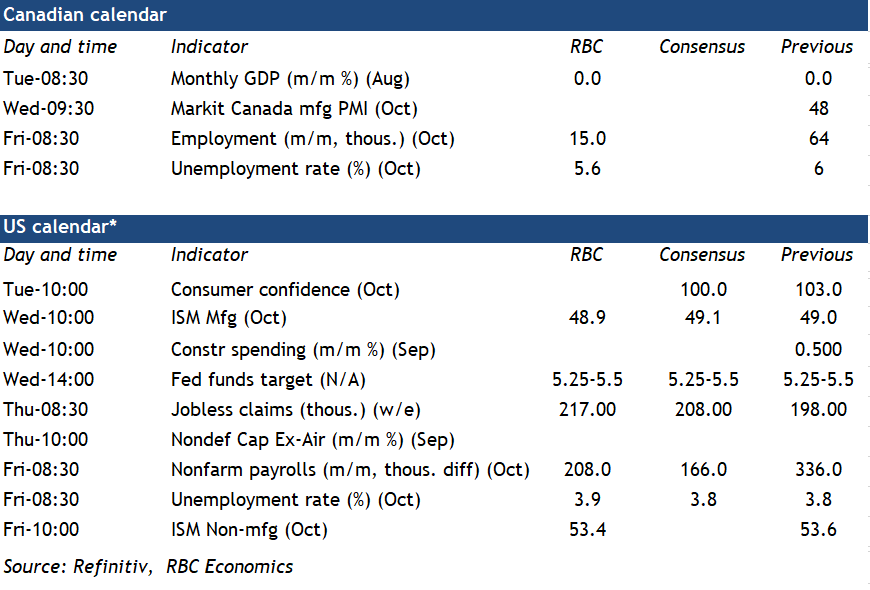

- Next week: ISM Indices (Wed. and Thu.), FOMC Decision (Wed.), Employment (Fri.)

International: G10 Central Banks Holding Steady

- This week's monetary policy meeting saw key G10 central banks hold interest rates steady at their latest announcements. The Bank of Canada held its policy rate at 5.00% and, while keeping the door open to further tightening, said past rate hikes are increasingly dampening economic activity and relieving price pressures. The European Central Bank held its Deposit rate at 4.00% and said the current level of interest rates should eventually see inflation return toward target, while also observing signs of weakness across the Eurozone economy.

- Next week: China PMIs (Tue.), Bank of Japan Policy Decision (Tue.), Eurozone CPI (Tue.)

Credit Market Insights: Interest Rates Are Small Potatoes for Small Business

- Earlier this month, Patrick Harker—the Federal Reserve Bank of Philadelphia president and a well-known dovish voter on the FOMC—generated significant publicity with his sentiment that the Fed should not consider additional rate hikes, given many small businesses are straining to endure tightening to date. But what does recent survey evidence indicate for the current state of small business lending and credit availability?

Topic of the Week: The Negotiations Continue: EU-US Trade

- European Union and United States trade officials have been at the negotiating table for months trying to settle on a trade deal between the two economies. The EU is seeking for the U.S. to end Trump-era tariffs as well as to ease some of the impact of recent U.S. green subsidies on the bloc.

Cliff Notes: Upside Inflation Risks Linger

Key insights from the week that was.

In Australia, the Q3 CPI printed at 1.2% (5.4%yr) for headline inflation and 1.2% (5.2%yr) for core trimmed mean inflation. The detail of the report highlighted that, although the disinflationary process remains intact, its pace is not as fast as Westpac and the RBA were anticipating. Indeed, on a six-month annualised basis, core inflation only edged lower Q2 to Q3 from 4.5% to 4.3%. In the quarter, major goods categories were stronger than expected, most notably automobiles and house purchase costs. Upside surprises were also seen within services, particularly ‘other recreational, sporting and cultural services’ – capturing cinemas, concerts and sporting events – which posted its strongest September gain since the introduction of GST in 2000, +3.4%.

The Commonwealth Rent Assistance, Child Care Subsidy and Energy Bill Relief programmes are providing some respite to stressed households. But ultimately, policy needs to bring inflation back to target if cost-of-living pressures are to fade. This is why Governor Bullock stated just before the CPI’s release that the Board “will not hesitate to raise the cash rate further if there is a material upward revision to the outlook for inflation.”

As outlined by Chief Economist Luci Ellis, the stronger-than-expected Q3 inflation print and the RBA’s clear messaging have led us to revise our view on the cash rate, with a 25bp hike to 4.35% now forecast for the November Board meeting. The resilience of the household sector to the tightening cycle to date, capacity constraints amid strong population growth as well as ongoing gains for wealth from housing also support a decision to hike. However, the RBA will also recognise that the labour market has turned and the risk of a price-wage spiral is receding. November’s decision to raise rates will therefore be finely balanced. And, in the months ahead, the RBA will closely scrutinise the evolution of both inflation and activity risks.

Offshore, central banks and Chinese stimulus dominated headlines.

The Bank of Canada held rates steady at 5.0% and unveiled new forecasts. The average annual GDP growth projections were cut by 0.6ppts to 1.2% for 2023 and 0.3ppt to 0.9% for 2024 but revised up 0.1ppt to 2.5% for 2025. However, year-end inflation for 2023 and 2024 was revised up, and the BoC now sees inflation returning to its 1-3% target band in 2025 rather than 2024. The statement also made clear that the Governing Council was attune to upside risks for inflation and was willing to raise rates if needed. It looks as though the BoC will tolerate above-target inflation in 2023 given the weak outlook for growth. But it remains to be seen if this patience will endure through 2024 if upside inflation risks materialise.

The European Central Bank subsequently kept its three key policy rates on hold at its October meeting, though President Christine Lagarde again noted inflation is expected to stay “too high for too long”. The ECB continues to believe that holding rates at their current level will allow the ECB to reach its inflation target. However, despite considerable uncertainty over the growth outlook and with financial conditions having also been tightened by changes in lending standards, Lagarde gave no indication about when rate cuts might occur when asked during the press conference. Given much of the easing in inflation in the September quarter came as a result of energy price base effects, the ECB is right to be cautious about the ongoing rate of disinflation.

Across in the US, Q3 GDP exceeded expectations growing 4.9% annualised in Q3. Personal consumption expenditure contributed more than half of total quarterly growth (around 2.7ppts), with strength evident across goods and services. A strong labour market and low 30-year fixed mortgage rates locked in during the pandemic are sustaining established households’ spending capacity, and being further supplemented by the remaining excess savings from the pandemic. However, confidence is weak and consumer caution over the outlook has risen of late.

It is worth noting that the quarterly profile for consumption has been inconsistent over the past year, leaving annual growth only marginally above the pre-pandemic decade average (2.4%yr compared to 2.3%yr). A similar assessment can be made for domestic demand overall, with annual growth currently 2.6%yr versus 2.4%yr pre-pandemic. With the labour market decelerating, confidence weak, and the full effect of financial and credit tightening to be felt, the message these results provide for 2024 and 2025 is that a material slowing of growth and inflation remains the most probable outcome. This would allow the FOMC to lower the fed funds rate through the period to stop a further tightening of financial conditions on a real basis and thereby minimise the risk of recession.

Speaking of mitigating downside risks, this week China’s Central Government announced stimulus measures worth RMB1trn, 0.8ppt of GDP. This is the first time a mid-year adjustment has been made to the fiscal deficit target since the Sichuan earthquake of 2008 and before that the Asian Financial Crisis. The stimulus will be used to fund disaster relief and infrastructure spending from Q4 2023 through 2024. With the funds to be raised by the Central Government, the cost of borrowing will be minimised and time delays between financing and investment kept to a minimum. Competition for the capital amongst the provinces is likely to keep the quality of projects high. Built into our growth forecast of 5.3% for 2023 and 2024 was an expectation of further stimulus broadly in line with that announced, so our forecasts are unchanged. Our concerns over the property sector also remain. To remove this uncertainty, authorities must first underwrite funding for developers then encourage households to step-up their demand. The eventual consequence will be a return of local government funding from land sales, reducing their need for debt issuanc

Summary 10/30 – 11/3

Monday, Oct 30, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Sep | 0.30% | 0.20% |

| 07:00 | EUR | Germany GDP Q/Q Q3 P | -0.20% | 0.00% |

| 08:00 | CHF | KOF Economic Barometer Oct | 95.6 | 95.9 |

| 09:30 | GBP | Mortgage Approvals (GBP) Sep | 44K | 45K |

| 09:30 | GBP | M4 Money Supply M/M Sep | 0.10% | 0.20% |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Oct | 93.3 | 93.3 |

| 10:00 | EUR | Eurozone Industrial Confidence Oct | -9 | |

| 10:00 | EUR | Eurozone Services Sentiment Oct | 4 | |

| 10:00 | EUR | Eurozone Consumer Confidence Oct F | -17.9 | -17.9 |

| 13:00 | EUR | Germany CPI M/M Oct P | 0.20% | 0.30% |

| 13:00 | EUR | Germany CPI Y/Y Oct P | 4.00% | 4.50% |

| 21:45 | NZD | Building Permits M/M Sep | -6.70% | |

| 23:30 | JPY | Unemployment Rate Sep | 2.60% | 2.70% |

| 23:50 | JPY | Industrial Production M/M Sep P | 2.50% | -0.70% |

| 23:50 | JPY | Retail Trade Y/Y Sep | 5.90% | 7.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Sep | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 07:00 | EUR | Germany GDP Q/Q Q3 P | |

| Forecast: -0.20% | Previous: 0.00% | ||

| 08:00 | CHF | KOF Economic Barometer Oct | |

| Forecast: 95.6 | Previous: 95.9 | ||

| 09:30 | GBP | Mortgage Approvals (GBP) Sep | |

| Forecast: 44K | Previous: 45K | ||

| 09:30 | GBP | M4 Money Supply M/M Sep | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Oct | |

| Forecast: 93.3 | Previous: 93.3 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Oct | |

| Forecast: | Previous: -9 | ||

| 10:00 | EUR | Eurozone Services Sentiment Oct | |

| Forecast: | Previous: 4 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Oct F | |

| Forecast: -17.9 | Previous: -17.9 | ||

| 13:00 | EUR | Germany CPI M/M Oct P | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 13:00 | EUR | Germany CPI Y/Y Oct P | |

| Forecast: 4.00% | Previous: 4.50% | ||

| 21:45 | NZD | Building Permits M/M Sep | |

| Forecast: | Previous: -6.70% | ||

| 23:30 | JPY | Unemployment Rate Sep | |

| Forecast: 2.60% | Previous: 2.70% | ||

| 23:50 | JPY | Industrial Production M/M Sep P | |

| Forecast: 2.50% | Previous: -0.70% | ||

| 23:50 | JPY | Retail Trade Y/Y Sep | |

| Forecast: 5.90% | Previous: 7.00% | ||

Tuesday, Oct 31, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | |

| 00:00 | NZD | ANZ Business Confidence Oct | 1.5 | |

| 00:30 | AUD | Private Sector Credit M/M Sep | 0.40% | |

| 01:00 | CNY | NBS Manufacturing PMI Oct | 50.4 | 50.2 |

| 01:00 | CNY | NBS Non-Manufacturing PMI Oct | 51.8 | 51.7 |

| 05:00 | JPY | Housing Starts Y/Y Sep | -6.20% | -9.40% |

| 05:00 | JPY | Consumer Confidence Index Oct | 35.1 | 35.2 |

| 06:30 | EUR | France Consumer Spending M/M Sep | 0.60% | -0.50% |

| 06:30 | EUR | France GDP Q/Q Q3 P | 0.10% | 0.50% |

| 07:00 | EUR | Germany Import Price Index M/M Sep | 0.40% | 0.40% |

| 07:00 | EUR | Germany Retail Sales M/M Sep | 0.50% | -1.20% |

| 07:30 | CHF | Real Retail Sales Y/Y Sep | -1.20% | -1.80% |

| 09:00 | EUR | Italy GDP Q/Q Q3 P | 0.10% | -0.40% |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 0.00% | 0.10% |

| 10:00 | EUR | Eurozone CPI Y/Y Oct P | 3.10% | 4.30% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct P | 4.20% | 4.50% |

| 12:30 | CAD | GDP M/M Aug | 0.10% | 0.00% |

| 12:30 | USD | Employment Cost Index Q3 | 1.00% | 1.00% |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Aug | 0.30% | 0.10% |

| 13:00 | USD | Housing Price Index M/M Aug | 0.50% | 0.80% |

| 13:45 | USD | Chicago PMI Oct | 44.7 | 44.1 |

| 14:00 | USD | Consumer Confidence Oct | 100.4 | 103 |

| 21:45 | NZD | Employment Change Q3 | 0.40% | 1.00% |

| 21:45 | NZD | Unemployment Rate Q3 | 3.90% | 3.60% |

| 21:45 | NZD | Labour Cost Index Q/Q Q3 | 1.00% | 1.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: -0.10% | Previous: -0.10% | ||

| 00:00 | NZD | ANZ Business Confidence Oct | |

| Forecast: | Previous: 1.5 | ||

| 00:30 | AUD | Private Sector Credit M/M Sep | |

| Forecast: | Previous: 0.40% | ||

| 01:00 | CNY | NBS Manufacturing PMI Oct | |

| Forecast: 50.4 | Previous: 50.2 | ||

| 01:00 | CNY | NBS Non-Manufacturing PMI Oct | |

| Forecast: 51.8 | Previous: 51.7 | ||

| 05:00 | JPY | Housing Starts Y/Y Sep | |

| Forecast: -6.20% | Previous: -9.40% | ||

| 05:00 | JPY | Consumer Confidence Index Oct | |

| Forecast: 35.1 | Previous: 35.2 | ||

| 06:30 | EUR | France Consumer Spending M/M Sep | |

| Forecast: 0.60% | Previous: -0.50% | ||

| 06:30 | EUR | France GDP Q/Q Q3 P | |

| Forecast: 0.10% | Previous: 0.50% | ||

| 07:00 | EUR | Germany Import Price Index M/M Sep | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 07:00 | EUR | Germany Retail Sales M/M Sep | |

| Forecast: 0.50% | Previous: -1.20% | ||

| 07:30 | CHF | Real Retail Sales Y/Y Sep | |

| Forecast: -1.20% | Previous: -1.80% | ||

| 09:00 | EUR | Italy GDP Q/Q Q3 P | |

| Forecast: 0.10% | Previous: -0.40% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | |

| Forecast: 0.00% | Previous: 0.10% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Oct P | |

| Forecast: 3.10% | Previous: 4.30% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct P | |

| Forecast: 4.20% | Previous: 4.50% | ||

| 12:30 | CAD | GDP M/M Aug | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 12:30 | USD | Employment Cost Index Q3 | |

| Forecast: 1.00% | Previous: 1.00% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Aug | |

| Forecast: 0.30% | Previous: 0.10% | ||

| 13:00 | USD | Housing Price Index M/M Aug | |

| Forecast: 0.50% | Previous: 0.80% | ||

| 13:45 | USD | Chicago PMI Oct | |

| Forecast: 44.7 | Previous: 44.1 | ||

| 14:00 | USD | Consumer Confidence Oct | |

| Forecast: 100.4 | Previous: 103 | ||

| 21:45 | NZD | Employment Change Q3 | |

| Forecast: 0.40% | Previous: 1.00% | ||

| 21:45 | NZD | Unemployment Rate Q3 | |

| Forecast: 3.90% | Previous: 3.60% | ||

| 21:45 | NZD | Labour Cost Index Q/Q Q3 | |

| Forecast: 1.00% | Previous: 1.10% | ||

Wednesday, Nov 1, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Building Permits M/M Sep | 2.60% | 7.00% |

| 00:30 | JPY | Manufacturing PMI Oct F | 49 | 48.5 |

| 01:45 | CNY | Caixin Manufacturing PMI Oct | 50.8 | 50.6 |

| 08:30 | CHF | Manufacturing PMI Oct | 44.9 | |

| 09:30 | GBP | Manufacturing PMI Oct F | 45.2 | 45.2 |

| 12:15 | USD | ADP Employment Change Oct | 135K | 89K |

| 13:30 | CAD | Manufacturing PMI Oct | 47.5 | |

| 13:45 | USD | Manufacturing PMI Oct F | 50 | 50 |

| 14:00 | USD | ISM Manufacturing PMI Oct | 49 | 49 |

| 14:00 | USD | ISM Manufacturing Prices Paid Oct | 44.5 | 43.8 |

| 14:00 | USD | ISM Manufacturing Employment Index Oct | 51.2 | |

| 14:00 | USD | Construction Spending M/M Sep | 0.40% | 0.50% |

| 14:30 | USD | Crude Oil Inventories | 1.4M | |

| 18:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% |

| 18:30 | USD | FOMC Press Conference | ||

| 23:50 | JPY | Monetary Base Y/Y Oct | 5.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Building Permits M/M Sep | |

| Forecast: 2.60% | Previous: 7.00% | ||

| 00:30 | JPY | Manufacturing PMI Oct F | |

| Forecast: 49 | Previous: 48.5 | ||

| 01:45 | CNY | Caixin Manufacturing PMI Oct | |

| Forecast: 50.8 | Previous: 50.6 | ||

| 08:30 | CHF | Manufacturing PMI Oct | |

| Forecast: | Previous: 44.9 | ||

| 09:30 | GBP | Manufacturing PMI Oct F | |

| Forecast: 45.2 | Previous: 45.2 | ||

| 12:15 | USD | ADP Employment Change Oct | |

| Forecast: 135K | Previous: 89K | ||

| 13:30 | CAD | Manufacturing PMI Oct | |

| Forecast: | Previous: 47.5 | ||

| 13:45 | USD | Manufacturing PMI Oct F | |

| Forecast: 50 | Previous: 50 | ||

| 14:00 | USD | ISM Manufacturing PMI Oct | |

| Forecast: 49 | Previous: 49 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Oct | |

| Forecast: 44.5 | Previous: 43.8 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Oct | |

| Forecast: | Previous: 51.2 | ||

| 14:00 | USD | Construction Spending M/M Sep | |

| Forecast: 0.40% | Previous: 0.50% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 1.4M | ||

| 18:00 | USD | Fed Interest Rate Decision | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 18:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Monetary Base Y/Y Oct | |

| Forecast: | Previous: 5.60% | ||

Thursday, Nov 2, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Goods Trade Balance (AUD) Sep | 9.58B | 9.64B |

| 07:30 | CHF | CPI M/M Oct | 0.10% | -0.10% |

| 07:30 | CHF | CPI Y/Y Oct | 1.70% | |

| 08:45 | EUR | Italy Manufacturing PMI Oct | 46.5 | 46.8 |

| 08:50 | EUR | France Manufacturing PMI Oct F | 42.6 | 42.6 |

| 08:55 | EUR | Germany Manufacturing PMI Oct F | 40.7 | 40.7 |

| 08:55 | EUR | Germany Unemployment Change Oct | 15K | 10K |

| 08:55 | EUR | Germany Unemployment Rate Oct | 5.80% | 5.70% |

| 09:00 | EUR | Eurozone Manufacturing PMI Oct F | 43 | 43 |

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | 58.20% | |

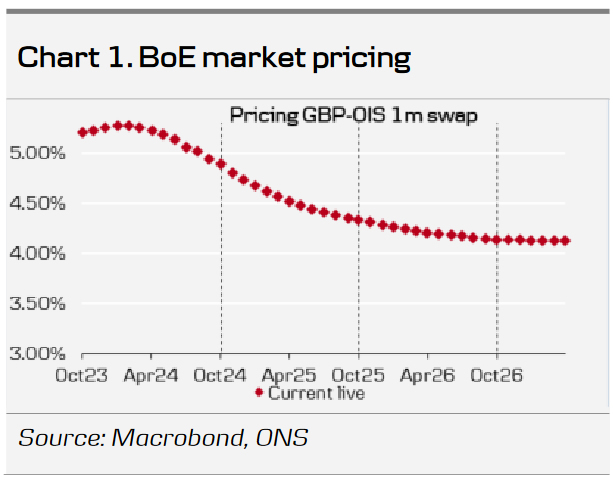

| 12:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% |

| 12:00 | GBP | MPC Official Bank Rate Votes | 2--0--7 | 4--0--5 |

| 12:30 | USD | Initial Jobless Claims (Oct 27) | 210K | 210K |

| 12:30 | USD | Nonfarm Productivity Q3 P | 4.00% | 3.50% |

| 12:30 | USD | Unit Labor Costs Q3 P | 1.10% | 2.20% |

| 14:30 | USD | Natural Gas Storage | 74B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Goods Trade Balance (AUD) Sep | |

| Forecast: 9.58B | Previous: 9.64B | ||

| 07:30 | CHF | CPI M/M Oct | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 07:30 | CHF | CPI Y/Y Oct | |

| Forecast: | Previous: 1.70% | ||

| 08:45 | EUR | Italy Manufacturing PMI Oct | |

| Forecast: 46.5 | Previous: 46.8 | ||

| 08:50 | EUR | France Manufacturing PMI Oct F | |

| Forecast: 42.6 | Previous: 42.6 | ||

| 08:55 | EUR | Germany Manufacturing PMI Oct F | |

| Forecast: 40.7 | Previous: 40.7 | ||

| 08:55 | EUR | Germany Unemployment Change Oct | |

| Forecast: 15K | Previous: 10K | ||

| 08:55 | EUR | Germany Unemployment Rate Oct | |

| Forecast: 5.80% | Previous: 5.70% | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Oct F | |

| Forecast: 43 | Previous: 43 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | |

| Forecast: | Previous: 58.20% | ||

| 12:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 5.25% | Previous: 5.25% | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 2--0--7 | Previous: 4--0--5 | ||

| 12:30 | USD | Initial Jobless Claims (Oct 27) | |

| Forecast: 210K | Previous: 210K | ||

| 12:30 | USD | Nonfarm Productivity Q3 P | |

| Forecast: 4.00% | Previous: 3.50% | ||

| 12:30 | USD | Unit Labor Costs Q3 P | |

| Forecast: 1.10% | Previous: 2.20% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 74B | ||

Friday, Nov 3, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:45 | CNY | Caixin Services PMI Oct | 50.4 | 50.2 |

| 07:00 | EUR | Germany Trade Balance (EUR) Sep | 16.3B | 16.6B |

| 07:45 | EUR | France Industrial Output M/M Sep | 0.00% | -0.30% |

| 09:30 | GBP | Services PMI Oct F | 49.2 | 49.2 |

| 10:00 | EUR | Eurozone Unemployment Rate Sep | 6.40% | 6.40% |

| 12:30 | USD | Nonfarm Payrolls Oct | 172K | 336K |

| 12:30 | USD | Unemployment Rate Oct | 3.80% | 3.80% |

| 12:30 | USD | Average Hourly Earnings M/M Oct | 0.30% | 0.20% |

| 12:30 | CAD | Net Change in Employment Oct | 63.8K | |

| 12:30 | CAD | Unemployment Rate Oct | 5.50% | |

| 13:45 | USD | Services PMI Oct F | 50.9 | 50.9 |

| 14:00 | USD | ISM Services PMI Oct | 53.2 | 53.6 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:45 | CNY | Caixin Services PMI Oct | |

| Forecast: 50.4 | Previous: 50.2 | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Sep | |

| Forecast: 16.3B | Previous: 16.6B | ||

| 07:45 | EUR | France Industrial Output M/M Sep | |

| Forecast: 0.00% | Previous: -0.30% | ||

| 09:30 | GBP | Services PMI Oct F | |

| Forecast: 49.2 | Previous: 49.2 | ||

| 10:00 | EUR | Eurozone Unemployment Rate Sep | |

| Forecast: 6.40% | Previous: 6.40% | ||

| 12:30 | USD | Nonfarm Payrolls Oct | |

| Forecast: 172K | Previous: 336K | ||

| 12:30 | USD | Unemployment Rate Oct | |

| Forecast: 3.80% | Previous: 3.80% | ||

| 12:30 | USD | Average Hourly Earnings M/M Oct | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 12:30 | CAD | Net Change in Employment Oct | |

| Forecast: | Previous: 63.8K | ||

| 12:30 | CAD | Unemployment Rate Oct | |

| Forecast: | Previous: 5.50% | ||

| 13:45 | USD | Services PMI Oct F | |

| Forecast: 50.9 | Previous: 50.9 | ||

| 14:00 | USD | ISM Services PMI Oct | |

| Forecast: 53.2 | Previous: 53.6 | ||

Canadian Economic Data to Reinforce Softer Growth Backdrop

We expect Canadian GDP was unchanged for a second straight month in August (slightly below the preliminary estimate for a 0.1% increase) after dropping 0.2% in June. Wholesale sale volumes increased 0.6% in August, but manufacturing volumes fell 0.7%. Retail sale volumes declined for a third straight month in August (-0.7%) and are tracking more than 2% (annualized) below their Q2 average in Q3 to-date. Our own tracking of card spending also flagged weaknesses in spending on discretionary services like hotels and food services, adding to evidence that consumer spending is wobbling further after coming essentially to a standstill in Q2.

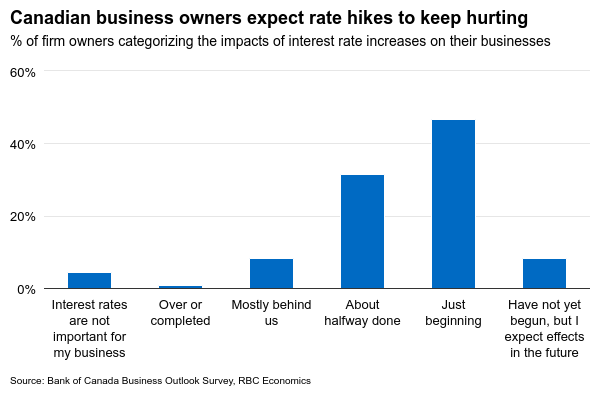

We continue to track a second consecutive quarterly dip in GDP in Q3 after output edged down 0.2% (annualized) in Q2, with those readings both looking substantially softer on a per-capita basis once accounting for surging population growth. And growth headwinds continue to build. More than 45% of businesses in the Bank of Canada’s Q3 Business Outlook Survey felt that the impact of higher interest rates on their businesses has only just begun.

We expect cracks that have begun to show up more clearly in the GDP growth backdrop will also become more evident in labour markets. Employment growth has remained positive in Canada. But with surging population growth boosting available labour supply, the gains have not been strong enough to prevent a half point rise in the unemployment rate since the spring. And labour demand has continued to slow with job openings still drifting lower. We look for another 15k increase in employment in October but alongside a tick higher in the unemployment rate to 5.6%.

Week ahead data watch

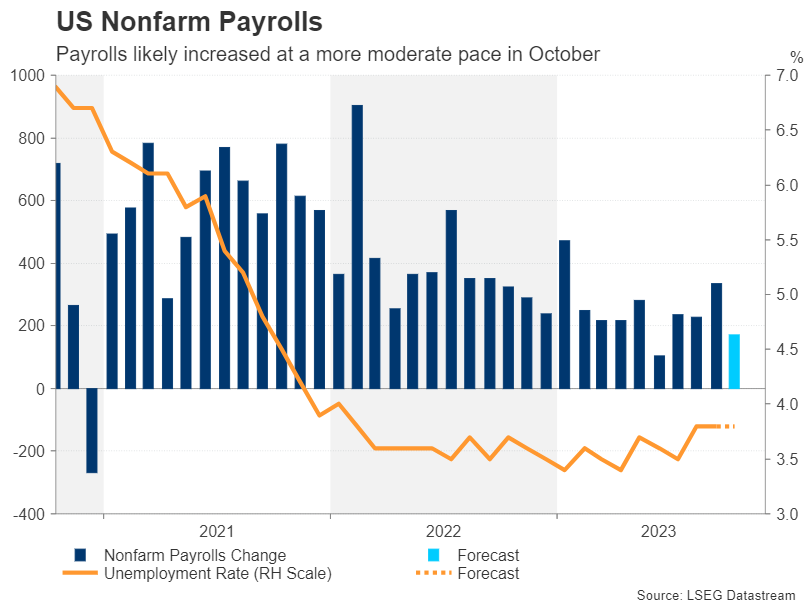

In the U.S., economic data has been substantially stronger, and we look for a 208k gain in payroll employment to be reported next week. Still, labour demand has also been slowing under the surface in the U.S. with job openings drifting lower and wage growth slowing. We look for the unemployment rate to tick up to 3.9% (despite higher employment) after climbing to 3.8% over August and September from 3.5% in July.

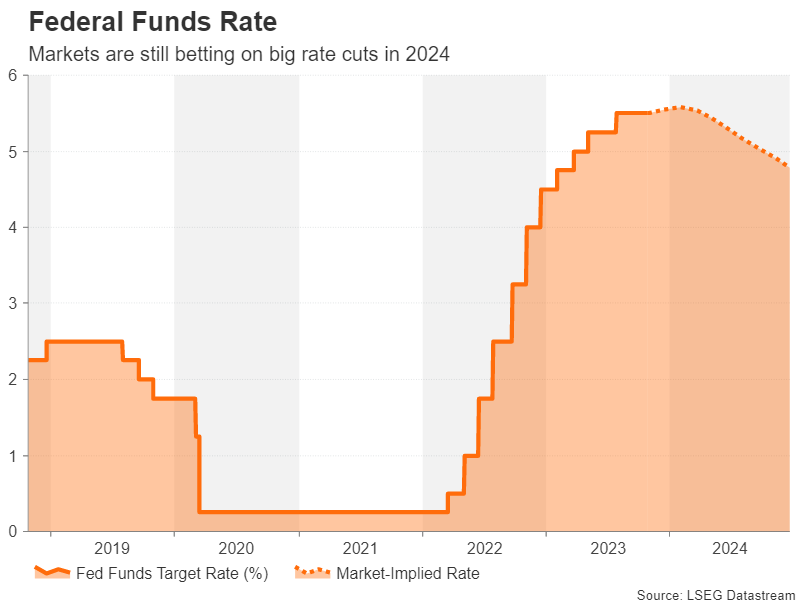

The U.S. Federal Reserve is widely expected to follow in the steps of the Bank of Canada and hold interest rates unchanged again in October after skipping a hike in September. U.S. economic growth numbers have remained exceptionally resilient, but inflation pressures moderated over the summer and that is allowing the Fed room to be patient as they wait for already high interest rates to slow growth with a lag.

Will Fed Officials Reiterate Their ‘Higher for Longer’ Mantra?

- Policymakers argue surge in yields counts as hike

- US economy continues to fire on all cylinders

- Fed to stand pat, but may deliver a hawkish message

- Decision on Wednesday at 18:00 GMT; press conference at 18:30 GMT

Yields do the work for the Fed

Although at their last gathering Fed policymakers maintained their projections of one more hike before the end credits of this tightening cycle roll, they have been appearing in dovish suits recently, signaling that the surge in Treasury yields since then has done the work for them, implying that another hike may eventually not be needed.

They stressed though that for inflation to return to their 2% objective, interest rates need to stay high for a prolonged period, with some of them leaving the door open to additional increases. Minneapolis Fed President Neel Kashkari, who has been an outspoken hawk during this hiking cycle, agreed with his colleagues but added that if long-term yields are higher due to expectations about what the Fed might do, then they may need to satisfy those expectations to maintain yields at those levels. More recently, Fed Chair Powell also acknowledged the role of rising yields, but still left additional action on the table.

Data points to a robust economy

The dollar corrected lower on officials’ yields-related remarks, but with economic data continuing to point to a resilient economy, its losses remained limited and short lived. The latest CPI data showed that headline inflation held steady at 3.7% y/y in September, instead of slowing to 3.6% as expected, while the employment report for the month pointed to a still-tight labor market.

On top of that, Wednesday’s GDP data revealed that the US economy grew by an astounding 4.9% q/q SAAR in Q3, well exceeding the already encouraging forecast of 4.3%, while the preliminary PMIs for October suggested that the world’s largest economy fared better than expected during the first month of the fourth quarter.

Upside risks surround the gathering

Yet, investors are skeptical on whether another hike may be warranted, perhaps as the rally in Treasury yields shows no signs of abating, despite a small rejection from the 5% zone on Monday. According to Fed funds futures, there is only a 30% probability for another 25bps hike by January and around 80bps worth of rate cuts expected by the end of next year.

Taking all that into account, Wednesday’s FOMC decision may attract special attention. Although virtually no one expects policymakers to act, the statement and the press conference may be scrutinized for clues and hints as to whether the door for more tightening remains open and whether the market is correct in penciling in so many basis points worth of rate cuts.

With the US economy still firing on all cylinders, the risks may be tilted towards a hawkish outcome. Even if officials do not hint at another rate increase, there are no economic signs justifying 80bps worth of cuts. Therefore, there is a decent chance for Powell and Co. to reiterate the view that interest rates may need to stay high for longer than the market is currently anticipating to safeguard inflation’s return to their objective.

Dollar set to continue drifting north

If this is the case, traders may be tempted to lift their implied rate path. They may not significantly add to the probability of another hike as a hawkish outcome will also drag Treasury yields higher, but they may scale back a decent amount of basis points worth of rate reductions for next year.

This could prove positive for the dollar. With the Euro area economy in a much worse shape than the US, and investors pricing in around 75bps worth of cuts by the ECB for next year, even after Thursday’s gathering, euro/dollar may be destined to extend its downtrend for a while longer.

Euro/dollar has been on a downward trajectory since July 18. Although it rebounded recently, just this week, it was rejected by the crossroads of the 50-day exponential moving average and the key resistance zone of 1.0665. A hawkish Fed could encourage the bears to reach and breach the low of October 3 at 1.0445. A break lower would confirm a lower low and perhaps aim for the low of November 30, 2022, at around 1.0290.

On the upside, a move back above 1.0665 would just turn the outlook neutral as it will only signal the pair’s return within the sideways range that contained most of the price action between January and September. For the picture to be considered positive, the bulls may need to drive the action all the way above the 1.1070 zone, which is the upper bound of the aforementioned range.

Week Ahead – Will BoJ Steal the Limelight from Fed and BoE?

- Central bank meetings continue in earnest with BoJ, Fed and BoE

- Fed and BoE to likely stand pat, but BoJ might tweak policy again

- NFP report and Eurozone flash GDP and CPI data also in focus

Fed pause likely to be of little relief for yields

Just a few weeks ago the November FOMC meeting was seen as a live one, but expectations of a rate hike have evaporated in the run up to Wednesday’s decision. The latest commentary from Fed officials has corroborated the markets’ view that the bar for further tightening is set quite high. However, as far as the Fed is concerned, it can be said that the bar for a rate cut has also been set very high. Investors have yet to be fully convinced by the higher for longer narrative even though the data supports the Fed’s version of the economy.

So as interest rates are kept on hold for the second straight meeting and in the absence of a new dot plot, investors will be hoping to get some insight on the rates outlook from Chair Powell’s press conference. In his last remarks before the meeting, Powell acknowledged that the tighter financial conditions from surging Treasury yields could lessen the need for further rate increases. But he also pointed out that if growth remains above trend and the labour market stays hot, the Fed may press the hike button again.

It’s unlikely that Powell will diverge much from those comments, although he may elaborate more on the impact of rising yields, which has the potential to spark some volatility should he allude that the Fed is done raising rates.

Will it be another hot jobs report?

But there’s also a risk that Powell may catch traders off guard again with his hawkishness, as US data keeps surprising to the upside, most recently with the advance GDP report. With a busy week lined up for US economic releases, it could be more of the same.

Quarterly wage numbers will be watched on Tuesday, along with the Chicago PMI and consumer confidence index. The ISM manufacturing PMI will be important on Wednesday. The JOLTS jobs openings for September are also due the same day, while on Thursday, factory orders might attract some attention after the very strong durable goods orders for September.

The real highlight, though, will be Friday’s nonfarm payrolls report as well as ISM’s non-manufacturing PMI. Following the shockingly strong 336k print for September, the October figure is predicted to come in a lot lower at 172k. But this would still be in line with a tight jobs market, especially for this late stage of the tightening cycle.

No change is expected for the unemployment rate, but earnings growth may accelerate slightly from 0.2% to 0.3% month-on-month.

Another solid report would likely add fuel to the rally in yields, potentially boosting the US dollar back towards the early October highs against a basket of currencies.

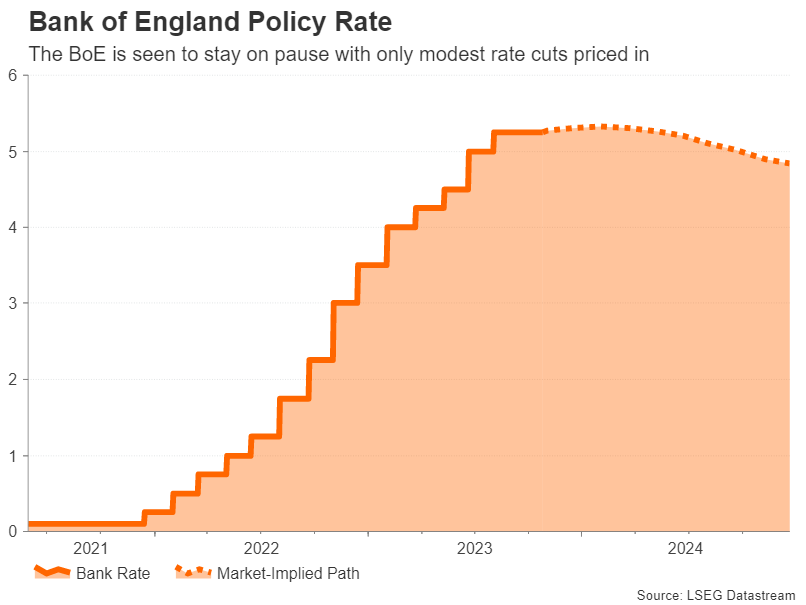

BoE pinning hopes on inflation drop

The Bank of England meets a day after the Fed on Thursday and it’s not expected to hike rates either. After the surprise pause in September, policymakers will probably hold firm on their decision to maintain rates at 5.25%.

The UK’s headline CPI rate unexpectedly held steady at 6.7% y/y in September, but the Bank is confident inflation will resume its decline in October when the new energy price cap came into effect. Hence, with inflation expected to fall sharply, unemployment edging higher and economic growth grinding to a halt, the BoE’s caution seems warranted.

Much of these downside risks have already been priced into sterling but some swings are possible depending on how gloomy or optimistic the BoE’s latest Monetary Policy Report is. When compared to the Fed or European Central Bank, investors see the BoE as being the least aggressive next year when it comes to projected rate cuts even as the economy flirts with a recession. Therefore, anything in the Bank’s forecasts that supports the higher for longer case might offer the pound some support.

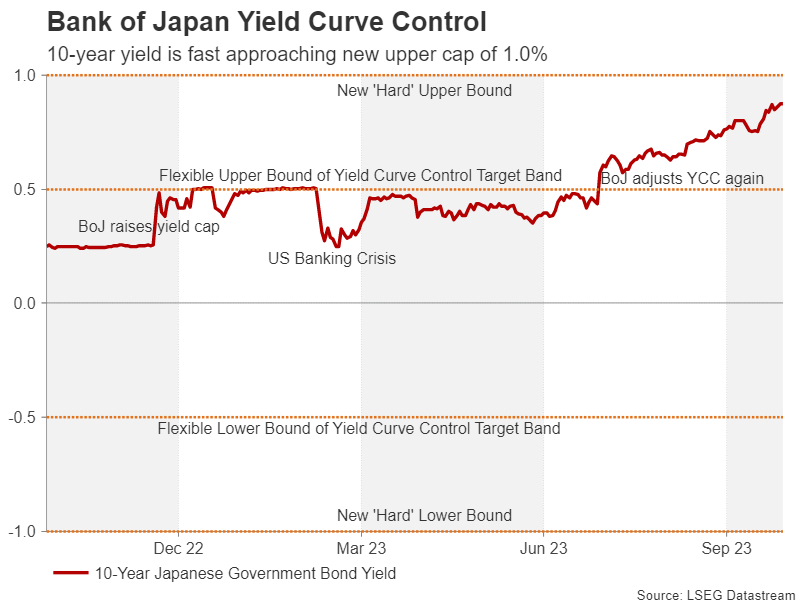

Will the BoJ come to the yen’s rescue?

With both the Fed and BoE set to stay on pause, the Bank of Japan meeting could be the week’s wildcard as there is growing speculation of a surprise policy tweak. According to local news reports, the BoJ is considering whether to raise the cap on the 10-year yield again after doubling it to 1.0% back in July.

Officially, the target band remains at plus or minus 0.5%, but it was tweaked to add some ‘flexibility’. But despite the creative language, there is little doubt the BoJ is well on its way to gradually winding down its ultra-accommodative policies as inflation in Japan has been running above 2% for some time now.

Even if price pressures have somewhat moderated in recent months, the Bank’s updated outlook report is expected to show that core CPI will overshoot the 2% target for the next two fiscal years, giving policymakers the green light to make further adjustments to the yield curve control policy. A relatively buoyant economy is another argument in favour of higher yields.

A further lifting of the yield cap above 1.0% would provide some much needed relief to the yen, which this week breached the 150 per dollar level. Whilst the move hasn’t prompted any intervention yet to defend the yen, the risk is that as long as Governor Ueda refuses to ditch his dovish rhetoric, any boost from a policy tweak would likely be limited.

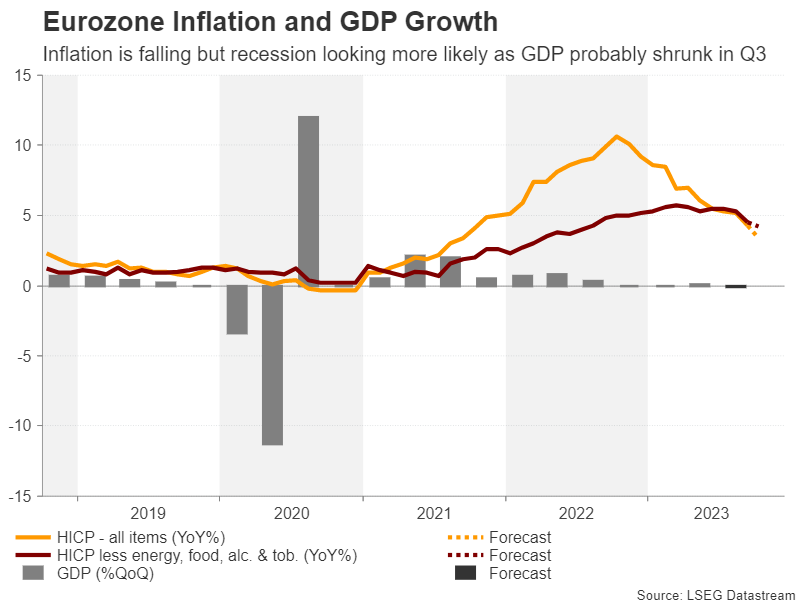

Euro on recession alert as GDP data incoming

The ECB gave its clearest indication yet that Eurozone rates have peaked even as President Lagarde declined to say this outright in her post-meeting press conference this week. But combined with worsening economic indicators and a resilient US economy, the euro is on the slide again and in danger of relinquishing control of the $1.05 handle.

It’s highly doubtful next week’s data will bring much cheer to the euro. The flash CPI readings for October are due on Tuesday, which will be released alongside the flash preliminary estimates of GDP growth in the third quarter.

Headline inflation is expected to have plunged from 4.3% to 3.4% y/y in October and the core measure that excludes all volatile items is forecast to have eased too.

The focus, though, will be on the GDP print, which is expected at -0.1% q/q, possibly signalling the start of a recession.

Can the loonie, aussie and kiwi halt their losses?

In Canada, weaker growth prospects have been weighing on the Bank of Canada’s mind too. Governor Tiff Macklem has hinted that further rate hikes are unlikely after the Bank kept rates steady this week, sending the loonie sharply lower.

Tuesday’s monthly GDP reading and Friday’s employment report for October are not anticipated to significantly alter the outlook for rates, possibly keeping the local dollar on the backfoot.

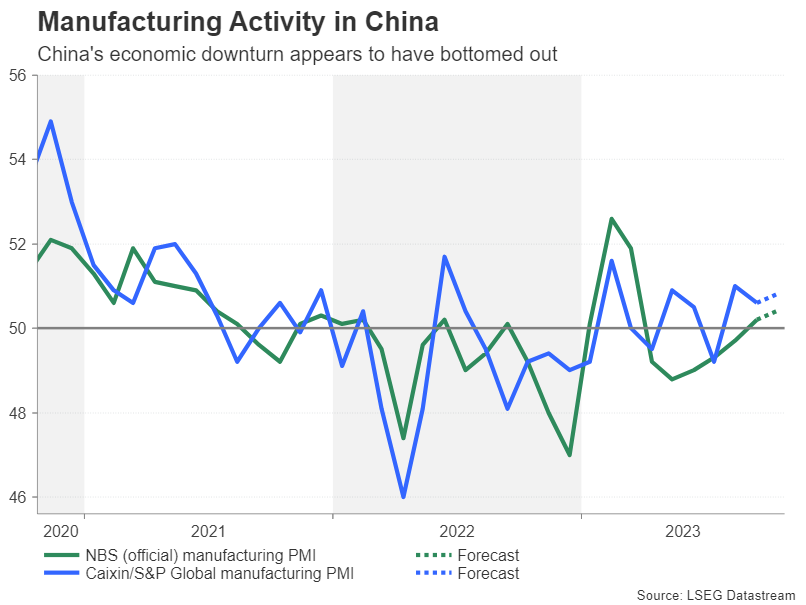

However, its aussie counterpart may receive a modest lift from Chinese PMI figures due on Tuesday and Wednesday should they point to improving sentiment in Australia’s largest export market.

Upbeat PMIs from China may also aid the New Zealand dollar, which has fallen to one-year lows. Kiwi traders will additionally be keeping an eye on New Zealand’s quarterly employment stats, starting with wage numbers on Wednesday and the jobless rate on Thursday.

Bank of England Preview – Soft Data Warrants BoE to Stay On Hold

- We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 2 November, which is in line with current market pricing.

- Overall, we expect the MPC to stick to its previous guidance emphasising the "higher for longer" approach.

- We expect a muted reaction in EUR/GBP but see risks as tilted to the topside.

We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 2 November. This is in line with current market pricing. We expect the vote split to be 6-3 with Greene, Haskel and Mann opting for an additional hike of 25bp and the rest of the MPC including the newest MPC member Sarah Breeden to vote for an unchanged decision. Note, this meeting will include updated projections and a press conference following the release of the statement.

Overall, we expect the MPC to stick to its previous guidance noting that the "current monetary policy stance is restrictive", that they "will ensure that Bank Rate is sufficiently restrictive for sufficiently long" and that "further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures". However, we expect the bar for further hikes down the road to increase adding a slight dovish tilt.

Since the last monetary policy decision in September, data releases have broadly been to the soft side. Wage growth for August was weaker than expected and broadly showing signs of easing in line with the REC and KPMG report, which "tends to lead changes in the official measure of annual wage growth" as noted by the BoE. While monthly GDP for August was overall in line with expectations at 0.2% m/m and 0.3% 3M/3M, growth will most likely be below the BoE forecast for Q3 from the August MPR at 0.4% q/q and the downward revision in September for 0.1% q/q. Likewise, retail sales for September remain weak with retail sales ex auto fuels at -1.0% m/m (-1.2% y/y). UK September inflation came in slightly higher than expected for both headline and core. In m/m SA terms, core inflation pressures remain muted at 0.04% while headline jumped higher to 0.5% on the back of an upward contribution from motor fuels. Importantly, inflation averaged 6.7% in Q3, which is lower than the BoE's forecast of 6.9% y/y. PMI's in September and October broadly remain in contractionary territory with all indices below 50 and continue to signal a gloomy growth outlook. Overall, with unemployment higher, inflation lower and GDP growth lower than expected by the BoE this supports our call of an unchanged decision and by extension the conclusion of the hiking cycle having been reached.

BoE call. We maintain our call that the BoE has delivered its final hike of this hiking cycle, which is in line with current market pricing. We expect the first rate cut of 25bp in June 2024 and subsequently a 25bp cut in the following quarters, totalling of 75bp of cuts for entire 2024.

FX. In our base case of an unchanged decision, we expect a muted reaction in EUR/GBP but on balance see risks as tilted to the topside. We anticipate the press conference to reiterate the MPC's current guidance emphasising the "higher for longer" narrative and the data dependent approach. We continue to forecast EUR/GBP to move modestly higher the coming year to 0.89 on the UK economy performing relatively worse than the euro area.

Weekly Focus – US Outperformance

High yields for longer remains the key narrative driving financial markets. 10-year US treasury yields traded close to 5% weighing on equity markets and JPY, as the contrast to the low yield regime in Japan grows larger still. Strong US data benefitted USD and risk-off sentiment took a toll on cyclically sensitive currencies like SEK and NOK. Oil prices receded back below USD90 per barrel, but energy prices largely remain elevated as markets are volatile and sensitive not least to the development in the Middle East.

The ECB kept rates unchanged for the first time since June last year and guided that they are done with additional rate hikes. President Lagarde made an effort not to rock the boat in terms of market pricing, she succeeded well and gave indications that this was a stock taking meeting only. Earlier this week, ECB's bank lending survey also highlighted that the transmission mechanism is working as banks' credit standards continue to tighten and firms and households' demand for loans has declined significantly.

PMI data indicates growth divergence between the euro area and the US. The euro area is likely in the midst of a technical recession, with composite PMI declining further to 46.5, significantly below consensus as the manufacturing recession accelerated further in October and the service sector also weakened more than expected. Germany is a key driver of the weak figures, however the much more extensive IFO survey does paint a less dire picture of the largest euro area economy and thus leaves a less downbeat impression. US PMI data was better than expected and the Q3 national accounts emphasised how solid the US economy really is, with annualised q/q GDP growth of 4.9%, primarily driven by very strong private consumption. Core PCE inflation was slightly below expectations, though, which drove US yields somewhat lower.

The Japanese data indicated, the economic recovery has lost some steam with composite PMI at 49.9, below the 50-threshold for the first time this year. Even so, we think the data supports another tweak of the yield curve control by the Bank of Japan (BoJ) this year, most likely at the meeting ending on Tuesday, with the most likely move as an increase in the de facto 10Y yield cap to 1.5%. The recent surge in global yields has also prompted the BoJ to intervene in JGB markets several times recently.

In the euro area, we expect a large decline in October headline inflation to 3.1% from 4.4% in September on the back of a large negative contribution from energy prices but also a continuation of the fading underlying price momentum we have seen in Q3. We expect, Eurostat's first estimate of Q3 GDP growth will reveal a small decline in economic activity.

It will be a very busy week in the US with FOMC meeting and several key data releases. We expect the Fed to remain on hold in line with consensus and market expectations, and look for no further hikes at a later stage either. We expect nonfarm payrolls growth to cool back towards the pre-September trend at +180k, yet still continue illustrating solid labour market conditions. Policymakers will keep a close eye on the earnings growth as well as the Q3 employment cost index to gauge how underlying inflation risks are developing.

Sunset Market Commentary

Markets

The first governors already hit the wires today after yesterday’s ECB meeting. Muller (Estonia), Vasle (Slovenia) and Nagel (Germany) all carry a hawkish label but seem to be at peace with the ECB holding rates steady for the first time in more than a year. They said that inflation remains too high but monetary policy is showing effect and should keep disinflation going. For Muller it’s the economy that will determine how long rates stay at their peak. He expects some stagnation before a gradual recovery in 2024. Nagel pulled the data-dependency card, with future decisions made on a meeting-by-meeting basis. Their comments didn’t have much impact on markets though. German Bunds eke out small gains in what is mainly technically inspired trading. Yields ease 1.1-3.4 bps with the front outperforming. US Treasuries marginally underperform after rallying yesterday. The front end of the curve loses less than 2 bps. Longer tenors add 0.3-2 bps with the 30-y aiming for a close above 5%. Economic data included decent to strong personal income (0.3%) and spending (0.7%) but were offset by September (core) deflators just missing the bar due to a downward 0.1 ppt revision of the August reading. We wouldn’t draw any conclusion from today’s market moves anyway, not with the huge batch of key eco indicators and events looming next week. Get ready for European Q3 GDP and October inflation numbers, the US October labour market report and ISM business confidence and of course the FOMC policy meeting. The Czech National Bank, Norges Bank, Bank of England & the Bank of Japan gather as well.

Stocks trade pretty volatile. The EuroStoxx50 swung from losses to gains back to losses (twice). All indices on Wall Street opened with gains but only the S&P500 (+0.1%) and Nasdaq (0.80%) can currently maintain some of them. Though fragile, the minor improvement in risk appetite lifts the euro from the daily lows. EUR/USD is trying to find a spot back above the upward sloping October trendline again (1.0585). DXY trades a tad lower at 106.54. The Japanese yen gets some relief. USD/JPY might close the week below 150, the level at which Japanese authorities stepped in back in October last year. Sterling is absolutely going nowhere just north of 0.87. Outperforming today is the Australian dollar, in part thanks to a 1% gain in oil. The Swiss franc underperforms G10 peers.

News & Views

Today, the ECB published the results of the survey of professional forecasters for the fourth quarter of 2023. Respondents made limited revisions to headline inflation (HICP) expectations for the 2023-25. Headline HICP inflation was expected to decline from 5.6% in 2023 to 2.7% in 2024 and 2.1% in 2025. Expectations for 2023 were revised upward by 0.1 percentage points, those for 2024 were unchanged, and those for 2025 were revised downward by 0.1 percentage points. The upward revision for the short-term was reportedly reflected higher oil prices. Expectations for core inflation for 2024 (2.9% from 3.1%), for 2025 (2.2% from 2.3%) and for the longer term (2.0%) also were downwardly revised. So, respondents still expect inflation to return close to target at the end of the ECB’s policy horizon. Forecasters also downwardly revised expectations for growth this year (0.5% from 0.6%) and growth in 2024 (0.9% from 1.1%). 2025 growth (1.5%) and long term growth were seen unchanged. Despite lower growth, forecasters still saw the profile for the unemployment rate slightly lower of the forecast horizon (6.5%, 6.7% and 6.6% in 2023-25).

Retail sales in Sweden for the month of September again were reported weaker than expected. Sales volumes decreased 1.4% from August. Only a modest 0.3% decline was expected. Sales also were 3.8% lower compared to the same month last year. The negative monthly dynamic questions a trend of cautious bottoming that potentially developed since spiring. Poor growth and the impact of rising interest rates on highly indebted consumers complicates the task of the Riksbank to address still too high inflation in a more decisive way. At EUR/SEK 11.81, the koruna continues fighting an uphill battle. This occurs even as the Riksbank today announced that it again sold $ 360 mln and € 95 mln of reserves related to its program to hedge part of its FX reserves (week ending 13 Oct).