Sample Category Title

Germany: What Drives Recent Divergence Between Employment and GDP?

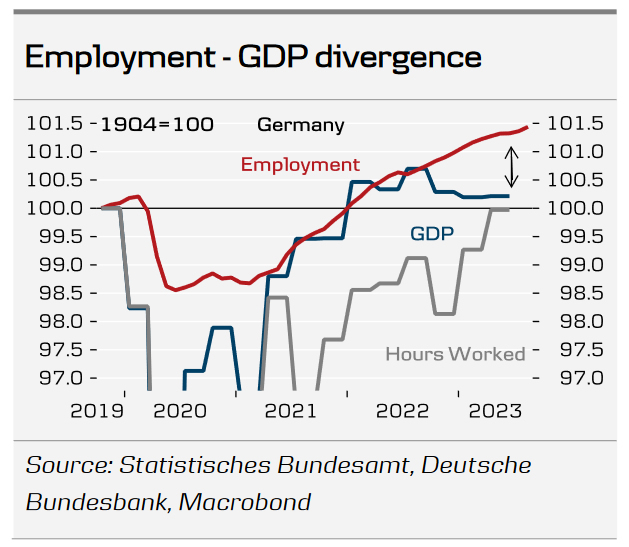

- The German labour market has remained remarkably strong despite weak economic activity overall. While GDP has fallen since 2022Q3 employment has increased continuously.

- We find that the major drivers behind strong employment growth in Germany is strong public sector employment growth and part-time employment.

- Also demographics, and a larger share of service sector employment drive the divergence between employment and GDP.

On the surface the German labour market has defied gravity by recording continuous increases in employment during the last year despite the slump in economic activity. Employment has increased with around 1.5% since 2019Q4 while GDP is broadly unchanged. However, beneath the surface we find that total hours worked has increased less than the number of employed persons since the share of part-time workers increased from 27.9% in 2019Q4 to 30.2% in 2023Q2. This reduction in average working time is one driver of the recent divergence between employment and GDP.

The reduction in average time worked per employee also happened during the global financial crisis as German companies have the option to reduce working time for employees instead of laying them off due to the so-called 'kurzarbeit' schemes.

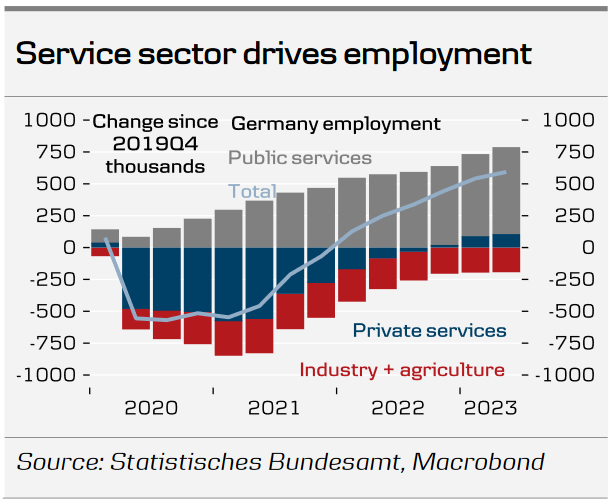

The rise in (public) service sector employment also explains why employment has been so strong compared to GDP. Employment in the public sector has increased each quarter since 2019Q4 except for one, and accounts for 115% of total employment growth. Private employment in the industry is still below pre-pandemic levels. The German industry has been in contraction since 2022Q3 and since then the private service sector has accounted for 80% of the employment increase in the private sector. Productivity is lower in both the public and private service sector compared to the industry as the industry has more capital per worker.

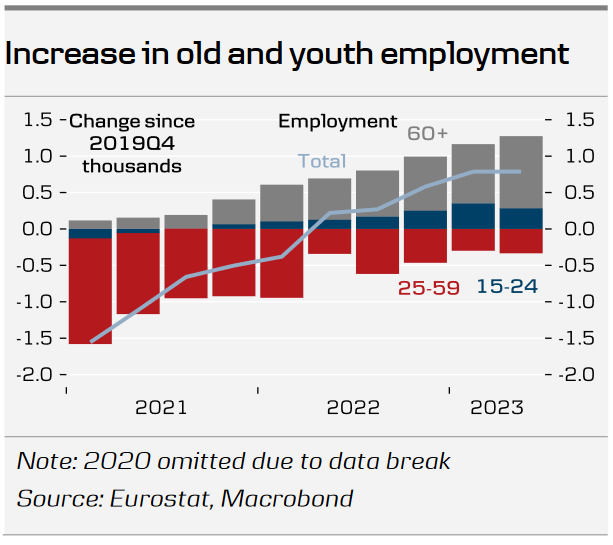

The recent labour market demographics is another explanation of the relatively strong aggregate employment figures. The German labour force is ageing and the number of employees above 60 years has increased with one million since 2019Q4. An ageing work force can affect productivity both positively and negatively but the majority of the effects are negative (see IMF - The Impact of Workforce Aging on European Productivity). Moreover, the share of part-time employment is larger for both old (23.3%) and young (25.7%) employees compared to prime working age employees (19.4%).

Taking stock of the current situation in the German economy high frequency indicators suggest that employment continued to increase in 2023Q3 driven by the service sector while GDP declined further. In the coming quarters, we expect employment to start declining as the monetary policy tightening works its' way through the economy to the labour market and economic activity becomes so weak that companies stop hoarding labour. Yet, we still foresee a tight labour market with the unemployment rate only marginally higher in 2024 as companies utilise the 'kurzarbeit' employment schemes.

BTCUSD Finds Strong Support at 50-day SMA

- Bitcoin pulls back after rejection at 200-day SMA

- Decline ceases at the 50-day SMA

- Momentum indicators point to more losses

BTCUSD (Bitcoin) had been forming a structure of higher highs and higher lows since its bounce off the September bottom of 24,915. However, the price has been on the retreat in the last few daily sessions after being repeatedly repelled by the 200-day simple moving average (SMA).

If selling interest intensifies and the price crosses below the 50-day SMA, the September support of 25,980 could act as the first line of defence. Piercing through that floor, the digital coin might then descend towards the September low of 24,915 before the June bottom of 24,750 gets tested.

On the flipside, bullish actions could propel the price towards the September resistance of 27,490 ahead of the recent peak of 28,592. Even higher, the crucial 30,000 psychological mark could curb further advances. A jump above that zone may pave the way for the April peak of 31,064.

Overall, BTCUSD appears to be undergoing a correction, but the 50-day SMA proves to be a tough hurdle for the bears. Hence, a break below the latter could trigger a steep decline.

Sunset Market Commentary

Markets:

Today centered around US September CPI inflation numbers. They printed… nearly bang in line with consensus. Headline CPI rose by 0.4% M/M (vs 0.3%) while core CPI increased 0.3% M/M (in line). The headline Y/Y-figure stabilized at 3.7%. The core slowed as forecast from 4.3% to 4.1%. The disinflationary process thus runs as expected. Up until last week, these inflation numbers together with stronger payrolls figures would have backed the case of the majority of Fed governors which want to raise the policy rate one final time this year. However, the correction since the start of this week driven by Fed comments now suggest that today’s inflation data back the case for a hold at the November policy meeting. Consensus is building in the US central bank that the yield increase since the latest Fed meeting (+50 bps at one stage) and since the previous Fed rate hike (+100 bps at one stage) substitutes for that final hike. The market reaction was interesting and actually quiet similar (but opposite) to last Friday’s payrolls. Last week, bearish bond sentiment entered exhaustion stages with strong payrolls unable to push bonds below sell-off lows. This time around, we’re in (bond) correction territory with today’s in line with consensus data triggering a test of the bond rebound highs but unable to push them above. To us, this suggests that from now on, we entered a sideways trading pattern bordered by the bond sell-off lows of last week and the rebound highs of this week. In yield terms, for the US 10-y gauge we’re talking about the 4.5%-4.9% range going forward. Daily changes on the US yield curve today vary between 8 bps (2-yr) and 5.4 bps (30-yr). Germany yields shadow the trend with yields adding 4.2 bps (2-yr) to 3.4 bps (30-yr). The dollar rebounds in the same way as (US) yields with the failed test of technical resistance in EUR/USD (1.0635/43) at play as well. The pair currently trades around 1.0560. European stock markets narrowly cling to gains while US stock markets barely hold their head above water in the opening.

News & Views:

In its October monthly oil market report the International Energy Agency (IEA) sees evidence of demand destruction as US gasoline consumption fell. At the same time, buoyant demand growth in China, India and Brazil, is mentioned as underpinning an expected increase of 2.3 mb/d to 101.9 mb/d in 2023, of which China accounts for 77%. However, according to the IEA assessment, the prospect that ‘higher for longer’ interest rates could slow economic and demand growth. Growth is expected to slow to 900 kb/d in 2024, as efficiency gains and a deteriorating economic climate weigh on oil use. Global output will increase by 1.5 mb/d and 1.7 mb/d in 2023 and 2024, respectively, to new record highs, driven by non-OPEC+ growth. Overall OPEC+ output is set to decline in 2023, although Iran may rank as the world’s second largest source of growth after the United States. Voluntary cuts are expected to keep the oil market in deficit in 2023. If extra cuts are unwound in January, the balance could shift to surplus, which would go some way to help replenish depleted inventories, which tumbled sharply in August. Oil today reversed yesterday’s decline with brent rebounding to $87.40/b.

The BoE published its credit conditions survey, a mostly qualitative assessment of supply and demand conditions derived from a questionnaire at Banks and Building societies. On the supply side, lenders reported that the availability of secured and unsecured credit to households decreased in the three months to end-Aug 2023 (Q3). It was expected to decrease slightly further over the next three months or stay unchanged. Overall availability of credit to the corporate sector was unchanged. Small business availability slightly increased while availability of credit to medium and large businesses remained unchanged in Q3. Overall availability was expected to be unchanged in Q4. On the demand side, demand for secured lending for house purchases decreased which is expected to continue in Q4. Demand for overall unsecured lending (including credit card lending) increased in Q3 and is also expected to do so in Q4. Demand for corporate lending from small businesses was unchanged, but decreased for medium-sized businesses and large firms. Lenders also reported spreads for most categories of lending to have decreased in Q3. Default rates for most categories of lending were expected to rise in Q4, except for large businesses.

US: Core Inflation Continues to Drift Lower, giving policymakers enough breathing room to remain on pause at November meeting

Core inflation continues to drift lower, giving policymakers enough breathing room to remain on pause at November meeting

The Consumer Price Index (CPI) rose 0.4% month-on-month in September, marking a deceleration from August's 0.6% m/m gain, and coming in a tick above the consensus forecast. On a twelve-month basis, headline inflation held steady at 3.7% .

- Energy prices rose 1.5% m/m, largely driven by a further increase in gasoline prices (+2.1% m/m). Food prices rose 0.2% m/m – matching August's monthly gain – as prices for 'food away from home' accelerated (to 0.4% m/m from 0.3% m/m), while prices for 'food at home' (0.1% m/m from 0.2% m/m) slowed.

Excluding the direct effects of food & energy, core inflation rose 0.3% m/m – matching August's gain. The twelve-month change continued to edge lower – falling 0.2 percentage points to 4.1% – though the truncated three-month annualized change rose to 3.1% (from 2.4% in August).

Price growth across services accelerated 0.6% m/m (from 0.4% m/m in August), which was the strongest monthly gain since February 2023.

- Shelter costs were a key factor pushing overall service costs higher, driven primarily by an acceleration in owners' equivalent rent (rising by 0.6% m/m from 0.4% m/m in August). Meanwhile, rent of primary residence (+0.5% m/m) matched August's gain.

- Non-housing services (aka the CPI measure of 'supercore') also accelerated last month, rising 0.6% m/m (from 0.4% m/m in August), pushing the twelve-month change to a six-month high of 4.6%.

Goods prices remained in deflationary territory for the fourth consecutive month, falling 0.4% m/m. Used vehicle prices (-2.5% m/m) accounted for the bulk of the pullback, though apparel (-0.8% m/m) and medical commodities (-0.3% m/m) also saw a small pullback in price growth.

Key Implications

The September CPI reading delivered few surprises, with the core measure coming in bang-on expectations, and headline just a tick higher. While the monthly price gains for core inflation have firmed in August/September (+0.3% m/m) relative to the July/August (+0.2% m/m) readings, the underlying trend on core remains favorable. The twelve-month change now sits at a two-year low while the more recent three-month annualized trend is running at an even softer 3.1%.

That said, there's still a lot of ground to cover before returning inflation to 2% and given the continued resilience of the labor market, there's plenty of opportunity for progress to stall over the coming months. The recent tightening in financial conditions will likely give policymakers enough breathing room to hold rates steady at its next interest rate announcement on November 1st. But unless the labor market shows clear evidence of cooling over the coming months, another rate hike later this year seems very likely.

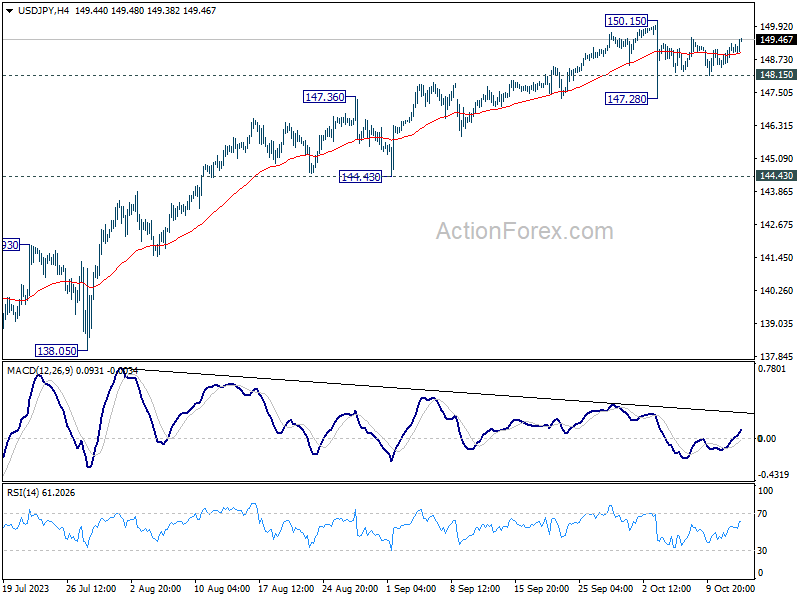

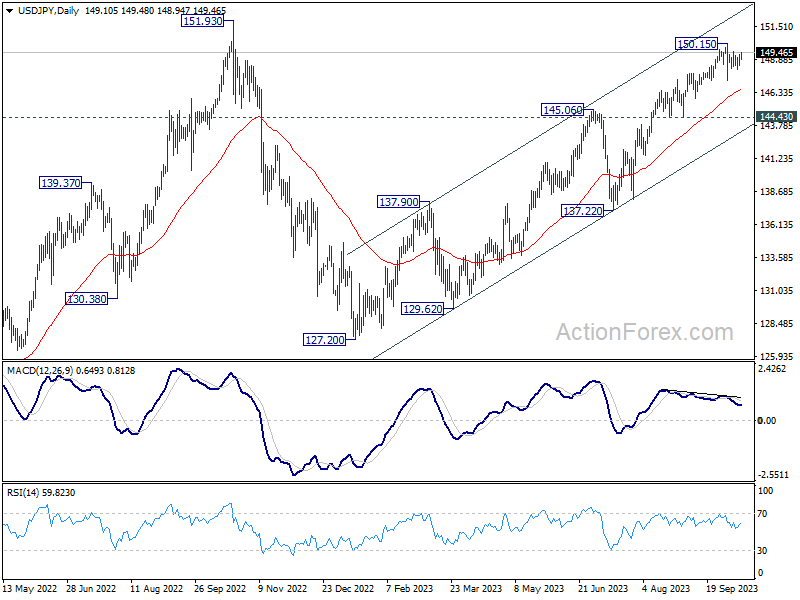

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.63; (P) 148.97; (R1) 149.52; More...

USD/JPY recovers mildly today but stays in consolidation from 150.15. Intraday bias remains neutral for the moment. On the downside, below 148.24 minor support will turn bias to the downside for another down leg through 147.28. But there is no confirmation of bearish trend reversal before firm break of 144.43 support. Another rally remains mildly in favor through 150.15 to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

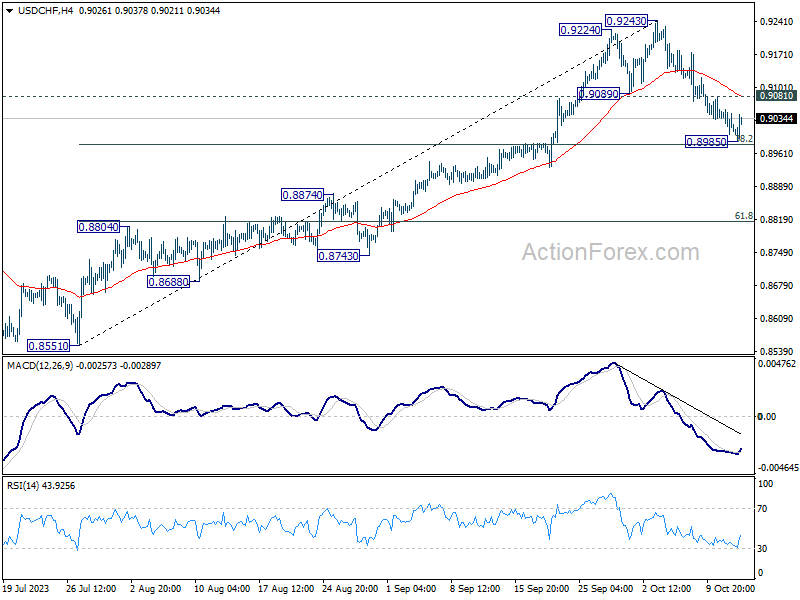

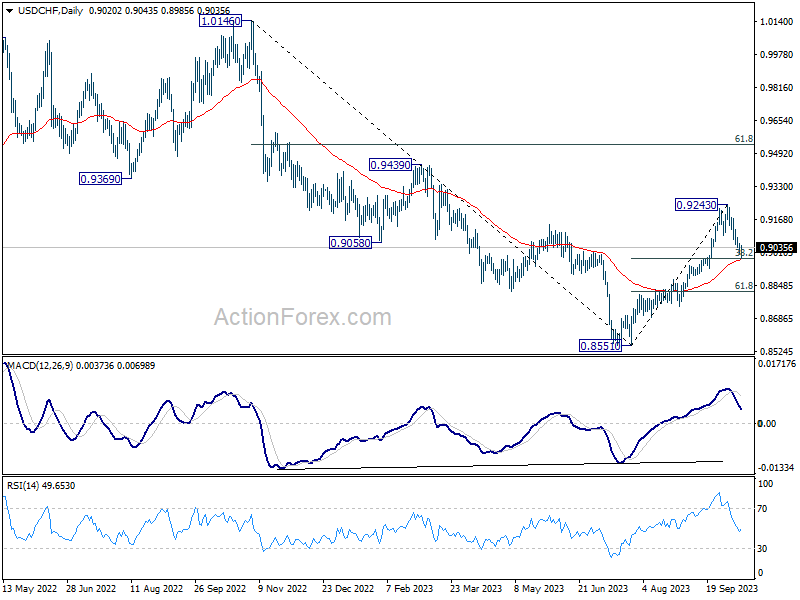

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8996; (P) 0.9026; (R1) 0.9049; More....

Intraday bias in USD/CHF is turned neutral first with current recovery. On the upside, above 0.9081 will argue that pull back from 0.9243 has completed at 0.8985, just ahead of 38.2% retracement of 0.8551 to 0.9243 at 0.8979. Intraday bias will be turned back to the upside for retesting 0.9243 high. Nevertheless, sustained break of 0.8979 will argue that deeper fall is under way to 61.8% retracement at 0.8815.

In the bigger picture, current development indicates that rise from 0.8551 is reversing whole down trend from 1.0146. Further rally would then be seen to 61.8% retracement at 0.9537 and above. For now, this will be the favored case as long as 55 D EMA (now at 0.8971) holds, even in case of deep pullback.

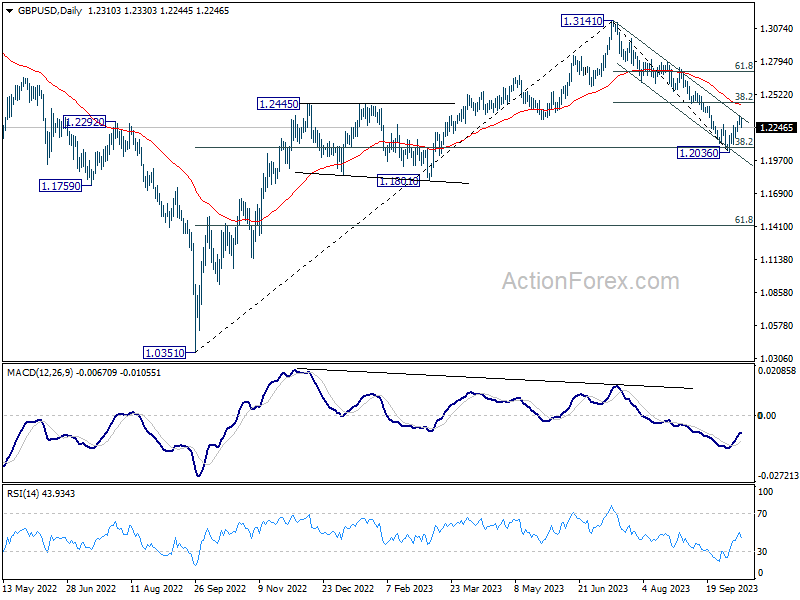

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2276; (P) 1.2307; (R1) 1.2344; More

Intraday bias in GBP/USD is turned neutral first with current retreat. On the upside, firm break of near term channel resistance (now at 1.2334) will target 38.2% retracement of 1.3141 to 1.2036 at 1.2458 next. Nevertheless, break of 1.2210 minor support indicate rejection by falling trendline resistance, and bring retest of 1.2036 low.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2440) holds, in case of rebound.

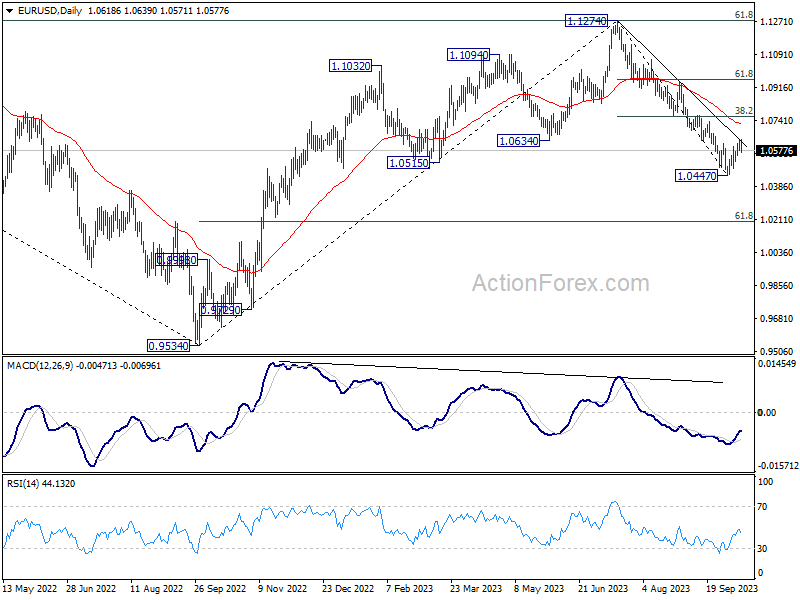

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0588; (P) 1.0611; (R1) 1.0643; More...

Intraday bias in EUR/USD is turned neutral first with current retreat. On the upside, break of 1.0639 will resume the rebound from 1.0447 to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763). On the downside, though, break of 1.0518 will indicate rejection by near term trend line resistance. Intraday bias will be back on the downside for resuming the fall from 1.1274 through 1.0447.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0719) holds, in case of rebound.

CPI Sparks Mild Dollar Rally, Jury’s Still Out on Sustained Momentum

Dollar is showing signs of revival in early session, in the wake of the release of CPI data, which indicated a marginally stronger headline inflation than anticipated. This uptick is further supplemented by a parallel recovery in treasury yields, lending some support to the greenback. However, any substantial upside for Dollar remains in check, as stock futures are holding steady, underscoring a lack of significant market jitters in response to the inflation data. Overall, while the momentum of Dollar's pull back this week has clearly receded, it remains to be seen if it is reversing.

For the day, Canadian Dollar and Swiss Franc are vying for top spots, closely trailing the greenback. Meanwhile, Australian and New Zealand Dollars are lagging, registering as the day's underperformers. British Pound is also on the weaker side, even though monthly GDP data showcased a return to growth. Euro presents a mixed picture, following the revelation from ECB meeting accounts about the narrowly-decided stance of most policymakers on the September rate hike. Yen, in a similar vein, is somewhat directionless, though there's apparent interest in pushing it closer to 150 mark against Dollar.

On the technical front, key levels across several currency pairs are in focus, including 1.0518 support in EUR/USD, 1.2110 support in GBP/USD, 0.9081 resistance in USD/CHF, and 1.3674 resistance in USD/CAD. A simultaneous break of these level is needed to offer a more unequivocal affirmation of Dollar's underlying bullish momentum, thus confirming the end of its near term correction.

In Europe, at the time of writing, FTSE is up 0.63%. DAX is up 0.24%. CAC is up 0.18%. Germany 10-year yield is up 0.023 at 2.749. Earlier in Asia, Nikkei rose 1.75%. Hong Kong HSI rose 1.93%. China Shanghai SSE rose 0.94%. Singapore Strait Times rose 0.81%. Japan 10-year JGB yield fell -0.0236 to 0.755.

US CPI rose 0.4% mom in Sep, core CPI up 0.3% mom

In September, US CPI rose 0.4% mom above expectation of 0.3% mom. CPI core (ex-food and energy) rose 0.3% mom, matched expectations. Energy index rose 1.5% mom. Food index rose 0.2% mom.

Over the last 12 months. CPI was unchanged at 3.7% yoy, above expectation of 3.6% yoy. CPI core slowed from 4.3% yoy to 4.1% yoy , matched expectations. Energy index was down -0.5% yoy while food index was up 3.7% yoy.

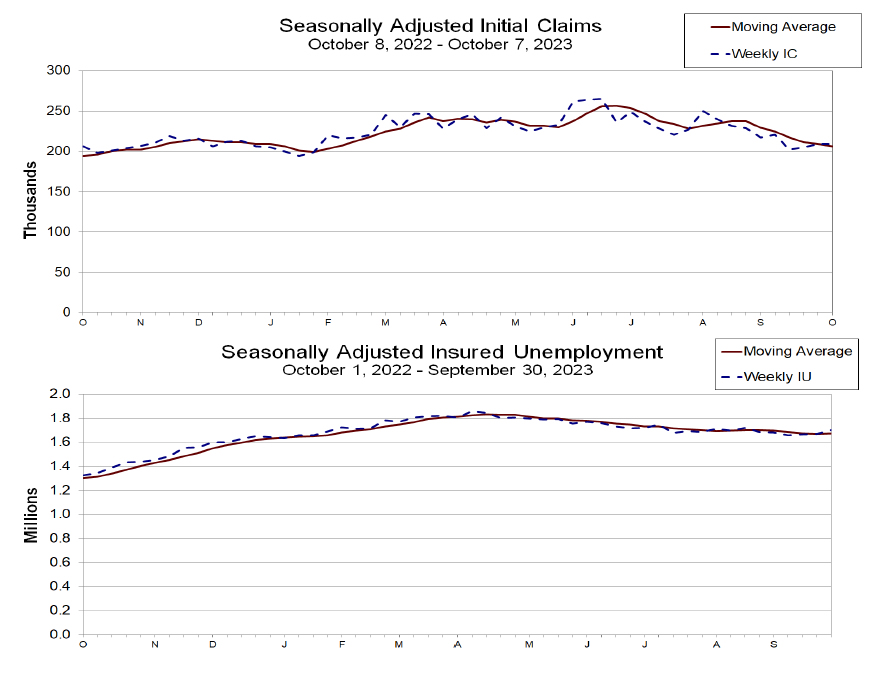

US initial jobless claims unchanged at 209k

US initial jobless claims was unchanged at 209k in the week ending October 7, below expectation of 215k. Four-week moving average of initial claims fell -3k to 206k. Continuing claims rose 30k to 1702k in the week ending September 30. Four-week moving average of continuing claims rose 5k to 1674k.

BoE's Pill: The question of sufficient policy action more finely balanced

BoE Chief Economist Huw Pill noted today that the pressing question of whether tightening has been adequate to curb high inflation is becoming "more finely balanced".

Over the past two years, the BoE has executed 14 consecutive interest rate hikes, a strategy that is still in the process of fully impacting the economy. "We have done a lot over the last two years. A lot of that policy is still to come through," Pill told a panel discussion at IMF meetings in Morocco.

But, "Whether we've done enough - or whether we have more to do - I think is becoming a more finely balanced issue," he added. Despite this, Pill assured that the bank remains committed to ensuring inflation returns to the 2% target on a lasting basis.

On the topic of potentially reducing rates, Pill deemed such conversations premature. He reaffirmed the bank's position that high borrowing costs are likely to be maintained for a duration.

UK GDP shows modest 0.2% mom growth in Aug, services the sole contributor

UK's GDP data for August reveals a mixed bag of results, characterized by modest growth and a sector-specific performance variance. The economy grew by 0.2% mom, aligning with market expectations

Dissecting the numbers, the services sector emerges as the sole contributor to GDP growth, registering a 0.4% mom increase. Contrastingly, the production output faced a downturn, shrinking by -0.7% mom , while the construction sector similarly contracted by -0.5% mom .

In a more expansive view, the 0.3% rise in GDP over the three months leading to August paints a picture of gradual, albeit inconsistent, economic expansion.

In this three months period, production led the charge with a 1.2% increase, highlighting a resilient manufacturing and industrial segment that counters the monthly dip in August. Construction also showed promise with a 0.9% rise, indicating a level of sustained activity in infrastructure development over the quarter. Services, though only increasing by a marginal 0.1%, maintained its positive contribution.

ECB Minutes: Despite being close call, solid majority back rate hike in Sep

Minutes from ECB's meeting held on 13-14 September 2023 revealed that "a solid majority of members" supported for the 25bps rate hike, event though the decision was described as a "close call".

These members were particularly concerned about the persistently high levels of inflation. They stressed the importance of the rate increase as it would "signal a strong determination" to bring inflation back to the target in a timely manner." The emphasis was on ensuring that the duration to realign inflation to the 2% target "should not extend beyond 2025."

A significant concern raised was the potential misinterpretation of ECB's commitment if there was a decision to pause. The minutes noted that "erring on the side of pausing the first time the decision was a close call could risk being interpreted as a weakening of the ECB's determination," especially given the backdrop of both headline and core inflation rates were above 5%.

Furthermore, it was highlighted that any such pause in the rate-setting process might be misconstrued, fueling market speculations that "the tightening cycle was over." Such speculation, the members argued, "increased the risk of a rebound in inflation."

ECB's Stournaras cautions against hasty monetary tightening amid rising geopolitical risks

ECB Governing Council member Yannis Stournaras emphasized caution against tightening monetary policy further today. He noted borrowing costs had already risen since the ECB's last policy meeting as a result of higher bond yields. Furthermore, given that minimum reserves are not subject to remuneration, the total interest dispensed by the 20 Eurozone central banks to their respective commercial banks would see a decline.

He noted borrowing costs had already risen since the ECB's last policy meeting as a result of higher bond yields. Furthermore, given that minimum reserves are not subject to remuneration, the total interest dispensed by the 20 Eurozone central banks to their respective commercial banks would see a decline.

Stournaras expressed skepticism regarding any immediate shift towards a tighter monetary stance. He articulated, "For the moment I see no reason why we should tighten monetary policy now because increasing the minimum requirements will imply monetary policy tightening."

He also responded to suggestions from some counterparts on an early end to the ECB's PEPP bond-buying initiative. Stournaras emphasized the importance of maintaining this tool, especially in the current context marked by significant geopolitical uncertainties.

He stated, "I see no value in bringing it (the end) forward especially now under the new uncertainty we have because of the events in Israel and Palestine." Reiterating ECB's need to retain its adaptability, he concluded, "So we need to keep our flexibility and act if necessary."

Japan's PPI slows to 2% yoy in Sep, trailing CPI core for the first time since 2021

Japan PPI slowed from 3.3% yoy to 2.0% yoy in September, below expectations of 2.3%. That's the lowest level since March 2021. Also, PPI is now below CPI core (at 3.1% yoy) for the first time since early 2021.

Import price index was unchanged at -15.6% yoy, the sixth month of decline. Export price index rose for the first time in seven months, up 0.2% yoy, comparing to prior month's -0.7% yoy.

For the month, PPI fell -0.3% mom. Import price index rose 0.6% mom. Export price index rose 0.5% mom.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0588; (P) 1.0611; (R1) 1.0643; More...

Intraday bias in EUR/USD is turned neutral first with current retreat. On the upside, break of 1.0639 will resume the rebound from 1.0447 to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763). On the downside, though, break of 1.0518 will indicate rejection by near term trend line resistance. Intraday bias will be back on the downside for resuming the fall from 1.1274 through 1.0447.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0719) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance Sep | -69% | -68% | ||

| 23:50 | JPY | Bank Lending Y/Y Sep | 2.90% | 3.10% | 3.10% | |

| 23:50 | JPY | PPI Y/Y Sep | 2.00% | 2.30% | 3.20% | 3.30% |

| 23:50 | JPY | Machinery Orders M/M Aug | -0.50% | 0.70% | -1.10% | |

| 00:00 | AUD | Consumer Inflation Expectations Oct | 4.80% | 4.60% | ||

| 06:00 | GBP | GDP M/M Aug | 0.20% | 0.20% | -0.50% | -0.60% |

| 06:00 | GBP | Industrial Production M/M Aug | -0.70% | -0.20% | -0.70% | -1.10% |

| 06:00 | GBP | Industrial Production Y/Y Aug | 1.30% | 1.70% | 0.40% | 1.00% |

| 06:00 | GBP | Manufacturing Production M/M Aug | -0.80% | -0.40% | -0.80% | -1.20% |

| 06:00 | GBP | Manufacturing Production Y/Y Aug | 2.80% | 3.40% | 3.00% | 3.10% |

| 06:00 | GBP | Goods Trade Balance Aug | -16.0B | -15.2B | -14.1B | -13.9B |

| 11:30 | EUR | ECB Meeting Accounts | ||||

| 12:00 | GBP | NIESR GDP Estimate (3M) Sep | -0.10% | 0.20% | 0.30% | |

| 12:30 | USD | Initial Jobless Claims (Oct 6) | 209K | 215K | 207K | |

| 12:30 | USD | CPI M/M Sep | 0.40% | 0.30% | 0.60% | |

| 12:30 | USD | CPI Y/Y Sep | 3.70% | 3.60% | 3.70% | |

| 12:30 | USD | CPI Core M/M Sep | 0.30% | 0.30% | 0.30% | |

| 12:30 | USD | CPI Core Y/Y Sep | 4.10% | 4.10% | 4.30% | |

| 14:30 | USD | Natural Gas Storage | 85B | 86B | ||

| 15:00 | USD | Crude Oil Inventories | -0.4M | -2.2M |

US initial jobless claims unchanged at 209k

US initial jobless claims was unchanged at 209k in the week ending October 7, below expectation of 215k. Four-week moving average of initial claims fell -3k to 206k.

Continuing claims rose 30k to 1702k in the week ending September 30. Four-week moving average of continuing claims rose 5k to 1674k.