Sample Category Title

US Inflation Data Brings Back Speculation of More Fed Rate Hikes

Market movers today

The main release on the global radar today is US consumer confidence from University of Michigan, which also includes the 5-10 year inflation expectations that have dropped slightly in recent months to 2.8% after hitting a peak of 3.1% back in May.

ECB President Christine Lagarde will be speaking on a panel at the IMF autumn meetings.

In the Nordics we get Swedish CPI for September, where we look for core inflation to fall to 6.6% y/y slightly below consensus of 6.7% (see more below). Also the Riksbank will release its first report on the two.

The 60 second overview

US inflation and markets. The big event for global macro and markets over the last 24 hours has been the release of September CPI data out of the US. While core inflation was in line with expectations at 0.3% m/m the headline measure surprised consensus by 0.1pp to the topside at a 0.4% m/m reading corresponding to 3.7% y/y. The data release triggered a sharp reaction in bond markets where yields rose and the curve bear steepened which then transmitted to worsening risk appetite across asset classes, incl. a stronger USD.

While the market reaction was to price in a higher probability of another rate hike from the Federal Reserve - now priced at roughly a c. 40% probability - we highlight the importance of the inflation details. Indeed it was primarily shelter that posted a surprise rise after several months of declines. Not only do we see signs from other indicators that this spike is unlikely to prove persistent but we also highlight that the underlying measures of inflation that the Federal Reserve normally refer actually came in fully in line with expectations. In that regard, we still maintain our call that we have already hit a peak in US policy rates.

Energy. Oil prices have stabilised after the rise earlier in the week. With respect to the war between Israel and Hamas, so far it has not escalated to a point that affects global oil supply. On the data front, the weekly US inventory report was a bearish reading for the oil market. US crude production increased last week and so did commercial inventories. The government also seems to have halted a further rebuild of strategic reserves. We look for oil prices to trade close to current levels near term.

Chinese headline CPI weaker, trade data stronger: Overnight Chinese CPI dropped to 0.0% y/y (consensus 0.1% y/y) in September from 0.1% y/y in August. It puts headline inflation closer to deflation again but mainly due to lower energy and food price inflation. Core inflation stayed unchanged at 0.8% y/y for the third month in a row and we are thus still some way from broad based deflation. Nevertheless, the low inflation is symptomatic of too weak demand relative to supply. Chinese trade data for September, also released this morning, were better than expected with exports rising to -6.2% y/y (consensus -8.0% y/y) from -8.8% y/y. While external demand is still a drag, the headwind is fading a bit. It likely reflects an easing manufacturing recession globally as signalled for example by a rise in ISM manufacturing new orders in recent months. Import growth was also stronger at -6.2% y/y (consensus -6.3% y/y) from -7.3% y/y in August.

German labour market. Yesterday, we published a piece diving into the recent developments in the German labour market. The German labour market has remained remarkably strong despite weak economic activity overall. While GDP has fallen since Q3 2022 employment has increased continuously. We find that the major drivers behind strong employment growth in Germany is strong public sector employment growth and part-time employment. Also demographics, and a larger share of service sector employment drive the divergence between employment and GDP. For more information please see Research Germany: What drives the recent divergence between employment and GDP?, 12 October.

Polish election. Poland goes to the polls this Sunday to elect a new parliament. The incumbent Law and Justice party (PiS) fights to secure its third consecutive term with the United Right coalition. If this happens, we will likely see increased confrontations between Poland and the EU over rule of law concerns in Poland. The recent polls show that neither PiS nor the opposition led by former EU council president Donald Tusk will be able to form a majority government. Although the polls are volatile and uncertain, it seems most likely that the election will result in a hung parliament where the Confederation party - which has not declared its support to any coalition yet - will be the king-maker. If the opposition wins a majority, we expect an immediate policy shift in Poland away from the confrontation with the EU and a reset of the Ukrainian grain import ban. Importantly, EU will likely release the 36€ billion in grants and loans from the pandemic recovery fund (NextGenerationEU) that it currently holds back due to rule of law concerns stemming from the current government. This will significantly boost the Polish economy and we expect to see a positive reaction from markets on the Zloty. Anything else should be negative for the Zloty.

Equities: Global equities fell yesterday mainly driven by US markets. The reasons were clear; a hotter than expected inflation print sent yields higher and equities lower. Interestingly, it did not lead to a defensive rotation! Two of the worst performing sectors were consumer staples and utilities. Yields were still the cause for the underperformance but for very different reasons. Consumer staples have recently reacted negatively to higher yields as this acts as tax on consumption, and high frequency data have shown some signs of weakness. Utilities sold off as investors realise the higher funding cost for a rather indebted sector that is also a part of the expensive and "long duration" green transition.

In US yesterday, Dow -0.5%, S&P 500 -0.6%, Nasdaq -0.6% and Russell 2000 -2.2%. Most Asian markets are in red this morning, reversing the gains from yesterday with the outperformers from yesterday, China and Japan leading the declines. Western futures are spilt, with European futures lower and US futures higher.

FI: US government bond yields moved higher on the back of the US inflation data with 10Y US Treasury yields rising some 15bp compared to a rise of 8bp in the 2Y segment. This had a spill-over effect on the European bond markets where the 10Y German government bond yield rose approx. 7bp combined with a modest steepening of the yield curves.

FX: EUR/USD moved sharply lower following the topside surprise to September inflation, ending the day below the 1.0550 mark. Today, focus turns to the September CPI release for Sweden, where we expect a downside surprise to both the headline and core measures, which in turn would support our base case of an unchanged Riskbank decision in November. Additionally, the Riksbank publishes the tentative results of the FX reserves hedging program, which commenced on 25 September. EUR/GBP moved higher on the soft GDP data out for August, highlighting our call that the Bank of England delivered its last hike in August.

Credit: Somewhat Hawkish US inflation data did not spook credit markets, which ended tighter for the day. Itrax main tightened 1.3bp to close at 81.9bp, while Itrax main tightened 5.9bp to close at 435.5bp. Primary market activity was also decent, with among others the Norwegian Rail Construction Company, NRC, printing a 4yr FRN at DM+440bp.

Nordic macro

Inflation statistics are released in Sweden today (08:00). We expect a CPIF decline to 3.5% and YoY and core inflation to decrease by 0.6 p.p. to 6.6% YoY. If we are correct, CPIF will be 0.3 p.p. below the Riksbank's forecast, while it will be spot on for core inflation. There is uncertainty regarding two areas: food prices and recreation/transportation services. Food prices are expected to see a marginal decline, while the other area, such as holiday travel prices, is expected to drop further after a surge during the summer. Falling electricity prices will push the energy component lower as it outweighs the rise in petrol prices. Both the Danish and Norwegian inflation came in lower than expected earlier this week and were mainly dragged down by the uncertain Swedish components which supports our forecast.

US Yields and Dollar Jump on Hotter-than-Expected CPI

US inflation data wasn’t very soothing for investors at yesterday’s release. The headline inflation remained steady at 3.7%, while initial jobless claims came in soft, after last Friday’s shocker NFP showed 336K new nonfarm job additions. The data softened the Federal Reserve (Fed) doves’ hand. The US 2-year yield jumped past the 5% level, while the 10-year yield returned above the 4.70% mark and the 30-year jumped 18 bp to above 4.80% after a $20 billion auction saw weak demand.

Of course, the stickiness in yesterday’s inflation data wasn’t a surprise. The rising food and energy prices were partly responsible for the latest surge, while shelter was again one big headache. The 3-month inflation sailed away from 2.4% to 3.1%. Core inflation remained steady, however, but supercore inflation – which excludes housing and good prices - spiked higher. As such, even though we think that the housing costs will come down and the positive pressure in energy started easing, the latest numbers were not convincing. Yet, the latest set of jobs and inflation data will unlikely change the Fed’s mind for the November meeting. The Fed is expected to sit on its hands, wait and see. But the first Fed rate cut won’t come so soon, and the Fed will try to capitalize on the ‘higher for longer’ policy to avoid having an accident on what they call ‘the last mile’. The Fed is expected to cut rates in July next year. The expectation was for June before yesterday’s CPI data. Activity on Fed funds futures still gives more than 90% chance for a no action in November, and around 70% chance for a no action in December.

The market reaction to yesterday’s data was very clear. The rebound in yields sent the US dollar rallying, and equities tumbling. The S&P500 retreated yesterday on the back of discouraging inflation data, and on news that nearly 9K more people at Ford joined the UAW strike, while GM, Ford and Stellantis laid off near 5K workers in response to the past weeks’ chaos – and it will certainly show in next set of jobs data. But now, stock traders’ attention will shift to earnings from today, as the US big banks will kick off the earnings season in a few hours.

The Dollar surfs on inflation wave

The US dollar index rallied back into its July to now ascending channel, the EURUSD sank below 1.06, after testing the July to October downtrending channel top. The minutes from the latest European Central Bank (ECB) meeting confirmed that the latest ECB rate hike was a close call. The latter further boosted the ECB doves, while the latest US inflation data held back the Fed doves from making further progress. If the Fed doves don’t take back control rapidly, we will likely see the EURUSD melt down toward 1.0410, to meet the 50% Fibonacci retracement on last year’s rally there. The dollar-yen remains cautiously bid near the 150 level, while Cable – which could’ve rallied above both a short-term and a long-term bearish trend channel, simply couldn’t take the chance after yesterday’s data showed a meagre GDP growth of 0.2% in August due to a weaker-than-expected recovery in industrial and manufacturing production. The good news is that inflation sinks fast in the UK as spending slows. The truflation for the UK has taken a dive below the 8% level. It’s still far from the Bank of England’s (BoE) 2% target, but at this speed, Rishi Sunak will get his inflation halved by the year end.

In energy, the selloff in crude oil extended to below $82pb as the EIA revealed a more than 10-mio barrel build in US crude inventories last week, but buyers gently return into the $80pb psychological level, which is – we know – the Saudi’s limit for eventually taking more action to restrict demand.

The Middle East continues to boil, and the tensions are expected to escalate further and threaten supply. The good news is, the EIA expects the growth in oil demand to slump by more than 50% next year, and the slowing demand growth should boost inventories to the positive territory, again, even though the world fuel consumption is still expected to hit a fresh record this year, driven by China.

But China should wake up first. The latest inflation numbers from China don’t sound like the Chinese will move the oil market anytime soon. The Chinese consumer prices remained flat in September, producer prices fell more than expected and imports came in weaker than expected. The only thing that’s exciting about China is the expectation that the government will throw more money on to the Chinese problems, and that could, maybe, inflate asset prices.

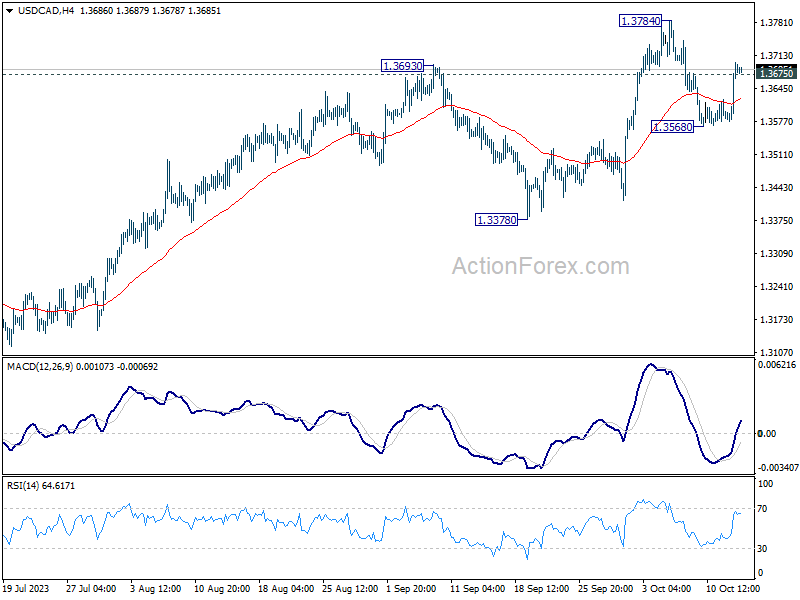

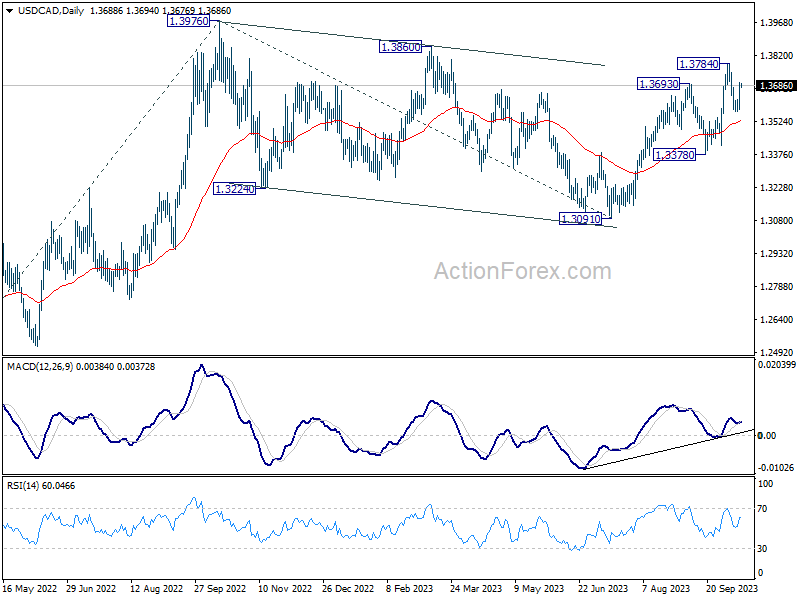

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3613; (P) 1.3657; (R1) 1.3735; More....

USD/CAD's break of 1.3675 minor resistance suggests that pull back from 1.3784 has completed at 1.3568 already. Intraday bias is back on the upside for retesting 1.3784 first. Firm break there will resume larger rise from 1.3091 to retest 1.3976 high. On the downside, below 1.3568 will bring another falling leg to extend the near term corrective pattern.

In the bigger picture, current development revives the case that corrective pattern from 1.3976 (2022 high) has completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target will be 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will now remain the favored case as long as 1.3378 support holds.

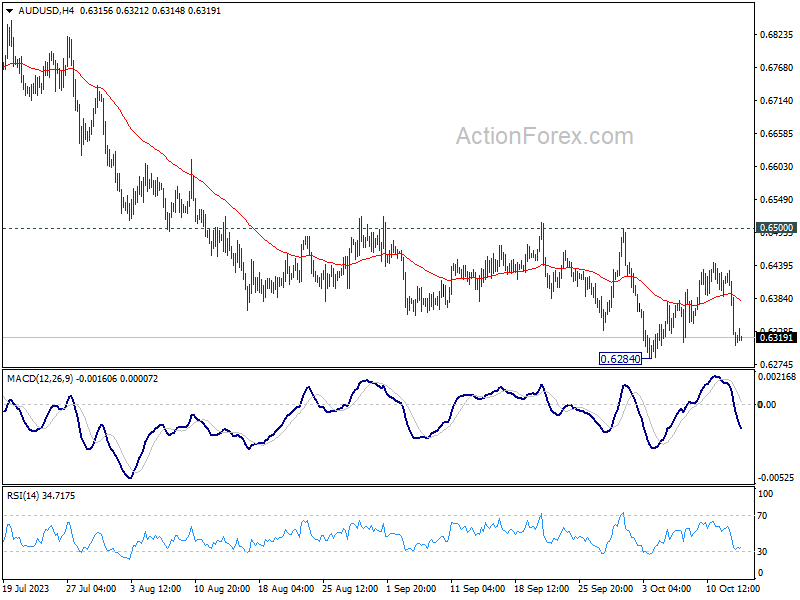

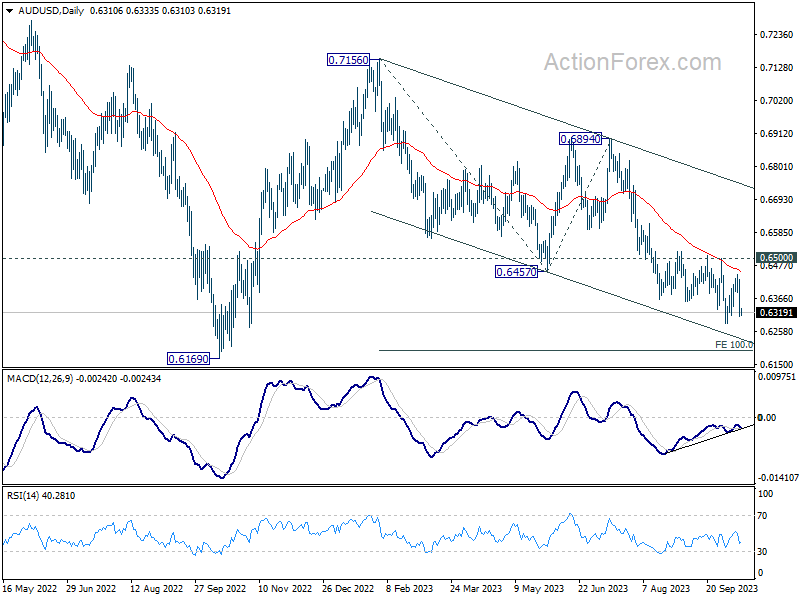

AUD/USD Daily Report

Daily Pivots: (S1) 0.6270; (P) 0.6351; (R1) 0.6394; More...

AUD/USD is still bounded in range above 0.6824 despite current decline. Intraday bias remains neutral first. Near term outlook remains bearish with 0.6500 resistance intact. Break of 0.6284 will resume the fall from 0.7156. Next target is 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195.

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

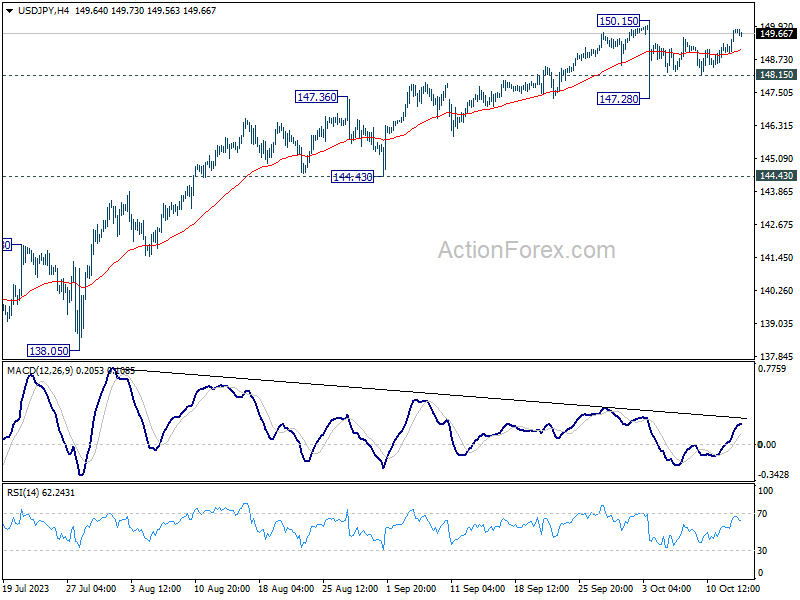

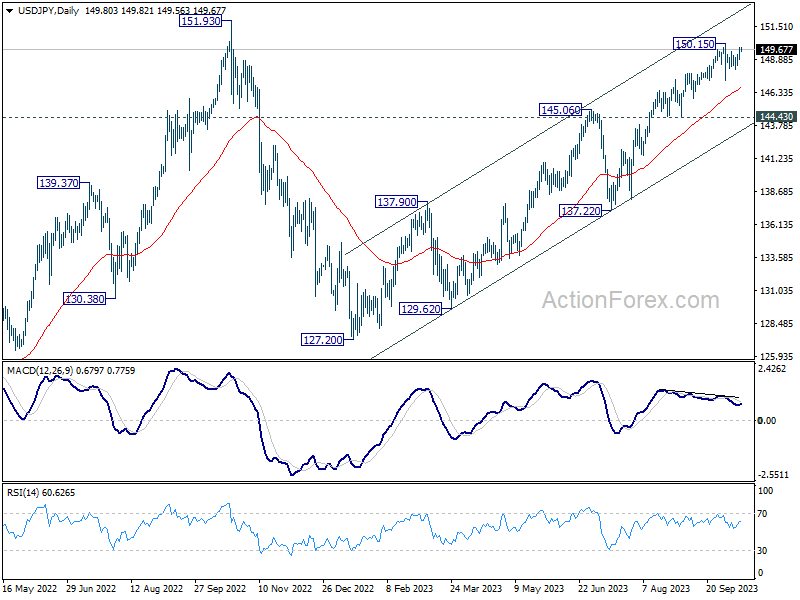

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.24; (P) 149.53; (R1) 150.11; More...

USD/JPY is still bounded in range below 150.15 despite current recovery, and intraday bias remains neutral. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high. On the downside, below 148.24 minor support will turn bias to the downside for another down leg through 147.28.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

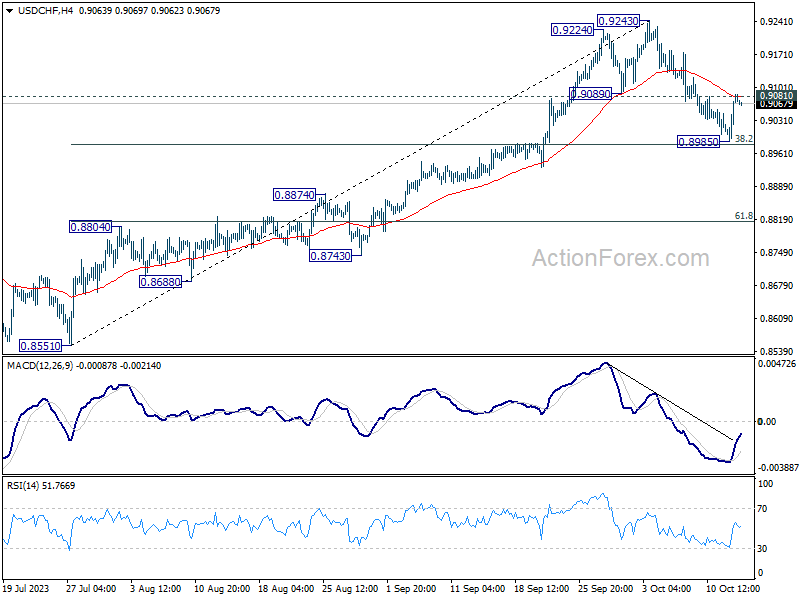

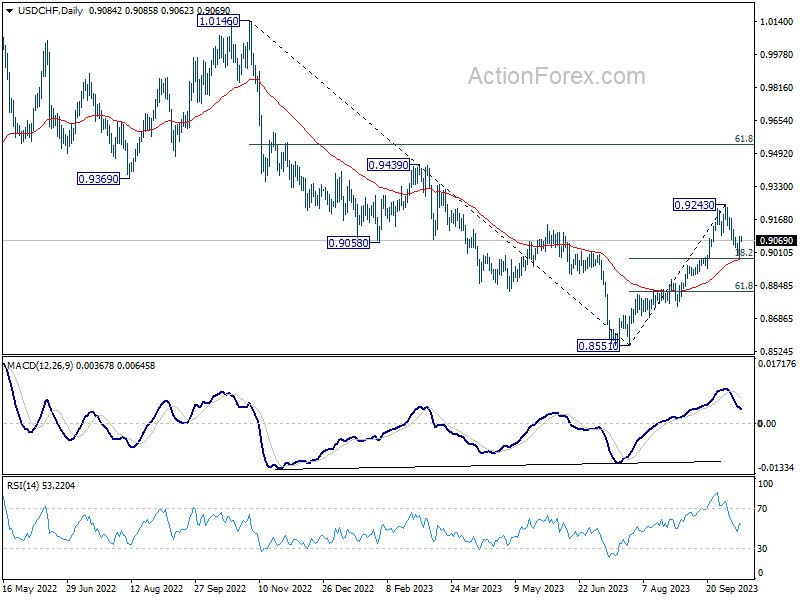

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9019; (P) 0.9053; (R1) 0.9120; More....

Immediate focus is now on 0.9081 resistance with current recovery. Break will suggest that USD/CHF's pull back from 0.9243 has completed at 0.8985, after drawing support from 38.2% retracement of 0.8551 to 0.9243 at 0.8979. Intraday bias will then be back on the upside for retesting 0.9243 high. Nevertheless, sustained break of 0.8979 will argue that deeper fall is under way to 61.8% retracement at 0.8815.

In the bigger picture, current development indicates that rise from 0.8551 is reversing whole down trend from 1.0146. Further rally would then be seen to 61.8% retracement at 0.9537 and above. For now, this will be the favored case as long as 55 D EMA (now at 0.8971) holds, even in case of deep pullback.

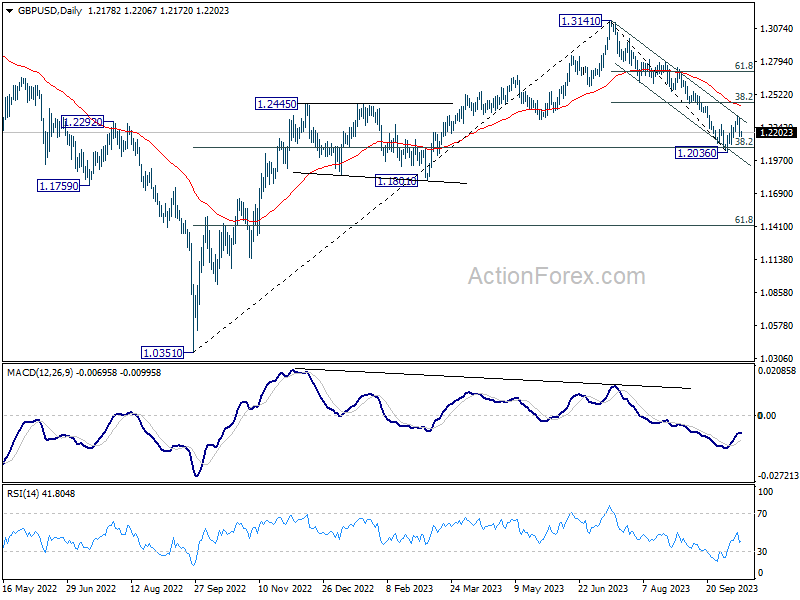

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2121; (P) 1.2226; (R1) 1.2281; More

GBP/USD's break of 1.2210 minor support suggests that recovery from 1.2036 has completed at 1.2336, after hitting falling channel resistance. Intraday bias is back on the downside for retesting 1.2036 low. Decisive break there will resume larger fall from 1.3141. On the upside, above 1.2336 minor resistance will resume the rebound instead.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2420) holds, in case of rebound.

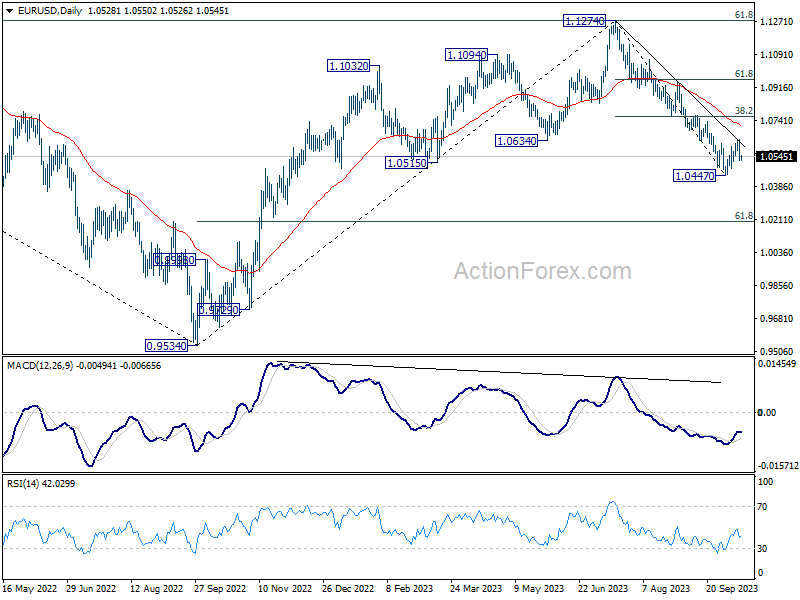

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0489; (P) 1.0565; (R1) 1.0603; More...

Immediate focus is back on 1.0518 minor support in EUR/USD with current fall. Firm break there will confirm that corrective recovery from 1.0447 has completed at 1.0639, after hitting near term falling trend line. Larger decline from 1.1274 should then be resumed through 1.0447 to 1.0119 fibonacci level. On the upside, though, above 1.0639 will resume the recovery to 1.0764 resistance.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0709) holds, in case of rebound.

Dollar and Yield Revival Amid Renewed Fed Rate Hike Fears

Dollar staged a notable comeback overnight, accompanied by a sharp ascent in treasury yields and a downtick in stocks. This resurgence was catalyzed by the release of US CPI data that stoked concerns of another Fed rate hike this year. However, this speculation has yet to be significantly mirrored in futures pricing, which currently pegs the likelihood of a December hike at a mere 33%. Despite this, the prevailing risk-off sentiment, marked by red-tinged major indexes, extends into Asian session.

Investors are now pivoting their attention towards the impending release of the University of Michigan consumer sentiment and inflation expectations data. A surprise revelation in these metrics could potentially catapult Dollar to close the week as the dominant currency.

In the broader currency arena, New Zealand Dollar is languishing as the week's underperformer, its decline exacerbated by unimpressive manufacturing data unveiled in today's Asian session. Australian Dollar trails closely behind, with Euro also succumbing to downward pressures. Conversely, Swiss Franc stands as the week's prime performer, although the revitalized Dollar threatens to usurp this lead. Canadian Dollar is exhibiting moderate strength, the Sterling and Yen are locked in a mixed performance standoff.

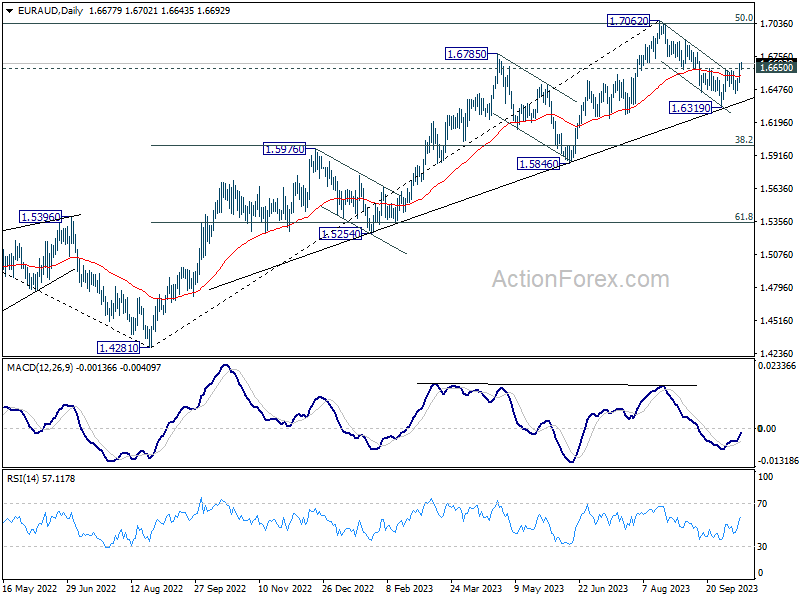

On the technical front, EUR/AUD's break of 1.6650 resistance now argues that correction from 1.7062 has completed at 1.6319 already, after drawing support from medium term trend line. Further rally is now in favor back to retest 1.7062 high. At the same time, EUR/USD's recovery from 1.0447 short term bottom could have completed at 1.0639. Break of 1.0518 minor support will resume EUR/USD fall from 1.1274 through 1.0447 support. If both scenarios play out as mentioned, AUD/USD should experience downside acceleration and power through 0.6284 to resume the larger down trend.

In Asia, at the time of writing, Nikkei is down -0.66%. Hong Kong HSI is down -2.05%. China Shanghai SSE is down -0.66%. Singapore Strait Times is down -0.86%. Japan 10-year JGB yield is up 0.0086 at 0.764. Overnight, DOW dropped -0.51%. S&P 500 dropped -0.62%. NASDAQ dropped -0.63%. 10-year yield rose 0.117 to 4.701.

Fed's Collins believes rates may have peaked in current cycle

Boston Fed President Susan Collins highlighted that recent rise in long-term yields implies some tightening of financial conditions. "If it persists, it likely reduces the need for further monetary-policy tightening in the near term," she noted in a speech yesterday.

Such market dynamics further bolstered Collins' perspective on the current tightening cycle led. "This reinforces my view that we are very near, and perhaps at, the peak federal funds rates for this tightening cycle," she stated, indicating that the cycle could be nearing its zenith.

However, Collins maintained a flexible stance on the future course of action, and clarified, "I would not take further tightening off the table yet."

Weighed in on yesterday's CPI data, which revealed that September's headline inflation held steady at 3.7% and core inflation eased to 4.1%. Collins said, "Today's CPI release is a reminder that restoring price stability will take time."

New Zealand BNZ PMI falls to 45.3, entrenched manufacturing downturn deepens

New Zealand manufacturing sector has further sunk into troubled waters, as evidenced by the continued and deepening contraction observed in recent data.

BusinessNZ Performance of Manufacturing Index for September highlighted this slowdown by dropping to 45.3, down from 46.1 the previous month. This marks its most dismal performance for a month unaffected by COVID-19 since May 2009 and sits notably below the long-term average activity rate of 52.9.

Delving into the specifics, there's a discernible decline across most metrics. While production saw a slight uptick, moving from 43.8 to 44.6, other areas weren't as fortunate. Employment indicators slid from 47.7 to 45.2, and new orders also receded from 46.6 to 44.9. Meanwhile, finished stocks dwindled, albeit marginally, from 52.0 to 51.6, and deliveries plunged from 47.8 to 44.3.

Catherine Beard, BusinessNZ's Director of Advocacy, highlighted the sustained downturn, pointing out that the sector "has now been in contraction for seven consecutive months, with little sign it is showing any improvement."

On the economic front, BNZ Senior Economist Doug Steel provided a bleak perspective, remarking, "the trend remains firmly downward." He also touched upon the challenges in discerning the exact causes of any PMI result but cited "falling sales, rising costs, and election uncertainty" as significant factors currently impacting the sector..

China's export slump persists but softens; imports shrink further as CPI stalls

China's trade figures for September revealed a continued, albeit moderating, decline in exports, marking the fifth consecutive month of contraction. Exports dropped by -6.2% yoy to USD 229.1B, an improvement from the -8.8% yoy decline recorded in the previous month. Despite this easing contraction, prolonged declines in shipments to major trade partners underscore the persisting challenges in the external sector.

A breakdown of the data shows exports to ASEAN countries contracted by -15.8% yoy, hitting USD 55B. The US, amidst a 14-month streak of declines, saw a -9.3% yoy contraction in goods from China, totaling USD 46B. European Union imports from China also fell by -11.6% yoy. In contrast, Russia exhibited a robust appetite for Chinese goods, with exports soaring by 20.6% yoy.

On the import front, China's inbound shipments contracted by -6.2% yoy to USD 221.4B, marking the seventh consecutive monthly decline but showing a slower pace compared to August's -7.3% yoy contraction. Consequently, trade surplus widened to USD 77.7B, outperforming market expectations.

Inflation dynamics within the country presented another layer of economic intricacies. China's CPI stagnated at 0.0% yoy in September, pulled down by a -3.2% yoy decline in food prices, and falling short of the anticipated 0.2% yoy increase. The National Bureau of Statistics cited a high base of comparison with last year and abundant food supply ahead of the Golden Week holiday as key factors behind the subdued inflation.

Simultaneously, PPI showed a -2.5% yoy decline, extending the 12-month streak of contraction yet revealing an easing trend from August's -3.0% yoy drop.

Looking ahead

Swiss PPI and Eurozone industrial production will be released in European session. Later in the day, US will release import price index and U of Michigan consumer sentiment.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0489; (P) 1.0565; (R1) 1.0603; More...

Immediate focus is back on 1.0518 minor support in EUR/USD with current fall. Firm break there will confirm that corrective recovery from 1.0447 has completed at 1.0639, after hitting near term falling trend line. Larger decline from 1.1274 should then be resumed through 1.0447 to 1.0119 fibonacci level. On the upside, though, above 1.0639 will resume the recovery to 1.0764 resistance.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0709) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Sep | 45.3 | 46.1 | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Sep | 2.40% | 2.40% | 2.50% | |

| 01:30 | CNY | CPI Y/Y Sep | 0.00% | 0.20% | 0.10% | |

| 01:30 | CNY | PPI Y/Y Sep | -2.50% | -2.40% | -3.00% | |

| 03:00 | CNY | Trade Balance (USD) Sep | 77.7B | 73.7B | 68.4B | |

| 06:30 | CHF | Producer and Import Prices M/M Sep | 0.20% | -0.20% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Sep | -0.80% | |||

| 09:00 | EUR | Eurozone Industrial Production M/M Aug | 0.10% | -1.10% | ||

| 12:30 | USD | Import Price Index M/M Sep | 0.60% | 0.50% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Oct P | 68 | 68.1 |

China’s export slump persists but softens; imports shrink further as CPI stalls

China's trade figures for September revealed a continued, albeit moderating, decline in exports, marking the fifth consecutive month of contraction. Exports dropped by -6.2% yoy to USD 229.1B, an improvement from the -8.8% yoy decline recorded in the previous month. Despite this easing contraction, prolonged declines in shipments to major trade partners underscore the persisting challenges in the external sector.

A breakdown of the data shows exports to ASEAN countries contracted by -15.8% yoy, hitting USD 55B. The US, amidst a 14-month streak of declines, saw a -9.3% yoy contraction in goods from China, totaling USD 46B. European Union imports from China also fell by -11.6% yoy. In contrast, Russia exhibited a robust appetite for Chinese goods, with exports soaring by 20.6% yoy.

On the import front, China's inbound shipments contracted by -6.2% yoy to USD 221.4B, marking the seventh consecutive monthly decline but showing a slower pace compared to August's -7.3% yoy contraction. Consequently, trade surplus widened to USD 77.7B, outperforming market expectations.

Inflation dynamics within the country presented another layer of economic intricacies. China's CPI stagnated at 0.0% yoy in September, pulled down by a -3.2% yoy decline in food prices, and falling short of the anticipated 0.2% yoy increase. The National Bureau of Statistics cited a high base of comparison with last year and abundant food supply ahead of the Golden Week holiday as key factors behind the subdued inflation.

Simultaneously, PPI showed a -2.5% yoy decline, extending the 12-month streak of contraction yet revealing an easing trend from August's -3.0% yoy drop.