Sample Category Title

BoE’s Bailey: Monetary decisions to go on to be tight

During his recent speech at IMF's annual meeting in Marrakech, BoE Governor Andrew Bailey reflected on previous month's decision to maintain interest rates at 5.25%. He characterized the decision as "a tight one", added that "they're going to go on being tight ones".

The MPC's narrow 5-4 vote to pause its series of consecutive rate hikes in September underscores the divided opinions within the bank regarding the best path forward.

Highlighting the bank's recent efforts, Bailey commented, "We have made, I think, particularly in the last few months, solid progress in terms of showing signs that inflation is being tackled."

However, he cautioned against overconfidence, adding, "let's not get carried away because there's an awful lot still to do."

The "last mile" of inflation management, according to Bailey, will considerably depend on "restrictive policy."

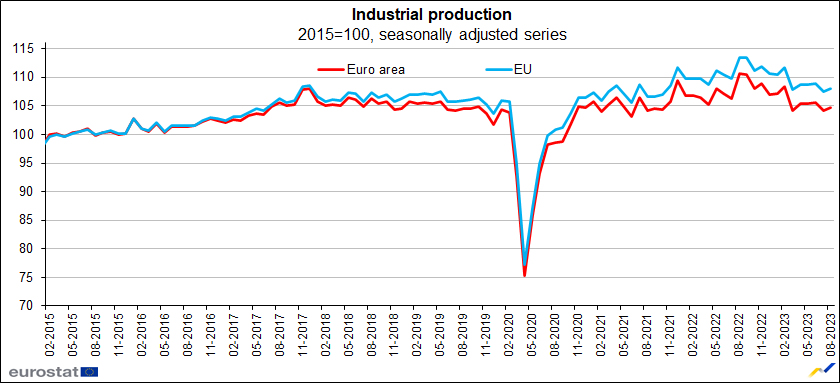

Industrial production in Eurozone and EU up 0.6% mom in Aug

Eurozone industrial production rose 0.6% mom in August, well above expectation of 0.1% mom. Production of durable consumer goods grew by 1.2% mom, non-durable consumer goods by 0.5% mom and capital goods by 0.3% mom, while production of intermediate goods fell by -0.3% mom and energy by 0.9% mom.

EU industrial production rose 0.6% mom. Among Member States for which data are available, the highest monthly increases were registered in Ireland (+6.1%), Slovakia (+4.5%) and Lithuania (+3.7%). The largest decreases were observed in Hungary (-2.4%), Croatia (-2.2%) and Belgium (-1.8%).

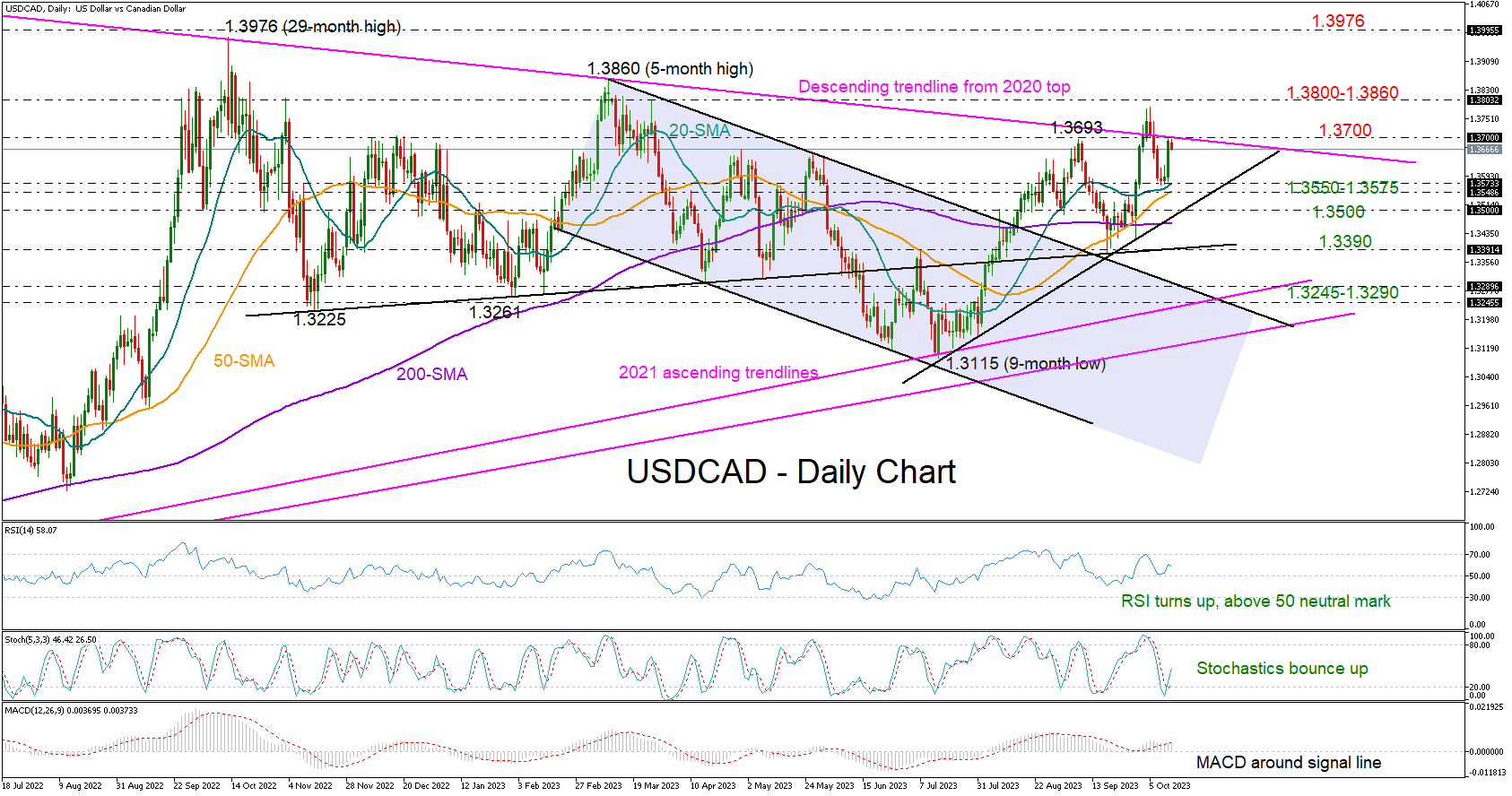

USDCAD Bulls Roar Back; Eyes on 1.3700

- USDCAD treats its wounds with solid bounce

- Caution needed as familiar resistance nearby

USDCAD gathered significant momentum on Thursday, flipping weekly losses into a 0.20% gain after a slightly stronger US CPI report.

The pair kept its footing above its simple moving averages (SMAs), but the descending trendline from the 2020 top resumed its resistance role, halting the bullish action marginally below 1.3700. Despite some positive signs coming from the RSI and the stochastic oscillator, the bulls need to break through that threshold to move towards the 2023 wall of 1.3800-1.3860. The 2022 peak of 1.3276 could be the next destination.

On the downside, the 20- and 50-day SMAs could hold the market above the short-term support trendline drawn from July near 1.3500. Note that the 200-day SMA is flattening in the same region. Hence, a step lower could trigger another negative correction towards the support line from November at 1.3390. Failure to bounce there could squeeze the price into the 1.3245-1.3290 zone, where the upper band of the broker bearish channel intersects the 2021 ascending trendline.

In brief, the recent solid rise in USDCAD looks appealing, but it may not last if it can't run sustainably above 1.3700.

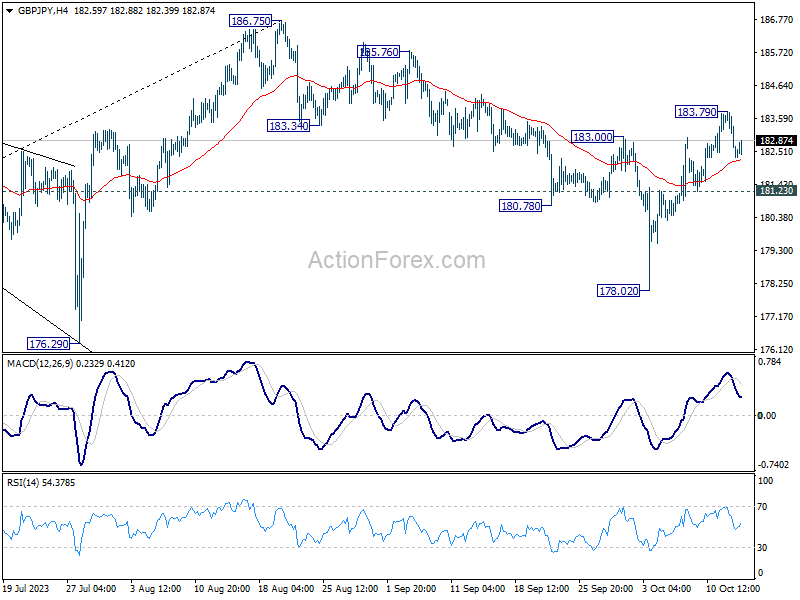

GBPJPY Gets Rejected Near July Highs

- GBPJPY rebounds from its lowest level since July

- Gets capped by the 50-day SMA and Ichimoku cloud

- Momentum indicators suggest a cautiously bullish tone

GBPJPY had been stuck in a prolonged uptrend since January, posting an eight-year high of 186.75 on August 22 before experiencing a pullback. Even though the pair attempted to rebound from its October lows and recoup some losses, its advance got rejected near the July peak of 184.00.

Should the price march higher and reclaim its 50-day simple moving average (SMA), immediate resistance could be met at the July high of 184.00. Piercing through that wall, the pair could revisit its eight-year high of 186.75. If that hurdle also fails, the price could post fresh multi-year highs, where the 190.00 psychological mark might curb further advances.

On the flipside, if the selling interest persists, the bears could attack the 180.72 support zone. Even lower, the July barrier of 179.45, which also acted as support in October, could provide additional downside protection. Breaking below that level, the price might face the October bottom of 178.05.

In brief, GBPJPY has been staging a solid rebound in the short-term, but it seems to be losing steam. Hence, a failure to reclaim the 50-day SMA could trigger a move to the downside.

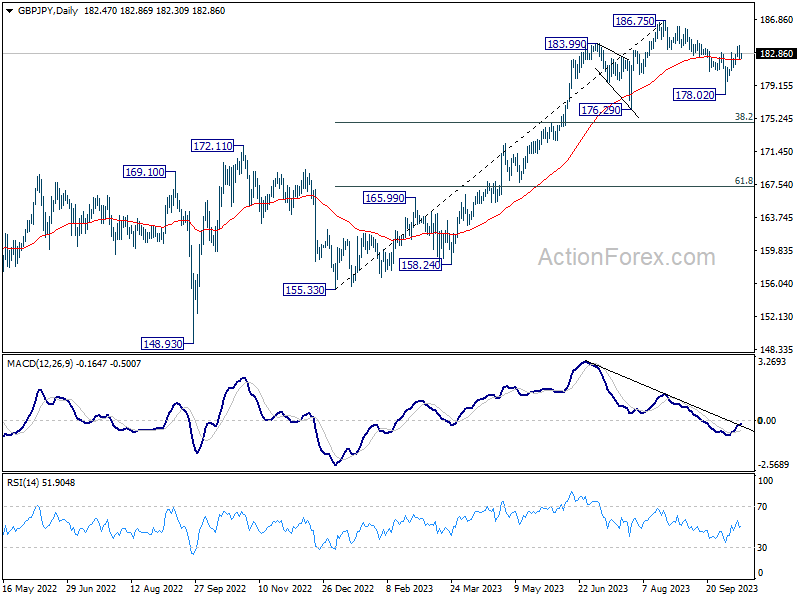

GBP/JPY Daily Outlook

Daily Pivots: (S1) 181.89; (P) 182.85; (R1) 183.37; More...

Intraday bias in GBP/JPY is turned neutral first with current retreat. Outlook is unchanged that pull back from 186.75 should have completed 178.02 already. Above 183.79 will resume the rebound from 178.02 to retest 186.75 high. On the downside, however, break of 181.23 will dampen this view, and turn bias back to the downside for 178.02 instead.

In the bigger picture, fall from 186.75 is currently seen as a corrective move only. As long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and bring lengthier and deeper consolidations.

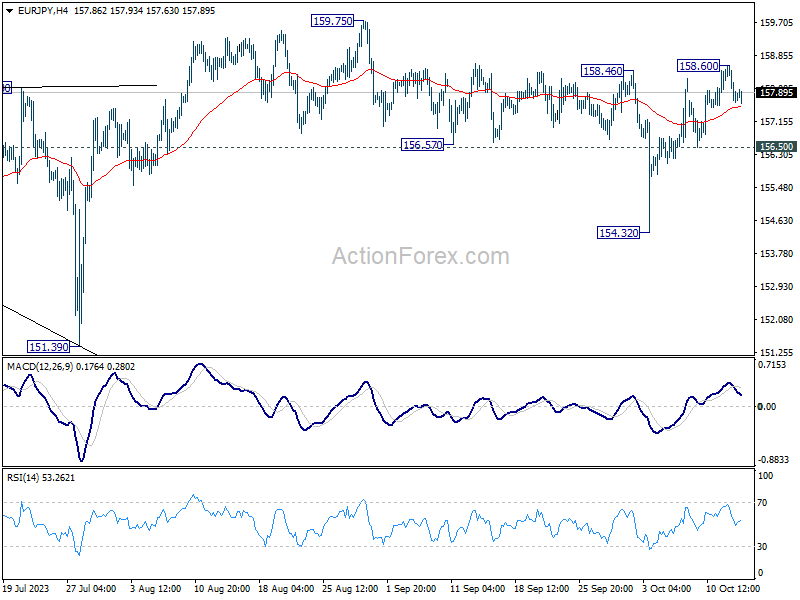

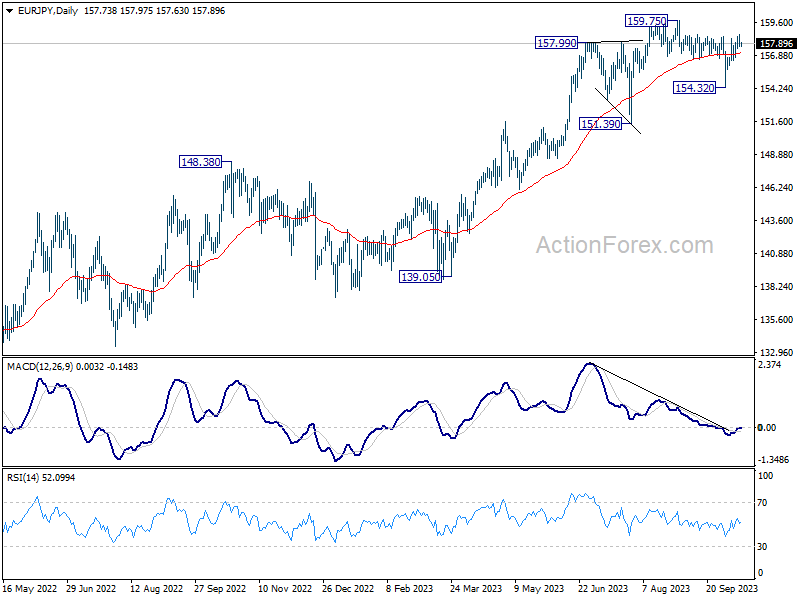

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.38; (P) 158.00; (R1) 158.34; More....

EUR/JPY retreated after hitting 158.60 and intraday bias is turned neutral first. Outlook is unchanged that pull back from 159.75 has probably completed with three waves down to 154.32. Above 158.60 should resume the rise form 154.32 to retest 159.75 high. However, break of 156.50 will dampen this view, and bring another fall to extend the corrective pattern from 159.75.

In the bigger picture, price actions from 159.75 are views as a corrective pattern for now. As long as 151.39 support holds, rise from 114.42 (2020 low) is still expected to continue through 159.75 at a later stage. Nevertheless, firm break of 151.39 will confirm medium term topping, and bring lengthier and deeper correction.

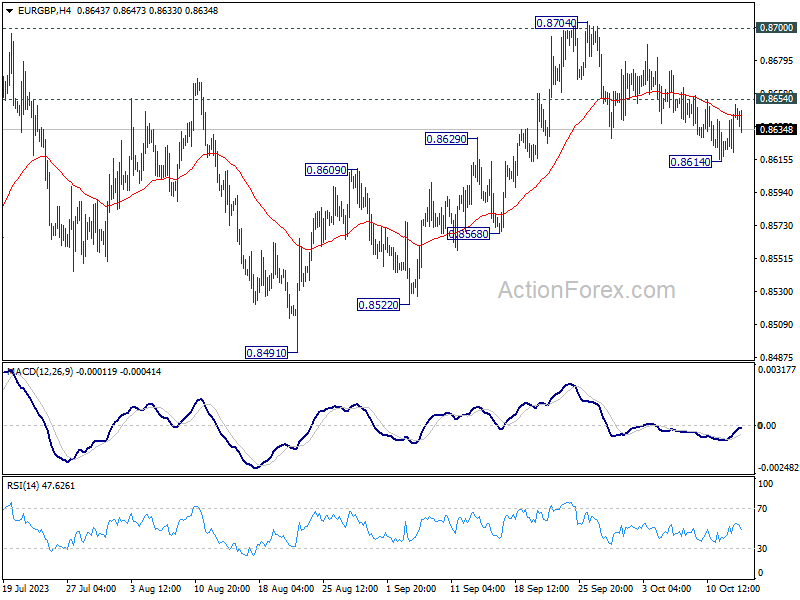

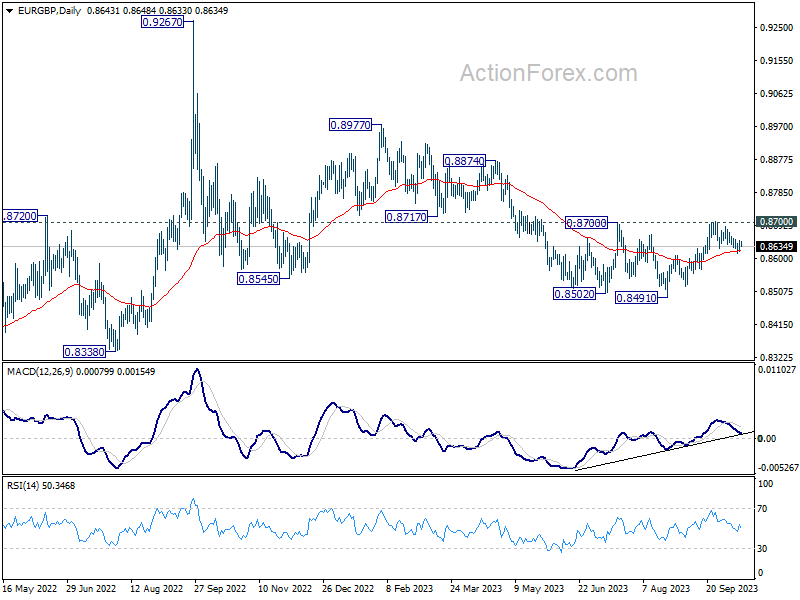

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8629; (P) 0.8641; (R1) 0.8659; More....

Intraday bias in EUR/GBP is turned neutral first but further decline is in favor with 0.8654 resistance intact. Below 0.8614 will resume the choppy fall form 0.8704 to 0.8568 support next. However, above 0.8654 minor resistance will turn intraday bias back to the upside for retesting 0.8700/4 resistance zone instead.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Decisive break of 0.8700 resistance will argue that this decline has completed with three waves down to 0.8491. Rise from 0.8491 could then be another leg inside the pattern and targets 0.8977 and above. However, rejection by 0.8700 will keep the down trend alive for another fall through 0.8491 at a later stage.

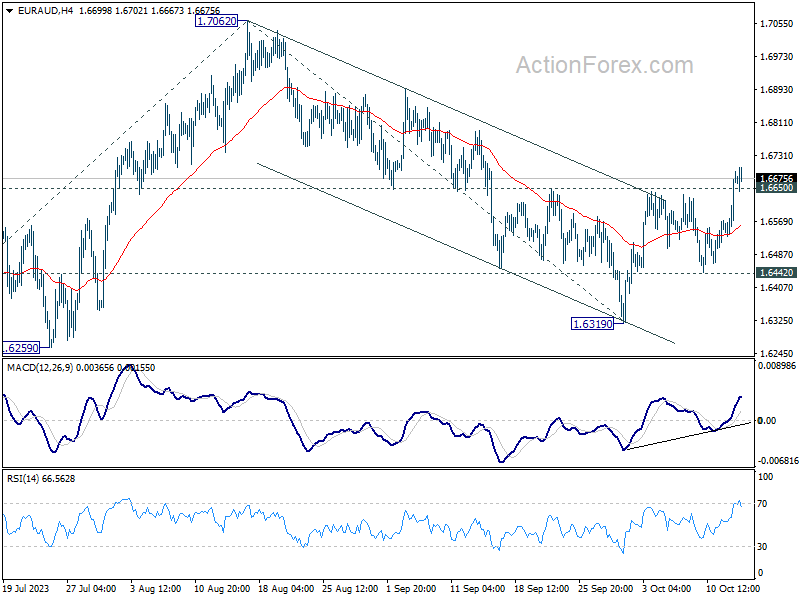

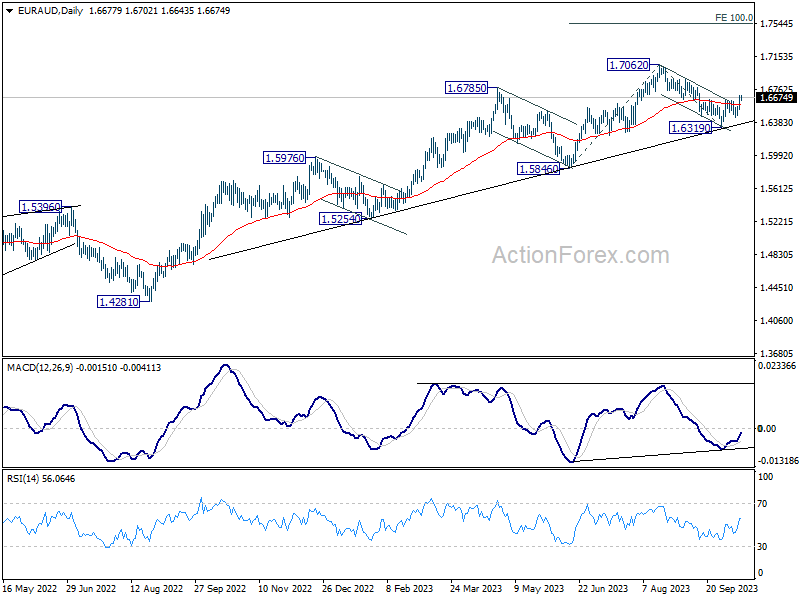

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6574; (P) 1.6634; (R1) 1.6734; More...

EUR/AUD's rebound from 1.6319 resumed and the break of 1.6650 resistance argues that correction from 1.7062 has completed. That came after drawing support from medium term trend line support. Intraday bias is back on the upside for retesting 1.7062 high. For now, risk will stay on the upside as long as 1.6442 support holds, in case of retreat.

In the bigger picture, the strong support from medium term rising trend line indicates that rise from 1.4281 (2022 low) is still in progress. On resumption, next target is 100% projection of 1.5846 to 1.7062 from 1.6319 at 1.7353. In any case, outlook will stay bullish as long as 1.6319 support holds.

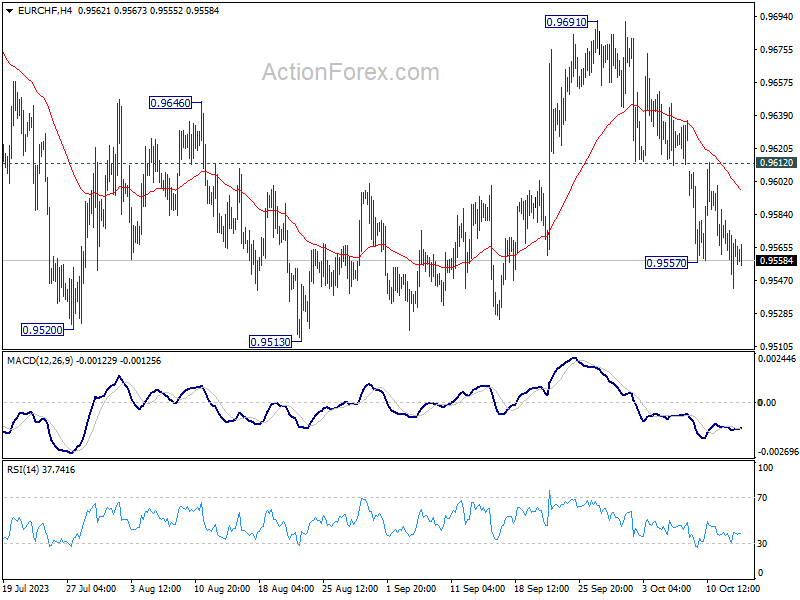

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9546; (P) 0.9563; (R1) 0.9581; More...

Intraday bias in EUR/CHF is back on the downside, as fall from 0.9691 resumed by breaking through 0.9557. Deeper fall would be seen to retest 0.9513 low first. Decisive break there will resume larger down trend from 1.0095. On the upside, above 0.9612 will turn bias back to the upside for 0.9691 instead.

In the bigger picture, medium term outlook will stay bearish as long as the cross is capped well below falling 55 W EMA (now at 0.9793). That is, down trend from 1.2004 (2018 high) could still resume through 0.9407 (2022 low). However, sustained trading above the 55 W EMA will raise the chance that 0.9470 is already a long term bottom. Further rise would then be seen to 1.0095 resistance to indicate bullish trend reversal.

Dollar Again in Pole Position

Markets

Yesterday, the focus was on the US CPI. After recent repositioning, the market reaction was telling. First the data. They were close to expectations, with headline CPI at 0.4% M/M and 3.7% Y/Y (0.3% M/M). Core inflation eased to 0.3% M/M and 4.1% y/y (down from 4.3%). Post-payrolls, the market mostly reacted with a soft bias, after Fed comments (Logan, Vice Chair Jefferson) that recent rise in LT (real) yields caused a similar tightening equal to a (final) 25 bps Fed hike. However, post-CPI markets clearly aren’t convinced that this trick will work. The September inflation, while as expected, remains from the 2.0% inflation target. Looking through the baseline effects in the Y/Y measure, a 0.3-0.4% monthly dynamics only suggests that the battle hasn’t been won yet. Markets put the Longan-Jefferson assessment aside with yields starting quite an impressive ascent, the long end taking the lead. The bond sell-off even accelerated on a poor $ 20 bln 30-y Treasury auction. A the end of the day; USD yields added between 8.7 bps (2-y) and 16 bps (30-y). The US 10-y real yield also rebounded 10. 8 bps. In retrospect, the Fed communication on higher longer rates being a potential substitute for Fed rate hikes apparently isn’t that evident for markets to cope with. Maybe, the market concludes that it has more work to do (for the Fed). German yields followed at a distance rising between 7.6 bps (30-y) and 5.3 bps (2-y). The rebound in (real) US yields blocked the post-payrolls equity rebound. US indices after opening in green closed with losses of about 0.5%/0.6%. The dollar rebounded. DXY jumped from the 105.7 area to close at 106.6. USD/JPY nears the 150 barrier again (close 149.81). EUR/USD initially tested the 1.0635/43 resistance area, but was pushed back to close near 1.053.

This morning, Asian equities suffer from the higher US (real) yields annex WS correction yesterday. Chinese data and headlines on other measures from Chinese authorities to support markets don’t convince investors (Cf infra). US Treasures regain modest ground after yesterday’s sell-off. The dollar also cedes a few ticks (EUR/USD 1.0545). Later today, consumer confidence from the U. of Michigan (including inflation expectations data) is the only data series with market moving potential. Yesterday’s price action suggests that the bottom in core yields might be well protected going into the Fed November 01 policy meeting. For the US 10-y, a consolidation pattern between 4.50% and 4.9% might be developing. Giving lingering geopolitical tensions and the equity rally running into resistance, the dollar is again in pole position. The EUR/USD 1.0448 correction low might come on the radar again. Als keep an eye at the start of the US earnings season with several major banks reporting today.

News and views

Chinese inflation rose by 0.2% M/M in September, with the Y/Y-outcome flat compared to market expectations of a 0.2% Y/Y increase. Details showed consumer goods falling by 0.9% Y/Y while services inflation remained positive at 1.3% Y/Y. Food prices were the main drag, falling by 3.2% Y/Y. On a product level, household items (-0.4% Y/Y) and transport & communication (-1.3% Y/Y) showed falling price levels. The Chinese producer price index rose by 0.4% M/M, the most since April 2022. The Y/Y-reading turned less negative (-2.5% Y/Y from -3%) because of less-challenging base effects and higher oil prices. The Chinese trade surplus rose from $68.2bn in August to $77.71bn in September. The underlying picture isn’t a rosy one though with imports dropping 6.2% Y/Y (from -7.3% Y/Y) and pointing to weak domestic demand. Exports declined by 6.2% as well (from -8.8% Y/Y) which serves as proof for sluggish global growth. The Chinese yuan continue to trade on the weak side against the USD (USD/CNY 7.30). Chinese stock markets join the global trend, falling by 1-2% this morning, despite rumours that the country is considering a state-backed stabilization fund to shore up confidence in the stock market.

Argentina’s central bank raised its policy rate by 15 percentage points to 133%. National CPI data showed another acceleration for September (+12.7% M/M & +138.3% Y/Y). Off the record, they also attempt to prop up the Argentina peso which trades in the shadow market as weak as USD/ARS 1040 (“dollar blue rate) compared to official rate of USD/ARS 350. The currency is under even more pressure than usual in the run-up to October 22 elections with front-runner candidate Milei encouraging Argentines to stop savings in pesos as he wants to replace the national currency with US dollars (dollarization).