Sample Category Title

The Weekly Bottom Line: Goodbye “How High”, Hello “How Long”

U.S. Highlights

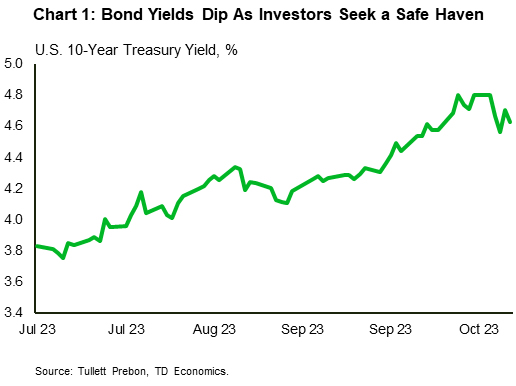

- U.S. bond yields retreated from highs reached last week, as heightened geopolitical risks in the Middle East boosted investors demand for safe haven assets.

- However, the recent overall surge in yields has prompted some Fed members to pay closer attention to tightening financial conditions as they determine the most appropriate policy path for interest rate.

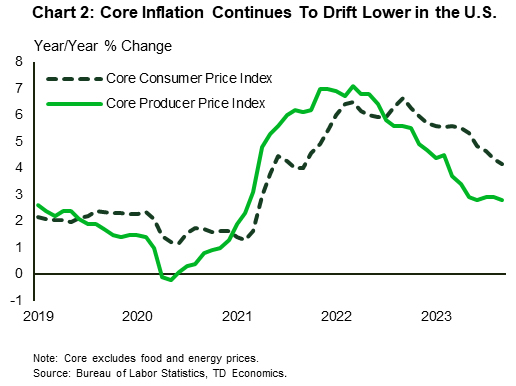

- Both producer prices and consumer prices suggest that the Fed still has some work to do to ensure inflation gets back to target, even as core prices continue to moderate.

Canadian Highlights

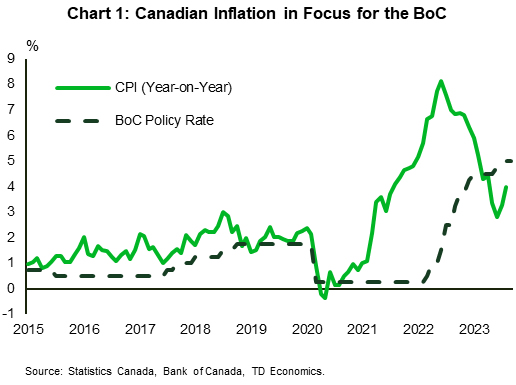

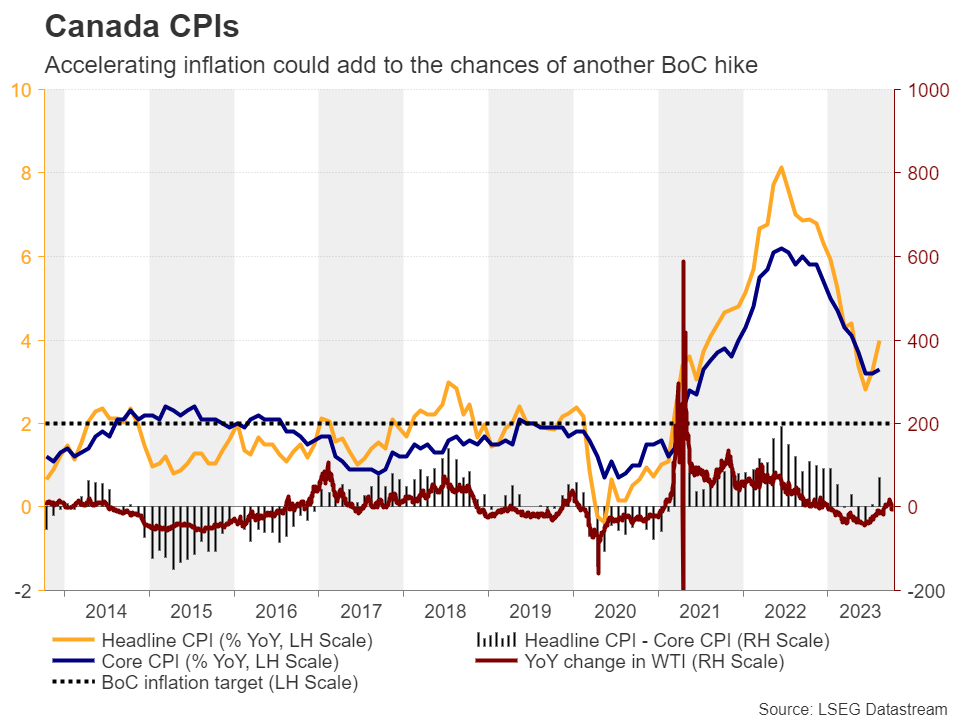

- The countdown to the Bank of Canada’s October 25th policy meeting is on, with recent data making the hike/no hike decision a close call.

- Investors are awaiting Canadian CPI data next week, which is unlikely to show much progress with the three-month rate of core inflation accelerating recently.

- The housing market continues to slide. With sales activity down and listing starting to jump, house prices continue to decline.

U.S. – Goodbye “How High”, Hello “How Long”

Last week’s tight financial conditions abated a bit this week, as conflict in the Middle East boosted demand for safe haven assets. As such, the 10-year Treasury yield took a reprieve from its upward trek and at the time of writing was down 17 basis points (bps) relative to the end of last week (Chart 1). Nonetheless, yields are still up 76 bps since July 26 when the Fed last raised the policy rate. Several factors have contributed to rising bond yields over the past few months including expectations of higher for longer interest rates and concerns about energy supply and prices.

The relatively higher yields have prompted some Fed officials to acknowledge that higher longer-term yields may be helping to achieve their policy objective. Dallas Fed President Lorie Logan remarked that “if long-term interest rates remain elevated because of higher term premiums, there may be less need to raise the fed-funds rate.” Similar sentiments were echoed by Fed governor Christopher Waller who said that “financial markets are tightening up and they are going to do some of the work for us”. Fed Vice Chair Philip Jefferson said that he would “remain cognizant of the tightening in financial conditions through higher bond yields” when assessing the path for interest rates. That sentiment was also echoed by Minneapolis Fed president Neel Kashkari.

The minutes released from the Fed’s September meeting revealed that, prior to the most recent run-up in bond yields, a “majority” of FOMC participants believed that another rate increase might be appropriate, while only “some” viewed no further increases as necessary. The tone of the minutes, economic projections and policy guidance was hawkish with Fed members expecting rates to be kept higher for even longer. This was reflected in a shallower path of expected rate cuts (FOMC commentary). Additionally, “several” participants commented that the Fed’s focus should be transitioning to how long to maintain restrictive policy, rather than how high to raise rates. Ultimately, all participants were in favor of maintaining restrictive policy for some time to ensure that inflation remains on a sustainable path downwards.

Both headline measures of producer prices (PPI) and consumer prices (CPI) show that the inflation battle is not quite over. On a yearly basis, PPI accelerated in September, while CPI held steady. The movements largely reflected gains in food and energy prices. Stripping out these volatile segments, core prices for both measures edged lower (Chart 2). While the downward tilt to core prices is sure to be welcomed by the Fed, rates are still too high for comfort given that near-term inflation expectations have inched higher in recent months and the labor market remains resilient.

American small businesses are also feeling less optimistic as expectations regarding the economic outlook and credit conditions deteriorated in September. Several firms noted that the Fed’s aggressive hiking campaign is weighing on credit with a net 26% of borrowers reporting paying higher interest rates versus three months ago. Nonetheless, the Fed will need to see a meaningful cooling in the jobs market and a sustained reduction in inflation, before shifting policy stance. As such, higher for longer may be around for some time.

Canada – Housing Slumps, With Inflation In Focus

The countdown to the Bank of Canada's (BoC's) October 25th policy meeting is on. While the Bank will be weighing the recent strength in the labour market alongside still stubbornly high inflation, the cracks forming in consumer spending and further weakness emanating from the housing market make the hike/no hike decision a tougher call. This had bond markets on a rollercoaster this week, as investors try to pin down what the BoC will do next.

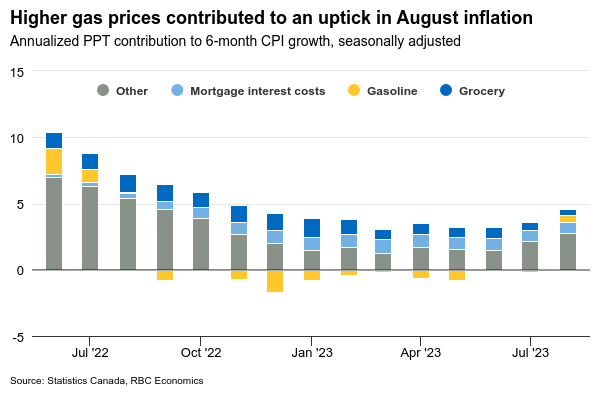

One report that could sway the BoC's hand is Canadian CPI released next week (Chart 1). The trend has not been a friend of the BoC lately. Consumer price inflation hit 4.0% year-on-year (y/y) in August, up from 3.3% y/y in July. While the headline number will get a lot of the media attention, the BoC will be looking at core inflation measures, which strip out more volatile price swings to get at underlying inflation trends. In August, the average of the Bank's trimmed mean and median inflation rates surprisingly increased to 4.0% y/y (from 3.8% y/y). The underlying trend here is also worrying. On a three-month annualized basis, the average of trimmed mean and median are clocking in at 4.5%. This signals that the annual core inflation rates might continue to show an upward bias in the coming months.

A mixture of services and goods inflation have been driving the momentum in core inflation recently. As our regular readers know, underlying services inflation (supercore) has been flying high on the back of persistently strong wage gains. Save for the discounting in airfares and travel relative services, supercore inflation has been running at an average pace of 5% for over a year now (Chart 2). With wages continuing to rise, services inflation is likely to remain elevated. More recently, we have seen core goods inflation starting to creep higher as well. Big purchase items like automobiles, sports/recreation, and household equipment, as well has personal care goods and clothing have seen prices rise once again. Combined with services, this has been a recipe for higher core inflation.

The one area of the economy that has been most responsive to the BoC's past rate hikes has been housing. Following the spring 2023 sales surge, the BoC's June and July rate hikes have pushed mortgage rates up by over 1 percentage point. This has not only forced many buyers to question whether to jump into the market, but has resulted in a large increase in the number of listings. Today's data have added to the negative trend, with sales down 9% since the June 2023 peak. With listings rising 35% since the spring, the sales-to-listings ratio is now at 51.4% (from 67.8% in April). The move away from a sellers' market has pushed house prices lower by 5.2% in the last four months.

For the BoC, the slowdown in the housing market shouldn't come as a surprise. This is the one area where the BoC's actions have the most impact. But as Governor Macklem said today, the BoC is "looking for clear signs that core inflation" is coming down. The issue here is that prior labour market strength will continue to push wages upwards, keeping inflation and the risk of another rate hike too high for comfort.

Weekly Economic & Financial Commentary: Inflation Continues to Gradually Drift Lower

Summary

United States: Inflation Continues to Gradually Drift Lower

- The Consumer Price Index (CPI) rose 0.4% in September, a monthly change that was a bit softer than the 0.6% increase registered in August. The core CPI rose 0.3% during the month, a pace unchanged from the month prior. Overall, the cooling trend in inflation remains in place and price pressures are likely to ease further, in our view. That noted, a 0.5% rise in the Producer Price Index (PPI) shows that continued progress on inflation is likely to be slow.

- Next week: Retail Sales (Tue.), Industrial Production (Tue.), Existing Home Sales (Thu.)

International: U.K. Growth Remains Near A Stand Still

- U.K. GDP rose 0.2% month-over-month in August, only partly offsetting a large July decline, meaning a contraction in overall Q3 GDP cannot be ruled out. Services output rose in August, though consumer facing services activity remained soft, and industrial output declined further. Given the underwhelming economic trends, we still expect the U.K. to fall into recession by Q4 of this year.

- Next week: China GDP (Wed.), U.K. CPI (Wed.), Japan CPI (Fri.)

Credit Market Insights: Where Credit is Due: Student Loans Explain Fall in Consumer Credit

- Total consumer credit outstanding, which excludes mortgages, fell $15.6 billion in August. The precipitous decline stemmed from a $26.9 billion decrease in consumer installment loans held by the federal government. Notably, this line includes student loans originated and purchased by the U.S. Department of Education.

Topic of the Week: Israel-Gaza Conflict Views & Potential Implications

- Hamas' attack on Israel marks another major geopolitical challenge permeating across the globe. Predicting the evolution of the Israel-Gaza conflict is difficult; however, Prime Minister Netanyahu's declaration of war against Hamas and subsequent rhetoric seem to suggest a speedy de-escalation is not on the horizon.

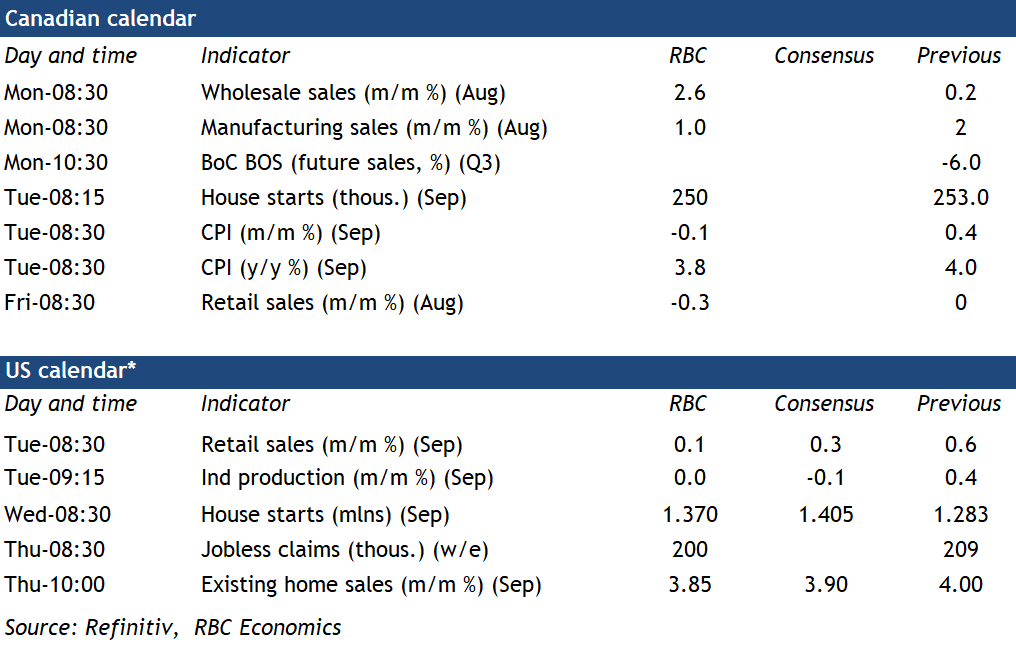

Canadian Inflation Expected to Edge Lower in September

Inflation data and the Bank of Canada’s closely-watched Business Outlook Survey will be front and center in a busy week of Canadian economic data releases. Canadian headline CPI growth is expected to edge down to 3.8% year-over-year in September from August’s 4% print. Year-over-year growth in energy prices likely accelerated – gasoline prices edged lower in September from August but were still up almost 7% from a year ago compared to a 1.5% year-over-year increase in August.

But food price growth is expected to continue to trend lower and the BoC has been more concerned about recent price growth in a range of ‘core’ measures designed to be a better gauge of broader Canadian (as opposed to globally produced) inflation pressures. We look for price growth excluding food and energy prices to slow to 3.3% year-over-year – just above the top end of the central bank’s (1 to 3%) target range despite mortgage interest costs continuing to surge higher. But the closely-watched 3-month rolling average of the BoC’s preferred ‘trim’ and ‘median’ price growth measures both accelerated to a 4 ½% annualized rate in August, adding to concerns that underlying price growth is not slowing despite a softening macroeconomic backdrop. We continue to expect price growth to slow going forward, and that would be consistent with year-over-year price growth ticking lower in each of the ‘trim’, ‘median’, and trim services ex-shelter (sometimes called ‘supercore’) measures in September.

Firms’ price-setting behaviour will also be front-and-center in the BoC’s own Business Outlook Survey. Prior surveys showed that firms’ were making larger and more frequent changes to prices during the initial spike in inflation. Subsequent surveys have suggested that pendulum is swinging back but the BoC’s Deputy Governor Vincent reiterated earlier this month that a return to ‘normal’ price-setting behaviour is needed to get inflation sustainably back to target. Firms’ inflation expectations will also be watched closely along with consumers’ views from the separate Survey of Consumer Expectations. We anticipate the BOS will signal softer business conditions in line with softening in near-term economic growth indicators, and some further easing in labour shortages given a higher unemployment rate and lower job openings.

Week ahead data watch

August retail sales likely edged down 0.3%, according to StatCan’s advanced indicator. We expect lower auto sales (down 1.8% on a seasonally adjusted basis) contributed to much of the slowdown. That decline was offset as Canadians paid more at the pumps, resulting in higher (nominal) gasoline sales. That implies a 1% drop in retail sales in volume terms.

We expect manufacturing sales to increase by 1% in August, in line with StatCan’s preliminary estimate. Most of the growth was seen in petroleum and coal product (higher prices) and food subsectors. ‘Core’ wholesale sales went up by 2.6% during that month, supported by higher sales in the machinery, equipment and supplies subsectors.

September U.S. retail sales likely ticked up 0.1% from the prior month. Unit auto sales recovered (+2%) in September after two consecutive declines in prior months. Gas prices were still high, but growing at a slower pace; sales at gas stations likely remained flat during that month.

U.S. industrial production was likely flat in September. Higher output in the manufacturing sector was offset by lower utility output. Higher hours worked in the manufacturing sector contributed to the former, while a lower number of heating and cooling days dragged the latter down.

Week Ahead – US Retail Sales and Earnings, Major Chinese Data, and UK Inflation and Employment Readings

US

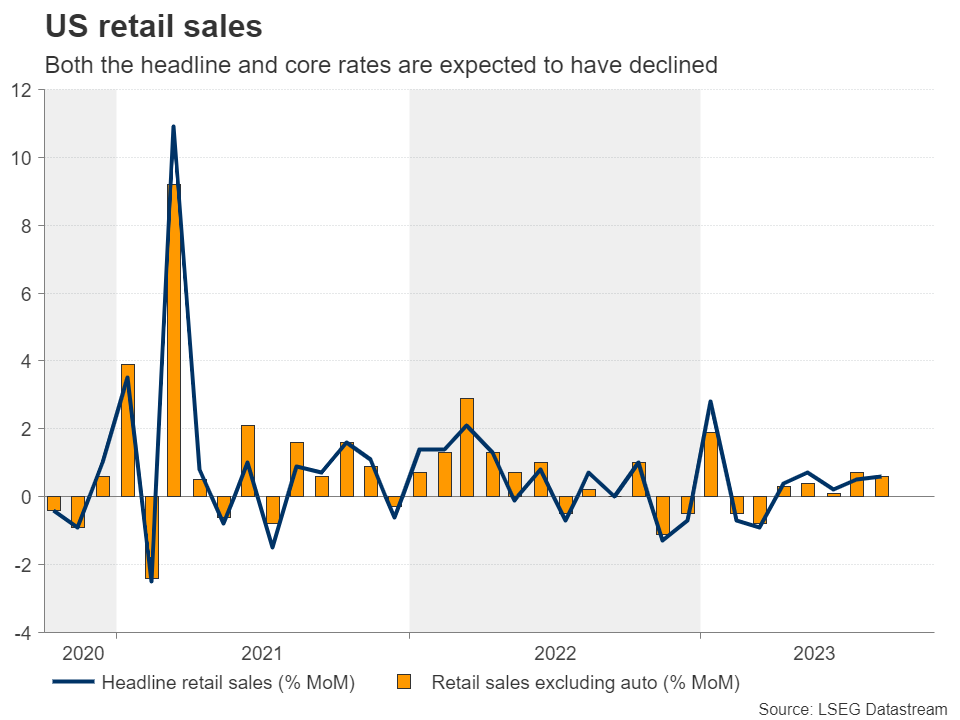

This week Wall Street will learn how quickly the US consumer is weakening and if the manufacturing part of the economy is close to entering recovery mode. The US retail sales report for September is expected to show monthly sales increased 0.3%, down from the 0.6% in the previous month. Sales excluding cars and gasoline are expected to rise 0.1%, a tick lower than the August reading. The Empire Manufacturing survey is expected to show the September surprise 1.9 expansion was not the beginning of a new trend as the headline reading falls to -5.0.

Much attention will fall on earnings season and a lot of Fed speak. Big earnings for the week will come from American Express, Bank of America, J&J, Lockheed Martin, Morgan Stanely, Netflix, Procter & Gamble, and Tesla.

The upcoming week is filled with Fed speak, as traders will focus on Fed Chair Jerome Powell’s speech at the Economic Club of New York and with the release of their Beige Book. The Fed hawks Bowman and Waller will draw extra attention to see if they are close to abandoning their calls for further tightening.

Washington DC will remain in the spotlight as House Republicans struggle to elect a new House speaker.

Eurozone

Christine Lagarde is once again the highlight with appearances over the weekend likely to attract interest. That said, I’m not sure how much we can learn at this point, we’ve heard a lot from the ECB President recently. That aside, the final HICP inflation reading will be of interest although revisions are that common and when they do occur, they’re often small.

UK

There are a number of key economic releases to watch out for next week, the most obvious being CPI inflation on Wednesday but jobs figures on Tuesday and retail sales on Friday will also be very closely monitored. Then there’s BoE Governor Andrew Bailey’s appearance over the weekend which could offer important insight after such a close vote at the last meeting. Huw Pill also appears on Monday.

Russia

Inflation rose faster than expected in September which will keep the pressure on the Russian central bank despite having already raised rates aggressively. Next up it’s PPI and the CBR will be hoping for some better news.

South Africa

Wednesday is the big day next week with inflation data due first and retail sales later on. Inflation is well within the SARB’s 3-6% target range but it won’t take much to make them nervous again and stimulate debate around the potential need for another rate hike.

Turkey

No major economic releases or events next week.

Switzerland

No major economic releases or events next week.

China

A busy week on the economic calendar. China central bank, PBoC’s decision on a set of key benchmark policy interest rates will be in the limelight while consensus is expecting another month of no rate cut on the 1-year Medium-Term Lending Facility rate at 2.50% out on Monday, and on Friday, the 1-year and 5-year Loan Prime rates are expected to remain unchanged at 3.45% and 4.2%. However, the persistent liquidity crunch in the property market has led to an increased risk of an impending default by Country Garden, China’s largest private property developer on its due bonds’ principal repayments in recent days may spark a rethinking of China’s monetary policy that is currently operating on a targeted easing approach.

On Wednesday, Q3 GDP, retail sales, industrial production, and the unemployment rate for September will be released. The consensus is expecting a slip in Q3 GDP growth to 4.4% y/y from 6.3% y/y in Q2. If it turns out as expected, it will be the weakest quarterly growth and put the 2023 annual growth target of around 5% at risk of not achieving it.

Industrial production is expected to ease slightly to 4.3% y/y from 4.5% y/y in August, together with retail sales from 4.6% y/y in August to 4.5% y/y for September. Meanwhile, the overall unemployment rate is expected to hold steady at 5.2% but the concern still lies in the youth unemployment rate that has gone dark since August as China halted the release of such data. Its last publication was for June which saw the youth unemployment rate skyrocketed to an unprecedented level of 21.3%.

On Thursday, the House Price Index is forecasted to revert to a marginally positive growth of just 0.1% y/y in September from -0.1% y/y recorded in August.

India

No key data releases.

Australia

On Tuesday, RBA meeting minutes will be released, and market participants will be on the lookout for any dovish comments after the official cash policy rate was left unchanged at 4.1% for the fourth consecutive meeting.

Employment change for September will be out on Thursday where it is forecasted to decrease to a smaller magnitude of +15K from +64.9K jobs added in August. So far, data from the ASX 30-day interbank cash rate futures as of 12 October is just pricing in only a paltry chance of 5% on a 25 basis points hike in the cash policy rate to 4.35% for the next RBA monetary policy meeting in November.

New Zealand

Q3 inflation rate will be released on Tuesday where it is forecasted to ease slightly to 5.8% y/y from 6% in Q2. If it turns out as expected, it will be the third consecutive quarter of moderation in inflationary pressures.

The Balance of Trade for September will be out on Friday, and the trade deficit is forecasted to shrink to NZ$-1.9 billion from NZ$-2.29 billion in August.

Japan

Two key data to focus on. Balance of Trade for September out on Thursday where the trade deficit is expected to shrink to JPY-425 billion from JPY-930.5 billion due to a reduction in imports growth to -12.9% y/y for September from 17.8% y/y in August while exports growth for September is expected to improve to 3.1% y/y from -0.8% y/y in August.

The key national inflation data for September will be released on Friday where the core inflation rate is expected to ease further to 2.7% y/y from 3.1% y/y in August, and the core-core inflation rate (excluding fresh food & energy) is also forecasted to dip to 4.1% y/y from 4.3% y/y in August. If these inflation numbers turn out as expected, the impetus for the Bank of Japan to normalise its negative interest rate policy in early 2024 is likely to be reduced.

Singapore

Balance of Trade and Non-oil exports (NODX) for September will be released on Tuesday. NODX growth has continued to decline in negative territory for eleven consecutive months where it plummeted by -20.1% y/y in August.

Economic Calendar

Saturday, Oct. 14

Economic Events:

- New Zealand election: Expectations are for a rightward and populist shift

- Top EU diplomat Borrell speaks after a three-day visit to China.

- IMF/World Bank meetings run through Sunday. ECB President Lagarde participates in a panel at the G30 international banking seminar.

- BOE Gov Bailey speaks on the G30 panel on global economic and monetary challenges.

Sunday, Oct. 15

Economic Events:

- Polish holds a parliamentary election

- India’s 20% export levy is set to expire.

- World Health Summit begins

Monday, Oct. 16

Economic Data/Events:

- US Empire Manufacturing index

- China medium-term lending facility rate

- India wholesale prices

- Italy CPI

- Japan industrial production

- Philippines overseas remittances

- US Treasury Secretary Yellen meets with euro-area finance ministers in Luxembourg.

- RBA’s Jones speaks at AFR Cryptocurrency Summit.

- Fed’s Harker speaks at a Mortgage Bankers Association event in Philadelphia.

- ECB’s Villeroy speaks at the Fintech forum in Paris.

- BOE chief economist Pill speaks at OMFIF Economic and Monetary Policy Institute.

- Russian Foreign Minister Lavrov visits China through Wednesday.

Tuesday, Oct. 17

Economic Data/Events:

- US retail sales, business inventories, industrial production, cross-border investment

- Canada housing starts, CPI

- Germany ZEW survey expectations

- Japan tertiary industry index

- Mexico international reserves

- New Zealand CPI

- Singapore trade

- UK jobless claims, unemployment

- Earnings from Goldman Sachs and Bank of America

- Chinese President Xi Jinping hosts world leaders including President Putin at the Belt and Road Initiative forum in Beijing

- BOE’s Dhingra is part of an inflation and cost of living panel at the Royal Economic Society Summit

- ECB’s de Guindos and Knot speak at the Joint ECB/IMF policy and research conference in Frankfurt.

- ECB’s Centeno makes opening remarks at a conference in Lisbon about central banks’ sanctioning powers

- Fed’s Williams moderates discussion with Intel CEO at Economic Club of New York.

- Fed’s Barkin speaks to the Real Estate Roundtable in Washington.

- South African Reserve Bank (SARB) issues monetary policy review.

Wednesday, Oct. 18

Economic Data/Events:

- Federal Reserve issues Beige Book economic survey.

- US housing starts

- China GDP, retail sales, industrial production

- Eurozone CPI

- Italy trade

- South Africa retail sales

- UK CPI

- Earnings from Morgan Stanley, Netflix, and Tesla

- RBA Governor Bullock speaks at AFSA annual summit in Sydney.

- Fed’s Harker speaks at an event at Philadelphia Fed.

- Fed’s Williams participates in a moderated discussion at Queens College.

- Sweden’s Riksbank Governor Thedeen and Deputy Governor Floden speak on monetary policy.

Thursday, Oct. 19

Economic Data/Events:

- US initial jobless claims, existing home sales, leading index

- Australia unemployment

- China property prices

- Japan trade

- Spain trade

- Fed Chair Powell speaks at the Economic Club of New York.

- Fed’s Goolsbee speaks at Wisconsin Manufacturers & Commerce Business Day.

- Fed’s Bostic speaks on policy and inequality at the New School in New York.

- Fed’s Harker speaks at CFA society in Philadelphia.

- Fed’s Logan speaks at a Money Marketeers of New York University event.

Friday, Oct. 20

Economic Data/Events:

- Canada retail sales

- China loan prime rates

- Eurozone new car registrations

- Hong Kong CPI

- Japan CPI

- New Zealand trade

- Taiwan export orders

- President Biden hosts the EU’s von der Leyen and Michel in Washington.

- Fed’s Harker speaks at a Risk Management Association event in Philadelphia.

Sovereign Rating Updates:

- Greece (S&P)**Note could receive first upgrade to investment grade status

- Italy (S&P)

- Netherlands (S&P)

- United Kingdom (S&P)

- France (Moody’s)

- Ireland (Moody’s)

- United Kingdom (Moody’s)

Summary 10/16 – 10/20

Monday, Oct 16, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Sep | 47.1 | |

| 23:01 | GBP | Rightmove House Price Index M/M Oct | 0.40% | |

| 04:30 | JPY | Industrial Production M/M Aug F | 0.00% | 0.00% |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Aug | 5.4B | 2.9B |

| 12:30 | CAD | Manufacturing Sales M/M Aug | 1.60% | |

| 12:30 | CAD | Wholesale Sales M/M Aug | 0.20% | |

| 12:30 | USD | Empire State Manufacturing Index Oct | -4.5 | 1.9 |

| 14:30 | CAD | BoC Business Outlook Survey | ||

| 21:45 | NZD | CPI Q/Q Q3 | 1.90% | 1.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Sep | |

| Forecast: | Previous: 47.1 | ||

| 23:01 | GBP | Rightmove House Price Index M/M Oct | |

| Forecast: | Previous: 0.40% | ||

| 04:30 | JPY | Industrial Production M/M Aug F | |

| Forecast: 0.00% | Previous: 0.00% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Aug | |

| Forecast: 5.4B | Previous: 2.9B | ||

| 12:30 | CAD | Manufacturing Sales M/M Aug | |

| Forecast: | Previous: 1.60% | ||

| 12:30 | CAD | Wholesale Sales M/M Aug | |

| Forecast: | Previous: 0.20% | ||

| 12:30 | USD | Empire State Manufacturing Index Oct | |

| Forecast: -4.5 | Previous: 1.9 | ||

| 14:30 | CAD | BoC Business Outlook Survey | |

| Forecast: | Previous: | ||

| 21:45 | NZD | CPI Q/Q Q3 | |

| Forecast: 1.90% | Previous: 1.10% | ||

Tuesday, Oct 17, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | RBA Minutes | ||

| 06:00 | GBP | Claimant Count Change Sep | 2.3K | 0.9K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Aug | 4.30% | 4.30% |

| 06:00 | GBP | Average Earnings Including Bonus (3Mo/Yr) Aug | 8.30% | 8.50% |

| 06:00 | GBP | Average Earnings Excluding Bonus (3Mo/Yr) Aug | 7.80% | 7.80% |

| 09:00 | EUR | Germany ZEW Economic Sentiment Oct | -9.5 | -11.4 |

| 09:00 | EUR | Germany ZEW Current Situation Oct | -80.5 | -79.4 |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Oct | -8.0 | -8.9 |

| 12:15 | CAD | Housing Starts Sep | 250K | 253K |

| 12:30 | CAD | CPI M/M Sep | 0.40% | |

| 12:30 | CAD | CPI - Core M/M Sep | 0.30% | |

| 12:30 | CAD | CPI Median Y/Y Sep | 4.10% | |

| 12:30 | CAD | CPI Common Y/Y Sep | 3.90% | |

| 12:30 | CAD | CPI Trimmed Y/Y Sep | 4.80% | |

| 12:30 | USD | Retail Sales M/M Sep | 0.30% | 0.60% |

| 12:30 | USD | Retail Sales ex Autos M/M Sep | 0.20% | 0.60% |

| 13:15 | USD | Industrial Production M/M Sep | -0.10% | 0.40% |

| 13:15 | USD | Capacity Utilization Sep | 79.60% | 79.70% |

| 14:00 | USD | Business Inventories Aug | 0.30% | 0.00% |

| 14:00 | USD | NAHB Housing Market Index Oct | 45 | 45 |

| 23:30 | AUD | Westpac Leading Index M/M Sep | -0.04% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | RBA Minutes | |

| Forecast: | Previous: | ||

| 06:00 | GBP | Claimant Count Change Sep | |

| Forecast: 2.3K | Previous: 0.9K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Aug | |

| Forecast: 4.30% | Previous: 4.30% | ||

| 06:00 | GBP | Average Earnings Including Bonus (3Mo/Yr) Aug | |

| Forecast: 8.30% | Previous: 8.50% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus (3Mo/Yr) Aug | |

| Forecast: 7.80% | Previous: 7.80% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Oct | |

| Forecast: -9.5 | Previous: -11.4 | ||

| 09:00 | EUR | Germany ZEW Current Situation Oct | |

| Forecast: -80.5 | Previous: -79.4 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Oct | |

| Forecast: -8.0 | Previous: -8.9 | ||

| 12:15 | CAD | Housing Starts Sep | |

| Forecast: 250K | Previous: 253K | ||

| 12:30 | CAD | CPI M/M Sep | |

| Forecast: | Previous: 0.40% | ||

| 12:30 | CAD | CPI - Core M/M Sep | |

| Forecast: | Previous: 0.30% | ||

| 12:30 | CAD | CPI Median Y/Y Sep | |

| Forecast: | Previous: 4.10% | ||

| 12:30 | CAD | CPI Common Y/Y Sep | |

| Forecast: | Previous: 3.90% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Sep | |

| Forecast: | Previous: 4.80% | ||

| 12:30 | USD | Retail Sales M/M Sep | |

| Forecast: 0.30% | Previous: 0.60% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Sep | |

| Forecast: 0.20% | Previous: 0.60% | ||

| 13:15 | USD | Industrial Production M/M Sep | |

| Forecast: -0.10% | Previous: 0.40% | ||

| 13:15 | USD | Capacity Utilization Sep | |

| Forecast: 79.60% | Previous: 79.70% | ||

| 14:00 | USD | Business Inventories Aug | |

| Forecast: 0.30% | Previous: 0.00% | ||

| 14:00 | USD | NAHB Housing Market Index Oct | |

| Forecast: 45 | Previous: 45 | ||

| 23:30 | AUD | Westpac Leading Index M/M Sep | |

| Forecast: | Previous: -0.04% | ||

Wednesday, Oct 18, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Sep | 5.30% | 5.20% |

| 00:30 | AUD | CPI Q/Q Q3 | 1.10% | 0.80% |

| 00:30 | AUD | CPI Y/Y Q3 | 5.30% | 6.00% |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q3 | 1.10% | 1.00% |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q3 | 5.00% | 5.90% |

| 08:00 | CHF | Credit Suisse Economic Expectations Oct | -27.6 | |

| 08:00 | EUR | Germany IFO Business Climate Oct | 85.9 | 85.7 |

| 08:00 | EUR | Germany IFO Current Assessment Oct | 88.5 | 88.7 |

| 08:00 | EUR | Germany IFO Expectations Oct | 83.3 | 82.9 |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Sep | -1.70% | -1.30% |

| 14:00 | USD | New Home Sales Sep | 684K | 675K |

| 14:00 | CAD | BoC Interest Rate Decision | 5.00% | 5.00% |

| 14:30 | USD | Crude Oil Inventories | -0.5M | -4.5M |

| 15:00 | CAD | BoC Press Conference | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Sep | 2.00% | 2.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Sep | |

| Forecast: 5.30% | Previous: 5.20% | ||

| 00:30 | AUD | CPI Q/Q Q3 | |

| Forecast: 1.10% | Previous: 0.80% | ||

| 00:30 | AUD | CPI Y/Y Q3 | |

| Forecast: 5.30% | Previous: 6.00% | ||

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q3 | |

| Forecast: 1.10% | Previous: 1.00% | ||

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q3 | |

| Forecast: 5.00% | Previous: 5.90% | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Oct | |

| Forecast: | Previous: -27.6 | ||

| 08:00 | EUR | Germany IFO Business Climate Oct | |

| Forecast: 85.9 | Previous: 85.7 | ||

| 08:00 | EUR | Germany IFO Current Assessment Oct | |

| Forecast: 88.5 | Previous: 88.7 | ||

| 08:00 | EUR | Germany IFO Expectations Oct | |

| Forecast: 83.3 | Previous: 82.9 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Sep | |

| Forecast: -1.70% | Previous: -1.30% | ||

| 14:00 | USD | New Home Sales Sep | |

| Forecast: 684K | Previous: 675K | ||

| 14:00 | CAD | BoC Interest Rate Decision | |

| Forecast: 5.00% | Previous: 5.00% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: -0.5M | Previous: -4.5M | ||

| 15:00 | CAD | BoC Press Conference | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Sep | |

| Forecast: 2.00% | Previous: 2.10% | ||

Thursday, Oct 19, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q3 | -3 | |

| 00:30 | AUD | Employment Change Sep | 20.3K | 64.9K |

| 00:30 | AUD | Unemployment Rate Sep | 3.70% | 3.70% |

| 06:00 | CHF | Trade Balance (CHF) Sep | 3.77B | 4.05B |

| 08:00 | EUR | Eurozone Current Account (EUR) Aug | 20.9B | |

| 12:30 | CAD | Industrial Product Price M/M Sep | 1.30% | |

| 12:30 | CAD | Raw Material Price Index Sep | 3.00% | |

| 12:30 | USD | Initial Jobless Claims (Oct 13) | 210K | 209K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Oct | -6.5 | -13.5 |

| 14:00 | USD | Existing Home Sales Sep | 3.90M | 4.04M |

| 14:30 | USD | Natural Gas Storage | 84B | |

| 21:45 | NZD | Trade Balance (NZD) Sep | -2291M | |

| 23:01 | GBP | GfK Consumer Confidence Oct | -20 | -21 |

| 23:30 | JPY | National CPI Y/Y Sep | 3.20% | |

| 23:30 | JPY | National CPI ex-Fresh Food Y/Y Sep | 2.80% | 3.10% |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Sep | 4.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q3 | |

| Forecast: | Previous: -3 | ||

| 00:30 | AUD | Employment Change Sep | |

| Forecast: 20.3K | Previous: 64.9K | ||

| 00:30 | AUD | Unemployment Rate Sep | |

| Forecast: 3.70% | Previous: 3.70% | ||

| 06:00 | CHF | Trade Balance (CHF) Sep | |

| Forecast: 3.77B | Previous: 4.05B | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Aug | |

| Forecast: | Previous: 20.9B | ||

| 12:30 | CAD | Industrial Product Price M/M Sep | |

| Forecast: | Previous: 1.30% | ||

| 12:30 | CAD | Raw Material Price Index Sep | |

| Forecast: | Previous: 3.00% | ||

| 12:30 | USD | Initial Jobless Claims (Oct 13) | |

| Forecast: 210K | Previous: 209K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Oct | |

| Forecast: -6.5 | Previous: -13.5 | ||

| 14:00 | USD | Existing Home Sales Sep | |

| Forecast: 3.90M | Previous: 4.04M | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 84B | ||

| 21:45 | NZD | Trade Balance (NZD) Sep | |

| Forecast: | Previous: -2291M | ||

| 23:01 | GBP | GfK Consumer Confidence Oct | |

| Forecast: -20 | Previous: -21 | ||

| 23:30 | JPY | National CPI Y/Y Sep | |

| Forecast: | Previous: 3.20% | ||

| 23:30 | JPY | National CPI ex-Fresh Food Y/Y Sep | |

| Forecast: 2.80% | Previous: 3.10% | ||

| 23:30 | JPY | National CPI ex Food Energy Y/Y Sep | |

| Forecast: | Previous: 4.30% | ||

Friday, Oct 20, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | GBP | Retail Sales Y/Y Sep | -0.40% | 0.40% |

| 06:00 | EUR | Germany PPI M/M Sep | 0.40% | 0.30% |

| 06:00 | EUR | Germany PPI Y/Y Sep | -12.60% | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Sep | 17.7B | 10.8B |

| 12:30 | CAD | Retail Sales M/M Aug | 0.30% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Aug | 1.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | GBP | Retail Sales Y/Y Sep | |

| Forecast: -0.40% | Previous: 0.40% | ||

| 06:00 | EUR | Germany PPI M/M Sep | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 06:00 | EUR | Germany PPI Y/Y Sep | |

| Forecast: | Previous: -12.60% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Sep | |

| Forecast: 17.7B | Previous: 10.8B | ||

| 12:30 | CAD | Retail Sales M/M Aug | |

| Forecast: | Previous: 0.30% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Aug | |

| Forecast: | Previous: 1.00% | ||

Week Ahead – US Retail Sales and UK CPI Data Enter the Sspotlight

- After US CPIs, US retail sales may also impact Fed hike expectations

- Will the UK inflation numbers increase the chances for another BoE hike?

- Aussie and Kiwi traders await Australia jobs report and New Zealand’s CPI

- China’s GDP could also impact those commodity-linked currencies

Will retail sales allow the dollar to extend its recovery?

The dollar traded on the back foot for the better half of this week due to dovish remarks by Fed officials who suggested that the surge in Treasury yields since they last met has done the work for them, implying that another hike before the end of the year may not be needed.

However, Thursday’s CPIs revealed that headline inflation held steady at 3.7% y/y, instead of slowing to 3.6% as expected, encouraging market participants to bring rate hike bets back to the table. From 28%, the probability for a final quarter-point rate increment increased to around 40%, while the rate reductions penciled in for next year have been reduced by around 10bps. This helped the dollar rebound.

As they try to further clear the fog, investors are likely to keep their gaze locked on more Fed speeches next week, with several officials scheduled to step onto the rostrum. It will be interesting to hear what they have to say in the aftermath of the inflation numbers.

That said, although their view on interest rates may be a priority for market participants, economic data may also be closely monitored for updated indications on how the world’s largest economic powerhouse has been faring.

On Tuesday, headline and core retail sales for September are forecast to have slowed to 0.2% m/m and 0.1% m/m respectively after both growing by 0.6% in August, while industrial production is also expected to have decelerated. On Thursday, although housing starts are seen increasing, the more forward-looking building permits are forecast to have slid, while on Friday, existing home sales are expected to have declined, suggesting that the housing market continues to cool down.

Nonetheless, with the Atlanta Fed GDPNow being upwardly revised to indicate that the US economy has expanded 5.1% in Q3, the dollar is unlikely to take another strong hit from slightly softer data, especially if Fed officials start talking about one more hike before the end credits of this tightening crusade roll. Even if the greenback pulls back again, such a retreat may be seen by the bulls as an opportunity to add to their positions at more attractive levels.

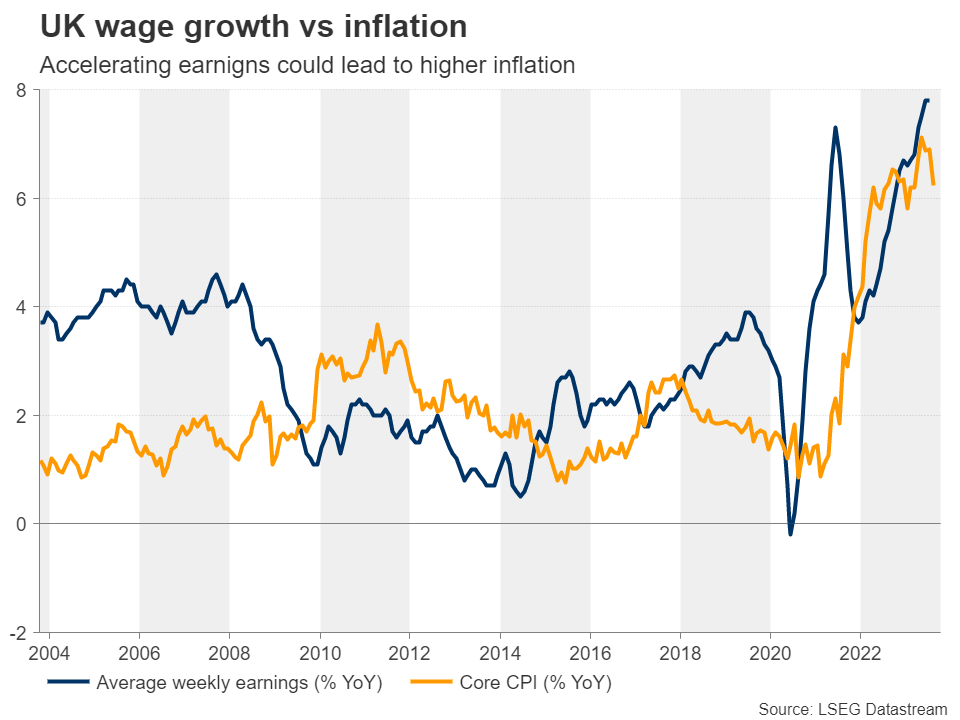

UK jobs, CPI, and retail sales data to shake the pound

The British pound will also enter the spotlight next week, with the agenda including the UK employment report for August on Tuesday, the CPI figures for September on Wednesday, and the retail sales for the same month on Friday.

At its latest gathering, the BoE kept rates steady citing slowing economic activity and a cooling labor market, and with the data since then keep painting a gloomy picture, investors are assigning a 78% probability for policymakers to remain sidelined at their next meeting in November, with the remaining 22% pointing to one last 25bps hike. They believe that a final hike is more likely to happen after the turn of the year, with a 55% probability assigned to the March 2024 decision.

The only data point corroborating more interest rate hikes by the BoE is wage growth, which remains elevated. Thus, for the hike probability to rise, just another print of strong weekly earnings may not be enough to change investors’ opinion. The CPI data may need to indicate that inflation is stickier than previously thought and retail sales may need to accelerate.

Loonie also awaits inflation numbers

Canada also releases its inflation numbers on Tuesday. In early September, the Bank of Canada kept interest rates untouched but noted that they remain concerned about the persistence of underlying inflationary pressures, and that’s why they remain prepared to raise rates further if needed.

Still, investors are not expecting any action at the upcoming meeting on October 25, assigning only a 23% probability for a 25bps increment, while the chances for hitting the hike button one last time by March 2024 are those of a coin toss. Even if participants are not convinced that another hike may be warranted this year, they could raise the probability for an increase being delivered at the turn of the year if the CPI numbers confirm the BoC’s concerns, something that may allow the loonie to recover some ground against its neighboring greenback.

Aussie and kiwi traders may have a very busy schedule

Traders of the other risk-linked currencies, the aussie and the kiwi, may also stay busy next week.

On Tuesday, the RBA releases the minutes of its latest gathering, where officials kept interest rates untouched for the fifth consecutive month but added that some further tightening of policy may be required, while on Thursday, Australia’s jobs data will be released.

Although investors see an 83% probability for the Bank to remain sidelined in November as well, they are assigning a decent 60% chance for another 25bps hike to be delivered by May 2024. Thus, numbers pointing to a still-tight labor market may encourage aussie traders to add to their long positions.

Kiwi traders may do the same if New Zealand’s CPI for Q3 comes in hotter than expected. The RBNZ stayed sidelined earlier this month and offered no hints on whether they are considering additional rate increases following the much-better-than-expected GDP data for Q2. However, similarly to the RBA, investors are assigning a more than 50% probability for one last 25bps hike by May.

Having said all that, due to the close trade ties Australia and New Zealand have with China, both currencies could also stay sensitive to developments and data concerning the world’s second largest economy. On Wednesday, China’s GDP for Q3 is on the agenda, accompanied by the industrial production, retail sales and fixed asset investment figures for September. Should these releases corroborate the view that the Chinese economy is stabilizing, the aussie and the kiwi could benefit.

Earnings season kicks off

In the equity arena, the earnings season is kicking off today with results from major US banks, while on Wednesday, Tesla and Netflix will make their numbers public after the closing bell.

Weekly Focus – Geopolitics and Inflation Spark Volatility in the Markets

Risk sentiment remained shaky over the past week as markets digested a mix of renewed geopolitical worries, mixed data on inflation and cautious signals from the central bankers. The conflict between Israel and Hamas has quickly escalated into the worst bloodbath in 50 years on both sides. Hamas's attacks are estimated to have caused 1300 casualties, most of which civilian, while Israel has begun a massive counteroffensive towards Gaza in response. Possible involvement of the Iran-backed Hezbollah remains a key worry, although many of the surrounding Arab nations, including Qatar and Egypt, have so far pushed to avoid further escalation. As both Israel and Iran are small natural gas exporters, and the production of the former has already been affected, European natural gas prices rose by around 40% this week. Oil markets have remained calmer, dampened by cooling demand and spare production capacity especially in Saudi Arabia. Read our early take on the outlook from Monday: Geopolitical radar - Extra edition: Fauda - what to expect from chaos in Israel? 9 October.

On the data front, US September CPI surprised to the upside for the second month in a row. Headline CPI rose by 0.4% m/m (consensus 0.3%), while core CPI was better in line with expectations at 0.3% m/m (consensus 0.3%). Shelter inflation (+0.65% m/m; Aug +0.29%) accelerated against expectations, even though more timely rental price indices still point towards moderating inflation. Health care prices, which are distorted by lagged estimation of health insurance premiums, contributed to the upside surprise as well. Excluding the two categories, core services inflation cooled in m/m terms, which is a positive signal of moderating underlying inflation for the Fed. We still believe rate hikes are already over in the US, which remains the base case for the markets as well. We discussed the mixed data in more detail in our monthly Global Inflation Watch, 13 October.

While equity and credit markets remained relatively stable, longer-dated US yields rose towards the end of the week and broad USD appreciated. Besides the CPI print, weak demand on 3y, 10y and 30y UST auctions played a role, as persistent budget deficits seem to remain a key worry for markets even amid the uncertain economic outlook. In any case, central bankers have sounded increasingly cautious about hiking rates further in an environment where financial conditions have tightened markedly since summer. September meeting minutes from both the ECB and the Fed also flagged growing worries about the risk of overtightening monetary policy.

Next week, the focus will turn to economic data. US retail sales are expected to signal weakening consumer demand after early credit card data and leading services PMI components fell in September. In Europe, German October ZEW index will provide hints on the latest investor sentiment amid higher uncertainty, and final September HICP data will give more detailed insight into inflation drivers. In UK, focus will be on both labour market and inflation data. The latest KPMG and REC report on jobs pointed towards cooling wage inflation, while markets will keep a close eye on if the August downtick in price inflation was just a one-off. In China, Q3 GDP is expected to come out around 1.0% q/q, which would pave way for the government to meet its growth target of 5%.

Fed’s Harker advocates for steady rates, doing nothing is still doing something

Philadelphia Fed President Patrick Harker said today that interest rates should remain steady, barring any significant economic upheaval.

He plainly stated, "Absent a stark turn in what I see in the data and hear from contacts, I believe that we are at the point where we can hold rates where they are."

Harker emphasized the need for patience, noting the lag between policy implementation and its tangible effects. He remarked, "It will take some time for the full impact of the higher rates to be felt."

In his view, by maintaining rates, "holding rates steady will let monetary policy do its work," which, given its current restrictive nature, would help curb inflation and stabilize the markets.

He further iterated the significance of policy inaction, saying, "By doing nothing, we are still doing something," implying that the current policy stance itself is a significant measure. He further remarked, "we are doing quite a lot."

Inflation remains a primary concern, with Harker clarifying the Fed's position: "We will not tolerate a reacceleration in prices." However, he also cautioned against knee-jerk reactions to short-term price fluctuations, indicating the need for a balanced approach. "But second, I do not want to overreact to the normal month-to-month variability of prices."

Sunset Market Commentary

Markets

Geopolitical tensions run ever higher after Israel called for an evacuation of all civilians in Gaza City, indicating the country is preparing for a ground invasion. Such a move would bring the clash in the Middle East into a new stage. While markets dismissed the conflict quickly earlier this week, they obviously remain vulnerable for any escalation. It’s no surprise then, that they err on the side of caution going into a weekend full of uncertainties. Core bonds rally with US Treasuries outperforming after being hit by yesterday’s marginally higher-than-expected (headline) CPI and poor 30-year bond auction. Yields in the US drop between 4.6 (2-y) and 10.1 bps (10-y). German yields drop 4.5 to 7.4 bps in a similar curve shift. Central bank speech included BoE’s governor stressing the need for restrictive monetary policy. He said there was progress on inflation but there is more to do. ECB’s Nagel vowed the central bank won’t rest until inflation is back at target and Simkus noted “all preconditions” are here to consider an earlier stop to the full PEPP reinvestments (currently scheduled to run through 2024). The comments did little to alter the current bond direction though. Important movers in commodity markets include oil. Brent surges >4% to $89.8/barrel amid mounting fears for supply disruption. Gold rallies 2.3%, taking out the $1900 barrier once again. Stock markets trade on the backfoot but left the lows behind in afternoon trading. EuroStoxx50 sheds 0.5% compared to a 1.1% loss earlier on the day. US markets open with gains between 0.1-0.8%, helped higher by the first, solid earnings from major US banks. The dollar recouped some of the losses incurred in the Asian session but remains set for marginal losses against most major peers. EUR/USD ekes out a slight gain to 1.0536 while DXY struggles in the mid 106/107 area. The Japanese yen appreciates a tad. At USD/JPY 149.5 the currency is nowhere near out of the danger zone though. The Swiss franc is also benefiting from its safe haven status. Scandinavian currencies buck the typical risk-off trend with the NOK eyeballing the oil price and SEK profiting from above-consensus inflation figures (see below). CE currencies trade quietly. The Czech crown outperforms local peers slightly while the Polish zloty stabilizes going into this weekend’s parliamentary elections.

News & Views

The Food Price Index of the UN Food and Agriculture Organization (FAO) was virtually unchanged in September from August. The index is now 10.7% below its corresponding level a year ago and 24.0% from the all-time high reached in March 2022. Vegetal oil prices decreased 3.9% M/M to be 14.6% lower Y/Y, driven by lower world prices for palm, sunflower, soy and rapeseed oils. Diary prices declined for the ninth consecutive month. Meat prices eased slightly (-1.0% M/M and 5.0% Y/Y). These were counterbalanced by 1.0% M/M rise in cereal prices. However this index still stands 14.6% below the level of August last year. Within this category, maize prices increased by 7.0% M/M after nine months of consecutive rises. By contrast, international wheat prices continued to drop, falling by 1.6% M/M. The rice price eased 0.5% M/M but still remains 27.8% above its year earlier value. Sugar staged the most outspoken move. The index jumped another 9.8% M/M, reaching the highest level since November 2010. The increase mainly reflects concerns with respect to production declines in key sugar producers, Thailand and India, due to drier-than-normal weather conditions. Prices rises could have been bigger were it not for the large Brazilian crop.

Inflation in Sweden slowed less than expected in September. Headline CPI inflation rose 0.5% M/M resulting in 6.5% Y/Y inflation, down from 7.3% Y/Y in August but less than the 6.3% consensus. CPIF inflation (index with a fixed interest rate, the Riksbank’s reference) grew 0.4% M/M to be 4.0% Y/Y. Core CPIF inflation (ex. energy) remains elevated at 0.5% M/M and 6.9% Y/Y. The monthly rise, amongst others, was driven by restaurants and hotels (0.6%), vulture and leisure (0.8%), healthcare (1.0%) household goods (2.0%) and clothing and footwear (4.7%). The Riksbank at its September 21 meeting raised the policy rate to 4.0% and left the door open for a ‘final’ 25 bps step if necessary. Today’s data raised the stakes for the November 23 meeting. However, the Riksbank also has to consider a very poor growth context and high consumer sensitivity to higher rates. The central bank today also reported that it sold USD 390 mln of FX in the week of September 25 as part of the hedging policy of FX reserves. The bank sold no euros. The amount was on the lower side of what some in the market expected. The Swedish krone gained modest ground today with EUR/SEK declining from about 11.58 to 11.54 currently.

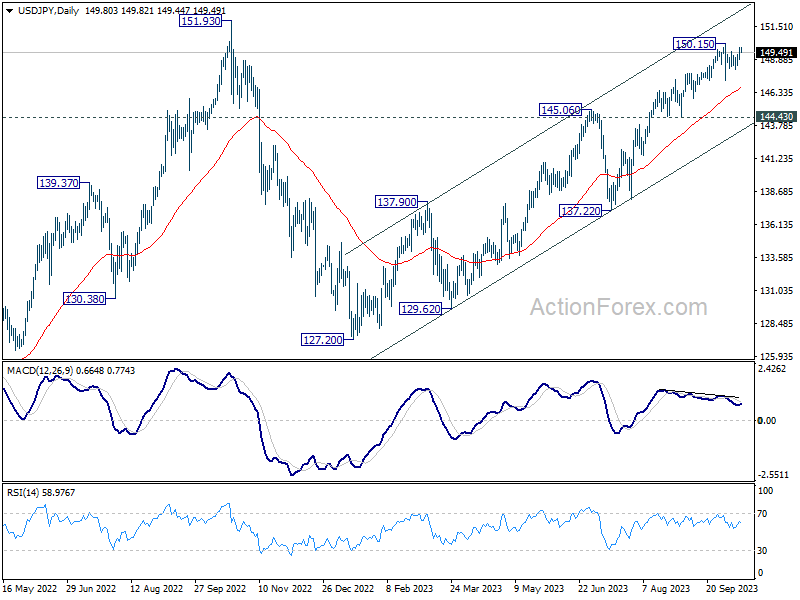

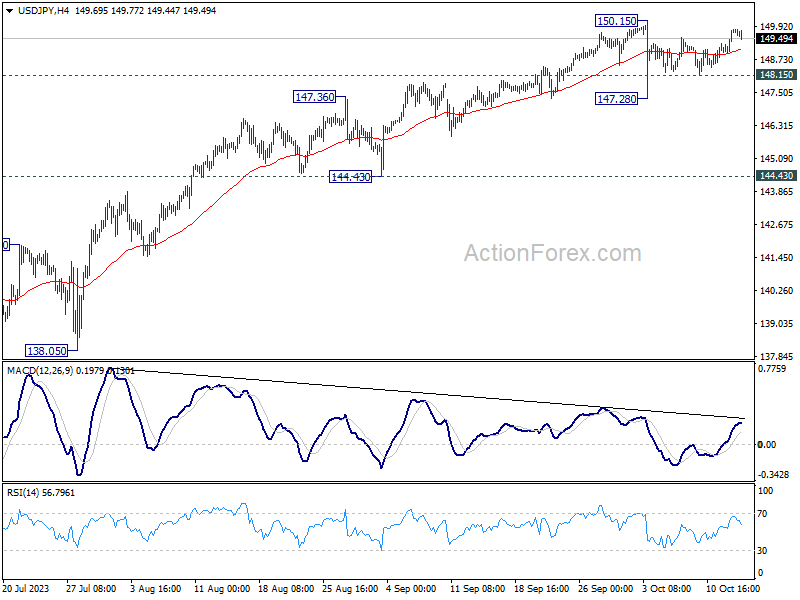

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.24; (P) 149.53; (R1) 150.11; More...

Intraday bias in USD/JPY remains neutral as it's still bounded in range below 150.15. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high. On the downside, below 148.24 minor support will turn bias to the downside for another down leg through 147.28.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.