Sample Category Title

GBP/USD: Remains Constructive Despite Weak UK Data

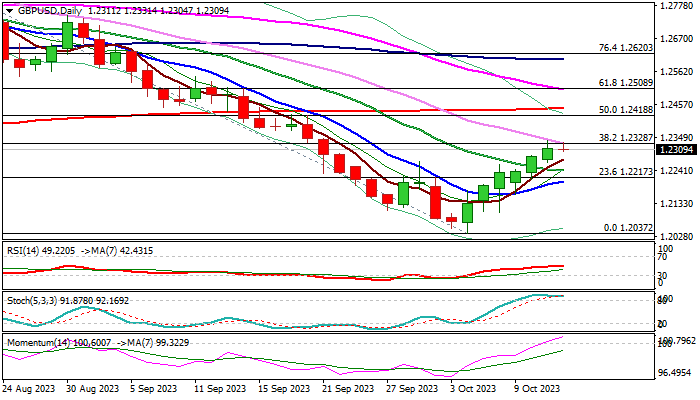

Cable is holding around 1.23 handle in early Thursday, after repeatedly cracking pivotal barrier at 1.2328 (Fibo 38.2% of 1.2800/1.2037 bear-leg, reinforced by falling 30DMA), but the action remains within a narrow range and with limited upside.

Sterling remains constructive despite weak UK economic data released earlier today, as Aug GDP was in line with expectations, but July’s figure was revised downward, while manufacturing sector performed below expectations and trade gap widened in August, adding to negative signals.

Anticipated fresh pressure on the US dollar after Fed minutes pointed to more careful approach to the monetary policy, in light of worsening global economic situation and growing uncertainty, would provide some support to pound.

Markets are awaiting release of US September CPI data (due later today) which would provide further relief to policymakers and weigh on greenback if inflation falls in line or below expectations.

Technical picture on daily chart is improving as rising 14-d momentum broke into positive territory and 10/20DMA’s turned to bullish configuration, though overbought stochastic and RSI moving sideways in neutrality zone (50) warn that bulls may face stronger headwinds.

Bullish scenario sees clear break of 1.2328 pivot as a minimum requirement to signal continuation of six-day recovery rally and expose targets at 1.2418/43 (50% retracement of 1.2800/1.2037 / 200DMA respectively).

Conversely, repeated failure at 1.2328 would increase risk of recovery stall, with extension below daily Tenkan-sen (1.2187) to signal reversal and shift near-term focus to the downside.

Res: 1.2328; 1.2386; 1.2418; 1.2443.

Sup: 1.2276; 1.2240; 1.2207; 1.2187.

Markets Advance As Focus Falls On US CPI

Asian shares advanced on Thursday following the moderately positive performance from Wall Street overnight as dovish Fed minutes and easing oil prices supported risk sentiment. However, markets remain cautious amid mounting geopolitical tensions in the Middle East and incoming US data. European markets opened higher ahead of the ECB meeting minutes while US futures are flashing green as the focus falls on the U.S. consumer inflation report later today. In the currency space, dollar weakness has been a theme this week amid growing expectations around US rates peaking. Looking at commodities, oil prices fell for a third day after industry data revealed a larger-than-expected rise in crude inventories, while gold continued its rebound as the USD and Treasury yields retreated.

Dollar steady ahead of US Inflation data

The September US Consumer Price Index (CPI) report is likely to influence expectations around whether the Fed will keep rates higher for longer.

Headline inflation is expected to cool to 0.3% month-on-month from 0.6% seen in the prior month while the core is projected to remain unchanged at 0.3%. Should September’s CPI report show evidence of cooling prices, this is likely to boost bets around the Fed pausing hikes for the rest of 2023 and weaken the dollar further. As of writing, traders are currently pricing in a 10% probability of a 25-basis point hike in November, with this rising to 30% by December, according to Fed Funds futures. A sticky inflation print may halt the decline in the dollar and see it resume its uptrend.

WTI Oil Futures’ Rebound Falters

- WTI futures fail to breach the ascending trendline

- Oil drops below 50-day SMA towards October low

- Momentum indicators tilt to the bearish side

WTI oil futures (November delivery) had been in a steady advance since July, climbing to a 13-month peak of 95.02 on September 28 before experiencing a correction. Even though oil managed to halt the retreat and recoup some losses, its recovery seems to be fading.

Should the bears attempt to push the price lower, the recent support of 81.50 could act as the first line of defense. Diving beneath that zone, the price could decline towards the August low of 77.60, which overlaps with the 200-day simple moving average (SMA). Even lower, the June resistance of 75.00 may provide downside protection.

On the flipside, if buying interest reignites, the price could re-test the ascending trendline that connects the higher lows since July ahead of the recent resistance of 87.20. Conquering this barricade, the bulls could aim for the September support of 88.20. A violation of that hurdle could open the door for the 13-month peak of 95.02.

In brief, WTI oil futures managed to pause the latest retreat but their recovery seems to be faltering. However, a fresh lower low is needed to turn the short-term picture to bearish.

Focus Turns to US September CPI

Markets

With only second tier data/news, there was no reason for markets to change course on the new corrective trends. Headline US PPI was marginally stronger than expected (0.5% M/M, 2.2% Y/Y vs 0.3% & 1.6% expected). However, with the core easing from 2.9% Y/Y to 2.8%, there was little reason for investors to consider any prepositioning going into today’s CPI. The US 10-y auction was average. The Minutes from the September 20 FOMC meeting showed a broad consensus that policy should be restrictive for some time. The majority of the governors still expected that one additional hike could be needed this year. However, as policy is now clearly in restrictive territory risks have become more two-sided, allowing the FOMC to proceed more carefully. The impact of the minutes of trading was modest. For US short-term yields, the downside is rather well protected as there is little reason for markets to row against the higher for longer mantra (2-y +1.25 bps). Yields at longer maturities simply continued their post-payrolls correction with the 30-y ceding another 13.8 bps. The 10-y US real yield also eased back to 2.24% compared to a cycle peak of 2.58% late last week. Similar story line for European/German bond markets. The 2-y German yield added 3.8 bps. The 30-y still declined 10.8 bps. Marginally rising inflation expectations at the ECB consumer survey again were largely ignored. European equities (EuroStoxx 50 -0.1%) took a breather after Tuesday’s sharp rally. US indices added up to 0.7% (Nasdaq) as market see the Fed nearing the end of its tightening cycle. Despite lower real yields and a constructive risk sentiment, the dollar correction develops in a very gradual way. The DXY USD index closed little changed at 106.82. EUR/USD closed at 1.062 from 1.0605 on Tuesday evening. Brent oil dropped from $88/b to $85.5, reversing the ‘war premium’ after the start of the war between Hamas and Israel.

Asian risk-sentiment is positive this morning, joining the positive tone on WS yesterday. Chinese markets were additionally supported as a state-owned investment fund reports to have raised its stakes in local banks. Later today, the focus turns to the US September CPI. Markets expects inflation to have eased further to 0.3% M/M and 3.6% Y/Y for the headline and 0.3% M/M and 4.1% for core. Given current market bias, a substantial upside surprise is probably needed to reverse the developing correction of lower LT yields and a softer dollar. US jobless claims, a $20bn 30-y US bond sale and the monthly US budget statement are wildcards. 4.50%/4.36% (23% retracement/previous top) remains first important support for the US 10-y yield. EUR/USD nears the 1.0635/1.0643 area. The UK monthly GDP published this morning printed as expected (0.2% M/M). Industrial activity again disappointed (-0.7% M/M). The services sector showed better resilience. Sterling eases marginally with EUR/GBP at 0.863 gaining a few ticks after modest sterling gains earlier this week.

News and View

Former Slovak PM Fico who won September 30 parliamentary elections with his SMER-party is set for a return to office after securing a deal with center-left Hlas presided by another former PM (Pelligrini) and the Slovak National Party (SNS) in what is considered a populist-nationalist coalition. Together, they have 79 out of 150 seats in parliament. Pelligrini will be speaker of parliament. Fico has an open anti-EU view on topics ranging from Russia to climate to migration, which are shared by SNS while Hlas is nationalist in the sense that it aims to strengthen the state’s role in the economy. To beef up Slovakia’s finances in 2024, PM Fico could be looking for a special levy on the financial sector modelled on the Italian one introduced by PM Meloni.

The Royal Institution of Chartered Surveyors (RICS) published its UK residential survey for September. The report depicts the continuation of a challenging market backdrop, with interest rates continuing to hamper mortgage affordability, and the disparity between tightening lettings supply and rising demand causing rental price rises. New buyer enquiries points to consistent weak demand, though less negative than in August (-39% vs -46%). The same goes for agreed sales (-37% from -46%) and sales expectations for the next three months (-24% from -36%). Going forward, near-term expectations point to a further price pull-back over the next three months, although again not quite as negative as in August (-48% from -65%). A net balance of +43% of survey participants saw an increase in tenant demand in the lettings market in September while there is a rising scarcity of listings becoming available on the rental market (-24%), squeezing rent prices higher (5% growth expected over next 12 months).

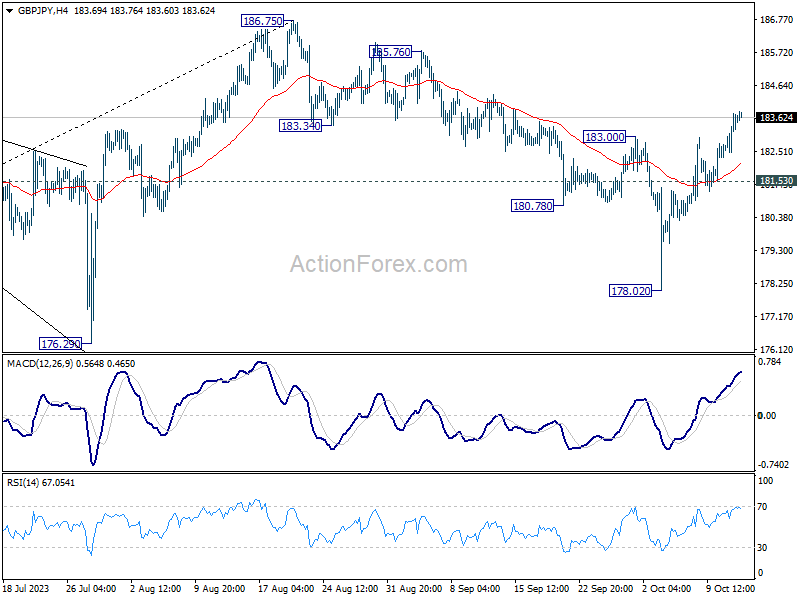

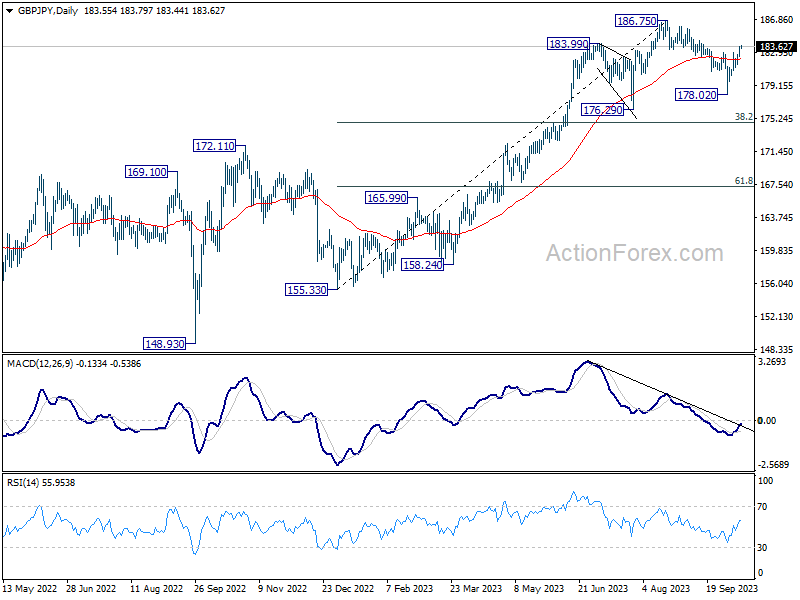

GBP/JPY Daily Outlook

Daily Pivots: (S1) 182.86 (P) 183.31; (R1) 184.12; More...

Intraday bias in GBP/JPY stays on the upside for the moment. Pull back from 186.75 should have completed 178.02 already. Stronger rally would be seen back to 185.67/186.75 resistance zone. However, below 181.53 minor support will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, fall from 186.75 is currently seen as a corrective move only. As long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and bring lengthier and deeper consolidations.

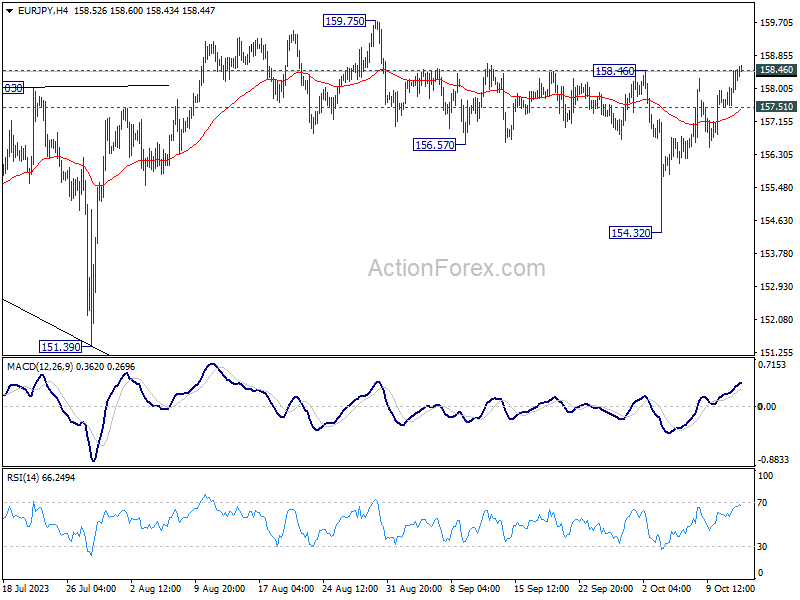

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.80; (P) 158.13; (R1) 158.75; More....

Break of 158.46 resistance indicates that corrective pull back from 159.75 has completed with three waves down to 154.32. Intraday bias is back on the upside for retesting 159.75 high . Firm break there will resume larger up trend. On the downside, below 157.51 minor support will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, price actions from 159.75 are views as a corrective pattern for now. As long as 151.39 support holds, rise from 114.42 (2020 low) is still expected to continue through 159.75 at a later stage. Nevertheless, firm break of 151.39 will confirm medium term topping, and bring lengthier and deeper correction.

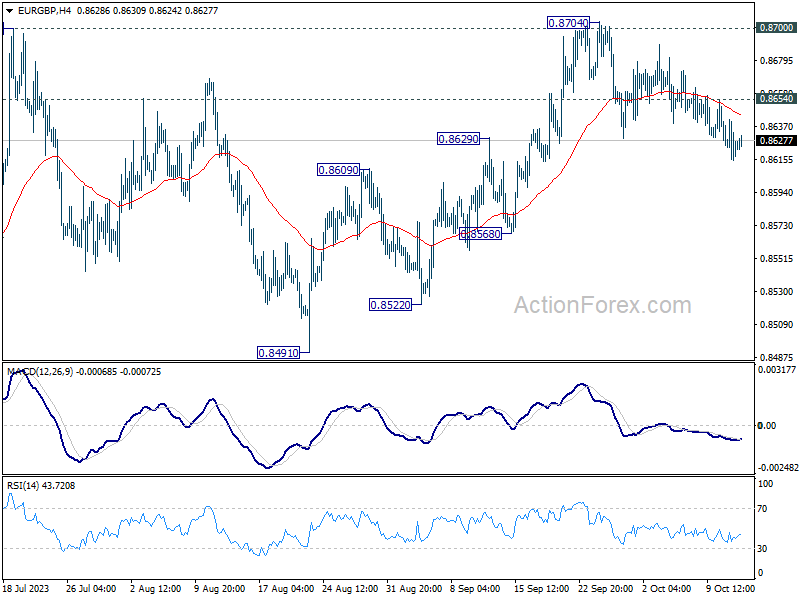

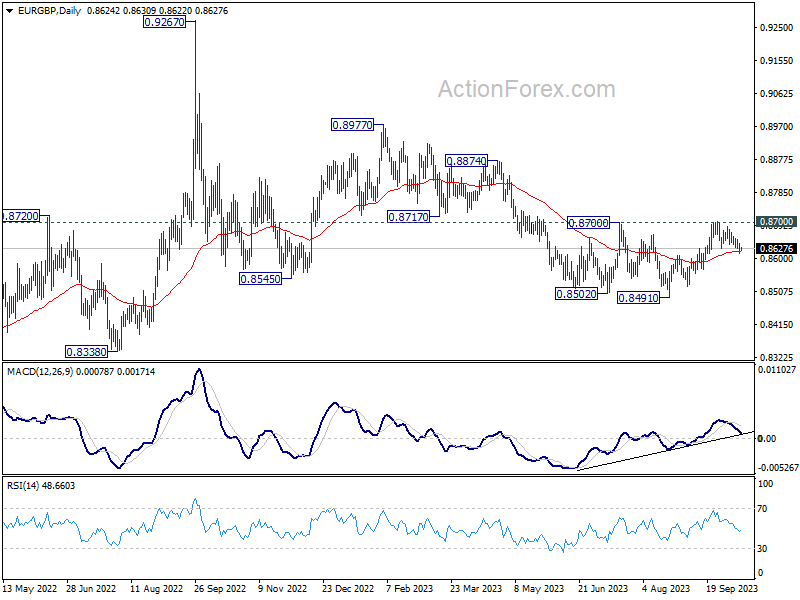

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8613; (P) 0.8628; (R1) 0.8640; More....

Downside momentum in EUR/GBP is not too convincing as seen in 4H MACD. But with 0.8654 minor resistance intact, further decline is expected, for 0.8568 support. Whole rebound form 0.8491 could have completed after rejection by 0.8700 resistance. Break of 0.8568 will bring retest of 0.8491 low. On the upside, though, above 0.8654 minor resistance will turn intraday bias neutral first.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Decisive break of 0.8700 resistance will argue that this decline has completed with three waves down to 0.8491. Rise from 0.8491 could then be another leg inside the pattern and targets 0.8977 and above. However, rejection by 0.8700 will keep the down trend alive for another fall through 0.8491 at a later stage.

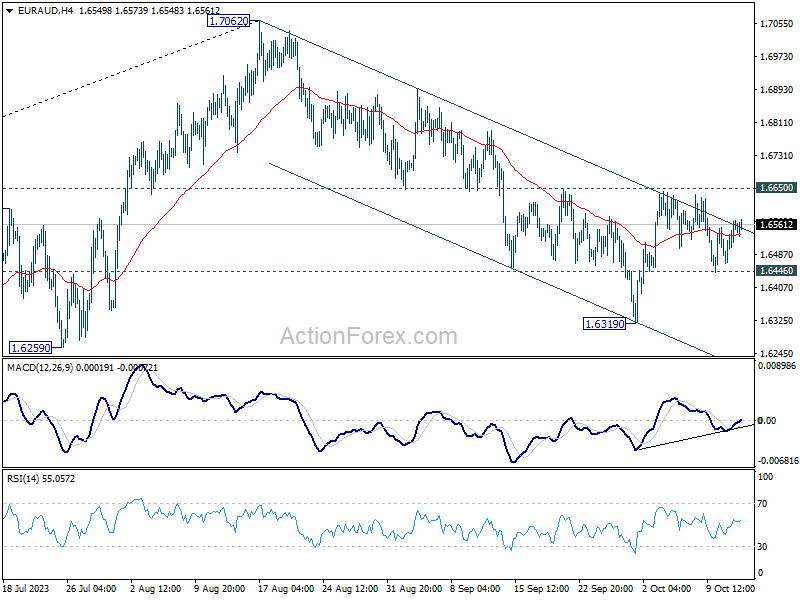

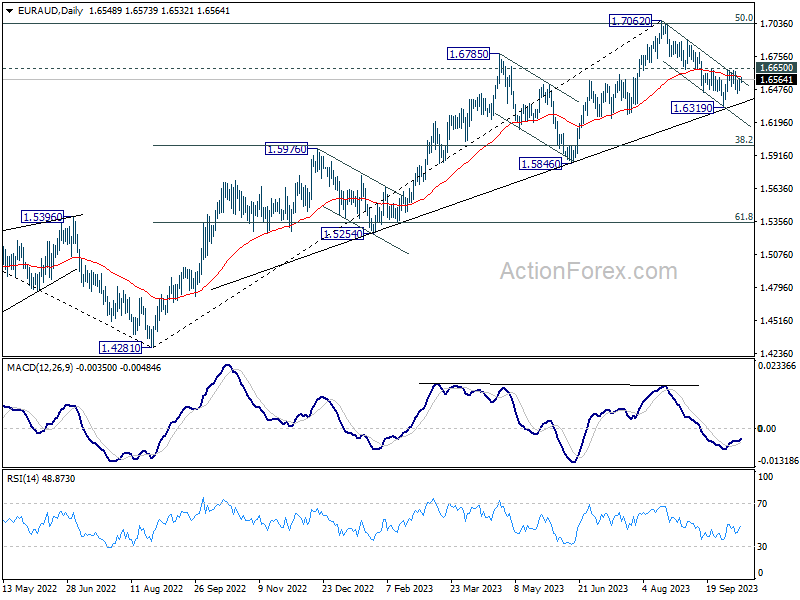

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6492; (P) 1.6533; (R1) 1.6599; More...

Intraday bias in EUR/AUD stays neutral for the moment. Sideway trading might continue further. On the downside, below 1.6446 minor support will bring retest of 1.6319. Break there will resume the decline from 1.7062 to 1.6000 fibonacci level. On the upside, firm break of 1.6650 resistance will argue that pull back from 1.7062 has completed, after drawing support from medium term rising trend line. Further rally would be seen back to retest 1.7062.

In the bigger picture, fall from 1.7062 is probably correcting whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support could be seen there to bring rebound, at least on first attempt. This will remain the favored case as long as 1.6650 resistance holds.

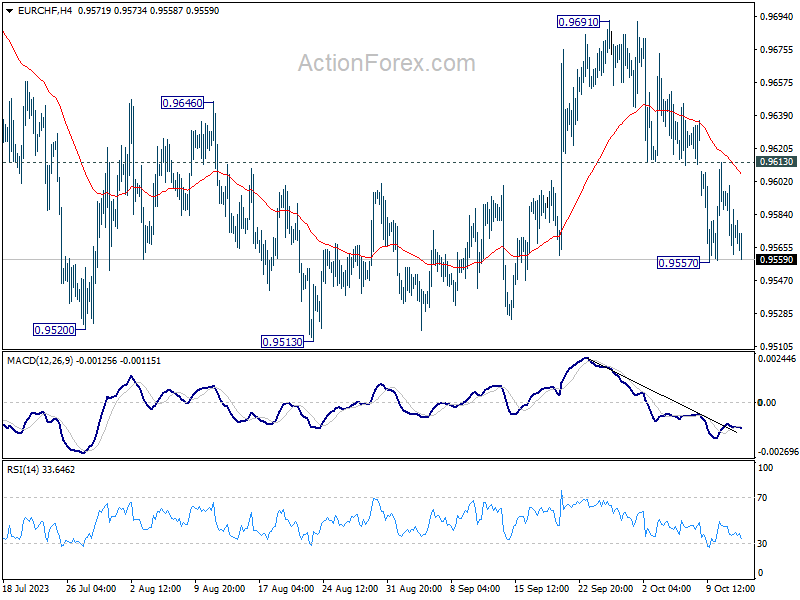

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9561; (P) 0.9581; (R1) 0.9599; More...

Intraday bias in EUR/CHF remains neutral, and deeper decline is in favor with 0.9613 resistance intact. Below 0.9557 will resume the fall from 0.9691 and bring retest of 0.9513 low. Decisive break there will resume larger down trend from 1.0095. On the upside, above 0.9613 will turn bias back to the upside for 0.9691 instead.

In the bigger picture, medium term outlook will stay bearish as long as the cross is capped well below falling 55 W EMA (now at 0.9793). That is, down trend from 1.2004 (2018 high) could still resume through 0.9407 (2022 low). However, sustained trading above the 55 W EMA will raise the chance that 0.9470 is already a long term bottom. Further rise would then be seen to 1.0095 resistance to indicate bullish trend reversal.

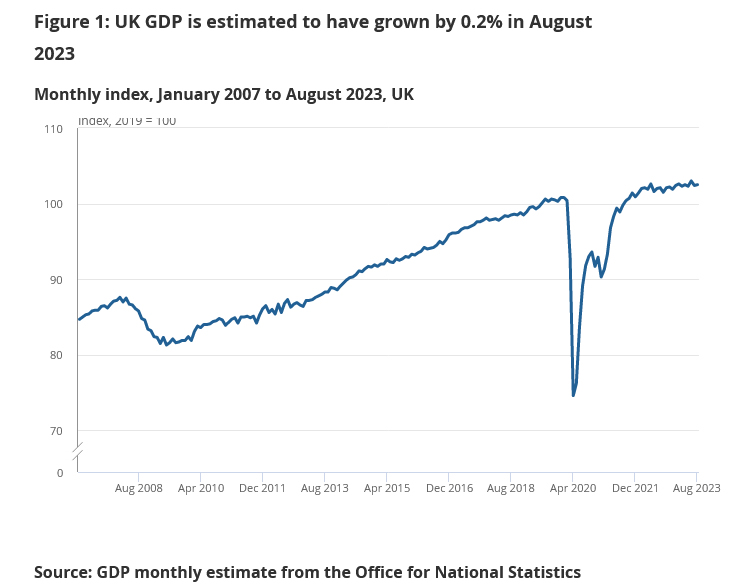

UK GDP shows modest 0.2% mom growth in Aug, services the sole contributor

UK's GDP data for August reveals a mixed bag of results, characterized by modest growth and a sector-specific performance variance. The economy grew by 0.2% mom, aligning with market expectations

Dissecting the numbers, the services sector emerges as the sole contributor to GDP growth, registering a 0.4% mom increase. Contrastingly, the production output faced a downturn, shrinking by -0.7% mom , while the construction sector similarly contracted by -0.5% mom .

In a more expansive view, the 0.3% rise in GDP over the three months leading to August paints a picture of gradual, albeit inconsistent, economic expansion.

In this three months period, production led the charge with a 1.2% increase, highlighting a resilient manufacturing and industrial segment that counters the monthly dip in August. Construction also showed promise with a 0.9% rise, indicating a level of sustained activity in infrastructure development over the quarter. Services, though only increasing by a marginal 0.1%, maintained its positive contribution.