Sample Category Title

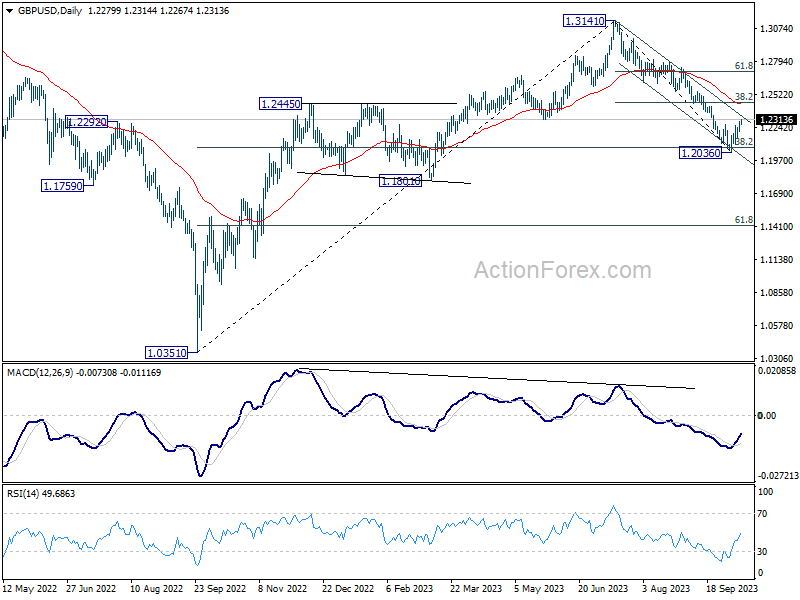

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2235; (P) 1.2263; (R1) 1.2314; More

Intraday bias in GBP/USD stays on the upside at this point. Rebound from 1.2036 short term bottom is in progress for near term channel resistance (now at 1.2338). Firm break there will target 38.2% retracement of 1.3141 to 1.2036 at 1.2458 next. Nevertheless, break of 1.2161 minor support will revive near term bearishness and bring retest of 1.2036 low.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2440) holds, in case of rebound.

Strong PPI and Falling Yields Leave Dollar Unfazed; Franc and Sterling Gain Momentum

Dollar is exhibiting mixed performance in today's relatively calm trading environment. Earlier losses were swiftly counteracted, illustrating the greenback's resilience amidst fluctuating conditions. Interestingly, the extended pullback in treasury yield has left Dollar unscathed, and it has similarly shrugged off stronger than expected PPI data. All eyes are now set on the release of the FOMC minutes, although tomorrow's CPI data release is anticipated to be the significant market mover.

On the European front, Sterling and Swiss Franc are leading the pack, demonstrating noticeable strength. Euro is lagging behind after two ECB policymakers who expressed the belief that the tightening cycle might have reached its conclusion. The commodity currencies, alongside the Yen, are on a slight decline.

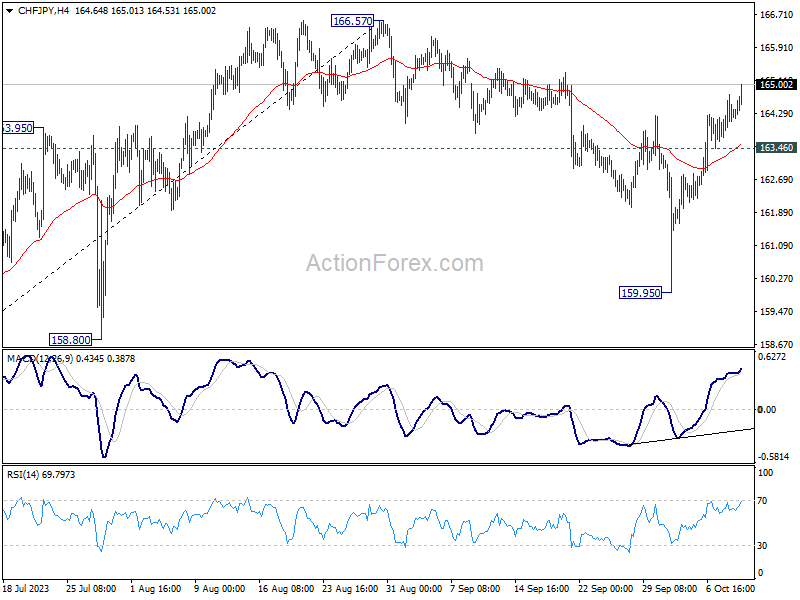

From a technical viewpoint, CHF/JPY's rally from 159.95 extends higher today. Current development suggests that corrective pull back from 166.57 has completed already. Further rise is in favor as long as 163.46 support holds, for retesting 166.57 high. At this point, it's unsure yet whether CHF/JPY is ready to break through 166.57 to resume the larger up trend. The development in other Yen and Franc pairs will be monitored to gauge the chance. However, it remains uncertain whether the cross is prepared to breach the 166.57 mark to resume its broader uptrend. To evaluate this possibility, analysts are keeping a close eye on the development in other Yen and Franc pairs.

In Europe, at the time of writing, FTSE is up 0.16%. DAX is up 0.11%. CAC is down -0.26%. Germany 10-year yield is down -0.0535. Earlier in Asia, Nikkei rose 0.60%. Hong Kong HSI rose 1.29%. China Shanghai SSE rose 0.12%. Singapore Strait Times dropped -0.19%. Japan 10-year JGB yield rose 0.0046 to 0.779.

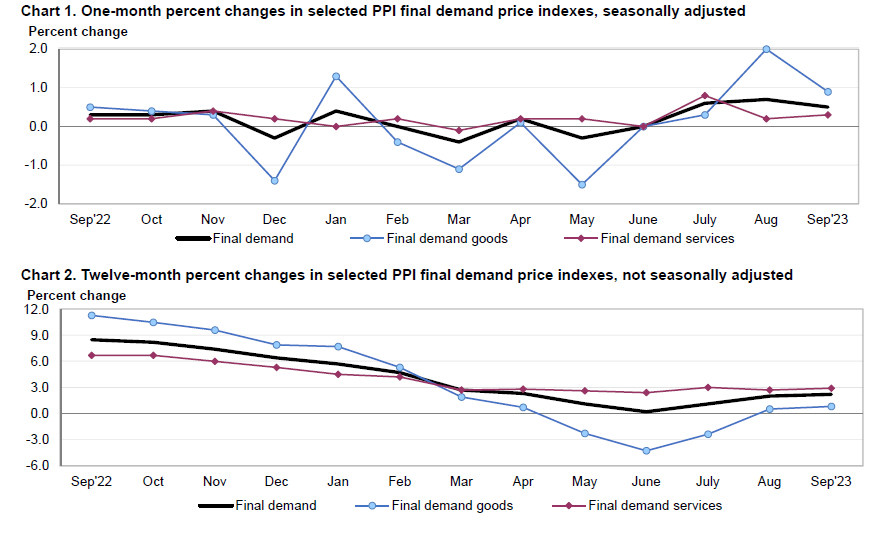

US PPI up 0.5% mom, 2.2% yoy in Sep, largest annual rise since Apr

US PPI for final demand rose 0.5% mom in September, above expectation of 0.4% mom. PPI less foods, energy, and trade services increased 0.2% mom, the fourth consecutive advance. PPI goods rose 0.9% mom while PPI services rose 0.3% mom.

For the 12 months period, PPI rose 2.2% yoy, above expectation of 1.6% yoy. That's the largest annual increase since April's 2.3% yoy. PPI less foods, energy and trade services was up 2.8% yoy.

Fed's Bowman: Policy rate may need to rise further

Fed Governor Michelle Bowman acknowledged in a speech the progress made in curbing inflation. However, she quickly pointed out "inflation remains well above the FOMC's 2 percent target."

She highlighted the robust pace of domestic spending and the prevailing tightness in the labor market. These factors indicate that "the policy rate may need to rise further and stay restrictive for some time to return inflation to the FOMC's goal."

Shifting her attention to the broader challenges faced by central banks, she elucidated, "As they have confronted price stability challenges, central banks have also faced new financial stability risks."

Specifically, she cited concerns related to the substantial fluctuations in interest rates amidst an environment characterized by sustained, heightened inflation.

Moreover, Bowman emphasized the potential risks arising from geopolitical tensions, explaining how they can instigate "greater financial market volatility." She also underscored the indirect impacts such tensions could have, including influencing economic activity and inflation.

ECB's consumer survey reveals rising inflation expectations amid subdued growth outlook

ECB's latest Consumer Expectations Survey for August paints a picture of an economy where consumers anticipate higher inflation rates but remain pessimistic about economic growth.

Specifically, the survey indicates that median inflation expectations for the next 12 months have risen from 3.4% to 3.5%. A similar uptrend was observed for the three-year horizon, with expectations inching up from 2.4% to 2.5%.

Household income expectations for the next year showed a slight increase, moving from 1.1% to 1.2%. However, a contrasting sentiment emerged for spending , with expectations slightly decreasing from 3.4% to 3.3%.

In terms of economic growth, the mood appears somewhat bearish. The survey revealed that median expectations for growth over the coming 12 months have declined, shifting from -0.7% to -0.8%.

ECB's Knot: Policy is in a good place

ECB Governing Council member Klaas Knot acknowledged the recent strides the central bank has made towards achieving its inflation target, but he emphasized that there's still "a long and winding road ahead". Nevertheless, expressing contentment with the current policy stance, he mentioned, "I do believe that policy at this moment is in a good place."

Knot did not shy away from underscoring ECB's readiness to take further action if needed, affirming, "we will remain vigilant and we stand ready to adjust interest rates even more if the disinflation process were to stall." He emphasized that ECB has a "credible prospect" of achieving its inflation target by 2025.

Highlighting challenges in the short term, Knot pointed out that the eurozone is currently grappling with economic stagnation. While the manufacturing sector is already in a recession, the services sector is also beginning to feel the pressure.

Nevertheless, Knot views this slowdown as "desirable in a way." Despite the immediate hurdles, Knot remains optimistic about the medium-term outlook, suggesting that growth is poised for a rebound in the foreseeable future.

ECB's De Cos: Market confidence reflects in rate expectations

ECB Governing Council member Pablo Hernandez de Cos noted that market pricing indicated a clear understanding of the central bank's communication, finding its intended policy path to be credible.

"They are interpreting well that there might be a need for the current rate to remain in the current (setting) for sufficiently long," he mentioned"

"They are also expecting that rates will decline, which for me is a kind of a confidence of the market that we will fulfil our mandate," he added.

However, De Cos voiced concerns about unforeseen challenges that might arise, emphasizing the high level of uncertainty surrounding economic prospects. New shocks could dictate different policy decisions by the ECB.

Offering insight into the economy, de Cos observed a potential dip in the near-term, hinting at a possible negative outcome for the third quarter. Despite this near-term pessimism, he expressed a lack of alarm, reassuring that a recovery is on the horizon for next year, driven by rejuvenating real incomes.

RBA's Kent: Some further tightening may be required

In a speech, RBA Assistant Governor, Chris Kent, indicated that while the effects of previous monetary tightening have not yet been fully realized, "some further tightening " might be on the horizon to keep inflation in check.

Kent asserted that the policies currently in place are beginning to stymie demand growth, a crucial step towards mitigating inflation.

"The lags of transmission mean that some further effects of rate increases to date are still to be felt through the economy, which will provide further impetus to lower inflation in the period ahead," he added.

However, with inflation persisting at elevated levels, Kent hinted at the necessity for additional measures. "The Board is paying close attention to economic developments here and overseas, and some further tightening of monetary policy may be required to ensure that inflation, which is still too high, returns to target in a reasonable timeframe."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2235; (P) 1.2263; (R1) 1.2314; More

Intraday bias in GBP/USD stays on the upside at this point. Rebound from 1.2036 short term bottom is in progress for near term channel resistance (now at 1.2338). Firm break there will target 38.2% retracement of 1.3141 to 1.2036 at 1.2458 next. Nevertheless, break of 1.2161 minor support will revive near term bearishness and bring retest of 1.2036 low.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2440) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | Germany CPI M/M Sep F | 0.30% | 0.30% | 0.30% | |

| 06:00 | EUR | Germany CPI Y/Y Sep F | 4.50% | 4.50% | 4.50% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Sep F | -11.20% | -17.60% | ||

| 12:30 | CAD | Building Permits M/M Aug | 3.40% | 0.50% | -1.50% | -3.80% |

| 12:30 | USD | PPI M/M Sep | 0.50% | 0.40% | 0.70% | |

| 12:30 | USD | PPI Y/Y Sep | 2.20% | 1.60% | 1.60% | 2.00% |

| 12:30 | USD | PPI Core M/M Sep | 0.30% | 0.20% | 0.20% | |

| 12:30 | USD | PPI Core Y/Y Sep | 2.70% | 2.30% | 2.20% | |

| 18:00 | USD | FOMC Minutes |

US PPI up 0.5% mom, 2.2% yoy in Sep, largest annual rise since Apr

US PPI for final demand rose 0.5% mom in September, above expectation of 0.4% mom. PPI less foods, energy, and trade services increased 0.2% mom, the fourth consecutive advance. PPI goods rose 0.9% mom while PPI services rose 0.3% mom.

For the 12 months period, PPI rose 2.2% yoy, above expectation of 1.6% yoy. That's the largest annual increase since April's 2.3% yoy. PPI less foods, energy and trade services was up 2.8% yoy.

ECB’s De Cos: Market confidence reflects in rate expectations

ECB Governing Council member Pablo Hernandez de Cos noted that market pricing indicated a clear understanding of the central bank's communication, finding its intended policy path to be credible.

"They are interpreting well that there might be a need for the current rate to remain in the current (setting) for sufficiently long," he mentioned"

"They are also expecting that rates will decline, which for me is a kind of a confidence of the market that we will fulfil our mandate," he added.

However, De Cos voiced concerns about unforeseen challenges that might arise, emphasizing the high level of uncertainty surrounding economic prospects. New shocks could dictate different policy decisions by the ECB.

Offering insight into the economy, de Cos observed a potential dip in the near-term, hinting at a possible negative outcome for the third quarter. Despite this near-term pessimism, he expressed a lack of alarm, reassuring that a recovery is on the horizon for next year, driven by rejuvenating real incomes.

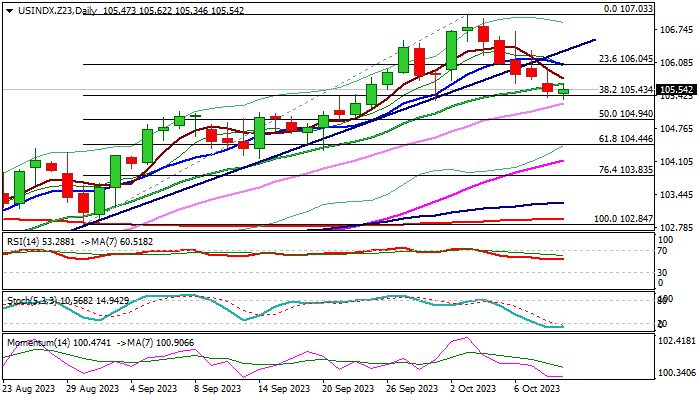

USD Index outlook: Bears Pause and Look for Fresh Signals from FOMC Minutes/Inflation Report

The dollar index remains at the back foot after a continuous five-day fall, but the range narrows on Wednesday, as traders await release the minutes of FOMC last policy meeting to get more clues on the central bank’s rate outlook for coming months.

Pullback from 107.03 (2023 high) also faces headwinds from important Fibo support at 105.43 (38.2% retracement of 102.84/107.03 upleg) which keeps the downside limited for the second straight day.

Oversold conditions on daily chart contribute to likely scenario of consolidation preceding fresh push lower, as the dollar’s sentiment was soured by the recent dovish shift in Fed policymakers’ comments, which suggest that the Fed may not need to tighten monetary policy much further than initially estimated.

Markets will focus on FOMC stance and US September inflation (due on Thursday) to get more information whether the policymakers are on track for another 25 basis points hike (November) or the central bank is done with tightening.

The dollar is likely to come under further pressure if Fed keeps dovish narrative, with sustained break of 105.43 pivot to spark fresh acceleration below 105.00 handle (near 50% retracement of 102.84/107.03) and unmask targets at 104.44/17 (Fibo 61.8% / Sep 14 trough).

Conversely, bounce above 106.00 barrier to strengthen near-term structure, however, return and close above broken trendline support (106.23) needed to confirm an end of corrective phase and bring larger bulls back to play.

Res: 105.65; 106.04; 106.23; 106.69.

Sup: 105.34; 104.94; 104.44; 104.17.

S&P500 (SPX) Found Buyers At The Equal Legs Area

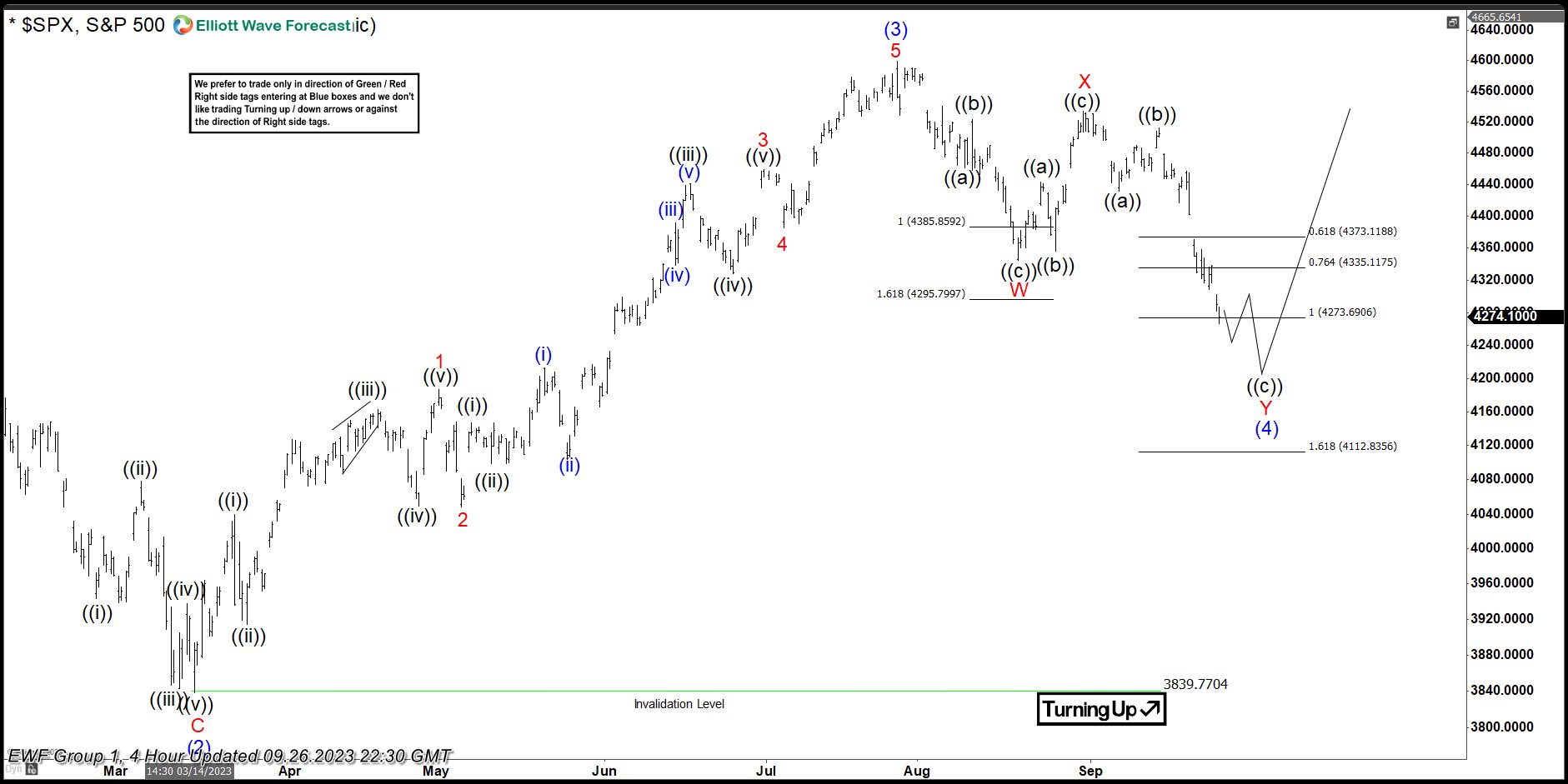

Hello fellow traders. In this technical article we’re going to take a quick look at the Elliott Wave charts of SPX published in membership area of the website. As our members know, S&P500 is trading within the cycle from the October’s 3492.7 low, which is unfolding as 5 waves structure. Recently we got 3 waves pull back which found buyers right at equal legs area as we expected. In the further text we are going to explain the Elliott Wave Forecast

SPX 4h Elliott Wave Analysis 09.21.2023

SPX is doing wave (4) blue pull back. The index is correcting the cycle from the 3839.7 low. Pull back looks incomplete at the moment. We expect another leg down toward 4274.7-4114.5 area to complete the correction.

SPX 4h Elliott Wave Analysis 09.26.2023

SPX made extension down and reached the extreme zone- equal legs area as expected. We see possibility of SPX making shallow bounce and another leg down within buyers zone, which will allow rest of the Indices to reach their extremes. At the marked zone SPX should ideally find buyers for further rally in wave (5) blue or for a 3 waves bounce at least.

SPX 4h Elliott Wave Analysis 10.10.2023

Buyers appeared at the marked extreme zone 4274.7-4114.5 and we are getting good reaction from there. As far as 4214.67 low holds, SPX should ideally keep trading higher in wave (5) red toward new highs. We need to see break of 07/27 peak to confirm next leg up is in progress.

GBP/USD Drifting ahead of UK GDP

- UK growth expected to rebound in August

- Fed members more dovish due to increase in US yields

The British pound is calm on Wednesday. In the European session, GBP/USD is trading at 1.2297, up 0.10%.

The UK economy has been struggling and GDP declined by 0.5% m/m in July. The markets are expecting a rebound on Wednesday, with GDP projected to rise by 0.2% m/m in August. For the three months to August, GDP is expected to increase by 0.3%, up from 0.2% in the previous release.

The IMF report on Tuesday didn’t bring much cheer, with the report stating that the Bank of England would need to maintain elevated interest rates into 2024 due to weak growth and sticky inflation. The same day, the BoE’s Financial Policy Committee also said that rates would have to “stay high for a long time”, warning that would put pressure on households.

The Federal Reserve has kept to a hawkish script, trying to convince the markets that the tightening cycle may not be over. That message has changed in recent days, as the Fed has become more dovish. The reason? US Treasury yields have been rising sharply, with 10-year yields hitting a 16-year high on Tuesday. The spike in yields has made borrowing costs more expensive and could act as a brake on the economy and push inflation lower without Fed intervention.

Atlanta Fed President Raphael Bostic said on Tuesday that the Fed didn’t need to raise rates anymore in order to push inflation back to the Fed’s 2% target. Bostic is considered a dove, but he has support for this position. Dallas Fed President Lorie Logan and San Francisco Fed President Mary Daly both stated that the increase in Treasury yields could mean less need for the Fed to raise rates in the current tightening cycle.

GBP/USD Technical

- 1.2179 and 1.2097 are providing support

- 1.2321 is a weak resistance line. Above, there is resistance at 1.2403

ECB’s Knot: Policy is in a good place

ECB Governing Council member Klaas Knot acknowledged the recent strides the central bank has made towards achieving its inflation target, but he emphasized that there's still "a long and winding road ahead". Nevertheless, expressing contentment with the current policy stance, he mentioned, "I do believe that policy at this moment is in a good place."

Knot did not shy away from underscoring ECB's readiness to take further action if needed, affirming, "we will remain vigilant and we stand ready to adjust interest rates even more if the disinflation process were to stall." He emphasized that ECB has a "credible prospect" of achieving its inflation target by 2025.

Highlighting challenges in the short term, Knot pointed out that the eurozone is currently grappling with economic stagnation. While the manufacturing sector is already in a recession, the services sector is also beginning to feel the pressure.

Nevertheless, Knot views this slowdown as "desirable in a way." Despite the immediate hurdles, Knot remains optimistic about the medium-term outlook, suggesting that growth is poised for a rebound in the foreseeable future.

Euro Calm as German Inflation Falls, FOMC Eyed

- German inflation declines

- Fed to release minutes of September meeting

The euro continues to have an uneventful week. In the European session, EUR/USD is trading at 1.0613, up 0.08%.

German inflation falls to 4.5%

German inflation was confirmed at 4.5% y/y in September, sharply lower than the August reading of 6.1%. It was the lowest level since the Ukraine war started in February 2022. Energy prices fell sharply and food prices were also lower. The core rate eased to 4.6%, a one-year low and down from 5.5% in August. The inflation report is another sign that the ECB’s rate hikes are working and pushing inflation lower. Still, there is a long way to go, as inflation in Germany and the eurozone remains well above the ECB’s 2% target.

Germany’s economy has slowed down considerably. GDP was flat in the second quarter and the economy may have contracted in Q3. The German economy, once the pride of Europe, has been battered by high interest rates, weak consumer consumption and falling exports.

In the US, the data calendar has been very light, allowing the markets to focus on Fedspeak. A host of Fed members had a similar message in noting that the spike in US yields could act as a brake on the economy due to higher borrowing costs. This could push inflation lower without the Fed having to raise interest rates.

The Fed clearly is not going to announce that rates have peaked since another rate hike would lead to some loss in credibility. Fed Chair Powell and his colleagues seem to striving for transparency, and any divisions at the Fed over policy are a result of the uncertainty in the economic outlook. Market pricing indicates that the Fed is unlikely to raise rates this year – according to the CME Fedwatch Tool, the odds of a rate hike stand at 25%. Investors will be hoping for some insights from the FOMC minutes of the September meeting, in which the Fed held rates at a target range of 5.25%-5.50%.

EUR/USD Technical

- There is support at 1.0545 and 1.0489

- 1.0641 and 1.0697 are the next resistance lines

ECB’s consumer survey reveals rising inflation expectations amid subdued growth outlook

ECB's latest Consumer Expectations Survey for August paints a picture of an economy where consumers anticipate higher inflation rates but remain pessimistic about economic growth.

Specifically, the survey indicates that median inflation expectations for the next 12 months have risen from 3.4% to 3.5%. A similar uptrend was observed for the three-year horizon, with expectations inching up from 2.4% to 2.5%.

Household income expectations for the next year showed a slight increase, moving from 1.1% to 1.2%. However, a contrasting sentiment emerged for spending , with expectations slightly decreasing from 3.4% to 3.3%.

In terms of economic growth, the mood appears somewhat bearish. The survey revealed that median expectations for growth over the coming 12 months have declined, shifting from -0.7% to -0.8%.