Sample Category Title

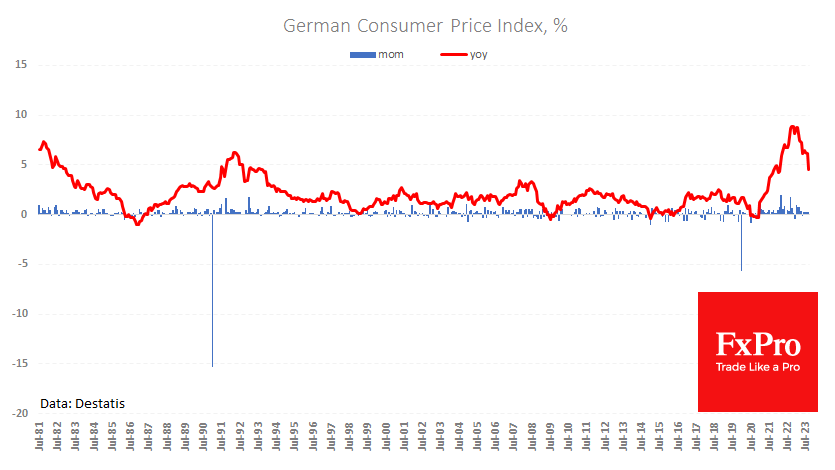

German CPI Below Forecasts, EURUSD Fights for 1.05

German consumer inflation slowed more than expected in September, according to Destatis’ preliminary estimate.

The price growth rate slowed to 4.5% y/y from 6.1% y/y vs. 4.6% y/y expected. However, the monthly rate growth remains elevated, with the last four months adding 0.3% each, bringing the annual rate to 3.6%.

Separately today, Spanish inflation accelerated to 3.5% from 2.6% the previous month and a low of 1.9% in June.

In general, the release of weaker-than-expected inflation and activity data adds to the pressure on the local currency, arguing for easing monetary policy.

Tomorrow’s composite data for the entire Euro-Zone is expected to reach 4.5% y/y, slowing from 5.2% in August.

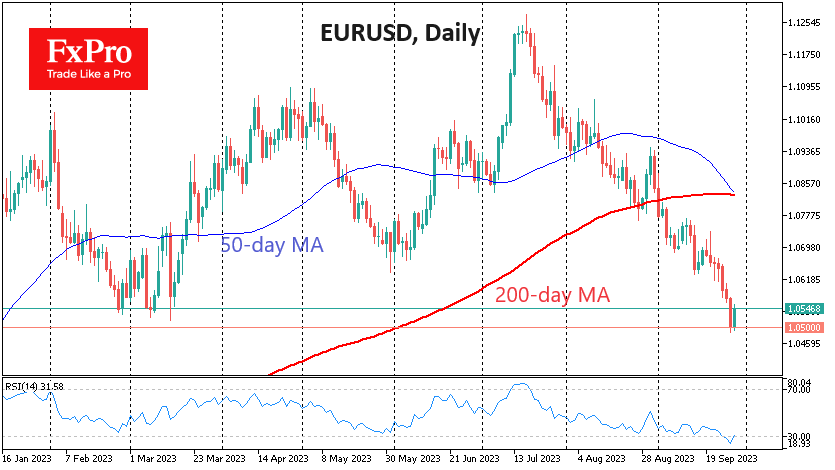

On Thursday, the EURUSD had a chance to hold above the 1.05 level thanks to the US currency’s weakness against its major rivals. So far, the move looks more like profit-taking on an eleventh consecutive week of gains for the Dollar. However, without any significant change in the fundamentals (inflation trends and the Fed’s rhetoric), this could temporarily consolidate forces and liquidity before the dollar gains further momentum, threatening to push the euro below parity.

The latter will be particularly true if yields on Italian and other eurozone debt continue to rise because of the failure to control public spending and revive the economy.

Sunset Market Commentary

Markets

It’s difficult to interpret today’s developments. Up until last week, markets would have rallied on slightly lower German (0.2% M/M & 4.3% Y/Y vs 0.3% & 4.5% expected) and Belgian (see below) inflation figures. In the same way, they would have concluded from an (outdated) revision to US Q2 GDP (consumption 0.8% Q/Qa instead of 1.7%) that central banks are done and will soon leave peak levels behind. Today’s releases didn’t have that impact. They were balanced by accelerating Spanish inflation (0.6% M/M from 0.5% M/M) and extremely low US weekly jobless claims (204k from 202k). On top, oil prices rallied from $92/b on Wednesday to $97.5/b this morning ($96/b currently). The fact that core bonds continue to sell-off in such an environment is very telling about underlying market sentiment with higher real rates and rising risk premia in the driver’s seat. The strength of today’s sell-off makes us nevertheless question whether we’re witnessing a short term technical exhaustion move or not. Daily changes on the German yield curve today vary between +5 bps (2-yr) and +10 bps (10-yr). The German 10-yr yield obviously reaches a new cycle peak above 2.9%. The EU 10y swap rate took out the 2022 top at 3.41%, taking a shot at the psychologic 3.5% mark. The Belgian 10y yield broke that mark for the first time since early 2012 (3.6% currently). The Italian 10-yr yield spread over Germany touches 200 bps for the first time since early this year with deteriorating public finances (2023 & 2024 deficits revised to 5.3% of GDP and 4.3% respectively) adding to the real yield rally. Daily changes on the US yield curve range between -3.2 bps (2-yr) and +5.7 bps (30-yr). Chicago Fed Goolsbee warned that tying monetary policy too closely to labor and GDP risk triggering an overshoot in policy rates. He believes that it is well possible to curb inflation without having a deep recession. Today’s bond sell-off doesn’t translate into hemorrhage at bourses, though their performance remains unconvincing (Europe flat; WS small opening losses). EUR/USD for a second straight session tried to move south of 1.05, but the YTD low at 1.0484 remains intact for now.

News & Views

Belgian statistical agency (Statbel) reported that the Belgian consumer price index declined by 0.69% M/M in September, reducing the Y/Y measure for headline inflation to 2.39% from 4.09% in August. The Y/Y figure marked the lowest level since July 2021. Core inflation, which does not take into account price evolutions of energy products and unprocessed food, stood at 6.95% in September, compared to 7.70% in August and 7.88% in July. Inflation for services more or less stabilized at 7.18% from 7.25%. Inflation for rents eased from 6.14% to 5.33%.The main monthly price increases in September concerned alcoholic beverages, motor fuels as well as travels abroad and city trips. However, plane tickets, confectionery, bread and cereals, hotel rooms, natural gas, vegetables, meat, non-alcoholic beverages, fruit and dairy products have had a decreasing effect on the index. The data published are according to the domestic methodology. Statbel indicated that a first estimate according to the European harmonized index (HICP) for Belgium amounts to 0.7% in September

Joined economic forecasts of five major economic institutions suggest that Germany’s GDP will contract by 0.6% this year, a strong downward revision from an expected growth of 0.3% seen in the spring forecast. According to Oliver Holtemöller of IWH, the most important reason for the revision is that industry and private consumption are recovering more slowly than expected. Recent indicators suggest that production fell again noticeably in the third quarter of 2023. However, the institutes’ forecast of 1.3% for 2024 is only 0.2 percentage points below their spring forecast. The institutes argue that wage increases have followed the price hikes, energy prices have fallen and that exporters have partially passed on their higher costs, so that purchasing power is returning. Therefore, the downturn is expected to subside by the end of the year. In the following years the institutes expect a decreasing growth potential due to a shrinking the labour force becoming more apparent. The number of unemployed people is expected to increase moderately to 2.6 mln in 2023 (was 2.42 mln in 2022), but the number might already again decrease in 2024. With respect to inflation the forecast sees inflation declining from 6.1% this year to 2.6% in 2024%. Core inflation is forecasted at 6.1% and 3.1% respectively.

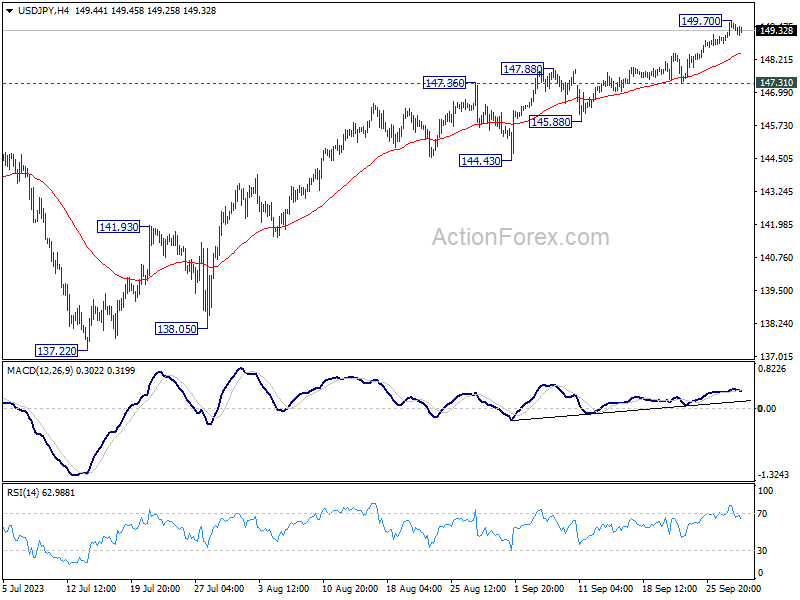

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.10; (P) 149.41; (R1) 149.95; More...

Intraday bias in USD/JPY is turned neutral with current retreat. Some consolidations could be seen but further rally is expected as long as 145.88 support holds. Above 149.70 will resume larger rise from 127.20 to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

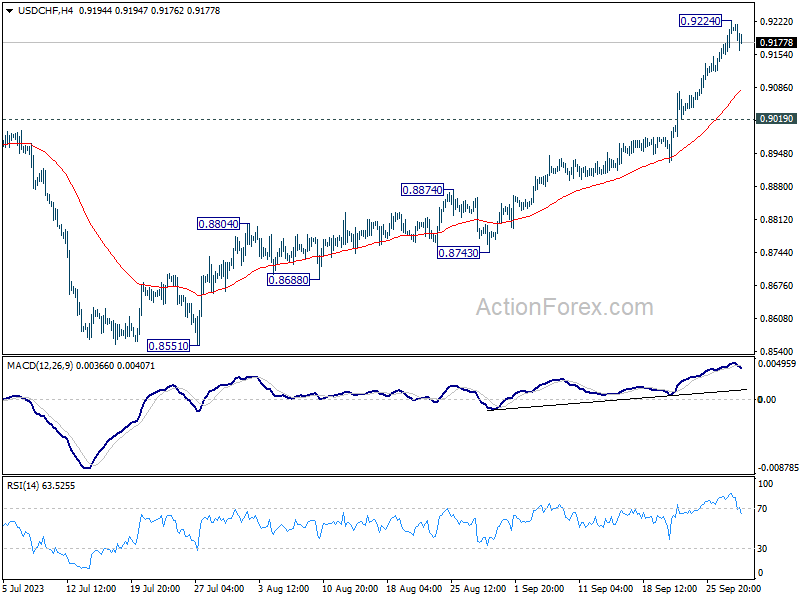

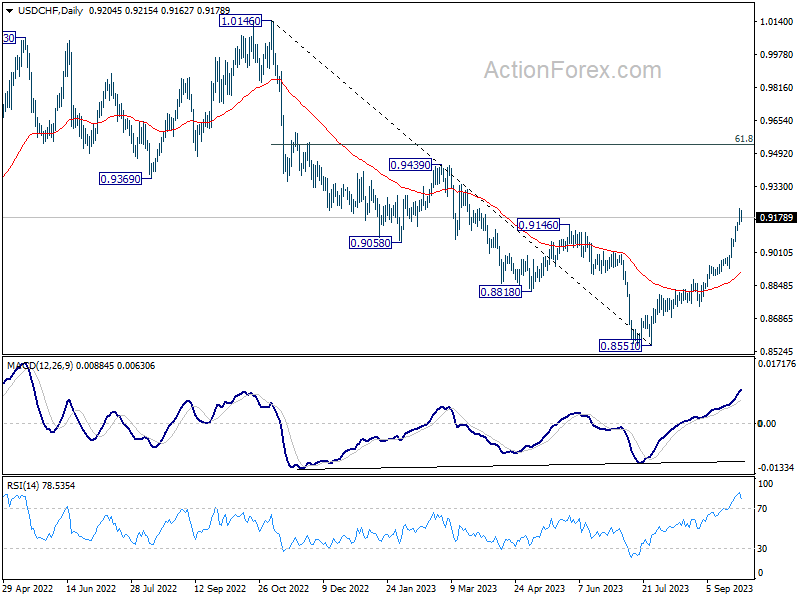

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9162; (P) 0.9193; (R1) 0.9245; More....

A temporary top is formed at 0.9224 in USD/CHF and intraday bias is turned neutral first. Some consolidations would be seen and deeper retreat cannot be ruled out. But risk will stay on the upside as long as 0.9019 support holds. Break of 0.9224 will resume the rally from 0.8551 to 0.9439 resistance next.

In the bigger picture, current development indicates that rise from 0.8551 is reversing whole down trend from 1.0146. Further rally would then be seen to 61.8% retracement at 0.9537 and above. For now, this will be the favored case as long as 55 D EMA (now at 0.8917) holds, even in case of deep pullback.

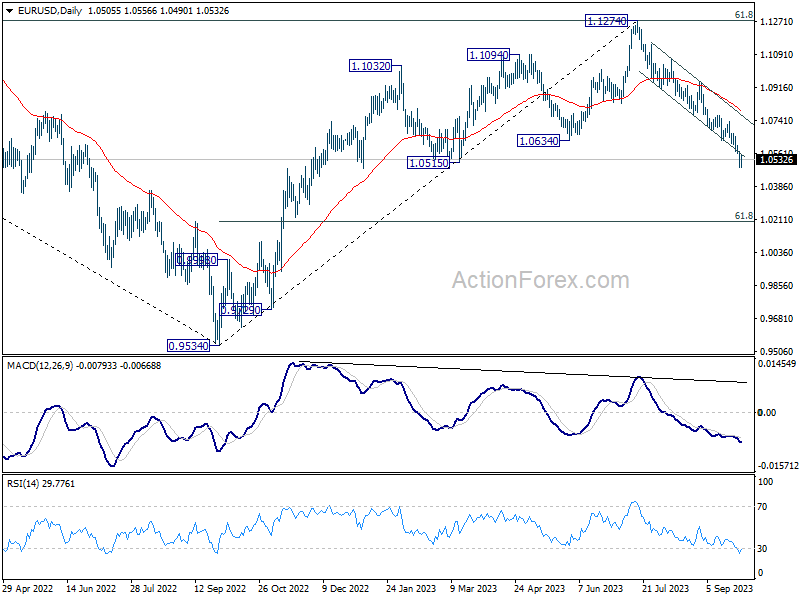

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0468; (P) 1.0523; (R1) 1.0558; More...

A temporary low is formed at 1.0487 in EUR/USD and intraday bias is turned neutral first. Some consolidations would be seen and stronger recovery cannot be ruled out. But risk will stay on the downside as long as 1.0764 support turned resistance holds. Break of 1.0487 will resume the fall from 1.1274 to 1.0199 fibonacci level.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, firm break of 1.0515 support will target 61.8% retracement of 0.9534 to 1.1274 at 1.0199. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0786) holds, in case of rebound.

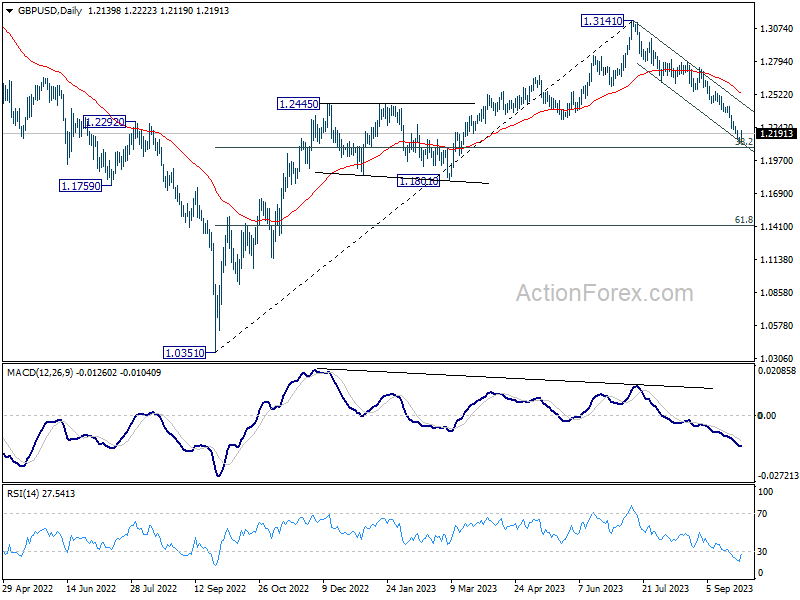

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2108; (P) 1.2138; (R1) 1.2164; More...

A temporary low should be in place at 1.2109 in GBP/USD and intraday bias is turned neutral first. Some consolidations could be seen, and stronger recovery cannot be ruled out. But near term risk will stay on the downside as long as 1.2618 support turned resistance holds. On the downside, decisive break of 1.2075 fibonacci level would carry larger bearish implication and target 1.1801 support next.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2526) holds, in case of rebound.

Dollar Turning Into Consolidation, US Yields Outshone by Europeans

Dollar is experiencing a broad retreat today, reflecting a phase of consolidation after its notable advancements in the recent days. Market participants are seemingly recalibrating their positions, with the closure of the month in sight and in anticipation of pivotal economic data slated for release next week.

While the rise in US 10-year yield continues to extend its robust performance, it finds itself overshadowed by surges in Germany and UK yields. Further consolidation in Dollar might be observed before the week concludes, although this trend remains highly sensitive to ongoing risk developments globally.

For now, Australian Dollar and Sterling emerge as frontrunners for today, with New Zealand Dollar tailing closely. In contrast, Canadian Dollar is bearing the brunt of the pullback, only outdone by US Dollar itself. Yen is also on the weaker side, while Euro and Swiss Franc are delivering mixed performance.

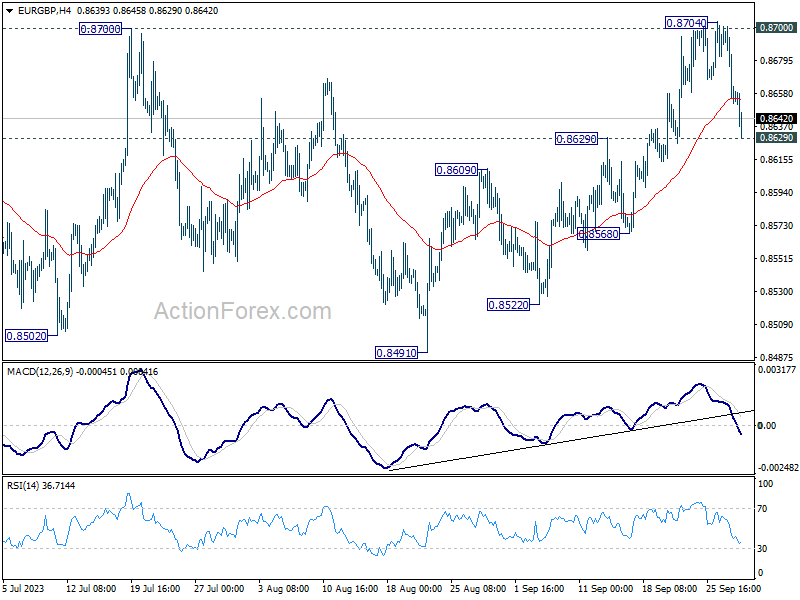

Technically, EUR/GBP is now eyeing 0.8629 resistance turned support. Firm break there should bring deeper decline back to 0.8568. More importantly, confirmed rejection by 0.8700 resistance will retain medium term bearishness in the cross. That would open the way for deeper fall through 0.8491 low to resume larger down trend from 0.9267 (2022 high).

In Europe, at the time of writing, FTSE is down -0.31%. DAX is up 0.10%. CAC is up 0.28%. Germany 10-year yield is up 0.0953 at 2.939. Earlier in Asia, Nikkei dropped -1.54%. Hong Kong HSI dropped -1.36%. China Shanghai SSE rose 0.10%. Singapore Strait Times rose 0.22%. Japan 10-year JGB yield rose 0.0212 to 0.761.

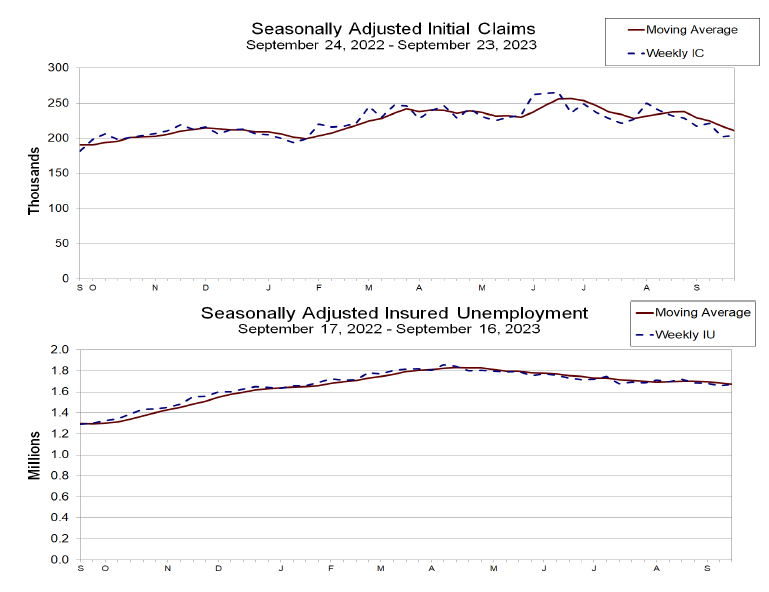

US initial jobless claims rose to 204k, vs exp. 200k

US initial jobless claims rose 2k to 204k in the week ending September 23, above expectation of 200k. Four-week moving average of continuing claims dropped -6k to 211k.

Continuing claims rose 12k to 1670k in the week ending September 16. Four-week moving average of continuing claims dropped -12k to 1674k.

Eurozone economic sentiment fell to 93.3, EU down to 92.8

Eurozone Economic Sentiment Indicator dropped slightly from 93.6 to 93.3 in September, down for the fifth month. Employment Expectation indicator rose from 102.2 to 102.7. Economic Uncertainty Indicator rose from 19.8 to 21.5.

Eurozone industry confidence rose from -9.9 to -9.0. Services confidence dropped from 4.3 to 4.0. Consumer confidence fell from -16.0 to -17.8. Retail trade confidence dropped from -5.1 to -5.7. Construction confidence fell from -5.4 to -6.2.

EU Economic Sentiment Indicator rose from 93.2 to 92.8. Amongst the largest EU economies, the ESI deteriorated in Spain (-3.2) and Italy (-2.2), while it improved in France (+2.7). Sentiment in Germany (+0.3), the Netherlands (+0.3) and Poland (-0.1) remained virtually stable.

German institutes forecast -0.6% GDP contraction this year, but downturn to subside by year-end

In the Joint Economic Forecast by five leading economic institutes, Germany is bracing for an economic contraction of -0.6% in 2023, a significant downward adjustment by 0.9% from the spring 2023 prediction. Nevertheless, the silver lining comes in the form of anticipated rebounds in the following years: Growth of 1.3% in 2024 and 1.5% in 2025. Notably, the 2024 figure represents a mere 0.2% adjustment from their spring forecast.

On the inflation front, CPI is expected to moderate from 2022's staggering 6.9% to a still elevated 6.1% in 2023, before cooling off substantially to 2.6% in 2024 and 1.9% in 2025. Labor market is anticipated to feel a slight pinch with unemployment ticking up from 5.3% in 2022 to 5.6% in both 2023 and 2024, before retracting to 5.3% in 2025.

The report highlights, "Business sentiment has recently deteriorated again, not least because of heightened political uncertainty." The third quarter of 2023 experienced a noticeable fall in production, attributed to the waning business sentiment.

Despite the bleak outlook, there are silver linings. The tailwind of wage increases following the price hike, declining energy prices, and exporters partially offsetting their higher costs offers a semblance of balance, and as a result, purchasing power is making a comeback.

"Therefore, the downturn is expected to subside by the end of the year, and the degree of capacity utilisation will rise again going forward," adds the report.

This biannual Joint Economic Forecast is commissioned by German Federal Ministry for Economic Affairs and Climate Action. Contributors to this report comprise of eminent institutes including DIW Berlin, ifo Institute, IfW Kiel, IWH, and RWI.

Mixed signals in New Zealand business confidence, ANZ anticipates another RBNZ hike

September has seen a noteworthy rebound in New Zealand's ANZ Business Confidence, rising from -3.7 to 1.5. However, a closer examination of the details offers a more nuanced picture.

Metrics such as own activity output experienced a slight decline, dropping from 11.2 to 10.9. More alarmingly, export intentions plummeted from a positive 7.5 to a -0.4. There were also declines in investment intentions (from -1.3 to -4.1) and employment intentions (from 4.6 to 1.2).

On the inflation front, cost expectations edged upwards from 75.3 to 78.6, while profit expectations showed an improvement, moving from -17.6 to -13.2. Pricing intentions rose from 44.0 to 47.1, but inflation expectations took a downward turn, shifting from 5.06 to 4.95.

ANZ provided their insights on this mixed bag of indicators, stating, "The New Zealand economy is certainly patchy, and the rebound in activity indicators – that's been evident since the start of the year – may be running out of steam."

They further highlighted the complexities in the inflation scenario: "Inflation pressures are gradually waning in the big picture, but not rapidly nor in a straight line, and the jury remains out on whether it's occurring fast enough to bring core inflation pressures down in a timely fashion."

Looking ahead, ANZ anticipates further action from RBNZ to ensure inflation is reined in effectively, with a 25 bps hike expected in November.

Australian retail sales see modest 0.2% mom rise amid cost-of-living pressures

The latest retail statistics out of Australia show a muted picture of consumer spending, with retail sales turnover in August rising only 0.2% mom (in seasonally adjusted terms) to AUD 35.4B, falling short of the anticipated 0.3% increase. Through the year, sales turnover was up 1.5% yoy.

According to Ben Dorber, the head of retail statistics at the Australian Bureau of Statistics (ABS), this modest rise indicates a notable restraint in consumer spending. Dorber noted, "The modest rise in August shows consumers continued to restrain their retail spending."

The trend growth in retail sales paints an even starker image. "In trend terms, retail turnover rose 0.1 per cent, and was up only 1.3 per cent compared to August 2022 - the smallest trend growth over 12 months in the history of the series," Dorber added.

Dorber highlighted, "Considering how high inflation and strong population growth have added to retail turnover in the past year, the historically low trend growth highlights just how much consumers have pulled back in response to cost-of-living pressures."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2108; (P) 1.2138; (R1) 1.2164; More...

A temporary low should be in place at 1.2109 in GBP/USD and intraday bias is turned neutral first. Some consolidations could be seen, and stronger recovery cannot be ruled out. But near term risk will stay on the downside as long as 1.2618 support turned resistance holds,. On the downside, decisive break of 1.2075 fibonacci level would carry larger bearish implication and target 1.1801 support next.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2526) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Sep | 1.5 | -3.7 | ||

| 01:30 | AUD | Retail Sales M/M Aug | 0.20% | 0.30% | 0.50% | |

| 08:00 | EUR | ECB conomic Bulletin | ||||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Sep | 93.3 | 92.5 | 93.3 | 93.6 |

| 09:00 | EUR | Eurozone Industrial Confidence Sep | -9 | -10.5 | -10.3 | -9.9 |

| 09:00 | EUR | Eurozone Services Sentiment Sep | 4 | 3.5 | 3.9 | 4.3 |

| 09:00 | EUR | Eurozone Consumer Confidence Sep F | -17.8 | -17.8 | -17.8 | |

| 12:00 | EUR | Germany CPI M/M Sep P | 0.30% | 0.30% | 0.30% | |

| 12:00 | EUR | Germany CPI Y/Y Sep P | 4.50% | 4.60% | 6.10% | |

| 12:30 | USD | Initial Jobless Claims (Sep 22) | 204K | 200K | 201K | 202K |

| 12:30 | USD | GDP Annualized Q2 F | 2.10% | 2.10% | 2.10% | |

| 12:30 | USD | GDP Price Index Q2 F | 1.70% | 2.00% | 2.00% | |

| 14:00 | USD | Pending Home Sales M/M Aug | 0.20% | 0.90% | ||

| 14:30 | USD | Natural Gas Storage | 90B | 64B |

US initial jobless claims rose to 204k, vs exp. 200k

US initial jobless claims rose 2k to 204k in the week ending September 23, above expectation of 200k. Four-week moving average of continuing claims dropped -6k to 211k.

Continuing claims rose 12k to 1670k in the week ending September 16. Four-week moving average of continuing claims dropped -12k to 1674k.

US Government Shutdown: Assessing Economic Impact and Recession Risks

The recurring spectre of a government shutdown has once again loomed over the United States, prompting concerns about its potential economic consequences. The shutdown may occur this weekend unless lawmakers agree on spending levels and whether to give more aid to Ukraine. Economists and analysts are closely examining the situation, weighing the likelihood of a recession, and evaluating the resilience of the American economy in the face of this uncertainty.

The Longer the Shutdown, the Greater the Damage

A recurring theme has emerged from past government shutdowns: their duration directly correlates with the extent of economic damage.

A brief shutdown is unlikely to significantly impede economic growth or push the nation into a recession, as both Wall Street and the Biden administration economists contend. Historical evidence from previous government funding stoppages supports this assertion, revealing limited economic disruption during short-lived closures.

However, the narrative shifts when contemplating a protracted shutdown scenario. A sustained government shutdown has the potential to erode economic growth, potentially impacting President Biden's re-election prospects. This challenge would compound other economic headwinds anticipated in the final months of the year, including elevated interest rates, the resumption of federal student loan payments, and a possible extended United Automobile Workers strike.

Consumer Confidence and Economic Mood

Beyond its direct economic impact, a government shutdown could adversely affect consumer sentiment. In past shutdowns, consumer confidence exhibited declines, primarily attributed to rising gas prices. The Conference Board's consumer confidence index saw an average drop of seven points in the month preceding previous shutdowns, though some of this decline reversed during the month following a reopening.

Shutdowns generate programmatic consequences that impose unwarranted economic stress and losses not fully reflected in GDP metrics. These include delays in Small Business Administration loans, the elimination of Head Start slots for working parents' children, and potential jeopardy to nutrition assistance for millions.

Quantifying Economic Impact

Goldman Sachs economists have estimated that each week of a government shutdown could reduce growth by approximately 0.2 percentage points.

This primarily results from federal workers going unpaid during shutdowns, immediately extracting spending power from the economy. However, these economists anticipate a subsequent growth increase of a similar magnitude in the quarter following the shutdown, driven by federal work resumption and the disbursement of back pay.

Past estimates by various economists and administrations align with this projection. Notably, the Trump administration calculated that a month-long shutdown in 2019 reduced growth by 0.13 percentage points per week. Following the shutdown's conclusion, the Congressional Budget Office indicated that real GDP had contracted by 0.1% in the fourth quarter of 2018 and 0.2% in the first quarter of 2019, with a slight overall loss in annual GDP.

Potential Challenges Beyond Previous Shutdowns

While historical evidence suggests that shutdowns have left limited permanent scars on the economy due to rebounding growth and confidence, present circumstances may warrant caution. Concerns arise regarding the spending behaviour of federal workers and potential difficulties for government contractors in recovering lost business.

A prolonged shutdown would disrupt the release of crucial government economic data, including reports on jobs and inflation, impairing the Federal Reserve's ability to make informed decisions on interest rates in the ongoing battle against inflation. This poses a more significant risk to economic growth compared to previous shutdowns, as it could hinder policymakers' ability to act effectively.

Economic Resilience but Slowing Growth

While the US economy appears robust enough to absorb a temporary setback, economists foresee a slowdown in the coming months, particularly if a government shutdown extends for several weeks. Key factors contributing to this include high interest rates, the resumption of federal student loan payments, and the potential for recession risks if the shutdown persists.

Analysts project third-quarter GDP growth, followed by a slowdown in the fourth quarter. They note that a two-week shutdown would have a limited impact, but if it extends for an entire quarter, it could push GDP into negative territory.

Beyond the economic realm, a government shutdown could underscore political dysfunction in Washington, unsettling investors and causing yields on Treasury bonds to rise. Elevated borrowing costs could result from this turmoil, increasing economic burdens.

Final Thoughts

As the threat of a government shutdown looms, the United States navigates a complex economic landscape. While the nation's economic resilience is evident, the duration of the shutdown remains a critical variable. A short hiatus may lead to minor disruptions, but a prolonged closure poses more substantial risks to economic growth, consumer confidence, and Fed policy effectiveness.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Promising Inflation Data ahead of Friday’s Eurozone HICP Release

Another mixed session in Europe on Thursday with US futures pointing to a similar open on Wall Street despite some promising inflation figures from the euro area.

While the eurozone HICP release isn't due until tomorrow, we do get some insight ahead of time from the individual country breakdowns and it's Germany that's offered a promising update this morning.

Headline inflation in North Rhine Westphalia fell to 4.2% this month from 5.8% in August, a huge move that will give the ECB confidence that its decision to all but declare an end to the tightening cycle a couple of weeks ago was correct.

The decline was expected due to the expiry of a transport subsidy last year which created more favourable base effects. But as we've seen so much over the last couple of years, until the figures drop, you can't be too confident.

The Spanish release was less cause for celebration but the increase from 2.6% to 3.5% was in line with expectations so there was no nasty shock that could be a cause for concern among investors or at the central bank.

The euro has firmed against the dollar today but the greenback is down against a bunch of currencies following an astonishingly strong performance over the last couple of months.

Is Oil running on fumes as Brent nears $100?

Oil prices are increasingly hitting the headlines, with Brent crude coming within five dollars of triple figures which will naturally bring back bad memories of last year's price surge. It is worth noting that, while oil could top $100, this is very different from 2022 and is largely being driven by OPEC+ tipping the market into deficit which is unlikely to be the long-term plan.

What's more, there may be some early signs that the oil rally is running on fumes as we get closer to $100, perhaps a sign that traders view it as a major psychological hurdle. That's what it proved to be in October and November last year, the last time Brent traded around these levels.

A challenging environment for Gold amid a hawkish Fed

Gold has completely fallen out of fashion, it seems, after tumbling below $1,900 on Wednesday. The yellow metal fell a little over 1.3% yesterday to its lowest level since mid-March and while it is marginally higher today on the back of a softer dollar, the near-term looks challenging.

The Fed's hawkish communication at a time when other central banks are adopting more of a neutral stance is boosting US yields and the dollar, and punishing gold. In the absence of more promising US data on inflation and the labour market, it may remain a tough environment for gold. And a government shutdown could complicate that further.