Sample Category Title

Don’t Get Too Excited by Soft Eurozone Inflation

The first set of inflation data from the Eurozone countries was mixed. German inflation eased more than expected from 6.4% to 4.3% in September, a level last seen before the war in Ukraine. Base effect due to public transport’s disappearance from the comparison and statistical distortions explained a part of the significant decline. In Spain however, prices jumped for the second straight month to 3.2%. The latter gave an idea of how the rising energy prices and weakening euro would impact the inflation figures in the coming months. Later this morning, we will find out the overall Eurozone inflation number for September. With a little bit of chance, the actual data will meet the soft market expectations, and strengthen the hand of the European Central Bank (ECB) doves. Yet this month’s figures should be taken with a pinch of salt.

The EURUSD tipped a toe below the 1.05 mark than rebounded on the back of a global retreat in the US dollar rally. The dollar retreated on the back of a soft set of economic data. Except from the light jobless claims report, the data showed that corporate profits didn’t improve as much as expected, real consumer spending slowed and the US GDP was revised marginally higher from 2% to 2.1%. The soft looking data led to some profit taking in the greenback. The dollar index retreated after a four-day rally that pushed it to the highest levels since November. The US 2-year yield retreated, but remains a touch above the 5% mark, while the 10-year yield flirted with the 4.70% level, with little respite as the longer end of the curve is impacted by a more crowded treasury issuance and the QT.

The US PCE, the Federal Reserve’s (Fed) favourite gauge of inflation, is due before the week ends, and the US government shuts down. Core PCE may have slowed in August but the headline figure will likely reflect the rising gasoline prices, which could push the Fed doves out of the race.

On the US most fun-to-watch political scene, there was not much progress regarding the negotiations to avoid a government shutdown. The US government will more likely be shut from next week, than the contrary. In Detroit, the UAW accepted to lower the pay rise that they demand to 30%. I am not sure that Ford, which decided to halt the construction of a 3.5 billion EV battery plant in Michigan will come back to its decision given the size of the rise that they will have to endure in all cases.

Winner winner, Japanese dinner

Inflation in Japan came in slower than expected in September. Core inflation in Tokyo was even negative on a monthly basis, whereas retail sales and industrial production didn’t slow, and one and two-month forecasts for industrial production were revised higher. Of course, they were, have you seen how supportive the Bank of Japan (BoJ) is! If the US dollar rally wasn’t cooling, we would’ve seen the USDJPY go straight above the 150 level. But any renewed strength in the US dollar could send the USDJPY above the 150 mark. If we hear no intervention from the Japanese, verbal or concrete, the rally could continue toward 155. But again, if you decide to swim in these waters, it means that you are taking the risk of a sudden intervention that could leave you on the backfoot in what is, in theory, nothing but a reasonable trade.

Higher for Longer Drive Up Bond Yields

Market movers today

Today we receive euro area inflation figures for September. We expect a decline in headline HICP to 4.4% from 5.3% in August driven by negative energy inflation, lower food prices, and a downtick in core inflation from 5.3% to 4.8%. The yearly growth rates will decline sharply as the base effects from inflation reducing government subsidies in 2022 and statistical distortions that kept inflation elevated over this summer fades. Yet, we expect the underlying momentum of inflation to remain high at 0.3% m/m and 0.4% m/m in seasonally adjusted headline and core inflation, respectively.

In Norway, unemployment figures are published.

In the US, we get PCE inflation figures for August. We have already received the CPI print for August but the PCE print should attract some attention as it is the Federal Reserve's preferred inflation measure. We also receive US real private consumption growth volume which we expect to land around zero or even slightly negative.

China releases PMIs for September over the weekend before going on holiday all of next week (Golden Week). For PMIs, we look for a slight further increase in the NBS manufacturing PMI whereas the Caixin PMI manufacturing may slip back after a stronger reading in August. The service PMIs are also worth keeping an eye on as a gauge of consumer spending.

In the UK, we receive the final 2023Q2 GDP figures.

The 60 second overview

There is positive sentiment in Asian equity markets this morning, following yesterday's positive sentiment in US and European equity markets despite the rising yields. The move in Asia is supported by optimism regarding spending in China during the "Golden Week" holiday.

The market is looking for a confirmation of the soft landing in the US economy from today's US data personal spending and income for August as well as a decline in the core-PCE that is one of Fed Chairman Powell's preferred measures of inflation. This should be supportive for the Federal Reserve being on hold even though we are pricing out some of the rate cuts for 2024 and 2025 as central banks are "higher for longer".

The potential US government shut-down is an additional factor creating uncertainty regarding the economy as stated by another Fed official, and would keep the Fed pausing.

We have several speeches by ECB members today and the market will be watching for comments on monetary policy.

Equities: Global equities were higher yesterday driven by US and Europe. Many moving parts - and not all moving in the same direction - made yesterday a tricky day for investors. The risk-on was driven by cyclicals and partly growth stocks despite European yields moving higher. Yesterday's big underperformer, and the only sector lower in the MSCI World Index was utilities. Hence, yesterday was not a one-way train but just as much a small reversal for the part of the market struggling the most in September. In US: Dow +0.4%, S&P 500 +0.6%, Nasdaq +0.8% and Russell 2000 +0.9%. Asian markets are mostly positive this morning with Chinese H-shares leading the way higher and Japan going against the tide. European and US futures are marginally higher.

FI: Furthermore, there is not much "flight to quality" despite the widening of the 10Y BTPS-Bund spread as the Bund ASW-spread is still below 60bp and the German curve continues to disinvert between 2Y and 10Y as the market is pricing out future rate cuts. In the US market bond yields ended lower ahead of today's inflation data. However, this morning we have seen a modest rise in US Treasury yields in Asian trading hours.

FX: Following six consecutive sessions of gains, the broad USD index fell modestly yesterday. The JPY recovered some lost ground vs the USD with USD/JPY back closer to 149. The SEK continued to perform, whereas the previous NOK rally faded as the oil price rally took a breather yesterday.

Credit: After an otherwise rough week credit spreads saw some relief yesterday where iTraxx Xover tightened 10bp and Main 2bp. Despite the positive tone, Xover has widened 25bp since trading in the new series commenced just over a week ago and Main 5bp above.

Nordic macro

Although the Norwegian labour market is still tight with solid demand for labour and low unemployment we are now seeing slightly slower employment growth, fewer vacancies and a gentle rise in the jobless rate. This deterioration is very moderate, however, and so we expect unemployment to be unchanged at 1.9% (s.a.) in September.

In Sweden, August retail sales is released. After the sharp setback between Q1 2022 and Q1 2023 retail sales has been on a slight upward trajectory and July was up 1% mom. Question is if it is sustainable. In the last NIER survey the depressed confidence among consumers and retailers fell back again. At 09.00, Martin Flodén is scheduled for a speech on monetary policy.

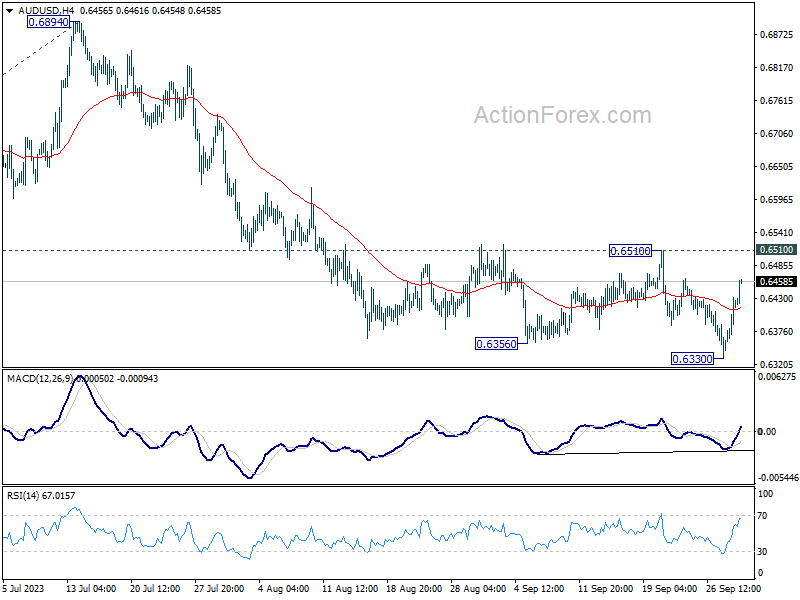

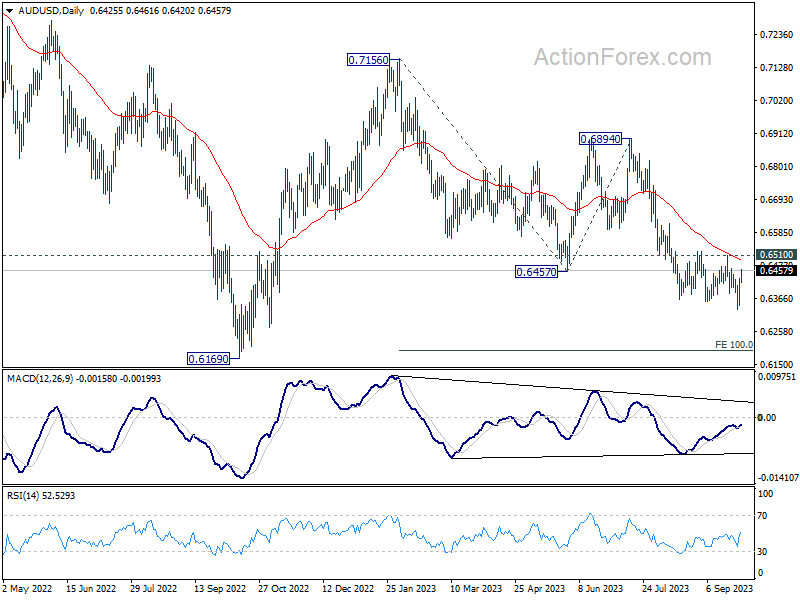

AUD/USD Daily Report

Daily Pivots: (S1) 0.6371; (P) 0.6402; (R1) 0.6458; More...

Intraday bias in AUD/USD is turned neutral as it rebounded strongly after hitting 0.6330. But as long as 0.6510 resistance holds, another decline is still expected. Break of 0.6330 will resume larger fall from 0.7156 to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195 next. However, firm break of 0.6510 will confirm short term bottoming, and turn bias back to the upside.

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

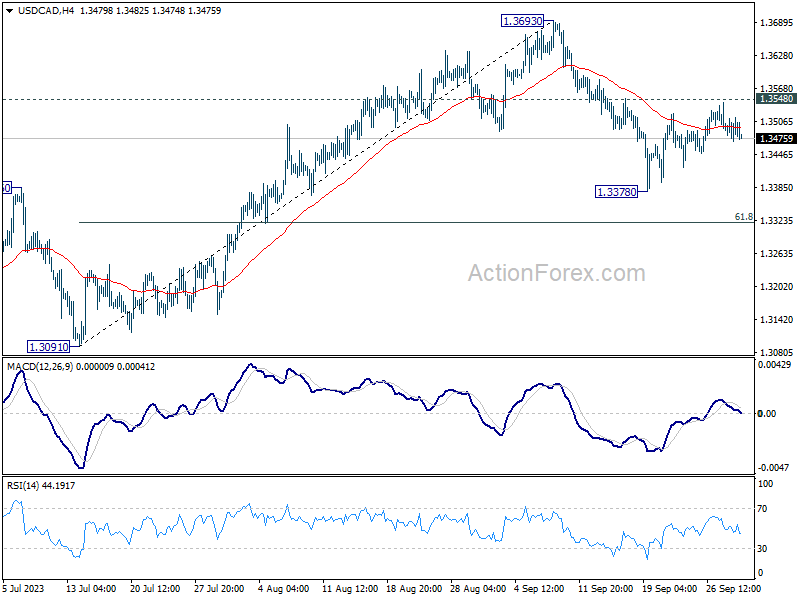

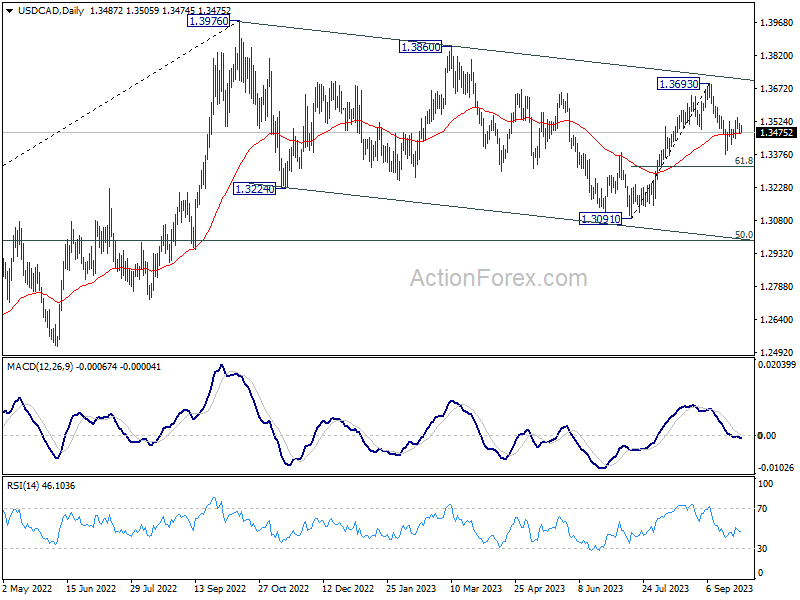

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3466; (P) 1.3491; (R1) 1.3511; More....

No change in USD/CAD as consolidation from 1.3378 is extending. Intraday bias stays neutral. Further decline remains mildly in favor. Break of 1.3378 will resume the fall from 1.3693, as another leg in the corrective pattern from 1.3976 high, to 61.8% retracement of 1.3091 to 1.3693 at 1.3321. However, firm break of 1.3548 will turn bias back to the upside for retesting 1.3693 instead.

In the bigger picture, price actions from 1.3976 are viewed as a corrective pattern to the up trend from 1.2005 (2021 low). Deeper decline could be seen as the pattern is now extending. But downside should be contained by 50% retracement of 1.2005 to 1.3796 at 1.2991. Rise from 1.2005 is still expected to resume after the correction completes.

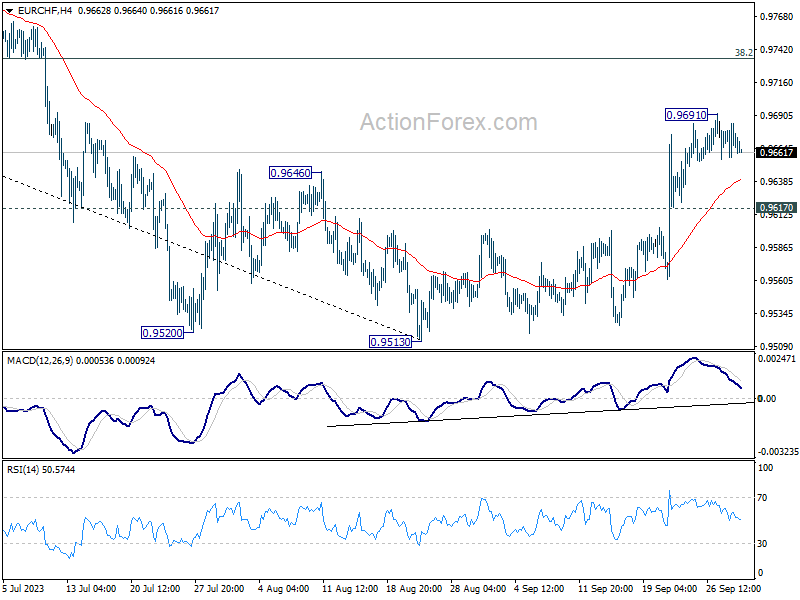

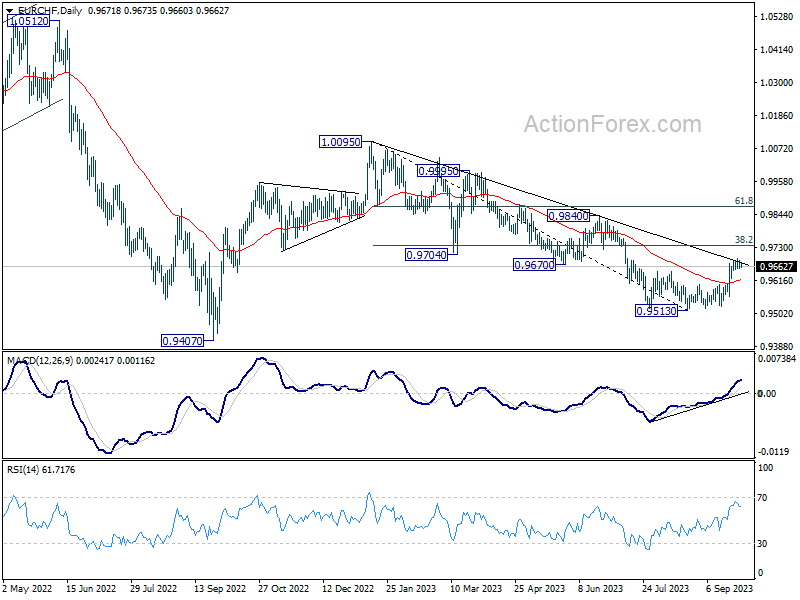

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9655; (P) 0.9671; (R1) 0.9682; More...

Intraday bias in EUR/CHF remains neutral for consolidation below 0.9691. Further rally will stay in favor as long as 0.9617 support holds. Above 0.9691 will resume the rise from 0.9513 to 38.2% retracement of 1.0095 to 0.9513 at 0.9735. However, firm break of 0.9617 will turn bias back to the downside for retesting 0.9513 low.

In the bigger picture, medium term outlook will stay bearish as long as the cross is capped well below falling 55 W EMA (now at 0.9799). That is, down trend from 1.2004 (2018 high) could still resume through 0.9407 (2022 low). However, sustained trading above the 55 W EMA will raise the chance that 0.9470 is already a long term bottom. Further rise would then be seen to 1.0095 resistance to indicate bullish trend reversal.

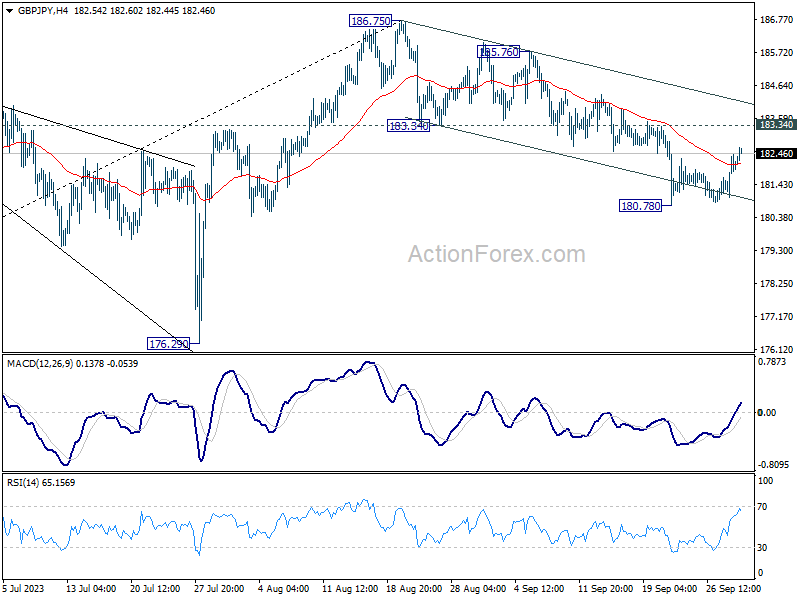

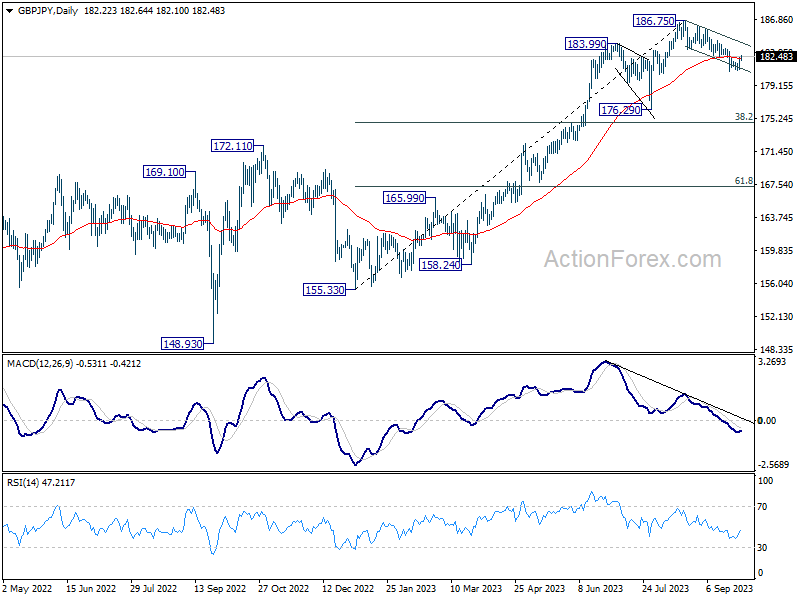

GBP/JPY Daily Outlook

Daily Pivots: (S1) 181.36; (P) 181.90; (R1) 182.73; More...

GBP/JPY's recovery from 180.78 extends higher today but stays below 183.34 resistance. Intraday bias remains neutral for the moment, and further decline is still in favor. On the downside, break of 180.78 will resume the fall from 186.75 to 176.29 support next. Nevertheless, firm break of 183.34 will turn bias back to the upside for retesting 186.75 high.

In the bigger picture, fall from 186.75 is currently seen as a corrective move only. As long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and bring lengthier and deeper consolidations.

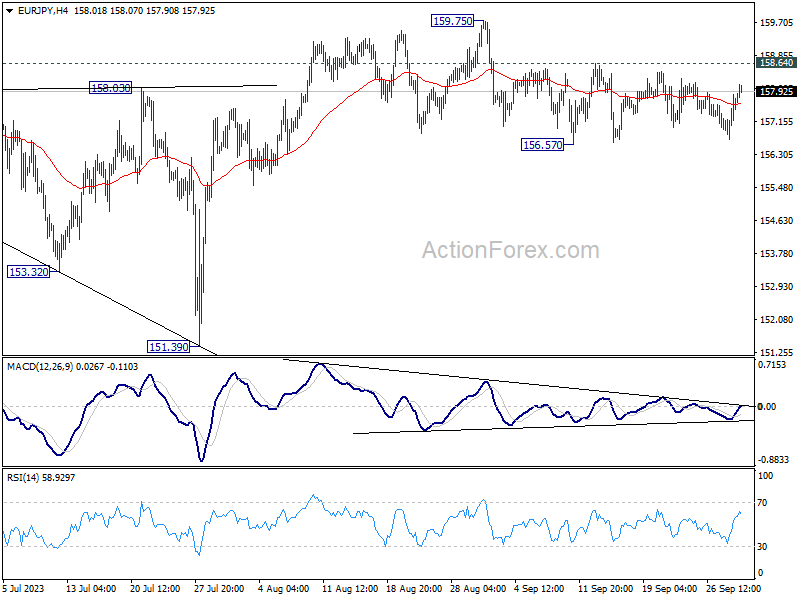

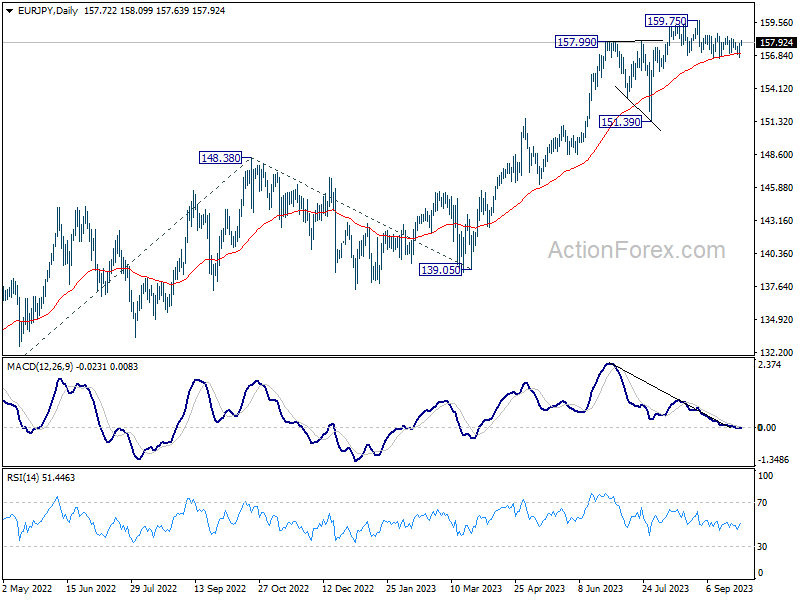

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.02; (P) 157.45; (R1) 158.18; More....

Range trading continues in EUR/JPY and intraday bias remains neutral. Risk stays on the downside with 158.64 resistance intact. On the downside, break of 156.57 support, and sustained trading below 55 D EMA (now at 156.96) will argue that fall from 159.75 is a larger scale correction. Deeper decline would be seen back towards 151.39 support. Nevertheless, above 158.64 would bring retest of 159.75 high instead.

In the bigger picture, as long as 151.39 support holds, rise from 114.42 is still expected to continue. Next target is 100% projection of 124.37 to 148.38 from 139.05 at 163.06. Sustained break there will pave the way to retest long term resistance at 169.96.

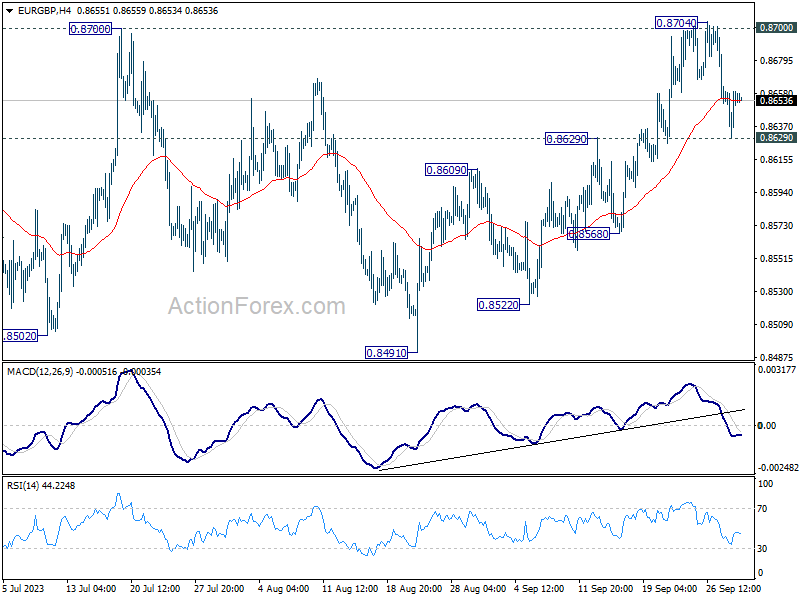

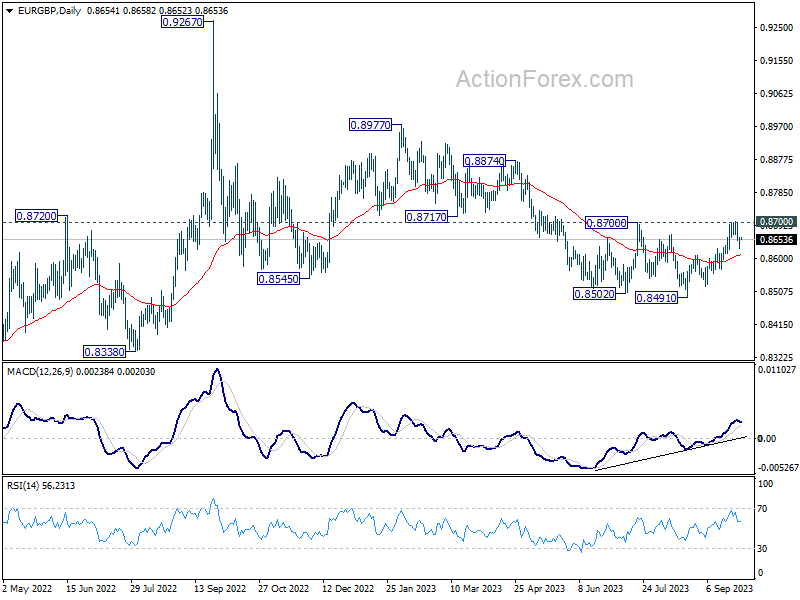

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8638; (P) 0.8650; (R1) 0.8669; More....

Range trading continues in EUR/GBP and intraday bias remains neutral. On the upside, decisive break of 0.8700 resistance will carry larger bullish implication and bring stronger rally to 0.8874 resistance next. Nevertheless, rejection by this resistance will maintain bearish outlook that larger down trend is not over. Break of 0.8629 resistance turned support will turn bias back to the downside for 0.8568 support first.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Decisive break there will argue that this decline has completed with three waves down to 0.8491. Rise from 0.8491 could then be another leg inside the pattern that targets 0.8977 and above. However, rejection by 0.8700 will keep the down trend alive for another fall through 0.8491 at a later stage.

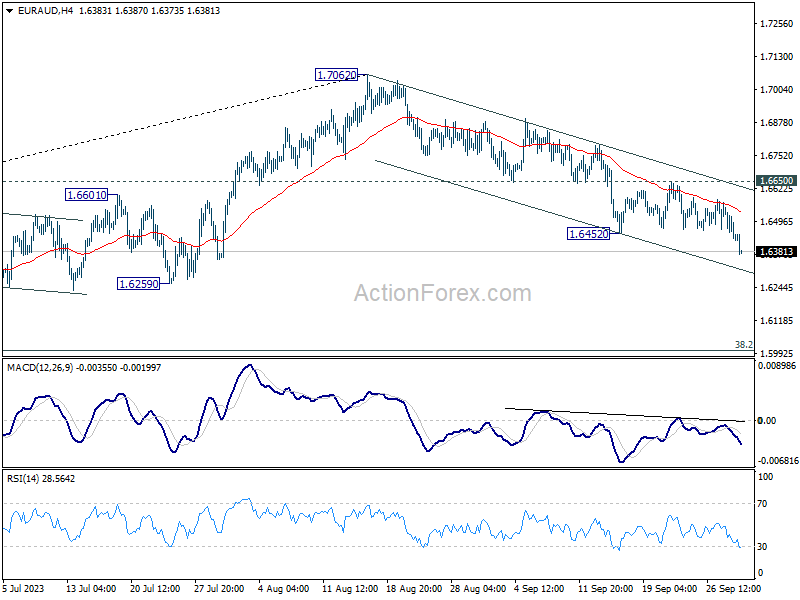

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6394; (P) 1.6474; (R1) 1.6519; More...

EUR/AUD's fall from 1.7062 resumed by breaking through 1.6452 support. Intraday bias is back on the downside for 1.6000 fibonacci level, as a larger scale correction. On the upside, break of 1.6650 resistance is needed to indicate short term bottoming. Outlook, outlook will stay mildly bearish in case of recovery.

In the bigger picture, fall from 1.7062 is probably correcting whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support should be seen there to bring rebound, at least on first attempt. This will remain the favored case as long as 1.6650 resistance holds.

Sentiment Turns at Quarter End, Eyes Set on Eurozone CPI and US PCE

The global markets experienced a noticeable shift in momentum as major US stock indexes concluded with substantial gains overnight, and treasury yields took a step back. This favorable swing persisted into Asian trading hours, marked by a remarkable rebound in Hong Kong stocks. Australian Dollar has been on the upswing, further bolstered by Copper's resurgence and a fresh wave of optimism concerning China's economic recovery. While Australian Dollar shows significant strength, New Zealand Dollar showcases a slight edge in its gains. Conversely, improved market sentiments have pushed Dollar and Yen to lower, with European majors demonstrating mixed performance.

Investors are now shifting their focus towards today's Eurozone CPI data, which holds significance in determining if ECB has truly concluded its tightening journey. Likewise, US PCE inflation will be in the spotlight to deduce if Fed will deliver another interest rate hike in the fourth quarter, as previously indicated by the dot plot. Canadian Dollar also anticipates GDP data, which could provide further clarity on its economy. Yet, some market participants may choose a more cautious stance, preferring to see what next week brings with the onset of a new quarter.

Technically, EUR/CAD recovered after dipping to 1.4155 yesterday. But surprise from today's Eurozone CPI could trigger another way of selling. Current fall from 1.5111 is in progress and even as a corrective move, more downside should be seen to 100% projection of 1.5111 to 1.4280 from 1.4822 at 1.3991. This coincides with 50% retracement of 1.2867 to 1.5111 at 1.3989. In any case, outlook will stay bearish as long as 1.4458 resistance holds.

In Asia, at the time of writing, Nikkei is down -0.34%. Hong Kong HSI is up 2.62%. Singapore Strait Times is up 0.42%. Overnight, DOW rose 0.35%. S&P 500 rose 0.59%. NASDAQ rose 0.83%. 10-year yield dropped -0.029 to 4.597.

Fed's Barkin: Path forward depends on inflationary pressures

Richmond Fed President Thomas Barkin highlighted the existing uncertainties surrounding the economic outlook in remarks made overnight. He stated, "The range of potential outcomes, to me, is still pretty broad," emphasizing the unpredictability of the current economic situation.

Reflecting on the recent decision of Fed to maintain status quo on interest rates, he said, "That's why I supported our decision to hold rates steady at the last meeting."

"We have time to see if we've done enough, or whether there's more work to be done," he added.

"The path forward to me depends on whether we can convince ourselves inflationary pressures are behind us, or whether we see them persisting," he said. Barkin further highlighted the significance of labor market developments in informing his perspective.

Japan's industrial output flat in Aug, Tokyo inflation eases in Sep

Japan's industrial output for August surprised by remaining steady month-on-month, outpacing expectations of a -0.8% mom decline. The seasonally adjusted index of production at factories and mines held its ground at 103.8, based on 2020 base of 100. Equally, index of industrial shipments ticked up by 0.1% to 103.2. In contrast, inventory index marked a -1.7% decrease to 104.6, registering the first decline in a quadrimestrial span.

The Ministry of Economy, Trade and Industry maintained a cautious tone on the economy's direction, indicating that industrial output "fluctuated indecisively." However, optimism is still present; the ministry's poll suggests that manufacturers anticipate a 5.8% uptick in production for September, followed by a 3.8% rise in October.

On the retail front, August saw a 7.0% yoy surge in retail sales, surpassing anticipated 6.4% yoy. This momentum builds upon the month's modest growth of 0.1% mom.

The labor market remained resilient, with the unemployment rate steadfast at 2.7%. The job offers-to-applicants ratio for August persisted at 1.29, unchanged from July.

Inflationary pressures seem to be cooling down. Tokyo's core CPI for September, excluding food, dipped more than forecasted, from 2.8% yoy to 2.5% yoy , as opposed to the predicted 2.6% yoy. Headline CPI decreased slightly from 2.9% yoy to 2.8% yoy. Additionally, core-core CPI, which excludes both food and energy, retreated from 4.0% yoy to 3.8% yoy.

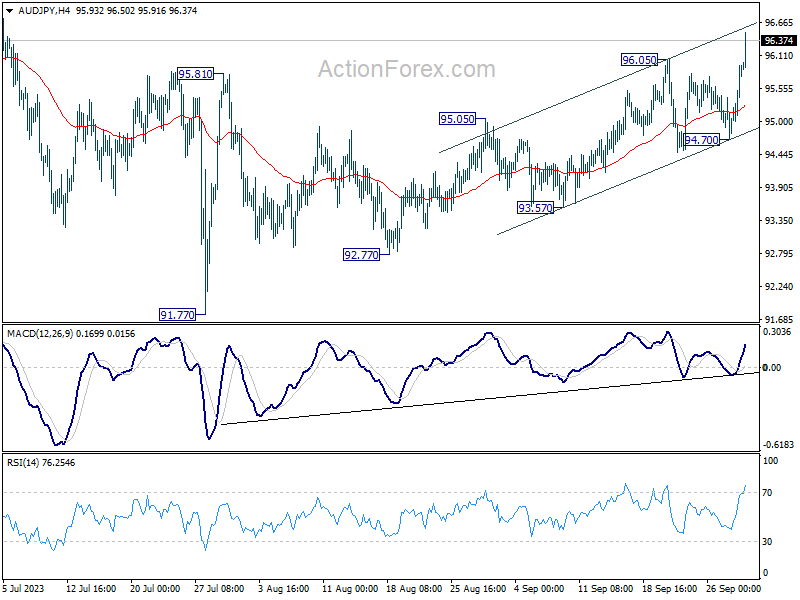

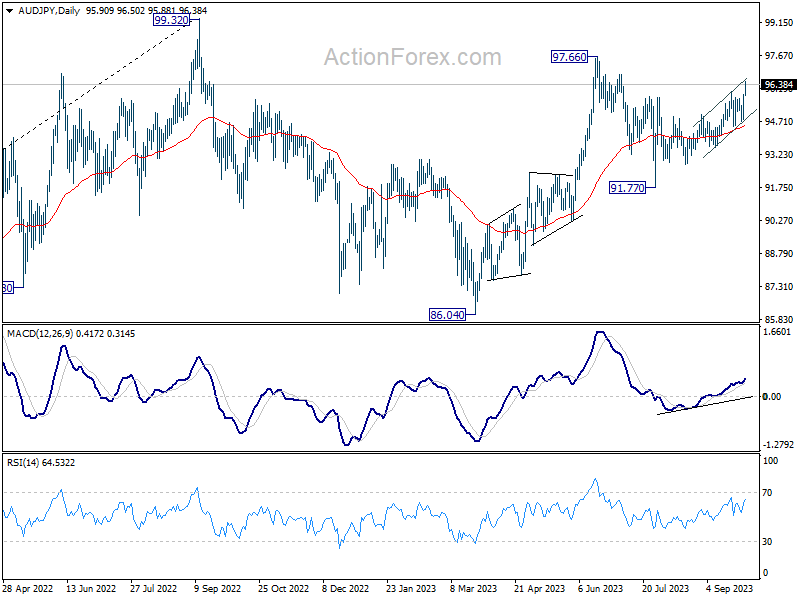

AUD/JPY and Copper soar on renewed China optimism

Australian Dollar experienced a significant surge in today's Asian trading session, fueled in part by the vigorous rebound observed in Hong Kong stocks, the Chinese Yuan, and Copper prices. The rebound in stocks could attributed possible position adjustments after a tumultuous quarter in Hong Kong and China, and with the impending long holiday in China lasting until October 9. But there's still a budding sentiment of optimism concerning China's potential for economic recuperation.

A noteworthy comment from the International Monetary Fund has contributed to this optimism. The IMF recently expressed its observation yesterday of certain stabilization signs in China's economy from the latest data sets. The institution holds a perspective that China could realistically achieve growth rate close to 5% this year. Looking forward, the IMF anticipates China's GDP growth to decelerate to approximately 3.5% over a medium-term horizon. Nevertheless, this pace could experience a boost if China embarks on economic reforms.

AUD/JPY has powerfully broken 96.05 resistance mark, which is indicative of resumption of its recent rise from the 92.77. However, the nature of the current rally doesn't explicitly suggest it's impulsive, maintaining an air of ambiguity around potential technical interpretations.

In one scenario, if price action from 91.77 serves as the second leg of the pattern originating from 97.66, then the peak of the current rally might be restricted by 97.66 resistance.

In another case, if the upswing from 91.77 is in continuation with the entire surge from 86.04, the climb could still be seen as the second leg of the pattern from the 2022 high of 99.32. As such, the upper boundary could be set by the 99.32 mark, even if 97.66 is surpassed.

So, upside potential appears to be limited for the medium term.

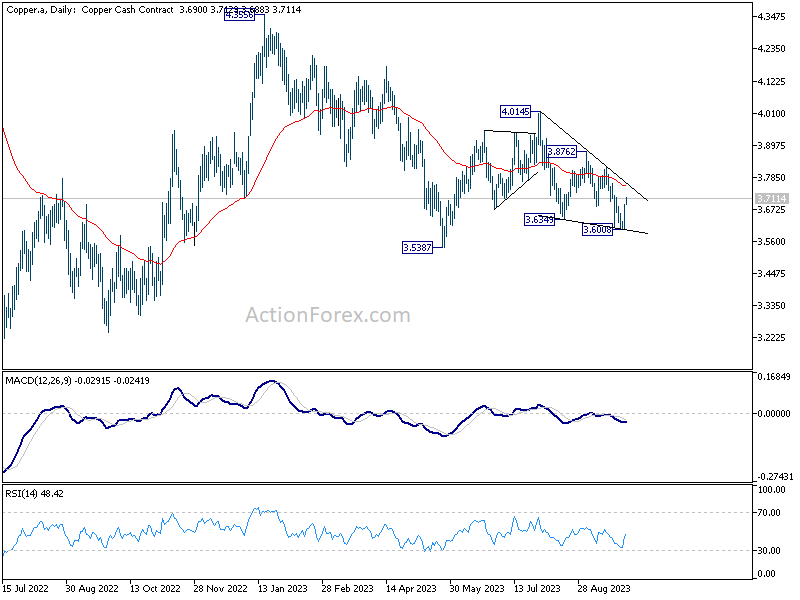

Turning to Copper, its robust rebound this week suggests that decline from 4.0145 might have culminated, completing three waves that bottomed at 3.6008. Sustained trading above 55 D EMA (now at 3.7540) would solidify this viewpoint, setting sights on 3.8762 resistance for validation.

For Australian Dollar to secure its foundational momentum, decisive break of 3.8762 resistance in Copper might be essential. Absent this, Aussie's rebound might retain its corrective nature.

Looking ahead

Eurozone CPI is the main highlight in European session today. Other data include Germany import prices, retail sales and unemployment; France consumer spending; UK Q2 GDP final, mortgage approvals and M4 money supply; and Swiss KOF economic barometer.

Later in the day, Canada GDP will be a focus. US will also release personal income and spending, PCE inflation, goods trade balance and Chicago PMI.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6394; (P) 1.6474; (R1) 1.6519; More...

EUR/AUD's fall from 1.7062 resumed by breaking through 1.6452 support. Intraday bias is back on the downside for 1.6000 fibonacci level, as a larger scale correction. On the upside, break of 1.6650 resistance is needed to indicate short term bottoming. Outlook, outlook will stay mildly bearish in case of recovery.

In the bigger picture, fall from 1.7062 is probably correcting whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support should be seen there to bring rebound, at least on first attempt. This will remain the favored case as long as 1.6650 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Sep | 2.80% | 2.90% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Sep | 2.50% | 2.60% | 2.80% | |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Sep | 3.80% | 4.00% | ||

| 23:30 | JPY | Unemployment Rate Aug | 2.70% | 2.60% | 2.70% | |

| 23:50 | JPY | Industrial Production M/M Aug P | 0.00% | -0.80% | -1.80% | |

| 23:50 | JPY | Retail Trade Y/Y Aug | 7.00% | 6.40% | 6.80% | 7.00% |

| 01:30 | AUD | Private Sector Credit M/M Aug | 0.40% | 0.30% | 0.30% | |

| 05:00 | JPY | Housing Starts Y/Y Aug | -9.4% | -8.90% | -6.70% | |

| 05:00 | JPY | Consumer Confidence Index Sep | 35.2 | 36.2 | 36.2 | |

| 06:00 | EUR | Germany Import Price Index M/M Aug | 0.50% | -0.60% | ||

| 06:00 | GBP | GDP Q/Q Q2 F | 0.20% | 0.20% | ||

| 06:00 | EUR | Germany Retail Sales M/M Aug | 0.50% | -0.80% | ||

| 06:00 | GBP | Current Account (GBP) Q2 | -14.0B | -10.8B | ||

| 06:30 | CHF | Real Retail Sales Y/Y Aug | -2.20% | |||

| 06:45 | EUR | France Consumer Spending M/M Aug | -0.40% | 0.30% | ||

| 07:00 | CHF | KOF Economic Barometer Sep | 90.5 | 91.1 | ||

| 07:55 | EUR | Germany Unemployment Change Aug | 14K | 18K | ||

| 07:55 | EUR | Germany Unemployment Rate Aug | 5.70% | 5.70% | ||

| 08:30 | GBP | Mortgage Approvals Aug | 48K | 49K | ||

| 08:30 | GBP | M4 Money Supply M/M Aug | 0.20% | -0.50% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Sep P | 4.50% | 5.20% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Sep P | 4.80% | 5.30% | ||

| 12:30 | USD | Personal Income M/M Aug | 0.40% | 0.20% | ||

| 12:30 | USD | Personal Spending Aug | 0.50% | 0.80% | ||

| 12:30 | USD | PCE Price Index M/M Aug | 0.50% | 0.20% | ||

| 12:30 | USD | PCE Price Index Y/Y Aug | 3.50% | 3.30% | ||

| 12:30 | USD | Core PCE Price Index M/M Aug | 0.20% | 0.20% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Aug | 3.90% | 4.20% | ||

| 12:30 | USD | Goods Trade Balance (USD) Aug P | -91.2B | -90.9B | ||

| 13:45 | USD | Chicago PMI Sep | 47.6 | 48.7 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Sep F | 67.7 | 67.7 |