Sample Category Title

Fed stands pat, 12 members see one more hike

Fed keeps federal funds rate unchanged at 5.25-5.50% as widely expected, by unanimous vote. Tightening bias is maintained as "The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals".

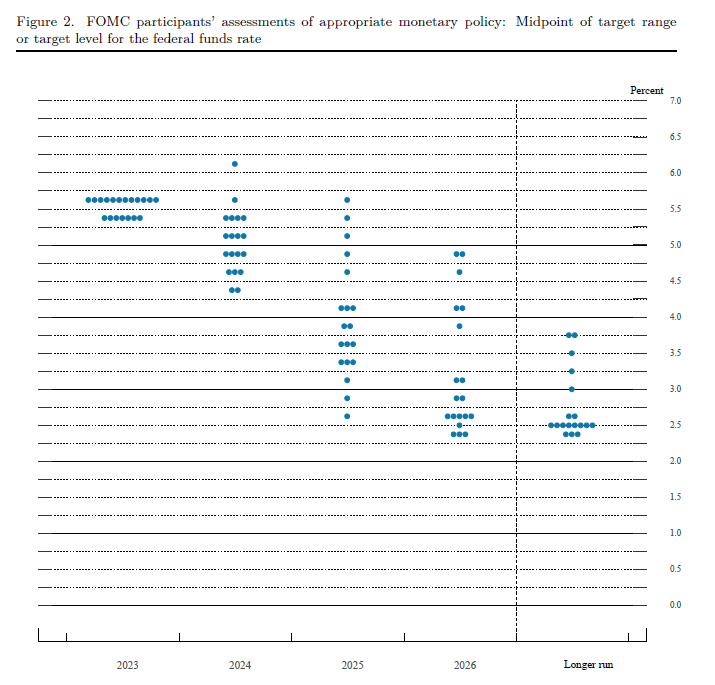

In the new dot plot, 12 of 19 policymakers penciled in one more 25bps rate hike this year to 5.50-5.75%. By

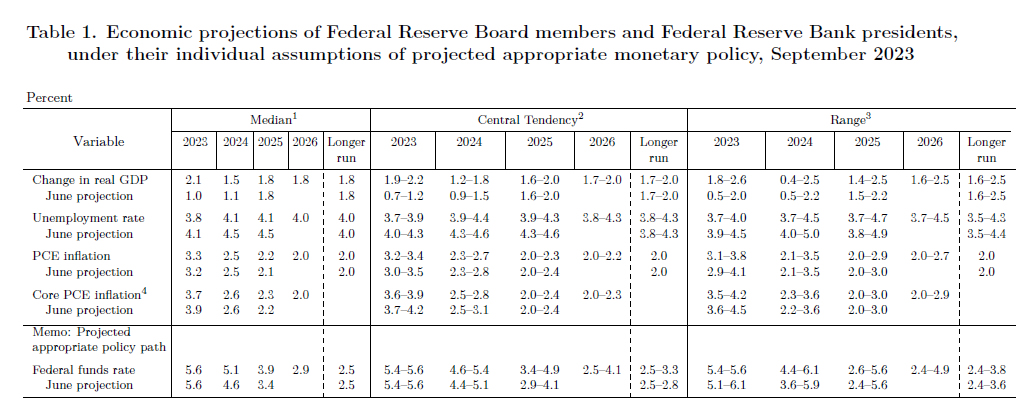

In the new median projections,

- 2023 GDP growth is revised up to 2.1% (from 1.0%).

- 2024 GDP growth is revised up to 1.5% (from 1.1%).

- 2025 GDP growth is unchanged at 1.8%.

- 2023 unemployment rate is revised down to 3.8% (from 4.1%).

- 2024 unemployment rate is revised down to 4.1% (from 4.4%).

- 2025 unemployment rate is revised down to 4.1% (from 4.5%).

- 2023 PCE inflation is revised up to 2.2% (from 3.2%).

- 2024 PCE inflation is unchanged at 2.5%.

- 2025 PCE inflation is revised up to 2.2% (from 2.1%).

- 2023 core PCE is revised down to 3.7% (from 3.9%).

- 2024 core PCE is unchanged at 2.6%.

- 2025 PCE is revised up to 2.3% (from 2.2%).

- 2023 federal funds rate unchanged at 5.6%.

- 2024 federal funds rate raised to 5.1% (from 4.6%).

- 2025 federal funds rate raised to 3.9% (from 3.4%).

Full Summary of Economic Projections here.

(FED) Federal Reserve Issues FOMC Statement

Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have slowed in recent months but remain strong, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. The Committee will continue to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Adriana D. Kugler; Lorie K. Logan; and Christopher J. Waller.

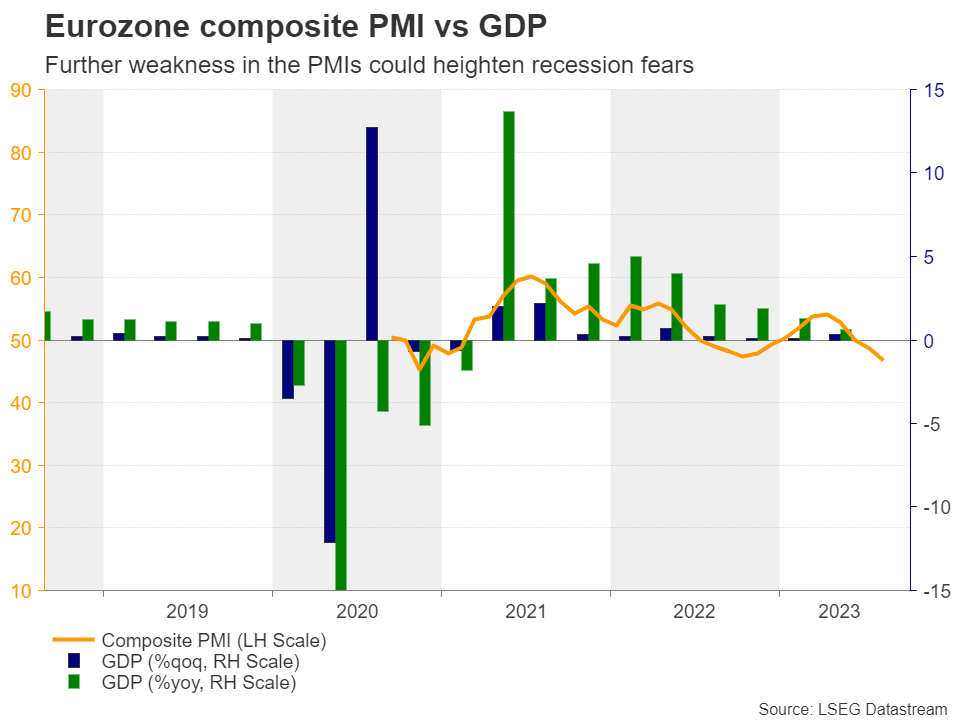

Will Eurozone PMIs Validate ECB Cut Bets?

- Investors see rate cuts by the ECB, despite post-meeting hawkish rhetoric

- Eurozone prel. PMIs the next piece of information that could shake those bets

- Euro could slide if the PMIs disappoint when released on Friday, at 08:00 GMT

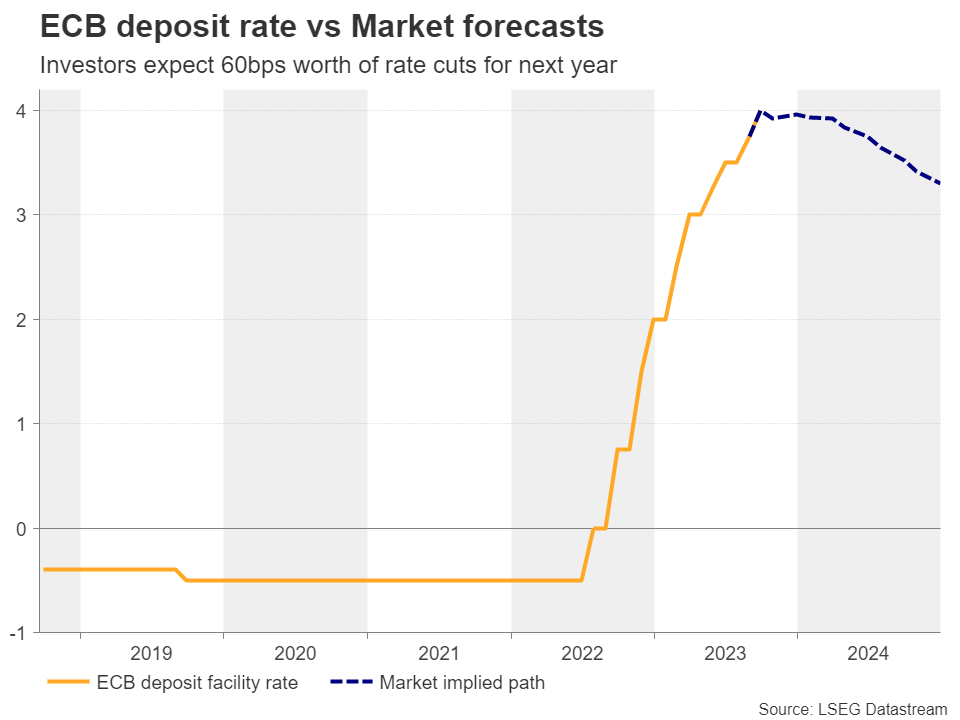

After ECB meeting, the market sees rate cuts for next year

Last week, the ECB decided to raise interest rates by 25bps, taking the deposit facility rate to a record high of 4%. However, with the latest data pointing to a severely wounded economy, officials cut their economic growth forecasts, and despite raising those for inflation, they hinted that this could be the last rate increase in this tightening cycle.

The euro tumbled and market participants began pricing a series of rate reductions for next year, allowing only a small probability for another hike by December. Even after several policymakers, including President Lagarde, pushed back on rate cut bets the following days, and noted that further increases cannot be ruled out, investors were not convinced. They are still assigning only a nearly 30% probability for another quarter-point increment and they are seeing rates being 60bps below current levels by the end of next year.

Attention now falls on Friday’s preliminary PMIs

This suggests that market participants are placing more trust in economic data than just remarks, and that they are more concerned about economic performance than high inflation. With that in mind, Friday’s preliminary PMIs for September may attract special attention. The manufacturing PMI is forecast to have slightly increased but to remain well below the boom-or-bust zone of 50 that separates expansion from contraction. What’s more, both the services and composite indices are expected to have slid further into the contractionary territory, ringing the recession alarm bells even louder.

Should this be the case, the euro is likely to come under renewed selling pressure, even if the price subindices point to some acceleration due to the latest rally in oil prices. For traders to start buying euros again, upcoming data may need to start pointing to some economic recovery, or at least a stabilization, something for which there is no evidence yet.

US and Eurozone growth dynamics drive euro/dollar

In contrast to the Eurozone data, US economic indicators have been pointing to a resilient economy, not justifying expectations of around 80bps worth of rate reductions by the Fed for 2024. Taking that into consideration, the risks surrounding the US dollar from the outcome of the FOMC decision on Wednesday may be tilted to the upside, as there may be a decent chance for the new dot plot to point to a higher rate path than the one currently implied by the market.

Ergo, a hawkish Fed combined with further softness in the Eurozone PMIs may be a toxic cocktail for euro/dollar. The pair has been in a recovery mode due to the relatively hawkish comments by several ECB policymakers after last Thursday’s decision, but that recovery may stay limited and short-lived below the 1.0765 resistance level, marked by the highs of September 12 and 13. Another round of declines would likely take the price back below the key territory of 1.0665 and perhaps confirm a bearish trend reversal on the daily chart. The next important support may be the 1.0530 zone, which stopped the pair from moving lower back in February and March.

For the outlook of euro/dollar to brighten again, the bulls must sweat a lot. They may have to drive the action all the way above the 1.1070 territory, which provided strong resistance on several occasions this year.

Could BoJ Upset Expectations for a Dull Meeting?

- Amidst a very busy week, the BoJ holds its sixth rate-setting meeting

- Market is not expecting fireworks; there is increasing commentary about negative rates

- The decision will come on Friday 03.00 GMT, press conference shortly afterwards

The week is expected to close on a high note

The Bank of Japan is holding its sixth meeting for 2023 on Friday, two days after the key Fed meeting. Despite the yen’s underperformance making new headlines, the BoJ is not expected to announce a change in its main interest rate. However, the market is curious whether the BoJ is ready to proceed to another amendment of its monetary policy toolkit, especially if the Fed opts for another rate hike on Wednesday.

At the last meeting in late July, the BoJ widened the boundary of its yield curve control (YCC) framework. This was seen as a shy first step towards the eventual normalization of monetary policy, as bond yields were finally allowed to increase a tad. The post-meeting BoJ members’ comments didn’t diverge from the usual commentary, closing the door to the buildup of hawkish expectations. However, the overall sentiment appears to have changed somewhat after Governor Ueda’s September 10 comment.

His “quiet exit” remark reignited market rumours that the BoJ is finally preparing to abandon its ultra-loose monetary policy stance. Further adjusting the YCC framework seems to be the easy next option for the BoJ, but the market is focusing on negative rates. The BoJ’s target rate has remained at -0.1% since February 2016. Interestingly, BoJ’s Tamura has already been on the airwaves downplaying the importance of a possible return to positive rates, by stating that the abandonment of negative rates is not the same as monetary policy tightening. Therefore, the BoJ policy board has probably already discussed this move and it is expected to be part of the discussion again this week.

Data releases failing to surprise on the upside lately

The basis for any BoJ move is the economic outlook. The strongly positive GDP figures for the second quarter of 2023 have been followed by mixed data. Similar to other countries, the housing sector remains under pressure with the July housing starts dropping very close to an 8-year low, and labour cash earnings showed a considerable slowdown in July. On the flip side, the PMI surveys remain optimistic, especially when compared to the euro area figures.

However, the BoJ’s focus falls squarely on the inflation data and wages. The August Tokyo inflation print surprised on the downside. If this tendency is confirmed by the national data, on Friday we could see the headline CPI dropping below 3% for the first time since July 2022. Various BoJ members have stated that inflation is expected to gradually re-accelerate after a period of slowdown. Therefore, a possible downside surprise could affect market sentiment, but it will probably not change BoJ’s strategy going forward.

Wages have emerged as the key input in BoJ’s analysis

What is affecting the BoJ members’ attitude are the developments in wages. Since the record-breaking wage agreements in April 2023, retail sales have been registering strong annual increases. For this trend to continue, firms need to continue with their aggressive wage hikes, further fueling spending and helping the public overcome the deflation mentality of the past decades. Importantly, Ueda stated that by year-end the BoJ could have enough on the 2024 wage negotiations. This could mean that a rate hike could be firmly on the agenda at the December 19 meeting.

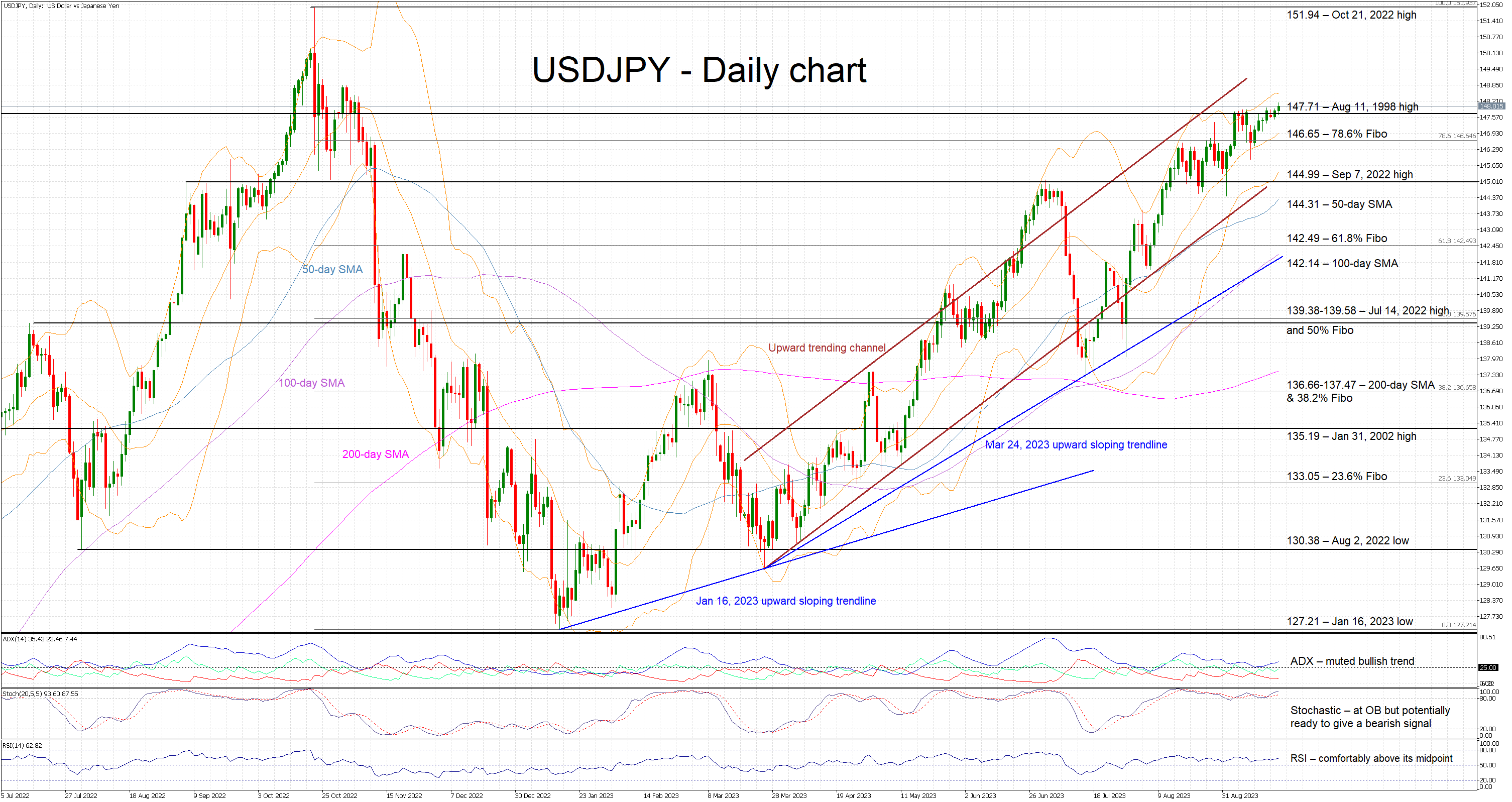

The yen needs help, especially if the Fed hikes on Wednesday

The yen continues to suffer against most currencies with the US dollar-yen pair making a new 2023 high and reaching its highest level since November 4, 2022. With the Japanese authorities limiting their reaction so far to verbal interventions, the burden falls on the BoJ to provide some support to the ailing yen. If the BoJ maintains its current stance on Friday, the US dollar-yen pair could set sail for the October 21, 2022 high at 151.94.

On the flip side, should the BoJ manage to surprise on Friday, we could see yen bulls staging a pullback similar to the mid-July correction with the main target being the 144.99 area. However, such a move could prove excessive and premature if the economic data don’t start to improve significantly over the next few trading days.

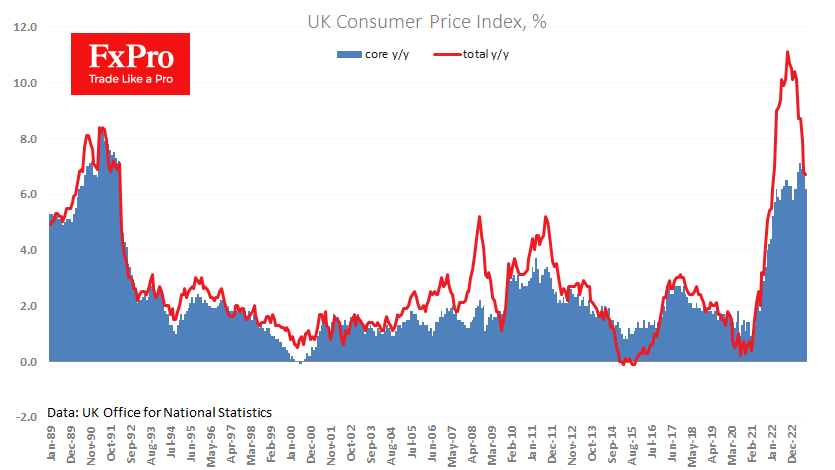

UK Inflation Slowdown Unlikely to Stop Rate Hike

UK consumer inflation slowed from 6.8% to 6.7% y/y, contrary to the expected acceleration to 7.0%. Core inflation, excluding food and energy, saw an even more significant slowdown of 6.2% from 6.9% y/y, well below the average forecast of 6.8%.

The weaker-than-expected data sparked a brief sell-off in GBPUSD, with the exchange rate dropping nearly 0.5% within minutes to 1.2330, a level last seen in May.

The UK’s annual price growth rate is still higher than other developed economies, outpacing several major emerging ones. The latest data has fuelled speculation that the Bank of England will pause on rate hikes or even end the hiking cycle that began almost two years ago.

But the dovish rhetoric looks premature in our view. These 9.1% y/y retail price increases are unacceptable for a developed country, and core inflation has been “too high for too long”, entrenching inflation expectations. A strong labour market increases the risk of secondary inflationary effects, exacerbated by the recent rise in commodity and energy prices.

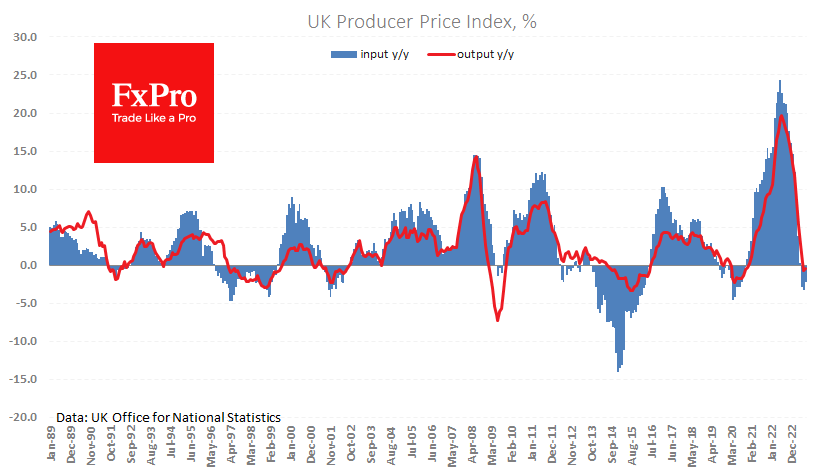

Producer input prices rose by 0.4% in August. Producer output prices have risen by 0.2% over the past two months, signalling the end of the deflationary impact on final inflation.

For over two months now, the Pound has been gently retreating against the Dollar because of contrasting economic data from these countries, with the UK being the weaker side. However, it would be a mistake to assume that the Bank of England will quickly turn its monetary policy towards easing, as this could increase pressure on Sterling and reinforce pro-inflationary factors.

Sunset Market Commentary

Markets

UK August inflation numbers this morning fell short of analyst expectations. The headline figure only rose by 0.3% m/m, unexpectedly lowering the yearly reading from 6.8% to 6.7%. Core inflation (ex. food and energy) eased from 6.9% to 6.2% compared to the 6.8% consensus. All other consumer prices gauges (CPIH, retail price index) similarly showed prices rising less than expected. The numbers come a day ahead of the Bank of England and follow a recent string of disappointing data, including PMIs. Markets since end August significantly pared back bets up to a point where the once almost 75 bps of additional tightening is reduced to a less than 50% chance for one final hike at the meeting tomorrow. Given the Bank of England’s reputation of erring to the dovish side there’s a real risk it is going to (ab)use this morning’s data not just to pause but to conclude, though not officially, the tightening cycle. UK gilts hugely outperform US Treasuries and German Bunds today. Yields tank more than 11 bps at the front end of the curve. Longer tenors shed 5.5-9 bps. Knock-on effects pushed German and US yields lower. They ease about 2 to 3.5 bps. Pound sterling declines but nothing dramatic, especially given the size of the yield declines. EUR/GBP rose from 0.862 to the mid 0.86/87 area. The dollar trades slightly weaker, giving EUR/USD another shot at the 1.07 big figure. DXY (trade-weighted greenback) eases marginally to trade sub 105. USD/JPY temporarily moved beyond the recent highs and went north of 148 before paring gains again. Other currencies including the AUD, SEK and NZD lead the scoreboard. These cyclicals enjoy a healthy risk bid as markets bet that yet another major central bank is (almost) done tightening. That brings us to tonight’s Fed policy meeting.

The Fed is expected to deliver a telegraphed, but still hawkish skip (5.25%/5.50% target range). However, with the decline in headline inflation at risk of slowing down, amongst others, due to a higher oil price and US economic growth holding up well, there is little reason for Fed governors to change the dot plot signaling an additional 25 bps step later this year. The higher for longer mantra might be reinforced by a further scaling back of rate cut expectations for end 2024 (4.6% in June). Fed governors also might raise their standing assessment on the 2.5% long term equilibrium rate. If so, it would be a clear confirmation that monetary policy has entered a new era. At the press conference, we don’t expect Fed Chair Powell to change his message from June in a profound way. From a bond market point of view, question is whether the tone of the Fed will be hawkish enough to force a break beyond recent cycle yield peak levels. The downside in yields in any case should stay well protected. The dollar will likely stay in the drivers’ seat.

News & Views

New EU car registrations rose by 21% Y/Y in August, marking the thirteenth consecutive month of growth. YTD, car registrations rose by 17.9%, totaling 7.1 million units. The market share of battery-electric cars exceeded 20% for the first time (21%, up from 11.6% in August last year), overtaking diesel for the second time this year and becoming the third-most-popular choice for new car buyers after hybrid-electric cards (24% market share from 22.5%) and petrol cars (32.7% from 38.7%). EU battery-electric car registrations surged by 118.1% Y/Y with Belgium recording the highest growth rate of 224.5%.

Polish central banker Wnorowski followed up on this morning’s comments by governor Glapinski. He said that the zloty’s drop since the unexpected 75 bps rate cut has been excessive and that a further weakening is not desirable. He added that the central bank learned its lesson and that any next moves will be more gradual. He hopes that November forecasts will show a faster decline of CPI towards target, backing such approach. The Polish zloty in a two-stage move rallied from EUR/PLN 4.6750 this morning to 4.61 currently. Polish zloty swap yield rise by up to 13 bps at the front end of the curve (2-yr).

Aussie Jumps as PBOC Holds Lending Rates, Hits 3-week High

- China maintains one-year and five-year loan prime rates

- Australian dollar records strong gains

The Australian dollar has posted strong gains on Wednesday. In the European session, AUD/USD is trading at 0.6491, up 0.58% and its highest level in three weeks.

China holds loans prime rates

China’s banks maintained their benchmark loan rates for September, a sign that the Chinese economy may be finding its footing after government support. As expected, the People’s Bank of China kept 1-year and 5-year loan prime rates at 3.45% and 4.2%, respectively. Recent Chinese releases have shown signs of improvement, including Friday’s retail sales and industrial production which beat expectations.

The world’s second-largest economy has deteriorated over the past few months and a CPI report in July which showed the economy was experiencing deflation set off alarm bells in the markets. The PBoC decision was seen as a vote of confidence in the economy, and the Australian dollar has responded with strong gains.

The RBA minutes, released on Tuesday, noted that board members listed weak domestic demand and contagion from China’s slowdown as risk factors for an economic slowdown. Despite these concerns, the RBA has signalled that inflation remains too high and has left the door open to further hikes. Inflation is currently running at 6% and the RBA has forecast that inflation will slow to around 3.25% by the end of 2024 and won’t fall back into the 2%-3% target range until late 2025.

It’s decision day at the Federal Reserve, which is widely expected to hold rates for only the second time in the current rate-tightening cycle. That doesn’t mean the meeting will be a sleeper. Investors will be interested to see if there are any revisions to the June dot plot, which projected one more hike this year and 100 basis points in rate cuts in 2024. Any changes in these forecasts could shift the Fed rate odds for the October meeting, which are currently at 27%, according to the FedWatch tool.

AUD/USD Technical

- AUD/USD is putting pressure on resistance at 0.6477. The next resistance line is 0.6524

- 0.6381 and 0.6332 are the next support levels

BoE Decision on Thursday a Coin Toss After Surprisingly Encouraging Inflation Report

Everyone at the Bank of England undoubtedly breathed a collective sigh of relief this morning, joining the rest of us, as inflation subsided much more than expected in August.

Not only did the headline CPI rate not rise last month, as was expected, it actually fell slightly, with the core rate falling a lot. So despite the unfavourable base effects for fuel, which many expected would lift the headline rate, price increases are finally easing at a decent rate.

There is obviously still a long way to go and further substantial progress will likely be made in the final months of the year but there are also upside risks, most notably oil prices. That said, the situation in the oil market is very different from the last couple of years so there isn't necessarily cause for panic on that front, it may just complicate things on the way back to the Bank's 2% target.

There is plenty more to celebrate in the breakdown of the data though, most notably the drop in services inflation which has been a major concern for the MPC amid soaring wages. But with inflation falling, energy prices declining and the labour market tightness easing, there is hope that pressures here will further subside too.

What's interesting is that markets now view tomorrow's BoE interest rate decision as a coin toss between 25 basis points and hold. Perhaps the MPC's words from earlier this month in front of the Treasury Select Committee are still ringing in traders ears but given the entirety of the data, I think we're more likely to see an ECB-style dovish hike tomorrow than a Fed-style stuttered exit.

Fed likely to pause but may refrain from suggesting they're done with hikes

The Fed meeting today is widely expected to end in an agreement not to hike interest rates this month with the key takeaway being whether they intend to again in this cycle. The ECB strongly hinted that it is probably done last week but I'm not convinced we'll get the same signal from the Fed and neither, it would appear, are markets.

We have seen the odds of another hike creeping up a little recently amid more resilience in the economy which will likely make the central bank a little apprehensive about declaring victory or even suggesting they believe they've done enough. If they are so bold as to follow in the footsteps of the ECB, it will be interesting to see what that does to yields and the dollar.

Oil pares gains amid possible pre-Fed profit-taking

Oil prices are down today after ending the session in negative territory on Tuesday as well, perhaps a sign that the trend is finally starting to run on fumes. I wouldn't say the price has peaked, despite this sudden reversal, but perhaps it could trigger some profit-taking. What is interesting is that there was no clear shortage of momentum ahead of the reversal which may make some question how significant a correction we're looking at.

Of course, the closer we get to $100 Brent, the more nervous some traders may get which may show more clearly in momentum indicators. Ultimately, with oil inventory data to come today and the Fed later, the coming period for crude is likely to be driven by the outcome of those events, as opposed to traders' current view. And the Fed in particular may have contributed to some of the profit-taking we're already seeing.

Gold steadies ahead of the Fed decision

The gold rebound has stalled over the last couple of sessions with the Fed meeting likely strongly contributing to that. There's clearly a lot of uncertainty ahead of the decision, not to mention the new economic projections and dot plot, so it's probably not surprising that we're seeing some caution. Arguably the most realistically favourable outcome for gold may be a pause and an ECB-like declaration that they've done enough, although with so much to absorb from the meeting, there will be other drivers too.

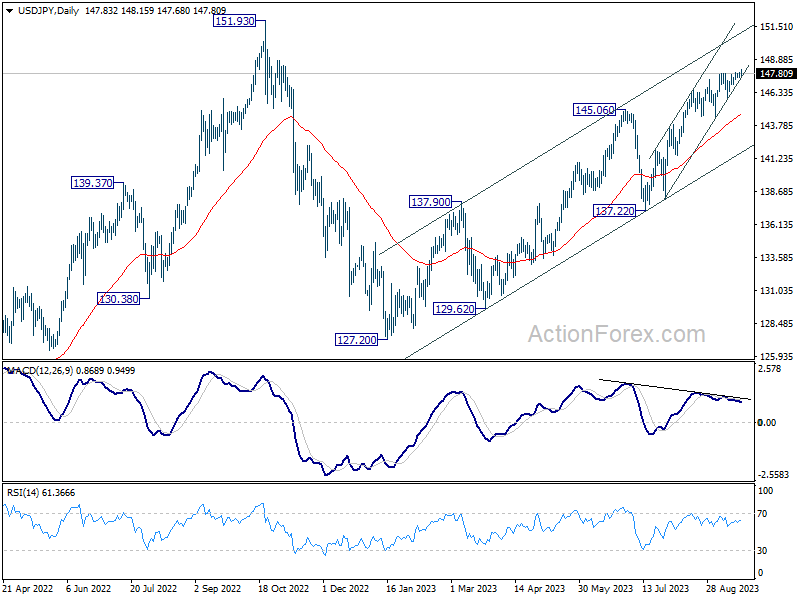

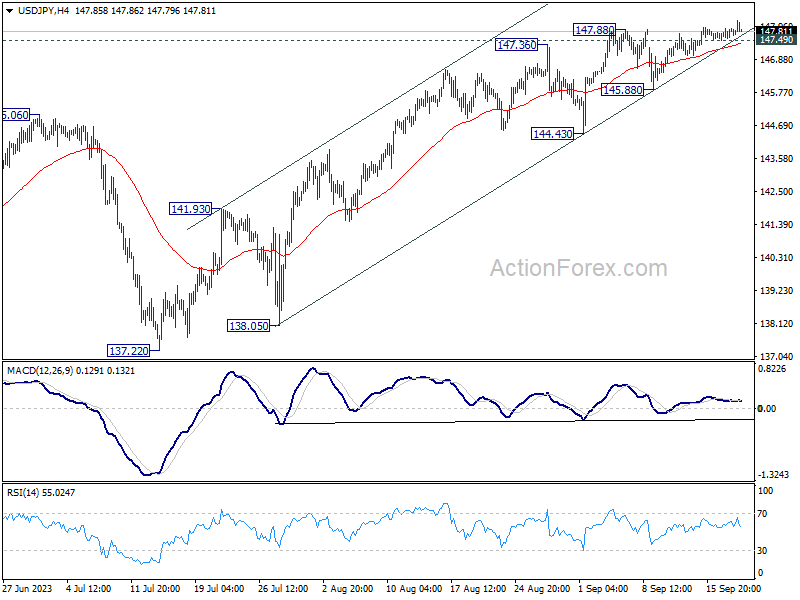

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.61; (P) 147.77; (R1) 148.02; More...

Intraday bias in USD/JPY remains mildly on the upside at this point. Current rise from 127.20 should target a retest on 151.93 high. On the downside, below 147.49 minor support will turn intraday bias neutral first. But outlook will stay bullish as long as 145.88 support holds, in case of retreat.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.